Uncategorized

Red States Fight Growing Efforts To Give “Basic Income” Cash To Residents

Red States Fight Growing Efforts To Give "Basic Income" Cash To Residents

By Kevin Hardy of Stateline

South Dakota state Sen. John Wiik likes…

Share this:

By Kevin Hardy of Stateline

South Dakota state Sen. John Wiik likes to think of himself as a lookout of sorts — keeping an eye on new laws, programs and ideas brewing across the states.

“I don’t bring a ton of legislation,” said Wiik, a Republican. “The main thing I like to do is try and stay ahead of trends and try and prevent bad things from coming into our state.”

This session, that meant sponsoring successful legislation banning cities or counties from creating basic income programs, which provide direct, regular cash payments to low-income residents to help alleviate poverty.

While Wiik isn’t aware of any local governments publicly floating the idea in South Dakota, he describes such programs as “bureaucrats trying to hand out checks to make sure that your party registration matches whoever signed the checks for the rest of your life.”

The economic gut punch of the pandemic and related assistance efforts such as the expanded child tax credit popularized the idea of directly handing cash to people in need. Advocates say the programs can be administered more efficiently than traditional government assistance programs, and research suggests they increase not only financial stability but also mental and physical health.

Still, Wiik and other Republicans argue handing out no-strings-attached cash disincentivizes work — and having fewer workers available is especially worrisome in a state with the nation’s second-lowest unemployment rate.

South Dakota is among at least six states where GOP officials have looked to ban basic income programs.

The basic income concept has been around for decades, but a 2019 experiment in Stockton, California, set off a major expansion. There, 125 individuals received $500 per month with no strings attached for two years. Independent researchers found the program improved financial stability and health, but concluded that the pandemic dampened those effects.

GOP lawmakers like Wiik fear that even experimental programs could set a dangerous precedent.

“What did Ronald Reagan say, ‘The closest thing to eternal life on this planet is a government program’?” Wiik said. “So, if you get people addicted to just getting a check from the government, it’s going to be really hard to take that away.”

The debate over basic income programs is likely to intensify as blue state lawmakers seek to expand pilot programs. Minnesota, for example, could become the nation’s first to fund a statewide program. But elected officials in red states are working to thwart such efforts — not only by fighting statewide efforts but also by preventing local communities from starting their own basic income programs.

Democratic governors in Arizona and Wisconsin recently vetoed Republican legislation banning basic income programs.

Last week, Texas Attorney General Ken Paxton sued Harris County to block a pilot program that would provide $500 per month to 1,900 low-income people in the state’s largest county, home to Houston.

Paxton, a Republican, argued the program is illegal because it violates a state constitutional provision that says local governments cannot grant public money to individuals.

Harris County Attorney Christian Menefee, a Democrat, called Paxton’s move “nothing more than an attack on local government and an attempt to make headlines.”

Meanwhile, several blue states are pushing to expand these programs.

Washington state lawmakers debated a statewide basic income bill during this year’s short session. And Minnesota lawmakers are debating whether to spend $100 million to roll out one of the nation’s first statewide pilot programs.

“We’re definitely seeing that shift from pilot to policy,” said Sukhi Samra, the director of Mayors for a Guaranteed Income, which formed after the Stockton experiment.

So far, that organization has helped launch about 60 pilot programs across the country that will provide $250 million in unconditional aid, she said.

Despite pushback in some states, Samra said recent polling commissioned by the group shows broad support of basic income programs. And the programs have shown success in supplementing — not replacing — social safety net programs, she said.

The extra cash gives recipients freedom of choice. People can fix a flat tire, cover school supplies or celebrate a child’s birthday for the first time.

“There’s no social safety net program that allows you to do that.” she said. “ … This is an effective policy that helps our families, and this can radically change the way that we address poverty in this country.”

Basic Income Experiments

The proliferation of basic income projects has been closely studied by researchers.

Though many feared that free cash would dissuade people from working, that hasn’t been the case, said Sara Kimberlin, the executive director and senior research scholar at Stanford University’s Center on Poverty and Inequality.

Stanford’s Basic Income Lab has tracked more than 150 basic income pilots across the country. Generally, those offer $500 or $1,000 per month over a short period.

“There isn’t anywhere in the United States where you can live off of $500 a month,” she said. “At the same time, $500 a month really makes a tremendous difference for someone who is living really close to the edge.”

Kimberlin said the research on basic income programs has so far been promising, though it’s unclear how long the benefits may persist once programs conclude. Still, she said, plenty of research shows how critical economic stability in childhood is to stability in adulthood — something both the basic income programs and the pandemic-era child tax credit can address.

Over the past five years, basic income experiments have varied across the country.

Last year, California launched the nation’s first state-funded pilot programs targeting former foster youth.

In Colorado, the Denver Basic Income Project aimed to help homeless individuals. After early successes, the Denver City Council awarded funding late last year to extend that program, which provides up to $1,000 per month to hundreds of participants.

A 2021 pilot launched in Cambridge, Massachusetts, provided $500 a month over 18 months to 130 single caregivers. Research from the University of Pennsylvania found the Cambridge program increased employment, the ability to cover a $400 emergency expense, and food and housing security among participants.

Children in participating families were more likely to enroll in Advanced Placement courses, earned higher grades and had reduced absenteeism.

“It was really reaffirming to hear that when families are not stressed out, they are able to actually do much better,” said Geeta Pradhan, president of the Cambridge Community Foundation, which worked on the project.

Pradhan said basic income programs are part of a national trend in “trust-based philanthropy,” which empowers individuals rather than imposing top-down solutions to fight poverty.

“There is something that I think it does to people’s sense of empowerment, a sense of agency, the freedom that you feel,” she said. “I think that there’s some very important aspects of humanity that are built into these programs.”

While the pilot concluded, the Cambridge City Council committed $22 million in federal pandemic aid toward a second round of funding. Now, nearly 2,000 families earning at or below 250% of the federal poverty level are receiving $500 monthly payments, said Sumbul Siddiqui, a city council member.

Siddiqui, a Democrat, pushed for the original pilot when she was mayor during the pandemic. While she said the program has proven successful, it’s unclear whether the city can find a sustainable source of funding to keep it going long term.

States look to expand pilots

Tomas Vargas Jr. was among the 125 people who benefited from the Stockton, California, basic income program that launched in 2019.

At the time, he heard plenty of criticism from people who said beneficiaries would blow their funds on drugs and alcohol or quit their jobs.

“Off of $500 a month, which amazed me,” said Vargas, who worked part time at UPS.

But he said the cash gave him breathing room. He had felt stuck at his job, but the extra money gave him the freedom to take time off to interview for better jobs.

Unlike other social service programs like food stamps, he didn’t have to worry about losing out if his income went up incrementally. The cash allowed him to be a better father, he said, as well as improved his confidence and mental health.

The experience prompted him to get into the nonprofit sector. Financially stable, he now works at Mayors for a Guaranteed Income.

“The person I was five years ago is not the person that I am now,” he said.

Washington state Sen. Claire Wilson, a Democrat, said basic income is a proactive way to disrupt the status quo maintained by other anti-poverty efforts.

“I have a belief that our systems in our country have never been put in place to get people out of them,” she said. “They kept people right where they are.”

Wilson chairs the Human Services Committee, which considered a basic income bill this session that would have created a pilot program to offer 7,500 people a monthly amount equivalent to the fair market rent for a two-bedroom apartment in their area.

The basic income bill didn’t progress during Washington’s short legislative session this year, but Wilson said lawmakers would reconsider the idea next year. While she champions the concept, she said there’s a lot of work to be done convincing skeptics.

In Minnesota, where lawmakers are considering a $100 million statewide basic income pilot program, some Republicans balked at the concept of free cash and its cost to taxpayers.

“Just the cost alone should be a concern,” Republican state Rep. Jon Koznick said during a committee meeting this month.

State Rep. Athena Hollins, a Democrat who sponsored the legislation, acknowledged the hefty request, but said backers would support a scaled-down version and “thought it was really important to get this conversation started.”

Much of the conversation in committee centered on local programs in cities such as Minneapolis and St. Paul. St. Paul Mayor Melvin Carter, a Democrat, told lawmakers the city’s 2020 pilot saw “groundbreaking” results.

After scraping by for years, some families were able to put money into savings for the first time, he said. Families experienced less anxiety and depression. And the pilot disproved the “disparaging tropes” from critics about people living in poverty, the mayor said.

Carter told lawmakers that the complex issue of economic insecurity demands statewide solutions.

“I am well aware that the policy we’re proposing today is a departure from what we’re all used to,” he said. “In fact, that’s one of my favorite things about it.”

Uncategorized

Retail losses lead February decline in reverse mortgage volume

A look at the divide between retail and wholesale shows the latter was stronger, but several trends are moving "in the right direction."

Share this:

Reverse mortgage volume dropped in February compared to the month prior, and new data compiled by Reverse Market Insight (RMI) shows that the primary culprit for the month was retail reverse mortgage originations.

The retail channel volume decrease of 15.7% effectively “masked” a gain of 3.9% posted on the wholesale side of the business, according to RMI. To get a better idea of the dynamics driving this data, RMD spoke with Jon McCue, RMI’s director of client relations, for additional perspective and a breakdown of why business moved this way.

Retail vs. wholesale drop

When asked about why retail suffered a heavier drop for the month, McCue said it could stem from a few different factors.

“I know some companies have gone back to brokering their loans because the volumes are not high enough to support their own staff to compete in the full correspondent space, so I’m sure there is an uptick in part to that,” McCue said. “Outside of that, a one-month decline like this is really too early to weigh in heavily with speculation. If this becomes a trend, then I think that would tell us more.”

Four of the top 10 lenders in the space — South River Mortgage, Goodlife Home Loans, Longbridge Financial and Liberty Reverse Mortgage — managed to post gains for the month. When asked about why the bigger lenders sustained drops in the retail and consumer-direct business channels compared to the wholesale side, McCue said part of it is data visibility.

“Given that the vast majority of brokers in the space only do zero to one loans a month, it is easier to see the significant decreases in the larger players since their volumes are more visible to the entire space,” he said.

“Because of this fact, when there are industry headwinds, we tend to see it first in the larger lenders simply because it is easier to see. However, if we go back to the November and December case number assignments, the writing was sort of on the wall that a month like this was coming.”

That’s because those were the two lowest case number assignment months in all of 2023, McCue said. South River Mortgage does not have a wholesale channel, so its growth was due entirely to retail, but for the other lenders it was a bit more channel-driven, with the exception of Longbridge, he added.

“Longbridge led the wholesale channel in February and was No. 3 in retail, so when combined it gave them a nice boost month over month,” McCue said. “Goodlife was all from their wholesale channel, and Liberty was a little bit of a combined effort as well from both its channels.”

Case numbers, product types

In terms of case numbers, the low-issuance months at the end of 2023 served as a bit of a telegraph, McCue noted.

“Since we are speaking of February endorsements, we need to go back to around the November and December case number assignments, which happened to be the lowest in all of 2023 at just over 2,600 and 2,200 respectively,” he explained.

“With that said, you shouldn’t be too surprised to see endorsements fall off in February. However, ever since the start of the year, we have seen an uptick in case numbers, which correlates to the uptick in activity LOs have been seeing and that [RMD has] reported on.”

Earlier in the year, RMD spoke to reverse mortgage managers and loan officers across the country, who did in fact report a more steady stream of inbound inquiries and product interest. Part of that was also due to an apparent increase in originator sentiment around the HECM for Purchase (H4P) product, which RMI hopes to see more of in the months ahead.

“We are firm believers that the H4P product is prime to take off,” McCue said. “When looking at H4P volumes over the years, interest rates have had very little to do with its success. In fact, the lowest levels of H4P were in the lowest rate environment during the 2020 pandemic as inventory tightened and seniors were not interested in moving given all that was happening.”

Industry perseverance

But other data suggests that seniors may be more willing to move again. He cited the 2024 Generational Trends report from by the National Association of Realtors (NAR), which indicated that the senior demographic made up the second-largest portions of buyers and sellers.

“This tells me [seniors] are moving again, so what are their options? For the right people in this high interest rate environment, an H4P may just be what they need,” McCue said. “And now that the program has gone through some recent changes, it is more closely related to its forward counterpart.”

The reverse mortgage industry, he added, is adding its own brand of perseverance to the table.

“With the rate environment we are in, it is tough, but case number assignments have been on the rise since January, the H4P product got some much needed improvements, and in speaking with LOs, it sounds like they are keeping busy,” McCue said. “Currently, all signs are pointing in the right direction, but that isn’t because of rates. It’s because of the hard work of all the professionals in this space working very hard to help their clients.”

interest rates pandemicUncategorized

Liquidity, not popularity, is what you should be watching

The frequency of calls that the market is in a euphoric bubble is increasing. It’s worth exploring some of the evidence used to reach that conclusion…

Share this:

The frequency of calls that the market is in a euphoric bubble is increasing. It’s worth exploring some of the evidence used to reach that conclusion before deciding whether now is the time to adopt a more cautious stance and to ready oneself for the benefits lower prices deliver.

Notwithstanding the need for more data and analysis to support these claims, we’ll begin by dealing a swift blow to the weakest argument that the market is due for a correction – that it’s risen a lot.

Yes, it is true that stocks in even higher-quality companies like Goodman Group (ASX:GMG), for example, have risen over 60 per cent in the last twelve months. Another high-quality company’s shares, Megaport (ASX:MP1) – a stock owned by the Montgomery Small Companies Fund – have risen by more than 250 per cent in the last year. Even the S&P/ASX200 is up 977 points or 14.4 per cent from its October lows.

Does that mean stocks are now going to fall? Perish the thought! A rising market is insufficiently compelling evidence the market is now due for a correction.

I find this argument difficult to accept as a reason to expect a pullback because it only recognises a rise in price and fails to acknowledge the level from whence that rise came. Were the shares undervalued before they took off, or were they already overpriced to begin with? The same argument also fails to answer whether the shares have now become overpriced on either a relative or absolute basis. Some insights into past or current valuations need to be provided. And remember, even then, prices can remain reflective of exuberance for a long time.

Let’s look at some of the more nuanced arguments.

The first is arguably related to increasing popularity.

The bullish sentiment in the financial markets is undeniably robust. According to the latest data from U.S.-based research firm ETFGI, total assets under management (AUM) for exchange-traded funds (ETFs) globally soared last month to the unprecedented level of U.S.$12.25 trillion. Notably, February marked the 57th consecutive month of net inflows into global ETFs, totalling U.S.$116.3 billion.

Focusing on the asset classes, equity ETFs are the predominant beneficiaries. In February alone, equity ETFs captured net inflows of U.S.$80.4 billion, pushing the year-to-date figure to U.S.$141.4 billion – a nearly sevenfold increase from the corresponding period in the previous year.

Zooming in on the subsectors reaping the benefits of these inflows, the U.S. market, particularly the technology sector, stands out. A prime example is the Vanguard Information Technology ETF (NYSE:VGT), which witnessed a nearly 10 per cent increase in its funds under management to U.S.$70 billion.

Yes, stocks are popular again, or is it ETFs themselves?

According to Grant’s Interest Rate Observer, more than 12,000 ETF products exist worldwide, up 140 per cent from just five years ago. Over the past 15 months alone, as many as 3,000 ETF products have launched, nearly matching the 3,700 companies listed on U.S. exchanges. Is the tail now wagging the dog? That’s a question for another time.

Once again, it’s safe to say stocks are popular.

This is reflected in the expansion of the price-to-earnings (P/E) ratio, which is a proxy for popularity. The higher the P/E, the more popular investing in a stock or the index must be. According to Bloomberg, back in September 2022, at the depths of the last market selloff, the P/E ratio of the S&P/ASX200 was 12.44 times. Today, the P/E ratio is 17.04 times. That shift reflects an improvement in sentiment towards investing in equities that can be at least partly attributed to a more sanguine outlook for interest rates and inflation.

Lest you worry that interest rates aren’t falling fast enough, however, keep in mind the improvement in sentiment has occurred as bond rates have actually risen.

More importantly, while P/Es have risen, they are a far cry from the levels of popularity they reflected during historical periods of euphoria.

Figure 1. U.S. S&P600 Small Cap Index P/E ratio

As you can see from Figure 1., which reveals the one-year forward P/E ratio for the U.S. S&P600 small cap index since the turn of the century, the multiple of earnings investors are willing to pay for smaller companies has only been lower after the GFC, during the GFC, and after the tech wreck in the early 2000s. While PE ratios have recently risen, they are nowhere near the levels of euphoria that preceded crashes in the past.

As you can see from Figure 1., which reveals the one-year forward P/E ratio for the U.S. S&P600 small cap index since the turn of the century, the multiple of earnings investors are willing to pay for smaller companies has only been lower after the GFC, during the GFC, and after the tech wreck in the early 2000s. While PE ratios have recently risen, they are nowhere near the levels of euphoria that preceded crashes in the past.

As an aside, the small cap investment universe is one of the most exciting parts of the market in which to invest. You can gain exposure to sectors, industries and themes that simply aren’t available in large caps. Also worth keeping in mind is the small cap universe is always expanding and being refreshed. New companies emerge, there are initial public offerings (IPOs), and all the merger and spinoff activity ensures there’s always an opportunity around the corner for those willing to devote their time to the analysis.

The second and third arguments are like the first: Related to popularity.

According to EPFR Global, investors poured U.S.$56 billion into U.S. equities in the middle week of March. This was a new record, and 39 per cent, or U.S.$22 billion, went into technology stocks. The previous record was in March 2021.

A Bank of America survey of global fund managers reveals the most bullish sentiment since November 2021, proving that those flows reflect popularity.

For me, these arguments are little more than clumsy measures of popularity. They do little to help predict the answer to the more important question of when the market will turn down. To do that, we’d need to measure when sentiment is changing, and we can’t forecast that. All measures of sentiment are coincident at best. The market will already be falling by the time you read measures of popularity are falling.

For what it’s worth, the preponderance of IPOs is one sign that boom conditions are becoming bubble-like. Typically, bubbles are defined by euphoria, which manifests in various ways. One is the proliferation of initial public offerings, and another is the magnitude of first-day price increases for those IPOs.

Investment banks know they must “feed the ducks while they’re quacking”, so they provide a steady stream of selldowns and sellouts when markets are hot and potentially irrational. And when markets are hot and irrational, those that missed out fear further opportunity costs, pushing IPO share prices higher on their first day.

In 1999, when I was working at Merrill Lynch, there was a stunning 470 IPOs in the U.S. and a reported 70 per cent first-day capital gain across all IPOs. I recall there was something like a 90 per cent first-day gain for Nasdaq-listed IPOs.

More recently, there were more than 300 IPOs in 2021 as the market heated up post-pandemic. There was also a lot of liquidity as you will see in a moment. First-day gains averaged more than 30 per cent. We are nowhere near those numbers today. In 2023, there weren’t many more than 50 IPOs, and the first-day average gain was about 10 per cent. The ducks aren’t quacking. Yet.

But the IPO market is waking up to the rise in popularity of equities.

In the U.S. chat platform Reddit (NYSE:RDDT) IPO’d on March 21. Its IPO price of U.S.$34 valued the social media company at U.S.$6.5 billion, but after it listed, the stock climbed to close its first day at $50.44 – a gain of over 48 per cent. And keep in mind Reddit has never made a profit in its 20 years of existence.

A few more of these, and we may indeed be adding to the chorus of those screaming ‘bubble’! I don’t think we’re there yet. Yes, stocks are more popular than they were in the recent past, but they are far from being at the levels of popularity seen in previous bubbles. And even the insider selling by Bezos and Zuckerberg shouldn’t raise eyebrows unless you believe they are prophetic market timers.

Jeff Bezos did sell shares worth U.S.$8.5 billion in February, Meta CEO Mark Zuckerberg sold U.S.$135 million worth of shares in early February, and famed investor Peter Thiel offloaded U.S.$175 million of stock this month. Three big sales do not a winter make.

I think it’s prudent to watch liquidity. Liquidity is the main driver of asset prices. Liquidity precedes popularity. Stocks can only become more popular when people have more money (liquidity). And liquidity has been rising since the middle of last year.

Figure 2. CrossBorder Capital liquidity heatmap

Figure 2., and figure 3., shows how more liquidity in 2021 (green in figure 2.) coincided and preceded a rally in markets, while a tightening of liquidity (red) coincided or even preceded the sell-off in equities of 2022. Today’s neutral shade suggests an improvement from 2023, which was positive for equities.

Figure 2., and figure 3., shows how more liquidity in 2021 (green in figure 2.) coincided and preceded a rally in markets, while a tightening of liquidity (red) coincided or even preceded the sell-off in equities of 2022. Today’s neutral shade suggests an improvement from 2023, which was positive for equities.

Figure 3. CrossBorder’s global liquidity cycle chart

And keep in mind even though rate cuts might be delayed, there is general acceptance that rates have peaked.

There will be bumps along the way, and nothing in the above discussion suggests the market won’t decline, but most of the so-called ‘signs’ the market is euphoric and therefore primed for something catastrophic appear premature.

nasdaq equities stocks pandemic etf interest ratesUncategorized

What If The Fed’s Hikes Are Actually Sparking US Economic Boom?

What If The Fed’s Hikes Are Actually Sparking US Economic Boom?

Authored by Ye Xie via Bloomberg,

As the US economy hums along month after…

Share this:

{kind=link}

Authored by Ye Xie via Bloomberg,

As the US economy hums along month after month, minting hundreds of thousands of new jobs and confounding experts who had warned of an imminent downturn, some on Wall Street are starting to entertain a fringe economic theory.

What if, they ask, all those interest-rate hikes the past two years are actually boosting the economy? In other words, maybe the economy isn’t booming despite higher rates but rather because of them.

It’s an idea so radical that in mainstream academic and financial circles, it borders on heresy — the sort of thing that in the past only Turkey’s populist president, Recep Tayyip Erdogan, or the most zealous disciples of Modern Monetary Theory would dare utter publicly.

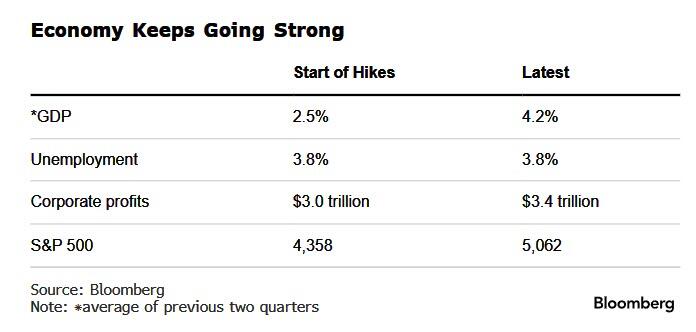

But the new converts — along with a handful who confess to being at least curious about the idea — say the economic evidence is becoming impossible to ignore. By some key gauges — GDP, unemployment, corporate profits — the expansion now is as strong or even stronger than it was when the Federal Reserve first began lifting rates.

This is, the contrarians argue, because the jump in benchmark rates from 0% to over 5% is providing Americans with a significant stream of income from their bond investments and savings accounts for the first time in two decades. “The reality is people have more money,” says Kevin Muir, a former derivatives trader at RBC Capital Markets who now writes an investing newsletter called The MacroTourist.

{kind=link}

These people — and companies — are in turn spending a big enough chunk of that new-found cash, the theory goes, to drive up demand and goose growth.

In a typical rate-hiking cycle, the additional spending from this group isn’t nearly enough to match the drop in demand from those who stop borrowing money. That’s what causes the classic Fed-induced downturn (and corresponding decline in inflation). Everyone was expecting the economy to follow that pattern and “slow precipitously,” Muir says. “I’m like no, it’s probably more balanced and might even be slightly stimulative.”

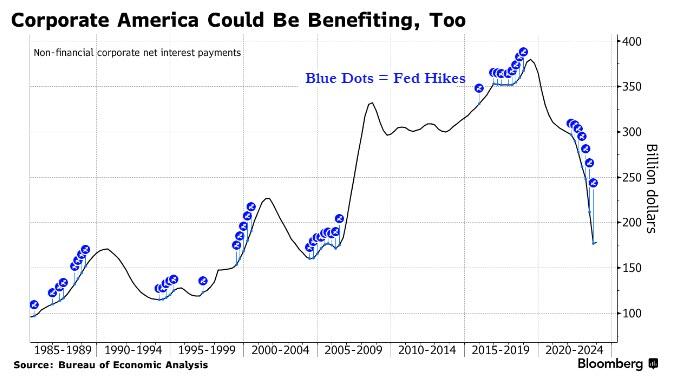

Muir and the rest of the contrarians — Greenlight Capital’s David Einhorn is the most high profile of them — say it’s different this time for a few reasons. Principal among them is the impact of exploding US budget deficits. The government’s debt has ballooned to $35 trillion, double what it was just a decade ago. That means those higher interest rates it’s now paying on the debt translate into an additional $50 billion or so flowing into the pockets of American (and foreign) bond investors each month.

That this phenomenon made rising rates stimulative, not restrictive, became obvious to the economist Warren Mosler many years ago. But as one of the most vocal advocates of Modern Monetary Theory, or MMT, his interpretation was long dismissed as the preachings of an eccentric crusader. So there’s a little sense of vindication for Mosler as he watches some of the mainstream crowd come around now. “I’ve been certainly talking about this for a very long time,” he says.

Muir readily admits to being one of those who had snickered at Mosler years ago. “I was like, you’re insane. That makes no sense.” But when the economy took off after the pandemic, he decided to take a closer look at the numbers and, to his surprise, concluded Mosler was right.

‘Really Weird’

Einhorn, one of Wall Street’s best-known value investors, came to the theory earlier than Muir, when he observed how slowly the economy was expanding even though the Fed had pinned rates at 0% after the global financial crisis. While hiking rates to extremes clearly wouldn’t help the economy — the blow to borrowers from a, say, 8% benchmark rate is just too powerful — lifting them to more moderate levels would, he figured.

Einhorn notes that US households receive income on more than $13 trillion of short-term interest-bearing assets, almost triple the $5 trillion in consumer debt, excluding mortgages, that they have to pay interest on. At today’s rates, that translates to a net gain for households of some $400 billion a year, he estimates.

“When rates get below a certain amount, they actually slow down the economy,” Einhorn said on Bloomberg’s Masters in Business podcast in February. He calls the chatter that the Fed needs to start cutting rates to avoid a slowdown “really weird.”

“Things are pretty good,” he said. “I don’t think that they’re really going to help anybody” by cutting rates.

(Rate cuts do figure prominently, it should be noted, in a corollary to the rate-hikes-lift-growth theory that another camp on Wall Street is backing. It posits that rate cuts will actually push inflation further down, not up.)

To be clear, the vast bulk of economists and investors still firmly believe in the age-old principle that higher rates choke off growth.

As evidence of this, they point to rising delinquencies on credit cards and auto loans and to the fact that job growth, while still robust, has slowed.

Mark Zandi, chief economist at Moody’s Analytics, spoke for the traditionalists when he called the new theory simply “off base.” But even Zandi acknowledges that “higher rates are doing less economic damage than in times past.”

Like the converts, he cites another key factor for this resilience: Many Americans managed to lock in uber-low rates on their mortgages for 30 years during the pandemic, shielding them from much of the pain caused by rising rates.

(This is a crucial difference with the rest of the world; mortgage rates rapidly adjust higher as benchmark rates rise in many developed nations.)

Bill Eigen chuckles when he recalls how so many on Wall Street were predicting catastrophe as the Fed began to ratchet up rates. “They’ll never go past 1.5% or 2%,” he intones, sarcastically, “because that will collapse the economy.”

Eigen, a bond fund manager at JPMorgan Chase, isn’t an outright proponent of the new theory. He’s more in the camp of those who sympathize with the broad contours of the idea. That stance helped him see the need to refashion his portfolio, loading it up with cash — a move that’s put him in the top 10% of active bond fund managers over the past three years.

Eigen has two side hustles outside of JPMorgan. He runs a fitness center and car repair shop. At both places, people keep spending more money, he says. Retirees, in particular. They are, he notes, perhaps the biggest beneficiaries of the higher rates.

“All of a sudden, all of this disposable income accrues to these people,” he says. “And they’re spending it.”

Retail losses lead February decline in reverse mortgage volume

Regeneron enters venture investing with $500M, poaches senior partner from ARCH

Skin in the Game: Oruka Takes on Blockbuster Drugs for Psoriasis, Dermatological Disorders

CNN Is Wrong… Deflation Is A Good Thing

Grizzly bear conservation is as much about human relationships as it is the animals

Simultaneous declines in housing permits, starts, and units under construction in March suggests seasonality glitch, not a change in trend

Do housing starts show we’re going into a recession?

Liquidity, not popularity, is what you should be watching

Kidney disease intervention outcomes encouraging, despite null result

Origins: From managing restaurants to reverse mortgage partnerships

-

International4 weeks ago

International4 weeks agoParexel CEO to retire; CAR-T maker AffyImmune promotes business leader to chief executive

-

Spread & Containment1 month ago

Spread & Containment1 month agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Government1 week ago

Government1 week agoClimate-Con & The Media-Censorship Complex – Part 1

-

Spread & Containment2 days ago

Spread & Containment2 days agoWHO Official Admits Vaccine Passports May Have Been A Scam

-

Spread & Containment1 week ago

Spread & Containment1 week agoFDA Finally Takes Down Ivermectin Posts After Settlement

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoVaccinated People Show Long COVID-Like Symptoms With Detectable Spike Proteins: Preprint Study

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoCan language models read the genome? This one decoded mRNA to make better vaccines.

-

Uncategorized1 week ago

Uncategorized1 week agoWhat’s So Great About The Great Reset, Great Taking, Great Replacement, Great Deflation, & Next Great Depression?