Uncategorized

Luongo: Why War Bonds Are Returning In Europe

Luongo: Why War Bonds Are Returning In Europe

Authored by Tom Luongo via Gold, Goats, ‘n Guns blog,

After a mostly peaceful Security Conference…

Share this:

Authored by Tom Luongo via Gold, Goats, 'n Guns blog,

After a mostly peaceful Security Conference in Munich over the weekend, Estonian Prime Minister Katja Kallas let the real purpose of all the recent hysteria over Ukraine funding out of the proverbial bag — Eurobonds.

Kallas was handed the bully pulpit to make the argument for $110 billion in Eurobonds be issued by the EU Commission to spend on arming Europe for the future and supporting Ukraine. It just sounds like more of the same that we’ve heard for two years now. More money for Ukraine. More war spending.

But this is a far more complex and nuanced issue than just making sure the West fights Russia to the last Ukrainian. This is ultimately about shoring up the EU’s fundamental weakness. It is an economic bloc with a common currency whose political authority is mostly powerless to control the value of that currency.

For this reason the EU leadership, nominally Davosian in their agenda, has been working their political machine towards giving the EU Commission that power through bond issuance and a centralized taxing mechanism.

They did this after COVID with their SURE Bonds, which they issued in 2020 to legitimize this process. I covered this in a long article in October last year when this very issue came up. Then ECB President Christine Lagarde made it public that they want to create a Eurobond Index to give these SURE bonds greater visibility in the vain hope someone will buy the next round of them.

There is also a major push happening offscreen for these bonds to become indexed next to everyone else’s, i.e. to more easily sell them to Muppet investors, through the imprimatur of them being official and backed by the full faith and credit of the EC. Of course, the initial investors in them have lost their ass as the bulk of them were issued when the ECB was at -0.6%. (See Here).

The ECB just held rates at 4.5%. The bond math doesn’t work. So, the EU got the last big lot of blood and treasure after the COVID operation from its investor class, who are now sitting on massive losses. Some of these investors, of course, were the member central banks themselves.

Don’t believe me? A €7 billion 0.1% coupon SURE bond maturing in October of 2040 is now trading at a yield of 3.867%. Now that doesn’t look so bad until you grep the price of that bond, which is trading with a bid/ask spread of 0.54/0.55… or a 45% loss.

This particular SURE bond has recovered in price back to around $0.61, after one of the biggest rallies in sovereign debt markets in history to end 2023. But that’s also just the quoted price. There is no price discovery on these, as there’s only on trade a week actually happening in Frankfurt where these things are listed.

They aren’t a market. They are, however, a massive political tool. Because they gave the EU Commission the ability to levy taxes to pay the 0.1% coupon on them. It’s the government tax and spend equivalent of “just the tip.” It’s only a small surcharge on your grocery bill… or whatever.

One problem is that the initial investors in these things are still sitting on 40% losses. If the first round are selling at a 40 to 50% discount what coupon are they going to have to offer to get anyone to buy the next round? nd it’s part of the reason why there is such urgency to get central banks to lower rates.

The EU can’t afford to raise the capital it needs to complete its fiscal integration plans with the ECB forced up to 4.5% to keep pace with Powell’s FED. They need these rates back near zero to fund their grand dreams of a hydrocarbon-free totalitarian future.

As always, this underscores the point I’ve been making for two-plus years now that Powell’s “higher for longer” rate policy is squeezing not just the European banking system but also it’s political objectives.

None of this is remotely sustainable at 5.5%. And for anyone who thinks the US is more vulnerable to this than the EU is, I invite you to explain that to me in grave detail with the dollar having drank nearly all of the euro’s milkshake in global trade over the past two years.

I’ll wait.

From SURE to War

The fate of these SURE bonds and all future EC bond issuances hangs in the balance here. In fact, the future of the EU itself hangs in the balance. And that’s why I was contacted by Sputnik News yesterday to give my thoughts on this subject.

“Eurobonds are the Holy Grail for European integration,” Tom Luongo, financial and geopolitical analyst, told Sputnik. “PM Kallas is telling you what the plan is. The EU’s Achilles’ heel is the euro itself and its lack of central taxing authority.”

“Eurobonds, issued through the European Commission, of this type are another way of handing that authority to Brussels, bypassing member state central banks and legislatures,” he added.

“If one was cynical, which I am, one would suspect that the EU’s support for the war in Ukraine was mostly driven by this desire to centralize power in Brussels,” Luongo argued. “You start a war in Ukraine by purposefully crossing Russia’s red lines, drive inflation up locally, and empty the military coffers of all the post-WWII weapons and ammunition that is now outdated. (…) If you are losing, as you are now, you play up the threat of Russia not stopping at Ukraine to justify shifting your domestic spending to a military build-up, issuing Eurobonds to pay for it.”

This plan for war bonds was shepherded by the usual suspects for EU militarization, French President Emmanuel Macron and EU President Charles Michel. And I want to stress here that nothing about this project is economic. It is purely political. They will expend whatever political capital they must to force this outcome on the people of Europe.

To folks like Macron, Michel, Ursula Von der Leyen and their bosses, European bourgeoisie and proletariats alike are just tax cattle. No wonder they are so against them eating beef.

So, let’s connect another couple of dots. Because now it should be obvious that this is why they threatened Hungary’s Viktor Orban with economic devastation for holding up their $50 billion aid package for Ukraine.

They need to keep Ukraine going to justify now spending another $100+ billion to launder into failing French and German banks sitting on massive losses from all the debt they bought during the NIRP (Negative Interest Rate Policy) period.

This is just the beginning of their plans for transferring sovereignty out of the hands of the member states and handing it to Brussels. But to sell this to global investors they have to prove to the world they have all the wayward voices under control.

Sovereign debt is secured through taxation and the productive capacity of the population. At this point the EU has neither.

NATO Forever

Now when I think about what all the principle players have been harping about for the past couple of weeks the common theme was NATO uber alles. This was echoed by everyone from President Biden at his latest press conference and Vice President Harris at Munich, to Hillary Clinton, clearly on more than a proof of life tour.

We had Alexei Navalny’s death used to raise money for war. Reports of Russia shooting US satellites out of orbit. Locusts!

It never stops with these people. There’s always a convenient Russian or Chinese bogeyman lurking behind every headline. But the underlying theme is to keep the money flowing into NATO. Trump’s comments on standing aside if Putin attacked a NATO country that didn’t pay its way were used by all of them to breathlessly support MOAR NATO.

But, in the end, this is just about the exercise of raw power against domestic populations. Putin and his army are no more a threat to Berlin than they are a threat to Kiev at this point.

NATO, and the plans to morph it into a global police force under UN control, is the reason for all of this. Europe wants the US to be a vassal after spending itself to death fighting the phantom menace of Putin. Eurobonds are the real story.

The rest is just noise.

N.B. As always, I will publish everything I sent to Sputnik News for the sake of transparency

Sputnik: The EU needs to work on a plan to issue $107.8 billion in eurobonds to boost the continent’s defense industry, and in the meantime do more to get weapons to Ukraine, Estonian Prime Minister Kaja Kallas told Bloomberg in an interview at the Munich Security Conference on Sunday. “We are in a place where we need to invest more and [explore] what we can do together, because the bonds that would be issued by separate countries individually are too small to scale up,” she said. “Eurobonds could have a much bigger impact.”

What is your overall opinion on this idea and its potential effectiveness?

Eurobonds are the Holy Grail for European integration. PM Kallas is telling you what the plan is. The EU’s Achilles’ heel is the euro itself and its lack of central taxing authority. Eurobonds, issued through the European Commission, of this type are another way of handing that authority to Brussels, bypassing member state central banks and legislatures.

If one was cynical, which I am, one would suspect that the EU’s support for the war in Ukraine was mostly driven by this desire to centralize power in Brussels. You start a war in Ukraine by purposefully crossing Russia’s red lines, drive inflation up locally, and empty the military coffers of all the post-WWII weapons and ammunition that is now outdated. If you win the war it’s great. Russia’s been subjugated and a new colonial frontier opens up for Europe to grab the collateral needed for the next iteration of Imperial Europe.

If you are losing, as you are now, you play up the threat of Russia not stopping at Ukraine to justify shifting your domestic spending to a military buildup, issuing Eurobonds to pay for it. The EU Commission has to be given direct taxing authority to guarantee the bonds to investors. Their SURE bonds, issued after COVID-19, were the first proof of this mechanism.

This is why they were so angry with Viktor Orban over blocking Ukraine aid. It legitimizes their central authority to guarantee to investors they can impose their will on EU members. while keeping Ukraine on financial life support to justify re-arming Europe.

While funding for Ukraine remains at a standstill in the US Congress, the EU appears to be heading towards accumulating more debt. What sort of risks does this method of joint borrowing pose for European countries? What anticipated and unforeseen consequences do you expect?

The risks are mostly political for the people of Europe. Because it means that if you think that things are out of control in Brussels now, just wait when you are paying taxes directly to the EU Commission. What you saw over the past month with Orban was a warning to the rest of the EU. There is no partnership here, there is only the exercise of raw power from the central authority.

By putting these words into the mouth of a rabid Russophobe like Estonia’s PM Kallas it’s meant to shame the rest of the EU to go along with this. What’s left of national sovereignty in Europe will die if the EU Commission continues getting these special bond issuances, €100 billion at a time.

While everyone was at Munich this past weekend talking about their ‘sacred commitment’ to NATO, the reality is that proposals like this will eventually blow apart NATO. NATO in the mind of the Eurocrats and globalists in DC is a precursor to a global police force administered by the United Nations. The more these people push for total integration of military, regulatory, political and economic cohesion, the more they will alienate the people they are trying to subjugate.

With Europe having its industries severely impacted by the financial crisis and many of them relocating their production, to what extent can this eurobonds strategy boost the continent’s defense industry? Is it wishful thinking by the Estonian Prime Minister?

It’s not wishful thinking on her part, it’s part of the process the laid out on the proverbial whiteboard in Brussels. Europe embarked on a very dangerous path by purposefully gutting their domestic economies through COVID lockdowns to get the first round of Eurobonds agreed to. Now they are using the phantom threat of a Russian invasion to get the second round issued.

The incipient inflation and overly strong euro as a currency is pushing their industries offshore as a result. But that is, again, part of the strategy. Because for every BASF plant built in the US, what comes with it are the strings of EU regulations which the local and federal governments must adopt. These are designed to collapse the competitive advantage of the foreign nation by raising their costs locally.

It’s always a poisoned carrot with these people. Always.

The fly in this ointment for them is their having to raise interest rates to keep pace with the Federal Reserve. With each month that passes where the Fed refuses to back off on interest rates the more the risks to Brussels’ plans multiply. The entire project is predicated on using cheap credit dollars to fund the transition to their preferred hydrocarbonless future, while simultaneously hollowing out their biggest competitor, the US, by tying it down in useless skirmishes like Ukraine through NATO.

Uncategorized

Comments on February Employment Report

The headline jobs number in the February employment report was above expectations; however, December and January payrolls were revised down by 167,000 combined. The participation rate was unchanged, the employment population ratio decreased, and the …

Share this:

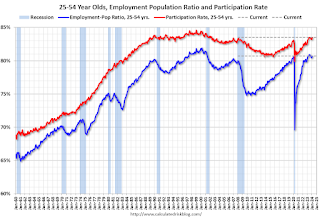

Prime (25 to 54 Years Old) Participation

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

The 25 to 54 years old participation rate increased in February to 83.5% from 83.3% in January, and the 25 to 54 employment population ratio increased to 80.7% from 80.6% the previous month.

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES). Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 4.3% YoY in February.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of people employed part time for economic reasons, at 4.4 million, changed little in February. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons decreased in February to 4.36 million from 4.42 million in February. This is slightly above pre-pandemic levels.

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 7.3% from 7.2% in the previous month. This is down from the record high in April 2020 of 23.0% and up from the lowest level on record (seasonally adjusted) in December 2022 (6.5%). (This series started in 1994). This measure is above the 7.0% level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.203 million workers who have been unemployed for more than 26 weeks and still want a job, down from 1.277 million the previous month.

This is close to pre-pandemic levels.

Job Streak

| Headline Jobs, Top 10 Streaks | ||

|---|---|---|

| Year Ended | Streak, Months | |

| 1 | 2019 | 100 |

| 2 | 1990 | 48 |

| 3 | 2007 | 46 |

| 4 | 1979 | 45 |

| 5 | 20241 | 38 |

| 6 tie | 1943 | 33 |

| 6 tie | 1986 | 33 |

| 6 tie | 2000 | 33 |

| 9 | 1967 | 29 |

| 10 | 1995 | 25 |

| 1Currrent Streak | ||

Summary:

The headline monthly jobs number was above consensus expectations; however, December and January payrolls were revised down by 167,000 combined. The participation rate was unchanged, the employment population ratio decreased, and the unemployment rate was increased to 3.9%. Another solid report.

Uncategorized

Immune cells can adapt to invading pathogens, deciding whether to fight now or prepare for the next battle

When faced with a threat, T cells have the decision-making flexibility to both clear out the pathogen now and ready themselves for a future encounter.

Share this:

How does your immune system decide between fighting invading pathogens now or preparing to fight them in the future? Turns out, it can change its mind.

Every person has 10 million to 100 million unique T cells that have a critical job in the immune system: patrolling the body for invading pathogens or cancerous cells to eliminate. Each of these T cells has a unique receptor that allows it to recognize foreign proteins on the surface of infected or cancerous cells. When the right T cell encounters the right protein, it rapidly forms many copies of itself to destroy the offending pathogen.

Importantly, this process of proliferation gives rise to both short-lived effector T cells that shut down the immediate pathogen attack and long-lived memory T cells that provide protection against future attacks. But how do T cells decide whether to form cells that kill pathogens now or protect against future infections?

We are a team of bioengineers studying how immune cells mature. In our recently published research, we found that having multiple pathways to decide whether to kill pathogens now or prepare for future invaders boosts the immune system’s ability to effectively respond to different types of challenges.

Fight or remember?

To understand when and how T cells decide to become effector cells that kill pathogens or memory cells that prepare for future infections, we took movies of T cells dividing in response to a stimulus mimicking an encounter with a pathogen.

Specifically, we tracked the activity of a gene called T cell factor 1, or TCF1. This gene is essential for the longevity of memory cells. We found that stochastic, or probabilistic, silencing of the TCF1 gene when cells confront invading pathogens and inflammation drives an early decision between whether T cells become effector or memory cells. Exposure to higher levels of pathogens or inflammation increases the probability of forming effector cells.

Surprisingly, though, we found that some effector cells that had turned off TCF1 early on were able to turn it back on after clearing the pathogen, later becoming memory cells.

Through mathematical modeling, we determined that this flexibility in decision making among memory T cells is critical to generating the right number of cells that respond immediately and cells that prepare for the future, appropriate to the severity of the infection.

Understanding immune memory

The proper formation of persistent, long-lived T cell memory is critical to a person’s ability to fend off diseases ranging from the common cold to COVID-19 to cancer.

From a social and cognitive science perspective, flexibility allows people to adapt and respond optimally to uncertain and dynamic environments. Similarly, for immune cells responding to a pathogen, flexibility in decision making around whether to become memory cells may enable greater responsiveness to an evolving immune challenge.

Memory cells can be subclassified into different types with distinct features and roles in protective immunity. It’s possible that the pathway where memory cells diverge from effector cells early on and the pathway where memory cells form from effector cells later on give rise to particular subtypes of memory cells.

Our study focuses on T cell memory in the context of acute infections the immune system can successfully clear in days, such as cold, the flu or food poisoning. In contrast, chronic conditions such as HIV and cancer require persistent immune responses; long-lived, memory-like cells are critical for this persistence. Our team is investigating whether flexible memory decision making also applies to chronic conditions and whether we can leverage that flexibility to improve cancer immunotherapy.

Resolving uncertainty surrounding how and when memory cells form could help improve vaccine design and therapies that boost the immune system’s ability to provide long-term protection against diverse infectious diseases.

Kathleen Abadie was funded by a NSF (National Science Foundation) Graduate Research Fellowships. She performed this research in affiliation with the University of Washington Department of Bioengineering.

Elisa Clark performed her research in affiliation with the University of Washington (UW) Department of Bioengineering and was funded by a National Science Foundation Graduate Research Fellowship (NSF-GRFP) and by a predoctoral fellowship through the UW Institute for Stem Cell and Regenerative Medicine (ISCRM).

Hao Yuan Kueh receives funding from the National Institutes of Health.

stimulus covid-19 yuan vaccine stimulusUncategorized

Stock indexes are breaking records and crossing milestones – making many investors feel wealthier

The S&P 500 topped 5,000 on Feb. 9, 2024, for the first time. The Dow Jones Industrial Average will probably hit a new big round number soon t…

Share this:

{kind=link}

{kind=link}

The S&P 500 stock index topped 5,000 for the first time on Feb. 9, 2024, exciting some investors and garnering a flurry of media coverage. The Conversation asked Alexander Kurov, a financial markets scholar, to explain what stock indexes are and to say whether this kind of milestone is a big deal or not.

What are stock indexes?

Stock indexes measure the performance of a group of stocks. When prices rise or fall overall for the shares of those companies, so do stock indexes. The number of stocks in those baskets varies, as does the system for how this mix of shares gets updated.

The Dow Jones Industrial Average, also known as the Dow, includes shares in the 30 U.S. companies with the largest market capitalization – meaning the total value of all the stock belonging to shareholders. That list currently spans companies from Apple to Walt Disney Co.

The S&P 500 tracks shares in 500 of the largest U.S. publicly traded companies.

The Nasdaq composite tracks performance of more than 2,500 stocks listed on the Nasdaq stock exchange.

The DJIA, launched on May 26, 1896, is the oldest of these three popular indexes, and it was one of the first established.

Two enterprising journalists, Charles H. Dow and Edward Jones, had created a different index tied to the railroad industry a dozen years earlier. Most of the 12 stocks the DJIA originally included wouldn’t ring many bells today, such as Chicago Gas and National Lead. But one company that only got booted in 2018 had stayed on the list for 120 years: General Electric.

The S&P 500 index was introduced in 1957 because many investors wanted an option that was more representative of the overall U.S. stock market. The Nasdaq composite was launched in 1971.

You can buy shares in an index fund that mirrors a particular index. This approach can diversify your investments and make them less prone to big losses.

Index funds, which have only existed since Vanguard Group founder John Bogle launched the first one in 1976, now hold trillions of dollars .

Why are there so many?

There are hundreds of stock indexes in the world, but only about 50 major ones.

Most of them, including the Nasdaq composite and the S&P 500, are value-weighted. That means stocks with larger market values account for a larger share of the index’s performance.

In addition to these broad-based indexes, there are many less prominent ones. Many of those emphasize a niche by tracking stocks of companies in specific industries like energy or finance.

Do these milestones matter?

Stock prices move constantly in response to corporate, economic and political news, as well as changes in investor psychology. Because company profits will typically grow gradually over time, the market usually fluctuates in the short term, while increasing in value over the long term.

The DJIA first reached 1,000 in November 1972, and it crossed the 10,000 mark on March 29, 1999. On Jan. 22, 2024, it surpassed 38,000 for the first time. Investors and the media will treat the new record set when it gets to another round number – 40,000 – as a milestone.

The S&P 500 index had never hit 5,000 before. But it had already been breaking records for several weeks.

Because there’s a lot of randomness in financial markets, the significance of round-number milestones is mostly psychological. There is no evidence they portend any further gains.

For example, the Nasdaq composite first hit 5,000 on March 10, 2000, at the end of the dot-com bubble.

The index then plunged by almost 80% by October 2002. It took 15 years – until March 3, 2015 – for it return to 5,000.

By mid-February 2024, the Nasdaq composite was nearing its prior record high of 16,057 set on Nov. 19, 2021.

Index milestones matter to the extent they pique investors’ attention and boost market sentiment.

Investors afflicted with a fear of missing out may then invest more in stocks, pushing stock prices to new highs. Chasing after stock trends may destabilize markets by moving prices away from their underlying values.

When a stock index passes a new milestone, investors become more aware of their growing portfolios. Feeling richer can lead them to spend more.

This is called the wealth effect. Many economists believe that the consumption boost that arises in response to a buoyant stock market can make the economy stronger.

Is there a best stock index to follow?

Not really. They all measure somewhat different things and have their own quirks.

For example, the S&P 500 tracks many different industries. However, because it is value-weighted, it’s heavily influenced by only seven stocks with very large market values.

Known as the “Magnificent Seven,” shares in Amazon, Apple, Alphabet, Meta, Microsoft, Nvidia and Tesla now account for over one-fourth of the S&P 500’s value. Nearly all are in the tech sector, and they played a big role in pushing the S&P across the 5,000 mark.

This makes the index more concentrated on a single sector than it appears.

But if you check out several stock indexes rather than just one, you’ll get a good sense of how the market is doing. If they’re all rising quickly or breaking records, that’s a clear sign that the market as a whole is gaining.

Sometimes the smartest thing is to not pay too much attention to any of them.

For example, after hitting record highs on Feb. 19, 2020, the S&P 500 plunged by 34% in just 23 trading days due to concerns about what COVID-19 would do to the economy. But the market rebounded, with stock indexes hitting new milestones and notching new highs by the end of that year.

Panicking in response to short-term market swings would have made investors more likely to sell off their investments in too big a hurry – a move they might have later regretted. This is why I believe advice from the immensely successful investor and fan of stock index funds Warren Buffett is worth heeding.

Buffett, whose stock-selecting prowess has made him one of the world’s 10 richest people, likes to say “Don’t watch the market closely.”

If you’re reading this because stock prices are falling and you’re wondering if you should be worried about that, consider something else Buffett has said: “The light can at any time go from green to red without pausing at yellow.”

And the opposite is true as well.

Alexander Kurov does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

dow jones sp 500 nasdaq stocks covid-19

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

People Who Received Ivermectin Were Better Off, Study Finds

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

COVID-19 May Lead To Persistent Cognitive Impairment, Brain Fog, And Lower IQ Scores

Europe Is Alarmed Enough To Begin Wargaming A Food Crisis

Wealth Inequality by Age in the Post‑Pandemic Era

Normalise the underlying conditions when “rating” a company’s share price

COVID-19 Lockdowns Had High Health, Economic Costs: Swedish Study

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges