International

Our thoughts on inflation – And why we just don’t buy it!

In our view, in the wake of the sell-off and reset in valuations for environmental sector stocks in the first half of the year, the fundamentals have never looked more attractive. Our strategy involves a pure play environmental thematic approach, with…

Share this:

In our view, in the wake of the sell-off and reset in valuations for environmental sector stocks in the first half of the year, the fundamentals have never looked more attractive.

- Our strategy involves a pure play environmental thematic approach, with an all-cap universe and no constraints.

- As an investment team, we have over 20 years of experience in investing thematically together with high level of industry / technology knowledge.

- Today, we see inflation expectations as well anchored. We argue that any rise in inflation will be temporary, paving the way for ‘lower for longer’ on interest rates.

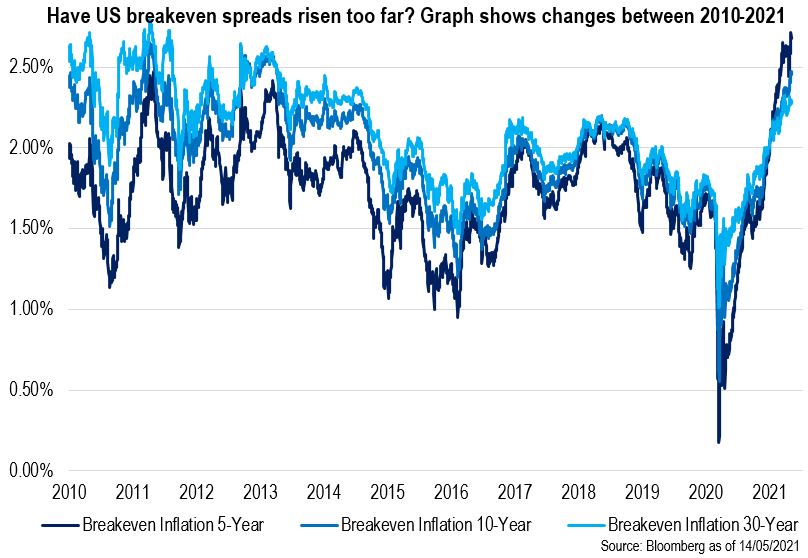

- In bond markets, 10-year breakeven spreads have fallen significantly over the last three days (from 2.60% to 2.45%). Being overweight US Treasury inflation-protected securities (TIPS) is, we believe, an extremely crowded trade. We expect it to significantly overshoot to the downside, which would see growth squeeze higher, everything else being equal.

Why are the fundamentals so attractive?

The sell-off earlier this year has effectively reset valuations. The price-to-earnings-to-growth ration of 0.57x for the universe of environmental stocks we invest in (with a 3-year CAGR earnings-per-share of 63.5%) compares to 1.91 and a 3-year CAGR earnings-per-share rate at 39.7% for the tech-heavy NASDAQ index.

We see pure environmental equities in wind, solar, hydrogen, electric vehicles (EV) and battery storage as under-owned. This creates, in our opinion, an asymmetric risk to the upside. Many potential investors cannot hold these stocks due to restrictions on capitalisation and/or systematic screening that fails to capture these companies.

In what respect is our strategy a pure play?

We invest in companies with environmental solutions/products and services – we do not invest in technology, financial, healthcare or retail companies with a low carbon footprint, but doing little for the environment.

Why do we have a contrarian view on inflation from here?

We see inflation expectations as well anchored currently. We would argue that the evidence suggests any rise will be temporary and pave the way for a ‘lower for longer’ world for interest rates.

The services component is large in the US consumer price index (CPI) and the sector is very price competitive.

We do not accept the idea of a new commodities ‘super cycle’ just because commodity prices are trading close to the highs of the 2000-2010 infrastructure boom in China. Restocking and double bookings for building inventories is, in our view, the driver of these valuations. It is not a case of structurally higher input cost pressure.

We believe there is still plenty of slack in the US labour market with little evidence of wage inflation.

Why do we see the rise in US breakeven spreads as overdone?

The trading around yesterday’s (20 May 2021) TIPS auction was, in our view, weak. This supports our argument below that the inflation trade has now ‘travelled and arrived at the destination.’ For us, this is the end of the line for breakevens.

Environmental stocks have been particularly vulnerable – and by far the hardest hit sector – when it comes to the reflation trade. We believe this is about to change …a whole lot.

Dislocation

Let us start with one of the most ‘unsustainable’ investing observations we have experienced for some time. The world’s largest environmental ETF with assets under management of USD 12 billion, the iShares Clean Energy ETF, started its life in 2008. In first quarter 2021, it hit an all-time record – the largest quarterly underperformance of this ETF on record relative to the USD 24 billion Energy Select Sector SPDR Fund.

In other words, stranded (energy) assets have just outperformed the transition (clean energy) economy by 43%. So far in second quarter of 2021, we are witnessing the second biggest quarterly underperformance of iShares Clean Energy relative to Energy Select Sector SPDR in history at – 20%. Yes, you guessed it, the biggest underperformance EVER over two consecutive quarters!

And this has all happened amid supportive policy commitments in the form of the Biden Infrastructure Plan, the US rejoining the Paris Climate Agreement, multiple announcements of net-zero commitments and accelerated timelines, with India recently joining in.

In addition there have been announcements of US regulatory support with extended tax incentives for wind, solar, storage, and carbon prices hitting all-time highs.

No surprise there, but the market bears remind us that when the market gets caught up in negative sentiment, investors find it hard to see the wood for the the trees. In other words, we think they risk focusing on the wrong things.

We have written at length about the outlook for the green economy. And about the companies whose business model it is to deliver environmental solutions to enable the energy transition and restore ecosystems. Our views on that subject are not the purpose of this post.

So why has this dislocation happened in environmental stocks?

Well, a perfect storm was created by:

(1) Elevated passive investor positioning in environmental stocks from December 20 through January 2021.

(2) ETF rebalancing creating havoc; but mostly it comes down to one thing…and that is inflation or rather the fear it is about to make a major comeback.

So, if we can crack the inflation debate, we can understand the future trajectory of the stock market valuations of the companies in the environmental solutions universe…

Firstly, I don’t know about you, but the vast majority of research and commentary we see is pushing inflation-is-back (and you-need-a-hedge) like never before – literally. According to our estimates, the monthly story count is the highest in 10 years.

Much has been written about inflation. The consensus on Wall (and the High) Street today is that inflation will not only overshoot as the US economy reopens, but will be structurally higher due to a ‘commodities super-cycle’ in conjunction with a tight labour market while there is little slack in the economy, meaning prices and wages must increase.

We do not believe higher structural inflation is ahead

Let’s start with US Federal Reserve Governor Lael Brainard, who has said that officials should be ‘patient though the transitory surge.’ Fed chair Jay Powell has made the same argument. While policymakers expect the Fed’s preferred measure of inflation to rise to around 2.4% this year, they forecast it will return to the Fed’s 2% goal in 2022.

The huge increase in the number of participants seeking to hedge inflation risk through TIPS is a key issue for the market. These new investors relish the carry they are currently making given the market reaction to headline inflation news and this encourages others to join in.

However, as we get through summer, and if as we expect US headline inflation falls back, the going will get tougher for these investors. How they react will be critical to determining the level of breakeven inflation spreads.

We see a high chance of an overshoot on the way down as holders panic.

What about the substantially higher US CPI and PPI releases?

We had expected nothing else than a number that would imply a wide range of uncertainty and will continue to do so during the reopening phase of economies globally. However, the headline number gives little information. Insight is needed into what drove the higher CPI print. This means diving into (1) services and; (2) goods

1. Services: Indeed, 60% of the month-over-month increase in the headline number was comprised of just five components – used cars, rental cars, lodging, airfares, and food away from home. These items are indeed very much transient in nature and hence will NOT contribute to structurally higher inflation. Services companies are in a much stronger position to extract higher prices in 2021 than they were in 2019 as citizens are desperate to go out for dinners, trips and experiences. But the barrier-to-entry into the service business is low, so super-normal pricing should rapidly see new competition and drive down inflation in 2022/23. The impact of rising rents is a another key risk to inflation as this has a high multiplier effect in year 1 and in all future years (whereas an oil-price driven spike is not carried forward to future years). However, with work-from-home being more of a norm, we don’t see this as a real risk. Indeed, rents might be a deflationary risk.

2. Goods: This is where there is more divided opinion. Some argue for the emergence of a new commodities super-cycle. We remain sceptical and think price rises are down to bottlenecks. Here, the most talked-about commodity is copper.

Consider these points:

- According to research from UBS, EV and renewables will add circa 6.5 metric tonnes of new demand for copper over the next decade. That would constitute around 25% of global demand (relative to 5% today), but most of that comes closer to 2030. Demand from China’s electricity grid rollout and construction is likely to fall from 30% of current demand to much lower levels as household formation slows. China currently comprises 60% of copper demand and is growing at 8% per annum, whereas the US/EU accounts for 25% and is growing at best at 1%.Even stimulus from the rest of the world and a COVID-19 recovery are not going to move the dial on overall demand growth. US/EU stimulus is never overly copper intensive – if every petrol station in the US had an EV super charger, it still wouldn’t move the dial. Of course, a COVID-19 recovery is positive for demand. However, using this to justify high copper prices today is a stretch, in our view.

- How tight is the market? We do not see anywhere near the physical tightness in markets that normally drives this kind of price spike, but of course, prices are a signal of future tightness and clearly the market is spooked about supply issues in the second half of the year (strikes, new outbreaks of COVID-19, etc.). While not much new supply will come online this year, we do not see the market as overly short. We see 10 major copper projects coming on stream to enable supply to match the 3% growth in net new demand through to 2030.

- On commodities such as iron ore, we could make many of the same arguments. However, here prices have been driven up by speculators rather than producers.

- Note that our view continues to be different for oil. We believe that demand will surprise to the upside and that supply will be much harder to adjust given seven years of structural underinvestment in new exploration and decline rates in the US coming down aggressively. We still believe oil prices could rise to USD 100/barrel. We note that the correlation of oil prices and the CPI is insignificant at 0.27, but it is at 0.71 for the producer price index.

3. Labour: Finally, there seem to be sufficient slack in the labour market. This supports our view that inflation is most likely to be transitory. “It seems unlikely, frankly, that we would see inflation moving up in a persistent way that would actually move inflation expectations up while there was still significant slack in the labour market,” said Chair Powell during an April 28 press conference.

According to Bloomberg Economics, until the unemployment rate falls to below 4% — which is broadly not expected before 2023 — policymakers will likely regard what upward pressure there is as benign. Recent wage dynamics are consistent with still widespread slack in the labour market; however, pockets of hotter growth are showing up.

- Faster wage inflation is concentrated among lower-earners, a trend the Fed will be inclined to support, not squelch.

- Subdued income expectations and perceptions of future job prospects show the persistence of pandemic scars, contrasting with fears of rising inflation expectations.

- Stepping back from the review of the data, it’s important to keep in mind that the post-pandemic equilibrium is not yet in view. Expanded unemployment benefits will continue to distort labour market conditions over the summer.

- More speculatively, it’s possible the pandemic will trigger a broader reconsideration of the work-life-balance with workers placing greater emphasis on flexibility over salary.

Summing up, a comprehensive view of the data, and broader considerations about potential shifts in the labour market, provide us with little reason for immediate concern about rising wages sustaining elevated inflation.

A very tight US labour market before the pandemic delivered very little underlying inflation, so why would we believe tight labour markets will deliver runaway inflation after the pandemic?

It’s all relative…base effects

Finally, beware of ‘base effects’. “These base effects will contribute about 1 percentage point to headline inflation, at about 0.7% of a percentage point, to core inflation in April and May,” said Chair Powell in his April press briefing. “So, significant increases, and they’ll disappear over the following months and they’ll be transitory.”

Deflationary forces still at play

Are we really convinced that all those dis-inflationary headwinds – from disruptive technical change and globalisation – that existed in the decade before the pandemic have all dissipated?

A number of structural factors have led to global deflation over the past three decades. These include globalisation, which has given us cheaper access to supplies and labour from around the world, slowing growth and aging of the population, which reduce demand over time, along with advances in technology and the internet.

Those forces are likely to keep pushing against higher price pressures. Online shopping has become even more important during the pandemic. Reflecting the importance of technology disrupting businesses, the Dallas, Atlanta and Richmond Federal Reserves are holding a virtual conference on the subject later this month.

Thus, we can’t help being slightly bemused by the market’s concern over structurally higher inflation when the biggest worry we have had for the past decade has been the lack of inflation. Inflation is not an issue per se; while rampant inflation is, we don’t see any evidence of that at all.

Indeed, we believe the bigger challenge over the long run is deflationary forces, not structurally higher inflation. By the way, if you believe in decarbonisation, the biggest deflationary effect is right in front of our noses: the sun, wind and water do not charge us for the marginal cost of a unit of energy produced, so power and energy prices will be one of the biggest actors in the deflationary rhetoric.

Alas, we think inflation expectations will continue to be re-anchored for 10-year breakeven spreads, making way for a transitory increase in headline inflation that will subside and keep interest rates lower for longer. This is constructive for risk assets broadly. In addition, we expect the continued record earnings delivery to push stock markets higher and we see sentiment catching up with what are in our view attractive fundamentals.

In conclusion, we think now is a great set up for the environmental solutions theme going into the second half of the year for the following reasons:

- An attractive level of valuations

- Low levels of investor participation

- A strong underlying demand picture

- Unwavering regulatory support

- Unprecedented investment into the energy transition

- Undue concerns about inflation risk

- A market that is significantly underweight growth following the overweight reflation trade

Any views expressed here are those of the author as of the date of publication, are based on available information, and are subject to change without notice. Individual portfolio management teams may hold different views and may take different investment decisions for different clients. This document does not constitute investment advice.

The value of investments and the income they generate may go down as well as up and it is possible that investors will not recover their initial outlay. Past performance is no guarantee for future returns.

Investing in emerging markets, or specialised or restricted sectors is likely to be subject to a higher-than-average volatility due to a high degree of concentration, greater uncertainty because less information is available, there is less liquidity or due to greater sensitivity to changes in market conditions (social, political and economic conditions).

Some emerging markets offer less security than the majority of international developed markets. For this reason, services for portfolio transactions, liquidation and conservation on behalf of funds invested in emerging markets may carry greater risk.

Writen by Edward Lees. The post Our thoughts on inflation – And why we just don’t buy it! appeared first on Investors' Corner - The official blog of BNP Paribas Asset Management, the sustainable investor for a changing world.

unemployment pandemic covid-19 stimulus reopening nasdaq emerging markets equities stocks fed federal reserve us treasury etf governor recovery interest rates unemployment stimulus commodities stock markets oil india eu chinaGovernment

President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

President Biden Delivers The "Darkest, Most Un-American Speech Given By A President"

Having successfully raged, ranted, lied, and yelled through…

Share this:

Having successfully raged, ranted, lied, and yelled through the State of The Union, President Biden can go back to his crypt now.

Whatever 'they' gave Biden, every American man, woman, and the other should be allowed to take it - though it seems the cocktail brings out 'dark Brandon'?

Tl;dw: Biden's Speech tonight ...

-

Fund Ukraine.

-

Trump is threat to democracy and America itself.

-

Abortion is good.

-

American Economy is stronger than ever.

-

Inflation wasn't Biden's fault.

-

Illegals are Americans too.

-

Republicans are responsible for the border crisis.

-

Trump is bad.

-

Biden stands with trans-children.

-

J6 was the worst insurrection since the Civil War.

(h/t @TCDMS99)

Tucker Carlson's response sums it all up perfectly:

"that was possibly the darkest, most un-American speech given by an American president. It wasn't a speech, it was a rant..."

Carlson continued: "The true measure of a nation's greatness lies within its capacity to control borders, yet Bid refuses to do it."

"In a fair election, Joe Biden cannot win"

And concluded:

“There was not a meaningful word for the entire duration about the things that actually matter to people who live here.”

Victor Davis Hanson added some excellent color, but this was probably the best line on Biden:

"he doesn't care... he lives in an alternative reality."

— Tucker Carlson (@TuckerCarlson) March 8, 2024

* * *

Watch SOTU Live here...

* * *

Mises' Connor O'Keeffe, warns: "Be on the Lookout for These Lies in Biden's State of the Union Address."

On Thursday evening, President Joe Biden is set to give his third State of the Union address. The political press has been buzzing with speculation over what the president will say. That speculation, however, is focused more on how Biden will perform, and which issues he will prioritize. Much of the speech is expected to be familiar.

The story Biden will tell about what he has done as president and where the country finds itself as a result will be the same dishonest story he's been telling since at least the summer.

He'll cite government statistics to say the economy is growing, unemployment is low, and inflation is down.

Something that has been frustrating Biden, his team, and his allies in the media is that the American people do not feel as economically well off as the official data says they are. Despite what the White House and establishment-friendly journalists say, the problem lies with the data, not the American people's ability to perceive their own well-being.

As I wrote back in January, the reason for the discrepancy is the lack of distinction made between private economic activity and government spending in the most frequently cited economic indicators. There is an important difference between the two:

-

Government, unlike any other entity in the economy, can simply take money and resources from others to spend on things and hire people. Whether or not the spending brings people value is irrelevant

-

It's the private sector that's responsible for producing goods and services that actually meet people's needs and wants. So, the private components of the economy have the most significant effect on people's economic well-being.

Recently, government spending and hiring has accounted for a larger than normal share of both economic activity and employment. This means the government is propping up these traditional measures, making the economy appear better than it actually is. Also, many of the jobs Biden and his allies take credit for creating will quickly go away once it becomes clear that consumers don't actually want whatever the government encouraged these companies to produce.

On top of all that, the administration is dealing with the consequences of their chosen inflation rhetoric.

Since its peak in the summer of 2022, the president's team has talked about inflation "coming back down," which can easily give the impression that it's prices that will eventually come back down.

But that's not what that phrase means. It would be more honest to say that price increases are slowing down.

Americans are finally waking up to the fact that the cost of living will not return to prepandemic levels, and they're not happy about it.

The president has made some clumsy attempts at damage control, such as a Super Bowl Sunday video attacking food companies for "shrinkflation"—selling smaller portions at the same price instead of simply raising prices.

In his speech Thursday, Biden is expected to play up his desire to crack down on the "corporate greed" he's blaming for high prices.

In the name of "bringing down costs for Americans," the administration wants to implement targeted price ceilings - something anyone who has taken even a single economics class could tell you does more harm than good. Biden would never place the blame for the dramatic price increases we've experienced during his term where it actually belongs—on all the government spending that he and President Donald Trump oversaw during the pandemic, funded by the creation of $6 trillion out of thin air - because that kind of spending is precisely what he hopes to kick back up in a second term.

If reelected, the president wants to "revive" parts of his so-called Build Back Better agenda, which he tried and failed to pass in his first year. That would bring a significant expansion of domestic spending. And Biden remains committed to the idea that Americans must be forced to continue funding the war in Ukraine. That's another topic Biden is expected to highlight in the State of the Union, likely accompanied by the lie that Ukraine spending is good for the American economy. It isn't.

It's not possible to predict all the ways President Biden will exaggerate, mislead, and outright lie in his speech on Thursday. But we can be sure of two things. The "state of the Union" is not as strong as Biden will say it is. And his policy ambitions risk making it much worse.

* * *

The American people will be tuning in on their smartphones, laptops, and televisions on Thursday evening to see if 'sloppy joe' 81-year-old President Joe Biden can coherently put together more than two sentences (even with a teleprompter) as he gives his third State of the Union in front of a divided Congress.

President Biden will speak on various topics to convince voters why he shouldn't be sent to a retirement home.

The state of our union under President Biden: three years of decline. pic.twitter.com/Da1KOIb3eR

— Speaker Mike Johnson (@SpeakerJohnson) March 7, 2024

According to CNN sources, here are some of the topics Biden will discuss tonight:

Economic issues: Biden and his team have been drafting a speech heavy on economic populism, aides said, with calls for higher taxes on corporations and the wealthy – an attempt to draw a sharp contrast with Republicans and their likely presidential nominee, Donald Trump.

Health care expenses: Biden will also push for lowering health care costs and discuss his efforts to go after drug manufacturers to lower the cost of prescription medications — all issues his advisers believe can help buoy what have been sagging economic approval ratings.

Israel's war with Hamas: Also looming large over Biden's primetime address is the ongoing Israel-Hamas war, which has consumed much of the president's time and attention over the past few months. The president's top national security advisers have been working around the clock to try to finalize a ceasefire-hostages release deal by Ramadan, the Muslim holy month that begins next week.

An argument for reelection: Aides view Thursday's speech as a critical opportunity for the president to tout his accomplishments in office and lay out his plans for another four years in the nation's top job. Even though viewership has declined over the years, the yearly speech reliably draws tens of millions of households.

Sources provided more color on Biden's SOTU address:

The speech is expected to be heavy on economic populism. The president will talk about raising taxes on corporations and the wealthy. He'll highlight efforts to cut costs for the American people, including pushing Congress to help make prescription drugs more affordable.

Biden will talk about the need to preserve democracy and freedom, a cornerstone of his re-election bid. That includes protecting and bolstering reproductive rights, an issue Democrats believe will energize voters in November. Biden is also expected to promote his unity agenda, a key feature of each of his addresses to Congress while in office.

Biden is also expected to give remarks on border security while the invasion of illegals has become one of the most heated topics among American voters. A majority of voters are frustrated with radical progressives in the White House facilitating the illegal migrant invasion.

It is probable that the president will attribute the failure of the Senate border bill to the Republicans, a claim many voters view as unfounded. This is because the White House has the option to issue an executive order to restore border security, yet opts not to do so

Maybe this is why?

Most Americans are still unaware that the census counts ALL people, including illegal immigrants, for deciding how many House seats each state gets!

— Elon Musk (@elonmusk) March 7, 2024

This results in Dem states getting roughly 20 more House seats, which is another strong incentive for them not to deport illegals.

While Biden addresses the nation, the Biden administration will be armed with a social media team to pump propaganda to at least 100 million Americans.

"The White House hosted about 70 creators, digital publishers, and influencers across three separate events" on Wednesday and Thursday, a White House official told CNN.

Not a very capable social media team...

The State of Confusion https://t.co/C31mHc5ABJ

— zerohedge (@zerohedge) March 7, 2024

The administration's move to ramp up social media operations comes as users on X are mostly free from government censorship with Elon Musk at the helm. This infuriates Democrats, who can no longer censor their political enemies on X.

Meanwhile, Democratic lawmakers tell Axios that the president's SOTU performance will be critical as he tries to dispel voter concerns about his elderly age. The address reached as many as 27 million people in 2023.

"We are all nervous," said one House Democrat, citing concerns about the president's "ability to speak without blowing things."

The SOTU address comes as Biden's polling data is in the dumps.

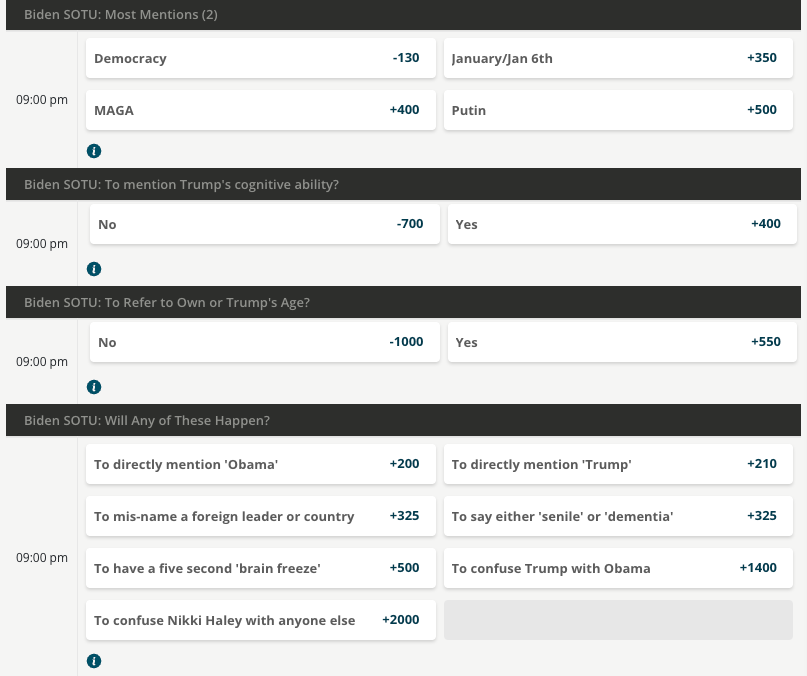

BetOnline has created several money-making opportunities for gamblers tonight, such as betting on what word Biden mentions the most.

As well as...

We will update you when Tucker Carlson's live feed of SOTU is published.

Fuck it. We’ll do it live! Thursday night, March 7, our live response to Joe Biden’s State of the Union speech. pic.twitter.com/V0UwOrgKvz

— Tucker Carlson (@TuckerCarlson) March 6, 2024

International

What is intersectionality and why does it make feminism more effective?

The social categories that we belong to shape our understanding of the world in different ways.

Share this:

The way we talk about society and the people and structures in it is constantly changing. One term you may come across this International Women’s Day is “intersectionality”. And specifically, the concept of “intersectional feminism”.

Intersectionality refers to the fact that everyone is part of multiple social categories. These include gender, social class, sexuality, (dis)ability and racialisation (when people are divided into “racial” groups often based on skin colour or features).

These categories are not independent of each other, they intersect. This looks different for every person. For example, a black woman without a disability will have a different experience of society than a white woman without a disability – or a black woman with a disability.

An intersectional approach makes social policy more inclusive and just. Its value was evident in research during the pandemic, when it became clear that women from various groups, those who worked in caring jobs and who lived in crowded circumstances were much more likely to die from COVID.

A long-fought battle

American civil rights leader and scholar Kimberlé Crenshaw first introduced the term intersectionality in a 1989 paper. She argued that focusing on a single form of oppression (such as gender or race) perpetuated discrimination against black women, who are simultaneously subjected to both racism and sexism.

Crenshaw gave a name to ways of thinking and theorising that black and Latina feminists, as well as working-class and lesbian feminists, had argued for decades. The Combahee River Collective of black lesbians was groundbreaking in this work.

They called for strategic alliances with black men to oppose racism, white women to oppose sexism and lesbians to oppose homophobia. This was an example of how an intersectional understanding of identity and social power relations can create more opportunities for action.

These ideas have, through political struggle, come to be accepted in feminist thinking and women’s studies scholarship. An increasing number of feminists now use the term “intersectional feminism”.

The term has moved from academia to feminist activist and social justice circles and beyond in recent years. Its popularity and widespread use means it is subjected to much scrutiny and debate about how and when it should be employed. For example, some argue that it should always include attention to racism and racialisation.

Recognising more issues makes feminism more effective

In writing about intersectionality, Crenshaw argued that singular approaches to social categories made black women’s oppression invisible. Many black feminists have pointed out that white feminists frequently overlook how racial categories shape different women’s experiences.

One example is hair discrimination. It is only in the 2020s that many organisations in South Africa, the UK and US have recognised that it is discriminatory to regulate black women’s hairstyles in ways that render their natural hair unacceptable.

This is an intersectional approach. White women and most black men do not face the same discrimination and pressures to straighten their hair.

“Abortion on demand” in the 1970s and 1980s in the UK and USA took no account of the fact that black women in these and many other countries needed to campaign against being given abortions against their will. The fight for reproductive justice does not look the same for all women.

Similarly, the experiences of working-class women have frequently been rendered invisible in white, middle class feminist campaigns and writings. Intersectionality means that these issues are recognised and fought for in an inclusive and more powerful way.

In the 35 years since Crenshaw coined the term, feminist scholars have analysed how women are positioned in society, for example, as black, working-class, lesbian or colonial subjects. Intersectionality reminds us that fruitful discussions about discrimination and justice must acknowledge how these different categories affect each other and their associated power relations.

This does not mean that research and policy cannot focus predominantly on one social category, such as race, gender or social class. But it does mean that we cannot, and should not, understand those categories in isolation of each other.

Ann Phoenix does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

africa uk pandemicGovernment

Biden defends immigration policy during State of the Union, blaming Republicans in Congress for refusing to act

A rising number of Americans say that immigration is the country’s biggest problem. Biden called for Congress to pass a bipartisan border and immigration…

Share this:

{kind=link}

President Joe Biden delivered the annual State of the Union address on March 7, 2024, casting a wide net on a range of major themes – the economy, abortion rights, threats to democracy, the wars in Gaza and Ukraine – that are preoccupying many Americans heading into the November presidential election.

The president also addressed massive increases in immigration at the southern border and the political battle in Congress over how to manage it. “We can fight about the border, or we can fix it. I’m ready to fix it,” Biden said.

But while Biden stressed that he wants to overcome political division and take action on immigration and the border, he cautioned that he will not “demonize immigrants,” as he said his predecessor, former President Donald Trump, does.

“I will not separate families. I will not ban people from America because of their faith,” Biden said.

Biden’s speech comes as a rising number of American voters say that immigration is the country’s biggest problem.

Immigration law scholar Jean Lantz Reisz answers four questions about why immigration has become a top issue for Americans, and the limits of presidential power when it comes to immigration and border security.

1. What is driving all of the attention and concern immigration is receiving?

The unprecedented number of undocumented migrants crossing the U.S.-Mexico border right now has drawn national concern to the U.S. immigration system and the president’s enforcement policies at the border.

Border security has always been part of the immigration debate about how to stop unlawful immigration.

But in this election, the immigration debate is also fueled by images of large groups of migrants crossing a river and crawling through barbed wire fences. There is also news of standoffs between Texas law enforcement and U.S. Border Patrol agents and cities like New York and Chicago struggling to handle the influx of arriving migrants.

Republicans blame Biden for not taking action on what they say is an “invasion” at the U.S. border. Democrats blame Republicans for refusing to pass laws that would give the president the power to stop the flow of migration at the border.

2. Are Biden’s immigration policies effective?

Confusion about immigration laws may be the reason people believe that Biden is not implementing effective policies at the border.

The U.S. passed a law in 1952 that gives any person arriving at the border or inside the U.S. the right to apply for asylum and the right to legally stay in the country, even if that person crossed the border illegally. That law has not changed.

Courts struck down many of former President Donald Trump’s policies that tried to limit immigration. Trump was able to lawfully deport migrants at the border without processing their asylum claims during the COVID-19 pandemic under a public health law called Title 42. Biden continued that policy until the legal justification for Title 42 – meaning the public health emergency – ended in 2023.

Republicans falsely attribute the surge in undocumented migration to the U.S. over the past three years to something they call Biden’s “open border” policy. There is no such policy.

Multiple factors are driving increased migration to the U.S.

More people are leaving dangerous or difficult situations in their countries, and some people have waited to migrate until after the COVID-19 pandemic ended. People who smuggle migrants are also spreading misinformation to migrants about the ability to enter and stay in the U.S.

3. How much power does the president have over immigration?

The president’s power regarding immigration is limited to enforcing existing immigration laws. But the president has broad authority over how to enforce those laws.

For example, the president can place every single immigrant unlawfully present in the U.S. in deportation proceedings. Because there is not enough money or employees at federal agencies and courts to accomplish that, the president will usually choose to prioritize the deportation of certain immigrants, like those who have committed serious and violent crimes in the U.S.

The federal agency Immigration and Customs Enforcement deported more than 142,000 immigrants from October 2022 through September 2023, double the number of people it deported the previous fiscal year.

But under current law, the president does not have the power to summarily expel migrants who say they are afraid of returning to their country. The law requires the president to process their claims for asylum.

Biden’s ability to enforce immigration law also depends on a budget approved by Congress. Without congressional approval, the president cannot spend money to build a wall, increase immigration detention facilities’ capacity or send more Border Patrol agents to process undocumented migrants entering the country.

4. How could Biden address the current immigration problems in this country?

In early 2024, Republicans in the Senate refused to pass a bill – developed by a bipartisan team of legislators – that would have made it harder to get asylum and given Biden the power to stop taking asylum applications when migrant crossings reached a certain number.

During his speech, Biden called this bill the “toughest set of border security reforms we’ve ever seen in this country.”

That bill would have also provided more federal money to help immigration agencies and courts quickly review more asylum claims and expedite the asylum process, which remains backlogged with millions of cases, Biden said. Biden said the bipartisan deal would also hire 1,500 more border security agents and officers, as well as 4,300 more asylum officers.

Removing this backlog in immigration courts could mean that some undocumented migrants, who now might wait six to eight years for an asylum hearing, would instead only wait six weeks, Biden said. That means it would be “highly unlikely” migrants would pay a large amount to be smuggled into the country, only to be “kicked out quickly,” Biden said.

“My Republican friends, you owe it to the American people to get this bill done. We need to act,” Biden said.

Biden’s remarks calling for Congress to pass the bill drew jeers from some in the audience. Biden quickly responded, saying that it was a bipartisan effort: “What are you against?” he asked.

Biden is now considering using section 212(f) of the Immigration and Nationality Act to get more control over immigration. This sweeping law allows the president to temporarily suspend or restrict the entry of all foreigners if their arrival is detrimental to the U.S.

This obscure law gained attention when Trump used it in January 2017 to implement a travel ban on foreigners from mainly Muslim countries. The Supreme Court upheld the travel ban in 2018.

Trump again also signed an executive order in April 2020 that blocked foreigners who were seeking lawful permanent residency from entering the country for 60 days, citing this same section of the Immigration and Nationality Act.

Biden did not mention any possible use of section 212(f) during his State of the Union speech. If the president uses this, it would likely be challenged in court. It is not clear that 212(f) would apply to people already in the U.S., and it conflicts with existing asylum law that gives people within the U.S. the right to seek asylum.

Jean Lantz Reisz does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

congress senate trump pandemic covid-19 mexico ukraine

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Redefining Poverty: Towards a Transpartisan Approach

Catastrophic Risk: Investing and Business Implications

The Digest #187

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Biden to call for first-time homebuyer tax credit, construction of 2 million homes

Is “Greedflation” Over?

Measuring Treasury Market Depth

GBPINR: Analysis and Projections for 2024

CADCHF: Central Bank Policies and Projections for 2024

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges