Uncategorized

Stock indexes are breaking records and crossing milestones – making many investors feel wealthier

The S&P 500 topped 5,000 on Feb. 9, 2024, for the first time. The Dow Jones Industrial Average will probably hit a new big round number soon t…

Share this:

The S&P 500 stock index topped 5,000 for the first time on Feb. 9, 2024, exciting some investors and garnering a flurry of media coverage. The Conversation asked Alexander Kurov, a financial markets scholar, to explain what stock indexes are and to say whether this kind of milestone is a big deal or not.

What are stock indexes?

Stock indexes measure the performance of a group of stocks. When prices rise or fall overall for the shares of those companies, so do stock indexes. The number of stocks in those baskets varies, as does the system for how this mix of shares gets updated.

The Dow Jones Industrial Average, also known as the Dow, includes shares in the 30 U.S. companies with the largest market capitalization – meaning the total value of all the stock belonging to shareholders. That list currently spans companies from Apple to Walt Disney Co.

The S&P 500 tracks shares in 500 of the largest U.S. publicly traded companies.

The Nasdaq composite tracks performance of more than 2,500 stocks listed on the Nasdaq stock exchange.

The DJIA, launched on May 26, 1896, is the oldest of these three popular indexes, and it was one of the first established.

Two enterprising journalists, Charles H. Dow and Edward Jones, had created a different index tied to the railroad industry a dozen years earlier. Most of the 12 stocks the DJIA originally included wouldn’t ring many bells today, such as Chicago Gas and National Lead. But one company that only got booted in 2018 had stayed on the list for 120 years: General Electric.

The S&P 500 index was introduced in 1957 because many investors wanted an option that was more representative of the overall U.S. stock market. The Nasdaq composite was launched in 1971.

You can buy shares in an index fund that mirrors a particular index. This approach can diversify your investments and make them less prone to big losses.

Index funds, which have only existed since Vanguard Group founder John Bogle launched the first one in 1976, now hold trillions of dollars .

Why are there so many?

There are hundreds of stock indexes in the world, but only about 50 major ones.

Most of them, including the Nasdaq composite and the S&P 500, are value-weighted. That means stocks with larger market values account for a larger share of the index’s performance.

In addition to these broad-based indexes, there are many less prominent ones. Many of those emphasize a niche by tracking stocks of companies in specific industries like energy or finance.

Do these milestones matter?

Stock prices move constantly in response to corporate, economic and political news, as well as changes in investor psychology. Because company profits will typically grow gradually over time, the market usually fluctuates in the short term, while increasing in value over the long term.

The DJIA first reached 1,000 in November 1972, and it crossed the 10,000 mark on March 29, 1999. On Jan. 22, 2024, it surpassed 38,000 for the first time. Investors and the media will treat the new record set when it gets to another round number – 40,000 – as a milestone.

The S&P 500 index had never hit 5,000 before. But it had already been breaking records for several weeks.

Because there’s a lot of randomness in financial markets, the significance of round-number milestones is mostly psychological. There is no evidence they portend any further gains.

For example, the Nasdaq composite first hit 5,000 on March 10, 2000, at the end of the dot-com bubble.

The index then plunged by almost 80% by October 2002. It took 15 years – until March 3, 2015 – for it return to 5,000.

By mid-February 2024, the Nasdaq composite was nearing its prior record high of 16,057 set on Nov. 19, 2021.

Index milestones matter to the extent they pique investors’ attention and boost market sentiment.

Investors afflicted with a fear of missing out may then invest more in stocks, pushing stock prices to new highs. Chasing after stock trends may destabilize markets by moving prices away from their underlying values.

When a stock index passes a new milestone, investors become more aware of their growing portfolios. Feeling richer can lead them to spend more.

This is called the wealth effect. Many economists believe that the consumption boost that arises in response to a buoyant stock market can make the economy stronger.

Is there a best stock index to follow?

Not really. They all measure somewhat different things and have their own quirks.

For example, the S&P 500 tracks many different industries. However, because it is value-weighted, it’s heavily influenced by only seven stocks with very large market values.

Known as the “Magnificent Seven,” shares in Amazon, Apple, Alphabet, Meta, Microsoft, Nvidia and Tesla now account for over one-fourth of the S&P 500’s value. Nearly all are in the tech sector, and they played a big role in pushing the S&P across the 5,000 mark.

This makes the index more concentrated on a single sector than it appears.

But if you check out several stock indexes rather than just one, you’ll get a good sense of how the market is doing. If they’re all rising quickly or breaking records, that’s a clear sign that the market as a whole is gaining.

Sometimes the smartest thing is to not pay too much attention to any of them.

For example, after hitting record highs on Feb. 19, 2020, the S&P 500 plunged by 34% in just 23 trading days due to concerns about what COVID-19 would do to the economy. But the market rebounded, with stock indexes hitting new milestones and notching new highs by the end of that year.

Panicking in response to short-term market swings would have made investors more likely to sell off their investments in too big a hurry – a move they might have later regretted. This is why I believe advice from the immensely successful investor and fan of stock index funds Warren Buffett is worth heeding.

Buffett, whose stock-selecting prowess has made him one of the world’s 10 richest people, likes to say “Don’t watch the market closely.”

If you’re reading this because stock prices are falling and you’re wondering if you should be worried about that, consider something else Buffett has said: “The light can at any time go from green to red without pausing at yellow.”

And the opposite is true as well.

Alexander Kurov does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

dow jones sp 500 nasdaq stocks covid-19Uncategorized

Marriage is not as effective an anti-poverty strategy as you’ve been led to believe

Marriage on its own won’t do away with child poverty, and in fact it can create even more instability for low-income families.

Share this:

Brides.com predicts that 2024 will be the “year of the proposal” as engagements tick back up after a pandemic-driven slowdown.

Meanwhile, support for marriage has found new grist in recent books, including sociologist Brad Wilcox’s “Get Married: Why Americans Must Defy the Elites, Forge Strong Families and Save Civilization” and economist Melissa Kearney’s “The Two-Parent Privilege.”

Kearney’s book was hailed by economist Tyler Cowen as possibly “the most important economics and policy book of this year.” This is not because it treads new ground but because, as author Kay Hymowitz writes, it breaks the supposed “taboo about an honest accounting of family decline.”

These developments are good news for the marriage promotion movement, which for decades has claimed that marriage supports children’s well-being and combats poverty. The movement dates back at least to the U.S. Department of Labor’s Moynihan Report of 1965, which argued that family structure aggravated Black poverty.

Forty years after the Moynihan Report, George W. Bush-era programs such as the Healthy Marriage Initiative sought to enlist churches and other community groups in an effort to channel childbearing back into marriage. These initiatives continue today, with the federally subsidized Healthy Marriage and Responsible Fatherhood programs.

Still, nearly 30% of U.S. children live in single-parent homes today, compared with 10% in 1965.

We are law professors who have written extensively about family structure and poverty. We, and others, have found that there is almost no evidence that federal programs that promote marriage have made a difference in encouraging two-parent households. That’s in large part because they forgo effective solutions that directly address poverty for measures that embrace the culture wars.

Marriage and social class

Today’s marriage promoters claim that marriage should not be just for elites. The emergence of marriage as a marker of class, they believe, is a sign of societal dysfunction.

According to census data released in 2021, 9.5% of children living with two parents – and 7.5% with married parents – lived below the poverty level, compared with 31.7% of children living with a single parent.

Kearney’s argument comes down to: 1 + 1 = 2. Two parents have more resources, including money and time to spend with children, than one. She marshals extensive research designed to show that children from married couple families are more likely to graduate from high school, complete college and earn higher incomes as adults than the children of single parents.

It is undoubtedly true that two parents – that is, two nonviolent parents with reliable incomes and cooperative behavior – have more resources for their children than one parent who has to work two jobs to pay the rent. However, this equation does not address causation. In other words, parents who have stable incomes and behaviors are more likely to stay together than parents who don’t.

Ethnographic studies indicate, for example, that the most common reasons unmarried women are no longer with the fathers of their children are the men’s violent behavior, infidelity and substance abuse.

Moreover, income volatility disproportionately affects parents who don’t go to college. So while they may have more money to invest in children together than apart, when one of these parents experiences a substantial drop in income, the other parent may have to decide whether to support the partner or the children on what is often a meager income.

The impact of having single parents also plays out differently by race and class. As sociologist and researcher Christina Cross explains, “Living apart from a biological parent does not carry the same cost for Black youths as for their white peers, and being raised in a two-parent family is not equally beneficial.”

For example, Cross found that living in a single-mother family is less likely to affect high school completion rates for Black children than for white children. Also, Black families tend to be more embedded in extended family than white families, and this additional support system may help protect children from negative outcomes associated with single-parent households.

Making men more ‘marriageable’

Kearney, to her credit, does note that economic insecurity largely explains what is happening to working-class families, and that no parent should have to tolerate violence or substance abuse. But she doubles down on the need to restore a norm of two-parent families.

Many of her policy prescriptions are sensible. She advocates for better opportunities for low-income men – to make them, in the words of sociologist William Julius Wilson, “marriageable.” Such policies would include wage subsidies to improve their job opportunities, investment in community colleges that provide skills training, and the removal of questions about criminal histories from job applications, so that candidates who have previously been incarcerated are not immediately disqualified.

A new marriage model

What marriage promotion efforts overlook, however, are the underlying changes in what marriage has become – both legally and practically.

The new marriage model rests on three premises.

The first is a moral command: Have sex if you want to, but don’t have children until you are ready. While the shotgun marriage once served as the primary response to unplanned pregnancy, such marriages today often derail education and careers and are more likely to result in divorce than other marriages. Research shows that lower-income women’s pregnancies are much more likely to be unplanned.

The second is the ability to pick a partner who will support you and assume joint responsibility for parenting. As women have attained more economic independence, they are less in need of men to raise children, particularly if their partners are insensitive or abusive. With healthy relationships, couples pick partners based on trust, commitment and equal respect. This is more difficult to do in communities with high rates of incarceration and few opportunities for stable employment.

And the third is economic and behavioral stability. Instability undermines even committed unions. Parents who wait until they find the right partner and have stable lives bring a lot more to parenting, whether they marry or not.

We believe that creating opportunities for low-income parents to reach this middle-class model is likely to be the most effective marriage promotion policy.

Economic support is key

In relationships that fall outside of these premises, 1 + 1 often becomes 1 + -1, which equals 0.

Being committed to a partner who can’t pay speeding tickets, runs up credit card bills, comes home drunk or can’t be relied on to pick up the children after school is not a recipe for success.

Economic principles suggest that businesses with more volatile income streams need a stronger capital base to withstand the downturns. Working-class couples who face economic insecurity see commitment as similarly misguided; without a capital base, a downturn for one partner can wipe out the other.

The Biden administration’s child tax credit expansion included in the American Rescue Plan Act of 2021 helped cut the child poverty rate – after accounting for government assistance – to a record low that year. It did more to address child poverty than marriage promotion efforts have ever done.

Researchers have described such income-support policies as the “ultimate multipurpose policy instrument.” They improve the economic circumstances of single-parent families and, in doing so, may also provide greater support for two-parent relationships.

Policymakers know how to solve child poverty – and these measures are far more effective than efforts to put two married parents in every household.

The authors do not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and have disclosed no relevant affiliations beyond their academic appointment.

subsidies pandemicUncategorized

Is the biotech market rally real? Data suggest comeback in private, public markets

After some halting starts, false dawns and fragile rallies, the biotech market may finally be back.

No, really.

In the last several months, several important…

Share this:

After some halting starts, false dawns and fragile rallies, the biotech market may finally be back.

No, really.

In the last several months, several important signals have added up to what feels like a rally, with more depth and certainty than some of the short-lived upticks during the doldrums of 2022 and 2023, when only the industry’s most optimistic souls were willing to call it a comeback.

But now, public biotechs are releasing positive data and raising money in follow-on offerings with ease. Biopharmas have already raised $13.7 billion in secondary raises in 2024, according to Stifel’s Tim Opler. Biotech’s benchmark index, the $XBI, is up 56% from last year’s lows and has broken the $100 mark, thanks to gains that go deep into the 120-company index. And in the private markets, crossover rounds are trickling back, and IPOs are showing signs of life.

Investors and executives told Endpoints News that this moment feels different, encouraged by a return to the basics, a focus on data, and signs of a healthier — if smaller — biotech ecosystem.

“We should be beyond any of the lows,” said Chris Garabedian, a venture portfolio manager at Perceptive Advisors and founder of the firm’s early-stage investing unit Xontogeny. “We are going to see continued forward momentum.”

Investor sentiment is “very different from what it was in ‘22 to ‘23, where it was all doom and gloom,” MoonLake Immunotherapeutics CEO Jorge Santos da Silva said. A year ago, “The question was like, ‘What are the 22 ways in which you can die?’ That has really changed.”

The XBI cracking $100 is encouraging, but a deeper look at the index shows more signs of strength. The exchange-traded fund, which lets investors buy shares of its basket of 120 biotech companies, has seen $457 million in net inflows over the past month, according to YCharts data. And about 80% of biotechs on the index — which includes giants like Vertex $VRTX and small companies like Avidity Biosciences $RNA — have seen their stock in the green over the past three months.

Some of that gain is clearly driven by a surge in M&A, including the buyouts of Seagen, Horizon, Cerevel, and Karuna, all of which have returned billions of dollars back to investors who need to put it back to work in the private or public markets. And industry insiders have said there’s also a breadth in the disease areas drawing interest, including obesity, cancer, cardiology, neurology, and inflammation.

Even ARCH Venture Partners managing director Bob Nelsen voiced some broader — albeit measured — optimism for the market.

“For our internal base case, we’re still assuming that things are going to suck like they have in the last couple of years,” Nelsen told Endpoints. “But we all believe that it has turned.”

Nelsen still implores his portfolio companies and limited partners to “assume it’s going to be worse than you think.” But his optimism is driven by two major trends: the easing of macro factors like interest rates and the persistence of M&A. He’s closely watching whether generalist investors — whose huge dollars can swing a sector up or down, as they did dramatically during the pandemic — will come back to biotech.

“The conventional wisdom in Q4 is, they were never coming back in the market,” he said. “Turns out, in Q4 they were buying.”

From atonement to ‘FOMO’

Jorge Santos da Silva

Jorge Santos da SilvaDa Silva said the industry had been “paying for our sins” committed in the boom years of 2019 to 2021, when hundreds of biotechs went public — many far from going into the clinic. Along with layoffs and company closures, it resulted in an infestation of the corporate walking dead in companies trading at values below the amount of cash on their books.

But the number of those companies with negative equity value has dropped in the past few months, suggesting that a much-needed cleanup from the go-go years is well in progress.

“I call it a detox,” da Silva said. “Whatever we did was clearly excessive and everyone knew it at the time. But when you’re at a party, it’s like, ‘Oh my God, this is crazy, but let’s keep going.’ The detox phase is definitely coming to an end.”

Otello Stampacchia

Otello StampacchiaOtello Stampacchia, the managing director of the Boston-based VC firm Omega Funds, said the mood is even “getting a little bit bubblicious” for biotechs with clinical-stage drug candidates in large markets with meaningful milestones in the next 12 to 18 months.

“There’s really a rush to get into those, particularly now that the indices have started flipping their dynamic,” said Stampacchia, who founded Omega two decades ago. “Up until early last fall, nobody wanted to catch the falling knife. It’s now the exact opposite dynamic, and there’s a bit of crowding in some of these names.”

“There’s real FOMO to invest in the right therapeutic products and the right therapeutic companies,” he added.

That’s carried through the private and public markets, Stampacchia said, noting that Omega participated in Alumis’ recent $259 million Series C raise — biotech’s biggest round this year. He said he was “incredibly surprised by the amount of demand there was for the deal.” All told, Omega has seen roughly half a dozen of its portfolio companies raise close to half a billion dollars over the last few months, with increased valuations.

“In each case, it really wasn’t difficult to syndicate,” he said. “There’s real demand.”

rna pandemic interest ratesUncategorized

“It seems impossible:” Bergen County, NJ’s housing market is vexing agents and buyers

While the housing market has cooled from the buying frenzy during the pandemic, agents in the leafy Bergen County suburbs say it’s also gotten worse. We…

Share this:

Real estate agents in the leafy suburbs of Bergen County, New Jersey say the current housing market — with historically low inventory and record-high prices — is actually more challenging than the multiple offer chaos they sweated through during the pandemic.

“At the height of the pandemic there were bidding wars and all that, but it didn’t seem impossible, but now it seems impossible to get our buyers into homes,” said Heather Corrigan, a RE/MAX Signature Homes agent based in Closter, a borough that is 24 miles north of Manhattan and renown for its schools.

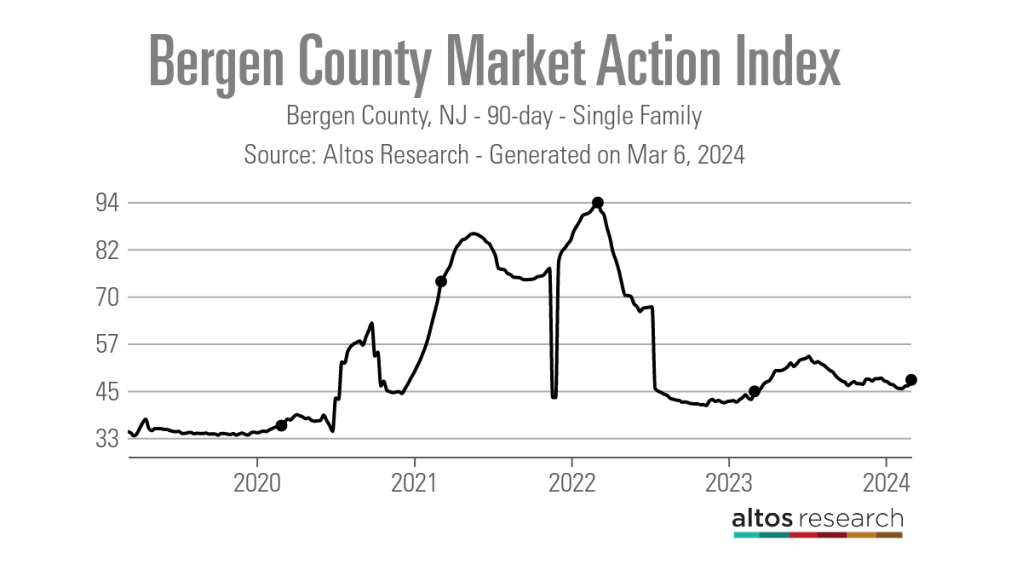

Altos Research’s Market Action Index score for the county, which has 70 municipalities, illustrates the challenges agents and their clients have faced. In March of 2022, the 90-day average Market Action Index score for the county hit a high of 93.84, before cooling over the past two years to a score of 47.98 as of March 6, 2024. Altos considers any score above 30 to be a seller’s market.

70 towns, 90 new listings

Local agents say the county’s tight inventory situation is largely to blame.

“We have been complaining about the lack of inventory for as long as I can remember, but then we at least had more listings,” Danny Yoon, an Edgewater, New Jersey-based Sotheby’s International Realty agent, said. “I was able to bring my clients to multiple listings for their consideration, but now I can only show them one or two in a given week. There is nothing to show.”

As of March 6, 2024, there was a 90-day average of 570 active single-family listings in Bergen County, according to Altos. This is down from a 90-day average of 752 active single-family listings a year ago and 2,052 active single-family listings in early March 2020, just at the onset of the COVID-19 pandemic.

“Bidding wars are still there but it isn’t as bad as during COVID,” said Lisa Comito, a broker at Howard Hanna Rand Realty and the president of Greater Bergen Realtors, which has nearly 9,000 members. “When we were coming out of COVID we were seeing 15 to 20 offers on a house, where you’d have to make a spreadsheet to show your seller. You aren’t getting that, but there is still a lot of competitive bidding.”

Like elsewhere in the country, agents blame the low interest rates of 2020 and 2021 for locking many would-be sellers into their homes.

“During the pandemic, people would downsize or sell their home on a whim,” Comito said. “Now it is a different conversation. If they are downsizing it is for quality of life or that they can’t maintain a large home anymore.”

Although agents are optimistic about what may come with the fast-approaching spring housing market, the numbers are not promising. Data from Altos Research shows that there were just 90 new single-family listings in Bergen County for the week ending March 1, 2024. This is the fewest number of new listings for the first week in March recorded in Altos’ data, which dates back to 2013.

“Some of the reports indicate that we are going to have more listings this year than last year, but the only way I can see that being correct is because we had so few listings last year,” Yoon said. “Even if we get more listings, it is not going to be enough for people. We are still going to suffer from lack of inventory.”

Prices climbing toward $1M

While questions remain over how many sellers will decide to enter the market this spring, agents are already seeing more buyers come to the market. That’s despite median list prices climbing to a record $899,000 in the first week of March 2024, up nearly $150,000 from March 2022, which Altos considers the market’s peak.

“There is a meme with two buyers sitting in chairs waiting for prices and interest rates to drop and the buyers are skeletons and I think there is some truth to that,” Corrigan said. “But now buyers are sick of waiting around and are deciding it is time to buy.”

Comito also believes the current interest rate environment is helping to encourage buyers to enter the market.

“Buyers right now have gotten more comfortable with the mortgage rates,” Comito said. “They have stayed pretty consistent, allowing people to adjust to them and they aren’t thinking as much about those low rates of the pandemic market.”

While buyers are facing inventory and interest rate challenges, agents say they are also facing competition from investors and the all-cash offers they are capable of making.

“I have well qualified clients who are putting down 25% and are coming over asking with no or limited inspections and they are getting beat out by investors with all-cash,” Corrigan said.

She noted that while some of the investors are larger corporations, there are also a lot of mom-and-pop investors out in the market, buying up inventory.

Comito noted that even first-time buyers are looking to get into rental properties.

“You are seeing first time buyers looking for multifamily properties where they can rent out the other units to help pay for their mortgage,” Comito said.

Even with the challenging housing market conditions, buyers are still flocking to Bergen County, and agents like Corrigan don’t see that changing.

“The schools are good, and everything is in close proximity,” Corrigan said. “Every town has its own unique features, whether it is a great library, the town pool, events they put on, great restaurants, it is really just a desirable place to live for so many people.”

mortgage rates real estate housing market pandemic covid-19 interest rates

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Liquidity Problems Are Closer Than You Think

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Is the biotech market rally real? Data suggest comeback in private, public markets

Interest rates, the best it gets. It’s time to deploy cash

Normalise the underlying conditions when “rating” a company’s share price

COVID-19 Lockdowns Had High Health, Economic Costs: Swedish Study

Stock Market’s Top Will Outlast Your Disbelief

Democrats “Nervous” Ahead Of Biden’s State Of The Union Address

The Sensitivity of Economic Sentiment to News Sentiment, By Partisan Affiliation

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges