S&P Futures, European Stocks Hit New All-Time Highs As Rates Slide

S&P Futures, European Stocks Hit New All-Time Highs As Rates Slide

European stocks hit a new record highs on Thursday, buoyed by optimism in Britain over easing lockdown restrictions, while the benign outlook on US interest rates revealed

Share this:

European stocks hit a new record highs on Thursday, buoyed by optimism in Britain over easing lockdown restrictions, while the benign outlook on US interest rates revealed in the latest FOMC Minutes where the Fed indicated it will maintain its commitment to supportive policy, helped push S&P futures to new all time highs after the cash index closed at a record on Wednesday. Treasury yields dropped, the dollar slipped and crude oil fell as the pandemic worsened in key regions just as OPEC+ prepares to add supply over the coming months.

At 7:30 a.m. EDT, Dow E-minis were flat, S&P 500 stock futures up 13.75 points or 0.34% and Nasdaq 100 E-minis were up 122 points, or 0.89%. The S&P 500 and the Dow ended a choppy session near record highs on Wednesday, while the tech-heavy Nasdaq is still more than 3% below its February all-time high.

On Wednesday, the Fed acknowledged an improving economic outlook buoyed by massive fiscal spending and accelerating vaccinations in minutes from its latest meeting which showed members felt the economy was still far short of target and were in no rush to scale back their $120 billion a month of bond buying. Policymakers noted it would be “some time” before conditions improve enough for the Fed to rein in its support. Between the commitment to low rates and speculation that Biden's infrastructure plan will be lowered down, interest rates resumed their decline. Elsewhere, Treasury Secretary Janet Yellen unveiled details of a plan to bring back about $2 trillion in corporate profits into the U.S. tax net. That would help fund the government’s spending initiatives, potentially reducing reliance on more borrowing that could drive rates higher.

“Many economists and market participants have been worried about a surge in inflation, but the Fed doesn’t seem to be,” Hussein Sayed, chief market strategist at FXTM, said in a client note. “So far, it seems we are in a Goldilocks situation. Expect U.S. stocks to continue outperforming non-U.S. stocks at least in the short term, equities to outperform bonds and, if corporate earnings surprise to the upside, this would pave the way for more record highs.”

Nasdaq futures jumped about 1% on Thursday, as tech-related stocks climbed ahead of weekly jobless claims data, helped by 10Y rates that dropped to session lows. FAAMG stocks rose between 0.8% and 1% in premarket trading. High-growth tech stocks have recovered in recent sessions as U.S. 10-year bond yields backed off from their 14-month highs.

In Europe, the Stoxx 600 index was up 0.3%, hitting a new high of 436.66 points, led higher by consumer products and services companies, with health care also higher, and insurance companies and banks falling as yield curves, particularly in the U.S., bull flattened. London’s blue chip FTSE 100 index was up 0.2%, while France’s CAC 40 Index jumped to its highest level since 2000. Anglo American Plc was one of the region’s biggest gainers after outlining plans to spin off its South African coal mines. AstraZeneca Plc also gained, outperforming health peers, after EU governments failed to agree on a policy that would limit the use of the drugmaker’s coronavirus vaccine over potential clotting side-effects. Here are some of the biggest European movers today:

- Johnson Matthey shares rise as much as 7.8% to hit the highest since July 2019. The firm’s update implied earnings ahead of expectations and the review of its health division could unlock significant value, Jefferies wrote in a note.

- Metso Outotec shares jump as much as 3.8% after the company signed a contract for the supply of a large-capacity Grate-Kiln pellet plant in the state of Odisha, India.

- Sage Group shares advance as much as 2.7% after Citi upgraded the software firm to buy from neutral. The broker said news flow is turning more positive and company’s valuation should subsequently begin to reflect greater confidence in the longer-term growth outlook.

- Telenor shares rise as much as 4% after the company and Axiata said they were in talks to merge their mobile-phone operations in Malaysia. Goldman Sachs the discussions said were “a strategic positive.” The broker said deal is “a positive for the local synergies it could generate.”

- Gerresheimer shares fall as much as 6.2% after the company reported 1Q organic growth that Commerzbank said was below estimates.

“It’s looking good as evaluations in Europe are much lower than they are in the U.S. so there is potentially more upside. The line of least resistance for European markets is higher,” said Michael Hewson, chief market analyst at CMC Markets. “In terms of economic re-opening, there is enough optimism built in at the moment to drive markets quite a bit higher from here, and the Fed has reiterated it’s going to remain on hold for a while,” Hewson said.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares ex-Japan inched up 0.3% in quiet trade. Japan’s Nikkei slipped 0.3%, not helped by news Tokyo’s governor had asked for emergency measures to stem a surge of COVID-19 infections.

Asian stocks advanced, erasing earlier losses with Hong Kong among leading gainers with AIA Group providing the biggest boost. The Hang Seng Index advanced more than 1% to the highest closing level since Mar. 18. Insurance giant AIA was the largest contributor to both the Hong Kong benchmark and the MSCI Asia Pacific Index. AIA rallied 6.2% as Morgan Stanley said the life insurer’s expansion in China is key to maintaining its “premium” valuation. The brokerage lifted its target on the company by 46%. Key measures in Australia and New Zealand were also among the top gainers in the region, with the S&P/ASX 200 index climbing to its highest since February 2020. Earlier, Asian stocks were dragged down by losses in Japan as Tokyo considered a return to stricter coronavirus measures amid rising infections. Sector-wise, communication services and utilities were the worst performers on the MSCI Asia Pacific Index. Financials and materials shares advanced.

China’s stocks edged higher following a two-day slide, boosted by a rebound in healthcare and consumer staples firms. The benchmark CSI 300 Index rose 0.2% to close at 5,112.21 points, after erasing an earlier decline. Trading has stayed in a narrow band this week, extending a trend since early last month. Turnover on the Shanghai and Shenzhen markets rebounded to 726 billion yuan ($111 billion), the highest since March 29. Liquor makers including Kweichow Moutai stabilized after recent declines, with CGS-CIMB analysts noting that baijiu distillers likely saw sales growth of 10%-20% in the first quarter relative to 2020 as consumption levels normalize. Moutai rose 0.4%. Such sideways trading offers investors a respite following the stock gauge’s swift tumble into a technical correction last month. While it will take time for the market to digest potential risks in the future, including potential liquidity tightening, bellwether stocks remain among the most valuable firms within various industries despite high valuations, according to an Everbright Securities note.

Japanese stocks slid as Tokyo sought a return to stricter coronavirus measures amid increasing infections. Banks drove a broad decline in the Topix, which was headed for its third-straight weekly drop. Travel and retail stocks were weak amid virus concerns. Advantest and Sony were the largest drags on the Nikkei 225. Fast Retailing gained ahead of its earnings report, just after the market close. Tokyo Governor Yuriko Koike said she will ask the central government to designate the capital as an area that requires stricter coronavirus measures. The nation’s capital reported 545 new cases on Thursday after 555 on Wednesday, the highest daily total since early February. “Infections in Japan are rising, which will impact sectors like services and logistics, though the impact on manufacturing will be limited,” said Takashi Ito, an equity market strategist at Nomura Securities in Tokyo. “With earnings season kicking off with retail companies, investors are keen to see what their outlook for the current fiscal year is like and what impact the pandemic has.”

Australian stocks jumped to a 13 month high, with the S&P/ASX 200 index rising 1% to close at 6,998.80, its highest level since since Feb. 21, 2020 and less than 200 points away from a record high. The benchmark climbed for a fifth consecutive session in its longest streak since Dec. 9. Miners led the rally as iron ore futures in Singapore held near their highest close in almost a month. EML Payments was the best performer, extending gains on the back of its deal to acquire payments firm Sentenial. Resolute Mining was the worst performer, snapping a four-day winning streak.

In rates, as shown above, Treasuries held gains across the curve, with 10-year yields richer by nearly 3bp on the day, down to 1.647%, vs little-changed bunds and gilts, flattening 2s10s by ~2bp. Yields on 10-year Treasuries have eased back to 1.642% from the recent 14-month high of 1.776%, but have struggled to break under 1.59%. The TSY curve is flatter as long end outperforms, while Treasuries lead bunds and gilts. Notable treasury futures flows according to Bloomberg include an $800k/DV01 5-year vs bond contract block trade printed at 5:09am ET. Fed speakers Thursday include Chair Powell in a panel discussion on the global economy during IMF meeting.

Gains by U.S. Treasuries helped risk assets, although analysts said markets will be tested next week when the U.S. earnings seasons gets underway.

In FX, the dollar fell against most of its G-10 peers; the greenback is about to extend its recent run lower if charts are anything to go by. Australian and New Zealand dollars lead gains along with Japanese yen, which extended an Asia session advance against the dollar to a high of 109.44, testing the 21-DMA. The euro pared an early advance to trade little changed; euro-dollar options are overpriced again and may remain so if the pair keeps rallying in the spot market due to market makers’ positioning. The pound was little changed after erasing an earlier advance amid cautiously improving sentiment on the nation’s vaccine rollout.

In commodities, oil prices fell after official figures showed a big increase in U.S. gasoline stockpiles, causing concerns about demand for crude weakening in the world’s biggest consumer of the resource at a time when supplies around the world are rising. Brent fell 22 cents to $62.94 a barrel while WTI lost 37 cents to $59.40 per barrel. Gold was at $1,743 an ounce after meeting resistance around $1,745.

Looking at today's calendar, the weekly initial claims report due at 830am ET is expected to show the number of Americans filing for new unemployment benefits dropped in the latest week, a further sign that the labor market’s conditions were improving. Also on deck today, Fed Chair Jerome Powell will speak at a virtual International Monetary Fund event at 1200 ET. We’ll also get the minutes of the ECB’s March meeting. Data releases include German factory orders for February and the March construction PMIs from both Germany and the UK. Otherwise, there’s the Euro Area’s PPI for February.

Market Snapshot

- S&P 500 futures up 0.3% to 4,081.50

- MXAP up 0.2% to 207.29

- STOXX Europe 600 up 0.3% to 435.66

- MXAPJ up 0.5% to 692.55

- Nikkei little changed at 29,708.98

- Topix down 0.8% to 1,951.86

- Hang Seng Index up 1.2% to 29,008.07

- Shanghai Composite little changed at 3,482.56

- Sensex up 0.7% to 50,006.37

- Australia S&P/ASX 200 up 1.0% to 6,998.77

- Kospi up 0.2% to 3,143.26

- Brent Futures down 0.3% to $62.95/bbl

- Gold spot up 0.3% to $1,742.74

- U.S. Dollar Index down 0.1% to 92.37

- German 10Y yield fell 0.6 bps to -0.330%

- Euro up 0.1% to $1.1879

Top Overnight News from Bloomberg

- The U.S. is proposing that countries should be able to tax more corporate profits based on revenues within their borders in a bid to reach a global taxation deal

- Currency traders have reaped gains this year betting on the U.K.’s vaccine success and against Europe’s stumbles. Now that trade in going in reverse

- ECB Governing Council member Robert Holzmann tells CNBC that the decision on PEPP bond purchases in the third quarter will be decided upon at the end of the second

- Peter Thiel is “pro-crypto” and “pro-Bitcoin maximalist,” but he also thinks the cryptocurrency may be undermining America

- The EU failed to form a united response to links between AstraZeneca Plc’s Covid-19 vaccine and a rare type of blood clotting, missing an opportunity to inject momentum into the bloc’s sluggish inoculation program

- Warren Buffett’s Berkshire Hathaway Inc. priced yen-denominated bonds on Thursday, as yield premiums in the Japanese market have tightened to the least in over two years

A quick look at global markets courtesy of Newsquawk

Asia-Pac bourses traded mixed-to-positive as the region took its cue from Wall Street where the major indices finished relatively flat after having meandered near their record levels following an anticlimactic FOMC Minutes release, although US equity futures gradually made headway after-hours. ASX 200 (+1.0%) advanced with resilience seen across all industries led by strength in the blue-chip miners and big 4 banks to lift the index briefly above the 7,000-milestone. Nikkei 225 (-0.1%) was subdued amid reports Japan is considering stronger COVID-19 controls in Tokyo and other cities but with losses cushioned by recent M&A news including the buyout offer for Toshiba and with Hitachi said to be in discussions with Bain regarding a potential sale of Hitachi Metals which boosted shares in the latter by nearly 5.0%, while the KOSPI (-0.1%) lacked direction as participants reflected on the stunning defeat by South Korea’s ruling Democratic party at the Seoul and Busan mayoral elections and as domestic COVID-19 cases continued to increase. Hang Seng (+1.2%) and Shanghai Comp. (+0.1%) were varied with sentiment in the mainland clouded by ongoing tensions in the South China Sea after the US warned China of its increasingly aggressive moves, while Hong Kong was underpinned by strength in the tech sector aside from industry heavyweight Tencent which was pressured on reports its largest shareholder plans to offload around USD 15bln of Co. shares. Finally, 10yr JGBs were lacklustre after the indecisive trade seen in USTs and as support from the firmer demand at the 5yr JGB auction dwindled, while Australian yields were slightly softer in the belly amid the RBA operation for AUD 2bln of government bonds.

Top Asian News

- India Seeks U.S. Help as China-Backed Hacks Threaten Military

- Uniqlo Owner’s Profit Rebounds as Pandemic Shoppers Return

- Jokowi Doubles Indonesia’s Wealth Fund Goal to $200 Billion

- Goldman-Backed ReNew to Invest $9 Billion in India’s Green Push

Stocks in Europe trade mostly higher, but with mild gains and off the best levels seen at the cash open (Euro Stoxx 50 +0.2%) as the region mimics a similar sentiment seen overnight and during US hours yesterday. US equity futures meanwhile see more of an advance with the NQ (+1.0%) and RTY (+0.8%) leading the gains. Fresh catalysts during European hours have been light, with a number of ECB speakers sticking to the script ahead of the ECB March accounts later today, whilst Fed Chair Powell is also poised to make an appearance at the IMF panel. European bourses see mostly broad-based gains with the exception of the IBEX (-0.1%) - weighed on by its exposure to Banks and Travel & Leisure, which reside as sectoral laggards in the region alongside Oil & Gas and Insurance. Meanwhile, some of the more defensive sectors are faring better - with Healthcare, Consumer Staples and Utilities posting relatively stronger performances thus far. The tech sector in Europe is also supported amid the low yield environment and following the Tech performance on Wall Street yesterday, whilst participants for now shrug off source reports that Apple (+0.6% pre-mkt) has postponed some production of some MacBooks and iPads due to the global component shortage. Source added that a a portion of the component orders for the two devices have been pushed back to H2-2021 from H1. In terms of individual movers, KPN (+3%) holds onto gains amid reports that PE firms EQT and Stonepeak are said to be mulling a joint USD 15bln bid for KPN, reportedly at over EUR 3/shr. Elsewhere, Johnson Matthey's (+3.4%) trading updates bolstered the stock to the top of the Stoxx 600.

Top European News

- EU Fails to Find United Response to AstraZeneca Vaccine Risk

- Tesla Bemoans ‘Irritating’ Approval Process for Berlin Plant

- American Financiers Want to Shake Up Fans-First German Soccer

- Norway’s $1.3 Trillion Wealth Fund to Add External Managers

In FX, the Buck is softer vs most G10 rivals in wake of the latest FOMC policy meeting minutes that added little new in terms of insight or guidance, but reaffirmed the message that there is some way to go before inflation and jobs hit target. Hence, the focus turns swiftly to Fed chair Powell at the IMF for his more up-to-date assessment of developments and the economic recovery outlook, especially given last Friday’s big US headline payrolls beat and a record high services ISM. On that note, the upcoming IJC release will provide an even more timely snapshot of the labour market ahead of his speech and comments from Bullard. Looking at the DXY, 92.500-000 continues to encapsulate trade following the break down from month end and earlier April highs in the index and Greenback overall, with underlying support forged from still relatively firm Treasury yields and a steeper curve in contrast to bullish-buoyant risk sentiment that is keeping the Dollar capped.

- JPY - Having repelled more selling pressure and another attempt to fill bids into 110.00, the Yen is now trying to breach half round number resistance at 109.50 convincingly before setting sights on more levels to fill gaps left behind following the sharp spike in Usd/Jpy that hit 110.97 on March 31.

- NZD/AUD - Also taking advantage of their US peer’s indecision, with the Kiwi and Aussie both surviving more concerted efforts to test round number and psychological support overnight when the general risk tone was fragile to stabilise around the middle of 0.7044-04 and 0.7648-03 respective ranges. Note, Nzd/Usd also had another downbeat business survey to contend with as ANZ sentiment soured and the activity outlook dipped, while Aud/Usd will be looking to the RBA’s FSR for some independent direction after unchanged policy and guidance from the Board earlier this week.

- CHF/EUR/GBP/CAD - The Franc and Euro have lost momentum vs the Dollar, though remain rangebound between 0.9302-0.9275 and 1.1893-1.1861 after fleeting or false upside forays on Wednesday, but Eur/Usd may now be reliant on ECB minutes for direction and also conscious that hefty option expiry interest lies just above the 200 DMA at the 1.1900 strike (1.9 bn), while not that much less resides between 1.1850-40 (1.5 bn to be precise). Elsewhere, the Pound seems to be at the whim of Eur/Gbp moves again, as Cable pivots 1.3750 and derives little impetus from a stronger than expected UK construction PMI, while bulls and bears tussle over the cross within a 0.8657-21 range. Conversely, Friday’s Canadian employment report should provide the Loonie with direction given Usd/Cad’s current containment around the 1.2600 axis eyeing crude/commodity prices and the unfolding wave of COVID-19.

- SCANDI/EM - The Sek has unwound some of its underperformance after mixed Swedish data, but the Rub remains under pressure amidst more punchy rhetoric from Russia in response to the threat of further US sanctions.

US Event Calendar

- 8:30am: March Continuing Claims, est. 3.64m, prior 3.79m

- 8:30am: April Initial Jobless Claims, est. 680,000, prior 719,000

Central Banks

- 11am: Fed’s Bullard Discusses Economy and Monetary Policy

- 12pm: Powell Takes Part in IMF Panel on Global Economy

- 2pm: Fed’s Kashkari Discusses U.S. Economic Outlook

DB's Jim Reid concludes the overnight wrap

Markets continued to hover around their all-time highs yesterday as investors digested the latest Fed minutes and looked forward to Chair Powell’s remarks today, with risk assets getting further support from the fact that bond yields continued to remain subdued in spite of some pretty strong data releases of late. By the close of trade, the S&P 500 had managed to eke out a +0.15% gain, which took the index to yet another record high, with the advance led by large tech companies in particular as the NYFANG index (+0.55%) recorded its 8th successive move higher. Meanwhile the overall environment remained an incredibly benign one for investors, with the VIX index of volatility falling to 17.16pts – its lowest level since the pandemic started – whilst Bloomberg’s index of US financial conditions eased further to its most accommodative level since late-2018.

In a day that didn’t see a massive amount of newsflow, the Fed minutes were the main highlight, and showed that the committee members remain cautious with regards to the economic recovery and do not feel any urgency to remove accommodation. The overall tone was dovish and there seemed to be no concern of an overheating economy – in fact the word overheat did not appear in the minutes at all – and Fed members believe it will be “some time” before asset purchases are tapered. Though the committee notably increased their economic and inflation forecasts last month, the minutes showed continued concerns stemming from the pandemic – including the pace of vaccinations and new variants. There were also concerns about stresses in the commercial real estate market “associated with the unwinding of mortgage forbearance and eviction moratoriums provided to households”, which they will continue to monitor.

US 10yr Treasuries were near flat just prior to the minutes being released and then rose +2.3bps by the end of the day to finish the session +1.8bps higher at 1.674%. Inflation expectations (+2.7bps) drove the small rise in yields, which was tempered by a drop in real yields (-0.9bps). Given the messaging that little-to-no action was expected in the short term the 2y10y curve steepened +2.2bps. However, in spite of yesterday’s moves higher for yields, the benchmark 10yr yield is still a little more than -10bps beneath its intraday high that it hit a little more than a week ago. This came as other Fed speakers sounded a relaxed note on inflation, with Dallas Fed President Kaplan saying that “when we get into the summer months of 2021 you’re going to see year-over-year comparisons that could be well in excess of 2.5%”. Meanwhile Governor Brainard said that after the “transitory pressures associated with reopening, it’s more likely that the entrenched inflation dynamics that we’ve seen for well over a decade will take over than that there will be a sustained surge in inflation for a persistent period”. Investors will be looking forward to Fed Chair Powell’s remarks later today, where he’s scheduled to speak at an IMF debate on the global economy at their virtual spring meetings. He’ll be appearing alongside the managing director of the IMF, the Irish finance minister and the Director-General of the World Trade Organization.

Overnight in Asia, markets have mostly taken Wall Street’s lead and are trading higher with the Hang Seng (+0.83%), Shanghai Comp (+0.19%), India’s Nifty (+0.73%) and Asx (+0.98%) all posting gains. An exception to this pattern are the Kospi (-0.01%) which is essentially flat and the Nikkei (-0.38%) which is trading down. Elsewhere, futures on the S&P 500 are up +0.43% following the index’s record high yesterday, and European ones are also pointing to a positive open.

Looking at other markets yesterday, European equities also hovered around their recent highs, with the major indices including the STOXX 600 (-0.22%), the DAX (-0.24%) and the CAC 40 (-0.01%) seeing modest declines. The main exception to this was the FTSE 100 (+0.91%) which hit a post-pandemic high as the index was supported by the weaker pound sterling (-0.63% vs USD). Sovereign bond yields fell back too across the region, with those on 10yr bunds (-0.8bps), OATs (-1.2bps) and gilts (-2.4bps) all moving lower.

In terms of the latest on the pandemic, the main news yesterday was with regard to the AstraZeneca vaccine as multiple countries adjusted their guidance following reviews of the blood clot incidents. The European Medicines Agency concluded that unusual blood clots with low blood platelets should be listed as very rare side effects of the vaccine, saying that most of the reported cases have been in women under 60 within 2 weeks of receiving the vaccine. Nevertheless, their view remained that the benefits still outweighed the risks of the vaccine, given the odds of hospitalisation and death from Covid-19. Here in the UK, the MHRA’s review vaccine regulator said that evidence of a link between blood clots and the AZ vaccine was stronger, but further work was still needed. In response, the JCVI said that under-30s would be offered an alternative vaccine, although those who’d already had a first dose of AZ and hadn’t suffered from blood clots should still get their second dose. Finally, South Korea moved to temporarily suspend the AZ vaccines for the under-60s.

More broadly, the global case count continues to remain elevated, and in absolute terms the weekly increase at the moment is still at a faster pace than that seen throughout all of February and March, according to John Hopkins data. In the US, the variant first found in the UK has now overtaken the initial strain of the virus as the most common across the country, whilst cases overall have flattened around 65k a day. With vaccinations continuing to accelerate, states are going ahead with plans to reopen parts of the economy this summer. Yesterday, New York announced beaches would be fully reopened as of the start of June after barring swimmers last year, which comes after California announced a full reopening as of June 15. However in Ontario, Canada’s biggest province, a state of emergency was declared overnight and a stay-at-home order was issued. And in Asia, the Tokyo region in Japan is looking at the return of restrictions such as bars and restaurants being asked to close early after the region reported 555 cases yesterday, the most since early February. In India, as the spread of the virus accelerates, the country is now facing vaccine shortages in various states and cities including in the financial capital of Mumbai. The worst-hit Indian state of Maharashtra reported around 60,000 cases yesterday, and the state’s health minister said that it has only 3 days’ worth of vaccines in stock.

There was progress at yesterday’s G20 finance ministers meeting on reaching agreement to reform global corporate taxes, with the communique saying that they would “continue our cooperation for a globally fair, sustainable, and modern international tax system”, with an aim to reach “a global and consensus-based solution… by mid-2021.” Discussions have been ongoing for some time about whether to create a global minimum tax rate, as well as what to do about the challenges from digitisation, and although these ideas have been mooted for some years, the arrival of the new US administration has seen renewed progress, with Treasury Secretary Yellen voicing support for a global minimum corporate tax rate in a speech earlier this week. Overnight, the FT reported that the Biden administration had proposed that the largest multinationals would pay levies based on their sales in each country.

Staying on the tax theme, it’s also worth noting that the US Treasury Department unveiled a more detailed set of corporate tax proposals to fund the Biden administration’s infrastructure package announced last week. Nevertheless, the plans would need to win backing in Congress, and the centrist Democratic senator Joe Manchin has already said that he’s in favour of a 25% corporate tax rate, rather than the 28% proposed by the administration. Given the 50-50 split in the Senate between Republicans and Democrats, the administration would need to find at least some Republican support to pass the package if just one Democratic senator opposed the plans. Speaking of Manchin, a Washington Post op-ed released overnight saw the Senator say that there “is no circumstance in which I will vote to eliminate or weaken the filibuster”.

Wrapping up with yesterday’s data, the main releases came from the March services and composite PMIs in Europe, where upward revisions from the flash reading pointed to some decent underlying momentum at the end of Q1. The Euro Area services PMI was revised up to 49.6 (vs. flash 48.8) and the composite PMI was also revised up to 53.2 (vs. flash 52.5). The UK did see a slight downgrade in its composite PMI to 56.4 (vs. flash 56.6), but both France and Germany saw upward revisions to 50 and 57.3 respectively. It’ll be interesting to see if this is sustained next month, as our European economists have written (link here) that tighter restrictions present some near-term downside risks to their growth views, even if their overall view for the year remains optimistic. The other main release came from the US trade balance for February, which showed the trade deficit widening to a record high of $71.1bn (vs. $70.5bn expected).

To the day ahead now, and one of the main highlights will be Fed Chair Powell’s appearance on a panel discussing the global economy. Other Fed speakers include Bullard and Kashkari, and we’ll also get the minutes of the ECB’s March meeting. Data releases include German factory orders for February and the March construction PMIs from both Germany and the UK. Otherwise, there’s the Euro Area’s PPI for February and the weekly initial jobless claims from the US.

International

United Airlines adds new flights to faraway destinations

The airline said that it has been working hard to "find hidden gem destinations."

Share this:

Since countries started opening up after the pandemic in 2021 and 2022, airlines have been seeing demand soar not just for major global cities and popular routes but also for farther-away destinations.

Numerous reports, including a recent TripAdvisor survey of trending destinations, showed that there has been a rise in U.S. traveler interest in Asian countries such as Japan, South Korea and Vietnam as well as growing tourism traction in off-the-beaten-path European countries such as Slovenia, Estonia and Montenegro.

Related: 'No more flying for you': Travel agency sounds alarm over risk of 'carbon passports'

As a result, airlines have been looking at their networks to include more faraway destinations as well as smaller cities that are growing increasingly popular with tourists and may not be served by their competitors.

Shutterstock

United brings back more routes, says it is committed to 'finding hidden gems'

This week, United Airlines (UAL) announced that it will be launching a new route from Newark Liberty International Airport (EWR) to Morocco's Marrakesh. While it is only the country's fourth-largest city, Marrakesh is a particularly popular place for tourists to seek out the sights and experiences that many associate with the country — colorful souks, gardens with ornate architecture and mosques from the Moorish period.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

"We have consistently been ahead of the curve in finding hidden gem destinations for our customers to explore and remain committed to providing the most unique slate of travel options for their adventures abroad," United's SVP of Global Network Planning Patrick Quayle, said in a press statement.

The new route will launch on Oct. 24 and take place three times a week on a Boeing 767-300ER (BA) plane that is equipped with 46 Polaris business class and 22 Premium Plus seats. The plane choice was a way to reach a luxury customer customer looking to start their holiday in Marrakesh in the plane.

Along with the new Morocco route, United is also launching a flight between Houston (IAH) and Colombia's Medellín on Oct. 27 as well as a route between Tokyo and Cebu in the Philippines on July 31 — the latter is known as a "fifth freedom" flight in which the airline flies to the larger hub from the mainland U.S. and then goes on to smaller Asian city popular with tourists after some travelers get off (and others get on) in Tokyo.

United's network expansion includes new 'fifth freedom' flight

In the fall of 2023, United became the first U.S. airline to fly to the Philippines with a new Manila-San Francisco flight. It has expanded its service to Asia from different U.S. cities earlier last year. Cebu has been on its radar amid growing tourist interest in the region known for marine parks, rainforests and Spanish-style architecture.

With the summer coming up, United also announced that it plans to run its current flights to Hong Kong, Seoul, and Portugal's Porto more frequently at different points of the week and reach four weekly flights between Los Angeles and Shanghai by August 29.

"This is your normal, exciting network planning team back in action," Quayle told travel website The Points Guy of the airline's plans for the new routes.

stocks pandemic south korea japan hong kong europeanInternational

Walmart launches clever answer to Target’s new membership program

The retail superstore is adding a new feature to its Walmart+ plan — and customers will be happy.

Share this:

It's just been a few days since Target (TGT) launched its new Target Circle 360 paid membership plan.

The plan offers free and fast shipping on many products to customers, initially for $49 a year and then $99 after the initial promotional signup period. It promises to be a success, since many Target customers are loyal to the brand and will go out of their way to shop at one instead of at its two larger peers, Walmart and Amazon.

Related: Walmart makes a major price cut that will delight customers

And stop us if this sounds familiar: Target will rely on its more than 2,000 stores to act as fulfillment hubs.

This model is a proven winner; Walmart also uses its more than 4,600 stores as fulfillment and shipping locations to get orders to customers as soon as possible.

Sometimes, this means shipping goods from the nearest warehouse. But if a desired product is in-store and closer to a customer, it reduces miles on the road and delivery time. It's a kind of logistical magic that makes any efficiency lover's (or retail nerd's) heart go pitter patter.

Walmart rolls out answer to Target's new membership tier

Walmart has certainly had more time than Target to develop and work out the kinks in Walmart+. It first launched the paid membership in 2020 during the height of the pandemic, when many shoppers sheltered at home but still required many staples they might ordinarily pick up at a Walmart, like cleaning supplies, personal-care products, pantry goods and, of course, toilet paper.

It also undercut Amazon (AMZN) Prime, which costs customers $139 a year for free and fast shipping (plus several other benefits including access to its streaming service, Amazon Prime Video).

Walmart+ costs $98 a year, which also gets you free and speedy delivery, plus access to a Paramount+ streaming subscription, fuel savings, and more.

If that's not enough to tempt you, however, Walmart+ just added a new benefit to its membership program, ostensibly to compete directly with something Target now has: ultrafast delivery.

Target Circle 360 particularly attracts customers with free same-day delivery for select orders over $35 and as little as one-hour delivery on select items. Target executes this through its Shipt subsidiary.

We've seen this lightning-fast delivery speed only in snippets from Amazon, the king of delivery efficiency. Who better to take on Target, though, than Walmart, which is using a similar store-as-fulfillment-center model?

"Walmart is stepping up to save our customers even more time with our latest delivery offering: Express On-Demand Early Morning Delivery," Walmart said in a statement, just a day after Target Circle 360 launched. "Starting at 6 a.m., earlier than ever before, customers can enjoy the convenience of On-Demand delivery."

Walmart (WMT) clearly sees consumers' desire for near-instant delivery, which obviously saves time and trips to the store. Rather than waiting a day for your order to show up, it might be on your doorstep when you wake up.

Consumers also tend to spend more money when they shop online, and they remain stickier as paying annual members. So, to a growing number of retail giants, almost instant gratification like this seems like something worth striving for.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic mexicoUncategorized

Comments on February Employment Report

The headline jobs number in the February employment report was above expectations; however, December and January payrolls were revised down by 167,000 combined. The participation rate was unchanged, the employment population ratio decreased, and the …

Share this:

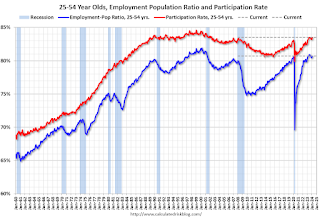

Prime (25 to 54 Years Old) Participation

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

{kind=link}

The 25 to 54 years old participation rate increased in February to 83.5% from 83.3% in January, and the 25 to 54 employment population ratio increased to 80.7% from 80.6% the previous month.

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES). Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 4.3% YoY in February.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of people employed part time for economic reasons, at 4.4 million, changed little in February. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons decreased in February to 4.36 million from 4.42 million in February. This is slightly above pre-pandemic levels.

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 7.3% from 7.2% in the previous month. This is down from the record high in April 2020 of 23.0% and up from the lowest level on record (seasonally adjusted) in December 2022 (6.5%). (This series started in 1994). This measure is above the 7.0% level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.203 million workers who have been unemployed for more than 26 weeks and still want a job, down from 1.277 million the previous month.

This is close to pre-pandemic levels.

Job Streak

| Headline Jobs, Top 10 Streaks | ||

|---|---|---|

| Year Ended | Streak, Months | |

| 1 | 2019 | 100 |

| 2 | 1990 | 48 |

| 3 | 2007 | 46 |

| 4 | 1979 | 45 |

| 5 | 20241 | 38 |

| 6 tie | 1943 | 33 |

| 6 tie | 1986 | 33 |

| 6 tie | 2000 | 33 |

| 9 | 1967 | 29 |

| 10 | 1995 | 25 |

| 1Currrent Streak | ||

Summary:

The headline monthly jobs number was above consensus expectations; however, December and January payrolls were revised down by 167,000 combined. The participation rate was unchanged, the employment population ratio decreased, and the unemployment rate was increased to 3.9%. Another solid report.

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Redefining Poverty: Towards a Transpartisan Approach

Catastrophic Risk: Investing and Business Implications

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Is the biotech market rally real? Data suggest comeback in private, public markets

The Digest #187

People Who Received Ivermectin Were Better Off, Study Finds

Interest rates, the best it gets. It’s time to deploy cash

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges