Uncategorized

Digital Realty Reports Fourth Quarter 2022 Results

Digital Realty Reports Fourth Quarter 2022 Results

PR Newswire

AUSTIN, Texas, Feb. 16, 2023

AUSTIN, Texas, Feb. 16, 2023 /PRNewswire/ — Digital Realty (NYSE: DLR), the largest global provider of cloud- and carrier-neutral data center, colocation a…

Share this:

Digital Realty Reports Fourth Quarter 2022 Results

PR Newswire

AUSTIN, Texas, Feb. 16, 2023

AUSTIN, Texas, Feb. 16, 2023 /PRNewswire/ -- Digital Realty (NYSE: DLR), the largest global provider of cloud- and carrier-neutral data center, colocation and interconnection solutions, announced today financial results for the fourth quarter of 2022. All per share results are presented on a fully diluted basis.

Highlights

- Reported net (loss) / income available to common stockholders of ($0.02) per share in 4Q22, compared to $3.71 in 4Q21

- Reported FFO per share of $1.45 in 4Q22, compared to $1.54 in 4Q21

- Reported Core FFO per share of $1.65 in 4Q22, compared to $1.67 in 4Q21

- Reported Constant-Currency Core FFO per share of $1.71 in 4Q22 and $6.91 per share for the twelve months ended December 31, 2022

- Signed total bookings during 4Q22 that are expected to generate $117 million of annualized GAAP rental revenue, including a $14 million contribution from interconnection

- Introduced 2023 Core FFO per share outlook of $6.65 - $6.75

Financial Results

Digital Realty reported revenues for the fourth quarter of 2022 of $1.2 billion, a 3% increase from the previous quarter and a 11% increase from the same quarter last year.

The company delivered fourth quarter of 2022 net income of $1 million, and net (loss) / income available to common stockholders of ($6) million, or ($0.02) per diluted share, compared to $0.75 per diluted share in the previous quarter and $3.71 per diluted share in the same quarter last year.

Digital Realty generated fourth quarter of 2022 Adjusted EBITDA of $639 million, a 3% increase from the previous quarter and a 9% increase over the same quarter last year.

The company reported fourth quarter of 2022 funds from operations (FFO) of $440 million, or $1.45 per share, compared to $1.55 per share in the previous quarter and $1.54 per share in the same quarter last year.

Excluding certain items that do not represent core expenses or revenue streams, Digital Realty delivered fourth quarter of 2022 Core FFO per share of $1.65, compared to $1.67 per share in the previous quarter, and $1.67 per share in the same quarter last year. Digital Realty delivered Constant-Currency Core FFO per share of $1.71 for the fourth quarter of 2022 and $6.91 per share for the twelve-month period ended December 31, 2022.

Leasing Activity

In the fourth quarter, Digital Realty signed total bookings that are expected to generate $117 million of annualized GAAP rental revenue, including a $14 million contribution from interconnection.

"Our fourth quarter results demonstrate the strengthening value proposition of PlatformDIGITAL and the growing momentum in our core business," said Digital Realty President and Chief Executive Officer Andy Power. "The Digital Realty team will continue to focus on delivering innovative and sustainable data center solutions while evolving to efficiently enable our customers to transform their businesses and succeed in the digital world."

The weighted-average lag between new leases signed during the fourth quarter of 2022 and the contractual commencement date was fifteen months.

In addition to new leases signed, Digital Realty also signed renewal leases representing $195 million of annualized GAAP rental revenue during the quarter. Rental rates on renewal leases signed during the fourth quarter of 2022 rolled up 0.8% on a cash basis and up 1.1% on a GAAP basis.

New leases signed during the fourth quarter of 2022 are summarized by region as follows:

Annualized GAAP | |||||||||||||

Base Rent | GAAP Base Rent | GAAP Base Rent | |||||||||||

The Americas | (in thousands) | Square Feet | per Square Foot | Megawatts | per Kilowatt | ||||||||

0-1 MW | $10,437 | 39 | $266 | 3.5 | $251 | ||||||||

> 1 MW | 23,311 | 217 | 107 | 18.6 | 104 | ||||||||

Other (1) | 11 | 0 | 52 | — | - | ||||||||

Total | $33,759 | 257 | $132 | 22.1 | $127 | ||||||||

EMEA (2) | |||||||||||||

0-1 MW | $20,492 | 49 | $415 | 6.5 | $264 | ||||||||

> 1 MW | 24,291 | 224 | 109 | 16.4 | 123 | ||||||||

Other (1) | 304 | 12 | 25 | — | - | ||||||||

Total | $45,087 | 285 | $158 | 22.9 | $163 | ||||||||

Asia Pacific (2) | |||||||||||||

0-1 MW | $2,240 | 5 | $409 | 0.4 | $463 | ||||||||

> 1 MW | 22,455 | 114 | 197 | 14.0 | 134 | ||||||||

Other (1) | 93 | 2 | 55 | — | - | ||||||||

Total | $24,788 | 121 | $204 | 14.4 | $143 | ||||||||

All Regions (2) | |||||||||||||

0-1 MW | $33,169 | 94 | $353 | 10.4 | $267 | ||||||||

> 1 MW | 70,057 | 555 | 126 | 49.0 | 119 | ||||||||

Other (1) | 409 | 14 | 29 | — | - | ||||||||

Total | $103,634 | 663 | $156 | 59.4 | $145 | ||||||||

Interconnection | $13,564 | N/A | N/A | N/A | N/A | ||||||||

Grand Total | $117,198 | 663 | $156 | 59.4 | $145 | ||||||||

Note: Totals may not foot due to rounding differences. | |

(1) | Other includes Powered Base Building® shell capacity as well as storage and office space within fully improved data center facilities. |

(2) | Based on quarterly average exchange rates during the three months ended December 31, 2022. |

Investment Activity

During the fourth quarter, Digital Realty closed on the sale of a 25% interest in a data center facility in Frankfurt, Germany to Digital Core REIT (SGX: DCRU) in a transaction that valued the facility at €558 million, or approximately $596 million (at 100% share). The transaction generated net proceeds to Digital Realty of €139.6 million, or approximately $150 million. Digital Core REIT has an option to acquire up to an 89.9% interest in the Frankfurt facility, subject to market conditions.

Also during the fourth quarter, Digital Realty acquired four sites totaling 65 acres that will support the future development of up to 84 megawatts of IT load for $55 million, or approximately $0.8 million per acre. Separately, Digital Realty entered into a ground lease with an option to purchase a 4.6-acre land parcel adjacent to its Dugny campus in Paris, France for a total expected investment of €34.3 million, or approximately $36.6 million.

Balance Sheet

Digital Realty had approximately $16.6 billion of total debt outstanding as of December 31, 2022, comprised of $16.1 billion of unsecured debt and approximately $0.5 billion of secured debt and other. At the end of the fourth quarter of 2022, net debt-to-Adjusted EBITDA was 6.9x, debt-plus-preferred-to-total enterprise value was 36.8% and fixed charge coverage was 4.9x.

During the fourth quarter of 2022, Digital Realty completed the following financing transactions:

- In mid-November, completed physical settlement of the remaining $0.5 billion under our September 2021 forward equity sale agreements.

- In early December, closed an offering of $350 million of additional 5.550% notes due 2028.

Subsequent to quarter end, Digital Realty closed a $740 million two-year US dollar term loan with an initial maturity date of March 31, 2025 and a one-year extension option.

2023 Outlook

Digital Realty introduced its 2023 Core FFO per share outlook of $6.65-$6.75 and provided its 2023 constant-currency Core FFO per share outlook of $6.65 - $6.75. The assumptions underlying the outlook are summarized in the following table.

As of | ||

Top-Line and Cost Structure | February 16, 2023 | |

Total revenue | $5.700 - $5.800 billion | |

Net non-cash rent adjustments (1) | ($55 - $60 million) | |

Adjusted EBITDA | $2.675 - $2.725 billion | |

G&A | $425 - $435 million | |

Internal Growth | ||

Rental rates on renewal leases | ||

Cash basis | Greater than 3.0% | |

GAAP basis | Greater than 3.0% | |

Year-end portfolio occupancy | 85.0% - 86.0% | |

"Same-capital" cash NOI growth (2) | 3.0% - 4.0% | |

Foreign Exchange Rates | ||

U.S. Dollar / Pound Sterling | $1.20 - $1.25 | |

U.S. Dollar / Euro | $1.00 - $1.05 | |

External Growth | ||

Dispositions / Joint Venture Capital | ||

Dollar volume | $1.5 - $2.5 billion | |

Cap rate | 0.0% - 10.0% | |

Development | ||

CapEx (3) | $2.3 - $2.5 billion | |

Average stabilized yields | 9.0% - 15.0% | |

Enhancements and other non-recurring CapEx (4) | $15 - $20 million | |

Recurring CapEx + capitalized leasing costs (5) | $230 - $240 million | |

Balance Sheet | ||

Long-term debt issuance | ||

Dollar amount | $1.0 - $1.5 billion | |

Pricing | 4.5% - 5.5% | |

Timing | First Half 2023 | |

Net income per diluted share | $1.15 - $1.25 | |

Real estate depreciation and (gain) / loss on sale | $5.25 - $5.25 | |

Funds From Operations / share (NAREIT-Defined) | $6.40 - $6.50 | |

Non-core expenses and revenue streams | $0.25 - $0.25 | |

Core Funds From Operations / share | $6.65 - $6.75 | |

Foreign currency translation adjustments | $0.00 - $0.00 | |

Constant-Currency Core Funds From Operations / share | $6.65 - $6.75 |

(1) | Net non-cash rent adjustments represent the sum of straight-line rental revenue and straight-line rental expense, as well as the amortization of above- and below-market leases (i.e., ASC 805 adjustments). |

(2) | The "same-capital" pool includes properties owned as of December 31, 2021 with less than 5% of total rentable square feet under development. It excludes properties that were undergoing, or were expected to undergo, development activities in 2022-2023, properties classified as held for sale, and properties sold or contributed to joint ventures for all periods presented. |

(3) | Includes land acquisitions. |

(4) | Other non-recurring CapEx represents costs incurred to enhance the capacity or marketability of operating properties, such as network fiber initiatives and software development costs. |

(5) | Recurring CapEx represents non-incremental improvements required to maintain current revenues, including second-generation tenant improvements and leasing commissions. |

Note: The Company does not provide a reconciliation for non-GAAP estimates on a forward-looking basis, where it is unable to provide a meaningful or accurate calculation or estimation of reconciling items and the information is not available without unreasonable effort. Please see Non-GAAP Financial Measures in this document for further discussion. | |

Non-GAAP Financial Measures

This document contains non-GAAP financial measures, including FFO, Core FFO and Adjusted EBITDA. A reconciliation from U.S. GAAP net income available to common stockholders to FFO, a reconciliation from FFO to Core FFO, and definitions of FFO and Core FFO are included as an attachment to this document. A reconciliation from U.S. GAAP net income available to common stockholders to Adjusted EBITDA, a definition of Adjusted EBITDA and definitions of net debt-to-Adjusted EBITDA, debt-plus-preferred-to-total enterprise value, cash NOI, and fixed charge coverage ratio are included as an attachment to this document.

The Company does not provide a reconciliation for non-GAAP estimates on a forward-looking basis, where it is unable to provide a meaningful or accurate calculation or estimation of reconciling items and the information is not available without unreasonable effort. This is due to the inherent difficulty of forecasting the timing and/or amount of various items that would impact net income attributable to common stockholders per diluted share, which is the most directly comparable forward-looking GAAP financial measure. This includes, for example, external growth factors, such as dispositions, and balance sheet items, such as debt issuances, that have not yet occurred, are out of the Company's control and/or cannot be reasonably predicted. For the same reasons, the Company is unable to address the probable significance of the unavailable information. Forward-looking non-GAAP financial measures provided without the most directly comparable GAAP financial measures may vary materially from the corresponding GAAP financial measures.

Investor Conference Call

Prior to Digital Realty's investor conference call at 5:00 p.m. ET / 2:00 p.m. PT on February 16, 2023, a presentation will be posted to the Investors section of the company's website at https://investor.digitalrealty.com/. The presentation is designed to accompany the discussion of the company's fourth quarter 2022 financial results and operating performance. The conference call will feature President & Chief Executive Officer Andy Power and Chief Financial Officer Matt Mercier.

To participate in the live call, investors are invited to dial +1 (888) 317-6003 (for domestic callers) or +1 (412) 317-6061 (for international callers) and reference the conference ID# 6468514 at least five minutes prior to start time. A live webcast of the call will be available via the Investors section of Digital Realty's website at https://investor.digitalrealty.com/.

Telephone and webcast replays will be available after the call until March 16, 2023. The telephone replay can be accessed by dialing +1 (877) 344-7529 (for domestic callers) or +1 (412) 317-0088 (for international callers) and providing the conference ID# 6581304. The webcast replay can be accessed on Digital Realty's website.

About Digital Realty

Digital Realty brings companies and data together by delivering the full spectrum of data center, colocation and interconnection solutions. PlatformDIGITAL®, the company's global data center platform, provides customers with a secure data "meeting place" and a proven Pervasive Datacenter Architecture (PDx®) solution methodology for powering innovation and efficiently managing Data Gravity challenges. Digital Realty gives its customers access to the connected communities that matter to them with a global data center footprint of 300+ facilities in 50+ metros across 28 countries on six continents. To learn more about Digital Realty, please visit digitalrealty.com or follow us on LinkedIn and Twitter.

Contact Information

Matt Mercier

Chief Financial Officer

Digital Realty

(737) 281-0101

Jordan Sadler / Jim Huseby

Investor Relations

Digital Realty

(737) 281-0101

Consolidated Quarterly Statements of Operations | Financial Supplement | |||||||||||||||||||||||

Unaudited and Dollars in Thousands, Except Per Share Data | Fourth Quarter 2022 | |||||||||||||||||||||||

Three Months Ended | Twelve Months Ended | |||||||||||||||||||||||

31-Dec-22 | 30-Sep-22 | 30-Jun-22 | 31-Mar-22 | 31-Dec-21 | 31-Dec-22 | 31-Dec-21 | ||||||||||||||||||

Rental revenues | $834,374 | $787,839 | $767,313 | $751,962 | $763,117 | $3,141,488 | $3,059,682 | |||||||||||||||||

Tenant reimbursements - Utilities | 247,725 | 251,420 | 218,198 | 224,547 | 195,340 | 941,891 | 739,116 | |||||||||||||||||

Tenant reimbursements - Other | 46,045 | 49,419 | 52,688 | 51,511 | 58,528 | 199,663 | 235,783 | |||||||||||||||||

Interconnection & other | 97,286 | 95,486 | 93,338 | 93,530 | 89,850 | 379,641 | 360,459 | |||||||||||||||||

Fee income | 7,508 | 6,169 | 5,072 | 5,757 | 4,133 | 24,506 | 13,442 | |||||||||||||||||

Other | 168 | 1,749 | 2,713 | 15 | 200 | 4,645 | 19,401 | |||||||||||||||||

Total Operating Revenues | $1,233,108 | $1,192,082 | $1,139,321 | $1,127,323 | $1,111,167 | $4,691,834 | $4,427,883 | |||||||||||||||||

Utilities | $268,561 | $271,844 | $223,426 | $241,239 | $213,933 | $1,005,070 | $784,574 | |||||||||||||||||

Rental property operating | 222,430 | 205,886 | 198,076 | 194,354 | 205,250 | 820,746 | 785,931 | |||||||||||||||||

Property taxes | 42,032 | 39,860 | 47,213 | 46,526 | 42,673 | 175,631 | 190,388 | |||||||||||||||||

Insurance | 4,578 | 4,002 | 3,836 | 3,698 | 3,507 | 16,114 | 17,425 | |||||||||||||||||

Depreciation & amortization | 430,130 | 388,704 | 376,967 | 382,132 | 378,883 | 1,577,933 | 1,486,632 | |||||||||||||||||

General & administration | 104,451 | 95,792 | 101,991 | 96,435 | 103,705 | 398,669 | 393,311 | |||||||||||||||||

Severance, equity acceleration, and legal expenses | 15,980 | 1,655 | 3,786 | 2,077 | 1,003 | 23,498 | 7,343 | |||||||||||||||||

Transaction and integration expenses | 17,350 | 25,862 | 13,586 | 11,968 | 12,427 | 68,766 | 47,426 | |||||||||||||||||

Impairment of investments in real estate | 3,000 | — | — | — | 18,291 | 3,000 | 18,291 | |||||||||||||||||

Other expenses | 3,615 | 1,096 | 70 | 7,657 | (1) | 12,438 | 2,550 | |||||||||||||||||

Total Operating Expenses | $1,112,127 | $1,034,701 | $968,950 | $986,087 | $979,669 | $4,101,865 | $3,733,874 | |||||||||||||||||

Operating Income | $120,981 | $157,381 | $170,371 | $141,236 | $131,498 | $589,969 | $694,009 | |||||||||||||||||

Equity in earnings (loss) of unconsolidated joint ventures | (28,112) | (12,254) | (34,088) | 60,958 | (7,714) | (13,496) | 62,282 | |||||||||||||||||

Gain / (loss) on sale of investments | (6) | 173,990 | — | 2,770 | 1,047,011 | 176,754 | 1,380,796 | |||||||||||||||||

Interest and other income (expense), net | (22,894) | 15,752 | 13,008 | 3,051 | (4,349) | 8,918 | (4,358) | |||||||||||||||||

Interest (expense) | (86,882) | (76,502) | (69,023) | (66,725) | (71,762) | (299,132) | (293,846) | |||||||||||||||||

Income tax benefit / (expense) | 17,676 | (19,576) | (16,406) | (13,244) | (3,961) | (31,551) | (72,799) | |||||||||||||||||

Loss from early extinguishment of debt | — | — | — | (51,135) | (325) | (51,135) | (18,672) | |||||||||||||||||

Net Income | $763 | $238,791 | $63,862 | $76,911 | $1,090,397 | $380,327 | $1,747,412 | |||||||||||||||||

Net loss / (income) attributable to noncontrolling interests | 3,326 | (1,716) | (436) | (3,629) | (22,587) | (2,455) | (38,153) | |||||||||||||||||

Net (Loss) / Income Attributable to Digital Realty Trust, Inc. | $4,089 | $237,075 | $63,426 | $73,282 | $1,067,811 | $377,872 | $1,709,259 | |||||||||||||||||

Preferred stock dividends, including undeclared dividends | (10,181) | (10,181) | (10,181) | (10,181) | (10,181) | (40,725) | (45,761) | |||||||||||||||||

Gain on / (Issuance costs associated with) redeemed preferred stock | — | — | — | — | — | — | 18,000 | |||||||||||||||||

Net (Loss) / Income Available to Common Stockholders | ($6,093) | $226,894 | $53,245 | $63,101 | $1,057,630 | $337,147 | $1,681,498 | |||||||||||||||||

Weighted-average shares outstanding - basic | 289,364,739 | 286,693,071 | 284,694,064 | 284,525,992 | 283,869,662 | 286,333,747 | 282,474,927 | |||||||||||||||||

Weighted-average shares outstanding - diluted | 301,712,082 | 296,414,726 | 285,109,903 | 285,025,099 | 284,868,184 | 297,919,336 | 283,221,968 | |||||||||||||||||

Weighted-average fully diluted shares and units | 307,546,353 | 302,257,518 | 290,944,163 | 290,662,421 | 290,893,110 | 303,708,327 | 289,912,489 | |||||||||||||||||

Net (loss) / income per share - basic | ($0.02) | $0.79 | $0.19 | $0.22 | $3.73 | $1.18 | $5.95 | |||||||||||||||||

Net (loss) / income per share - diluted | ($0.02) | $0.75 | $0.19 | $0.22 | $3.71 | $1.13 | $5.94 | |||||||||||||||||

Funds From Operations and Core Funds From Operations | Financial Supplement | |||||||||||||||||||||||

Unaudited and in Thousands, Except Per Share Data | Fourth Quarter 2022 | |||||||||||||||||||||||

Three Months Ended | Twelve Months Ended | |||||||||||||||||||||||

Reconciliation of Net Income to Funds From Operations (FFO) | 31-Dec-22 | 30-Sep-22 | 30-Jun-22 | 31-Mar-22 | 31-Dec-21 | 31-Dec-22 | 31-Dec-21 | |||||||||||||||||

Net (Loss) / Income Available to Common Stockholders | ($6,093) | $226,894 | $53,245 | $63,101 | $1,057,630 | $337,147 | $1,681,498 | |||||||||||||||||

Adjustments: | ||||||||||||||||||||||||

Non-controlling interest in operating partnership | (586) | 5,400 | 1,500 | 1,600 | 23,100 | 7,914 | 39,100 | |||||||||||||||||

Real estate related depreciation & amortization (1) | 422,951 | 381,425 | 369,327 | 374,162 | 372,447 | 1,547,865 | 1,463,512 | |||||||||||||||||

Depreciation related to non-controlling interests | (13,856) | (8,254) | - | - | - | (22,110) | - | |||||||||||||||||

Unconsolidated JV real estate related depreciation & amortization | 33,927 | 30,831 | 29,022 | 29,320 | 24,146 | 123,099 | 85,800 | |||||||||||||||||

(Gain) / loss on real estate transactions | 572 | (173,990) | (1,144) | (2,770) | (1,047,010) | (177,332) | (1,445,229) | |||||||||||||||||

Impairment of investments in real estate | 3,000 | - | - | - | 18,291 | 3,000 | 18,291 | |||||||||||||||||

Funds From Operations - diluted | $439,915 | $462,306 | $451,949 | $465,412 | $448,602 | $1,819,583 | $1,842,971 | |||||||||||||||||

Weighted-average shares and units outstanding - basic | 295,199 | 292,536 | 290,528 | 290,163 | 289,895 | 292,123 | 289,165 | |||||||||||||||||

Weighted-average shares and units outstanding - diluted (2)(3) | 307,546 | 302,258 | 290,944 | 290,662 | 290,893 | 303,708 | 289,912 | |||||||||||||||||

Funds From Operations per share - basic | $1.49 | $1.58 | $1.56 | $1.60 | $1.55 | $6.23 | $6.37 | |||||||||||||||||

Funds From Operations per share - diluted (2)(3) | $1.45 | $1.55 | $1.55 | $1.60 | $1.54 | $6.03 | $6.36 | |||||||||||||||||

Three Months Ended | Twelve Months Ended | |||||||||||||||||||||||

Reconciliation of FFO to Core FFO | 31-Dec-22 | 30-Sep-22 | 30-Jun-22 | 31-Mar-22 | 31-Dec-21 | 31-Dec-22 | 31-Dec-21 | |||||||||||||||||

Funds From Operations - diluted | $439,915 | $462,306 | $451,949 | $465,412 | $448,602 | $1,819,583 | $1,842,971 | |||||||||||||||||

Other non-core revenue adjustments | (3,786) | (1,818) | 456 | 13,916 | 9,859 | 8,768 | (19,388) | |||||||||||||||||

Transaction and integration expenses | 17,350 | 25,862 | 13,586 | 11,968 | 12,427 | 68,766 | 47,426 | |||||||||||||||||

Loss from early extinguishment of debt | - | - | - | 51,135 | 325 | 51,135 | 18,672 | |||||||||||||||||

(Gain on) / Issuance costs associated with redeemed preferred stock | - | - | - | - | - | - | (18,000) | |||||||||||||||||

Severance, equity acceleration, and legal expenses (4) | 15,980 | 1,655 | 3,786 | 2,077 | 1,003 | 23,498 | 7,343 | |||||||||||||||||

(Gain) / Loss on FX revaluation | 14,564 | (1,120) | 29,539 | (67,676) | 14,308 | (24,694) | 30,505 | |||||||||||||||||

Other non-core expense adjustments | 3,615 | 1,046 | 70 | 7,657 | (1) | 12,388 | (15,939) | |||||||||||||||||

Core Funds From Operations - diluted | $487,638 | $487,931 | $499,386 | $484,490 | $486,525 | $1,959,444 | $1,893,590 | |||||||||||||||||

Weighted-average shares and units outstanding - diluted (2)(3) | 295,519 | 292,830 | 290,944 | 290,662 | 290,893 | 292,528 | 289,912 | |||||||||||||||||

Core Funds From Operations per share - diluted (3) | $1.65 | $1.67 | $1.72 | $1.67 | $1.67 | $6.70 | $6.53 | |||||||||||||||||

(1) Real Estate Related Depreciation & Amortization | Three Months Ended | Twelve Months Ended | ||||||||||||||||||||||

31-Dec-22 | 30-Sep-22 | 30-Jun-22 | 31-Mar-22 | 31-Dec-21 | 31-Dec-22 | 31-Dec-21 | ||||||||||||||||||

Depreciation & amortization per income statement | $430,130 | $388,704 | $376,967 | $382,132 | $378,883 | 1,577,933 | 1,486,632 | |||||||||||||||||

Non-real estate depreciation | (7,179) | (7,279) | (7,640) | (7,970) | (6,436) | (30,068) | (23,120) | |||||||||||||||||

Real Estate Related Depreciation & Amortization | $422,951 | $381,425 | $369,327 | $374,162 | $372,447 | $1,547,865 | 1,463,512 | |||||||||||||||||

(2) | For all periods presented, we have excluded the effect of dilutive series C, series J, series K and series L preferred stock, as applicable, that may be converted into common stock upon the occurrence of specified change in control transactions as described in the articles supplementary governing the series C, series J, series K and series L preferred stock, as applicable, which we consider highly improbable. See above for calculations of diluted FFO and the share count detail section that follows the reconciliation of Core FFO to AFFO for calculations of weighted average common stock and units outstanding. For definitions and discussion of FFO and Core FFO, see the definitions section. |

(3) | Certain of Teraco's minority indirect shareholders have the right to put their shares in an upstream parent company of Teraco to Digital Realty in exchange for cash or the equivalent value of shares of Digital Realty common stock, or a combination thereof. US GAAP requires Digital Realty to assume the put right is settled in shares for purposes of calculating diluted EPS. This same approach was utilized to calculate FFO/share. The potential future dilutive impact associated with this put right will be excluded from Core FFO and AFFO until settlement occurs – causing diluted share count to be higher for FFO than for Core FFO and AFFO. |

(4) | Relates to severance and other charges related to the departure of company executives and integration-related severance. |

Adjusted Funds From Operations (AFFO) | Financial Supplement | |||||||||||||||||||||||

Unaudited and in Thousands, Except Per Share Data | Fourth Quarter 2022 | |||||||||||||||||||||||

Three Months Ended | Twelve Months Ended | |||||||||||||||||||||||

Reconciliation of Core FFO to AFFO | 31-Dec-22 | 30-Sep-22 | 30-Jun-22 | 31-Mar-22 | 31-Dec-21 | 31-Dec-22 | 31-Dec-21 | |||||||||||||||||

Core FFO available to common stockholders and unitholders | $487,638 | $487,931 | $499,386 | $484,490 | $486,525 | $1,959,444 | $1,893,590 | |||||||||||||||||

Adjustments: | ||||||||||||||||||||||||

Non-real estate depreciation | 7,179 | 7,279 | 7,640 | 7,970 | 6,436 | 30,068 | 23,120 | |||||||||||||||||

Amortization of deferred financing costs | 3,753 | 3,270 | 3,330 | 3,634 | 3,515 | 13,987 | 14,397 | |||||||||||||||||

Amortization of debt discount/premium | 1,276 | 1,146 | 1,193 | 1,214 | 1,107 | 4,829 | 4,545 | |||||||||||||||||

Non-cash stock-based compensation expense | 16,042 | 15,948 | 15,799 | 14,453 | 15,097 | 62,242 | 61,855 | |||||||||||||||||

Straight-line rental revenue | (29,392) | (18,123) | (17,278) | (18,810) | (16,497) | (83,604) | (63,096) | |||||||||||||||||

Straight-line rental expense | (208) | 2,679 | (2,237) | 4,168 | 5,753 | 4,401 | 27,499 | |||||||||||||||||

Above- and below-market rent amortization | (762) | (465) | 196 | 335 | 910 | (696) | 6,070 | |||||||||||||||||

Deferred tax expense / (benefit) | (4,885) | (5,233) | (769) | (1,604) | (13,731) | (12,491) | 19,394 | |||||||||||||||||

Leasing compensation & internal lease commissions | 9,578 | 9,866 | 9,411 | 13,261 | 9,564 | 42,117 | 42,826 | |||||||||||||||||

Recurring capital expenditures (1) | (109,999) | (66,200) | (43,497) | (46,770) | (87,550) | (266,466) | (217,103) | |||||||||||||||||

AFFO available to common stockholders and unitholders (2) | $380,220 | $438,097 | $473,173 | $462,341 | $411,130 | $1,753,831 | $1,813,096 | |||||||||||||||||

Weighted-average shares and units outstanding - basic | 295,199 | 292,536 | 290,528 | 290,163 | 289,895 | 292,123 | 289,165 | |||||||||||||||||

Weighted-average shares and units outstanding - diluted (3) | 295,519 | 292,830 | 290,944 | 290,662 | 290,893 | 292,528 | 289,912 | |||||||||||||||||

AFFO per share - diluted (3) | $1.29 | $1.50 | $1.63 | $1.59 | $1.41 | $6.00 | $6.25 | |||||||||||||||||

Dividends per share and common unit | $1.22 | $1.22 | $1.22 | $1.22 | $1.16 | $4.88 | $4.64 | |||||||||||||||||

. | ||||||||||||||||||||||||

Diluted AFFO Payout Ratio | 94.8 % | 81.5 % | 75.0 % | 76.7 % | 82.1 % | 81.4 % | 74.2 % | |||||||||||||||||

Three Months Ended | Twelve Months Ended | |||||||||||||||||||||||

Share Count Detail | 31-Dec-22 | 30-Sep-22 | 30-Jun-22 | 31-Mar-22 | 31-Dec-21 | 31-Dec-22 | 31-Dec-21 | |||||||||||||||||

Weighted Average Common Stock and Units Outstanding | 295,199 | 292,536 | 290,528 | 290,163 | 289,895 | 292,123 | 289,165 | |||||||||||||||||

Add: Effect of dilutive securities | 320 | 294 | 416 | 499 | 998 | 405 | 747 | |||||||||||||||||

Weighted Avg. Common Stock and Units Outstanding - diluted | 295,519 | 292,830 | 290,944 | 290,662 | 290,893 | 292,528 | 289,912 | |||||||||||||||||

(1) | Recurring capital expenditures represent non-incremental building improvements required to maintain current revenues, including second-generation tenant improvements and external leasing commissions. Recurring capital expenditures do not include acquisition costs contemplated when underwriting the purchase of a building, costs which are incurred to bring a building up to Digital Realty's operating standards, or internal leasing commissions. |

(2) | For a definition and discussion of AFFO, see the definitions section. For a reconciliation of net income available to common stockholders to FFO and Core FFO, see above. |

(3) | For all periods presented, we have excluded the effect of dilutive series C, series J, series K and series L preferred stock, as applicable, that may be converted into common stock upon the occurrence of specified change in control transactions as described in the articles supplementary governing the series C, series J, series K and series L preferred stock, as applicable, which we consider highly improbable. See above for calculations of diluted FFO available to common stockholders and unitholders and for calculations of weighted average common stock and units outstanding. |

Consolidated Balance Sheets | Financial Supplement | |||||||||||||||||||||

Unaudited and in Thousands, Except Share and Per Share Data | Fourth Quarter 2022 | |||||||||||||||||||||

31-Dec-22 | 30-Sep-22 | 30-Jun-22 | 31-Mar-22 | 31-Dec-21 | ||||||||||||||||||

Assets | ||||||||||||||||||||||

Investments in real estate: | ||||||||||||||||||||||

Real estate | $26,136,057 | $24,876,600 | $24,065,933 | $23,769,712 | $23,625,451 | |||||||||||||||||

Construction in progress | 4,789,134 | 4,222,142 | 3,362,114 | 3,523,484 | 3,213,387 | |||||||||||||||||

Land held for future development | 118,452 | 34,713 | 37,460 | 107,003 | 133,683 | |||||||||||||||||

Investments in real estate | $31,043,643 | $29,133,455 | $27,465,507 | $27,400,199 | $26,972,522 | |||||||||||||||||

Accumulated depreciation and amortization | (7,268,981) | (6,826,918) | (6,665,118) | (6,467,233) | (6,210,281) | |||||||||||||||||

Net Investments in Properties | $23,774,662 | $22,306,537 | $20,800,389 | $20,932,966 | $20,762,241 | |||||||||||||||||

Investment in unconsolidated joint ventures | 1,991,426 | 1,912,958 | 1,942,549 | 2,044,074 | 1,807,689 | |||||||||||||||||

Net Investments in Real Estate | $25,766,088 | $24,219,495 | $22,742,937 | $22,977,040 | $22,569,930 | |||||||||||||||||

Cash and cash equivalents | $141,773 | $176,969 | $99,226 | $157,964 | $142,698 | |||||||||||||||||

Accounts and other receivables (1) | 969,292 | 861,117 | 797,208 | 774,579 | 671,721 | |||||||||||||||||

Deferred rent | 601,590 | 556,198 | 554,016 | 545,666 | 547,385 | |||||||||||||||||

Customer relationship value, deferred leasing costs & other intangibles, net | 3,092,627 | 3,035,861 | 2,521,390 | 2,640,795 | 2,735,486 | |||||||||||||||||

Goodwill | 9,208,497 | 8,728,105 | 7,545,107 | 7,802,440 | 7,937,440 | |||||||||||||||||

Operating lease right-of-use assets | 1,351,329 | 1,253,393 | 1,310,970 | 1,361,942 | 1,405,441 | |||||||||||||||||

Other assets | 353,802 | 384,079 | 385,202 | 420,119 | 359,459 | |||||||||||||||||

Total Assets | $41,484,998 | $39,215,217 | $35,956,057 | $36,680,546 | $36,369,560 | |||||||||||||||||

Liabilities and Equity | ||||||||||||||||||||||

Global unsecured revolving credit facilities | $2,150,451 | $2,255,139 | $1,440,040 | $943,325 | $398,172 | |||||||||||||||||

Unsecured term loans | 797,449 | 729,976 | — | — | — | |||||||||||||||||

Unsecured senior notes, net of discount | 13,120,033 | 12,281,410 | 12,695,568 | 13,284,650 | 12,903,370 | |||||||||||||||||

Secured debt and other, net of premiums | 528,870 | 491,984 | 158,699 | 160,240 | 146,668 | |||||||||||||||||

Operating lease liabilities | 1,471,044 | 1,363,712 | 1,418,540 | 1,472,510 | 1,512,187 | |||||||||||||||||

Accounts payable and other accrued liabilities | 1,868,884 | 1,621,406 | 1,619,222 | 1,572,359 | 1,543,623 | |||||||||||||||||

Deferred tax liabilities, net | 1,192,752 | 1,145,097 | 611,582 | 649,112 | 666,451 | |||||||||||||||||

Accrued dividends and distributions | 363,716 | — | — | — | 338,729 | |||||||||||||||||

Security deposits and prepaid rent | 369,654 | 341,552 | 341,140 | 346,911 | 336,578 | |||||||||||||||||

Total Liabilities | $21,862,853 | $20,230,276 | $18,284,791 | $18,429,107 | $17,845,778 | |||||||||||||||||

Redeemable non-controlling interests - operating partnership | 1,514,680 | 1,429,920 | 41,047 | 42,734 | 46,995 | |||||||||||||||||

Equity | ||||||||||||||||||||||

Preferred Stock: $0.01 par value per share, 110,000,000 shares authorized: | ||||||||||||||||||||||

Series J Cumulative Redeemable Preferred Stock (2) | $193,540 | $193,540 | $193,540 | $193,540 | $193,540 | |||||||||||||||||

Series K Cumulative Redeemable Preferred Stock (3) | 203,264 | 203,264 | 203,264 | 203,264 | 203,264 | |||||||||||||||||

Series L Cumulative Redeemable Preferred Stock (4) | 334,886 | 334,886 | 334,886 | 334,886 | 334,886 | |||||||||||||||||

Common Stock: $0.01 par value per share, 392,000,000 shares authorized (5) | 2,887 | 2,851 | 2,824 | 2,824 | 2,824 | |||||||||||||||||

Additional paid-in capital | 22,142,868 | 21,528,384 | 21,091,364 | 21,069,391 | 21,075,863 | |||||||||||||||||

Dividends in excess of earnings | (4,698,313) | (4,336,201) | (4,211,685) | (3,916,854) | (3,631,929) | |||||||||||||||||

Accumulated other comprehensive income (loss), net | (595,798) | (862,804) | (475,561) | (188,844) | (173,880) | |||||||||||||||||

Total Stockholders' Equity | $17,583,334 | $17,063,920 | $17,138,632 | $17,698,207 | $18,004,568 | |||||||||||||||||

Noncontrolling Interests | ||||||||||||||||||||||

Noncontrolling interest in operating partnership | $419,317 | $421,484 | $432,213 | $444,029 | $425,337 | |||||||||||||||||

Noncontrolling interest in consolidated joint ventures | 104,814 | 69,617 | 59,374 | 66,470 | 46,882 | |||||||||||||||||

Total Noncontrolling Interests | $524,131 | $491,101 | $491,587 | $510,499 | $472,219 | |||||||||||||||||

Total Equity | $18,107,465 | $17,555,021 | $17,630,219 | $18,208,706 | $18,476,787 | |||||||||||||||||

Total Liabilities and Equity | $41,484,998 | $39,215,217 | $35,956,057 | $36,680,546 | $36,369,560 | |||||||||||||||||

(1) | Net of allowance for doubtful accounts of $33,048 and $28,574 as of December 31, 2022 and December 31, 2021, respectively. |

(2) | Series J Cumulative Redeemable Preferred Stock, 5.250%, $200,000 and $200,000 liquidation preference, respectively ($25.00 per share), 8,000,000 and 8,000,000 shares issued and outstanding as of December 31, 2022 and December 31, 2021, respectively. |

(3) | Series K Cumulative Redeemable Preferred Stock, 5.850%, $210,000 and $210,000 liquidation preference, respectively ($25.00 per share), 8,400,000 and 8,400,000 shares issued and outstanding as of December 31, 2022 and December 31, 2021, respectively. |

(4) | Series L Cumulative Redeemable Preferred Stock, 5.200%, $345,000 and $345,000 liquidation preference, respectively ($25.00 per share), 13,800,000 and 13,800,000 shares issued and outstanding as of December 31, 2022 and December 31, 2021, respectively. |

(5) | Common Stock: 291,148,222 and 284,415,013 shares issued and outstanding as of December 31, 2022 and December 31, 2021, respectively. |

Reconciliation of Earnings Before Interest, Taxes, Depreciation & | |||||||||||||||||||

Amortization and Financial Ratios | Financial Supplement | ||||||||||||||||||

Unaudited and Dollars in Thousands | Fourth Quarter 2022 | ||||||||||||||||||

Three Months Ended | |||||||||||||||||||

Reconciliation of Earnings Before Interest, Taxes, Depreciation & Amortization (EBITDA) (1) | 31-Dec-22 | 30-Sep-22 | 30-Jun-22 | 31-Mar-22 | 31-Dec-21 | ||||||||||||||

Net (Loss) / Income Available to Common Stockholders | ($6,093) | $226,894 | $53,245 | $63,101 | $1,057,630 | ||||||||||||||

Interest | 86,882 | 76,502 | 69,023 | 66,725 | 71,762 | ||||||||||||||

Loss from early extinguishment of debt | — | — | — | 51,135 | 325 | ||||||||||||||

Income tax expense (benefit) | (17,676) | 19,576 | 16,406 | 13,244 | 3,961 | ||||||||||||||

Depreciation & amortization | 430,130 | 388,704 | 376,967 | 382,132 | 378,883 | ||||||||||||||

EBITDA | $493,244 | $711,676 | $515,642 | $576,337 | $1,512,561 | ||||||||||||||

Unconsolidated JV real estate related depreciation & amortization | 33,927 | 30,831 | 29,023 | 29,319 | 24,146 | ||||||||||||||

Unconsolidated JV interest expense and tax expense | 53,481 | 11,948 | 6,708 | 21,111 | 15,222 | ||||||||||||||

Severance, equity acceleration, and legal expenses | 15,980 | 1,655 | 3,786 | 2,077 | 1,003 | ||||||||||||||

Transaction and integration expenses | 17,350 | 25,862 | 13,586 | 11,968 | 12,427 | ||||||||||||||

(Gain) / loss on sale of investments | 6 | (173,990) | — | (2,770) | (1,047,011) | ||||||||||||||

Impairment of investments in real estate | 3,000 | — | — | — | 18,291 | ||||||||||||||

Other non-core adjustments, net | 15,127 | (94) | 31,633 | (48,858) | 14,307 | ||||||||||||||

Non-controlling interests | (3,326) | 1,716 | 436 | 3,629 | 22,587 | ||||||||||||||

Preferred stock dividends, including undeclared dividends | 10,181 | 10,181 | 10,181 | 10,181 | 10,181 | ||||||||||||||

(Gain on) / Issuance costs associated with redeemed preferred stock | — | — | — | — | — | ||||||||||||||

Adjusted EBITDA | $638,969 | $619,786 | $610,994 | $602,994 | $583,713 | ||||||||||||||

(1) For definitions and discussion of EBITDA and Adjusted EBITDA, see the definitions section. | |||||||||||||||||||

Three Months Ended | |||||||||||||||||||

Financial Ratios | 31-Dec-22 | 30-Sep-22 | 30-Jun-22 | 31-Mar-22 | 31-Dec-21 | ||||||||||||||

Total GAAP interest expense | $86,882 | $76,502 | $69,023 | $66,725 | $71,762 | ||||||||||||||

Capitalized interest | 24,581 | 17,304 | 14,131 | 14,751 | 15,328 | ||||||||||||||

Change in accrued interest and other non-cash amounts | (67,909) | 31,860 | (43,952) | 52,324 | (37,974) | ||||||||||||||

Cash Interest Expense (2) | $43,554 | $125,666 | $39,202 | $133,800 | $49,116 | ||||||||||||||

Preferred dividends | 10,181 | 10,181 | 10,181 | 10,181 | 10,181 | ||||||||||||||

Total Fixed Charges (3) | $121,644 | $103,987 | $93,335 | $91,657 | $97,271 | ||||||||||||||

Coverage | |||||||||||||||||||

Interest coverage ratio (4) | 5.3x | 6.1x | 6.6x | 6.1x | 6.0x | ||||||||||||||

Cash interest coverage ratio (5) | 11.9x | 4.6x | 12.6x | 4.0x | 9.8x | ||||||||||||||

Fixed charge coverage ratio (6) | 4.9x | 5.5x | 6.0x | 5.5x | 5.4x | ||||||||||||||

Cash fixed charge coverage ratio (7) | 10.0x | 4.3x | 10.4x | 3.7x | 8.3x | ||||||||||||||

Leverage | |||||||||||||||||||

Debt to total enterprise value (8) (9) | 35.2 % | 34.5 % | 27.1 % | 25.5 % | 20.5 % | ||||||||||||||

Debt plus preferred stock to total enterprise value (10) | 36.8 % | 36.2 % | 28.5 % | 26.8 % | 21.7 % | ||||||||||||||

Pre-tax income to interest expense (11) | 1.0x | 4.1x | 1.9x | 2.2x | 16.2x | ||||||||||||||

Net Debt to Adjusted EBITDA (12) | 6.9x | 6.7x | 6.2x | 6.3x | 6.1x | ||||||||||||||

(2) | Cash interest expense is interest expense less amortization of debt discount and deferred financing fees and includes interest that we capitalized. We consider cash interest expense to be a useful measure of interest as it excludes non-cash based interest expense. |

(3) | Fixed charges consist of GAAP interest expense, capitalized interest, and preferred dividends. |

(4) | Adjusted EBITDA divided by GAAP interest expense plus capitalized interest (including our pro rata share of unconsolidated joint venture interest expense). |

(5) | Adjusted EBITDA divided by cash interest expense (including our pro rata share of unconsolidated joint venture interest expense). |

(6) | Adjusted EBITDA divided by fixed charges (including our pro rata share of unconsolidated joint venture fixed charges). |

(7) | Adjusted EBITDA divided by the sum of cash interest expense, and preferred dividends (including our pro rata share of unconsolidated joint venture cash fixed charges). |

(8) | Mortgage debt and other loans divided by market value of common equity plus debt plus preferred stock. |

(9) | Total enterprise value defined as market value of common equity plus debt plus preferred stock. |

(10) | Same as (8), except numerator includes preferred stock. |

(11) | Calculated as net income plus interest expense divided by GAAP interest expense. |

(12) | Calculated as total debt at balance sheet carrying value, plus capital lease obligations, plus Digital Realty's pro rata share of unconsolidated joint venture debt, less cash and cash equivalents (including Digital Realty's pro rata share of unconsolidated joint venture cash) divided by the product of Adjusted EBITDA (including Digital Realty's pro rata share of unconsolidated joint venture EBITDA), multiplied by four. |

Definitions

Funds From Operations (FFO):

We calculate funds from operations, or FFO, in accordance with the standards established by the National Association of Real Estate Investment Trusts, or Nareit, in the Nareit Funds From Operations White Paper - 2018 Restatement. FFO represents net income (loss) (computed in accordance with GAAP), excluding gains (or losses) from real estate transactions, impairment of investment in real estate, real estate related depreciation and amortization (excluding amortization of deferred financing costs), unconsolidated JV real estate related depreciation & amortization, non-controlling interests in operating partnership and after adjustments for unconsolidated partnerships and joint ventures. Management uses FFO as a supplemental performance measure because, in excluding real estate related depreciation and amortization and gains and losses from property dispositions and after adjustments for unconsolidated partnerships and joint ventures, it provides a performance measure that, when compared year over year, captures trends in occupancy rates, rental rates and operating costs. We also believe that, as a widely recognized measure of the performance of REITs, FFO will be used by investors as a basis to compare our operating performance with that of other REITs. However, because FFO excludes depreciation and amortization and captures neither the changes in the value of our data centers that result from use or market conditions, nor the level of capital expenditures and capitalized leasing commissions necessary to maintain the operating performance of our data centers, all of which have real economic effect and could materially impact our financial condition and results from operations, the utility of FFO as a measure of our performance is limited. Other REITs may not calculate FFO in accordance with the NAREIT definition and, accordingly, our FFO may not be comparable to other REITs' FFO. FFO should be considered only as a supplement to net income computed in accordance with GAAP as a measure of our performance.

Core Funds from Operations (Core FFO):

We present core funds from operations, or Core FFO, as a supplemental operating measure because, in excluding certain items that do not reflect core revenue or expense streams, it provides a performance measure that, when compared year over year, captures trends in our core business operating performance. We calculate Core FFO by adding to or subtracting from FFO (i) other non-core revenue adjustments, (ii) transaction and integration expenses, (iii) loss from early extinguishment of debt, (iv) gain on / issuance costs associated with redeemed preferred stock, (v) severance, equity acceleration, and legal expenses, (vi) gain/loss on FX revaluation, and (vii) other non-core expense adjustments. Because certain of these adjustments have a real economic impact on our financial condition and results from operations, the utility of Core FFO as a measure of our performance is limited. Other REITs may calculate Core FFO differently than we do and accordingly, our Core FFO may not be comparable to other REITs' Core FFO. Core FFO should be considered only as a supplement to net income computed in accordance with GAAP as a measure of our performance.

Adjusted Funds from Operations (AFFO):

We present adjusted funds from operations, or AFFO, as a supplemental operating measure because, when compared year over year, it assesses our ability to fund dividend and distribution requirements from our operating activities. We also believe that, as a widely recognized measure of the operations of REITs, AFFO will be used by investors as a basis to assess our ability to fund dividend payments in comparison to other REITs, including on a per share and unit basis. We calculate AFFO by adding to or subtracting from Core FFO (i) non-real estate depreciation, (ii) amortization of deferred financing costs, (iii) amortization of debt discount/premium, (iv) non-cash stock-based compensation expense, (v) straight-line rental revenue, (vi) straight-line rental expense, (vii) above- and below-market rent amortization, (viii) deferred tax expense / (benefit), (ix) leasing compensation and internal lease commissions, and (x) recurring capital expenditures. Other REITs may calculate AFFO differently than we do and, accordingly, our AFFO may not be comparable to other REITs' AFFO. AFFO should be considered only as a supplement to net income computed in accordance with GAAP as a measure of our performance.

EBITDA and Adjusted EBITDA:

We believe that earnings before interest, loss from early extinguishment of debt, income taxes, and depreciation and amortization, or EBITDA, and Adjusted EBITDA (as defined below), are useful supplemental performance measures because they allow investors to view our performance without the impact of non-cash depreciation and amortization or the cost of debt and, with respect to Adjusted EBITDA, unconsolidated joint venture real estate related depreciation & amortization, unconsolidated joint venture interest expense and tax, severance, equity acceleration, and legal expenses, transaction and integration expenses, gain on sale / deconsolidation, impairment of investments in real estate, other non-core adjustments, net, non-controlling interests, preferred stock dividends, including undeclared dividends, and issuance costs associated with redeemed preferred stock. Adjusted EBITDA is EBITDA excluding unconsolidated joint venture real estate related depreciation & amortization, unconsolidated joint venture interest expense and tax, severance, equity acceleration, and legal expenses, transaction and integration expenses, gain on sale / deconsolidation, impairment of investments in real estate, other non-core adjustments, net, non-controlling interests, preferred stock dividends, including undeclared dividends, and gain on / issuance costs associated with redeemed preferred stock. In addition, we believe EBITDA and Adjusted EBITDA are frequently used by securities analysts, investors and other interested parties in the evaluation of REITs. Because EBITDA and Adjusted EBITDA are calculated before recurring cash charges including interest expense and income taxes, exclude capitalized costs, such as leasing commissions, and are not adjusted for capital expenditures or other recurring cash requirements of our business, their utility as a measure of our performance is limited. Other REITs may calculate EBITDA and Adjusted EBITDA differently than we do and, accordingly, our EBITDA and Adjusted EBITDA may not be comparable to other REITs' EBITDA and Adjusted EBITDA. Accordingly, EBITDA and Adjusted EBITDA should be considered only as supplements to net income computed in accordance with GAAP as a measure of our financial performance.

Net Operating Income (NOI) and Cash NOI:

Net operating income, or NOI, represents rental revenue, tenant reimbursement revenue and interconnection revenue less utilities expense, rental property operating expenses, property taxes and insurance expenses (as reflected in the statement of operations). NOI is commonly used by stockholders, company management and industry analysts as a measurement of operating performance of the company's rental portfolio. Cash NOI is NOI less straight-line rents and above- and below-market rent amortization. Cash NOI is commonly used by stockholders, company management and industry analysts as a measure of property operating performance on a cash basis. However, because NOI and cash NOI exclude depreciation and amortization and capture neither the changes in the value of our data centers that result from use or market conditions, nor the level of capital expenditures and capitalized leasing commissions necessary to maintain the operating performance of our data centers, all of which have real economic effect and could materially impact our results from operations, the utility of NOI and cash NOI as measures of our performance is limited. Other REITs may calculate NOI and cash NOI differently than we do and, accordingly, our NOI and cash NOI may not be comparable to other REITs' NOI and cash NOI. NOI and cash NOI should be considered only as supplements to net income computed in accordance with GAAP as measures of our performance.

Additional Definitions

Net debt-to-Adjusted EBITDA ratio is calculated as total debt at balance sheet carrying value, plus capital lease obligations, plus Digital Realty's pro rata share of unconsolidated joint venture debt, less cash and cash equivalents (including Digital Realty's pro rata share of unconsolidated joint venture cash) divided by the product of Adjusted EBITDA (including Digital Realty's pro rata share of unconsolidated joint venture EBITDA), multiplied by four.

Debt-plus-preferred-to-total enterprise value is mortgage debt and other loans plus preferred stock divided by mortgage debt and other loans plus the liquidation value of preferred stock and the market value of outstanding Digital Realty Trust, Inc. common stock and Digital Realty Trust, L.P. units, assuming the redemption of Digital Realty Trust, L.P. units for shares of Digital Realty Trust, Inc. common stock.

Fixed charge coverage ratio is Adjusted EBITDA divided by the sum of GAAP interest expense, capitalized interest, scheduled debt principal payments and preferred dividends. For the quarter ended December 31, 2022, GAAP interest expense was $87 million, capitalized interest was $25 million and scheduled debt principal payments and preferred dividends was $10 million.

Reconciliation of Net Operating Income (NOI) | Three Months Ended | Twelve Months Ended | ||||||||||||||

(in thousands) | 31-Dec-22 | 30-Sep-22 | 31-Dec-21 | 31-Dec-22 | 31-Dec-21 | |||||||||||

Operating income | $120,981 | $157,381 | $131,498 | $589,969 | $694,009 | |||||||||||

Fee income | (7,508) | (6,169) | (4,133) | (24,506) | (13,442) | |||||||||||

Other income | (168) | (1,749) | (200) | (4,645) | (19,401) | |||||||||||

Depreciation and amortization | 430,130 | 388,704 | 378,883 | 1,577,933 | 1,486,632 | |||||||||||

General and administrative | 104,451 | 95,792 | 103,705 | 398,669 | 393,311 | |||||||||||

Severance, equity acceleration, and legal expenses | 15,980 | 1,655 | 1,003 | 23,498 | 7,343 | |||||||||||

Transaction expenses | 17,350 | 25,862 | 12,427 | 68,766 | 47,426 | |||||||||||

Other expenses | 3,615 | 1,096 | (1) | 12,438 | 2,550 | |||||||||||

Net Operating Income | $687,830 | $662,572 | $641,472 | $2,645,122 | $2,616,720 | |||||||||||

Cash Net Operating Income (Cash NOI) | ||||||||||||||||

Net Operating Income | $687,830 | $662,572 | $641,472 | $2,645,122 | $2,616,720 | |||||||||||

Straight-line rental revenue | (32,226) | (17,505) | (16,345) | (70,394) | (64,107) | |||||||||||

Straight-line rental expense | (680) | 2,499 | 5,453 | 2,857 | 27,050 | |||||||||||

Above- and below-market rent amortization | (762) | (465) | 910 | (696) | 6,069 | |||||||||||

Cash Net Operating Income | $654,163 | $647,101 | $631,490 | $2,576,887 | $2,585,732 | |||||||||||

Constant Currency CFFO Reconciliation | Three Months Ended | Twelve Months Ended | ||||||||||||||

(in thousands) | 31-Dec-22 | 30-Sep-22 | 31-Dec-21 | 31-Dec-22 | 31-Dec-21 | |||||||||||

Core FFO (1) | $487,638 | $486,525 | $1,959,444 | $1,893,590 | ||||||||||||

Core FFO impact of holding '21 Exchange Rates Constant (2) | 16,867 | — | 62,128 | — | ||||||||||||

Constant Currency Core FFO | $504,505 | $486,525 | $2,021,572 | $1,893,590 | ||||||||||||

Weighted-average shares and units outstanding - diluted | 295,519 | 290,893 | 292,528 | 289,912 | ||||||||||||

Constant Currency CFFO Per Share | $1.71 | $1.67 | $6.91 | $6.53 | ||||||||||||

1) | As reconciled to net income on page 13. |

2) | Adjustment calculated by holding currency translation rates for 2022 constant with average currency translation rates that were applicable to the same periods in 2021. |

This document contains forward-looking statements within the meaning of the federal securities laws, which are based on current expectations, forecasts and assumptions that involve risks and uncertainties that could cause actual outcomes and results to differ materially. Such forward-looking statements include statements relating to: our economic outlook, our expected investment and expansion activity, anticipated continued demand for our products and service, our liquidity, our joint ventures, supply and demand for data center and colocation space, our acquisition and disposition activity, pricing and net effective leasing economics, market dynamics and data center fundamentals, our strategic priorities, our product offerings, available inventory, rent from leases that have been signed but have not yet commenced and other contracted rent to be received in future periods, rental rates on future leases, lag between signing and commencement, cap rates and yields, investment activity, the company's FFO, Core FFO, constant currency Core FFO and net income, 2023 outlook and underlying assumptions, information related to trends, our strategy and plans, leasing expectations, weighted average lease terms, the exercise of lease extensions, lease expirations, debt maturities, annualized rent at expiration of leases, the effect new leases and increases in rental rates will have on our rental revenue, our credit ratings, construction and development activity and plans, projected construction costs, estimated yields on investment, expected occupancy, expected square footage and IT load capacity upon completion of development projects, backlog NOI, NAV components, and other forward-looking financial data. Such statements are based on management's beliefs and assumptions made based on information currently available to management. Such statements are subject to risks, uncertainties and assumptions and are not guarantees of future performance and may be affected by known and unknown risks, trends, uncertainties and factors that are beyond our control. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, estimated or projected. Some of the risks and uncertainties that may cause our actual results, performance or achievements to differ materially from those expressed or implied by forward-looking statements include, among others, the following:

- reduced demand for data centers or decreases in information technology spending;

- increased competition or available supply of data center space;

- decreased rental rates, increased operating costs or increased vacancy rates;

- the suitability of our data centers and data center infrastructure, delays or disruptions in connectivity or availability of power, or failures or breaches of our physical and information security infrastructure or services;

- our dependence upon significant customers, bankruptcy or insolvency of a major customer or a significant number of smaller customers, or defaults on or non-renewal of leases by customers;

- our ability to attract and retain customers;

- breaches of our obligations or restrictions under our contracts with our customers;

- our inability to successfully develop and lease new properties and development space, and delays or unexpected costs in development of properties;

- the impact of current global and local economic, credit and market conditions;

- our inability to retain data center space that we lease or sublease from third parties;

- global supply chain or procurement disruptions, or increased supply chain costs;

- information security and data privacy breaches;

- difficulty managing an international business and acquiring or operating properties in foreign jurisdictions and unfamiliar metropolitan areas;

- our failure to realize the intended benefits from, or disruptions to our plans and operations or unknown or contingent liabilities related to, our recent acquisitions;

- our failure to successfully integrate and operate acquired or developed properties or businesses;

- difficulties in identifying properties to acquire and completing acquisitions;

- risks related to joint venture investments, including as a result of our lack of control of such investments;

- risks associated with using debt to fund our business activities, including re-financing and interest rate risks, our failure to repay debt when due, adverse changes in our credit ratings or our breach of covenants or other terms contained in our loan facilities and agreements;

- our failure to obtain necessary debt and equity financing, and our dependence on external sources of capital;

- financial market fluctuations and changes in foreign currency exchange rates;

- adverse economic or real estate developments in our industry or the industry sectors that we sell to, including risks relating to decreasing real estate valuations and impairment charges and goodwill and other intangible asset impairment charges;

- our inability to manage our growth effectively;

- losses in excess of our insurance coverage;

- our inability to attract and retain talent;

- impact on our operations and on the operations of our customers, suppliers and business partners during a pandemic, such as COVID-19;

- environmental liabilities, risks related to natural disasters and our inability to achieve our sustainability goals;

- our inability to comply with rules and regulations applicable to our company;

- Digital Realty Trust, Inc.'s failure to maintain its status as a REIT for federal income tax purposes;

- Digital Realty Trust, L.P.'s failure to qualify as a partnership for federal income tax purposes;

- restrictions on our ability to engage in certain business activities;

- changes in local, state, federal and international laws and regulations, including related to taxation, real estate and zoning laws, and increases in real property tax rates; and

- the impact of any financial, accounting, legal or regulatory issues or litigation that may affect us.

The risks included here are not exhaustive, and additional factors could adversely affect our business and financial performance. Several additional material risks are discussed in our annual report on Form 10–K for the year ended December 31, 2021 and other filings with the U.S. Securities and Exchange Commission. Those risks continue to be relevant to our performance and financial condition. Moreover, we operate in a very competitive and rapidly changing environment. New risk factors emerge from time to time and it is not possible for management to predict all such risk factors, nor can it assess the impact of all such risk factors on the business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We expressly disclaim any responsibility to update forward-looking statements, whether as a result of new information, future events or otherwise. Digital Realty, Digital Realty Trust, the Digital Realty logo, Interxion, Turn-Key Flex, Powered Base Building, and PlatformDIGITAL, Data Gravity Index and Data Gravity Index DGx are registered trademarks and service marks of Digital Realty Trust, Inc. in the United States and/or other countries. All other names, trademarks and service marks are the property of their respective owners.

View original content to download multimedia:https://www.prnewswire.com/news-releases/digital-realty-reports-fourth-quarter-2022-results-301749346.html

SOURCE Digital Realty

Uncategorized

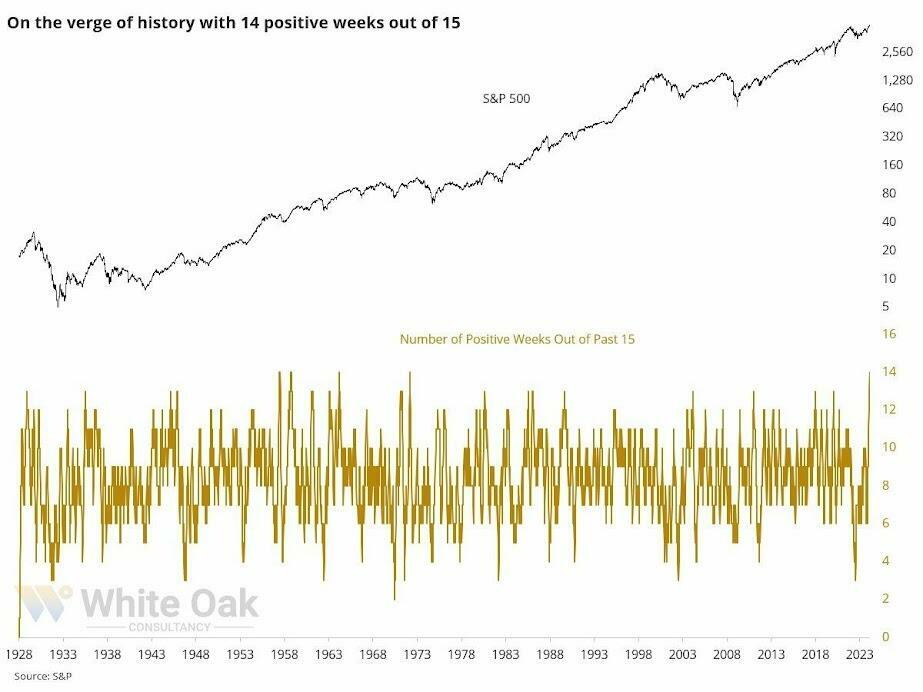

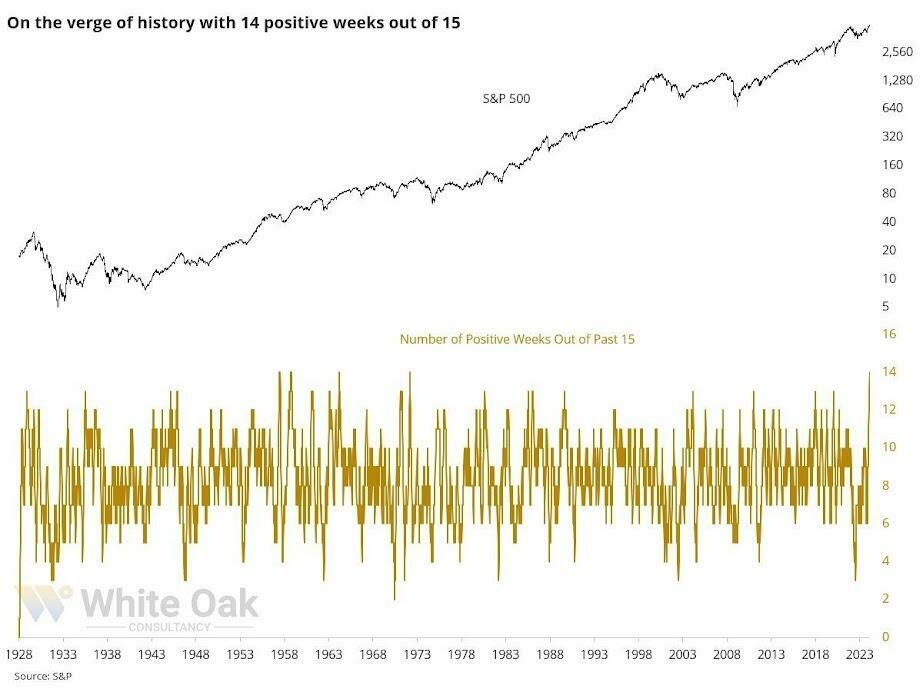

Stock indexes are breaking records and crossing milestones – making many investors feel wealthier

The S&P 500 topped 5,000 on Feb. 9, 2024, for the first time. The Dow Jones Industrial Average will probably hit a new big round number soon t…

Share this:

The S&P 500 stock index topped 5,000 for the first time on Feb. 9, 2024, exciting some investors and garnering a flurry of media coverage. The Conversation asked Alexander Kurov, a financial markets scholar, to explain what stock indexes are and to say whether this kind of milestone is a big deal or not.

What are stock indexes?

Stock indexes measure the performance of a group of stocks. When prices rise or fall overall for the shares of those companies, so do stock indexes. The number of stocks in those baskets varies, as does the system for how this mix of shares gets updated.

The Dow Jones Industrial Average, also known as the Dow, includes shares in the 30 U.S. companies with the largest market capitalization – meaning the total value of all the stock belonging to shareholders. That list currently spans companies from Apple to Walt Disney Co.

The S&P 500 tracks shares in 500 of the largest U.S. publicly traded companies.

The Nasdaq composite tracks performance of more than 2,500 stocks listed on the Nasdaq stock exchange.

The DJIA, launched on May 26, 1896, is the oldest of these three popular indexes, and it was one of the first established.

Two enterprising journalists, Charles H. Dow and Edward Jones, had created a different index tied to the railroad industry a dozen years earlier. Most of the 12 stocks the DJIA originally included wouldn’t ring many bells today, such as Chicago Gas and National Lead. But one company that only got booted in 2018 had stayed on the list for 120 years: General Electric.

The S&P 500 index was introduced in 1957 because many investors wanted an option that was more representative of the overall U.S. stock market. The Nasdaq composite was launched in 1971.

You can buy shares in an index fund that mirrors a particular index. This approach can diversify your investments and make them less prone to big losses.

Index funds, which have only existed since Vanguard Group founder John Bogle launched the first one in 1976, now hold trillions of dollars .

Why are there so many?

There are hundreds of stock indexes in the world, but only about 50 major ones.

Most of them, including the Nasdaq composite and the S&P 500, are value-weighted. That means stocks with larger market values account for a larger share of the index’s performance.

In addition to these broad-based indexes, there are many less prominent ones. Many of those emphasize a niche by tracking stocks of companies in specific industries like energy or finance.

Do these milestones matter?

Stock prices move constantly in response to corporate, economic and political news, as well as changes in investor psychology. Because company profits will typically grow gradually over time, the market usually fluctuates in the short term, while increasing in value over the long term.

The DJIA first reached 1,000 in November 1972, and it crossed the 10,000 mark on March 29, 1999. On Jan. 22, 2024, it surpassed 38,000 for the first time. Investors and the media will treat the new record set when it gets to another round number – 40,000 – as a milestone.

The S&P 500 index had never hit 5,000 before. But it had already been breaking records for several weeks.

Because there’s a lot of randomness in financial markets, the significance of round-number milestones is mostly psychological. There is no evidence they portend any further gains.

For example, the Nasdaq composite first hit 5,000 on March 10, 2000, at the end of the dot-com bubble.

The index then plunged by almost 80% by October 2002. It took 15 years – until March 3, 2015 – for it return to 5,000.

By mid-February 2024, the Nasdaq composite was nearing its prior record high of 16,057 set on Nov. 19, 2021.

Index milestones matter to the extent they pique investors’ attention and boost market sentiment.

Investors afflicted with a fear of missing out may then invest more in stocks, pushing stock prices to new highs. Chasing after stock trends may destabilize markets by moving prices away from their underlying values.

When a stock index passes a new milestone, investors become more aware of their growing portfolios. Feeling richer can lead them to spend more.

This is called the wealth effect. Many economists believe that the consumption boost that arises in response to a buoyant stock market can make the economy stronger.

Is there a best stock index to follow?

Not really. They all measure somewhat different things and have their own quirks.

For example, the S&P 500 tracks many different industries. However, because it is value-weighted, it’s heavily influenced by only seven stocks with very large market values.

Known as the “Magnificent Seven,” shares in Amazon, Apple, Alphabet, Meta, Microsoft, Nvidia and Tesla now account for over one-fourth of the S&P 500’s value. Nearly all are in the tech sector, and they played a big role in pushing the S&P across the 5,000 mark.

This makes the index more concentrated on a single sector than it appears.

But if you check out several stock indexes rather than just one, you’ll get a good sense of how the market is doing. If they’re all rising quickly or breaking records, that’s a clear sign that the market as a whole is gaining.

Sometimes the smartest thing is to not pay too much attention to any of them.

For example, after hitting record highs on Feb. 19, 2020, the S&P 500 plunged by 34% in just 23 trading days due to concerns about what COVID-19 would do to the economy. But the market rebounded, with stock indexes hitting new milestones and notching new highs by the end of that year.

Panicking in response to short-term market swings would have made investors more likely to sell off their investments in too big a hurry – a move they might have later regretted. This is why I believe advice from the immensely successful investor and fan of stock index funds Warren Buffett is worth heeding.

Buffett, whose stock-selecting prowess has made him one of the world’s 10 richest people, likes to say “Don’t watch the market closely.”

If you’re reading this because stock prices are falling and you’re wondering if you should be worried about that, consider something else Buffett has said: “The light can at any time go from green to red without pausing at yellow.”

And the opposite is true as well.

Alexander Kurov does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

dow jones sp 500 nasdaq stocks covid-19Uncategorized

Marriage is not as effective an anti-poverty strategy as you’ve been led to believe

Marriage on its own won’t do away with child poverty, and in fact it can create even more instability for low-income families.

Share this:

Brides.com predicts that 2024 will be the “year of the proposal” as engagements tick back up after a pandemic-driven slowdown.

Meanwhile, support for marriage has found new grist in recent books, including sociologist Brad Wilcox’s “Get Married: Why Americans Must Defy the Elites, Forge Strong Families and Save Civilization” and economist Melissa Kearney’s “The Two-Parent Privilege.”

Kearney’s book was hailed by economist Tyler Cowen as possibly “the most important economics and policy book of this year.” This is not because it treads new ground but because, as author Kay Hymowitz writes, it breaks the supposed “taboo about an honest accounting of family decline.”

These developments are good news for the marriage promotion movement, which for decades has claimed that marriage supports children’s well-being and combats poverty. The movement dates back at least to the U.S. Department of Labor’s Moynihan Report of 1965, which argued that family structure aggravated Black poverty.

Forty years after the Moynihan Report, George W. Bush-era programs such as the Healthy Marriage Initiative sought to enlist churches and other community groups in an effort to channel childbearing back into marriage. These initiatives continue today, with the federally subsidized Healthy Marriage and Responsible Fatherhood programs.

Still, nearly 30% of U.S. children live in single-parent homes today, compared with 10% in 1965.

We are law professors who have written extensively about family structure and poverty. We, and others, have found that there is almost no evidence that federal programs that promote marriage have made a difference in encouraging two-parent households. That’s in large part because they forgo effective solutions that directly address poverty for measures that embrace the culture wars.

Marriage and social class

Today’s marriage promoters claim that marriage should not be just for elites. The emergence of marriage as a marker of class, they believe, is a sign of societal dysfunction.

According to census data released in 2021, 9.5% of children living with two parents – and 7.5% with married parents – lived below the poverty level, compared with 31.7% of children living with a single parent.

Kearney’s argument comes down to: 1 + 1 = 2. Two parents have more resources, including money and time to spend with children, than one. She marshals extensive research designed to show that children from married couple families are more likely to graduate from high school, complete college and earn higher incomes as adults than the children of single parents.

It is undoubtedly true that two parents – that is, two nonviolent parents with reliable incomes and cooperative behavior – have more resources for their children than one parent who has to work two jobs to pay the rent. However, this equation does not address causation. In other words, parents who have stable incomes and behaviors are more likely to stay together than parents who don’t.

Ethnographic studies indicate, for example, that the most common reasons unmarried women are no longer with the fathers of their children are the men’s violent behavior, infidelity and substance abuse.

Moreover, income volatility disproportionately affects parents who don’t go to college. So while they may have more money to invest in children together than apart, when one of these parents experiences a substantial drop in income, the other parent may have to decide whether to support the partner or the children on what is often a meager income.

The impact of having single parents also plays out differently by race and class. As sociologist and researcher Christina Cross explains, “Living apart from a biological parent does not carry the same cost for Black youths as for their white peers, and being raised in a two-parent family is not equally beneficial.”

For example, Cross found that living in a single-mother family is less likely to affect high school completion rates for Black children than for white children. Also, Black families tend to be more embedded in extended family than white families, and this additional support system may help protect children from negative outcomes associated with single-parent households.

Making men more ‘marriageable’

Kearney, to her credit, does note that economic insecurity largely explains what is happening to working-class families, and that no parent should have to tolerate violence or substance abuse. But she doubles down on the need to restore a norm of two-parent families.

Many of her policy prescriptions are sensible. She advocates for better opportunities for low-income men – to make them, in the words of sociologist William Julius Wilson, “marriageable.” Such policies would include wage subsidies to improve their job opportunities, investment in community colleges that provide skills training, and the removal of questions about criminal histories from job applications, so that candidates who have previously been incarcerated are not immediately disqualified.

A new marriage model

What marriage promotion efforts overlook, however, are the underlying changes in what marriage has become – both legally and practically.

The new marriage model rests on three premises.

The first is a moral command: Have sex if you want to, but don’t have children until you are ready. While the shotgun marriage once served as the primary response to unplanned pregnancy, such marriages today often derail education and careers and are more likely to result in divorce than other marriages. Research shows that lower-income women’s pregnancies are much more likely to be unplanned.

The second is the ability to pick a partner who will support you and assume joint responsibility for parenting. As women have attained more economic independence, they are less in need of men to raise children, particularly if their partners are insensitive or abusive. With healthy relationships, couples pick partners based on trust, commitment and equal respect. This is more difficult to do in communities with high rates of incarceration and few opportunities for stable employment.

And the third is economic and behavioral stability. Instability undermines even committed unions. Parents who wait until they find the right partner and have stable lives bring a lot more to parenting, whether they marry or not.

We believe that creating opportunities for low-income parents to reach this middle-class model is likely to be the most effective marriage promotion policy.

Economic support is key

In relationships that fall outside of these premises, 1 + 1 often becomes 1 + -1, which equals 0.

Being committed to a partner who can’t pay speeding tickets, runs up credit card bills, comes home drunk or can’t be relied on to pick up the children after school is not a recipe for success.

Economic principles suggest that businesses with more volatile income streams need a stronger capital base to withstand the downturns. Working-class couples who face economic insecurity see commitment as similarly misguided; without a capital base, a downturn for one partner can wipe out the other.

The Biden administration’s child tax credit expansion included in the American Rescue Plan Act of 2021 helped cut the child poverty rate – after accounting for government assistance – to a record low that year. It did more to address child poverty than marriage promotion efforts have ever done.

Researchers have described such income-support policies as the “ultimate multipurpose policy instrument.” They improve the economic circumstances of single-parent families and, in doing so, may also provide greater support for two-parent relationships.

Policymakers know how to solve child poverty – and these measures are far more effective than efforts to put two married parents in every household.

The authors do not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and have disclosed no relevant affiliations beyond their academic appointment.

subsidies pandemicUncategorized

Divergences And Other Technical Warnings

While the bulls remain entirely in control of the market narrative, divergences and other technical warnings suggest becoming more cautious may be prudent….

Share this:

While the bulls remain entirely in control of the market narrative, divergences and other technical warnings suggest becoming more cautious may be prudent.

In January 2020, we discussed why we were taking profits and reducing risk in our portfolios. At the time, the market was surging, and there was no reason for concern. However, just over a month later, the markets fell sharply as the “pandemic” set in. While there was no evidence at the time that such an event would occur, the markets were so exuberant that only a trigger was needed to spark a correction.

“When you sit down with your portfolio management team, and the first comment made is ‘this is nuts,’ it’s probably time to think about your overall portfolio risk. On Friday, that was how the investment committee both started and ended – ‘this is nuts.'” – January 11th, 2020.

As the S&P 500 index approaches another psychological milestone of 5000, we again see numerous warning signs emerging that suggest the risk of a correction is elevated. Does that mean a correction will ensue tomorrow? Of course not. As the old saying goes, “Markets can remain irrational longer than you can remain solvent.” However, just as in 2020, it took more than a month before the warnings became reality.