Government

Did Lockdowns Set A Global Revolt In Motion?

Did Lockdowns Set A Global Revolt In Motion?

Authored by Jeffrey Tucker via The Brownstone Institute,

My first article on the coming backlash…

Share this:

Authored by Jeffrey Tucker via The Brownstone Institute,

My first article on the coming backlash - admittedly wildly optimistic - went to print April 24, 2020.

After 6 weeks of lockdown, I confidently predicted a political revolt, a movement against masks, a population-wide revulsion against the elites, a demand to reject “social distancing” and streaming-only life, plus widespread disgust at everything and everyone involved.

I was off by four years. I wrongly assumed back then that society was still functioning and that our elites would be responsive to the obvious flop of the whole lockdown scheme. I assumed that people were smarter than they proved to be. I also did not anticipate just how devastating the effects of lockdown would be: in terms of learning loss, economic chaos, cultural shock, and the population-wide demoralization and loss of trust.

The forces that set in motion those grim days were far more deep than I knew at the time. They involved a willing complicity from tech, media, pharma, and the administrative state at all levels of society.

There is every evidence that it was planned to be exactly what it became; not just a foolish deployment of public health powers but a “great reset” of our lives. The newfound powers of the ruling class were not given up so easily, and it took far longer for people to shake off the trauma than I had anticipated.

Is that backlash finally here? If so, it’s about time.

New literature is emerging to document it all.

The new book “White Rural Rage: The Threat to American Democracy” is a viciously partisan, histrionic, and gravely inaccurate account that gets nearly everything wrong but one: vast swaths of the public are fed up, not with democracy but its opposite of ruling class hegemony.

The revolt is not racial and not geographically determined. It’s not even about left and right, categories that are mostly a distraction. it’s class-based in large part but more precisely about the rulers vs. the ruled.

With more precision, new voices are emerging among people who detect a “vibe change” in the population.

One is Elizabeth Nickson’s article “Strongholds Falling; Populists Seize the Culture.”

She argues, quoting Bret Weinstein, that:

“The lessons of [C]ovid are profound. The most important lesson of Covid is that without knowing the game, we outfoxed them and their narrative collapsed .... The revolution is happening all over the socials, especially in videos. And the disgust is palpable.”

A second article is “Vibe Shift” by Santiago Pliego:

“The Vibe Shift I’m talking about is the speaking of previously unspeakable truths, the noticing of previously suppressed facts. I’m talking about the give you feel when the walls of Propaganda and Bureaucracy start to move as you push; the very visible dust kicked up in the air as Experts and Fact Checkers scramble to hold on to decaying institutions; the cautious but electric rush of energy when dictatorial edifices designed to stifle innovation, enterprise, and thought are exposed or toppled. Fundamentally, the Vibe Shift is a return to—a championing of—Reality, a rejection of the bureaucratic, the cowardly, the guilt-driven; a return to greatness, courage, and joyous ambition.”

We truly want to believe this is true. And this much is certainly correct: the battle lines are incredibly clear these days. The media that uncritically echo the deep-state line are known: Slate, Wired, Rolling Stone, Mother Jones, New Republic, New Yorker, and so on, to say nothing of the New York Times. What used to be politically partisan venues with certain predictable biases are now more readily described as ruling-class mouthpieces, forever instructing you precisely how to think while demonizing disagreement.

After all, all of these venues, in addition to the obvious case of the science journals, are still defending the lockdowns and everything that followed. Rather than express regret for their bad models and immoral means of control, they have continued to insist that they did the right thing, regardless of the civilization-wide carnage everywhere in evidence, while ignoring the relationship between the policies they championed and the terrible results.

Instead of allowing their mistakes to change their own outlook, they have adapted their own worldview to allow for snap lockdowns anytime they deem them necessary. In holding this view, they have forged a view of politics that it is embarrassingly acquiescent to the powerful.

The liberalism that once questioned authority and demanded free speech seems extinct. This transmogrified and captured liberalism now demands compliance with authority and calls for further restrictions on free speech. Now anyone who makes a basic demand for normal freedom—to speak or choose one’s own medical treatment or to decline to wear a mask—can reliably anticipate being denounced as “right-wing” even when it makes absolutely no sense.

The smears, cancellations, and denunciations are out of control, and so unbearably predictable.

It’s enough to make one’s head spin. As for the pandemic protocols themselves, there have been no apologies but only more insistence that they were imposed with the best of intentions and mostly correct. The World Health Organization wants more power, and so does the Centers for Disease Control and Prevention. Even though the evidence of the failure of pharma pours in daily, major media venues pretend that all is well, and thereby out themselves as mouthpieces for the ruling regime.

The issue is that major and unbearably obvious failures have never been admitted. Institutions and individuals who only double down on preposterous lies that everyone knows are lies only end up discrediting themselves.

That’s a pretty good summary of where we are today, with vast swaths of elite culture facing an unprecedented loss of trust. Elites have chosen the lie over truth and cover-up over transparency.

This is becoming operationalized in declining traffic for legacy media, which is shedding costly staff as fast as possible. The social media venues that cooperated closely with government during the lockdowns are losing cultural sway while uncensored ones like Elon Musk’s X are gaining attention. Disney is reeling from its partisanship, while states are passing new laws against WHO policies and interventions.

Sometimes this whole revolt can be quite entertaining.

When the CDC or WHO posts an update on X, when they allow comments, it is followed by thousands of reader comments of denunciation and poking fun, with flurries of comments to the effect of “I will not comply.”

DEI is being systematically defunded by major corporations while financial institutions are turning on it. Indeed, the culture in general has come to regard DEI as a sure indication of incompetence. Meanwhile, the outer reaches of the “great reset” such as the hope that EVs would replace internal combustion have come to naught as the EV market has collapsed, along with consumer demand for fake meat to say nothing of bug eating.

As for politics, yes, it does seem like the backlash has empowered populist movements all over the world. We see them in the farmers’ revolt in Europe, the street protests in Brazil against a sketchy election, the widespread discontent in Canada over government policies, and even in migration trends out of US blue states toward red ones. Already, the administrative state in D.C. is working to secure itself against a possible unfriendly president in the form of Donald Trump or RFK, Jr.

So, yes, there are many signs of revolt. These are all very encouraging.

What does all this mean in practice? How does this end? How precisely does a revolt take shape in an industrialized democracy? What is the mostly likely pathway for long-term social change?

These are legitimate questions.

For hundreds of years, our best political philosophers have opined that no system can function in a sustainable way in which a huge majority is coercively governed by a tiny elite with a class interest in serving themselves at public expense.

That seems correct. In the days of the Occupy Wall Street movement of 15 years ago, the street protesters spoke of the 1 percent vs. the 99 percent. They were speaking of those with the money inside the traders’ buildings as opposed to the people on the streets and everywhere else.

Even if that movement misidentified the full nature of the problem, the intuition into which it tapped spoke to a truth. Such a disproportionate distribution of power and wealth is dangerously unsustainable. Revolution of some sort threatens. The mystery right now is what form this takes. It’s unknown because we’ve never been here before.

There is no real historical record of a highly developed society ostensibly living under a civilized code of law that experiences an upheaval of the type that would be required to unseat the rulers of all the commanding heights. We’ve seen political reform movements that take place from the top down but not really anything that approximates a genuine bottom-up revolution of the sort that is shaping up right now.

We know, or think we know, how it all transpires in a tinpot dictatorship or a socialist society of the old Soviet bloc. The government loses all legitimacy, the military flips loyalties, there is a popular revolt that boils over, and the leaders of the government flee. Or they simply lose their jobs and take up new positions in civilian life. These revolutions can be violent or peaceful but the end result is the same. One regime replaces another.

It’s hard to know how this translates to a society that is heavily modernized and seen as non-totalitarian and even existing under the rule of law, more or less. How does revolution occur in this case? How does the regime come around to adapting itself to a public revolt against governance as we know it in the US, UK, and Europe?

Yes, there is the vote, if we can trust that. But even here, there are the candidates, which are that for a reason. They specialize in politics, which does not necessarily mean doing the right thing or reflecting the aspirations of the voters behind them. They are responsive to their donors first, as we have long discovered. Public opinion can matter but there is no mechanism that guarantees a smoothly responsive pathway from popular attitudes to political outcomes.

There is also the pathway of industrial change, a migration of resources out of legacy venues to new ones. Indeed, in the marketplace of ideas, the amplifiers of regime propaganda are failing but we also observe the response: widened censorship. What’s happening in Brazil with the full criminalization of free speech can easily happen in the US.

In social media, were it not for Elon’s takeover of Twitter, it’s hard to know where we would be. We have no large platform in which to influence the culture more broadly. And yet the attacks on that platform and other enterprises owned by Musk are growing. This is emblematic of a much more robust upheaval taking place, one that suggests change is on the way.

But how long does such a paradigm shift take? Thomas Kuhn’s “The Structure of Scientific Revolutions” is a bracing account of how one orthodoxy migrates to another not by the ebb and flow of proof and evidence but through dramatic paradigm shifts. An abundance of anomalies can wholly discredit a current praxis but that doesn’t make it go away. Ego and institutional inertia perpetuate the problem until its most prominent exponents retire and die and a new elite replaces them with different ideas.

In this model, we can expect that a failed innovation in science, politics, or technology could last as long as 70 years before finally being displaced, which is roughly how long the Soviet experiment lasted. That’s a depressing thought. If this is true, we still have another 60 plus years of rule by the management professionals who enacted lockdowns, closures, shot mandates, population propaganda, and censorship.

And yet, people say that history is moving faster now than in the past. If a future of freedom is ours just lying in wait, we need that future here sooner rather than later, before it is too late to do anything about it.

The slogan became popular about ten years ago: the revolution will be decentralized with the creation of robust parallel institutions. There is no other path.

The intellectual parlor game is over. This is a real-life struggle for freedom itself. It’s resist and rebuild or doom.

International

Fauci Adviser Secretly Messaged Zoologist Who Funneled Money to Chinese Lab: Emails

Fauci Adviser Secretly Messaged Zoologist Who Funneled Money to Chinese Lab: Emails

Authored by Zachary Stieber via The Epoch Times,

A top…

Share this:

Authored by Zachary Stieber via The Epoch Times,

A top adviser to Dr. Anthony Fauci secretly messaged a zoologist who funneled money from Dr. Fauci’s agency to a laboratory in the Chinese city where the first COVID-19 cases appeared, according to newly disclosed emails.

Peter Daszak speaks to media upon arriving at the Wuhan Institute of Virology in China's central Hubei province, on Feb. 3, 2021. (Hector Retamal/AFP via Getty Images)

Dr. David Morens, the adviser, sent at least four messages to Peter Daszak, the zoologist, the emails show. Images of the email headers were obtained and released by the U.S. House of Representatives Select Subcommittee on the Coronavirus Pandemic.

Dr. Morens, who was messaging from his personal email, wrote to Mr. Daszak, the president of EcoHealth Alliance, and others on April 26, 2020; July 13, 2020; and Feb. 20, 2022. At least three of the messages were about a grant from the U.S. National Institute of Allergy and Infectious Diseases (NIAID) to EcoHealth to study bat coronaviruses. Money from that grant was funneled by EcoHealth to the Wuhan Institute of Virology.

“Please read and acknowledge receipt -- Actions needed regarding 2R01AI110964-06,” the subject line of one message stated.

In another, Dr. Morens was responding after Mr. Daszak told him an NIAID grant officer said “he’s unable to talk with me anymore about our suspended [grant].”

The grant was suspended on April 24, 2020, by former President Donald Trump’s administration after the COVID-19 pandemic started. President Joe Biden’s administration restored funding in 2023, although it suspended and later banned the Wuhan lab from receiving money.

An inspector general determined in a 2023 report that EcoHealth and the National Institutes of Health (NIH) failed to properly monitor research being done in Wuhan. EcoHealth also failed to obtain documents the NIH requested following the emergence of COVID-19, which EcoHealth blamed on a lack of cooperation from Chinese officials. The NIH is the NIAID’s parent agency.

Dr. Morens in a previously released email said that he “retained very few emails or documents” on the origins of COVID-19 “and continue to request that correspondence on sensitive issues be sent to me at my gmail address.”

He said in another email that “I try to always communicate on gmail because my NIH email is FOIA’d constantly“ and that ”I will delete anything I don’t want to see in the New York Times.”

The newly acquired emails, sourced from a whistleblower, show “further attempts by Dr. Morens to subvert public transparency,” Rep. Brad Wenstrup (R-Ohio), chairman of the subcommittee, said on April 1

He was writing to Dr. Gerald Keusch, director of the National Emerging Infectious Diseases Laboratory Institute at Boston University.

Dr. Keusch was part of the emails between Dr. Morens and Mr. Daszak.

Dr. Wenstrup asked Dr. Keusch to provide all communications between Dr. Keusch and Dr. Morens about the origins of COVID-19, EcoHealth, or the Wuhan lab, in addition to communications between Dr. Keusch and government agencies on the same topics.

Dr. Keusch, Dr. Morens, and EcoHealth did not respond to requests for comment.

Some experts and government agencies believe that COVID-19 originated at the Wuhan lab, which was conducting risky experiments on coronaviruses. Some others favor the natural origin theory. No animal intermediary has been identified as of yet.

Dr. Morens answered questions from the House subcommittee in January. According to a readout of the interview, Dr. Morens said Mr. Daszak is a close friend. He said that he “stood with 100% certainty behind the zoonotic origin of COVID-19, ”even though he acknowledged not exploring any evidence supporting the lab theory. Dr. Morens also denied deleting material on the origins of COVID-19 or making attempts to skirt the Freedom of Information Act.

“The select subcommittee has serious questions about the legitimacy of these claims,” the panel said at the time. “Chairman Wenstrup plans to receive access to Dr. Morens’s personal email account.”

Government

Louisiana’s housing market has an insurance problem

Agents across the state are lamenting rapidly rising homeowners insurance costs that hamper clients’ purchasing power

Share this:

After heating up like the rest of the country, the Louisiana housing market has continued to cool since interest rates began to rise in the second half of 2022. While the slowdown has resulted in a return to pre-pandemic levels of market activity, real estate agents across the state believe that an issue far greater than 7% mortgage rates may cause the housing market to slow further.

“We have an insurance problem,” said Charlotte Johnson, a Keller Williams agent based in Mandeville. “Our insurance is pricing people out of their homes.”

Between 2018 and 2023, homeowners insurance rates in Louisiana jumped 24.9%, according to an analysis by S&P Global. From 2022 to 2023 alone, rates jumped 21.2%. This has been a hard pill for many homebuyers and owners to swallow.

Marx Sterbcow, a real estate lawyer and managing attorney at Sterbcow Law Group, based roughly 40 miles north of New Orleans, insurance costs have created a rapid run-up in his annual premium. He paid $4,700 in 2022, $11,500 in 2023 and received a quote of $28,000 for 2024.

“I’m not sure what else can be done to lower the costs other than to increase the deductibles. My house has never had a claim, has all the added bells and whistles to help mitigate against any potential claim,” Sterbcow said.

Although Sterbcow is relatively close to the coast in the New Orleans metro area, increasing his property’s risk for hurricane damage, the challenge of rising insurance costs is a statewide issue.

“There are some legislative issues with insurance and taxes on insurance, but there is no doubt that we have had more severe natural disasters,” said Stephen Lovecchio, the owner of the New Orleans branch of insurance firm The Woodlands Financial Group. “The insurance companies are only trying to make a nickel on every dollar, but if we have to pay out for a $100 million or $200 million storm, rates have to go up accordingly.”

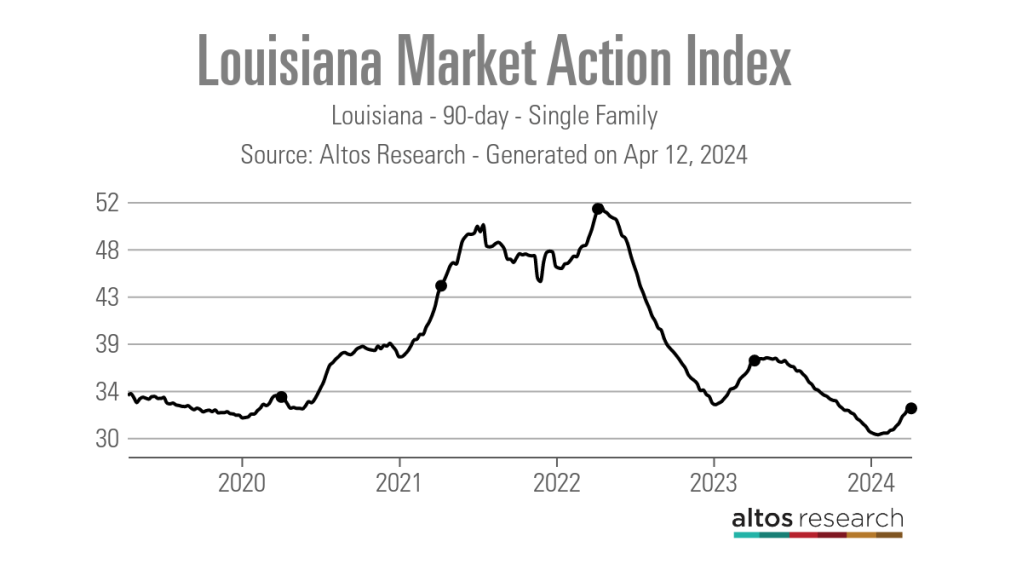

Across the state, agents feel these rising insurance costs on top of higher mortgage rates and list prices. According to Altos Research data, 90-day median list prices have risen from roughly $230,000 in April 2020 to $275,000 in early April 2024, contributing to the slowdown in home sales.

According to data from Redfin, 2,491 homes were sold in Louisiana in February 2024, down 6.2% year over year, and nearly identical to the 2,492 homes sold in February 2020 prior to the COVID-19 pandemic.

Additionally, the state’s 90-day average Altos Market Action Index score was 32.75 as of April 5, 2024 — down from 37.21 one year earlier, but nearly identical to the score of 32.77 recorded in mid-February 2020. Altos classifies scores above 30 to be indicative of a sellers’ market.

“Sellers will want top dollar for their property, but we are seeing buyers starting to look at negotiating things like closing costs or buying down their interest rate,” said Jessica Huber, a Keller Williams Realty First Choice agent based in Prairieville. “I’ve seen buyers ask for and get between $8,000 and $10,000 in closing costs covered. Prices are still higher than they were previously, but at least in my area, sellers are working with buyers.”

Another indicator of the slower market conditions is the statewide rise in inventory. After the 90-day average reached a floor of 5,010 single-family active listings in mid-April 2022, it has increased to 12,028 as of early April 2024. In comparison, statewide inventory was at 14,129 active listings in mid-February 2020.

While inventory is clearly headed in the right direction, local agents say that it is still hard for buyers at certain price points to find quality listings.

“Inventory feels pretty balanced,” said Josh Foster, an EXIT Realty Southern agent based in Sulphur. “I think we are running close to about a six-month supply, but one of the things we are still running into is that there is still not a lot of homes in that sweet spot for most buyers — right at the $200,000 to $300,000 mark, two acres with three or four bedrooms. It’s just not out there.”

With these “sweet spot”-type properties, when one does come on the market, Foster said he has seen some multiple-offer situations, but nothing like the post-pandemic surge of 2020 and 2021.

With transaction volume slowing, agents are doing everything they can to make sure the deals they have close successfully. For most, this means bringing a homeowners insurance agent into the transaction much sooner than they used to.

“Now we are getting the insurance quote before we even submit an offer on a house, so that they know what their total payment is going to be,” Johnson said. “It is a lot more legwork than before, but at least we know before we make an offer if the client can even afford their monthly payment, or even if they can get the mortgage because the insurance premium will impact their debt-to-income ratio.”

In addition to helping current buyers, agents are also working with past clients to help them manage their homeowners insurance costs.

“I’ve had people call me to list their house because they can no longer afford their insurance. So, I have been teaching people about the need to shop around for insurance,” Johnson said. “I’ve been fortunate that I’ve been able to help them find better rates so that they can stay in their home. Your insurance company doesn’t have to be your insurance company forever.”

Although the insurance challenges facing Louisiana’s real estate market will not disappear overnight, agents are hopeful for the future. Under current state laws, insurance carriers are banned from dropping homeowners who have been customers for at least three years.

In late March, however, the Louisiana House of Representatives voted to allow insurance companies more leeway in dropping homeowner policies. The bill still needs to be passed by the state Senate, but agents are hopeful the change would entice more carriers to offer coverage in higher-risk areas, giving homeowners and buyers more choices.

“The reinsurers see this rule and they don’t want to be part of things in Louisiana — they don’t want to come here,” Johnson said. “So, we have a situation where we don’t have competition and so that is driving up the prices even higher.”

Lovecchio also noted that he expects insurance premiums to decline in the coming years.

“The new insurance commissioner is allowing companies to raise and lower rates a lot quicker, so hopefully consumers will see less lag time on their rate changes,” Lovecchio said.

“I think prices will moderate a bit moving forward. We’ve seen them stop going up, so that is good — it is the first step. But we also hope some more carriers will enter our markets and bring them lower because we really need rates to go down.”

home sales mortgage rates real estate housing market pandemic covid-19 senate house of representatives interest ratesInternational

The idea that US interest rates will stay higher for longer is probably wrong

A gap has opened up between inflation in the US compared to other regions like Europe and China.

Share this:

{kind=link}

{kind=link}

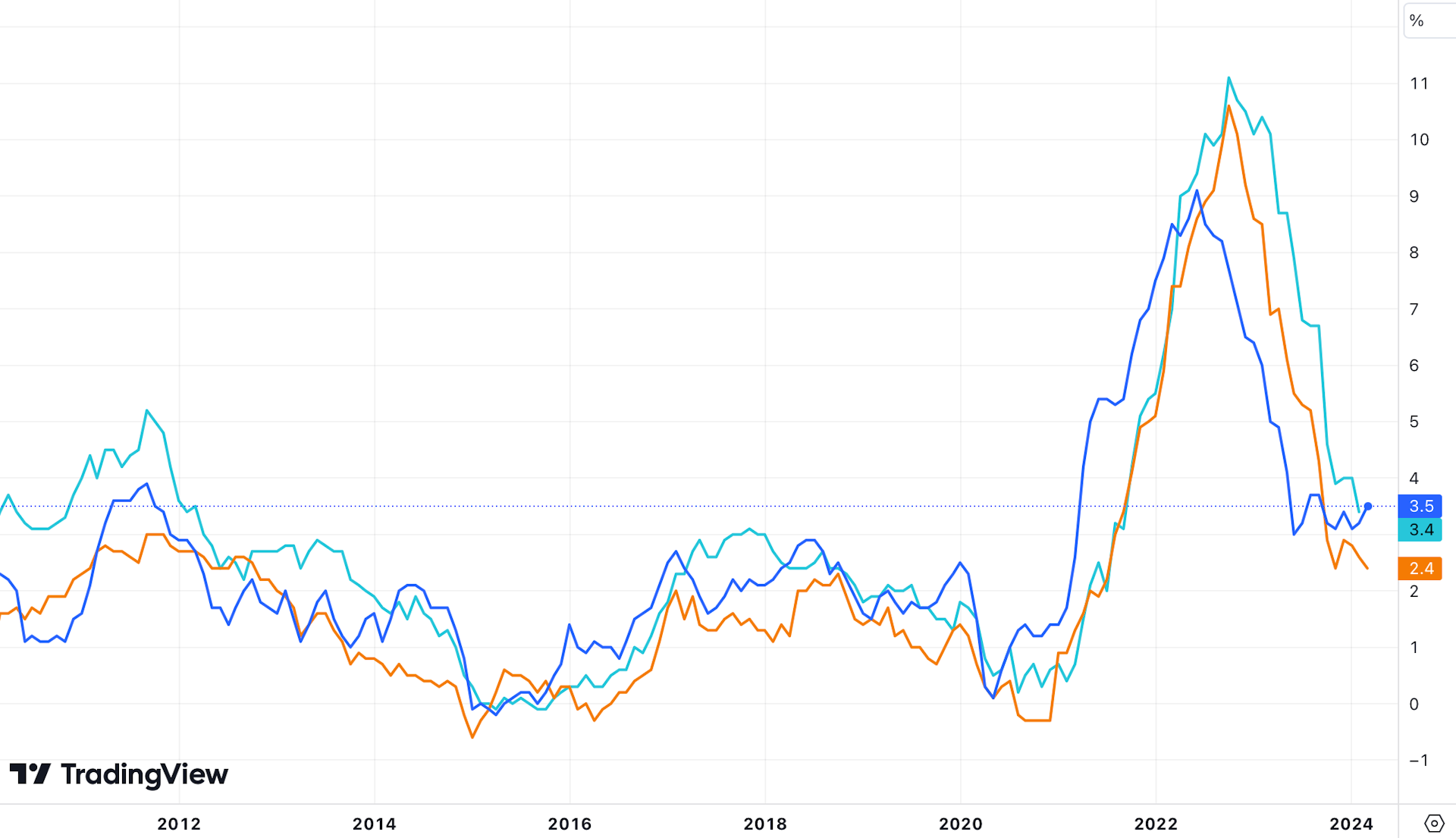

The 0.4% rise in US consumer prices in March didn’t look like headline news. It was the same as the February increase, and the year-on-year rise of 3.5% is still sharply down from 5% a year ago.

All the same, this modest uptick in annual inflation from 3.2% in February has cast doubt on whether the US central bank, the Federal Reserve, can afford to cut headline interest rates as fast as it has been signalling. To further complicate matters, a gap has opened up between the US inflation rate and that of other regions, notably the EU.

US inflation vs EU and UK

{kind=link}

Financial markets’ instant reaction was bearish. They dumped stocks while buying EU government bonds, in expectation of a boost from the European Central Bank cutting its rates sooner. They also bought the US dollar, anticipating it will strengthen when European rates come down. But how is this likely to play out?

Can they all be right?

The US economy has returned to steady expansion after the COVID-19 pandemic disruption of 2020-22, while Europe is struggling to achieve any growth. This helps to explain the difference in the inflation figures.

The strength of the US economy was already putting pressure on the Fed to cut less quickly. A higher interest rate helps to stop strong demand straining supply chains and making prices rise too fast. The quickening of consumer-price inflation gives the Fed an added incentive to be hawkish on rates – to convince businesses and households that it will keep monetary conditions tight until inflation falls back to the 2% target.

The interest rates on advance purchases of US debt (the “Fed futures” market) show that a majority of traders now expect the Fed will not drop its interest rate from the current level (of 5.25% to 5.5%) to below 5% until December. A week ago, most thought this would have happened by September.

The trouble is that an extended period of higher rates could be very damaging because there’s so much debt in the system. In particular, last year’s wobbles in the US banking sector, and wider concerns about institutional investors exposed to a slump in commercial real estate, are strong incentives to reduce credit costs before too long.

Consequently, few believe the US headline interest rate will still be at present levels a year from now. Yet the longer that inflation endures, the more the pressure to delay further rate cuts. Most Americans now believe inflation will stay around 3% for the next year, an expectation echoed in markets for assets viewed as protecting against inflation (such as gold and cryptocurrencies).

Election-year inflation dangers

An especially fraught presidential election race also limits the Fed’s manoeuvring room. The White House has pitched its 2024-25 federal budget as helping to subdue inflation, by lowering working families’ living costs and forcing companies to pass-on cost savings.

But while Joe Biden aims to spend US$7.3 trillion (£5.8 trillion) in pursuit of his plans, congressional opponents are likely to block many of the tax increases intended to pay for them.

That’s likely to mean a continued widening of the US federal deficit, injecting more demand and keeping up inflationary pressure. That pressure could be worsened by the punitive tariffs that Republicans want to impose on cheap imports, to which many Democrats are sympathetic. An increasingly bipartisan push for tighter border controls would also raise US inflation risk, by stemming the inflow of cheap labour that has kept unskilled wages down.

US federal deficit

The case for cutting anyway

Despite these caveats, financial markets could well still be proved wrong about the speed of US rate cuts. Besides the private-sector debt concerns, one additional potential justification for cutting sooner actually relates to inflation. While central banks respect the conventional wisdom that higher interest rates reduce inflation, they cannot disregard evidence that the effect may be reversed if rates are kept high for too long.

When businesses expect interest rates to stay high, they raise prices to compensate, especially if heavier debt repayments spur employees to ask for more pay. Notably, the rising cost of mortgages in the US was one of the factors in March’s inflation surprise. The Fed can best tackle this by maintaining the assurance of lower interest rates, so that accommodation costs can fall.

Meanwhile, China is grappling with falling prices, which can do even worse damage than an inflation overshoot. There is still a possibility of China trying to escape this situation by flooding the world with cheap goods, and energy costs falling sharply when the Russia-Ukraine war ends. This would leave central banks in Europe and America concerned to stop their inflation falling too far, by cutting rates faster than the market currently expects.

The Fed must finally factor in the global downside of holding firm while other central banks’ interest rates fall. This would deal a double blow to the many countries, and non-US companies, that have borrowed in US dollars to finance their expansion plans. They would pay relatively more on their dollar debt, while their local currency revenues would buy fewer dollars, since the dollar strengthens as US interest rates move relatively higher.

The dollar’s global reach means that if the Fed doesn’t let headline rates fall, it could exacerbate a global slowdown. That would rebound against American producers, especially those now reliant on Europe, Latin America and Asia as major export markets. So when the ECB cuts rates, the Fed can be still expected to follow, even if it means US inflation remaining above target into 2025. This could mean another boost to stock prices, fresh incentives to borrow more money, and greater instability for the years ahead.

Alan Shipman does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

bonds government bonds pandemic covid-19 stocks fed federal reserve real estate mortgages us dollar white house tariffs interest rates gold european europe uk russia ukraine eu china

What millennials and gen Z professionals need to know about developing a meaningful career

Silver and Gold: The Winning Bet

Tracking ticks in Georgia to help monitor emerging diseases

Jim Jordan Investigating Renewed DOJ, FBI Contacts With Big Tech, Amid Concerns Of Censorship Pressure

Immigration And Its Impact On Employment

How the national living wage helps the UK’s poorest households: new research

How Ivermectin Trials Were Designed To Fail

New government guidance for PE lets teachers and pupils down

A small robot car can reduce children’s stress before surgery

Cyclical Rally Could Look Very Different From Here

-

International3 weeks ago

International3 weeks agoParexel CEO to retire; CAR-T maker AffyImmune promotes business leader to chief executive

-

Spread & Containment1 month ago

Spread & Containment1 month agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Government6 days ago

Government6 days agoClimate-Con & The Media-Censorship Complex – Part 1

-

Spread & Containment4 days ago

Spread & Containment4 days agoFDA Finally Takes Down Ivermectin Posts After Settlement

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoVaccinated People Show Long COVID-Like Symptoms With Detectable Spike Proteins: Preprint Study

-

Uncategorized1 week ago

Uncategorized1 week agoCan language models read the genome? This one decoded mRNA to make better vaccines.

-

Uncategorized5 days ago

Uncategorized5 days agoWhat’s So Great About The Great Reset, Great Taking, Great Replacement, Great Deflation, & Next Great Depression?

-

International3 weeks ago

International3 weeks agoJapanese Preprint Calls For mRNA VaccinesTo Be Suspended Over Blood Bank Contamination Concerns