Uncategorized

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Watch: President Biden Delivers The "Darkest, Most Un-American Speech Given By A President"

Having successfully raged, ranted, lied, and yelled…

Share this:

Having successfully raged, ranted, lied, and yelled through the State of The Union, President Biden can go back to his crypt now.

Whatever 'they' gave Biden, every American man, woman, and the other should be allowed to take it - though it seems the cocktail brings out 'dark Brandon'?

Tl;dw: Biden's Speech tonight ...

-

Fund Ukraine.

-

Trump is threat to democracy and America itself.

-

Abortion is good.

-

American Economy is stronger than ever.

-

Inflation wasn't Biden's fault.

-

Illegals are Americans too.

-

Republicans are responsible for the border crisis.

-

Trump is bad.

-

Biden stands with trans-children.

-

J6 was the worst insurrection since the Civil War.

(h/t @TCDMS99)

Tucker Carlson's response sums it all up perfectly:

"that was possibly the darkest, most un-American speech given by an American president. It wasn't a speech, it was a rant..."

Carlson continued: "The true measure of a nation's greatness lies within its capacity to control borders, yet Bid refuses to do it."

"In a fair election, Joe Biden cannot win"

And concluded:

“There was not a meaningful word for the entire duration about the things that actually matter to people who live here.”

Victor Davis Hanson added some excellent color, but this was probably the best line on Biden:

"he doesn't care... he lives in an alternative reality."

— Tucker Carlson (@TuckerCarlson) March 8, 2024

* * *

Watch SOTU Live here...

* * *

Mises' Connor O'Keeffe, warns: "Be on the Lookout for These Lies in Biden's State of the Union Address."

On Thursday evening, President Joe Biden is set to give his third State of the Union address. The political press has been buzzing with speculation over what the president will say. That speculation, however, is focused more on how Biden will perform, and which issues he will prioritize. Much of the speech is expected to be familiar.

The story Biden will tell about what he has done as president and where the country finds itself as a result will be the same dishonest story he's been telling since at least the summer.

He'll cite government statistics to say the economy is growing, unemployment is low, and inflation is down.

Something that has been frustrating Biden, his team, and his allies in the media is that the American people do not feel as economically well off as the official data says they are. Despite what the White House and establishment-friendly journalists say, the problem lies with the data, not the American people's ability to perceive their own well-being.

As I wrote back in January, the reason for the discrepancy is the lack of distinction made between private economic activity and government spending in the most frequently cited economic indicators. There is an important difference between the two:

-

Government, unlike any other entity in the economy, can simply take money and resources from others to spend on things and hire people. Whether or not the spending brings people value is irrelevant

-

It's the private sector that's responsible for producing goods and services that actually meet people's needs and wants. So, the private components of the economy have the most significant effect on people's economic well-being.

Recently, government spending and hiring has accounted for a larger than normal share of both economic activity and employment. This means the government is propping up these traditional measures, making the economy appear better than it actually is. Also, many of the jobs Biden and his allies take credit for creating will quickly go away once it becomes clear that consumers don't actually want whatever the government encouraged these companies to produce.

On top of all that, the administration is dealing with the consequences of their chosen inflation rhetoric.

Since its peak in the summer of 2022, the president's team has talked about inflation "coming back down," which can easily give the impression that it's prices that will eventually come back down.

But that's not what that phrase means. It would be more honest to say that price increases are slowing down.

Americans are finally waking up to the fact that the cost of living will not return to prepandemic levels, and they're not happy about it.

The president has made some clumsy attempts at damage control, such as a Super Bowl Sunday video attacking food companies for "shrinkflation"—selling smaller portions at the same price instead of simply raising prices.

In his speech Thursday, Biden is expected to play up his desire to crack down on the "corporate greed" he's blaming for high prices.

In the name of "bringing down costs for Americans," the administration wants to implement targeted price ceilings - something anyone who has taken even a single economics class could tell you does more harm than good. Biden would never place the blame for the dramatic price increases we've experienced during his term where it actually belongs—on all the government spending that he and President Donald Trump oversaw during the pandemic, funded by the creation of $6 trillion out of thin air - because that kind of spending is precisely what he hopes to kick back up in a second term.

If reelected, the president wants to "revive" parts of his so-called Build Back Better agenda, which he tried and failed to pass in his first year. That would bring a significant expansion of domestic spending. And Biden remains committed to the idea that Americans must be forced to continue funding the war in Ukraine. That's another topic Biden is expected to highlight in the State of the Union, likely accompanied by the lie that Ukraine spending is good for the American economy. It isn't.

It's not possible to predict all the ways President Biden will exaggerate, mislead, and outright lie in his speech on Thursday. But we can be sure of two things. The "state of the Union" is not as strong as Biden will say it is. And his policy ambitions risk making it much worse.

* * *

The American people will be tuning in on their smartphones, laptops, and televisions on Thursday evening to see if 'sloppy joe' 81-year-old President Joe Biden can coherently put together more than two sentences (even with a teleprompter) as he gives his third State of the Union in front of a divided Congress.

President Biden will speak on various topics to convince voters why he shouldn't be sent to a retirement home.

The state of our union under President Biden: three years of decline. pic.twitter.com/Da1KOIb3eR

— Speaker Mike Johnson (@SpeakerJohnson) March 7, 2024

According to CNN sources, here are some of the topics Biden will discuss tonight:

Economic issues: Biden and his team have been drafting a speech heavy on economic populism, aides said, with calls for higher taxes on corporations and the wealthy – an attempt to draw a sharp contrast with Republicans and their likely presidential nominee, Donald Trump.

Health care expenses: Biden will also push for lowering health care costs and discuss his efforts to go after drug manufacturers to lower the cost of prescription medications — all issues his advisers believe can help buoy what have been sagging economic approval ratings.

Israel's war with Hamas: Also looming large over Biden's primetime address is the ongoing Israel-Hamas war, which has consumed much of the president's time and attention over the past few months. The president's top national security advisers have been working around the clock to try to finalize a ceasefire-hostages release deal by Ramadan, the Muslim holy month that begins next week.

An argument for reelection: Aides view Thursday's speech as a critical opportunity for the president to tout his accomplishments in office and lay out his plans for another four years in the nation's top job. Even though viewership has declined over the years, the yearly speech reliably draws tens of millions of households.

Sources provided more color on Biden's SOTU address:

The speech is expected to be heavy on economic populism. The president will talk about raising taxes on corporations and the wealthy. He'll highlight efforts to cut costs for the American people, including pushing Congress to help make prescription drugs more affordable.

Biden will talk about the need to preserve democracy and freedom, a cornerstone of his re-election bid. That includes protecting and bolstering reproductive rights, an issue Democrats believe will energize voters in November. Biden is also expected to promote his unity agenda, a key feature of each of his addresses to Congress while in office.

Biden is also expected to give remarks on border security while the invasion of illegals has become one of the most heated topics among American voters. A majority of voters are frustrated with radical progressives in the White House facilitating the illegal migrant invasion.

It is probable that the president will attribute the failure of the Senate border bill to the Republicans, a claim many voters view as unfounded. This is because the White House has the option to issue an executive order to restore border security, yet opts not to do so

Maybe this is why?

Most Americans are still unaware that the census counts ALL people, including illegal immigrants, for deciding how many House seats each state gets!

— Elon Musk (@elonmusk) March 7, 2024

This results in Dem states getting roughly 20 more House seats, which is another strong incentive for them not to deport illegals.

While Biden addresses the nation, the Biden administration will be armed with a social media team to pump propaganda to at least 100 million Americans.

"The White House hosted about 70 creators, digital publishers, and influencers across three separate events" on Wednesday and Thursday, a White House official told CNN.

Not a very capable social media team...

The State of Confusion https://t.co/C31mHc5ABJ

— zerohedge (@zerohedge) March 7, 2024

The administration's move to ramp up social media operations comes as users on X are mostly free from government censorship with Elon Musk at the helm. This infuriates Democrats, who can no longer censor their political enemies on X.

Meanwhile, Democratic lawmakers tell Axios that the president's SOTU performance will be critical as he tries to dispel voter concerns about his elderly age. The address reached as many as 27 million people in 2023.

"We are all nervous," said one House Democrat, citing concerns about the president's "ability to speak without blowing things."

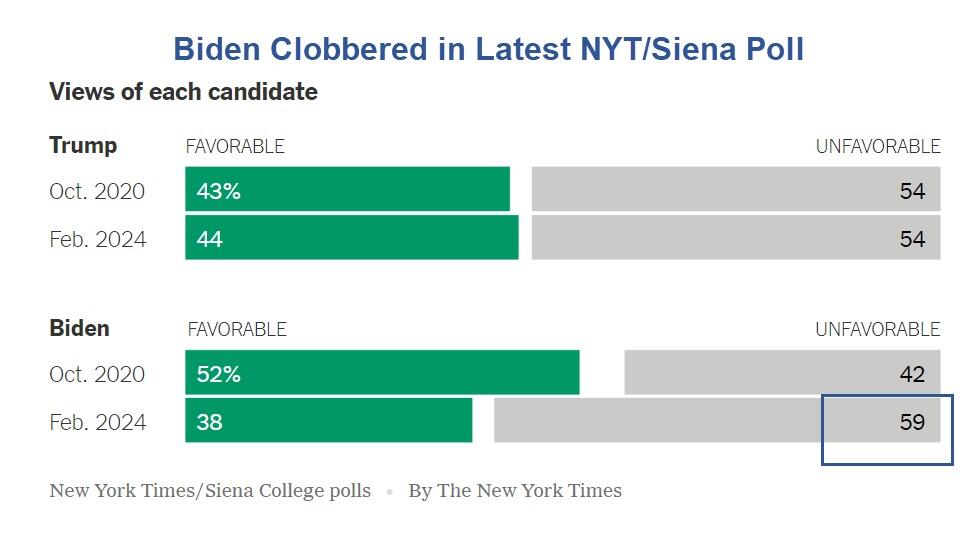

The SOTU address comes as Biden's polling data is in the dumps.

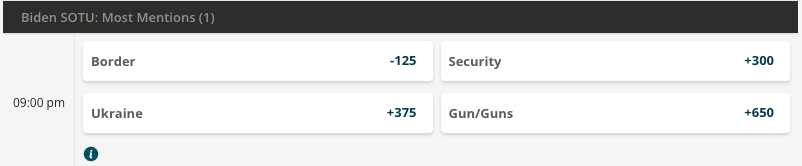

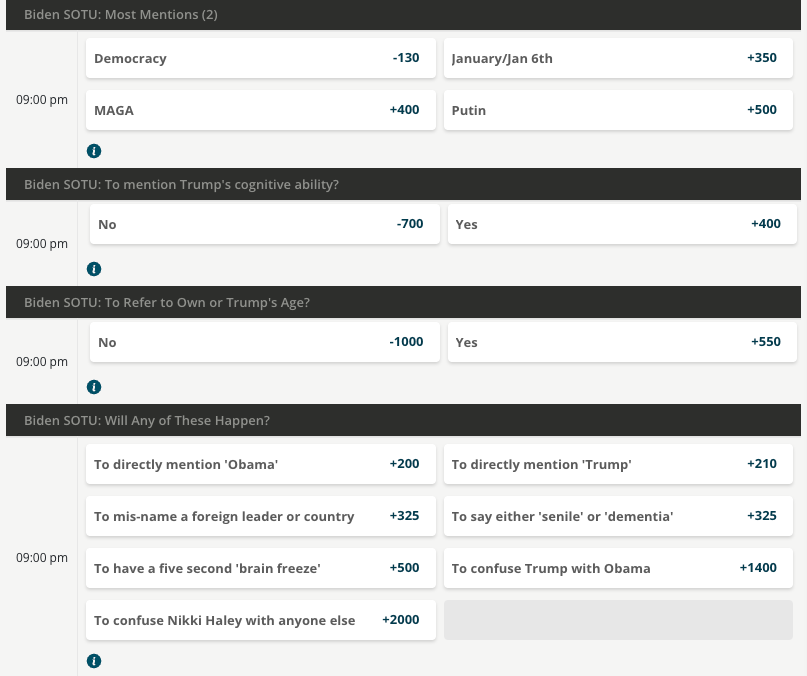

BetOnline has created several money-making opportunities for gamblers tonight, such as betting on what word Biden mentions the most.

As well as...

We will update you when Tucker Carlson's live feed of SOTU is published.

Fuck it. We’ll do it live! Thursday night, March 7, our live response to Joe Biden’s State of the Union speech. pic.twitter.com/V0UwOrgKvz

— Tucker Carlson (@TuckerCarlson) March 6, 2024

Uncategorized

Is the biotech market rally real? Data suggest comeback in private, public markets

After some halting starts, false dawns and fragile rallies, the biotech market may finally be back.

No, really.

In the last several months, several important…

Share this:

After some halting starts, false dawns and fragile rallies, the biotech market may finally be back.

No, really.

In the last several months, several important signals have added up to what feels like a rally, with more depth and certainty than some of the short-lived upticks during the doldrums of 2022 and 2023, when only the industry’s most optimistic souls were willing to call it a comeback.

But now, public biotechs are releasing positive data and raising money in follow-on offerings with ease. Biopharmas have already raised $13.7 billion in secondary raises in 2024, according to Stifel’s Tim Opler. Biotech’s benchmark index, the $XBI, is up 56% from last year’s lows and has broken the $100 mark, thanks to gains that go deep into the 120-company index. And in the private markets, crossover rounds are trickling back, and IPOs are showing signs of life.

Investors and executives told Endpoints News that this moment feels different, encouraged by a return to the basics, a focus on data, and signs of a healthier — if smaller — biotech ecosystem.

“We should be beyond any of the lows,” said Chris Garabedian, a venture portfolio manager at Perceptive Advisors and founder of the firm’s early-stage investing unit Xontogeny. “We are going to see continued forward momentum.”

Investor sentiment is “very different from what it was in ‘22 to ‘23, where it was all doom and gloom,” MoonLake Immunotherapeutics CEO Jorge Santos da Silva said. A year ago, “The question was like, ‘What are the 22 ways in which you can die?’ That has really changed.”

The XBI cracking $100 is encouraging, but a deeper look at the index shows more signs of strength. The exchange-traded fund, which lets investors buy shares of its basket of 120 biotech companies, has seen $457 million in net inflows over the past month, according to YCharts data. And about 80% of biotechs on the index — which includes giants like Vertex $VRTX and small companies like Avidity Biosciences $RNA — have seen their stock in the green over the past three months.

Some of that gain is clearly driven by a surge in M&A, including the buyouts of Seagen, Horizon, Cerevel, and Karuna, all of which have returned billions of dollars back to investors who need to put it back to work in the private or public markets. And industry insiders have said there’s also a breadth in the disease areas drawing interest, including obesity, cancer, cardiology, neurology, and inflammation.

Even ARCH Venture Partners managing director Bob Nelsen voiced some broader — albeit measured — optimism for the market.

“For our internal base case, we’re still assuming that things are going to suck like they have in the last couple of years,” Nelsen told Endpoints. “But we all believe that it has turned.”

Nelsen still implores his portfolio companies and limited partners to “assume it’s going to be worse than you think.” But his optimism is driven by two major trends: the easing of macro factors like interest rates and the persistence of M&A. He’s closely watching whether generalist investors — whose huge dollars can swing a sector up or down, as they did dramatically during the pandemic — will come back to biotech.

“The conventional wisdom in Q4 is, they were never coming back in the market,” he said. “Turns out, in Q4 they were buying.”

From atonement to ‘FOMO’

Jorge Santos da Silva

Jorge Santos da SilvaDa Silva said the industry had been “paying for our sins” committed in the boom years of 2019 to 2021, when hundreds of biotechs went public — many far from going into the clinic. Along with layoffs and company closures, it resulted in an infestation of the corporate walking dead in companies trading at values below the amount of cash on their books.

But the number of those companies with negative equity value has dropped in the past few months, suggesting that a much-needed cleanup from the go-go years is well in progress.

“I call it a detox,” da Silva said. “Whatever we did was clearly excessive and everyone knew it at the time. But when you’re at a party, it’s like, ‘Oh my God, this is crazy, but let’s keep going.’ The detox phase is definitely coming to an end.”

Otello Stampacchia

Otello StampacchiaOtello Stampacchia, the managing director of the Boston-based VC firm Omega Funds, said the mood is even “getting a little bit bubblicious” for biotechs with clinical-stage drug candidates in large markets with meaningful milestones in the next 12 to 18 months.

“There’s really a rush to get into those, particularly now that the indices have started flipping their dynamic,” said Stampacchia, who founded Omega two decades ago. “Up until early last fall, nobody wanted to catch the falling knife. It’s now the exact opposite dynamic, and there’s a bit of crowding in some of these names.”

“There’s real FOMO to invest in the right therapeutic products and the right therapeutic companies,” he added.

That’s carried through the private and public markets, Stampacchia said, noting that Omega participated in Alumis’ recent $259 million Series C raise — biotech’s biggest round this year. He said he was “incredibly surprised by the amount of demand there was for the deal.” All told, Omega has seen roughly half a dozen of its portfolio companies raise close to half a billion dollars over the last few months, with increased valuations.

“In each case, it really wasn’t difficult to syndicate,” he said. “There’s real demand.”

rna pandemic interest ratesUncategorized

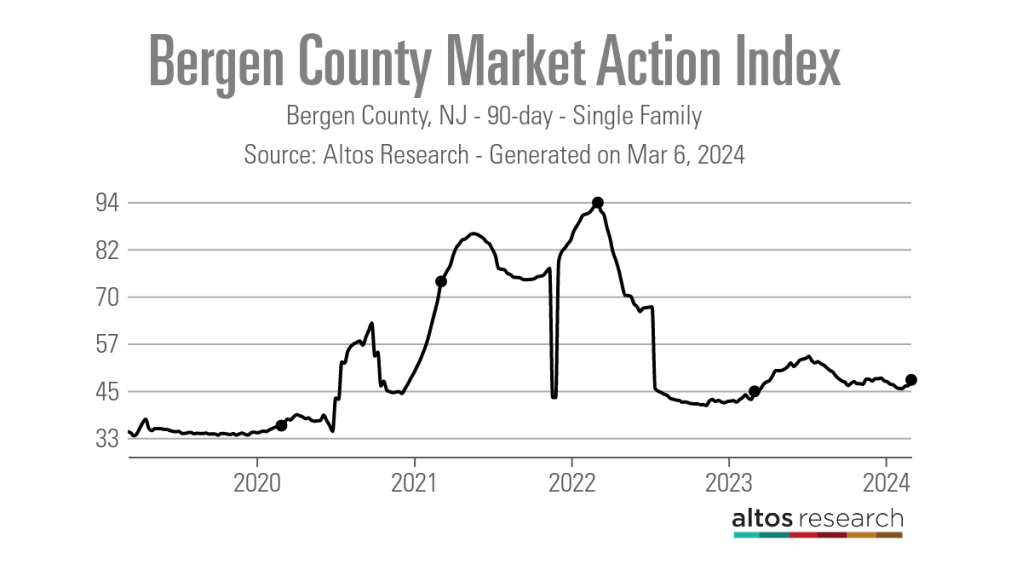

“It seems impossible:” Bergen County, NJ’s housing market is vexing agents and buyers

While the housing market has cooled from the buying frenzy during the pandemic, agents in the leafy Bergen County suburbs say it’s also gotten worse. We…

Share this:

Real estate agents in the leafy suburbs of Bergen County, New Jersey say the current housing market — with historically low inventory and record-high prices — is actually more challenging than the multiple offer chaos they sweated through during the pandemic.

“At the height of the pandemic there were bidding wars and all that, but it didn’t seem impossible, but now it seems impossible to get our buyers into homes,” said Heather Corrigan, a RE/MAX Signature Homes agent based in Closter, a borough that is 24 miles north of Manhattan and renown for its schools.

Altos Research’s Market Action Index score for the county, which has 70 municipalities, illustrates the challenges agents and their clients have faced. In March of 2022, the 90-day average Market Action Index score for the county hit a high of 93.84, before cooling over the past two years to a score of 47.98 as of March 6, 2024. Altos considers any score above 30 to be a seller’s market.

70 towns, 90 new listings

Local agents say the county’s tight inventory situation is largely to blame.

“We have been complaining about the lack of inventory for as long as I can remember, but then we at least had more listings,” Danny Yoon, an Edgewater, New Jersey-based Sotheby’s International Realty agent, said. “I was able to bring my clients to multiple listings for their consideration, but now I can only show them one or two in a given week. There is nothing to show.”

As of March 6, 2024, there was a 90-day average of 570 active single-family listings in Bergen County, according to Altos. This is down from a 90-day average of 752 active single-family listings a year ago and 2,052 active single-family listings in early March 2020, just at the onset of the COVID-19 pandemic.

“Bidding wars are still there but it isn’t as bad as during COVID,” said Lisa Comito, a broker at Howard Hanna Rand Realty and the president of Greater Bergen Realtors, which has nearly 9,000 members. “When we were coming out of COVID we were seeing 15 to 20 offers on a house, where you’d have to make a spreadsheet to show your seller. You aren’t getting that, but there is still a lot of competitive bidding.”

Like elsewhere in the country, agents blame the low interest rates of 2020 and 2021 for locking many would-be sellers into their homes.

“During the pandemic, people would downsize or sell their home on a whim,” Comito said. “Now it is a different conversation. If they are downsizing it is for quality of life or that they can’t maintain a large home anymore.”

Although agents are optimistic about what may come with the fast-approaching spring housing market, the numbers are not promising. Data from Altos Research shows that there were just 90 new single-family listings in Bergen County for the week ending March 1, 2024. This is the fewest number of new listings for the first week in March recorded in Altos’ data, which dates back to 2013.

“Some of the reports indicate that we are going to have more listings this year than last year, but the only way I can see that being correct is because we had so few listings last year,” Yoon said. “Even if we get more listings, it is not going to be enough for people. We are still going to suffer from lack of inventory.”

Prices climbing toward $1M

While questions remain over how many sellers will decide to enter the market this spring, agents are already seeing more buyers come to the market. That’s despite median list prices climbing to a record $899,000 in the first week of March 2024, up nearly $150,000 from March 2022, which Altos considers the market’s peak.

“There is a meme with two buyers sitting in chairs waiting for prices and interest rates to drop and the buyers are skeletons and I think there is some truth to that,” Corrigan said. “But now buyers are sick of waiting around and are deciding it is time to buy.”

Comito also believes the current interest rate environment is helping to encourage buyers to enter the market.

“Buyers right now have gotten more comfortable with the mortgage rates,” Comito said. “They have stayed pretty consistent, allowing people to adjust to them and they aren’t thinking as much about those low rates of the pandemic market.”

While buyers are facing inventory and interest rate challenges, agents say they are also facing competition from investors and the all-cash offers they are capable of making.

“I have well qualified clients who are putting down 25% and are coming over asking with no or limited inspections and they are getting beat out by investors with all-cash,” Corrigan said.

She noted that while some of the investors are larger corporations, there are also a lot of mom-and-pop investors out in the market, buying up inventory.

Comito noted that even first-time buyers are looking to get into rental properties.

“You are seeing first time buyers looking for multifamily properties where they can rent out the other units to help pay for their mortgage,” Comito said.

Even with the challenging housing market conditions, buyers are still flocking to Bergen County, and agents like Corrigan don’t see that changing.

“The schools are good, and everything is in close proximity,” Corrigan said. “Every town has its own unique features, whether it is a great library, the town pool, events they put on, great restaurants, it is really just a desirable place to live for so many people.”

mortgage rates real estate housing market pandemic covid-19 interest ratesUncategorized

A review of the Australian private credit market in 2023

2023 marked a year of both challenges and opportunities for the Australian private credit market. On the one hand, the tighter credit conditions in the…

Share this:

{kind=link}

2023 marked a year of both challenges and opportunities for the Australian private credit market. On the one hand, the tighter credit conditions in the first half of the year saw decreased activity in mergers and acquisitions (M&A), project finance and real estate development financing. On the other, the latter part of the year boasted a more stable interest rate and inflation outlook, as well as improved credit margins, supporting more resilient private credit portfolios.

Ernst and Young (EY) publish an annual report on the Australian private credit landscape, which is a must-read for anyone following this asset class, whether you are a believer or still sitting on the fence. I have summarised my key learnings from this report in the article below.

Market size – despite a slow 2023, there is still a big runway for growth

In 2023, the Australian private credit market saw robust growth of 7 per cent, with total assets under management reaching AU$188 billion. Whilst solid, this was moderate compared to the 32 per cent growth experienced in 2022. According to EY, business-related loans amounted to AU$112 billion, while commercial real estate-related loans amounted to AU$76 billion. Focussing on business-related loans, this included all lending that was not commercial real estate-related, such as leveraged and sponsor lending, direct lending, middle-market, small-to-medium sized business lending (SME), special situations, distressed and venture debt.

Importantly, private credit in Australia only represented 12 per cent of the total business related-loan market. Offshore, the private credit market globally was estimated to be as large as U.S.$1.6 trillion during 2023 and forecasted to continue to grow double digits well into 2028. As such, there is clearly still a big runway for growth here domestically.

Resilient performance – some sector challenges but borrower quality is key

Performance has been a strong point of attraction in accessing Australian private credit, with majority of providers being able to continue to pay out anywhere from cash plus three per cent per annum through economic shifts and challenges such as COVID-19 and the interest rate environment over the last couple of years.

In 2023, this, in part, can be attributed to insolvencies being very company-specific and experienced in more cyclical and challenged sectors. EY noted these to be construction, accommodation, hospitality and food, business services and retail trade. The ability for private credit providers to access a growing universe of quality borrowers, leaving more traditional finance providers, is a key thematic fuelling the continued stability of outcomes. Moreover, the Reserve Bank of Australia (RBA) noted in a recent report that SME lending accounted for over 50 per cent of total business lending in Australia. Despite this, lending to Australian SMEs only grew by six per cent over the year to September 2023.

The report also notes that more than 50 per cent of SMEs have issues accessing finance from traditional providers, with time to assess and approve being cited as a major impediment. Borrowers are also seeking alternate funding providers due to the size of the loans they are after (generally less than $2 million), duration (generally less than 12 months) and seeking to provide security outside of residential property. As such, this has carved out an area of the market that is starved for funding where niche private credit providers are still able to source strong forms of protection at the borrower level for working capital-focussed lending. In fact, the Australian Banking Association approximated the Australian SME loan market to be as large as AU$451 billion in 2022.

Outlook – energy transition is a big opportunity

EY further deduces that the economy-wide energy transition is another significant theme that will impact the Australian private credit market. With the need for capital investment in energy generation, technology, and infrastructure, private credit lenders are expected to play a crucial role.

In fact, quoting another recent EY publication, “Australia must attract an estimated $1.5 trillion in capital by 2030 and up to $9 trillion by 2060 to fund the transition to net zero emissions.” What role will private credit providers play here? EY namely cites in the form of new capital investments, refinancing and acquisition of lenders or loan books as traditional finance providers closely monitor their climate-related exposures under the new Australian sustainability reporting standards.

In conclusion, the Australian private credit market is navigating challenges with resilience and is well-positioned for growth in 2024. With improving economic conditions, a focus on sustainable investments, and a track record of portfolio quality, private credit lenders are poised to play a vital role in supporting Australia’s growing debt market.

real estate covid-19

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Liquidity Problems Are Closer Than You Think

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Normalise the underlying conditions when “rating” a company’s share price

Interest rates, the best it gets. It’s time to deploy cash

COVID-19 Lockdowns Had High Health, Economic Costs: Swedish Study

Stock Market’s Top Will Outlast Your Disbelief

Democrats “Nervous” Ahead Of Biden’s State Of The Union Address

Alteration Of Gut Microbiota Affects The Severity And Complications Of COVID-19

People Who Received Ivermectin Were Better Off, Study Finds

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges