Wells Fargo: 2 Big 16% Dividend Stocks to Buy (And 1 to Avoid)

Wells Fargo: 2 Big 16% Dividend Stocks to Buy (And 1 to Avoid)

Share this:

The coronavirus epidemic, and the economic and society lockdowns put in place to combat it, have body-slammed the financial world; the S&P 500 is still down 13% even after a 5 week rally, while oil prices are stuck in a doldrums, with Brent trading at just $30 and WTI at $25. Corporate earnings season has been grim, and some 120 S&P companies have rescinded their 2020 guidance while others have canceled dividend payments or stock buybacks.

So, investors are confused; they aren’t seeing the usual signals that indicate what the market may do, and opinions are deeply divided on whether we’ll see a true rally or a long-term bear cycle.

Writing from Wells Fargo, head of equity strategy Chris Harvey has come down on the bearish side, but with a caveat. “A near-term equity market pullback should not be unexpected – but we believe selloffs will be much shallower than those in the recent past,” he says, and goes on to add, “There still is substantial uncertainty, and the path forward is not set in stone. Market participants are deciphering shades of gray and for now we are accepting of data that is merely less bad.”

Looking at possible ways forward, Harvey expects that the ‘shallower’ selloff will find support from dividend stocks. He’s predicting that the equity market’s current upward trend has pushed the dividend future contract up towards $50. He does not expect dividend stocks to falter in CY20; they are the logical defensive move for investors seeking to remain in the market while protecting their income stream.

Harvey’s colleagues at Well Fargo are extrapolating from his general stance, and applying it to individual stocks. In a series of reports, the firm’s stock analysts outlined some low-cost, high-return dividend stocks that investors need to consider – and also one that may be too risky to try. We’ve pulled the details from the TipRanks database, so let’s find out what makes these stock moves so compelling.

Energy Transfer LP (ET)

We’ll start in the energy sector, where strong dividends are common. The collapse of oil prices – America’s WTI benchmark dipped into negative territory for the first time ever on April 20 – hurt the industry, but there is still some resilience there. Energy is a non-negotiable requirement in modern society, and there is always current demand for hydrocarbon products. Energy Transfer, a midstream company, is well positioned to take advantage of hydrocarbon demand; it controls pipelines, terminals, and storage tanks for both crude oil and natural gas in 38 states. The company operates mainly in the Texas-Oklahoma-Louisiana and Midwest-Appalachian regions.

ET finished 2019 with a solid earnings report, beating both the EPS and revenue expectations while growing both metric year-over-year. Heading into Q1, the company had also increased its distributable cash flow by 2%, to $1.55 billion, an excellent signal for dividend investors. The company will report Q1 this evening, and the outlook is for 32 cents EPS, down 15.7% sequentially. At the same time, the revenue forecast is looking at a 6.8% yoy increase to $14.02 billion.

The cash flow is likely to be the more important figure, as far as investors are concerned. ET has been keeping up reliable payments for the last eleven years, and the current quarterly dividend, of 30.5 cents, is set for payment on May 19. The current payout ratio is high but still affordable – and even if earnings drop to the expected 32 cents, the company will still be able to cover the dividend payment. And at 16%, the dividend yield is simply stellar – far higher than the 2% average among S&P listed companies.

Analyst Michael Blum reviewed this stock for Wells Fargo, and took a clearly bullish position. Blum rates ET shares a Buy, with a $12 price target that suggests an impressive 59% upside potential for the coming year. (To watch Blum’s track record, click here)

Supporting his stance on ET, Blum looks to the long-term and writes, “[H]ydrocarbon use will [not] dramatically decrease within the next ten years (and beyond) and thus, [we are] not concerned with obsolescence risk for its pipeline assets. The company would consider renewable investments if they met ET’s return thresholds. However, to date, returns for renewable projects are below that of midstream.”

Overall, the analyst consensus on ET is a Moderate Buy, based on 13 recent reviews. The breakdown among those reviews skews positive, with 8 Buys versus 5 Holds. Shares are selling for $7.64, and the average price target of $11.85 implies an upside of 55%. (See ET stock analysis on TipRanks)

MPLX LP (MPLX)

Staying in the energy industry, we’ll look at MPLX. This company was spun off of Marathon Petroleum in 2012, to handle the oil giant’s midstream operations. Marathon still holds a controlling interest in MPLX, which in turn owns and operates assets in pipelines, terminals, inland river shipping, and refineries. MPLX operates in both the petroleum and natural gas midstream segments.

MPLX has a seven-year history of growing its dividend, and the current payment of 68.75 cents per quarter is due out on May 15. Annualized, the dividend comes to $2.75 and gives a yield of 16%. Compared to current interest rates, which have been slashed to the bone in an attempt to counter the economic hit from the coronavirus shutdowns, this yield is a clear attraction for investors.

The dividend is supported by a cash-rich business model. MPLX generated $4.1 billion in net cash during calendar year 2019, and returned $2.8 billion to shareholders through dividends and buybacks. The company has reduced its capital spending for 2020 to compensate for reduced income during the 1H20 economic downturn. The company a heavy net loss for Q1, of $2.7 billion, but still was able to generate $1 billion net cash.

Michael Blum, quoted above, also cast his gaze on MPLX. He wrote, “We entered 2020 with a defensive mindset... We continue to expect near-term volatility as crude storage fills and WTI oil prices likely head lower… the sector is technically oversold, which should create long-term buying opportunities for investors that have the wherewithal to step in... for investors with a bit more risk appetite, [MPLX] appears attractive on a multi-year time horizon…”

In line with this stance, Blum gives MPLX a Buy rating. His $24 price target implies a strong upside potential here of 38%.

For the most part, Wall Street appears to agree with Blum on MPLX. The stock has received 11 recent reviews, of which 8 are Buys and 3 are Holds, making the analyst consensus rating a Moderate Buy. Shares are currently trading for $17.72, while the average price target of $21.80 suggests a one-year upside potential of 23%. (See MPLX stock analysis on TipRanks)

Bain Capital Specialty Finance (BCSF)

The world of business development companies (BDCs) has long sparked the interest of investors. These companies invest capital into the business world, earning their own profits on the returns. Bain has $105 billion in assets under management, in real estate, venture capital, and both private and public equity. Current economic conditions have hit Bain hard, as many of the company’s portfolio assets are underperforming due to the coronavirus shutdowns.

Despite volatile earnings, Bain is maintaining its dividend. The 41-cent dividend is sustainable at current earnings levels, and has been held steady for the past six quarter – but the payout ratio of 93% indicates that there is not much slack here. The yield, however, is 15.6%, so for investors willing to shoulder the risk, the reward may be substantial.

Well Fargo analyst Finian O’Shea sees too much risk here to justify the possible reward. The analyst points out that BCSF has started process to open up a rights offering, putting common stock at a discount. This is a move to raise new capital fast, and shows softness in the stock’s position. O’Shea writes, “…this is the first of what the market speculates as a wave of below-NAV issuance in the BDC industry. We don’t see a big wave noting BCSF was more leveraged, at 1.72x net including revolvers as of 12/31 – so there was not a lot of mark to market leeway.”

To this end, O’Shea rates the stock a Sell, predicting it will underperform in the coming year. In line with this, O’Shea cut the price target by nearly half, to $9.50, suggesting an 11% downside from current levels. (To watch O’Shea’s track record, click here)

The Wall Street analyst corps, generally, are cautious on this stock. The consensus rating, a Hold, is based on a single Buy along with 2 Holds and 1 Sell. The upside is also modest; the average price target of $10.67 indicates room for just 0.66% growth from the $10.60 share price. (See Bain Capital stock analysis on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

The post Wells Fargo: 2 Big 16% Dividend Stocks to Buy (And 1 to Avoid) appeared first on TipRanks Financial Blog.

International

United Airlines adds new flights to faraway destinations

The airline said that it has been working hard to "find hidden gem destinations."

Share this:

Since countries started opening up after the pandemic in 2021 and 2022, airlines have been seeing demand soar not just for major global cities and popular routes but also for farther-away destinations.

Numerous reports, including a recent TripAdvisor survey of trending destinations, showed that there has been a rise in U.S. traveler interest in Asian countries such as Japan, South Korea and Vietnam as well as growing tourism traction in off-the-beaten-path European countries such as Slovenia, Estonia and Montenegro.

Related: 'No more flying for you': Travel agency sounds alarm over risk of 'carbon passports'

As a result, airlines have been looking at their networks to include more faraway destinations as well as smaller cities that are growing increasingly popular with tourists and may not be served by their competitors.

Shutterstock

United brings back more routes, says it is committed to 'finding hidden gems'

This week, United Airlines (UAL) announced that it will be launching a new route from Newark Liberty International Airport (EWR) to Morocco's Marrakesh. While it is only the country's fourth-largest city, Marrakesh is a particularly popular place for tourists to seek out the sights and experiences that many associate with the country — colorful souks, gardens with ornate architecture and mosques from the Moorish period.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

"We have consistently been ahead of the curve in finding hidden gem destinations for our customers to explore and remain committed to providing the most unique slate of travel options for their adventures abroad," United's SVP of Global Network Planning Patrick Quayle, said in a press statement.

The new route will launch on Oct. 24 and take place three times a week on a Boeing 767-300ER (BA) plane that is equipped with 46 Polaris business class and 22 Premium Plus seats. The plane choice was a way to reach a luxury customer customer looking to start their holiday in Marrakesh in the plane.

Along with the new Morocco route, United is also launching a flight between Houston (IAH) and Colombia's Medellín on Oct. 27 as well as a route between Tokyo and Cebu in the Philippines on July 31 — the latter is known as a "fifth freedom" flight in which the airline flies to the larger hub from the mainland U.S. and then goes on to smaller Asian city popular with tourists after some travelers get off (and others get on) in Tokyo.

United's network expansion includes new 'fifth freedom' flight

In the fall of 2023, United became the first U.S. airline to fly to the Philippines with a new Manila-San Francisco flight. It has expanded its service to Asia from different U.S. cities earlier last year. Cebu has been on its radar amid growing tourist interest in the region known for marine parks, rainforests and Spanish-style architecture.

With the summer coming up, United also announced that it plans to run its current flights to Hong Kong, Seoul, and Portugal's Porto more frequently at different points of the week and reach four weekly flights between Los Angeles and Shanghai by August 29.

"This is your normal, exciting network planning team back in action," Quayle told travel website The Points Guy of the airline's plans for the new routes.

stocks pandemic south korea japan hong kong europeanInternational

Walmart launches clever answer to Target’s new membership program

The retail superstore is adding a new feature to its Walmart+ plan — and customers will be happy.

Share this:

It's just been a few days since Target (TGT) launched its new Target Circle 360 paid membership plan.

The plan offers free and fast shipping on many products to customers, initially for $49 a year and then $99 after the initial promotional signup period. It promises to be a success, since many Target customers are loyal to the brand and will go out of their way to shop at one instead of at its two larger peers, Walmart and Amazon.

Related: Walmart makes a major price cut that will delight customers

And stop us if this sounds familiar: Target will rely on its more than 2,000 stores to act as fulfillment hubs.

This model is a proven winner; Walmart also uses its more than 4,600 stores as fulfillment and shipping locations to get orders to customers as soon as possible.

Sometimes, this means shipping goods from the nearest warehouse. But if a desired product is in-store and closer to a customer, it reduces miles on the road and delivery time. It's a kind of logistical magic that makes any efficiency lover's (or retail nerd's) heart go pitter patter.

Walmart rolls out answer to Target's new membership tier

Walmart has certainly had more time than Target to develop and work out the kinks in Walmart+. It first launched the paid membership in 2020 during the height of the pandemic, when many shoppers sheltered at home but still required many staples they might ordinarily pick up at a Walmart, like cleaning supplies, personal-care products, pantry goods and, of course, toilet paper.

It also undercut Amazon (AMZN) Prime, which costs customers $139 a year for free and fast shipping (plus several other benefits including access to its streaming service, Amazon Prime Video).

Walmart+ costs $98 a year, which also gets you free and speedy delivery, plus access to a Paramount+ streaming subscription, fuel savings, and more.

If that's not enough to tempt you, however, Walmart+ just added a new benefit to its membership program, ostensibly to compete directly with something Target now has: ultrafast delivery.

Target Circle 360 particularly attracts customers with free same-day delivery for select orders over $35 and as little as one-hour delivery on select items. Target executes this through its Shipt subsidiary.

We've seen this lightning-fast delivery speed only in snippets from Amazon, the king of delivery efficiency. Who better to take on Target, though, than Walmart, which is using a similar store-as-fulfillment-center model?

"Walmart is stepping up to save our customers even more time with our latest delivery offering: Express On-Demand Early Morning Delivery," Walmart said in a statement, just a day after Target Circle 360 launched. "Starting at 6 a.m., earlier than ever before, customers can enjoy the convenience of On-Demand delivery."

Walmart (WMT) clearly sees consumers' desire for near-instant delivery, which obviously saves time and trips to the store. Rather than waiting a day for your order to show up, it might be on your doorstep when you wake up.

Consumers also tend to spend more money when they shop online, and they remain stickier as paying annual members. So, to a growing number of retail giants, almost instant gratification like this seems like something worth striving for.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic mexicoUncategorized

Comments on February Employment Report

The headline jobs number in the February employment report was above expectations; however, December and January payrolls were revised down by 167,000 combined. The participation rate was unchanged, the employment population ratio decreased, and the …

Share this:

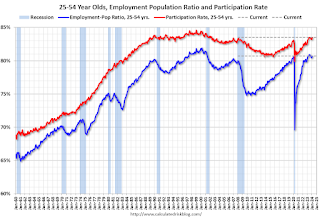

Prime (25 to 54 Years Old) Participation

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

{kind=link}

The 25 to 54 years old participation rate increased in February to 83.5% from 83.3% in January, and the 25 to 54 employment population ratio increased to 80.7% from 80.6% the previous month.

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES). Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 4.3% YoY in February.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of people employed part time for economic reasons, at 4.4 million, changed little in February. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons decreased in February to 4.36 million from 4.42 million in February. This is slightly above pre-pandemic levels.

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 7.3% from 7.2% in the previous month. This is down from the record high in April 2020 of 23.0% and up from the lowest level on record (seasonally adjusted) in December 2022 (6.5%). (This series started in 1994). This measure is above the 7.0% level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.203 million workers who have been unemployed for more than 26 weeks and still want a job, down from 1.277 million the previous month.

This is close to pre-pandemic levels.

Job Streak

| Headline Jobs, Top 10 Streaks | ||

|---|---|---|

| Year Ended | Streak, Months | |

| 1 | 2019 | 100 |

| 2 | 1990 | 48 |

| 3 | 2007 | 46 |

| 4 | 1979 | 45 |

| 5 | 20241 | 38 |

| 6 tie | 1943 | 33 |

| 6 tie | 1986 | 33 |

| 6 tie | 2000 | 33 |

| 9 | 1967 | 29 |

| 10 | 1995 | 25 |

| 1Currrent Streak | ||

Summary:

The headline monthly jobs number was above consensus expectations; however, December and January payrolls were revised down by 167,000 combined. The participation rate was unchanged, the employment population ratio decreased, and the unemployment rate was increased to 3.9%. Another solid report.

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Redefining Poverty: Towards a Transpartisan Approach

Catastrophic Risk: Investing and Business Implications

The Digest #187

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Interest rates, the best it gets. It’s time to deploy cash

Deterra Royalties half-yearly result: stable performance and growth Initiatives

Deflationary pressures in China – be careful what you wish for

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges