Uncategorized

CNN Is Wrong… Deflation Is A Good Thing

CNN Is Wrong… Deflation Is A Good Thing

Authored by Soham Patil via The Mises Institute,

A recent video by CNN states that lower prices…

Share this:

Authored by Soham Patil via The Mises Institute,

A recent video by CNN states that lower prices are bad for the United States economy and that consumers must get used to the newer, higher prices.

The video goes so far as to say, “We’re never going to pay 2019 prices again.”

The video claims that deflation is responsible for a long list of problems including layoffs, high unemployment, and falling incomes.

Americans should simply get used to paying more and more each year and be happy about it. Except, deflation is actually good for consumers despite the contentions of inflation-supporting economists.

The conclusion that inflation is a good thing is reached by the mishandling of economic terms.

While Austrian economics accepts that inflation is the expansion of the money supply, mainstream economics contends that inflation is an increase in the general price level in an economy. This skewed definition allows one to erroneously conclude that inflation causes prosperity by raising profits and incomes through higher consumer prices. The problem with this is that “price inflation” is also often caused by real inflation: the increase of the money supply. An increase in the money supply comes from the creation of additional units of money ex nihilo, out of nothing. The wealth of savers is diluted by the expansion of the money supply, which leads to the hardships many Americans face.

Further, while the video contends that the pandemic may have caused rising prices, it cannot explain the continual growth of prices even after the effects of the pandemic have subsided. The pandemic is not responsible for the continual trend of increasing prices; the growth of the money supply is.

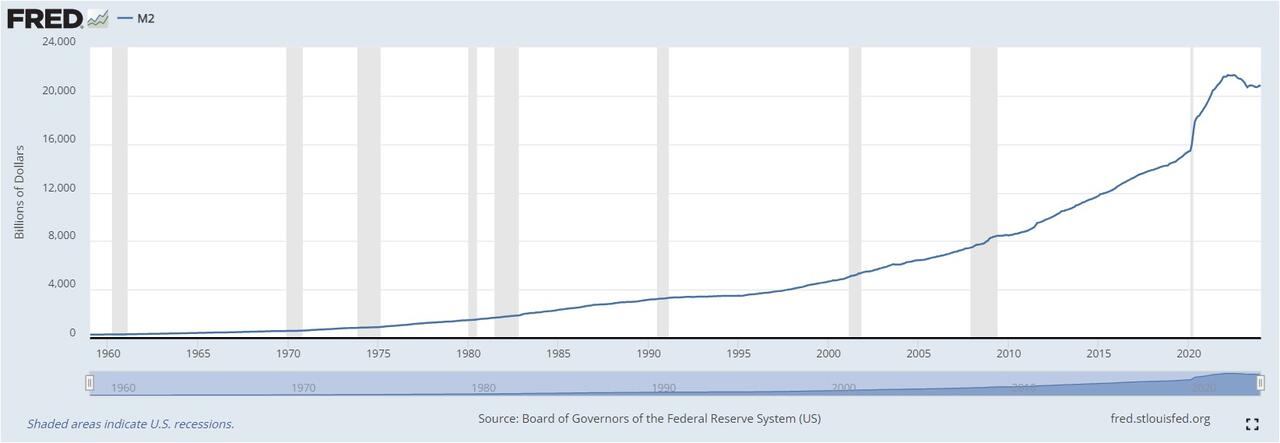

Figure 1: The M2 in the United States, 1959–2024

Source: FRED. Data from the Board of Governors of the Federal Reserve System.

While the money supply of US dollars has increased steadily over the past few decades, a significant jump can be seen after 2019 when the Federal Reserve’s expansionary monetary policies caused a great rise in the money supply. This growth, uncompensated by additional production due to the pandemic, caused the price inflation that many now blame solely on the pandemic. The truth is that if the pandemic were the cause of prices rising a significant amount, the absence of the pandemic should account for a proportionally drastic deflationary period afterward. This never occurred, and thus the money supply paints a more honest picture of inflation than any index of a collection of prices ever could.

By contrast, deflation, as opposed to inflation, is often a good thing for consumers. Deflation means that the same unit of money is worth more today than it was yesterday. Consumers thus can buy more today than they could yesterday. Instead of actively being impoverished during conditions of inflation, consumers would rather be made richer during times of deflation.

The reason many economists are quick to champion inflation as creating prosperity is because central banks have previously used expansionary monetary policies to temporarily boost the economy by increasing aggregate demand. Several of these policies, often specifically lowering interest rates, cause a boom-bust cycle. When the money supply is expanded and cheap credit is abundant, firms are able to take on ambitious projects that they may not have been able to previously. Malinvestment results from the unsustainable credit expansion created by extremely low interest rates. There is greater demand for the factors of production, and an increase is seen in conventional metrics of economic growth such as gross domestic product.

During the process of malinvestment, an increase in employment occurs due to the firms having access to cheap and easy credit, allowing for greater business spending. However, when firms lose access to cheap and easy credit due to the central banks having to prioritize cutting inflation, jobs are lost. These job losses are not the fault of the deflation but rather the malinvestment during economic booms. Without malinvestment and inflation, resources would have been invested in more-profitable endeavors, making better use of these resources.

Artificially cheap credit causes a misallocation of resources by skewing price information. Eventually, a bust must follow the boom. In this period, deflation often occurs due to market actors coming to more-realistic valuations of the factors of production. After these realistic valuations come about, consumers are able to pay less for their goods and services . . . at least until the central bank causes the next boom-bust cycle.

In conclusion, it would be wrong to pinpoint deflation as a potential issue for the economy.

To do so would be to conflate the cause and effect of how money supply affects an economy.

Contrary to CNN’s video, the Federal Reserve throughout its history has not helped the cause of consumers, evidenced by the exponential growth of prices since its foundation.

Uncategorized

Regeneron enters venture investing with $500M, poaches senior partner from ARCH

Regeneron, the 35-year-old drugmaker still led by its co-founders, is getting into the venture investing arena.

The New York pharma will commit $100 million…

Share this:

Regeneron, the 35-year-old drugmaker still led by its co-founders, is getting into the venture investing arena.

The New York pharma will commit $100 million per year for five years, it said Monday morning. The drugmaker is the exclusive limited partner for the fund, which launched this month under the name Regeneron Ventures. It will invest in biotech startups, devices, tools and “enabling technologies.”

Leading the firm are former Regeneron senior vice presidents Jay Markowitz and Michael Aberman. Markowitz spent the past three years at ARCH Venture Partners as a senior partner, and Aberman was most recently CEO of seed-stage immuno-oncology biotech XenImmune Therapeutics.

Most large pharma companies have venture arms of their own. Regeneron is stepping onto the court as it matures into the next $100 billion market cap drugmaker. It fell below that arbitrary mark on Friday, with its stock $REGN closing down 1.7% on April 12.

The Tarrytown-based pharma has largely favored R&D pacts over acquisitions throughout its history and still operates as an entrepreneurial company with its co-founders Len Schleifer and George Yancopoulos still serving as CEO and chief scientific officer, respectively.

Michael Aberman

Michael AbermanThe venture team will invest “agnostic to therapeutic area, technology and stage of development,” Markowitz said in a statement. Regeneron’s therapeutic interests are quite broad: cardiovascular/metabolic, blood cancers, oncology, ophthalmology and infectious disease, among others.

“Our goal is to cultivate an ecosystem where the next generation of biotech companies can thrive, drawing on the lessons learned and successes achieved at Regeneron and throughout our careers,” Aberman said in the press release.

Regeneron’s entry into biotech venture investing comes as industry insiders cross their fingers that the optimism of the past few months sustains itself for a broader, deeper recovery for drug developers. Record amounts of capital were deployed on the public financing side in the first quarter of 2024 as PIPEs were all the rage. On the private side, venture dollars returned to pre-pandemic levels but are still far off the quarterly numbers of the 2020 and 2021 go-go days.

recovery pandemicUncategorized

The March CPI, the Inflation Picture, and the Fed

The higher than expected March CPI released on Wednesday freaked everyone out and got the markets convinced we will see fewer, if any, interest rate cuts…

Share this:

The higher than expected March CPI released on Wednesday freaked everyone out and got the markets convinced we will see fewer, if any, interest rate cuts this year. I have never been a Fed tea leaf reader, and am not about to change professions now, but it will be bad news if the Fed puts off rate cuts that can revitalize the housing market.

The big concern posed by the CPI, following higher-than-expected inflation numbers in January and February, is whether inflation is reaccelerating. We know that rental inflation is still high as an outcome of the surge in working from home at the start of the pandemic.

But we can be very confident that it will slow sharply over the course of the year due to the much slower inflation rate shown in indexes (including the BLS index) measuring rents in units that change hands. This means that rental inflation will not be an ongoing problem that the Fed has to worry about.

However, the recent data have shown an uptick in inflation, even pulling out rent. This is ostensibly the cause for concern.

There are two important points to be made about this uptick. First, it is not unusual to see large jumps, and falls, in CPI inflation excluding rent. Rent is a huge factor in the index, and since the pace of rental inflation changes slowly, it anchors the overall rate. Inflation is much more erratic when rent is excluded as shown below.

Note that there were many points at which inflation in the non-shelter CPI crossed 2.0 percent even in the low-inflation decade preceding the pandemic. In fact, year-over-year inflation in this index hit 2.1 percent in January of 2020, just before the pandemic started. It was at 2.5 percent in July of 2018. So a somewhat above-target reading for the non-shelter CPI should not be a major cause for concern by itself.

However, there is the question of whether the recent uptick reflects underlying trends. Here the story points in the opposite direction.

The day after the CPI report came out, we got a much more benign reading on the Producer Price Index (PPI). The overall figure for the month was 0.2 percent (0.154 to be more precise), with the core also at 0.2 percent. There are differences in coverage and methodology between the CPI and PPI, but inflation in the indexes still track each other closely.

The figure below shows the PPI for services, the PPI for goods, and the CPI.

What is perhaps most striking is how closely the CPI follows the PPI for services. That probably shouldn’t be surprising, since services account for almost two-thirds of the CPI. (It is important to note that the PPI does not include rent, so these are services minus rent.)

When the CPI goes substantially above or below the service component of the PPI is following movements in the goods component. As can be seen the CPI has been well above the service component in the PPI since May of 2022. The cause here is the supply chain problems that sent goods inflation sky-rocketing a bit more than a year earlier.

The good news in this picture is that the goods component of the PPI has been far below the service CPI for a bit over a year, and for part of this period was even negative. This is just another way of showing the widely noted fact that the prices of supply chain goods have stabilized and in many cases are even falling. This looks likely to continue for the near-term future, especially if we don’t have a policy of blocking cheaper imports with higher tariffs as some presidential candidates are advocating.

The Wage Story

There is another part of the longer-term inflation picture that needs to be included, the slowing of wage growth. Our various wage indices show somewhat different figures for wage growth, but they tell basically the same story. Wage growth accelerated sharply as the economy reopened in the second half of 2020 and especially 2021 and 2022, as employers had to compete to hire and retain workers.

We saw record rates of quits, as workers left jobs that didn’t pay enough, offer advancement opportunities, had unsafe workplaces, or where the boss was a jerk. This is a great story, as workers saw gains in wages that outpaced inflation and workplace satisfaction hit a record high. The gains in wages were especially large for those at the bottom of the wage distribution.

While that is a very bright picture, we could not sustain nominal wage gains of the sort we were seeing in 2021 and the first half of 2022, and still hit the Fed’s 2.0 percent inflation target. Wage growth peaked at roughly 6.0 percent, 2.5 percentage points higher than the rates we were seeing before the pandemic.

To be clear, wages were not driving inflation. There was a shift from wages to profits at the start of the pandemic. It doesn’t make sense to say that wages are the cause of inflation when the profit share is increasing. But it is true that given current rates of productivity growth, we cannot have 6.0 percent wage growth and sustain anything close to a 2.0 percent rate of inflation. (FWIW, I am not a fan of the Fed’s 2.0 percent inflation target, but the Fed is.)

However, wage growth has slowed sharply over the last two years, getting close to its pre-pandemic pace. Again, there are differences by indices, but the pace of wage growth has fallen by roughly 2.0 percentage points, leaving it 0.5 percentage points above its pre-pandemic pace.

One index, the Indeed Wage Tracker, has fallen back to its 2019 rate of wage growth. This index is noteworthy because it measures wages in job postings for new hires. In this sense it can be thought of as being analogous to the new tenant rent indexes that measure the rents of units that turn over.

Just as most people don’t move every month, most people don’t change jobs every month, but we expect the rents of units that don’t turn over to roughly follow the rents of units that do change hands. In the same way, it is reasonable to think that wage patterns of workers who stay in their jobs will roughly follow wage patterns for newly hired workers. The Indeed Wage Tracker is telling us that wage growth has fallen back to a non-inflationary pace. This may take some time to show up in the other wage series, but we can be pretty confident of the direction of change.

Profit Shares and Productivity

There are two other reasons we can be reasonably confident inflation is now under control. The first is that the rise in profit shares at the start of the pandemic has not gone away. In fact, profit shares increased somewhat in the fourth quarter, indicating we are going in the wrong direction.

It is not clear why profit shares continue to rise, and not fall back towards pre-pandemic levels. (Yeah, corporations are greedy, but they have always been greedy.) The increase during the supply-chain crisis was understandable, companies have much more market power when supply is constrained. But unless conditions of competition were permanently altered by the pandemic, it’s hard to see why they would stay elevated, and we certainly should not expect them to continue to rise.

In any case, the rise in the profit share in the fourth quarter, suggests that a lower pace of inflation would be consistent with the wage growth we are now seeing, if the profit share were to remain stable. If the profit share were to fall back towards its pre-pandemic level (which was already well above its level at the start of the century), we could sustain considerably lower inflation with the current pace of wage growth.

In other words, there seems little basis for believing that the current rate of wage growth is inconsistent with the Fed’s 2.0 percent inflation target. In this respect, the Biden administration is on exactly the right track in going after abuses of market power that allow for higher margins, such as attempting to block the merger of the nation’s two largest supermarket chains, Albertson’s and Safeway. Similarly, cracking down on drug companies abusing their government-granted patent monopolies will also have the effect of reducing profit margins.

The other big wildcard in this story is productivity growth. Productivity growth soared in the last three quarters of 2023, averaging 3.7 percent over this period. Productivity growth is notoriously erratic and the data are subject to large revisions. We also have to note that growth was horrible in 2022, actually falling for the year. So, it is far too early to claim we are on a faster growth path. Nonetheless, the recent data are encouraging and it looks like we will have respectable numbers again for the first quarter, although not above 3.0 percent.

Given advances in AI and other technologies, it hardly seems absurd to think we may be seeing a productivity uptick. We are clearly at the very beginning of the uses of many of these technologies, so there will be many gains that we will see down the road.

If we can sustain a faster pace of productivity growth, then we can have faster nominal wage growth and still hit the Fed’s 2.0 percent inflation target. To be clear, I am not talking about a wildly rapid pace of growth, if we can just sustain a 2.0 percent rate, well below the rates we saw in the upturn from 1995 to 2005 and the long Golden Age from 1947 to 1973, then 4.0 percent wage growth would be consistent with 2.0 percent inflation, even after a period in which profit margins shrank somewhat.

Time to Declare Victory and Lower Rates

The long and short here is that it is really time for the Fed to declare victory in its war inflation and start lowering interest rates. One problem that seems to be delaying rate cuts is that the economy remains strong, leaving Chair Powell and other Fed officials to talk about the situation as a one-sided choice. They see a risk of inflation if they lower rates too much or too soon, but there is little basis for concern about a recession or rising unemployment.

However, that leaves other negative effects of high interest rates out of the equation, most notably their impact on the housing market. The number of existing homes being sold in the last year is down by almost a third from its 2020-21 pace. This means that millions of people who would otherwise be looking to move are being kept in place by the Fed’s high interest rate policy.

Higher interest rates are also a drain on people’s budgets insofar as they have credit card debt or other forms of short-term debt. And it makes it more expensive to buy new or used cars. The rise in interest rates also creates stress on the financial system. This stress led to the failure of Silicon Valley Bank last year, along with several other smaller banks. With luck we won’t see another major round of bank failures this year, but higher rates unambiguously increase the risk.

In short, even if the economy does not need lower rates to sustain a healthy growth path right now, there is a real cost to keeping rates high. It’s time for Fed to change course.

The post The March CPI, the Inflation Picture, and the Fed appeared first on Center for Economic and Policy Research.

recession unemployment pandemic fed housing market recession tariffs interest ratesUncategorized

Let’s Be Honest: The Economy Is NOT Doing Well

Let’s Be Honest: The Economy Is NOT Doing Well

Authored by Connor O’Keeffe via The Epoch Times (emphasis ours),

The American economy is…

Share this:

{kind=link}

Authored by Connor O'Keeffe via The Epoch Times (emphasis ours),

The American economy is not all right. But to see why, you need to look beyond the dramatic numbers we keep seeing in the headlines and establishment talking points.

{kind=link}

Take, for instance, the latest jobs report. For the third month in a row, the American economy added significantly more jobs than most economists had been expecting—a total of 303,000 for March. On its face, that’s a good number.

But as Ryan McMaken laid out over the weekend, things don’t look as strong when you dig into the data. For instance, virtually all the jobs added are part-time jobs. Full-time jobs have actually been disappearing since December of last year. In fact, as McMaken highlighted, “The year-over-year measure of full-time jobs has fallen into recession territory.”

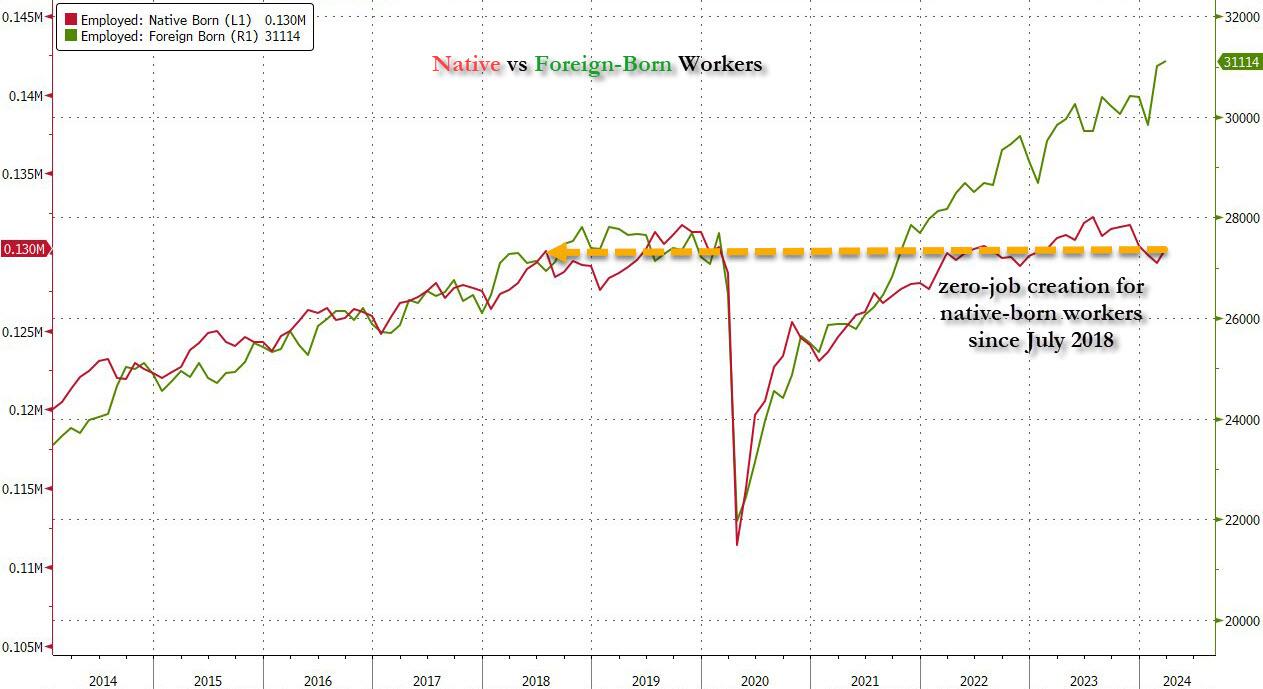

Also, most of these new part-time jobs are going to immigrants, many of whom are in the country illegally. There has been zero job creation for native-born Americans since mid-2018. While immigrants are not harming the economy by working, the scale of new foreign-born workers has papered over the employment struggles of the native-born population.

{kind=link}

Further, government jobs accounted for almost a quarter of those added—way above the standard ten to twelve percent. Just like with government spending and economic growth, government hiring boosts the official jobs number while draining the actual, value-producing economy.

Some economists, like Daniel Lacalle, argue that the U.S. economy is already experiencing a private-sector recession but that government spending and hiring are propping up the official data enough to hide it.

A recession is inevitable, thanks to the last decade of interest rate manipulation by the Federal Reserve—and especially to its dramatic actions during the pandemic. The recession-like conditions in full-time jobs is further evidence that Lacalle is right.

But jobs numbers are only part of the story. The stock market has been fluctuating a lot recently, not because of changing consumer needs or the adoption of some new technology, but based on what Federal Reserve officials are saying about what the central bank will do this year.

At the same time, prices are still high. And they continue to rise at a rate that frustrates even some of President Joe Biden’s biggest economic cheerleaders. Our dollars are worth about 20 percent less than they were four years ago, with no prospect of that trend reversing. That hurts.

But instead of addressing this economic pain, much less their role in creating it, members of the political class are still pretending everything is great. They’re even gearing up to make things worse by, for example, sending even more of our money to the Ukrainian government. All to prolong a war it’s losing, not because of a lack of money, but because of a lack of soldiers.

And at home, President Biden is scrambling to put the brakes on energy production and to transfer money from the working class to his base of college graduates, all before he’s up for reelection in November.

Predictably and appropriately, the establishment’s head-in-the-sand economic strategy is coinciding with a notable decrease in support for the Democrats—the establishment’s preferred party these days. President Biden is behind in the polls in six of the seven swing states and is losing support from working-class and nonwhite voters.

The political establishment and its preferred candidates deserve to lose support, not only for failing to acknowledge America’s economic problems but for causing them in the first place.

From Mises.org

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

The March CPI, the Inflation Picture, and the Fed

Popular media company files for bankruptcy, plans to liquidate

Let’s Be Honest: The Economy Is NOT Doing Well

Regeneron enters venture investing with $500M, poaches senior partner from ARCH

CNN Is Wrong… Deflation Is A Good Thing

-

International3 weeks ago

International3 weeks agoParexel CEO to retire; CAR-T maker AffyImmune promotes business leader to chief executive

-

Spread & Containment1 month ago

Spread & Containment1 month agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Government1 week ago

Government1 week agoClimate-Con & The Media-Censorship Complex – Part 1

-

International15 hours ago

International15 hours agoWHO Official Admits Vaccine Passports May Have Been A Scam

-

Spread & Containment6 days ago

Spread & Containment6 days agoFDA Finally Takes Down Ivermectin Posts After Settlement

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoVaccinated People Show Long COVID-Like Symptoms With Detectable Spike Proteins: Preprint Study

-

Uncategorized1 week ago

Uncategorized1 week agoCan language models read the genome? This one decoded mRNA to make better vaccines.

-

Uncategorized1 week ago

Uncategorized1 week agoWhat’s So Great About The Great Reset, Great Taking, Great Replacement, Great Deflation, & Next Great Depression?