Uncategorized

Fannie and Freddie: Single Family Serious Delinquency Rate Decreased, Multi-family Decreased in March

Today, in the Calculated Risk Real Estate Newsletter: Fannie and Freddie: Single Family Serious Delinquency Rate Decreased, Multi-family Decreased in March

Brief excerpt: Single-family serious delinquencies decreased in March, and multi-family serious …

Share this:

Brief excerpt:

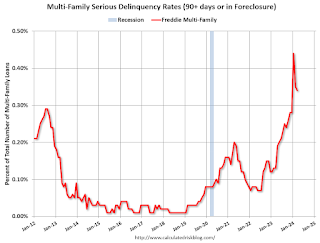

Single-family serious delinquencies decreased in March, and multi-family serious delinquencies decreased again after the huge surge in January.

...

Freddie Mac reports that the multi-family delinquencies rate declined to 0.34% in March, down from 0.35% in February, and down from 0.44% in January.

This graph shows the Freddie multi-family serious delinquency rate since 2012. Rates were still high in 2012 following the housing bust and financial crisis.

The multi-family rate increased following the pandemic and has increased recently as rent growth has slowed, vacancy rates have increased, and borrowing rates have increased sharply. The rate surged higher in January but declined in February and March - but is still at a high level. This will be something to watch as more apartments come on the market.

Uncategorized

Popular fast-food restaurant chain files Chapter 11 bankruptcy

A stack of legal problems has pushed a popular fast-food restaurant chain to file Chapter 11 bankruptcy.

Share this:

The restaurant industry continues navigating through the aftermath of the Covid-19 pandemic, as many fast-food and fast-casual chains battle financial distress related to reduced foot traffic, as well as inflated food prices and rising interest rates.

Fast-casual Tex-Mex chain Tijuana Flats Restaurants on April 19 filed for Chapter 11 bankruptcy in the U.S. Bankruptcy Court for the Middle District of Florida, after launching a strategic review in November 2023 seeking answers for turning around the struggling chain.

Related: Bankrupt fast-food chain exits Chapter 11; to expand size 4 times

The company sold the company to a new ownership group, closed 11 of its locations and filed for a bankruptcy reorganization to revitalize its restaurants and reinvigorate the customer experience.

Reorganization, however, is not an option for another restaurant chain, as Foxtrot and Dom’s Kitchen & Market, with 33 locations across the U.S., filed for Chapter 7 liquidation on April 23 after failing to recover from financial distress dating back to the Covid pandemic.

Another restaurant chain, Sticky's, will have a chance to recover from the Covid pandemic's effects through a reorganization plan.

Sticky's to reorganize in Chapter 11

Sticky's Holdings, the parent company of New York-based chicken fingers fast-food chain Sticky's, filed for Chapter 11 bankruptcy on April 25 to reorganize its business after suffering financial distress from reduced traffic following the Covid pandemic, rising commodity prices, and lawsuits.

The debtor listed $5.75 million in assets and $4.67 million in liabilities in its petition. It's largest unsecured creditor is US Foods, owed over $449,000.

Sticky's, which opened in 2012, grew in sales from about $500,000 in 2013 to $22 million in 2023, but the Covid pandemic that significantly affected the restaurant industry starting in 2020 depressed store traffic. Revenue suffered and foot traffic has not returned to pre-pandemic levels, according to a declaration filed by Sticky's CEO Jamie Greer.

Rising inflation caused commodity prices to increase, forcing Sticky's to raise its menu prices, which further stifled traffic to the restaurant chain. As part of its efforts to reduce costs, the company in early 2021 exited its corporate offices on East 33rd Street in New York before its lease expired, according to the declaration.

Related: Luxury appliance retailer files Chapter 7 bankruptcy to liquidate

Legal problems drive restaurant chain to bankruptcy

The debtor's landlord filed a summary judgment on June 22, 2021, to recover the remaining rent and legal fees, which a court granted with a $600,000 award. The debtor has appealed the judgment costing the company more in legal fees.

More legal problems fell on Sticky's as on June 30, 2022, Sticky Fingers Restaurants LLC filed a lawsuit against Sticky's Holdings in the U.S. District Court for the Southern District of New York for alleged trademark infringement violations. The costs and expenses related to the ongoing litigation has imposed significant further financial hardship on the debtor, court papers said.

The debtor on Feb. 23, 2024, entered into an equity financing transaction that converted $2.42 million in convertible notes issued Nov. 9, 2022, and due March 31, 2024. The transaction substantially reduced the debtor's short-term liquidity needs, the declaration said. However, the company's financial headwinds prevented the debtor from continuing operations leading it to file bankruptcy to seek a reorganization.

Sticky's is a chain of chicken fingers and sandwich restaurants that serves fresh, never frozen and antibiotic-free chicken. It offers 18 in-house sauces for its chicken products.

Sticky's currently operates 12 locations, with nine in New York and three in New Jersey. It has closed two locations in New York and one each in New Jersey and Pennsylvania. The company had established a franchise entity to operate potential franchise operations, but none opened.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocks interest ratesUncategorized

Why Are There So Many Americans That Can’t Find A Job Even Though They Are Desperate To Be Hired?

Why Are There So Many Americans That Can’t Find A Job Even Though They Are Desperate To Be Hired?

Authored by Michael Snyder via The Economic…

Share this:

Authored by Michael Snyder via The Economic Collapse blog,

According to the absurd numbers that the government feeds us, the unemployment rate is very low and there are lots of jobs available. But if what they are telling us is true, why are so many Americans not able to find work? As you will see below, some people haven’t been hired even though they have literally applied for hundreds of jobs.

There seems to be an enormous disconnect between what is actually happening in the real economy and the economic narrative that they are constantly pushing. By the time you are done reading this article, I think that you will agree with me.

Earlier this week, I received an email from a reader that has not been able to find work after seven months of searching.

He gave me permission to share part of that email with you, and it is certainly quite heartbreaking…

Hi Michael,

I am a long-time reader of theeconomiccollapseblog.com, and your recent article comparing the economy to the movie “Weekend at Bernie’s” really stood out to me.

I’m really trying to figure out WHY it is so hard to find a job.

I was laid off from my job as a Custodial Foreman in September 2023, and have had ZERO results for my countless hours spent searching for comparable work.

I don’t know if you want to use any of this for an article or not, but if you do, please just keep doing what you normally do: Praising Jesus Christ. Without my faith in him I don’t know what I’d do.

When I wake up, I make coffee and turn on the computer and go through the state’s unemployment job search sites they provided me when I was laid off. I have been looking and also applying for jobs DAILY since September 2023. And these are not “rocket science” positions; I’m simply looking for Maintenance or Custodial or Groundskeeper type jobs. You know, “normal working class” type jobs.

But after ~300 applications (And these are all just to the jobs that I not only have experience for but also would actually want to do), I have had 1 interview. One interview in 7 months of applying and sending tailored cover letters with, daily!

If the economy is doing so “great”, why can’t he find employment?

Some of you may be tempted to think that he is just an isolated case.

Well, here is another example of an experienced worker that has applied for approximately 300 jobs without any success…

Royal Siu, who lives in Seattle and is trained as a pharmacist, likes to make his friends guess how many jobs he’s applied to. They’ll often toss out some number around 40, he told BI. He’ll tell them to keep going. Most give up by the time they reach 100. That’s when Siu drops that he’s applied to about 300 jobs. “It’s usually a shock factor to them,” he said.

Siu, who’s trying to use his pharmacy degree to work in other parts of healthcare, is finding it harder to land interviews than in a prior job search. The 28-year-old was getting more phone screenings and first and second interviews in the past. This time, it’s been a couple of months since he had a screening call. So he continues to turn to his network but also doesn’t stop applying.

What in the world is going on here?

I thought that there were “millions” of good jobs just waiting for someone to step into them.

Something definitely does not add up.

Even Americans with advanced degrees from top schools are increasingly finding themselves out of work.

If you doubt this, just check out these numbers…

Even at some top business schools, the number of recently minted M.B.A.s without jobs has roughly doubled from a couple of years ago, when U.S. companies were rushing to hire as many workers as they could, according to data from the schools.

At Harvard Business School, 20% of job-seeking 2023 M.B.A. graduates didn’t have one three months after graduation, up from 8% in 2021. At Stanford’s Graduate School of Business, 18% didn’t, compared with 9% in 2021. About 13% of those at the Massachusetts Institute of Technology’s Sloan School of Management didn’t have a job within three months, up from about 5% in 2021.

How are those numbers possible if the unemployment rate is hovering near “historic lows”?

Of course the truth is that we have been sold a lie.

If you do not have a job, you are classified by the U.S. government as either “unemployed” or “not in the labor force”.

In 2008 and 2009, the combined total of those two categories never even reached 90 million.

Today, the combined total of those two categories is over 106 million.

The Biden administration says that only 6,429,000 Americans are officially “unemployed”.

The other 99,989,000 Americans without a job are considered to be “not in the labor force”.

And more will be lumped into those two categories soon, because large employers all over the nation continue to conduct mass layoffs.

For example, thousands of Tesla workers in California and Texas were just notified that they will be losing their jobs…

The notifications in California and Texas, where the electric vehicle (EV) maker has large presences, came in the form of WARN notices, according to reports.

In California, the planned Tesla headcount reductions will hit approximately 3,300 workers, The San Francisco Standard reported Tuesday.

They will apparently occur at locations in a total of four different cities in the Golden State.

Meanwhile, Texas will see almost 2,700 employees in Austin lose their jobs, according to the Austin American-Statesman.

Sadly, the pace of layoffs is likely to increase during the months ahead, because business activity in the U.S. is declining…

The U.S. economy lost momentum in April, a pair of S&P surveys found, as businesses reported a decline in new orders and reduced employment for the first time since the pandemic.

The flash U.S. manufacturing purchasing managers index slipped to a four-month low of 49.9 in April from 51.9 in March.

The S&P flash U.S. services PMI fell to a five-month low of 50.9 this month from 51.7 in March.

The surveys are the first indicators of each month to give a sense of how the U.S. economy is performing.

Meanwhile, the cost of living crisis just continues to escalate.

Shockingly, at one station in California gasoline now costs $7.29 per gallon…

Soaring gas prices have skyrocketed to a whopping $7.29 per gallon in some parts of California – which is above the current the national hourly minimum wage.

While the average price for a gallon of gas varies from state to state – drivers in a certain Silicon Valley town are facing particularly extortionate rates that set them back almost $150 for a full tank.

The Chevron gas station in Menlo Park was exposed on Sunday by a bewildered customer who posted on X that the price per gallon was four cents ‘above the federal hourly minimum wage.’

If you think that this is bad, just wait until the war in the Middle East transforms into the apocalyptic conflict that I believe it will become.

I am entirely convinced that inflation will continue to be a major problem even as economic activity in the U.S. slows down even more.

We are already experiencing “stagflation”.

What is eventually coming will be so much worse than that.

Of course the economic pain that we are going through is just one of the factors that is systematically destroying our nation.

A Warning to America: 25 Ways the US is Being Destroyed | Explained in Under 2 Minutes pic.twitter.com/qwmBO8DmMt

— Western Lensman (@WesternLensman) April 22, 2024

Just about all of our major institutions are crumbling, just about every sector of our society is in the process of melting down, and conditions are rapidly getting worse all around us.

And now we are heading into the most chaotic election season in the entire history of our country.

This is a recipe for disaster, but there is no turning back now.

* * *

Michael’s new book entitled “Chaos” is available in paperback and for the Kindle on Amazon.com, and you can check out his new Substack newsletter right here.

Uncategorized

Another strong personal income and spending report, but beware the uptick in inflation

– by New Deal democratPersonal income and spending has become one of the two most important monthly reports I follow. This is in large part because…

Share this:

{kind=link}

{kind=link}

- by New Deal democrat

In March, nominally income rose 0.5%, while nominal spending for the second month in a row rose a sharp 0.8%. Prices as measured by the PCE deflator increased 0.3% for the month, meaning that in real terms income increased 0.2% and spending rose 0.5%. Since just before the pandemic real incomes are up 7.2%, and spending is up 11.3%:

On a YoY basis, the PCE price index is up 2.7%, the second monthly increase in a row from January’s three year low of 2.4%. While n the previous 16 months, the YoY measure had been declining at the rate of 0.25%/month, suggesting that it would hit the Fed’s 2.0% target this spring, that trend has stopped:

As I indicated in the intro, for the past 50+ years, real spending on services has generally increased even during recessions. It is real spending on goods which declines. Last month real services spending rose 0.2%, while real goods spending rose a sharp 1.1%:

Popular fast-food restaurant chain files Chapter 11 bankruptcy

Popular fast-food chain files Chapter 11 bankruptcy facing lawsuits

Cashless Society: WEF Boasts That 98% Of Central Banks Are Adopting CBDCs

The Biotech Startup Contraction Continues… And That’s A Good Thing

Philly Fed: State Coincident Indexes Increased in 44 States in March (3-Month Basis)

Target store introduces a new ‘over 18’ policy

Popular fast-food chain files Chapter 11 bankruptcy; faces lawsuits

Bankrupt fast-food chain exits Chapter 11; to expand size 4 times

U.S. growth slowdown, with inflation spike, raises early stagflation risks

Another strong personal income and spending report, but beware the uptick in inflation

-

Government3 weeks ago

Government3 weeks agoClimate-Con & The Media-Censorship Complex – Part 1

-

Spread & Containment1 week ago

Spread & Containment1 week agoJ&J’s AI head jumps to Recursion; Doug Williams resigns as Sana’s R&D chief

-

Government3 days ago

Government3 days agoCOVID-19 Vaccine Emails: Here’s What The CDC Hid Behind Redactions

-

Spread & Containment2 weeks ago

Spread & Containment2 weeks agoWHO Official Admits Vaccine Passports May Have Been A Scam

-

Spread & Containment3 weeks ago

Spread & Containment3 weeks agoFDA Finally Takes Down Ivermectin Posts After Settlement

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoVaccinated People Show Long COVID-Like Symptoms With Detectable Spike Proteins: Preprint Study

-

Uncategorized1 hour ago

Popular fast-food restaurant chain files Chapter 11 bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCan language models read the genome? This one decoded mRNA to make better vaccines.