Uncategorized

Middle Class Can’t Afford Homes In Nearly Half Of Top 100 US Metros, Study Finds

Middle Class Can’t Afford Homes In Nearly Half Of Top 100 US Metros, Study Finds

By Sam Bourgi of CreditNews,

Housing is becoming an exclusively…

Share this:

By Sam Bourgi of CreditNews,

Housing is becoming an exclusively upper-class privilege in a growing number of cities.

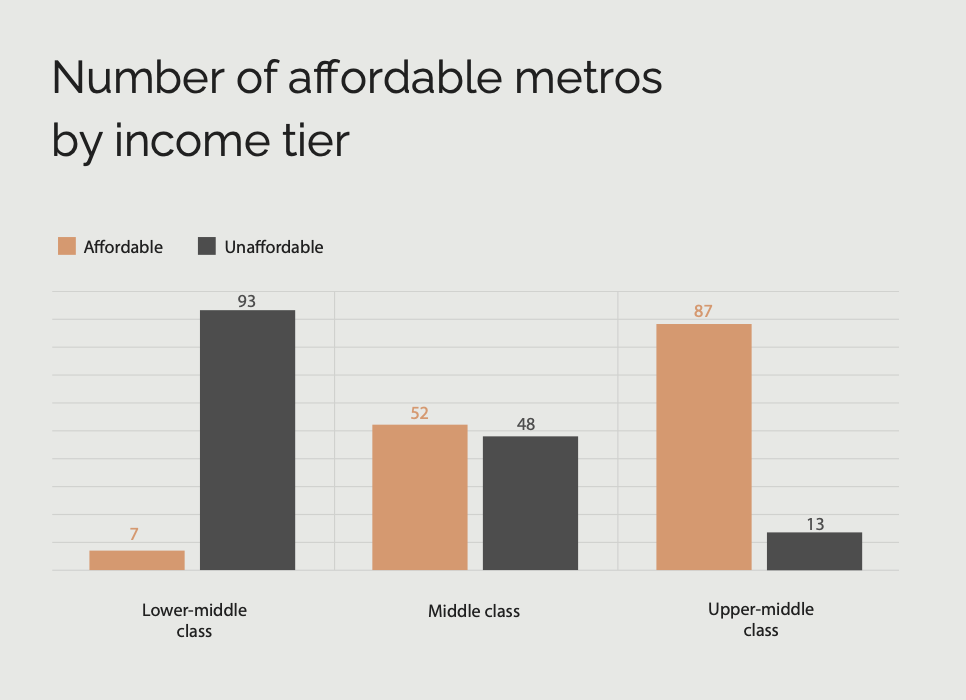

According to a new study by Creditnews Research, in 2024, middle-class households could afford to buy an average home in just 52 of the country’s 100 largest metros.

Just five years earlier, they could afford a home in 91 of the top 100 metros.

The situation is far worse for lower middle-class households, as they can only afford a home in seven of the largest 100 metros.

In total, 41 out of the 100 metros require a gross annual income of $100,000 or more to qualify for an average home. In 13 metros, an average income of more than $155,000 is needed.

In those cities, even the upper-middle class doesn’t qualify for an average home.

The study determined affordability by looking at how much income households need to earn to afford a down payment, mortgage payment, and related fees for an average home.

A home is considered affordable if monthly housing and mortgage costs don’t exceed 28% of a household’s gross income.

“There’s no two ways about it: Housing affordability has worsened significantly since Covid,” the report said. Since the pandemic, 39 of the most populous metros have fallen below the affordability threshold.

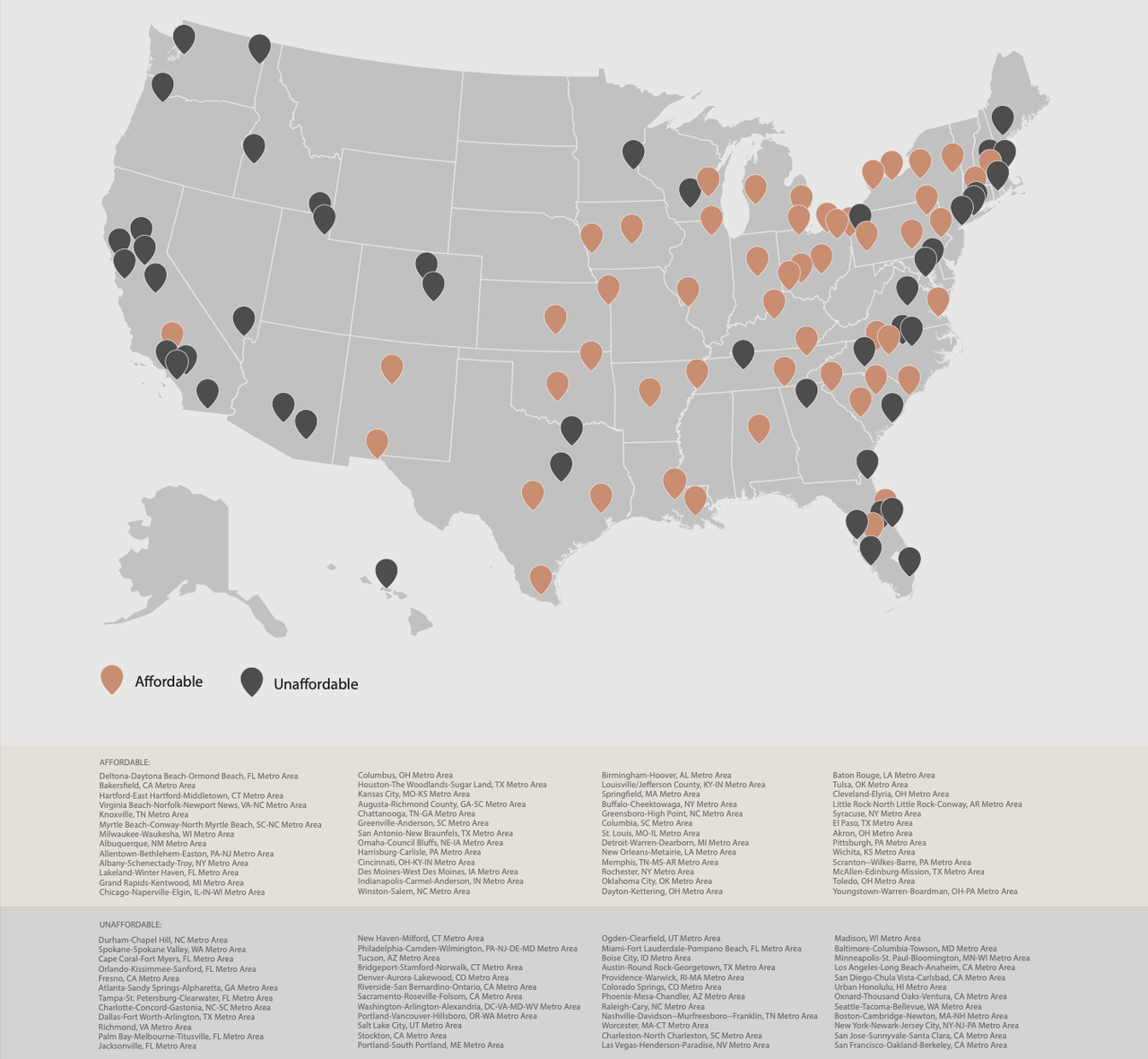

As expected, the most affordable areas for the middle class are located in the Midwest, Rust Belt, and parts of Texas, while the West Coast, Tri-State Area, and Hawaii are largely out of reach.

Affording a home is no longer a guarantee for the middle class

Being considered “middle class” doesn’t carry the same significance as it did just a few years ago.

“In the past, if you were middle class, it was almost assumed you would become a homeowner,” said Ali Wolf, chief economist of Zonda, a housing market research firm.

“Today, the aspiration is still there, but it is a lot more difficult. You have to be wealthy or lucky.”

That's all thanks to a “perfect storm” of elevated mortgage rates, sky-high home prices, and a lack of inventory, making housing more unaffordable.

The result is that middle-income buyers, or those with an annual income of up to $75,000, could only afford about one-quarter of listings on the market last year.

According to Nadia Evangelou, the director of real estate research at the National Association of Realtors, “Middle-income buyers face the largest shortage of homes among all income groups, making it even harder for them to build wealth through homeownership.”

Mortgage rates creep closer to 7%

After falling between November and January, mortgage rates are creeping back up.

According to Freddie Mac, 30-year fixed-rate mortgages reached 6.88% in the week of April 11 and at some point climbed well above 7%.

“As mortgage rates increase, it’s never good news for the housing market, especially when more sellers are in the mix,” said HousingWire lead analyst Logan Mohtashami.

“We saw a bounce in demand early in the year as rates fell. However, just like last year, when mortgage rates headed higher, it limits sales growth.”

The reversal seems to be driven by a surprise spike in inflation, which has come out higher than expected for four consecutive months

“For homebuyers, the latest CPI report means mortgage rates will stay higher for longer because it makes the Fed unlikely to cut interest rates in the next few months,” said Chen Zaho, Redfin’s economic research lead.

“Housing costs are likely to continue going up for the near future, but persistently high mortgage rates and rising supply could cool home-price growth by the end of the year, taking some pressure off costs.”

Uncategorized

NIH Refuses To Release Details Of COVID-19 Vaccine Royalty Agreement

NIH Refuses To Release Details Of COVID-19 Vaccine Royalty Agreement

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. National Institutes of Health (NIH) is refusing to release additional information about an agreement it reached over a COVID-19 vaccine that has earned it at least $400 million.

The NIH declined to provide any materials in response to a Freedom of Information Act request from The Epoch Times.

“The NIH withholds the entirety of the records as they are protected from release,” Gorka Garcia-Malene, an NIH officer, told The Epoch Times in a letter.

She cited an exemption outlined in the act that allows government agencies to partially or fully withhold information.

“In this case, exemption 3 incorporates 35 U.S.C. 209 (f), which reads in relevant part, ‘No Federal agency shall grant any license under a patent or patent application on a federally owned invention unless the person requesting the license has supplied the agency with a plan for development or marketing of the invention, except that any such plan shall be treated by the Federal agency as commercial and financial information obtained from a person and privileged and confidential and not subject to disclosure under section 552 of title 5,’” Ms. Garcia-Malene wrote.

“Exemption 4 protects from disclosure trade secrets and commercial or financial information that is privileged and confidential,” she added.

In February 2023, Moderna announced that it had paid $400 million to the NIH and would make additional payments in the future as part of a licensing agreement for spike proteins used in the company’s COVID-19 vaccine. The Epoch Times obtained a copy of the contract, which confirmed the payment but redacted details of the future payments.

The Epoch Times then lodged a new request, seeking more details about the future payments, which are said to be based on how many COVID-19 vaccines are sold.

Ms. Garcia-Malene was responding to the new request.

James Love, director of the nonprofit Knowledge Ecology International, said the information should be made public.

“The NIH put out several press statements about the royalty dispute with Moderna, and they should not now claim it is some secret confidential information. And when hundreds of millions of dollars are at stake, the public interest in transparency is large too,” Mr. Love told The Epoch Times in an email.

“There are a lot of NIH officials who resent transparency,” he added.

Inquiries to NIH spokespersons received away messages. Another request for comment, sent to one of the addresses provided in the away messages, was not returned.

The Epoch Times plans to appeal the NIH’s decision.

The NIH is one of several government agencies that receive royalty payments. Officials there have fought against attempts to acquire information on these payments, but in 2023, they disclosed some $325 million in royalties received between 2009 and 2020 after being sued.

Some experts say the payments, made to the agency and many of its top scientists, should be stopped.

“Neither the government nor any government employee should have any financial interest in a product for which the government has any involvement in licensing or promoting,“ Aaron Siri, managing partner of Siri & Glimstad LLP, told The Epoch Times in an email. ”It creates a dangerous conflict of interest.”

Move on BioNTech

The NIH is trying to obtain more money from COVID-19 vaccine manufacturers, according to recent filings.

BioNTech, Pfizer’s partner, said in the forms that the NIH served it with a notice of default because the NIH’s position is that BioNTech owes it money from COVID-19 vaccine sales.

BioNTech said it does not think it owes the NIH money but that “the ultimate outcome of these matters is uncertain and we cannot guarantee that our interpretation of these license agreements will prevail, or that we will not ultimately need to pay some or all of the royalty and other related amounts in dispute.”

The NIH did not return inquiries on the BioNTech filings.

The NIH has said previously it licensed its spike protein technology to BioNTech for the Pfizer-BioNTech COVID-19 vaccine.

The Epoch Times has submitted a Freedom of Information Act request for the notice of default and related documents. Another request seeks information on whether the NIH has threatened or served Pfizer with a similar notice.

However much money the U.S. government receives in royalties will be much less than it has paid for the vaccines. The government has purchased hundreds of millions of shots, spending north of $30 billion.

Uncategorized

Bitcoin’s resilience tested: Price up 577% amid pandemics, war and corporate embrace

Quick Take As we approach the Bitcoin halving and bid farewell to the current epoch, it is crucial to reflect on the events that have transpired since…

Share this:

Quick Take

As we approach the Bitcoin halving and bid farewell to the current epoch, it is crucial to reflect on the events that have transpired since the previous halving in May 2020. The world has witnessed a series of significant events that have shaped the economic landscape and influenced the adoption of Bitcoin.

The COVID-19 pandemic, which began in March 2020, had a detrimental effect on the global economy throughout the entire cycle. The aftermath of the pandemic has led to severe inflation and currency debasement, the effects of which are still felt today.

In August 2020, Michael Saylor, then CEO of MicroStrategy, made a bold move by adopting Bitcoin, resulting in the company accumulating more than 1% of the total Bitcoin supply as of April 2024. The FASB introduced rules that will positively influence corporate adoption by establishing fair value accounting for Bitcoin in corporate treasuries.

El Salvador made history by making Bitcoin legal tender and implementing a dollar-cost averaging (DCA) approach to acquiring the digital asset.

China’s ban on Bitcoin in the summer of 2021 caused a significant drop in the hash rate, which plummeted by approximately 50%.

Geopolitical tensions escalated, with multiple wars and invasions occurring, most notably Russia’s invasion of Ukraine in February 2022 and the recent conflict in the Middle East.

The introduction of Bitcoin ordinals paved the way for the launch of Runes at block 840,000.

This cycle also marked the first time that the balance of Bitcoin on exchanges decreased, indicating a shift in investor behavior.

In this cycle, the digital asset exchange FTX collapsed alongside several crypto lending platforms like Celsius and BlockFi.

In January 2024, the launch of Bitcoin ETFs became an instant success, further solidifying Bitcoin’s position in the financial world.

Other notable events included the highest inflation and interest rates in recent history, reminding us that while the future remains unpredictable, the limited supply of 21 million Bitcoin remains a constant.

Despite the challenges and events that have unfolded, Bitcoin has surged an impressive 577% since the last halving.

The post Bitcoin’s resilience tested: Price up 577% amid pandemics, war and corporate embrace appeared first on CryptoSlate.

bitcoin crypto pandemic covid-19 cryptoUncategorized

The bifurcation of the new vs. existing home markets continues

– by New Deal democratThe bifurcation of the new vs. existing home markets continued in March, per the report on existing home sales and prices yesterday….

Share this:

{kind=link}

{kind=link}

- by New Deal democrat

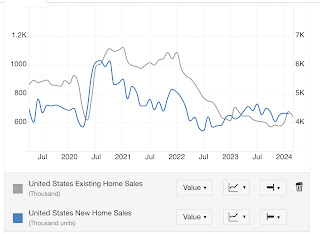

The bifurcation of the new vs. existing home markets continued in March, per the report on existing home sales and prices yesterday. Remember that, unlike existing homeowners, house builders can vary square footage, amenities, lot sizes, and offer price and/or mortgage incentives to counteract the effect of interest rate hikes.

On a seasonally adjusted basis, existing home sales declined from 438,000 to 419,000 in March. But this is well within the seasonally adjusted range of the past 16 months (gray, right scale in the graph below){also, note I am using Trading Economics graphs due to restrictions put on FRED by the Realtors; also note difference in scales):

{kind=link}

NIH Refuses To Release Details Of COVID-19 Vaccine Royalty Agreement

Bitcoin’s resilience tested: Price up 577% amid pandemics, war and corporate embrace

Economic Warning From The NFIB

The bifurcation of the new vs. existing home markets continues

Bankrupt nationwide retailer closes several more stores

“We’re not shoving anything down anyone’s throat,” Ford exec says about EVs

Huge Bond Wagers Make Some Hedge Funds Too-Big-To-Fail, IMF Warns

Realtor.com Reports Active Inventory UP 29.1% YoY; New Listings Up 7.2% YoY

Middle Class Can’t Afford Homes In Nearly Half Of Top 100 US Metros, Study Finds

-

International4 weeks ago

International4 weeks agoParexel CEO to retire; CAR-T maker AffyImmune promotes business leader to chief executive

-

Spread & Containment2 weeks ago

Spread & Containment2 weeks agoClimate-Con & The Media-Censorship Complex – Part 1

-

International6 days ago

International6 days agoWHO Official Admits Vaccine Passports May Have Been A Scam

-

Spread & Containment2 weeks ago

Spread & Containment2 weeks agoFDA Finally Takes Down Ivermectin Posts After Settlement

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoVaccinated People Show Long COVID-Like Symptoms With Detectable Spike Proteins: Preprint Study

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoCan language models read the genome? This one decoded mRNA to make better vaccines.

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoWhat’s So Great About The Great Reset, Great Taking, Great Replacement, Great Deflation, & Next Great Depression?

-

Uncategorized3 days ago

Uncategorized3 days agoRed States Fight Growing Efforts To Give “Basic Income” Cash To Residents