Government

Futures Rebound Fizzles On Slowing iPhone Demand, Omicron Fears

Futures Rebound Fizzles On Slowing iPhone Demand, Omicron Fears

U.S. index futures regained some ground alongside Asian markets while European stocks slumped to session lows in a delayed response to yesterday’s late Omicron-driven US selloff,

Share this:

U.S. index futures regained some ground alongside Asian markets while European stocks slumped to session lows in a delayed response to yesterday's late Omicron-driven US selloff, as markets remained volatile following the biggest two-day plunge in more than a year, spurred by concern about the omicron coronavirus variant and Federal Reserve tightening. Investors await data for unemployment claims, as well as earnings from companies including Dollar General and Kroger. Tech is the weakest sector, dropping in sympathy after Apple warned its suppliers of slowing iPhone demand. Nasdaq futures pared earlier gains of up to 0.8% to trade down 0.1% while S&P futures are only 0.2% higher after rising as much as 0.9%.

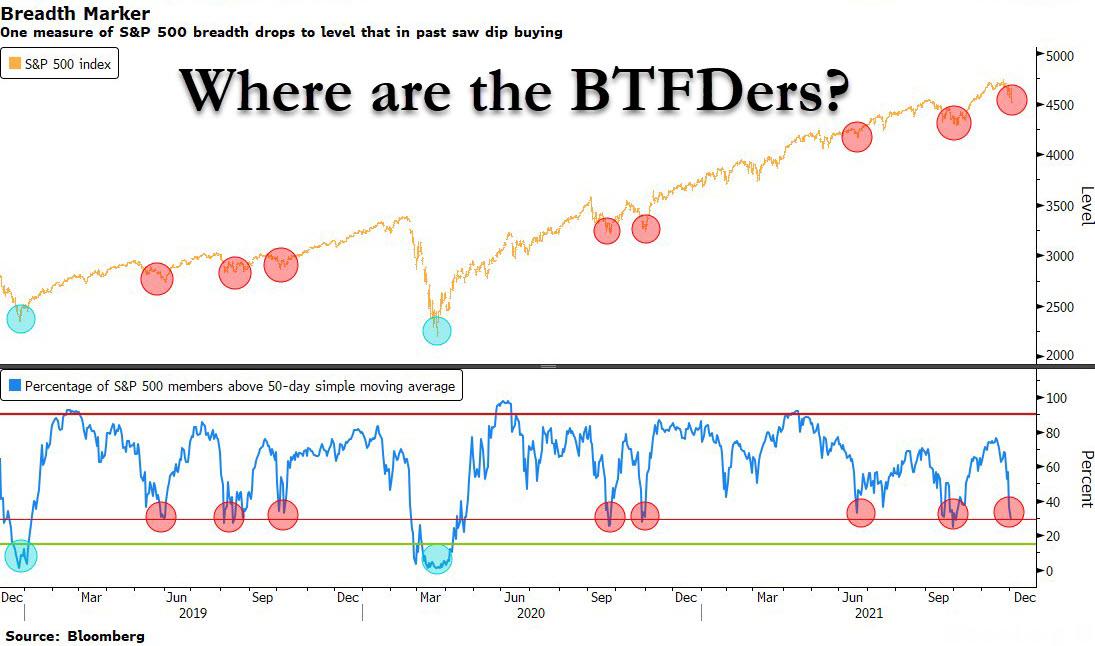

While the knee-jerk reaction of stock investors may “continue to be to take profits before the end of the year,” there is “plenty of liquidity available to drive stock prices higher as dip-buyers enter the market,” Ed Yardeni wrote in a note. The U.S. economy grew at a modest to moderate pace through mid-November, while price hikes were widespread amid supply-chain disruptions and labor shortages, the Federal Reserve said in its Beige Book survey Tuesday.

Cruise-ship operator Carnival jumped 3.8% in premarket trading, while Pfizer and Moderna fell as the World Health Organization said that existing vaccines will likely protect against severe cases of the variant. Boeing contracts gained 3.4% after a report that the flagship 737 Max aircraft has regained airworthiness approval in China. With lots of uncertainty surrounding the pandemic and Fed policy, the size of potential market swings is still considerable. Here are some other notable premarket movers today:

Apple (AAPL US) shares fell 1.8% in premarket trading after the iPhone maker was said to tell suppliers that demand for its flagship product has slowed. Wall Street analysts, however, remained bullish.

- U.S. stocks tied to former President Donald Trump rise in premarket trading following a report his media group is in talks to raise new financing. Digital World Acquisition (DWAC US) +24%, Phunware (PHUN US) +38%.

- Katapult (KPLT US) shares sink 14% in premarket after the financial technology firm said its gross originations over a two-month period were lower than 2020 levels.

- Vir (VIR US) shares jump 8.1% in premarket trading after its Covid-19 antibody treatment, co-developed with Glaxo, looked to be effective against the new omicron variant in early testing.

- Snowflake (SNOW US) is up 17% premarket following quarterly results that impressed analysts, though some raise questions over the data software company’s valuation.

- CrowdStrike (CRWD US) shares jumped 5.1% in premarket after it boosted its revenue forecast for the full year.

- Square’s (SQ US) shares are 0.4% higher premarket. Corporate name change to Block Inc. indicates “a symbolic rebirth,” according to Barclays as it shows a broader set of possibilities than those of a pure payments company.

- Okta’s (OKTA US) shares advanced in postmarket trading. 3Q results show the cybersecurity company is well- positioned to deliver growth, even if some analysts say its guidance looks conservative and that its growth was not as strong as in prior quarters.

The Omicron variant also hurt risk appetite, making the safe-haven bonds more attractive to investors, pushing yields down - although yields picked up again in early European trading. Volatility in equity markets as measured by the Vix hit its highest since February on Wednesday, before easing on Thursday, but remained well above this year’s average and almost twice as high as a month ago.

Investors are braced for volatility to continue through December, stirred by tightening central-bank policies to fight inflation just as the omicron variant complicates the outlook for the pandemic recovery. The recent market turmoil may offer investors a chance to position for a trend reversal in reopening and commodity trades, according to JPMorgan Chase & Co.

"Investors will need to maintain their calm during a period of uncertainty until the scientific data give a clearer picture of which scenario we face," said Mark Haefele, chief investment officer at UBS Global Wealth Management in Zurich. “This, in turn, will help shape the reaction of central bankers."

Also weighing on stock markets, and flattening the U.S. yield curve, were remarks by Federal Reserve Chair Jerome Powell, who said that he would consider a faster end to the Fed's bond-buying programme, which could open the door to earlier interest rate hikes. In his second day of testimony in Congress on Wednesday, Powell reiterated that the U.S. central bank needs to be ready to respond to the possibility that inflation does not recede in the second half of next year. read more

"In this past what we’ve seen is central banks using COVID as an excuse to remain dovish, and what we're seeing is central banks turn hawkish despite rising concerns around COVID, so it is a bit of a shift in communication," said Mohammed Kazmi, portfolio manager at UBP.

That said, the market is now so oversold, this is where we usually see aggressive dip-buying.

In Europe, tech companies were the worst performers after Apple warned its component suppliers of slowing demand for its iPhone 13, the news dragged index heavyweight ASML Holding NV more than 4%. Meanwhile, travel shares were among the worst performers as the omicron variant continued to pop upin countries around the world, including the U.S., Norway, Ireland and South Korea.

The Euro Stoxx 50 dropped as much as 1.7% while the Stoxx 600 Index fell 1.5%, extending declines to trade at a session low, with all sectors in the red and led lower by technology and travel stocks. The Stoxx 600 Technology Index slumped as much as 3.9%, the most in two months. Vifor Pharma surged by a record 18% following a report that Australia’s CSL is in advanced talks to acquire Swiss drugmaker. Here are some of the biggest European movers today:

- Vifor Pharma shares rise as much as 18% on a report that Australia’s CSL is in advanced talks to acquire the Swiss-based drug maker and developer while working with BofA on a A$4 billion funding package.

- Argenx jumps as much as 9.5% after Kepler Cheuvreux upgrades the stock to buy, saying the biotech company is on the brink of launching its first commercial product.

- Duerr gains as much as 7.2%, most since Aug. 10, after Deutsche Bank upgrades to buy and sets aa Street-high PT of EU60 for the German engineering company, citing the digitalization of the industry.

- Daily Mail & General Trust rises as much as 3.9% after Rothermere Continuation raised its bid for all DMGT’s Class A shares by 5.9% to 270p a share in cash.

- Klarabo surges as much as 54% as shares start trading on Nasdaq Stockholm after the Swedish property company raised SEK750m in an IPO.

- Eurofins Scientific declines for a fourth session, falling as much as 3.2%, as Goldman Sachs downgrades the company to neutral from buy “following strong outperformance YTD.”

- Deliveroo drops as much as 6.4% after an offering of 17.6m shares by CEO Will Shu and CFO Adam Miller at a price of 278p a share, representing a 4.2% discount to the last close.

- M&S falls as much as 3.4% after UBS cut its rating to neutral from buy, citing limited upside to its new price target as well as “little room for meaningful upgrades.”

Earlier in the session, Asian stocks erased an earlier loss to trade slightly up, as traders continued to assess the potential impact of the omicron virus strain and the Federal Reserve’s efforts to keep inflation in check. The MSCI Asia Pacific Index rose 0.2% after falling 0.4% in the morning. South Korea led regional gains, helped by large-cap chipmakers, while Japan was among the worst performers after the government dropped a plan for a blanket halt to all new incoming flight reservations. Asia’s equity benchmark is still down about 4% so far this year after rebounding in the past two sessions from a one-year low reached earlier this week.

Despite the region’s underperformance against the U.S. and Europe, cheap valuations and foreign-investor positioning have prompted brokerages including Credit Suisse Group AG and Nomura Securities Co. Ltd. to turn bullish on Asia’s prospects next year. “Equity markets continue to play omicron tennis and traders looking for short-term direction should just wait for the next virus headline and then act accordingly,” said Jeffrey Halley, a senior market analyst at Oanda Corp. “Volatility, and not market direction, will be the winner this week.” Chinese technology shares including Alibaba Group Holding slid after Beijing was said to be planning to close a loophole used by the sector to go public abroad, fueling concern over existing overseas listings.

Japanese equities declined, following U.S. peers lower after the first American case of the omicron coronavirus variant was confirmed. Electronics makers and telecoms were the biggest drags on the Topix, which fell 0.5%. SoftBank Group and TDK were the largest contributors to a 0.7% loss in the Nikkei 225. The S&P 500 posted its worst two-day selloff since October 2020 after the first U.S. case of the new strain was reported. Federal Reserve Chair Jerome Powell reiterated that officials should consider a quicker reduction of monetary stimulus amid elevated inflation. “Truth is, there’s probably a lot of people who are wanting to buy stocks at some point,” said Naoki Fujiwara, chief fund manager at Shinkin Asset Management. “But, with omicron still an unknown, people are responding sensitively to news development, and that’s keeping them from buying.”

India’s benchmark equity index climbed for a second day, led by software exporters, on an improving economic outlook and as investors grabbed some beaten-down stocks after recent declines. The S&P BSE Sensex Index rose 1.4% to close at 58,461.29 in Mumbai, the biggest advance since Nov. 1. Its two-day gains increased to 2.5%, the most since Aug. 31. The NSE Nifty 50 Index also surged by a similar magnitude. All of the 19 sector sub-indexes compiled by BSE Ltd. were up, led by a gauge of utilities companies. “India underperformed the global markets in recent weeks. Investors are now going for value buying in stocks at lower levels,” said A. K. Prabhakar, head of research at IDBI Capital Market Services. The Sensex gained in three of the past four sessions after plunging 2.9% on Friday, the biggest drop since April. The rally, however, is in contrast to most global peers which are witnessing volatility on worries over the spread of the omicron variant. High frequency indicators in India, such as tax collection and manufacturing activities, have shown robust growth in recent months, while the country’s economy expanded 8.4% in the quarter ended in September, according to an official data release on Tuesday. Mortgage lender HDFC contributed the most to the Sensex’s gain, increasing 3.9%. Out of 30 shares in the index, 27 rose and three fell.

In rates, trading has been relatively quiet as bunds and gilts bull steepen a touch with risk offered, while cash TSYs bear flatten, cheapening ~5bps across the curve.Treasuries retraced part of yesterday’s rally that sent the benchmark 30-year rate to the lowest since early January. A large buyer of 5-year U.S. Treasury options targets the yield dropping around 17bps. 5s10s, 5s30s spreads flattened by ~1bp and ~2bp to multimonth lows; 10-year yields around 1.43%, cheaper by more than 3bp on the day while bunds and gilt yields are richer by ~1bp. Front-end and belly of the curve underperform vs long-end, while bunds and gilts outperform Treasuries. With little economic data slated, speeches by several Fed officials are main focal points. Peripheral spreads tighten with 10y Spain outperforming after well received auctions, albeit with a small size on offer. U.S. economic data slate includes November Challenger job cuts (7:30am) and initial jobless claims (8:30am)

In FX, the Bloomberg Dollar Spot Index fell to a day low in the European session and the greenback traded mixed versus its Group-of-10 peers as most crosses consolidated in recent ranges. Two-week implied volatility in the major currencies trades in the green Thursday as it now captures the next policy decisions by the world’s major central banks. Euro- dollar on the tenor rises by as much as 138 basis points to touch 8.22%, highest in a year; the relative premium, however, remains below parity as realized has risen to levels unseen since August 2020. The pound rose along with some other risk- sensitive currencies following the British currency’s three-day slump against the dollar. Long-end gilts underperformed, leading to some steepening of the curve. The yen fell for the first day in three while the Swiss franc fell a second day. The Hungarian forint rose to almost a three-week high after the central bank in Budapest raised the one-week deposit rate by 20 basis points to 3.10%. Economists in a Bloomberg survey were evenly split in predicting a 10 or 20 basis point increase.

The Turkish lira resumed its slump after President Recep Tayyip Erdogan abruptly replaced his finance minister amid deepening rifts in the administration over aggressive interest-rate cuts that have undermined the currency and fueled inflation. Poland’s central bank Governor Adam Glapinski sent the zloty to a three-week high against the euro on Thursday with his changed rhetoric on inflation, which he no longer sees as transitory after prices surged at the fastest pace in more than two decades.

Currency market volatility also rose, with euro-dollar one-month volatility gauges below Monday's one-year peak but still at elevate levels .

"Liquidity in some areas of the market is still quite poor as people grapple with this news and as we head towards year-end, a lot of it is really liquidity driven, which is leading to some volatility," said UBP's Kazmi. "Even in the most liquid market of the U.S. treasury market we've seen some fairly large moves on very little newsflow at times."

In commodities, crude futures extend Asia’s gains. WTI adds 2.2% near $67, Brent near $70.50 ahead of today’s OPEC+ meeting. Spot gold finds support near Tuesday’s, recovering somewhat to trade near $1,774/oz. Base metals are mixed: LME aluminum drops as much as 1.1%, nickel, zinc and tin hold in the green

Looking at the day ahead now, and central bank speakers include the Fed’s Quarles, Bostic, Daly and Barkin, as well as the ECB’s Panetta. Data releases include the Euro Area unemployment rate and PPI inflation for October, while there’s also the weekly initial jobless claims. Lastly, the OPEC+ group will be meeting.

Market Snapshot

- S&P 500 futures up 0.7% to 4,540.25

- STOXX Europe 600 down 1.0% to 466.37

- MXAP up 0.2% to 192.07

- MXAPJ up 0.7% to 629.36

- Nikkei down 0.7% to 27,753.37

- Topix down 0.5% to 1,926.37

- Hang Seng Index up 0.5% to 23,788.93

- Shanghai Composite little changed at 3,573.84

- Sensex up 1.3% to 58,436.52

- Australia S&P/ASX 200 down 0.1% to 7,225.18

- Kospi up 1.6% to 2,945.27

- Brent Futures up 2.4% to $70.53/bbl

- Gold spot down 0.6% to $1,771.73

- U.S. Dollar Index little changed at 96.03

- German 10Y yield little changed at -0.35%

- Euro little changed at $1.1320

Top Overnight News from Bloomberg

- Federal Reserve Bank of Cleveland President Loretta Mester said she’s “very open” to scaling back the Fed’s asset purchases at a faster pace so it can raise interest rates a couple of times next year if needed

- A United Nations gauge of global food prices rose 1.2% last month, threatening to make it more expensive for households to put a meal on the table. It’s more evidence of inflation soaring in the world’s largest economies and may make it even harder for the poorest nations to import food, worsening a hunger crisis

- Germany is poised to clamp down on people who aren’t vaccinated against Covid-19 and drastically curtail social contacts to ease pressure on increasingly stretched hospitals

- Some investors buffeted by concerns about tighter monetary policy are turning their sights to China’s battered junk bonds, given they offer some of the biggest yield buffers anywhere in global credit markets

- Pfizer Inc. says data on how well its Covid-19 vaccine protects against the omicron variant should be available within two to three weeks, an executive said

- GlaxoSmithKline Plc said its Covid-19 antibody treatment looks to be effective against the new omicron variant in early testing

A more detailed look at global markets courtesy of Newsquawk

Asian equity markets traded tentatively following the declines on Wall St where all major indices extended on losses and selling was exacerbated on confirmation of the first Omicron case in the US, while the Asia-Pac region also contended with its own pandemic concerns. ASX 200 (-0.2%) was subdued amid heavy losses in the tech sector and with a surge of infections in Victoria state, although downside in the index was cushioned amid inline Retail Sales and Trade Balance, as well as M&A optimism after Woolworths made a non-binding indicative proposal for Australian Pharmaceutical Industries. Nikkei 225 (-0.7%) weakened after the government instructed airlines to halt inbound flight bookings for a month due to fears of the new variant and with auto names also pressured by declines in monthly sales amid the chip supply crunch. KOSPI (+1.6%) showed resilience amid expectations for lawmakers to pass a record budget today and recouped opening losses despite the record increase in daily infections and confirmation of its first Omicron cases, while the index also shrugged off the highest CPI reading in a decade which effectively supports the case for further rate increases by the BoK. Hang Seng (+0.6%) and Shanghai Comp. (-0.1%) were choppy following another liquidity drain by the PBoC and with tech pressured in Hong Kong as Alibaba shares extended on declines after recently slipping to a 4-year low in its US listing. Beijing regulatory tightening also provided a headwind as initial reports suggested China is to crack down on loopholes used by tech firms for foreign IPOs, although this was later refuted by China, and the CBIRC is planning stricter regulations on major shareholders of banks and insurance companies, as well as confirmed it will better regulate connected transactions of banks. Finally, 10yr JGBs were higher as prices tracked gains in global counterparts and amid the risk aversion in Japan, although prices are off intraday highs after hitting resistance during a brief incursion to the 152.00 level and despite the marginally improved metrics from 10yr JGB auction.

Top Asian News

- Asia Stocks Swing as Investors Weigh Omicron Impact, Fed Views

- Apple Tells Suppliers IPhone Demand Slowing as Holidays Near

- Moody’s Cuts China Property Sales View on Financing Difficulties

- Faith in Singapore Leaders Hit by Record Covid Wave, Poll Shows

Bourses across Europe have held onto losses seen at the cash open (Euro Stoxx 50 -1.4%; Stoxx -1.2%), as the region plays catchup to the downside seen on Wall Street – seemingly sparked by a concoction of hawkish Fed rhetoric and the discovery of the Omicron variant in the US. Nonetheless, US equity futures are firmer across the board but to varying degrees – with the cyclical RTY (+1.1%) and the NQ (+0.3%) the current laggard. European futures ahead of the cash open saw some mild fleeting impetus on reports GlaxoSmithKline's (-0.3%) COVID treatment Sotrovimab retains its activity against Omicron variant, and the UK MHRA simultaneously approved the use of Sotrovimab – but caveated that it is too early to know whether Omicron has any impact on effectiveness. Conversely, brief risk-off crept into the market following commentary from a South African Scientist who warned the country is seeing an exponential rise in new COVID cases with a predominance of Omicron variant across the country – with the variant causing the fastest ever community transmission - but expects fewer active cases and hospitalisations this wave. Back to Europe, Euro indices see broad-based losses whilst the downside in the FTSE 100 (-0.7%) is less severe amid support from its heavyweight Oil & Gas sector – the outperforming sector in the region. Delving deeper, sectors see no overarching theme nor bias – Food & Beverages, Autos and Banks are towards the top of the bunch, whilst Tech, Telecoms, and Travel &Leisure. Tech is predominantly weighed on by reports that Apple (-2% pre-market) reportedly told iPhone component suppliers that demand slowed down. As such ASML (-5.0%), STMicroelectronics (-4.4%) and Infineon (-3.6%) reside among the biggest losers in the Stoxx 600. Deliveroo (-5.3%) is softer following an offering of almost 18mln at a discount to yesterday's close. In terms of market commentary, Morgan Stanley believes that inflation will remain high over the next few months, in turn supporting commodities, financials and some cyclical sectors. The bank identifies beneficiaries including EDF (-1.5%), Engie (-1.2%), SSE (-0.2%), Legrand (-1.3%), Tesco (-0.5%), BT (-0.8%), Michelin (-1.6%) and Sika (-0.9%).

Top European News

- Shell Kicks Off First Wave of Buybacks From Permian Sale

- Omicron Threatens to Prolong Pain in Bid to Vaccinate the World

- Apple, Suppliers Drop Premarket After Report Demand Slowed

- Valeo, Gestamp Gain After Barclays Raises to Overweight

In FX, currency markets are still in a state of flux, or limbo bar a few exceptions, and the Greenback is gyrating against major peers awaiting the next major event that could provide clearer direction and a more decisive range break. Thursday’s agenda offers some scope on that front via US initial jobless claims and a host of Fed speakers, but in truth NFP tomorrow is probably more likely to be influential even though chair Powell has effectively given the green light to fast-track tapering from December. In the interim, the index continues to keep a relatively short leash around 96.000, and is holding within 96.138-95.895 confines so far today.

- JPY/CHF - Although risk considerations look supportive for the Yen, on paper, UST-JGB/Fed-BoJ differentials coupled with technical impulses are keeping Usd/Jpy buoyant on the 113.00 handle, with additional demand said to have come from Japanese exporters overnight. However, the headline pair may run into offers/resistance circa 113.50 and any breach could be capped by decent option expiry interest spanning 113.60-75 (1.5 bn). Similarly, the Franc has slipped back below 0.9200 on yield and Swiss/US Central Bank policy stances plus near term outlooks, and hardly helped by a slowdown in retail sales.

- GBP/CAD/NZD - All firmer vs their US counterpart, though again well within recent admittedly wide ranges, and the Pound perhaps more attuned to Eur/Gbp fluctuations as the cross retreats to retest 0.8500 and Cable rebounds to have another look at 1.3300 where a fairly big option expiry resides (850 mn). Indeed, Sterling has largely shrugged off the latest BoE Monthly Decision Maker Panel release that in truth did not deliver any clues on what is set to be another knife-edge MPC gathering in December. Elsewhere, the Loonie is straddling 1.2800 with eyes on WTI crude ahead of Canadian jobs data on Friday and the Kiwi is hovering above 0.6800 after weaker NZ Q3 terms of trade were offset to some extent by favourable Aud/Nzd headwinds.

- AUD/EUR - Both narrowly mixed against US Dollar, with the Aussie pivoting 0.7100 in wake of roughly in line trade and retail sales data overnight, but wary about the latest virus outbreak in the state of Victoria, while the Euro is sitting somewhat uncomfortably on the 1.1300 handle amidst softer EGB yields and heightened uncertainty about what the ECB might or might not do in December on the QE guidance front.

In commodities, WTI and Brent front-month futures are firmer intraday as traders gear up for the JMMC and OPEC+ confabs at 12:00GMT and 13:00GMT, respectively. The jury is still split on what the final decision could be, but the case for OPEC+ to pause the planned monthly relaxation of output curbs by 400k BPD has been strengthening against the backdrop of Omicron coupled with the coordinated SPR releases (an updating Rolling Headline is available on the Newsquawk headline feed). As expected, OPEC sources have been testing the waters in the run-up, whilst yesterday's JTC/OPEC meetings largely surrounded the successor to the Secretary-General position. Oil market price action will likely be centred around OPEC+ today in the absence of any macro shocks. WTI Jan resides around USD 66.50/bbl (vs low USD 65.41/bbl) whilst Brent Feb briefly topped USD 70/bbl (vs low USD 68.73/bbl). Elsewhere, spot gold has eased further from the USD 1,800/oz after failing to sustain a break above the 50, 100 and 200 DMAs which have all converged to USD 1,791/oz today. LME copper is on the backfoot amid the cautious risk sentiment, with the red metal back under USD 9,500/t but off overnight lows.

US Event Calendar

- 7:30am: Nov. Challenger Job Cuts -77.0% YoY, prior -71.7%

- 8:30am: Nov. Initial Jobless Claims, est. 240,000, prior 199,000; 8:30am: Nov. Continuing Claims, est. 2m, prior 2.05m

- 9:45am: Nov. Langer Consumer Comfort, prior 52.2

DB's Jim Reid concludes the overnight wrap

With investors remaining on tenterhooks to find out some definitive information on the Omicron variant, yesterday saw markets continue to see-saw for a 4th day running. Following one of the biggest sell-offs of the year on Friday, we then had a partial bounceback on Monday, another bout of fears on Tuesday (not helped by the prospect of faster tapering), and yesterday saw another rally back before risk sentiment turned sharply later in the day as an initial case of the Omicron variant was discovered in the US. You can get some idea of this by the fact that Europe’s STOXX 600 (+1.71%) posted its best daily performance since May, whereas the S&P 500 moved from an intraday high where it had been up +1.88%, before shedding all those gains and more to close -1.18% lower. In fact, that decline means the S&P has now lost over -3% in the last two sessions, marking its worst 2-day performance in over a year, and this heightened volatility saw the VIX index close back above 30 for the first time since early February.

In terms of developments about Omicron, we’re still in a waiting game for some concrete stats, but there was positive news early on from the World Health Organization’s chief scientist, who said that they think vaccines “will still protect against severe disease as they have against the other variants”. On the other hand, there was further negative news out of South Africa, as the country reported 8,561 infections over the previous day, with a positivity rate of 16.5%. That’s up from 4,373 cases the day before, and 2,273 the day before that, so all eyes will be on whether this trend continues, and also on what that means for hospitalisation and death rates over the days ahead.

Against this backdrop, calls for fresh restrictions mounted across a range of countries, particularly on the travel side. In the US, it’s been reported already by the Washington Post that President Biden could today announce stricter testing requirements for arriving travellers. Meanwhile, France is moving to require non-EU arrivals to show a negative test before arrival, irrespective of their vaccination status. The EU Commission further said that member states should conduct daily reviews of essential travel restrictions, and Commission President von der Leyen also said that the EU should discuss the topic of mandatory vaccinations. There was also a Bloomberg report that German Chancellor Merkel would recommend mandatory vaccinations from February 2022, according to a Chancellery paper that they’d obtained. That came as Slovakia sought to incentivise vaccination uptake among older citizens, with the cabinet backing a €500 hospitality voucher for residents over 60 who’ve been vaccinated.

As on Tuesday, the other main headlines yesterday were provided by Fed Chair Powell, who re-emphasised his more hawkish rhetoric around inflation before the House Financial Services Committee. Notably he said that “We’ve seen inflation be more persistent. We’ve seen the factors that are causing higher inflation to be more persistent”, though yields on 2yr Treasuries (-1.4bps) already had the shift in stance priced in. New York Fed President Williams echoed that view in an interview, noting it would be germane to discuss and decide whether it was appropriate to accelerate the pace of tapering at the December FOMC. 10yr yields (-4.1bps) continued their decline, predominantly driven by the turn in sentiment following the negative Omicron headlines. That latest round of curve flattening left the 2s10s slope at its flattest level since early January around the time of the Georgia Senate race that ushered in the prospect of much larger fiscal stimulus.

In terms of markets elsewhere, strong data releases helped to support risk appetite earlier in yesterday’s session, with investors also looking forward to tomorrow’s US jobs report for November that will be an important one ahead of the Fed’s decision in less than a couple of weeks’ time. The ISM manufacturing release for November saw the headline number come in roughly as expected at 61.1 (vs. 61.2 expected), and also included a rise in both the new orders (61.5) and the employment (53.3) components relative to last month. Separately, the ADP’s report of private payrolls for November likewise came in around expectations, with a +534k gain (vs. +526k expected).

Staying on the US, one thing to keep an eye out over the next 24 hours will be any news on a government shutdown, with funding currently set to run out by the weekend as it stands. The headlines yesterday weren’t promising for those hoping for an uneventful, tidy resolution, as Politico indicated that some Congressional Republicans would not agree to an expedited process to fund the government should certain vaccine mandates remain in place. An expedited process is necessary to avoid a government shutdown at the end of the week, so one to watch.

After the incredibly divergent equity performances in the US and Europe, we’ve seen a much more mixed performance in Asia overnight, with the KOSPI (+1.09%), Hang Seng (+0.23%), and CSI (+0.23%) all advancing, whereas the Shanghai Composite (-0.05%) and the Nikkei (-0.60%) are trading lower. In terms of the latest on Omicron, authorities in South Korea confirmed five cases, which came as the country also reported that CPI in November rose to its fastest since December 2011, at +3.7% (vs +3.1% expected). Separately in China, 53 local Covid-19 cases were reported in Inner Mongolia, whilst Harbin province reported 3 local cases. Looking forward, futures are indicating a positive start in the US with those on the S&P 500 (+0.64%) pointing higher.

Back in Europe, sovereign bonds lost ground yesterday, and yields on 10yr bunds (+0.5bps), OATs (+1.1bps) and BTPs (+4.2bps) continued to move higher. Interestingly, there was a continued widening in peripheral spreads, with the gap between both Italian and Spanish 10yr yields over bunds reaching their biggest level in over a year, at 135bps and 77bps, respectively. Another factor to keep an eye on in Europe is another round of increases in natural gas prices, with futures up +3.42% to their highest level since mid-October yesterday.

Lastly on the data front, the main other story was the release of the manufacturing PMIs from around the world. We’d already had the flash readings from a number of the key economies, so they weren’t too surprising, but the Euro Area came in at 58.4 (vs. flash 58.6), Germany came in at 57.4 (vs. flash 57.6), and the UK came in at 58.1 (vs. flash 58.2). One country that saw a decent upward revision was France, with the final number at 55.9 (vs. flash 54.6), which marks an end to 5 successive monthly declines in the French manufacturing PMI. One other release were German retail sales for October, which unexpectedly fell -0.3% (vs. +0.9% expected).

To the day ahead now, and central bank speakers include the Fed’s Quarles, Bostic, Daly and Barkin, as well as the ECB’s Panetta. Data releases include the Euro Area unemployment rate and PPI inflation for October, while there’s also the weekly initial jobless claims. Lastly, the OPEC+ group will be meeting.

Government

President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

President Biden Delivers The "Darkest, Most Un-American Speech Given By A President"

Having successfully raged, ranted, lied, and yelled through…

Share this:

Having successfully raged, ranted, lied, and yelled through the State of The Union, President Biden can go back to his crypt now.

Whatever 'they' gave Biden, every American man, woman, and the other should be allowed to take it - though it seems the cocktail brings out 'dark Brandon'?

Tl;dw: Biden's Speech tonight ...

-

Fund Ukraine.

-

Trump is threat to democracy and America itself.

-

Abortion is good.

-

American Economy is stronger than ever.

-

Inflation wasn't Biden's fault.

-

Illegals are Americans too.

-

Republicans are responsible for the border crisis.

-

Trump is bad.

-

Biden stands with trans-children.

-

J6 was the worst insurrection since the Civil War.

(h/t @TCDMS99)

Tucker Carlson's response sums it all up perfectly:

"that was possibly the darkest, most un-American speech given by an American president. It wasn't a speech, it was a rant..."

Carlson continued: "The true measure of a nation's greatness lies within its capacity to control borders, yet Bid refuses to do it."

"In a fair election, Joe Biden cannot win"

And concluded:

“There was not a meaningful word for the entire duration about the things that actually matter to people who live here.”

Victor Davis Hanson added some excellent color, but this was probably the best line on Biden:

"he doesn't care... he lives in an alternative reality."

— Tucker Carlson (@TuckerCarlson) March 8, 2024

* * *

Watch SOTU Live here...

* * *

Mises' Connor O'Keeffe, warns: "Be on the Lookout for These Lies in Biden's State of the Union Address."

On Thursday evening, President Joe Biden is set to give his third State of the Union address. The political press has been buzzing with speculation over what the president will say. That speculation, however, is focused more on how Biden will perform, and which issues he will prioritize. Much of the speech is expected to be familiar.

The story Biden will tell about what he has done as president and where the country finds itself as a result will be the same dishonest story he's been telling since at least the summer.

He'll cite government statistics to say the economy is growing, unemployment is low, and inflation is down.

Something that has been frustrating Biden, his team, and his allies in the media is that the American people do not feel as economically well off as the official data says they are. Despite what the White House and establishment-friendly journalists say, the problem lies with the data, not the American people's ability to perceive their own well-being.

As I wrote back in January, the reason for the discrepancy is the lack of distinction made between private economic activity and government spending in the most frequently cited economic indicators. There is an important difference between the two:

-

Government, unlike any other entity in the economy, can simply take money and resources from others to spend on things and hire people. Whether or not the spending brings people value is irrelevant

-

It's the private sector that's responsible for producing goods and services that actually meet people's needs and wants. So, the private components of the economy have the most significant effect on people's economic well-being.

Recently, government spending and hiring has accounted for a larger than normal share of both economic activity and employment. This means the government is propping up these traditional measures, making the economy appear better than it actually is. Also, many of the jobs Biden and his allies take credit for creating will quickly go away once it becomes clear that consumers don't actually want whatever the government encouraged these companies to produce.

On top of all that, the administration is dealing with the consequences of their chosen inflation rhetoric.

Since its peak in the summer of 2022, the president's team has talked about inflation "coming back down," which can easily give the impression that it's prices that will eventually come back down.

But that's not what that phrase means. It would be more honest to say that price increases are slowing down.

Americans are finally waking up to the fact that the cost of living will not return to prepandemic levels, and they're not happy about it.

The president has made some clumsy attempts at damage control, such as a Super Bowl Sunday video attacking food companies for "shrinkflation"—selling smaller portions at the same price instead of simply raising prices.

In his speech Thursday, Biden is expected to play up his desire to crack down on the "corporate greed" he's blaming for high prices.

In the name of "bringing down costs for Americans," the administration wants to implement targeted price ceilings - something anyone who has taken even a single economics class could tell you does more harm than good. Biden would never place the blame for the dramatic price increases we've experienced during his term where it actually belongs—on all the government spending that he and President Donald Trump oversaw during the pandemic, funded by the creation of $6 trillion out of thin air - because that kind of spending is precisely what he hopes to kick back up in a second term.

If reelected, the president wants to "revive" parts of his so-called Build Back Better agenda, which he tried and failed to pass in his first year. That would bring a significant expansion of domestic spending. And Biden remains committed to the idea that Americans must be forced to continue funding the war in Ukraine. That's another topic Biden is expected to highlight in the State of the Union, likely accompanied by the lie that Ukraine spending is good for the American economy. It isn't.

It's not possible to predict all the ways President Biden will exaggerate, mislead, and outright lie in his speech on Thursday. But we can be sure of two things. The "state of the Union" is not as strong as Biden will say it is. And his policy ambitions risk making it much worse.

* * *

The American people will be tuning in on their smartphones, laptops, and televisions on Thursday evening to see if 'sloppy joe' 81-year-old President Joe Biden can coherently put together more than two sentences (even with a teleprompter) as he gives his third State of the Union in front of a divided Congress.

President Biden will speak on various topics to convince voters why he shouldn't be sent to a retirement home.

The state of our union under President Biden: three years of decline. pic.twitter.com/Da1KOIb3eR

— Speaker Mike Johnson (@SpeakerJohnson) March 7, 2024

According to CNN sources, here are some of the topics Biden will discuss tonight:

Economic issues: Biden and his team have been drafting a speech heavy on economic populism, aides said, with calls for higher taxes on corporations and the wealthy – an attempt to draw a sharp contrast with Republicans and their likely presidential nominee, Donald Trump.

Health care expenses: Biden will also push for lowering health care costs and discuss his efforts to go after drug manufacturers to lower the cost of prescription medications — all issues his advisers believe can help buoy what have been sagging economic approval ratings.

Israel's war with Hamas: Also looming large over Biden's primetime address is the ongoing Israel-Hamas war, which has consumed much of the president's time and attention over the past few months. The president's top national security advisers have been working around the clock to try to finalize a ceasefire-hostages release deal by Ramadan, the Muslim holy month that begins next week.

An argument for reelection: Aides view Thursday's speech as a critical opportunity for the president to tout his accomplishments in office and lay out his plans for another four years in the nation's top job. Even though viewership has declined over the years, the yearly speech reliably draws tens of millions of households.

Sources provided more color on Biden's SOTU address:

The speech is expected to be heavy on economic populism. The president will talk about raising taxes on corporations and the wealthy. He'll highlight efforts to cut costs for the American people, including pushing Congress to help make prescription drugs more affordable.

Biden will talk about the need to preserve democracy and freedom, a cornerstone of his re-election bid. That includes protecting and bolstering reproductive rights, an issue Democrats believe will energize voters in November. Biden is also expected to promote his unity agenda, a key feature of each of his addresses to Congress while in office.

Biden is also expected to give remarks on border security while the invasion of illegals has become one of the most heated topics among American voters. A majority of voters are frustrated with radical progressives in the White House facilitating the illegal migrant invasion.

It is probable that the president will attribute the failure of the Senate border bill to the Republicans, a claim many voters view as unfounded. This is because the White House has the option to issue an executive order to restore border security, yet opts not to do so

Maybe this is why?

Most Americans are still unaware that the census counts ALL people, including illegal immigrants, for deciding how many House seats each state gets!

— Elon Musk (@elonmusk) March 7, 2024

This results in Dem states getting roughly 20 more House seats, which is another strong incentive for them not to deport illegals.

While Biden addresses the nation, the Biden administration will be armed with a social media team to pump propaganda to at least 100 million Americans.

"The White House hosted about 70 creators, digital publishers, and influencers across three separate events" on Wednesday and Thursday, a White House official told CNN.

Not a very capable social media team...

The State of Confusion https://t.co/C31mHc5ABJ

— zerohedge (@zerohedge) March 7, 2024

The administration's move to ramp up social media operations comes as users on X are mostly free from government censorship with Elon Musk at the helm. This infuriates Democrats, who can no longer censor their political enemies on X.

Meanwhile, Democratic lawmakers tell Axios that the president's SOTU performance will be critical as he tries to dispel voter concerns about his elderly age. The address reached as many as 27 million people in 2023.

"We are all nervous," said one House Democrat, citing concerns about the president's "ability to speak without blowing things."

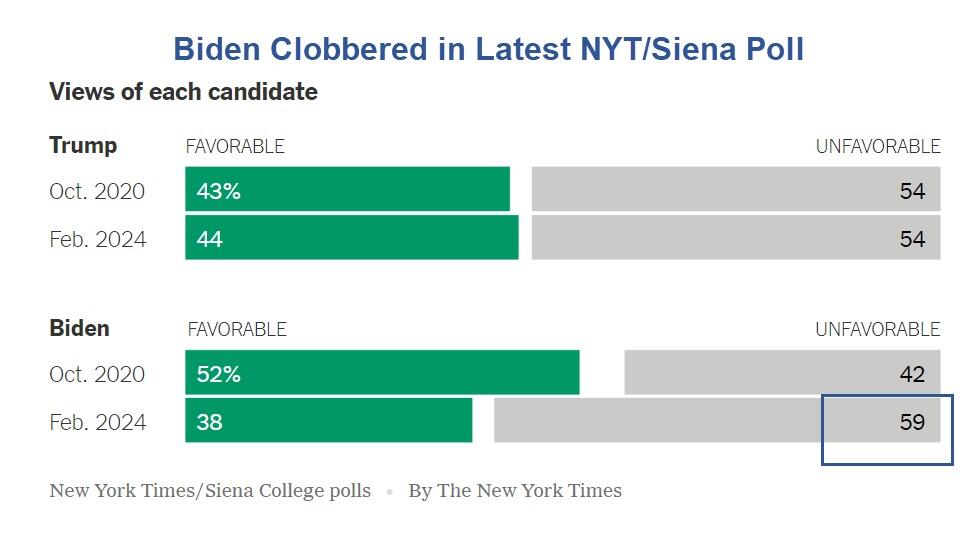

The SOTU address comes as Biden's polling data is in the dumps.

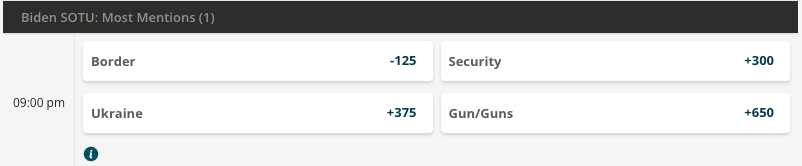

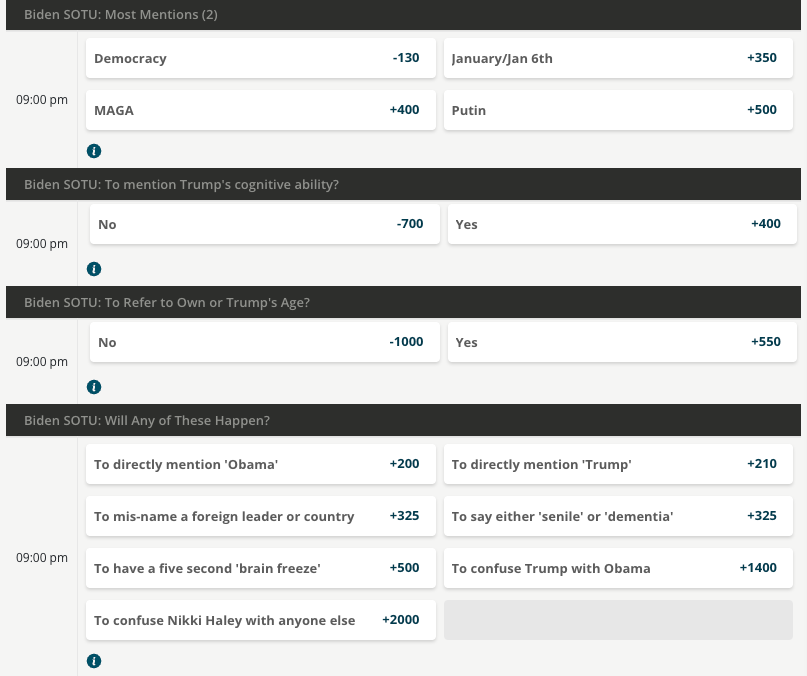

BetOnline has created several money-making opportunities for gamblers tonight, such as betting on what word Biden mentions the most.

As well as...

We will update you when Tucker Carlson's live feed of SOTU is published.

Fuck it. We’ll do it live! Thursday night, March 7, our live response to Joe Biden’s State of the Union speech. pic.twitter.com/V0UwOrgKvz

— Tucker Carlson (@TuckerCarlson) March 6, 2024

International

What is intersectionality and why does it make feminism more effective?

The social categories that we belong to shape our understanding of the world in different ways.

Share this:

The way we talk about society and the people and structures in it is constantly changing. One term you may come across this International Women’s Day is “intersectionality”. And specifically, the concept of “intersectional feminism”.

Intersectionality refers to the fact that everyone is part of multiple social categories. These include gender, social class, sexuality, (dis)ability and racialisation (when people are divided into “racial” groups often based on skin colour or features).

These categories are not independent of each other, they intersect. This looks different for every person. For example, a black woman without a disability will have a different experience of society than a white woman without a disability – or a black woman with a disability.

An intersectional approach makes social policy more inclusive and just. Its value was evident in research during the pandemic, when it became clear that women from various groups, those who worked in caring jobs and who lived in crowded circumstances were much more likely to die from COVID.

A long-fought battle

American civil rights leader and scholar Kimberlé Crenshaw first introduced the term intersectionality in a 1989 paper. She argued that focusing on a single form of oppression (such as gender or race) perpetuated discrimination against black women, who are simultaneously subjected to both racism and sexism.

Crenshaw gave a name to ways of thinking and theorising that black and Latina feminists, as well as working-class and lesbian feminists, had argued for decades. The Combahee River Collective of black lesbians was groundbreaking in this work.

They called for strategic alliances with black men to oppose racism, white women to oppose sexism and lesbians to oppose homophobia. This was an example of how an intersectional understanding of identity and social power relations can create more opportunities for action.

These ideas have, through political struggle, come to be accepted in feminist thinking and women’s studies scholarship. An increasing number of feminists now use the term “intersectional feminism”.

The term has moved from academia to feminist activist and social justice circles and beyond in recent years. Its popularity and widespread use means it is subjected to much scrutiny and debate about how and when it should be employed. For example, some argue that it should always include attention to racism and racialisation.

Recognising more issues makes feminism more effective

In writing about intersectionality, Crenshaw argued that singular approaches to social categories made black women’s oppression invisible. Many black feminists have pointed out that white feminists frequently overlook how racial categories shape different women’s experiences.

One example is hair discrimination. It is only in the 2020s that many organisations in South Africa, the UK and US have recognised that it is discriminatory to regulate black women’s hairstyles in ways that render their natural hair unacceptable.

This is an intersectional approach. White women and most black men do not face the same discrimination and pressures to straighten their hair.

“Abortion on demand” in the 1970s and 1980s in the UK and USA took no account of the fact that black women in these and many other countries needed to campaign against being given abortions against their will. The fight for reproductive justice does not look the same for all women.

Similarly, the experiences of working-class women have frequently been rendered invisible in white, middle class feminist campaigns and writings. Intersectionality means that these issues are recognised and fought for in an inclusive and more powerful way.

In the 35 years since Crenshaw coined the term, feminist scholars have analysed how women are positioned in society, for example, as black, working-class, lesbian or colonial subjects. Intersectionality reminds us that fruitful discussions about discrimination and justice must acknowledge how these different categories affect each other and their associated power relations.

This does not mean that research and policy cannot focus predominantly on one social category, such as race, gender or social class. But it does mean that we cannot, and should not, understand those categories in isolation of each other.

Ann Phoenix does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

africa uk pandemicGovernment

Biden defends immigration policy during State of the Union, blaming Republicans in Congress for refusing to act

A rising number of Americans say that immigration is the country’s biggest problem. Biden called for Congress to pass a bipartisan border and immigration…

Share this:

{kind=link}

{kind=link}

President Joe Biden delivered the annual State of the Union address on March 7, 2024, casting a wide net on a range of major themes – the economy, abortion rights, threats to democracy, the wars in Gaza and Ukraine – that are preoccupying many Americans heading into the November presidential election.

The president also addressed massive increases in immigration at the southern border and the political battle in Congress over how to manage it. “We can fight about the border, or we can fix it. I’m ready to fix it,” Biden said.

But while Biden stressed that he wants to overcome political division and take action on immigration and the border, he cautioned that he will not “demonize immigrants,” as he said his predecessor, former President Donald Trump, does.

“I will not separate families. I will not ban people from America because of their faith,” Biden said.

Biden’s speech comes as a rising number of American voters say that immigration is the country’s biggest problem.

Immigration law scholar Jean Lantz Reisz answers four questions about why immigration has become a top issue for Americans, and the limits of presidential power when it comes to immigration and border security.

1. What is driving all of the attention and concern immigration is receiving?

The unprecedented number of undocumented migrants crossing the U.S.-Mexico border right now has drawn national concern to the U.S. immigration system and the president’s enforcement policies at the border.

Border security has always been part of the immigration debate about how to stop unlawful immigration.

But in this election, the immigration debate is also fueled by images of large groups of migrants crossing a river and crawling through barbed wire fences. There is also news of standoffs between Texas law enforcement and U.S. Border Patrol agents and cities like New York and Chicago struggling to handle the influx of arriving migrants.

Republicans blame Biden for not taking action on what they say is an “invasion” at the U.S. border. Democrats blame Republicans for refusing to pass laws that would give the president the power to stop the flow of migration at the border.

2. Are Biden’s immigration policies effective?

Confusion about immigration laws may be the reason people believe that Biden is not implementing effective policies at the border.

The U.S. passed a law in 1952 that gives any person arriving at the border or inside the U.S. the right to apply for asylum and the right to legally stay in the country, even if that person crossed the border illegally. That law has not changed.

Courts struck down many of former President Donald Trump’s policies that tried to limit immigration. Trump was able to lawfully deport migrants at the border without processing their asylum claims during the COVID-19 pandemic under a public health law called Title 42. Biden continued that policy until the legal justification for Title 42 – meaning the public health emergency – ended in 2023.

Republicans falsely attribute the surge in undocumented migration to the U.S. over the past three years to something they call Biden’s “open border” policy. There is no such policy.

Multiple factors are driving increased migration to the U.S.

More people are leaving dangerous or difficult situations in their countries, and some people have waited to migrate until after the COVID-19 pandemic ended. People who smuggle migrants are also spreading misinformation to migrants about the ability to enter and stay in the U.S.

3. How much power does the president have over immigration?

The president’s power regarding immigration is limited to enforcing existing immigration laws. But the president has broad authority over how to enforce those laws.

For example, the president can place every single immigrant unlawfully present in the U.S. in deportation proceedings. Because there is not enough money or employees at federal agencies and courts to accomplish that, the president will usually choose to prioritize the deportation of certain immigrants, like those who have committed serious and violent crimes in the U.S.

The federal agency Immigration and Customs Enforcement deported more than 142,000 immigrants from October 2022 through September 2023, double the number of people it deported the previous fiscal year.

But under current law, the president does not have the power to summarily expel migrants who say they are afraid of returning to their country. The law requires the president to process their claims for asylum.

Biden’s ability to enforce immigration law also depends on a budget approved by Congress. Without congressional approval, the president cannot spend money to build a wall, increase immigration detention facilities’ capacity or send more Border Patrol agents to process undocumented migrants entering the country.

4. How could Biden address the current immigration problems in this country?

In early 2024, Republicans in the Senate refused to pass a bill – developed by a bipartisan team of legislators – that would have made it harder to get asylum and given Biden the power to stop taking asylum applications when migrant crossings reached a certain number.

During his speech, Biden called this bill the “toughest set of border security reforms we’ve ever seen in this country.”

That bill would have also provided more federal money to help immigration agencies and courts quickly review more asylum claims and expedite the asylum process, which remains backlogged with millions of cases, Biden said. Biden said the bipartisan deal would also hire 1,500 more border security agents and officers, as well as 4,300 more asylum officers.

Removing this backlog in immigration courts could mean that some undocumented migrants, who now might wait six to eight years for an asylum hearing, would instead only wait six weeks, Biden said. That means it would be “highly unlikely” migrants would pay a large amount to be smuggled into the country, only to be “kicked out quickly,” Biden said.

“My Republican friends, you owe it to the American people to get this bill done. We need to act,” Biden said.

Biden’s remarks calling for Congress to pass the bill drew jeers from some in the audience. Biden quickly responded, saying that it was a bipartisan effort: “What are you against?” he asked.

Biden is now considering using section 212(f) of the Immigration and Nationality Act to get more control over immigration. This sweeping law allows the president to temporarily suspend or restrict the entry of all foreigners if their arrival is detrimental to the U.S.

This obscure law gained attention when Trump used it in January 2017 to implement a travel ban on foreigners from mainly Muslim countries. The Supreme Court upheld the travel ban in 2018.

Trump again also signed an executive order in April 2020 that blocked foreigners who were seeking lawful permanent residency from entering the country for 60 days, citing this same section of the Immigration and Nationality Act.

Biden did not mention any possible use of section 212(f) during his State of the Union speech. If the president uses this, it would likely be challenged in court. It is not clear that 212(f) would apply to people already in the U.S., and it conflicts with existing asylum law that gives people within the U.S. the right to seek asylum.

Jean Lantz Reisz does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

congress senate trump pandemic covid-19 mexico ukraine

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Redefining Poverty: Towards a Transpartisan Approach

Catastrophic Risk: Investing and Business Implications

The Digest #187

Biden to call for first-time homebuyer tax credit, construction of 2 million homes

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Deterra Royalties half-yearly result: stable performance and growth Initiatives

Deflationary pressures in China – be careful what you wish for

Is “Greedflation” Over?

Revving up tourism: Formula One and other big events look set to drive growth in the hospitality industry

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges