Uncategorized

Why you shouldn’t worry about ‘what comes next’

Lately, I’ve seen a number of media reports pondering if world economies – and equity markets – are headed for a soft, hard or no landing. To me,…

Share this:

Lately, I’ve seen a number of media reports pondering if world economies – and equity markets – are headed for a soft, hard or no landing. To me, this kind of talk is a bit of a distraction. Because, as a long-term investor, the objective is still the same: to buy quality companies at good prices.

For some time now, economists and commentators have predicted a recession in the U.S. and Australia. But so far, strong jobs and rising company profit margins have combined to help both countries avoid one.

It may yet be the case that inflation persists for so long central bankers will, in an effort to avoid inflation expectations becoming entrenched, be forced to raise rates wildly beyond current estimates and ultimately drive their respective economies into recession. But we aren’t there yet.

At the moment, we have inflation still high but falling, and economies growing. That’s a ‘disinflationary boom’, and in the past fifty years, disinflationary booms have fuelled good returns for innovative growth companies – precisely the companies many experts suggest are currently overpriced.

I remain convinced, however, that investors should not now be looking at aggregates nor become distracted by broad statements about whether ‘the market’ is expensive or not. We have just exited a period of heightened or ‘wild’ volatility and have now entered a period of ‘normal’ volatility, which will be accompanied by a return to fundamentals and value driving returns.

Companies that beat expectations will do well, and companies that disappoint will see selling impact their share prices. This is normal. Good news is good news, and bad news is bad news.

Richcession

A new phrase doing the rounds is Richcession, coined by Wall Street Journal journo Justin Lahart.

It could just be a fad. A typical recession hits the wallets of the poor and the middle class. The wealthy are merely ‘inconvenienced’. The current period of economic uncertainty however is characterised by the wealthy reacting most adversely or being the most adversely affected. It’s a period when the rich change their spending habits the most, and it’s being observed in the U.S.

Lower-income earners benefitted during the pandemic from government stimulus and personal cheques. Wage increases have also been won by lower-income workers thanks to a tight labour market.

But many wealthier IT workers (the average salary at Google is US$133,000) are losing their jobs thanks to massive layoffs. Elsewhere, salaries for the wealthy are flat, while falling property and equity prices are having a direct negative wealth effect.

By way of anecdotal evidence, Bentonville, Arkansas–based retailer Walmart recently reported its quarterly results and said it’s gaining market share through higher-income consumers trading down.

CEO Doug McMillon told analysts that more than half of the market share gains Walmart saw in the U.S. last quarter were from high-income shoppers and that its Sam’s Club stores captured a greater share of spending for both mid- and high-income shoppers.

“We’re gaining share across income cohorts, including at the higher end, which made up nearly half of the gains we saw in the U.S. again this quarter, and we’re also capturing a greater share of wallet at Sam’s Club in the U.S. with both mid- and higher-income shoppers.”

Net sales for Walmart U.S. came in 8.0 per cent higher year-over-year, or $113.7 billion for Q4 fiscal year 2023. The company saw “continued strong market share gains in grocery, including high-income households.”

December 2022 saw the largest sales volume in the retailer’s history. Compared to two years ago, same-store sales increased 13.9 per cent.

Another phrase: No landing

There’s buzz around another new phrase, and this time it’s the “no landing” scenario. It sounds like an updated version of the Goldilocks economy, describing economic conditions that are ‘just right’.

The chatter is that the U.S. avoids a recession, at least in 2023, and continues to grow, albeit anaemically thanks in no small part to a resilient labour market.

According to Bloomberg: “As U.S. inflation receded over the past few months, some economists warned that the situation might get sticky – the kind where inflation seems to retreat only to gum up the works again. Last week, that scenario seemed to arrive. While new data showed overall inflation still falling, if only slightly, for January, consumer prices rose again, potentially a sign of a feared persistence that could push the Fed to raise rates for longer. Still, the overall economy remains robust, with more blowout job numbers and resilient spending (and skyrocketing credit card debt). Though the Fed’s timeline for snuffing out high prices is hard to predict, one thing may seem a bit clearer: Corporate profits appear to have peaked after a two-year bonanza, with some businesses retrenching. And while market observers continue to debate whether the U.S. economy will manage a soft landing, enter a full downturn or maybe experience a series of “little recessions,” there may be a fourth option: the so-called “no landing” scenario. This pattern includes a strong economy, a muscular labor market—and inflation that won’t go away.”

So, thanks to considerably stronger-than-expected U.S. economic data, instead of a choice between a soft landing or a hard landing, an additional ‘no landing’ scenario has been thrown into the mix.

The outcomes for investors however haven’t really changed. First, if modest economic growth continues and inflation subsides, we’ll have a great environment for innovative growth stocks, which equals Goldilocks or ‘no landing’. If, however, growth continues and is accompanied by persistent or sticky inflation and employment remains robust, interest rate expectations will be recalibrated – by investors and central banks – and they will have to rise faster and higher than currently anticipated. In such a scenario, we should reasonably expect a bumpier road ahead, and the plane will have to land.

recession pandemic stimulus economic growth stocks fed recession stimulusUncategorized

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Today, in the Calculated Risk Real Estate Newsletter: Part 1: Current State of the Housing Market; Overview for mid-March 2024

A brief excerpt: This 2-part overview for mid-March provides a snapshot of the current housing market.

I always like to star…

Share this:

A brief excerpt:

This 2-part overview for mid-March provides a snapshot of the current housing market.There is much more in the article.

I always like to start with inventory, since inventory usually tells the tale!

...

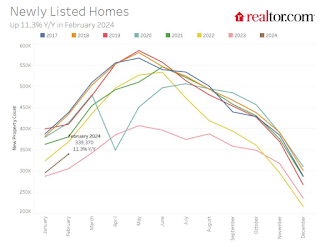

Here is a graph of new listing from Realtor.com’s February 2024 Monthly Housing Market Trends Report showing new listings were up 11.3% year-over-year in February. This is still well below pre-pandemic levels. From Realtor.com:

However, providing a boost to overall inventory, sellers turned out in higher numbers this February as newly listed homes were 11.3% above last year’s levels. This marked the fourth month of increasing listing activity after a 17-month streak of decline.Note the seasonality for new listings. December and January are seasonally the weakest months of the year for new listings, followed by February and November. New listings will be up year-over-year in 2024, but we will have to wait for the March and April data to see how close new listings are to normal levels.

There are always people that need to sell due to the so-called 3 D’s: Death, Divorce, and Disease. Also, in certain times, some homeowners will need to sell due to unemployment or excessive debt (neither is much of an issue right now).

And there are homeowners who want to sell for a number of reasons: upsizing (more babies), downsizing, moving for a new job, or moving to a nicer home or location (move-up buyers). It is some of the “want to sell” group that has been locked in with the golden handcuffs over the last couple of years, since it is financially difficult to move when your current mortgage rate is around 3%, and your new mortgage rate will be in the 6 1/2% to 7% range.

But time is a factor for this “want to sell” group, and eventually some of them will take the plunge. That is probably why we are seeing more new listings now.

Uncategorized

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45%…

Share this:

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45% of US respondents in 2023, according to the latest Harris Poll data. That’s exactly the same as the previous year.

Pharma’s highest point was in February 2021 — as Covid vaccines began to roll out — with a 62% positive US perception, and helping the industry land at an average 55% positive sentiment at the end of the year in Harris’ 2021 annual assessment of industries. The pharma industry’s reputation hit its most recent low at 32% in 2019, but it had hovered around 30% for more than a decade prior.

“Pharma has sustained a lot of the gains, now basically one and half times higher than pre-Covid,” said Harris Poll managing director Rob Jekielek. “There is a question mark around how sustained it will be, but right now it feels like a new normal.”

The Harris survey spans 11 global markets and covers 13 industries. Pharma perception is even better abroad, with an average 58% of respondents notching favorable sentiments in 2023, just a slight slip from 60% in each of the two previous years.

Pharma’s solid global reputation puts it in the middle of the pack among international industries, ranking higher than government at 37% positive, insurance at 48%, financial services at 51% and health insurance at 52%. Pharma ranks just behind automotive (62%), manufacturing (63%) and consumer products (63%), although it lags behind leading industries like tech at 75% positive in the first spot, followed by grocery at 67%.

The bright spotlight on the pharma industry during Covid vaccine and drug development boosted its reputation, but Jekielek said there’s maybe an argument to be made that pharma is continuing to develop innovative drugs outside that spotlight.

“When you look at pharma reputation during Covid, you have clear sense of a very dynamic industry working very quickly and getting therapies and products to market. If you’re looking at things happening now, you could argue that pharma still probably doesn’t get enough credit for its advances, for example, in oncology treatments,” he said.

vaccine pandemic covid-19Uncategorized

Q4 Update: Delinquencies, Foreclosures and REO

Today, in the Calculated Risk Real Estate Newsletter: Q4 Update: Delinquencies, Foreclosures and REO

A brief excerpt: I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened followi…

Share this:

{kind=link}

A brief excerpt:

I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble). The two key reasons are mortgage lending has been solid, and most homeowners have substantial equity in their homes..There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ mortgage rates real estate mortgages pandemic interest rates

...

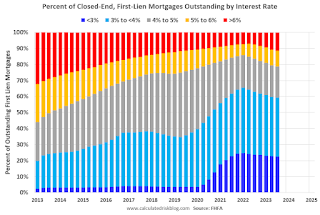

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023 (Q4 2023 data will be released in a two weeks).

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 22.6% of loans are under 3%, 59.4% are under 4%, and 78.7% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

{kind=link}

Q4 Update: Delinquencies, Foreclosures and REO

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Digital Currency And Gold As Speculative Warnings

Bougie Broke The Financial Reality Behind The Facade

‘Bougie Broke’ – The Financial Reality Behind The Facade

Bitcoin on Wheels: The Story of Bitcoinetas

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

The most potent labor market indicator of all is still strongly positive

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges