A new report from the National Academies of Science,

Engineering, and Medicine (NASEM), An Updated Measure of

Poverty: (Re)Drawing the Line, has hit Washington with

something of a splash. Its proposals deserve a warm welcome across the political spectrum. Unfortunately, they are not always getting it from the conservative side of the aisle.

The AEI’s Kevin

Corinth sees the NASEM proposals as a path to adding billions of dollars to federal

spending. Congressional

testimony by economist Bruce Meyer takes NASEM to task for

outright partisan bias. Yet in their more analytical writing, these and other conservative critics offer many of the same criticisms of the obsolete methods that constitute the current approach to measuring poverty. As I will explain below, many of their recommendations for improvements are in harmony with the NASEM report. Examples

include the need for better treatment of healthcare costs, the inclusion of

in-kind benefits in resource measures, and greater use of administrative data

rather than surveys.

After some reading, I have come to think that the disconnect

between the critics’ political negative reaction to the NASEM report and their accurate

analysis of flaws in current poverty measures has less to do with the

conceptual basis of the new proposals and more with the way they should be put

to work. That comes more clearly into focus if we distinguish between what we

might call the tracking and the treatment functions,

or macro and micro functions, of poverty

measurement.

The tracking function has an analytic focus. It is a matter

of assessing how many people are poor at a given time and tracing how their

number varies in response to changes in policies and economic conditions. The

treatment function, in contrast, has an administrative focus. It sets a poverty

threshold that can be used to determine who is eligible for specific government

programs and what their benefits will be.

There are parallels in the tracking and treatment methods

that were developed during the Covid-19 pandemic. By early in 2020, it was

clear to public health officials that something big was happening, but slow and

expensive testing made it hard to track how and where the SARS-CoV-2 virus was

spreading. Later, as tests became faster and more accurate, tracking improved.

Wastewater testing made it possible to track the spread of the virus to whole

communities even before cases began to show up in hospitals. As time went by,

improved testing methods also led to better treatment decisions at the micro

level. For example, faster and more accurate home antigen tests enabled

effective use of treatments like Paxlovid, which works best if taken soon after

symptoms develop.

Poverty measurement, like testing for viruses, also plays

essential roles in both tracking and treatment. For maximum effectiveness, what

we need is a poverty measure that can be used at both the macro and micro

level. The measures now in use are highly flawed in both applications. Both the

NASEM report itself and the works of its critics offer useful ideas about where

we need to go. The following sections will deal first with the tracking

function, then with the treatment function, and then with what needs to be done

to devise a poverty measure suitable for both uses.

The tracking function of poverty measurement

As a tracking tool, the purpose of any poverty measure is to

improve understanding. Each proposed measure represents the answer to a

specific question. To understand poverty fully – what it is, how it has

changed, who is poor, and why – we need to ask lots of questions. At this macro

level, it is misguided to look for the one best measure of poverty.

First some basics. All of the poverty measures discussed

here consist of two elements, a threshold, or measure of needs, and

a measure of resources available to meet those needs. The

threshold is based on a basic bundle of goods and services

considered essential for a minimum acceptable standard of living. The first

step in deriving a threshold is to define the basic bundle and determine its

cost. The basic bundle can be defined in absolute terms or relative to median standards

of living. If absolute, the cost of the basic bundle can be adjusted from year

to year to reflect inflation, and if relative, to reflect changes in the

median. Once the cost of the basic bundle is established, poverty thresholds

themselves may be adjusted to reflect the cost of essentials not explicitly

listed in the basic bundle. Further adjustments in the thresholds may be

developed to reflect household size and regional differences.

Similarly, a poverty measure can include a narrower or

broader definition of resources. A narrow definition might consider only a

household’s regular inflows of cash. A broader definition might include the

cash-equivalent value of in-kind benefits, benefits provided through the tax

system, withdrawals from retirement savings, and other sources of purchasing

power.

Finally, a poverty measure needs to specify the economic

unit to which it applies. In some cases, that may be an individual. In other

cases, it may be a family (a group related by kinship, marriage, adoption, or

other legal ties) or a household (a group of people who live together and share

resources regardless of kinship or legal relationships). Putting it all

together, an individual, family, or household is counted as poor if their

available resources are less than the applicable poverty threshold.

The current official poverty measure (OPM), which dates from

the early 1960s, includes very simple versions of each of these components. It

defines the basic bundle in absolute terms as three times the cost of a

“thrifty food plan” determined by the U.S. Department of Agriculture. It then

converts that to a set of thresholds for family units that vary by family size,

with special adjustments for higher cost of living in Alaska and Hawaii. The

OPM defines resources as before-tax regular cash income, including wages,

salaries, interest, and retirement income; cash benefits such as Temporary

Assistance for Needy Families and Supplemental Security Income; and a few other

items. Importantly, the OPM does not include tax credits or the cash-equivalent

value of in-kind benefits in its resource measure.

The parameters of the OPM were initially calibrated to

produce a poverty rate for 1963 of approximately 20 percent. After that, annual

inflation adjustments used the CPI-U, which to this day remains the most widely

publicized price index. As nominal incomes rose due to economic growth and

inflation, and as cash benefits increased, the share of the population living

below the threshold fell. By the early 1970s, it had reached 12 percent. Since

then, however, despite some cyclical ups and downs, it has changed little.

Today, nearly everyone views the OPM as functionally

obsolete. Some see it as overstating the poverty rate, in that its measure of

resources ignores in-kind benefits like the Supplemental Nutrition Assistance

Program (SNAP) and tax credits like the Earned Income Tax Credit (EITC). Others

see it as understating poverty on the grounds that three times the cost of food

is no longer enough to meet minimal needs for shelter, healthcare, childcare,

transportation, and modern communication services. Almost no one sees the OPM

as just right.

In a recent paper in the Journal of

Political Economy, Richard V. Burkhauser, Kevin Corinth, James

Elwell, and Jeff Larrimore provide an excellent overview of the overstatement

perspective. The question they ask is what percentage of American households

today lack the resources they need to reach the original three-times-food

threshold. Simply put, was Lyndon Johnson’s “War on Poverty,” on its own terms,

a success or failure?

To answer that question, they develop what they call

an absolute full-income poverty measure (FPM). Their first

step in creating the FPM was to include more expense categories in the basic

bundle, but calibrate it to make the FPM poverty rate for 1963 equal to the OPM

rate for that year. Next, they expanded the resource measure to reflect the

growth of in-kind transfer programs and the effects of taxes and tax credits.

They also adopt the household, rather than the family, as their basic unit of

analysis. Burkhauser et al. estimate that adding the full value of the EITC and

other tax credits to resources, along with all in-kind transfer programs, cuts

the poverty rate in 2019 to just 4 percent, far below the official 10.6

percent.

Going further, Burkhauser et al. raise the issue of the

appropriate measure of the price level to be used in adjusting poverty

thresholds over time. They note that many economists consider that the

CPI-U overstates

the rate of inflation, at least for the economy as a whole. Instead,

they prefer the personal consumption expenditure (PCE) index, which the Fed

uses as a guide to monetary policy. Replacing the CPI-U with the PCE reduces

the FPM poverty rate for 2019 to just 1.6 percent. It is worth noting, however,

that some observers maintain that prices in the basket of goods purchased by

poor households tend to rise at a faster rate than the average for all

households. In that case, an FPM adjusted for inflation using the PCE would not

fully satisfy one of the criteria set by Burkhauser et al., namely, that “the

poverty measure should reflect the share of people who lack a minimum level of

absolute resources.” (For further discussion of this point, see, e.g., this

report to the Office of Management and Budget.)

Burkhauser et al. do not represent 1.6 percent as the “true”

poverty rate. As they put it, although the FPM does point to “the near

elimination of poverty based on standards from more than half a century ago,”

they see that as “an important but insufficient indication of progress.” For a

fuller understanding, measuring success or failure of Johnson’s War on Poverty

is not enough. A poverty measure for today should give a better picture of the

basic needs of today’s households and the resources available to them.

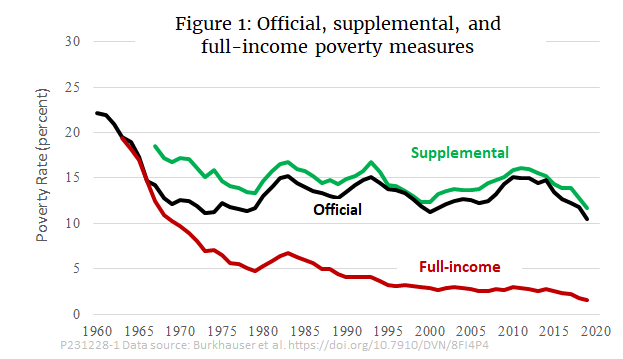

The Supplemental

Poverty Measure (SPM), which the Census Bureau has published since

2011, is the best known attempt to modernize the official measure. The SPM

enlarges the OPM’s basic bundle of essential goods to include not only food,

but also shelter, utilities, telephone, and internet. It takes a relative

approach, setting the threshold as a percentage of median expenditures and

updating it not just for inflation, but also for the growth in real median

household income. On the resource side, the SPM adds many cash and in-kind benefits,

although not as many as the FPM. It further adjusts measured resources by

deducting some necessary expenses, such as childcare and out-of-pocket

healthcare costs. Finally, the SPM moves away from the family as its unit of

analysis toward a household concept.

Since the SPM adds items to both thresholds and resources,

it could, depending on its exact calibration, have a value either higher or

lower than the OPM. In practice, as shown in Figure 1, it has tracked a little

higher than the OPM. (For comparison, Burkhauser et al. calculate a variant of

their FPM that uses a relative rather than an absolute poverty threshold. The

relative FPM, not shown in Figure 1, tracks slightly higher than the SPM in

most years.)

That brings us back to our starting point, the NASEM report.

Its centerpiece is a recommended revision of the SPM that it calls the

principal poverty measure (PPM). The PPM directly addresses several

acknowledged shortcomings of the SPM. Some of the most important

recommendations include:

- A

further movement toward the household as the unit of analysis. To

accomplish that, the PPM would place more emphasis on groups of people who

live together and less on biological and legal relationships.

- A

change in the treatment of healthcare costs. The SPM treats out-of-pocket

healthcare spending as a deduction from resources but does not treat

healthcare as a basic need. The PPM adds the cost of basic health

insurance to its basic package of needs, adds the value of subsidized

insurance (e.g., Medicaid or employer-provided) to its list of resources,

and (like the SPM) deducts any remaining out-of-pocket healthcare spending

from total resources.

- A

change in the treatment of the costs of shelter that does a better job of

distinguishing between the situation faced by renters and homeowners.

- Inclusion

of childcare as a basic need and subsidies to childcare as a resource.

Although Burkhauser et al. do not directly address the PPM,

judging by their criticisms of the SPM, it seems likely that they would regard

nearly all of these changes as improvements. Many of the changes

recommended in the NASEM report make the PPM more similar to the FPM than is

the SPM.

Since the NASEM report makes recommendations regarding

methodology for the PPM but does not calculate values, the PPM is not shown in

Figure 1. In principle, because it modifies the way that both needs and

resources are handled, the PPM could, depending on its exact calibration,

produce poverty rates either above or below the SPM.

Measurement for treatment

The OPM, FPM, SPM, and PPM are just a few of the many

poverty measures that economists have proposed over the years. When we confine

our attention to tracking poverty, each of them adds to our understanding. When

we turn to treatment, however, things become more difficult. A big part of the

reason is that none of the above measures is really suitable for making

micro-level decisions regarding the eligibility of particular households for

specific programs.

For the OPM, that principle is laid out explicitly in U.S.

Office of Management and Budget Statistical Policy Directive No. 14,

first issued in 1969 and revised in 1978:

The poverty levels used by the Bureau of the Census were

developed as rough statistical measures to record changes in the number of

persons and families in poverty and their characteristics, over time. While

they have relevance to a concept of poverty, these levels were not developed

for administrative use in any specific program and nothing in this Directive

should be construed as requiring that they should be applied for such a

purpose.

Despite the directive, federal and state agencies do use the

OPM, or measures derived from it, to determine eligibility for many programs,

including Medicaid, SNAP, the Women, Infants, and Children nutrition program,

Affordable Care Act premium subsidies, Medicare Part D low-income subsidies,

Head Start, and the National School Lunch Program. The exact eligibility

thresholds and the rules for calculating resources vary from program to

program. The threshold at which eligibility ends or phase-out begins for a

given household may be equal to the Census Bureau’s official poverty threshold,

a fraction of that threshold, or a multiple of it. The resource measure may be

regular cash income as defined by the OPM, or a modification based on various

deductions and add-backs. Some programs include asset tests as well as income

tests in their measures of resources. The exact rules for computing thresholds

and resources vary not only from one program to another, but from state to

state.

That brings us to what is, perhaps, the greatest source of

alarm among conservative critics of the NASEM proposals. That is the concern

that a new poverty measure such as the PPM would be used in a way that raised

qualification thresholds while resource measures remained unchanged. It is easy

to understand how doing so by administrative action could be seen as a backdoor

way of greatly increasing welfare spending without proper legislative

scrutiny.

Kevin Corinth articulates this fear in a recent

working paper for the American Enterprise Institute. He notes that

while the resource measures that agencies should use in screening applications

are usually enshrined in statute, the poverty thresholds are not. If the Office

of Management and Budget were to put its official stamp of approval on a new

poverty measure such as the SPM or PPM, Corinth maintains that agencies would

fall in line and recalculate their thresholds based on the new measure without

making any change in the way they measure resources.

Corinth calculates that if the current OPM-based thresholds

were replaced by new thresholds derived from the SPM, federal spending for SNAP

and Medicaid alone would increase by $124 billion by 2033. No similar

calculation can be made for the PPM, since it has not been finalized, but

Corinth presumes that it, too, would greatly increase spending if it were used

to recalculate thresholds while standards for resources remained unchanged.

Clearly, Corinth is onto a real problem. The whole

conceptual basis of the SPM and PPM is to add relevant items in a balanced

manner to both sides of the poverty equation, so that they more accurately

reflect the balance between the cost of basic needs and the resources available

to meet them. Changing one side of the equation while leaving the other

untouched makes little sense.

Logically, then, what we need is an approach to poverty

measurement that is both conceptually balanced and operationally suitable for

use at both the macro and micro levels. Corinth himself acknowledges that at

one point, when he notes that “changes could be made to both the SPM resource

measure and SPM thresholds.” However, he does not follow up with specific

recommendations for doing so. To fill the gap, I offer some ideas of my own in

the next section.

Toward a balanced approach to micro-level poverty

measurement

To transform the PPM from a tracking tool into one suitable

for determining individual households’ eligibility for specific public

assistance programs would require several steps.

1. Finalize a package of basic needs. For

the PPM, those would include food, clothing, telephone, internet, housing needs

based on fair market rents, basic health insurance, and childcare. The NASEM

report recommends calibrating costs based on a percentage of median

expenditures, but conceptually, they could instead be set in absolute terms,

either based on costs in a given year or averaged over a fixed period leading

up to the date of implementation of the new approach.

2. Convert the package of needs into thresholds. Thresholds

would vary according to the size and composition of the household unit. They

could also vary geographically, although there is room for debate on how fine

the calibration should be. Thresholds would be updated to reflect changes in

the cost of living as measured by changes in median expenditures or (in the

absolute version) changes in price levels.

3. Finalize a list of resources. These

would include cash income plus noncash benefits that households can use to meet

food, clothing, and telecommunication needs; plus childcare subsidies, health

insurance benefits and subsidies, rent subsidies, and (for homeowners) imputed

rental income; minus tax payments net of refundable tax credits; minus work

expenses, nonpremium out-of-pocket medical expenses, homeowner costs if

applicable, and child support paid to another household.

4. Centralize collection of data on resources. Determining

eligibility of individual households for specific programs would require

assembling data from many sources. It would be highly beneficial to centralize

the reporting of total resources as much as possible, so that all resource data

would be available from a central PPM database. The IRS could provide data on

cash income other than public benefits (wages, salaries, interest, dividends,

etc.) and payments made to households through refundable tax credits such as

the EITC. The federal or state agencies that administer SNAP, Medicaid and

other programs could provide household-by-household data directly to the PPM

database. Employers could report the cash-equivalent value of employer-provided

health benefits along with earnings and taxable benefits.

5. Devise a uniform format for reporting eligible

deductions from resources. Individual households applying for

benefits from specific programs would be responsible for reporting applicable

deductions from resources, such as work expenses, out-of-pocket medical

expenses, homeowner costs and so on. A uniform format should be developed for

reporting those deductions along with uniform standards for documenting them so

that the information could be submitted to multiple benefit programs without

undue administrative burden.

6. Use net total resources as the basis for all

program eligibility. Decisions on eligibility for individual

programs should use net total resources, as determined by steps (4) and (5), to

determine eligibility for individual programs.

7. Harmonization of program phase-outs. It

would be possible to implement steps (1) through (6) without making major

changes to the phase-in and phaseout rules for individual programs. However,

once a household-by-household measure of net total resources became available,

it would be highly desirable to use it to compute benefit phaseouts from all

programs in a harmonized fashion. At present, for example, a household just

above the poverty line might face a phaseout rate of 24 percent for SNAP and 21

percent for EITC, giving it an effective marginal tax rate of 45 percent, not

counting other programs or income and payroll taxes. As explained in this

previous commentary, such high effective marginal tax rates impose

severe work disincentives, especially on families that are just making the

transition from poverty to self-sufficiency. Replacing the phase-outs for

individual programs with a single harmonized “tax” on total resources as

computed by the PPM formula could significantly mitigate work

disincentives.

Implementing all of these steps would clearly be a major

administrative and legislative undertaking. However, the result would be a

public assistance system that was ultimately simpler, less prone to error, and

less administratively burdensome both for government agencies at all levels and

for poor households.

Conclusion

In a recent

commentary for the Foundation for Research on Equal Opportunity,

Michael Tanner points to the potentially far-reaching significance of proposed

revisions to the way poverty is measured. “Congress should use this opportunity

to debate even bigger questions,” he writes, such as “what is poverty, and how

should policymakers measure it?” Ultimately, he continues, “attempts to develop

a statistical measure of poverty venture beyond science, reflecting value

judgments and biases. Such measures cannot explain everything about how the

poor really live, how easily they can improve their situation, or how

policymakers can best help them.”

The “beyond science” caveat is worth keeping in mind for all

discussions of poverty measurement. A case in point is the issue of whether to

use an absolute or relative approach in defining needs. It is not that one is

right and the other wrong. Rather, they reflect fundamentally different

philosophies as to what poverty is. For example, as noted earlier, Burkhauser

et al. compute both absolute and relative versions of their full-income poverty

measure. The absolute version is the right one for answering the historical

question they pose about the success or failure of the original War on Poverty,

but for purposes of policy today, the choice is not so clear. Some might see an

absolute measure, when used in a micro context, as producing too many false

negatives, that is, failures to help those truly in need. Others might see the

relative approach as producing too many false positives, spending hard-earned

taxpayer funds on people who could get by on their own if they made the effort.

The choice is more a matter of values than of science.

The choice of a price index for adjusting poverty measures

over time also involves values as well as science. Should the index be one

based on average consumption patterns for all households, such as the PCE or

chained CPI-U, or should it be a special index based on the consumption

patterns of low-income households? Should the index be descriptive, that is,

based on observed consumption patterns for the group in question? Or should it

be prescriptive, that is, based on a subjective estimate of “basics needed to

live and work in the modern economy” as is the approach taken by the ALICE Essentials

Index?

In closing, I would like to call attention to four

additional reasons why conservative critics of existing poverty policy should

welcome the proposed PPM, even in its unfinished state, as a major step in the

right direction.

The PPM is inherently less prone to error. Bruce Meyer is

concerned that “the NAS[EM]-proposed changes to poverty measurement would

produce a measure of poverty that does a worse job identifying the most

disadvantaged, calling poor those who are better off and not including others

suffering more deprivation.” In fact, many features of the PPM make it

inherently less prone than either the OPM or the SPM to both false positives

and false negatives. The most obvious is its move toward a full-income

definition of resources. That avoids one of the most glaring flaws in the OPM,

namely, the identification of families as poor who in fact receive sufficient

resources in the form of in-kind transfers or tax credits. The PPM also

addresses some of the flaws of the SPM that Meyer singles out in his testimony,

most notably in the treatment of healthcare. Furthermore, by placing

greater emphasis on administrative data sources and less on surveys, the PPM

would mitigate underreporting of income and benefits, which Burkhauser et al.

identify as a key weakness of the SPM. (See NASEM Recommendations 6.2 and 6.3).

The PPM offers a pathway toward consistency and

standardization in poverty policy. In his critique of the

PPM, Tanner suggests that “Congress should decouple program eligibility from

any single poverty measure, and adopt a broader definition of poverty that

examines the totality of the circumstances that low-income people face and their

potential to rise above them.” I see that kind of decoupling as exactly the

wrong approach. Our existing welfare system is already a clumsy accretion

of mutually inconsistent means-tested programs – as many as 80 of them, by

one count. It is massively wasteful and daunting to navigate. In large

part that is precisely because each component represents a different view of

the “totality of circumstances” of the poor as seen by different policymakers

at different times. What we need is not decoupling, but standardization and

consistency. The proposed system-wide redefinition of poverty offers a perfect

opportunity to make real progress in that direction.

The PPM would be more family-friendly. One

pro-family feature of the PPM is its recognition of childcare costs on both the

needs and the resources sides of the poverty equation. In addition, by moving

toward households (defined by resource-sharing) rather than families (defined

by legal relationships), the PPM would mitigate the marriage

penalties that are built into some of today’s OPM-based poverty

programs.

Properly implemented, the PPM would be more

work-friendly. As noted above, the benefit cliffs,

disincentive deserts, and high effective marginal tax rates of existing

OPM-based poverty programs create formidable work disincentives. Moving toward

a harmonized phaseout system based on the PPM’s full-income approach to

resources could greatly reduce work disincentives, especially for households

just above the poverty line that are struggling to take the last steps toward

self-sufficiency.

In short, it is wrong to view the proposed PPM as part of a

progressive plot to raid the government budget for the benefit of the

undeserving, as some conservative critics seem to have done. Rather, both

conservatives and progressives should embrace the PPM as a promising step

forward and direct their efforts toward making sure it is properly

implemented.

Based on a version originally published by Niskanen Center.

subsidies

economic growth

pandemic

covid-19

monetary policy

fed

irs

congress

treatment

testing

spread

Read More

{kind=link}