Government

“We Have 15,000 Samples In Wuhan … Could Do Full Genomes Of 700 CoVs”: Rand Paul Drops COVID Bombshell

"We Have 15,000 Samples In Wuhan … Could Do Full Genomes Of 700 CoVs": Rand Paul Drops COVID Bombshell

Last week Senator Rand Paul (R-KY)…

Share this:

Last week Senator Rand Paul (R-KY) wrote in a Tuesday op-ed that officials from 15 federal agencies "knew in 2018 that the Wuhan Institute of Virology was trying to create a coronavirus like COVID-19."

These officials knew that the Chinese lab was proposing to create a COVID 19-like virus and not one of these officials revealed this scheme to the public. In fact, 15 agencies with knowledge of this project have continuously refused to release any information concerning this alarming and dangerous research.

Government officials representing at least 15 federal agencies were briefed on a project proposed by Peter Daszak’s EcoHealth Alliance and the Wuhan Institute of Virology. -Rand Paul

Paul was referring to the DEFUSE project, which was revealed after DRASTIC Research uncovered documents showing that DARPA had been presented with a proposal by EcoHealth Alliance to perform gain-of-function research on bat coronavirus.

New documents released by Drastic Research show Peter Daszak and the EcoHealth Alliance had applied for funds that would allow them to further modify coronavirus spike proteins and find potential furin cleavage sites.

— Rep. Gallagher Press Office (@RepGallagher) September 23, 2021

Rep. Gallagher explains why that's so important. pic.twitter.com/6aEPyuW7Go

Now, Paul points to an email between EcoHealth's Daszak and "Fauci Flunky" David Morens from April 26, 2020 (noted days before by the House Select Subcommittee on the Coronavirus Pandemic), when the lab-leak hypothesis was gaining traction against Fauci - who funded EcoHealth research in Wuhan, and Daszak's orchestrated denials and the forced "natural origin" narrative.

In it, Daszak laments the "real and present danger that we are being targeted by extremists" (for pointing out that they were manipulating bat covid down the street from where a bat covid pandemic broke out), and called Donald Trump "shockingly ignorant."

He also told David that he would restrict communications "to gmail from now on," and planned to mount a response to an NIH request which appears to suggest moving out of Wuhan - to which Daszak says "Even that would be a loss - we have 15,000 samples in freezers in Wuhan and could do the full genomes of 700+ Co Vs we've identified if we don't cut this thread."

"... and could do the full genomes of 700+ CoVs [coronaviruses]"

— Rand Paul (@RandPaul) April 16, 2024

Which means Daszak, funded by Fauci, lied when he said "every single one of the SARSr-CoV sequences @EcoHealthNYC discovered in China is already published."

In 2016 Peter Daszak (the man Fauci’s NIH was funding) openly talked about the gain of function research being done in China.

— MAZE (@mazemoore) April 9, 2024

The research Fauci said never happened.

Daszak actually talked about creating a killer virus. pic.twitter.com/iYseialw6Z

Daszak lies even when the facts are in full view and the lies are obvious.

— Richard H. Ebright (@R_H_Ebright) April 13, 2024

He has no shame, and he has no decency.

And Anthony Fauci concealed the '700 unknown coronaviruses' in Wuhan.

Nor did Fauci ever publicly admit COVID-19 could have been one of those 700 unknowns.

— Rand Paul (@RandPaul) April 16, 2024

Meanwhile, an EcoHealth progress report referenced "two chimeric bat SARS-like CoVs constructed on a WIV-1 backbone."

— Rebecca (@Rebecca21951651) April 13, 2024

About that Gmail thing...

Have you also subpoenaed their Gmail accounts? https://t.co/s03cElB0Cv pic.twitter.com/ZDvpwCHsAp

— zerohedge (@zerohedge) April 17, 2024

This is crazy

— Elon Musk (@elonmusk) April 16, 2024

Crazy indeed!

Amazing! Imagine masquerading as a hero during a pandemic that killed millions that he helped create. Then he had the audacity to harm more with a vaccine and blame the unvaccinated for the pandemic. The more the pieces come together, the more evil this man looks. And I thought…

— Emily (@eekymom) April 16, 2024

Fauci Funded Seamless Ligation, a Technique Used for HIDING Human Fingerprints on Lab-Created Bugs

— ????·Bryne (@riss1130) April 16, 2024

pic.twitter.com/zmoaXncDd3

International

Semi Shock: ASML Craters As Orderbook Plummets After China Frontrunning Ends With A Bang

Semi Shock: ASML Craters As Orderbook Plummets After China Frontrunning Ends With A Bang

Exactly three months ago, AI stocks were soaring,…

Share this:

Exactly three months ago, AI stocks were soaring, semiconductor names were flying and the tech sector was euphoric after Dutch chip giant ASML - the world’s sole producer of equipment needed to make the most advanced chips and Europe’s most valuable technology company - reported a record surge in its orderbook (just days after its Asian peer Taiwan Semi did the same)...

... and which the market immediately concluded, in its infinite stupidity, that this was the definitive confirmation of a flood of demand for AI chips and infrastructure with Bloomberg pouring oil on the fire, saying that the ASML results were "a sign that the semiconductor industry may be recovering" adding that "chipmakers are increasingly optimistic the sector’s outlook following a slump that dates back to the Covid-19 pandemic, with TSMC last week projecting strong revenue growth in 2024."

Not so fast, we countered and as we clearly warned in a January article titled "Tech Euphoria Sparked By ASML Surge To All-Time High On Flood Of Chinese Orders... There's Just One Problem"...

Tech Euphoria Sparked By ASML Surge To All-Time High On Flood Of Chinese Orders... There's Just One Problem https://t.co/ScGoWO2Ayy

— zerohedge (@zerohedge) January 24, 2024

... the reason for the surge in ASML orders was that China, and its proxies in Taiwan and other Asian countries, has been flooding the market with chip purchase orders ahead of Biden's escalating China chip sanctions, knowing that the door is closing amid a barrage of sanctions limiting exports of high tech chips - and chipmaking devices - and that it needs to buy today what it may need for the next few years, if not indefinitely. (as explained in "Behind The Tech Meltup: A One-Time Chinese Chip Buying Frenzy To Frontrun Export Curbs").

And sure enough, China accounted for 39% of ASML’s sales in the fourth quarter and became the Veldhoven-based company’s largest market in 2023! Before speculation of chip sanctions, China accounted for only 8% in January to March.

So what? Well, such one-time buying spurts are - as the name implies - one-time... and as we reported 3 months ago, ASML has been targeted by the US effort to curb exports of cutting-edge technology to China, and Bloomberg reported that ASML exports to China have now effectively been halted, vaporizing whatever portion of the order backlog is thanks to China. This led us to conclude the following:

And so with China now scrubbed from the list of ASML clients - forget being its top customer - the question is who will fill the void. Luckily, demand for AI is keeping the chip sector afloat... or so the experts say, the same experts who fawned over ASML's result today which sparked a buying frenzy in the shares, which soared over 9% today, the biggest increase since November 2022, and hitting an all time high.

Good luck keeping that all time high with your largest customer now barred from future purchases by the State Department. As for "record AI chip demand", this quarter will prove very informative how much is real and how much is vapor once the volatility from China's erratic orderflow is finally removed.

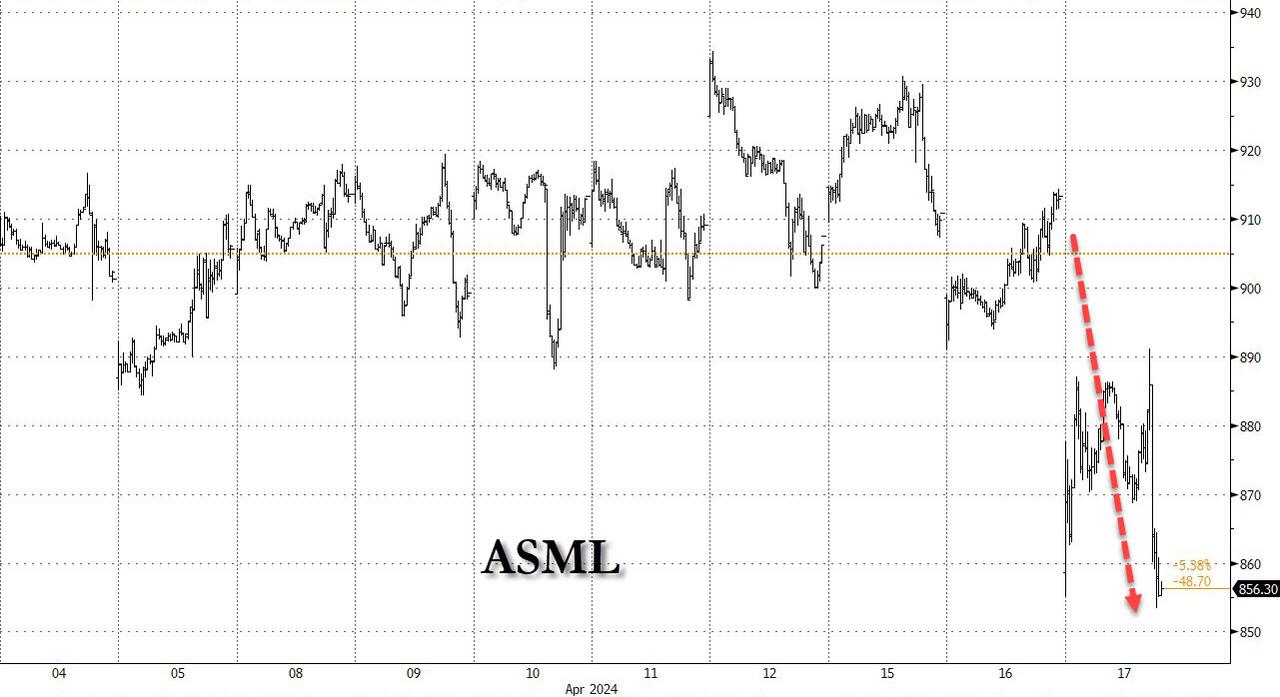

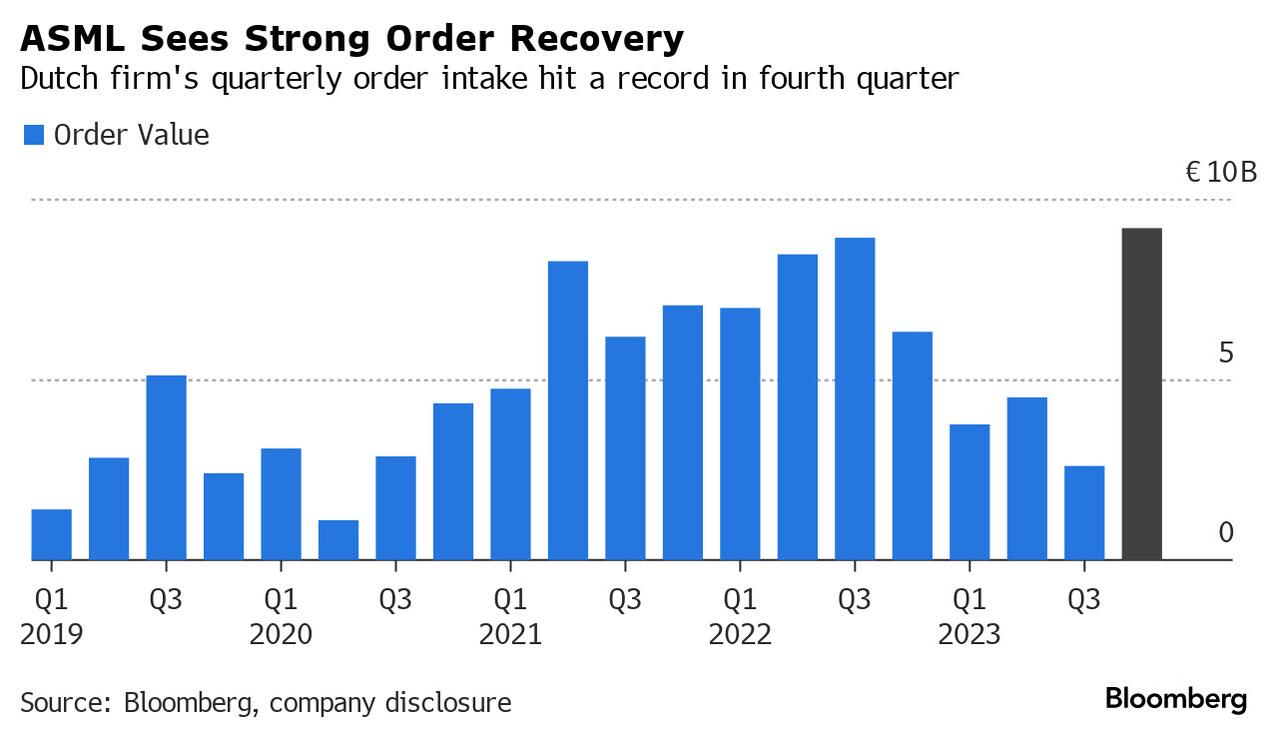

So fast forward three months when "this quarter" is now in the history books, and this morning we got confirmation that everything we said was correct (and that the market, in its infinite stupidity wisdom, was wrong. Case in point: on Wednesday, ASML stock was one of the worst performers among the European tech sector, after the largest European company posted orders that fell short of analysts’ expectations, as Taiwanese chipmakers held off buying the Dutch firm’s most advanced machines.

Bookings at Europe’s most valuable technology firm fell 61% in the first quarter from the previous three months to €3.6 billion ($3.8 billion), wildly missing the market's ridiculous estimates of €4.63 billion, just as we said it would.

As Bloomberg notes, the world's top chipmakers like Taiwan Semi and Samsung Electronics held off new orders as manufacturer clients work through stockpiles of hardware used in smartphones, computers and cars. That’s hurting ASML, which also forecast sales this quarter below analyst expectations. And why did TSMC and Samsung over-order? Simple: they too, were expecting the flood of Chinese last-ditch orders, and were looking to frontrun it.

Well they did... and now everyone has a huge surplus of equipment!

Investors had expected TSMC to book significant EUV tools in the first quarter, according to Redburn Atlantic analyst Timm Schulze-Melander (but not according to ZeroHedge). The disappointment in orders leaves earnings and revenue for next year “vulnerable,” he said, confirming what we said one quarter ago when everyone was rushing to buy the stock on a one-off surge in orders.

The level of EUV orders is “extremely low,” indicating major ASML clients like TSMC, Samsung and Intel didn’t increase investments in the high-end equipment, Oddo BHF analyst Stephane Houri said. ASML saw the biggest slump in demand for its top-end extreme ultraviolet machines. Orders for them plunged to €656 million in the period from €5.6 billion in the previous quarter.

In other words, the frontrunning of China's order book is now dead and buried.

And now comes the hangover, ASML now sees sales in the current quarter between €5.7 billion and €6.2 billion, missing estimates of €6.5 billion before demand picks up. And while the company scrambled to reassure the market that "nothing is fucked here", and pushed demand into the second half as every company does when it misses quarterly expectations...

“Our outlook for the full year 2024 is unchanged, with the second half of the year expected to be stronger than the first half, in line with the industry’s continued recovery from the downturn,” Chief Executive Officer Peter Wennink said in a statement Wednesday. “We see 2024 as a transition year.”

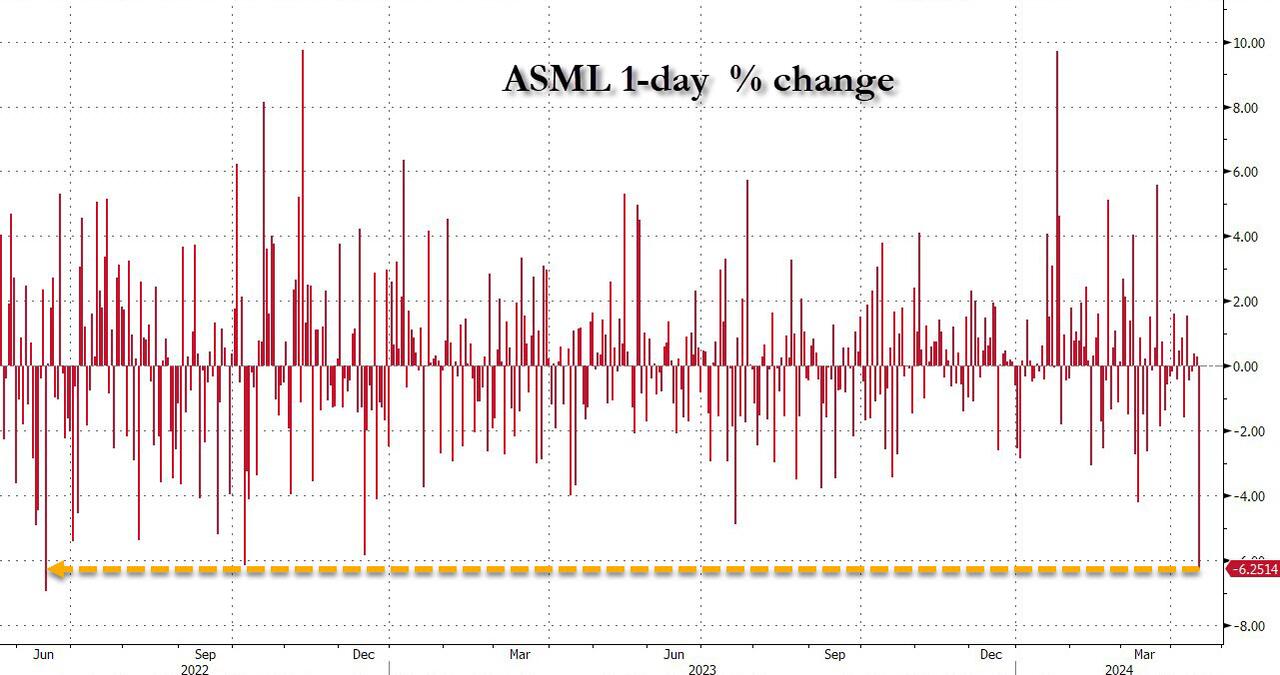

... the market was less than willing to buy the BS this time, and with the company admitting that as much as 15% of China sales this year will be affected by the new export control measures - 50% is a more realistic number - the stock finally tumbled as the hangover finally arrives, if with a three month delay, and today the stock tumbled more than 6%....

... the biggest one day drop since last June.

International

EM Debt 2024: Solid Beginnings

Emerging markets (EM) debt performed well in the first quarter of 2024, and we anticipate more of the same in the next quarter, thanks to a benign global…

Share this:

Emerging markets (EM) debt performed well in the first quarter of 2024, and we anticipate more of the same in the next quarter, thanks to a benign global macro backdrop, solid EM credit fundamentals, improving technical conditions, and still-decent valuations.

We continue to believe that there are attractive opportunities for investors to increase exposure to long-duration securities to lock in attractive real and nominal yields.

Despite strong performance this year, we also see selective value in high-beta, high-yield credit because we believe the global market environment will be conducive to its outperformance.

We also continue see scope for fundamental differentiation and prefer countries with easier access to multilateral and bilateral funding (including frontier and distressed credit).

Meanwhile, the corporate credit space continues to exhibit a combination of differentiated fundamental drivers, favorable supply technical conditions, and attractive relative valuations to select sovereign curves. We are seeking investment opportunities where corporate credit fundamentals and attractive spreads coincide. Short-maturity bonds have outperformed, but opportunities in longer bonds are appearing. We continue to focus on issuers with low refinancing needs, robust balance sheets, and positive credit trajectories.

Below, we break down some of our largest active positions by beta bucket, which is how we allocate our risk budget.

A View of the Potential Opportunities: Overweight/Underweight

High-Beta Bucket

In the high-beta bucket, our largest overweight positions are in Egypt, Ukraine, and Ghana, and our largest underweight positions are in Rwanda, Kenya, and Nigeria.

Egypt (overweight): Significant external financing—which was unlocked through the recently announced International Monetary Fund (IMF) package and foreign direct investment (FDI) deal—is more than adequate to meet Egypt’s needs. The external sector could also prove resilient following the sharp depreciation of the Egyptian pound. We also believe there is room for further spread compression toward peers in the high-beta bucket and curve steepening.

Ukraine’s potential restructuring could be more favorable to eurobond holders than previously anticipated.

Ukraine (overweight): We have increased our overweight based on a potential restructuring that we have interpreted as more favorable for eurobond holders than previously anticipated. Multilateral and bilateral support also remains strong.

Ghana (overweight): We believe the restructuring process is regaining momentum. The prospect of lower core rates and the rally in high-yield names could support recovery values.

Rwanda (underweight): Imbalances in the external sector and unattractive valuations make Rwanda vulnerable.

Kenya (underweight): Spreads have tightened to levels at which we believe there is better value in other high-beta names.

Nigera (underweight): Valuations are tight relative to peers.

Medium-Beta Bucket

In the medium-beta bucket, our largest overweight positions are in Ivory Coast, Guatemala, and Benin, and our largest underweight positions are in Bahrain, Romania, and Dominican Republic.

Ivory Coast (overweight): We believe valuations are favorable relative to peers. The country’s debt is also supported by strong fundamentals and support from development partners, including the IMF. We also believe Senegal’s peaceful post-election political transition will bolster confidence in the Ivory Coast’s political process ahead of its own elections next year.

Benin (overweight): We believe the country’s bonds will continue to be supported by strong fundamental performance and prudent macroeconomic policies. The country will also receive further support from the IMF under the Resilience and Sustainability Facility in late 2024.

Guatemala (overweight): Macroeconomic conditions are strong and valuations are attractive, and although President Bernardo Arévalo will likely face political obstacles, we believe strong leverage ratios and low fiscal deficits will keep Guatemala a strong credit.

Dominican Republic’s valuations are at their tightest levels since 2007.

Bahrain (underweight): Weak fiscal reform efforts, a deterioration in regional geopolitical risks, and tight valuations make us cautious.

Romania (underweight): We are concerned about deteriorating fiscal risks and political noise ahead of this year’s elections. Romania has already been a prolific issuer this year and is running the risk of an abundance of supply.

Dominican Republic (underweight): Although fundamentals continue to be among the strongest in the region, valuations are at their tightest levels since 2007.

Low-Beta Bucket

In the low-beta bucket, our largest overweight positions are in Saudi Arabia, Bermuda, and Paraguay and our largest underweight positions are in Poland, Uruguay, and Indonesia.

Saudi Arabia (overweight): Efforts to diversify the economy away from the energy sector remain largely on track. Oil prices are supportive of the current investment spend, and we see value in Saudi Arabia relative to some of its regional peers.

We believe Paraguay is on an improving fundamental trajectory.

Bermuda (overweight): Bermuda’s bonds have similar valuations to those of Peru and Chile, but we believe the country has a stronger fundamental trajectory with less institutional uncertainty.

Paraguay (overweight): Although Paraguay has lagged year-to-date, we believe the country is on an improving fundamental trajectory and has attractive valuations for the low-beta bucket.

Poland (underweight): Although the medium-term policy framework looks more favorable under the new government, we remain cautious near term due to an increase in political noise following last year’s elections.

Uruguay (underweight): Credit fundamentals in Uruguay remain strong, but bond prices have compressed materially since the COVID-19 pandemic, and we believe this results in limited scope for additional spread tightening.

Indonesia (underweight): Valuations are unappealing. The country’s fundamental outlook became murkier after presidential elections in February, and there is risk of fiscal slippage should the new government increase spending. In addition, a slowdown in the windfall from commodity exports and a persistently strong U.S. dollar could weaken external positions.

Marco Ruijer, CFA, is a portfolio manager on William Blair’s emerging markets debt team.

Want more insights on the economy and investment landscape? Subscribe to our blog.

The post EM Debt 2024: Solid Beginnings appeared first on William Blair.

bonds pandemic covid-19 emerging markets pound spread recovery oil poland ukraineGovernment

The New York Fed Consumer Credit Panel: A Foundational CMD Data Set

As the Great Financial Crisis and associated recession were unfolding in 2009, researchers at the New York Fed joined colleagues at the Board of Governors…

Share this:

As the Great Financial Crisis and associated recession were unfolding in 2009, researchers at the New York Fed joined colleagues at the Board of Governors and Philadelphia Fed to create a new kind of data set. Household liabilities, particularly mortgages, had gone from being a quiet little corner of the financial system to the center of the worst financial crisis and sharpest recession in decades. The new data set was designed to provide fresh insights into this part of the economy, especially the behavior of mortgage borrowers. In the fifteen years since that effort came to fruition, the New York Fed Consumer Credit Panel (CCP) has provided many valuable insights into household behavior and its implications for the macro economy and financial stability.

The CCP was one of the first data sets drawn from credit bureau data, one of the earliest features of the Center for Microeconomic Data (CMD), and the primary source material for some of the CMD’s most important contributions to policy and research. Here we review a few of the main household debt themes over the past fifteen years, and how our analyses contributed to their understanding.

The New York Fed Consumer Credit Panel

The CCP is drawn from anonymized credit bureau data provided by Equifax and includes quarterly information on the liabilities of a dynamic panel of individuals (5 percent of the population with a credit report—approximately 14.2 million individuals in 2023:Q4) and their household members (an additional 11.5 percent/ 32.9 million individuals) beginning in the first quarter of 1999. The data are unique in many ways, but the dynamic panel structure was among the most important features since, in each quarter, the data provide a representative picture of credit outcomes of the U.S. population.

The data include all the major forms of household debt: mortgage and home equity lines of credit, credit cards, auto loans, and student loans. For each individual we observe the opening and closing of accounts, balances and credit limits on existing accounts, payment status on all forms of debt, and other features of the credit report, such as the individual’s credit score. In addition, we know the individual’s location (to the census block) and year of birth. More details on the data are available in Lee and van der Klaauw (2010).

The Great Financial Crisis and Recovery

The CCP immediately became an invaluable resource in understanding the extreme challenges that American households were facing even as the financial system and the economy began to recover. In one of the first analyses using the data, The Financial Crisis at the Kitchen Table, we documented the enormous run-up and subsequent decline in household debt and payment delinquencies between 2007 and 2009. In addition, we showed in numerous Liberty Street Economics posts that households had gone from borrowing heavily prior to the peak in home prices to defaulting and paying off debt at a rapid pace beginning in 2007.

The deleveraging process finally concluded in 2013 (see the chart below), but not before millions of households had lost their homes through foreclosure or lost access to credit through bankruptcy. (Stay turned for our forthcoming post on the long-term consequences for those families.) The fact that the CCP presents a comprehensive picture of household balance sheets also enabled us to identify a then little-known dimension of the housing market boom and bust—the behavior of real estate speculators. Perhaps most importantly, the CCP now provides an early warning signal for stresses in the household sector—something that was not available before the GFC. It also reveals the households and neighborhoods where those stresses may occur.

Total Cash Flow from Household Debt Turned Slightly Positive in 2013

Student Debt

As the mortgage and housing markets began to return to a more stable footing after 2012, a new issue for household finance began to emerge: student debt. By 2012, student debt was the second largest household liability and the CCP provided insights into the rapid growth and performance of that stock of debt over the subsequent decade. These analyses were especially valuable because of the paucity of other information on student borrowing: While the federal government plays a dominant role in the market, only the CCP provided the kind of information needed to assess the role of student debt on household balance sheets and provided information about how student debt has become an increasingly important determinant of well-being.

By 2012 Student Debt Became the Second Largest Household Liability behind Mortgage Debt

Over time, the issues that our analyses pointed to became a central point of policy debate, and our work provided valuable evidence on the effects of various proposals.

Household Debt during the Pandemic and Beyond

Many of the concerns that had manifested themselves in the first decade of the CCP were very much in the forefront of economic policy discussions as the COVID-19 pandemic hit the U.S. in 2020. Seeking to avoid a wave of defaults and consumer distress, officials provided monetary and fiscal stimulus, placed moratoria on foreclosures, offered forbearance on many mortgages and student loans, and encouraged lenders to work with borrowers on their other obligations. To help provide greater clarity on how the pandemic and these policies were affecting households, we acquired monthly CCP updates that allowed high-frequency analyses, and these proved themselves invaluable in charting the patterns of hardship and the incidence of the policy benefits. In particular, widespread forbearances were unprecedented and the CCP enabled us to follow borrowers whose mortgages and student loan payments were paused.

As the forbearance programs largely wound down, we were able to take a look back at who benefited and a look ahead at what might come next for these borrowers. In the end, student loan forbearance lasted far longer than that for mortgages, and we were able to document important impacts of this policy. As policy discussion turned to the idea of permanent student loan forgiveness we were able to provide deep insights into who would benefit and how much in general and based on the specifics of the White House plan. We also were able to show that the unique combination of economic outcomes and policy interventions during COVID had a profound impact on household balance sheets and cash flows, including reductions in credit card debt and delinquency rates, that continues to affect the macroeconomy today.

A Large Impact on Research and a Bright Future

In addition to these major areas of enduring interest, the CCP has shown its value in many other ways. The current attention to rising credit card and auto loan delinquencies is a contemporary example and there will continue to be many more. In the meantime, CCP data have been used in hundreds of research studies, deepening understanding of how household liabilities affect welfare and the economy. The initial idea of the CCP was to give policymakers insight into household debt developments in order to avoid a repeat of the events of the Great Financial Crisis. But the scope of analysis using CCP data has also begun to extend beyond household debt to study trends, such as migration, small business finance, gentrification, and disaster resilience. We remain committed to using the data to help us understand the underpinnings and disparities in household finances and to allow us to monitor developments on a high-frequency basis.

Andrew F. Haughwout is the director of Household and Public Policy Research in the Federal Reserve Bank of New York’s Research and Statistics Group.

Donghoon Lee is an economic research advisor in Consumer Behavior Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Daniel Mangrum is a research economist in Equitable Growth Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Joelle Scally is a regional economic principal in the Federal Reserve Bank of New York’s Research and Statistics Group.

Wilbert van der Klaauw is the economic research advisor for Household and Public Policy Research in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Andrew Haughwout, Donghoon Lee, Daniel Mangrum, Joelle Scally, and Wilbert van der Klaauw , “The New York Fed Consumer Credit Panel: A Foundational CMD Data Set,” Federal Reserve Bank of New York Liberty Street Economics, April 17, 2024, https://libertystreeteconomics.newyorkfed.org/2024/04/the-new-york-fed-consumer-credit-panel-a-foundational-cmd-data-set/.

{kind=link}

{kind=link}

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

California Auditor Finds Homeless Council Can’t Account For Money Spent

Crib-Notes For The ‘Trial Of The Century’

Cheap grocery chain adds a fancy Whole Foods-style feature

The WHO’s Road To Totalitarianism

The New York Fed Consumer Credit Panel: A Foundational CMD Data Set

Victor Davis Hanson: Gaming The 2024 Campaign

Deborah Birx Gets Her Close-Up

Conservatives Seek To Ban Private Funding Of Elections Ahead Of 2024 Races

Is Paxlovid A Dud?

Goldman Soars On “Near-Perfect” Top To Bottom Beat As Solomon Sees Rebound In Dealmaking

-

International4 weeks ago

International4 weeks agoParexel CEO to retire; CAR-T maker AffyImmune promotes business leader to chief executive

-

Government2 weeks ago

Government2 weeks agoClimate-Con & The Media-Censorship Complex – Part 1

-

Spread & Containment3 days ago

Spread & Containment3 days agoWHO Official Admits Vaccine Passports May Have Been A Scam

-

Spread & Containment1 week ago

Spread & Containment1 week agoFDA Finally Takes Down Ivermectin Posts After Settlement

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoVaccinated People Show Long COVID-Like Symptoms With Detectable Spike Proteins: Preprint Study

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoCan language models read the genome? This one decoded mRNA to make better vaccines.

-

Uncategorized1 week ago

Uncategorized1 week agoWhat’s So Great About The Great Reset, Great Taking, Great Replacement, Great Deflation, & Next Great Depression?

-

Spread & Containment4 weeks ago

Spread & Containment4 weeks agoJapanese Preprint Calls For mRNA VaccinesTo Be Suspended Over Blood Bank Contamination Concerns