Government

The Rapidly Failing EU

The Rapidly Failing EU

Authored by Alasdair Macleod via GoldMoney.com,

It is not widely realised that the EU concept is on its last legs. The bureaucratic inefficiencies and bad leadership were fully exposed last week over the inability…

Share this:

Authored by Alasdair Macleod via GoldMoney.com,

It is not widely realised that the EU concept is on its last legs. The bureaucratic inefficiencies and bad leadership were fully exposed last week over the inability of the EU to distribute vaccines and the attempts to blame everyone else. But a larger problem is hidden in the euro structure, comprised of banking and TARGET2 settlement systems.

This article discusses the precarious financial position of the commercial banks and the gaming of the TARGET2 system by national regulators to hide bad debts. The bad debt situation is now set to deteriorate at a faster pace thanks to the economic consequences of coronavirus lockdowns and is not helped by lack of vaccines, which defers the return to economic normality.

It is no exaggeration to conclude that the failure of its settlement system will bring down the ECB and the national central banks. The ECB will be gone, and NCBs will reform to administer new national currencies — there can be no other outcome.

With the euro failure the European Commission is likely to cede power to national interests, heralding a new era of immense political uncertainty as new currencies and government financing arrangements are devised.

Introduction

At a political level there appears to be frightening levels of ignorance about the economic consequences of punishing Britain for Brexit at a time when the EU’s own economy is teetering on the edge of a financial crisis.

Last week Britain’s remaining Remainers were revealed by the extraordinary behaviour of the European Union to have been little more than tilting at windmills. Without consulting the Irish or the British, the Commission triggered Article 16 of the Trade and Cooperation Agreement, in effect putting a customs border between Ireland and Northern Ireland. This was in direct contravention of earlier promises to respect the Good Friday agreement by not doing so. It was at the EU’s insistence that no border should exist onshore, separating Northern Ireland from the rest of the UK for customs’ purposes. Despite this breach of an agreement upon which the ink was barely dry, the British government managed to keep its cool and persuade the EU to reconsider and back down.

The reason for recounting these events is to make the point that the EU system apparently has been designed to promote and appoint the unelectable in a grand-scale parody of the Peter principle. This origins behind this particular foul-up were bureaucratic. The EU was determined to take covid vaccine distribution out of the hands of member states and then procrastinated for three vital months while other nations such as the UK and US placed advanced orders for hundreds of millions of vaccines.

Policies, mostly political without much regard to economic consequences, get mired in EU bureaucracy, plus the need often to consult 27 different member states and print labels in all their different languages. Consequently, the European Medicines Agency, which reportedly was closed on holiday between 23 December and 4 January in the middle of the pandemic, only approved the AstraZeneca vaccine last Friday, by which time Britain had already vaccinated millions.

Far fewer Europeans proportionately have been immunised, with dire political consequences for Europe’s national leaders, particularly those with elections looming, such as in France. The Italian government has fallen, yet again, with its handling of the coronavirus crisis very much to blame. And unusually for the normally tolerant Dutch public, even they have rioted in the streets.

This is not the only post-Brexit teething problem. The UK government refused to accord diplomatic status to the EU on the basis that member nations are represented in London already and that the EU is not a state, but a commission. Logistics are still being fouled up between the UK and France by weaponised bureaucracy, which is already leading to further friction at senior government levels.

Behind it all appears to be an overriding desire to punish the UK for Brexit. To the other 27 nations remaining in the EU the UK must be shown to suffer from the disadvantages of independence. This is why the British success in vaccinating its own population and the ineptitude of the EU rankles so much. If the focus on punishing the UK for Brexit continues, it may hurt the British economy, but more importantly it will hurt the EU even more, bearing in mind trade imbalances between the two favour the EU’s exports.

The EU is sacrificing its own economy when it can least afford to do so. But while we are deflected by the politics, there are far deeper issues to do with economics and money.

The monetary error behind the EU concept

The concept underlying the EU can be summed up as the socialising of the wealth of the northern states to subsidise the southern and less developed member nations. In keeping with its post-war low political profile, Germany went along with the European project’s evolution from being a trading bloc into a currency union.

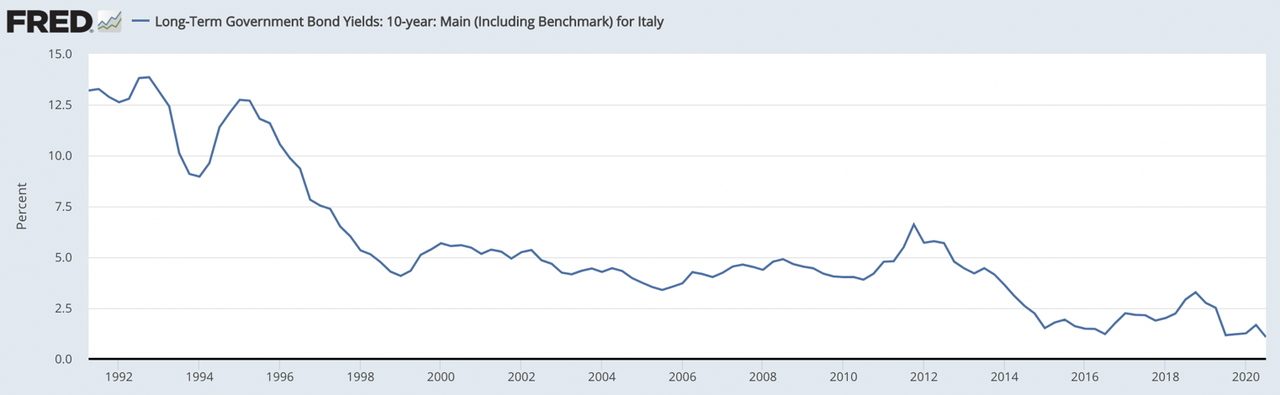

The euro was intended to be a leveller, enabling nations like Italy, Spain and Greece to piggyback on Germany’s debt rating, on the statist argument that being issued by a sovereign nation tied into a common currency and settlement system, there is little difference between owning German and Italian, or even Greek sovereign debt. The consequences were that through investing institutions Germany’s savers directly and indirectly subsidised debt issued at levels that fail to compensate for the borrower’s true risk. The FRED chart below shows the effect on the Italian 10-year benchmark bond yield.

In the run up to the replacement of national currencies by the euro the Maastricht rules for qualification were ignored, otherwise Italy’s level of sovereign debt would have disqualified its entry. The market rate for Italy’s 10-year government bond was a yield of 12.4% when the Maastricht treaty setting the conditions for entry into monetary union came into effect in 1992. Germany’s equivalent benchmark yielded 8.3%. Today the German benchmark yields minus 0.62% and the Italian plus 1.07%. Not only has the gap converged to less than 2%, but by the end of 2020 the quantity of Italian government debt had increased to over 150% of GDP.

Similar examples can be made of the other PIGS — Portugal, Greece and Spain. Clearly, the evidence is that markets are not pricing sovereign risk as they should, and their yields are being heavily suppressed. The outlook for budget deficits in these nations is simply dire, even leading to recent speculation that the ECB will have to cancel some of its huge holdings of the PIGS’s government debt.

That this is the case leads us to define the basic flaw in the euro system: it is not an economically determined project at all; it is simply a political construction to deliver political objectives.

The ECB and its impossible task

In the introduction we laid bare the lack of bureaucratic urgency over vaccination procurement and the subsequent panic in Brussels. By way of contrast, the ECB’s president served as Chair of the IMF and before that held a number of roles in the French government, including economy and finance minister. She was appointed to the ECB as a safe pair of hands. And as such, she has inherited an impossible position, because she has no mandate to moderate the inflationary policies she inherited

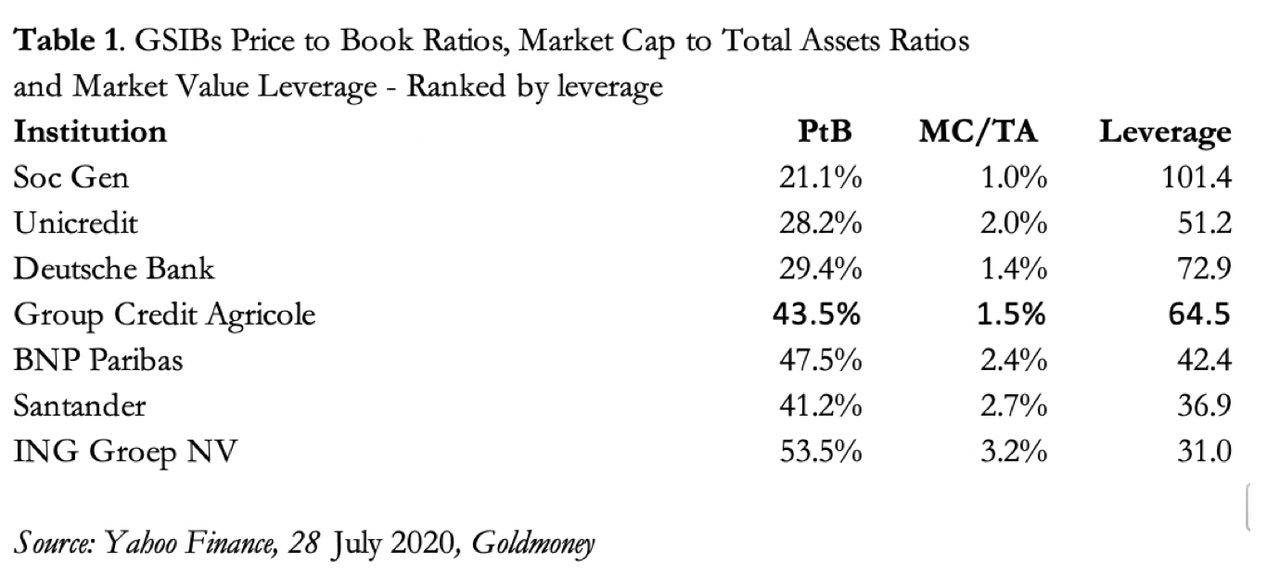

More correctly, she inherited two impossibilities. The first is to continue to distribute Germany’s national savings to support the PIGS, and the second is a banking system that is well and truly broken. Table 1 shows the relationship between the Eurozone G-SIBs’ balance sheet totals, their balance sheet equity and market capitalisations to illustrate the latter point.

G-SIB is the acronym for a global systemically important bank, which has extra capital buffers designed to ensure it does not create or spread counterparty risk. By implication, smaller banks are less secure, so these Eurozone G-SIBs should be better capitalised in terms of available liquidity. Yet, when one observes that Société Générale’s equity valuation in the market is only 21.1% of its book value, giving shareholders a market leverage of 101.4 times its balance sheet one must take note. And in taking note the true level of non-performing loans should also be established as well as any off-balance sheet liabilities. Other Eurozone G-SIBS are less operationally geared for their shareholders, but there is little doubt that their market ratings inform us that after taking account of undeclared NPLs many of them are not only technically insolvent but shouldn’t be trading.

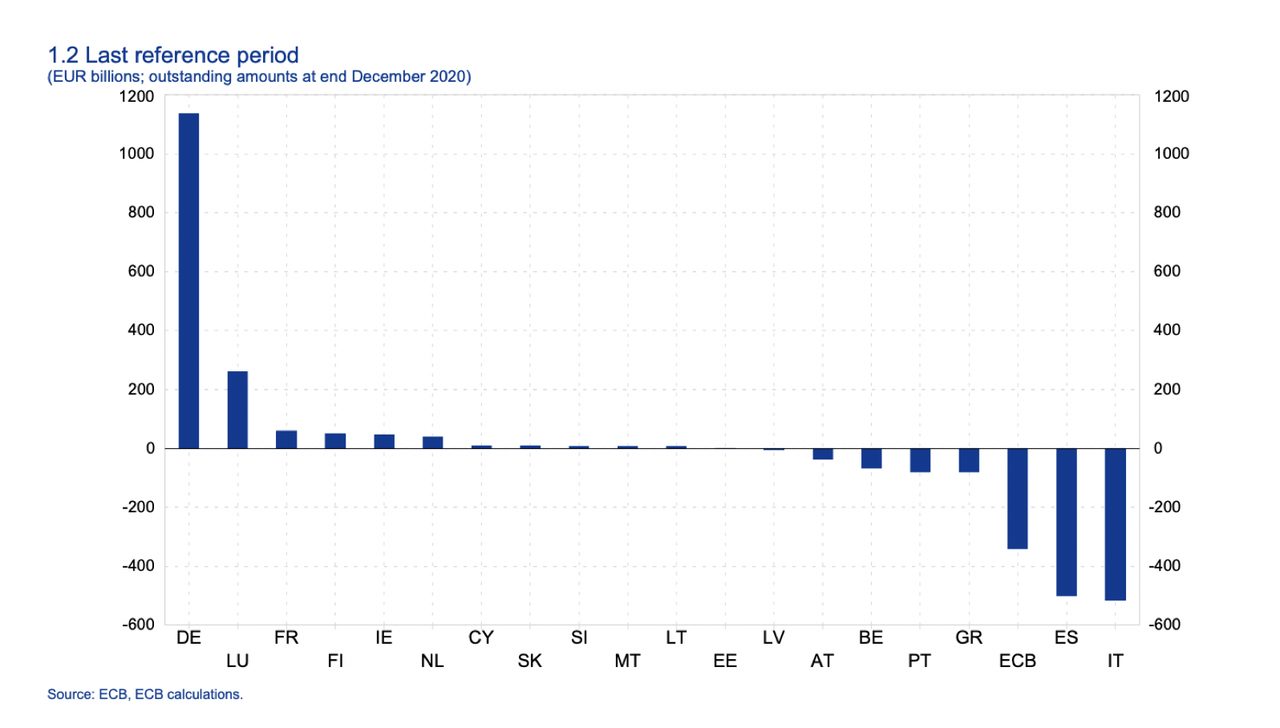

Much of the devil is to be found in those non-performing loans. It has become routine for national regulators to deem them performing so that they can act as collateral for loans from the national central bank. When they then become lost in the TARGET2 settlement system they are forgotten, and miraculously the commercial bank appears solvent again. But TARGET2 becomes riddled with those bad debts and imbalances arise as the next chart from the ECB’s data warehouse shows.

This is one way Germany’s national savings are being redistributed to the PIGS. At end-December, Germany’s Bundesbank was “owed” €1,136bn, an amount that has increased by 26% in 2020. At the same time, the greatest debtors, Italy, Spain, Greece and Portugal increased their combined debts by €242bn to €1,180bn. But the most rapid deterioration for its size is in Greece’s negative balance, more than doubling by €54.6bn from €25.7bn at end-2019. Spain’s deficit is also increasing at a worrying pace, up from €392.4bn to €500bn, and Italy’s from €439.4bn to €516bn.

If one national central bank runs a Target2 deficit with the other central banks, it is because it has loaned money to its commercial banks to cover payment transfers, instead of progressing them through the settlement system. The loans to commercial banks appear as an asset on the national central bank’s balance sheet, which is offset by a liability to the ECB’s Eurosystem through TARGET2 — hence the PIGS’ deficits. But under the rules, if the TARGET2 system fails, the costs are shared out by the ECB on the pre-set capital key formula based on the equity ownership of ECB shares by the national banks.

The ECB itself has a deficit of €342bn arising from non-transfer of bond purchases by national central banks on its behalf, reducing apparent deficits among the debtors and suppressing the amount owed to NCBs like the Bundesbank. In other words, the ECB’s negative balance means that the seriousness of the situation in underrepresented by the statistics.

It is in the interest of a national central bank to run a greater deficit in relation to its capital key by supporting the insolvent banks in its jurisdiction. That way, if TARGET2 fails, its write-off becomes greater than its contribution to the ECB’s recapitalisation. Along with Luxembourg, Germany is the obvious loser in the arrangement. Germany’s equity ownership in the ECB is 26.38% of the euro-area national banks’ total equity interest. If TARGET2 collapsed, the Bundesbank would lose the trillion plus euros owed to it by the others and the ECB itself, and additionally have to pay up to €400bn of the net losses, based on current imbalances. That is currently a notional cost for the Bundesbank of at least €1.536 trillion, wiping out its own balance sheet.

To understand how and why the problem arises, we must go back to the earlier European banking crisis following Lehman, which has informed current regulatory practices at national levels. If the national banking regulator deems loans to be non-performing, the losses would be a national banking problem. Alternatively, if the regulator deems them to be performing, they are eligible for the national central bank’s refinancing operations. A commercial bank using the questionable loans as collateral borrows from the national central bank, which in turn borrows to cover by withholding payments into the TARGET2 system. Insolvent loans are thereby removed from the PIGS’ national banking systems and lost in the Eurosystem.

In Italy’s case, the very high level of non-performing loans peaked at 17.1% in September 2015 but by mid-2020 had been reduced to 6.5%. Given the incentives for the regulator to deflect the non-performing loan problem from the domestic economy into the Eurosystem, it would be a miracle if any of the reduction in NPLs is genuine. And with all the covid-19 lockdowns, Italian NPLs will be soaring again and much of this increase is yet to be reflected in the commercial banks’ accounting systems.

In the member states with negative TARGET2 balances such as Italy, there have been long established and growing trends towards liquidity problems for legacy industries, rendering many of them insolvent for decades without the drip feed of additional credit. With the banking regulator incentivised to not admit these recorded and unrecorded NPL problems in the domestic economy, loans to these insolvent companies have been continually rolled over and increased by funding them through TARGET2. The consequence is that new businesses have been starved of bank credit for lack of balance sheet and banking enthusiasm. The system which has turned commercial banks into zombies along with the majority of their borrowers could not be more calculated to cripple the Italian economy and restrict its prospects for recovery.

Officially, there is no problem, because the ECB and all the national central bank TARGET2 positions net out to zero, and the mutual accounting between the central banks in the system keeps it that way. To its architects, a systemic failure of TARGET2 is inconceivable. But because some national central banks are now accustomed to using TARGET2 as a source of funding for their own insolvent banking systems, the coronavirus crisis threatens to increase imbalances even further, threatening to bring the euro-settlement system down.

The Eurosystem member with the greatest problem is Germany’s Bundesbank, now owed well over a trillion euros through TARGET2. The risk of losses is now set to accelerate rapidly as a consequence of repeated rounds of Covid lockdowns in the PIGS. The Bundesbank is right to be very concerned. This is a direct quote from Professor Sinn’s paper referenced in endnote iii:

“… the Target issue hit political headlines when the new President of the German Bundesbank, Jens Weidmann, voiced his concerns over the Bundesbank’s target claims in a letter to ECB president Mario Draghi. In the letter Weidmann not only demanded higher credit rating criteria for collateral submitted against refinancing loans, but also called for collateralisation of the Bundesbank’s soaring Target claims. Weidmann wrote his Target letter after several months of silence on the part of the Bundesbank, during which it conducted extensive internal analysis of the Target issue. This letter marked a departure by Weidmann from the Bundesbank’s earlier position that Target balances represent irrelevant balances and a normal by-product of money creation in the European currency system.”

So Weidmann knows precisely the danger described in this article. As a mechanism that permits the PIGS to shelter nonperforming loans in increasing quantities, the TARGET2 setup has become rotten to the core. And now, thanks to the economic impact of the coronavirus, sooner rather than later the settlement system will blow up. To balance the asset side of its balance sheet the Bundesbank has liabilities of €2,227bn owed into its commercial banking system, and insufficient equity to absorb TARGET2 write-offs. Nor have the PIGS central banks the capital to cover them. In other words, if TARGET2 collapses, all Eurozone central banks including the ECB will simply fail.

Until then, TARGET2 is a devil’s pact which is in no one’s interest to break.

The sheer scale of a TARGET2 failure makes a resolution appear impossible. Current imbalances over the whole system total €1.621 trillion, but actually more when the ECB’s own borrowings through the system are taken into account. As mentioned above, according to the capital keys, in a systemic failure the Bundesbank’s net TARGET2 assets of €1.136 trillion would be replaced by liabilities up to €400bn, the rest of the losses being spread around the other national banks.[v] No one knows how it would work out because failure of the settlement system was never contemplated; but many if not all of the national central banks would have to be bailed out, presumably by the ECB as guarantor of the system. But with only €7.66bn of subscribed capital the ECB’s balance sheet equity is miniscule compared with the losses involved, and its shareholders will themselves be seeking bailouts in turn to bail the ECB. A TARGET2 failure would appear to require the ECB to effectively expand its QE programmes to recapitalise itself and the whole eurozone central banking system.

Now that really would be a crisis, the likes of which has never been seen before, where a central bank prints money purely to save itself and its regional agents.

The ending of TARGET2 is therefore likely to be a complete write-off for the national central banks and also will mark the end of the ECB, at least in its current form. Assuming the status of the euro as a medium of credit and exchange is to continue, a different and formulaic system of currency management designed to recapitalise the national central banks and keep the currency moderately scarce throughout the Eurozone would have to be implemented. And its implementation would have to be instantaneous, and probably prove to be impossible.

The EU’s future following the ECB’s failure

The failure of TARGET2 would require national central banks to address their relationship with their commercial banking networks properly. It is beyond our scope to see how this might be done in individual jurisdictions, being more interested in the bigger picture and the prospects for the euro and its successors.

If the TARGET2 system collapses, loans denominated in euros will be called in. To the extent that EU corporations have deposits and liquid investments in foreign currencies, they will inevitably become a source of funds, driving the euro’s exchange rate higher against those other currencies. Furthermore, foreigners who use the euro as the basis of a carry trade, for example to back positions in the fx swap market, will also have their positions unwound, leading to further demand for euros on the foreign exchanges. This phenomenon, which is usually associated with the US dollar, is often described as a crisis-driven dash for cash.

Given the extent to which the dollar is currently over-owned by foreigners and while the euro is under-owned internationally, it is the dollar which is likely to suffer most from a eurozone monetary crisis, at least initially. This will be the background against which Germany’s Bundesbank will be considering its options.

The case for a new mark

An imminent failure of the Eurosystem, which we can now see is becoming inevitable, is also being seen as a danger by the Bundesbank. This is the logical conclusion from Weidmann’s letter to Mario Draghi at the ECB. It therefore follows that there is a Plan B being developed, which at the least will be intended to insulate the Bundesbank from the difficulties faced by other national central banks and the ECB itself. This can only be achieved with a new currency, based on the Germany mark before it was folded into the euro. That way the euro-based Bundesbank can be written off as the Eurosystem collapses, while a mark-based Bundesbank emerges.

Germany will not want to resuscitate old enmities. The Bundesbank will be acutely aware what its own survival would mean for the PIGS, and especially for France whose to be dashed eurozone ambitions are essentially political. Interest rates in the replacement currencies for these nations would almost certainly rise sharply, collapsing their bond markets, undermining any surviving commercial banks, and national finances. These nations would have no practical alternative but to seek the shelter of a better form of money than the euro in order to stabilise their bond markets, and with a view to having continuing access to credit. In short, the monetary consensus would move from an overtly inflationary monetary system gamed by the national central banks and their regulators to one based on a sounder form of money.

Instead of fully abandoning inflationary habits, the intention would always be to resume inflationary funding. The Bundesbank is therefore likely to resist moves which in effect leaves it in the position of the defunct ECB, taking on responsibility for the circulation of all money in the former eurozone. Admittedly, the German government might view the situation differently, but even it is likely be aware of the political implications of appearing to have escaped a euro crisis relatively unscathed compared with the other nations, and then taking over control of the defunct eurozone’s money.

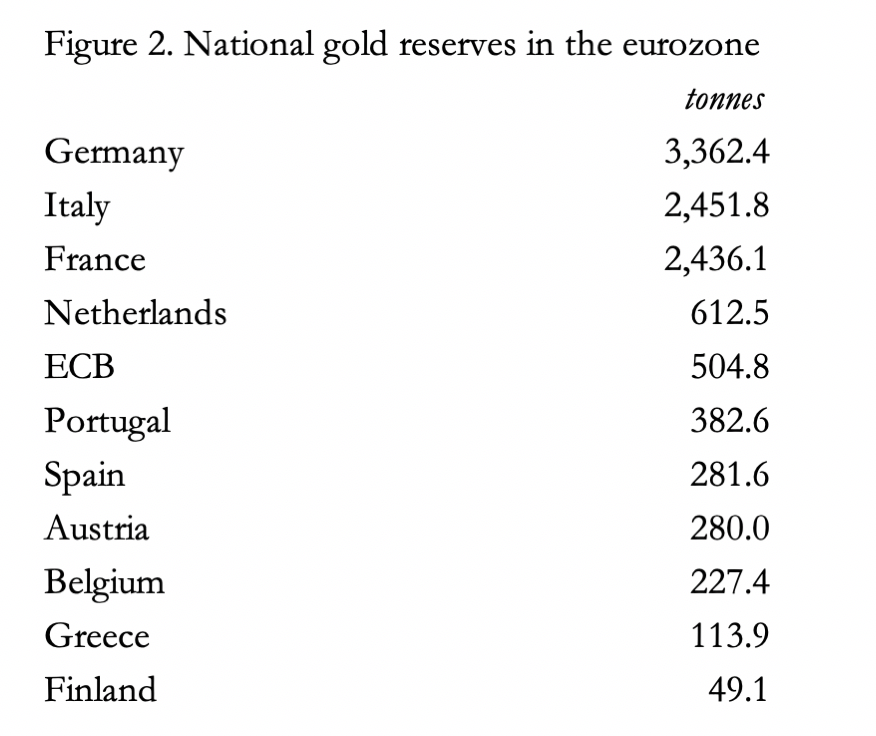

The obvious solution is to return to a credible gold standard, and to encourage other member states to do the same. Figure 2 shows the official gold reserves of key member states, assuming for our purposes that they actually exist, there is no double counting, can be repatriated where necessary and are not leased out to or swapped with other parties.

The ECB’s gold reserves were originally created by transfers from national central banks, so we can assume its 504.8 tonnes will be mostly transferred back to them, because other than central banks outside the eurozone they are the ECB’s only creditors. That being the case, the top ten eurozone holders will have up to 10,702 tonnes between them. The gold is, however, unevenly distributed, with Germany, Italy and France possessing significant reserves. But Holland and Portugal have ample reserves for their size as well.

All these nations, including Germany, are likely to be reluctant to mobilise their gold to back new currencies. Germany recovered from two currency collapses in the last century without doing so, and the Bundesbank is likely to take the view that possession of its gold reserves will be enough to convince its citizens that a new mark will be stable and credible money. Furthermore, it is not sufficient to turn fiat into gold exchange currencies without addressing government spending. Not only does a successful gold standard require balanced budgets, but a deliberate reduction in overall spending must be maintained for the standard to stick over time. The failure of the Maastricht treaty in this respect illustrates the difficulties of fiscal discipline.

Politically, it requires a reversal of the European social democratic ideal, risking a political vacuum, threatened to be replaced by various forms of extremism.

International influences

The political and monetary evolution of a post-euro Europe will not be determined solely by endogenous events. Elsewhere, I have written about the likely fate of the US dollar, which in this inflationary era is likely to be dramatic for different reasons. Obviously, the implications of two separate developing crises for each other and the timings involved cannot be predicted with any certainty, but there are common threads. The most notable is the suppression of interest rates and government bond yields by the ECB and the Fed in their respective jurisdictions.

Both central banks have maintained these objectives by monetary inflation, allowing debt creation to proceed and consequently inflating asset bubbles. These bubbles have different characteristics, the ECB imposing negative interest rates while the Fed has respected the zero bound. With the US economy being more financial in nature and the dollar being the international reserve currency, the dollar’s inflation is the primary driver of global commodity prices and esoterica such as cryptocurrencies — all of which are now inflating rapidly.

A common linkage between the two is through the G-SIBs. A failure in the eurozone’s banking system will almost certainly undermine that of the US, as well as others. History has shown that even a minor bank failure in a distant land can have major consequences worldwide. In this context, it is to be hoped that by exposing the faults in both the TARGET2 system and the eurozone’s commercial banks that a greater understanding of the monetary dangers faced by us all has been achieved. And for citizens in the EU, the regaining of national power from the Brussels bureaucracy should be an improvement on the current situation — assuming it is used wisely.

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Government

Walmart joins Costco in sharing key pricing news

The massive retailers have both shared information that some retailers keep very close to the vest.

Share this:

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trumpGovernment

Walmart has really good news for shoppers (and Joe Biden)

The giant retailer joins Costco in making a statement that has political overtones, even if that’s not the intent.

Share this:

{kind=link}

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trump

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

When Military Rule Supplants Democracy

Catastrophic Risk: Investing and Business Implications

The Digest #187

Redefining Poverty: Towards a Transpartisan Approach

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

Dropping Like a Stone: ON RRP Take‑up in the Second Half of 2023

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Deterra Royalties half-yearly result: stable performance and growth Initiatives

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 day ago

Walmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges