Government

What Flood?

What Flood?

Share this:

Another 2.1 million Americans have filed this week with their state governments in order to determine their eligibility for unemployment insurance. That brings the 10-week disaster total for these initial jobless claims to an enormous 40.8 million. How did it get to be so many, and why, as states are opening back up, is it continuing in the millions all the way through the month of May?

This is not simply a case of disease and the panicked government response to really, really bad virus models. It is almost certainly, as I’ve written throughout the pandemic, the combination of three big errors all drawn from what’s always called objective science but in reality are dangerously simplified subjective opinions based on very little useful knowledge.

The epidemiology estimates aren’t even the biggest of the three mistakes.

Those belong to econometrics, as usual, which told politicians worldwide that the global economy in general, and various domestic economies specifically, were in pretty good shape to begin this thing. Trade wars were receding and central banks had responded in force to what the models all treated as an otherwise rapidly fading minor nuisance (in actuality a globally synchronized downturn).

With central banks and federal governments now throwing “stimulus” into overdrive, the perceived effectiveness of which being their third error, the prior belief in the strong economy starting point absolutely convinced officials they could institute these devastating shutdowns with manageable economic disruption.

Only, these negatives continue to seriously pile up week after week. Even the Fed Chairman realizes for his actual contributions (very little) he’s put everyone in a very tough spot. Therefore, the really obvious and truly shameful fit of outright lying.

Companies are clearly still in the mood to purge employees. Why?

After all, the government has handed out hundreds of billions in cash loans (which will almost certainly be forgiven, meaning they’ll be turned into grants) for all sorts of purposes on top of the “helicopter” payments to citizens meant to keep up some minimally acceptable level of overall spending.

To begin with, the thing about jobless claims is that you first have to be involuntarily separated from your previous employer. This rules out the “gaming” of the system taking place as Congress generously bumped up unemployment payments more than what the lowest paid workers receive. In other words, you can’t quit your job in order to get paid more on unemployment; the process begins, and ends, with employer action.

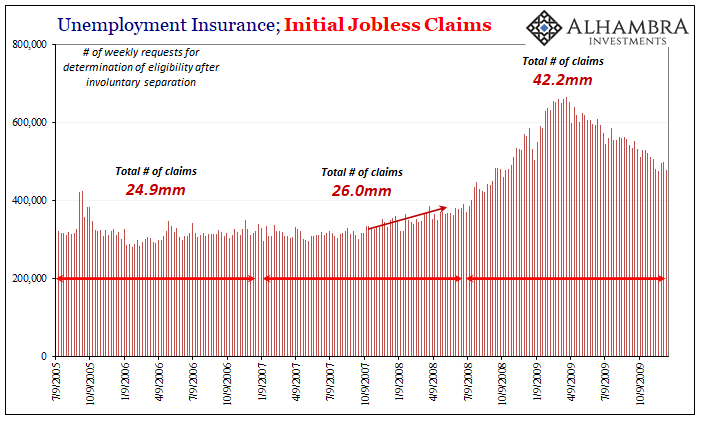

To give us a sense of the relevant context, we can go back to the Great “Recession” for some badly needed scale. While 40.8 million in 2020 is whatever counts as more than alarming, over the worst part of the 2008-09 contraction jobless claims added up to about 42.2 million. That compared to around 25 million in the same number of weeks (about a year and a half) over the last half of 2005 and all of 2006, and then 26 million throughout 2007 and through the first half of 2008.

It was only around July 2008 that jobless claims really accelerated. And, as the cumulative total piled up by October 2008, that plus the obviousness of GFC1 changed the labor force in a way no post-war recession had before. American workers began dropping out of it by the hundreds of thousands, thus beginning the as-yet unresolved participation problem right in the thick of what was a global dollar shortage.

Subprime mortgages ultimately had very little to do with any of this. It had instead everything to do with liquidity and company behavior.

Given that it was a monetary event, you can begin to appreciate why it had become so bad in the labor market (a net increase of ~16 million jobless claims beginning in July 2008 represented a truly enormous wave of layoffs). Companies weren’t just hit with declining revenues, as in any recession, they also were made to understand how they couldn’t depend upon banks and markets for even the basics of working capital cash.

Liquidity risks were no longer mere troubling perceptions, survival was at stake for even the best of names.

I’m talking about companies like McDonalds which needed (and always needs) to fund working capital regardless of health, ill or not, on its top or bottom lines. Banks withdrew liquidity backstops and credit lines, and then commercial paper became impossible to negotiate on reasonable terms.

Some like McDonalds, Verizon, and Caterpillar were forced to almost beg. In one of the more absurd aspects of the 2008 panic, there was the global fastfood chain knocking at the door of the Federal Reserve getting it to buy commercial paper the market wouldn’t on any terms. Big Macs had become Too Big To Fail, too.

What do you do if as a C-Suite officer you found yourself in such a situation? The first thing is that you vow never to be so vulnerable again. As a company, you make it a policy, informal or otherwise, to self-insure on liquidity. That means any number of things, up to and including holding large cash balances far greater than you ever would have before August 2007.

While the panic was ongoing, slash to the bone! Conserve cash at all costs, including an over-attention to the cost structure – therefore, the shocking number of 2008 and 2009 layoffs that actually continued well into 2010. It was that bad, as the American labor force began to realize right when it started in October 2008.

And it explains a lot about why jobless claims have been so low over the last ten years since the labor market finally bottomed out; that attention to liquidity risk and therefore the cost structure has never gone away. Layoffs have been minimal for years because businesses never hired that many back. Job growth has likewise been almost non-existent (2mm payrolls per year is pitiful) precluding the need for large numbers of layoffs and employee turnover in the post-GFC1 era.

The Fed says it flooded the world with liquidity, but companies sure haven’t seen it, or acted out, that way.

Now the truly shocking turn of events in March 2020, beginning with another prime example of helpless, hopeless, hapless central bankers. Jobless claims keep going, ten weeks now and still more than 2 million. The layoffs haven’t stopped; they’ve not come close to stopping, apparently. That net change of +23 million even had it taken a year and a half like during the Great “Recession” would have represented a massive deflationary wave.

All in ten weeks!

Again, why?

To piece together some answer – beyond the overly simplistic COVID-19, duh – we’ll first turn to JP Morgan’s Jamie Dimon (of all people). Though he likes to opine on interest rates in a way that must please Jay Powell to no end, Dimon’s annual letter to shareholders written last month surely did not.

Companies have already drawn down more than $50 billion of their revolvers to prepare themselves for the crisis (this already dramatically exceeds what happened in the global financial crisis). Many others have requested additional credit, which we have been offering judiciously – more than $25 billion of new credit extensions were approved in the month of March alone. [emphasis added]

Those like McDonalds and Caterpillar who learned something important about the last time, GFC1, they aren’t going to count on the Fed for a “flood” of liquidity this time around.

And it’s the Fed’s data that gives us the systemic scale to this contradictory belief in action. Commercial and Industrial (C&I) loans have absolutely surged, up more than 25% in just two months. The very same two months, of course, as jobless claims.

Prior to GFC2, C&I loans had been on the downswing dating back to January 2019 (the late 2018 landmine). Corporate America, it seems, had been in no mood to borrow and invest productively throughout last year, with the balance of this credit actually shrinking modestly from August 2019 up to February 2020. Hardly an indication of the strong economic start to this mess.

March and April, on the contrary, are unprecedented. There’s nothing like this anywhere in the series. Furthermore, it’s continued right on through the end of May (just like jobless claims) in the Fed’s weekly H.8 figures – another $100 billion added in the last four weeks (up to last week).

Corporate managers primed to invest given so much “stimulus?” Absolutely not. The extraordinary actions in drawing cash from revolvers during the Fed’s greatest monetary “flood” in its history is like bond yields a negative reflection against monetary policy.

There’s no money in it, as US (and global) companies know only too well from experience. Repeated experience.

To which the BEA provides more evidence and color. In its updated estimates for Q1 real GDP, revised down to -5.1%, we get our first look at corporate profits during the first quarter, before all this really got started.

With profits sinking sharply in Q1, that plus liquidity fears (materializing during GFC2 with the same kinds of credit and cash disruptions witnessed a dozen years earlier) have undoubtedly supercharged the negative pressures the COVID-19 shutdowns injected.

The models never saw any of it coming. But, as noted yesterday, they’re now starting to get some sense of it – and it ain’t pretty.

The lingering economic issues won’t be the coronavirus but the liquidity virus. The financial media and those in the financial services industry think of the Fed as being this awesome monetary instrument, effective in whatever it undertakes, while real economy participants see the central bank in a very different way.

Right there’s the net 23.8 million jobless claims and the fact it only took ten weeks for all these separations.

What the mainstream pictures of Jay Powell:

What Jay Powell really is (as real economy participants like banks in the bond market realize):

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Government

Walmart joins Costco in sharing key pricing news

The massive retailers have both shared information that some retailers keep very close to the vest.

Share this:

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trumpGovernment

Walmart has really good news for shoppers (and Joe Biden)

The giant retailer joins Costco in making a statement that has political overtones, even if that’s not the intent.

Share this:

{kind=link}

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trump

The Coming Of The Police State In America

When Military Rule Supplants Democracy

Catastrophic Risk: Investing and Business Implications

Dropping Like a Stone: ON RRP Take‑up in the Second Half of 2023

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

The Digest #187

Redefining Poverty: Towards a Transpartisan Approach

Students lose out as cities and states give billions in property tax breaks to businesses − draining school budgets and especially hurting the poorest students

Is the United States overestimating China’s power?

Biden to call for first-time homebuyer tax credit, construction of 2 million homes

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 day ago

International1 day agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire