Uncategorized

VERSABANK REPORTS CONTINUED STRONG RESULTS FOR FIRST QUARTER 2023 HIGHLIGHTED BY 69% YEAR-OVER-YEAR GROWTH IN NET INCOME TO RECORD $9.4 MILLION

VERSABANK REPORTS CONTINUED STRONG RESULTS FOR FIRST QUARTER 2023 HIGHLIGHTED BY 69% YEAR-OVER-YEAR GROWTH IN NET INCOME TO RECORD $9.4 MILLION

PR Newswire

LONDON, ON, March 8, 2023

– Digital Banking Operations Realizing Significant Operating Leve…

Share this:

VERSABANK REPORTS CONTINUED STRONG RESULTS FOR FIRST QUARTER 2023 HIGHLIGHTED BY 69% YEAR-OVER-YEAR GROWTH IN NET INCOME TO RECORD $9.4 MILLION

PR Newswire

LONDON, ON, March 8, 2023

– Digital Banking Operations Realizing Significant Operating Leverage from Strong Loan Portfolio Growth as Transitory Costs for Growth Initiatives Substantially Dissipate –

All amounts are unaudited and in Canadian dollars and are based on financial statements prepared in compliance with International Accounting Standard 34 Interim Financial Reporting, unless otherwise noted. Our first quarter 2023 ("Q1 2023") unaudited Interim Consolidated Financial Statements for the period ended January 31, 2023 and Management's Discussion and Analysis ("MD&A"), are available online at www.versabank.com/investor-relations, SEDAR at www.sedar.com and EDGAR at www.sec.gov/edgar.shtml. Supplementary Financial Information will also be available on our website at www.versabank.com/investor-relations.

LONDON, ON, March 8, 2023 /PRNewswire/ - VersaBank ("VersaBank" or the "Bank") (TSX: VBNK; NASDAQ: VBNK), a North American leader in business-to-business digital banking, as well as technology solutions for cybersecurity, today reported its results for the first quarter of fiscal 2023 ended January 31, 2023. All figures are in Canadian dollars unless otherwise stated.

CONSOLIDATED AND SEGMENTED FINANCIAL SUMMARY

(unaudited) | As at or for the three months ended | ||||||||

January 31 | October 31 | January 31 | |||||||

(thousands of Canadian dollars except per share amounts) | 2023 | 2022 | Change | 2022 | Change | ||||

Financial results | |||||||||

Total revenue | $ 25,918 | $ 24,252 | 7 % | $ 18,266 | 42 % | ||||

Cost of funds(1) | 2.95 % | 2.45 % | 20 % | 1.29 % | 129 % | ||||

Net interest margin(1) | 2.83 % | 2.81 % | 1 % | 2.77 % | 2 % | ||||

Net interest margin on loans(1) | 3.03 % | 3.03 % | (0 %) | 3.23 % | (6 %) | ||||

Net income | 9,417 | 6,429 | 46 % | 5,566 | 69 % | ||||

Net income per common share basic and diluted | 0.34 | 0.23 | 48 % | 0.19 | 79 % | ||||

Balance sheet and capital ratios | |||||||||

Total assets | $ 3,531,690 | $ 3,265,998 | 8 % | $ 2,415,346 | 46 % | ||||

Book value per common share(1) | 12.77 | 12.37 | 3 % | 11.78 | 8 % | ||||

Common Equity Tier 1 (CET1) capital ratio | 11.19 % | 12.00 % | (7 %) | 14.83 % | (25 %) | ||||

Total capital ratio | 15.34 % | 16.52 % | (7 %) | 20.34 % | (25 %) | ||||

Leverage ratio | 9.21 % | 9.84 % | (6 %) | 12.69 % | (27 %) | ||||

(1) See definitions under 'Non-GAAP and Other Financial Measures' in the Q1 2023 Management's Discussion and Analysis. | |||||||||

(thousands of Canadian dollars) | |||||||||||||||

for the three months ended | January 31, 2023 | October 31, 2022 | January 31, 2022 | ||||||||||||

Digital | DRTC | Eliminations/ | Consolidated | Digital | DRTC | Eliminations/ | Consolidated | Digital | DRTC | Eliminations/ | Consolidated | ||||

Banking | Adjustments | Banking | Adjustments | Banking | Adjustments | ||||||||||

Net interest income | $ 24,274 | $ - | $ - | $ 24,274 | $ 22,477 | $ - | $ - | $ 22,477 | $ 16,885 | $ - | $ - | $ 16,885 | |||

Non-interest income | 2 | 1,833 | (191) | 1,644 | 38 | 1,778 | (41) | 1,775 | - | 1,422 | (41) | 1,381 | |||

Total revenue | 24,276 | 1,833 | (191) | 25,918 | 22,515 | 1,778 | (41) | 24,252 | 16,885 | 1,422 | (41) | 18,266 | |||

Provision for (recovery of) credit losses | 385 | - | - | 385 | 205 | - | - | 205 | 2 | - | - | 2 | |||

23,891 | 1,833 | (191) | 25,533 | 22,310 | 1,778 | (41) | 24,047 | 16,883 | 1,422 | (41) | 18,264 | ||||

Non-interest expenses: | |||||||||||||||

Salaries and benefits | 6,684 | 1,573 | - | 8,257 | 5,678 | 1,541 | - | 7,219 | 5,440 | 643 | - | 6,083 | |||

General and administrative | 2,862 | 455 | (191) | 3,126 | 5,154 | 457 | (41) | 5,570 | 3,482 | 183 | (41) | 3,624 | |||

Premises and equipment | 623 | 329 | - | 952 | 624 | 361 | - | 985 | 582 | 347 | - | 929 | |||

10,169 | 2,357 | (191) | 12,335 | 11,456 | 2,359 | (41) | 13,774 | 9,504 | 1,173 | (41) | 10,636 | ||||

Income (loss) before income taxes | 13,722 | (524) | - | 13,198 | 10,854 | (581) | - | 10,273 | 7,379 | 249 | - | 7,628 | |||

Income tax provision | 3,789 | (8) | - | 3,781 | 3,939 | (95) | - | 3,844 | 1,961 | 101 | - | 2,062 | |||

Net income (loss) | $ 9,933 | $ (516) | $ - | $ 9,417 | $ 6,915 | $ (486) | $ - | $ 6,429 | $ 5,418 | $ 148 | $ - | $ 5,566 | |||

Total assets | $ 3,522,279 | $ 23,797 | $ (14,386) | $ 3,531,690 | $ 3,267,479 | $ 22,345 | $ (23,826) | $ 3,265,998 | $ 2,412,167 | $ 23,767 | $ (20,588) | $ 2,415,346 | |||

Total liabilities | $ 3,174,197 | $ 27,751 | $ (21,435) | $ 3,180,513 | $ 2,912,249 | $ 25,755 | $ (22,681) | $ 2,915,323 | $ 2,072,691 | $ 25,147 | $ (19,443) | $ 2,078,395 | |||

HIGHLIGHTS FOR THE FIRST QUARTER OF FISCAL 2023

Consolidated

- Consolidated revenue increased 42% year-over-year and 7% sequentially to a record $25.9 million, driven by higher interest income resulting substantially from strong loan growth;

- Consolidated net income increased 69% year-over-year and 46% sequentially to a record1 $9.4 million as a function of higher net interest income attributable substantially to strong loan growth and modest NIM expansion. The sequential trend also reflected lower non-interest expenses;

- Consolidated earnings per share increased 79% year-over-year and 48% sequentially to $0.34 as a function of higher net income and the purchase and cancellation of VersaBank's common shares through its Normal Course Issuer Bid ("NCIB") for its common shares;

- Purchased and cancelled 822,296 common shares under its NCIB, bringing the total number purchased through the NCIB as at January 31, 2023 to 1,017,596; and,

- Completed submission of the requisite US regulatory filings to the OCC and Federal Reserve Bank of Minneapolis seeking approval of VersaBank's proposed acquisition of OCC-chartered US bank, Stearns Bank Holdingford. VersaBank anticipates receiving a decision with respect to approval of the proposed application from US regulators during the second calendar quarter of 2023 and, if favourable, will proceed to complete the acquisition as soon as possible, subject to Canadian regulatory (OSFI) approval.

(1) | Record net income excludes the first quarter 2017 which benefitted from the recognition of $8.8 million in deferred income tax assets derived from the tax loss carry-forwards assumed pursuant to the amalgamation of VersaBank with PWC Capital Inc. on January 31, 2017. |

Digital Banking Operations

- Loans increased 46% year-over-year and 8% sequentially to a record $3.24 billion, driven primarily by growth in the Bank's Point-of-Sale ("POS") Financing portfolio, which increased 68% year-over-year and 9% sequentially, as well as growth in the Bank's Commercial Real Estate ("CRE") portfolios, which increased 5% year-over-year and 6% sequentially;

- Revenue increased 44% year-over-year and 8% sequentially to a record $24.3 million due primarily to loan growth and redeployment of available cash into higher yielding, low risk securities, offset partially by higher interest expense attributable to higher deposit balances;

- Net interest margin increased 6 bps, or 2%, year-over-year and increased 2 bps, or 1%, sequentially to 2.83% as a function of higher yields earned on the Bank's lending and treasury assets attributable primarily to a higher interest rate environment resulting from the Bank of Canada tightening monetary policy over the course of the past year;

- Net interest margin on loans decreased 20 bps, or 6%, year-over-year and was unchanged sequentially, at 3.03%, due primarily to a shift in the Bank's funding mix and the Bank successfully executing on its strategy to grow its POS Financing portfolio, offset partially by higher yields earned on the Bank's lending portfolio due to higher interest rates;

- Provision for Credit Losses ("PCLs") as a percentage of average loans was 0.05%, compared with a 12-quarter average of 0.00%, which remains among the lowest of the publicly traded Canadian Schedule I (federally licensed) Banks; and,

- Efficiency ratio (excluding DRTC) improved 1,406 bps (or 25%) year-over-year and 877 bps (or 18%) sequentially to 42%.

DRTC (Cybersecurity Services and Banking and Financial Technology Development)

- Revenue for the Cybersecurity Services component of DRTC (Digital Boundary Group, or DBG) decreased 3% year-over-year to $2.3 million as a function of lower service work volume in the current quarter while gross profit increased 17% to $1.6 million as a function primarily of improved operational efficiency. Sequentially, revenue and gross profit for Digital Boundary Group decreased 19% and 6% respectively as a function of lower engagements in the first quarter of fiscal 2023. DBG's gross profit amounts are included in DRTC's consolidated revenue which is reflected in non-interest income in VersaBank's consolidated statements of income and comprehensive income. DBG remained profitable on a standalone basis within DRTC.

MANAGEMENT COMMENTARY

"Our record results for the first quarter, highlighted by 69% year-over-year growth in net income to $9.4 million, reflect the significant operating leveraging inherent in our value-added, branchless, digital banking model," said David Taylor, President and Chief Executive Officer, VersaBank. "Our loan portfolio grew 46% year-over-year and non-interest expense, as expected, trended to normalized levels following our strategic growth investments in fiscal 2022. As a result, our efficiency ratio improved substantially – more than 875 bps sequentially and more than 1,400 bps year-over-year – to 42%, and return on common equity improved 347 bps sequentially and 421 bps year-over-year to 10.79% – clear evidence of the true efficiency and earnings potential of our model at scale."

"Looking out to the remainder of fiscal 2023, we expect to see similar healthy sequential growth in our Canadian loan portfolio to that of the first quarter of this year, as consumer spending remains healthy in the sectors of the economy our Canadian Point of Sale business finances. Importantly, VersaBank was specifically designed to do well in good economic environments and even better in more challenging economic environments."

"We also look forward to the additional upside potential of the broad roll out of our Receivable Purchase Program in the U.S. Following submission of our requisite filings for our proposed U.S. bank acquisition, we remain optimistic with respect to near-term approval and continue to actively prepare for the significant opportunity to broadly offer our differentiated and attractive financing solution to U.S. partners, which is already proving successful in its limited roll out to date. As we continue to grow our loan portfolio on both sides of the border, and with non-interest expense returning to normalized levels in the near-term, we expect to continue to realize the full potential of the return on equity generation capability of our model."

"The cybersecurity segment within DRTC continues to be driven by our Digital Boundary Group operation, which was profitable in the current quarter and has been every quarter since being acquired by DRTC in late 2020. The market for DBG's critical cybersecurity services continues to rapidly expand as businesses and government entities are increasingly concerned about the likelihood of cybersecurity attacks. Recently, DBG added a major publicly traded, North American financial institution as a customer, further evidence of its leadership in the industry and the significant opportunity for growth."

Financial Review

Consolidated

Net Income – Net income for the first quarter of fiscal 2023 was $9.4 million, or $0.34 per common share (basic and diluted), compared with $6.4 million, or $0.23 per common share (basic and diluted) for the fourth quarter of fiscal 2022 and $5.6 million, or $0.19 per common share (basic and diluted), for the same period of fiscal 2022. The sequential and year-over-year increases were a function of higher revenue attributable primarily to lending asset growth, with the year-over-year trend reflecting a partial offset due to higher non-interest expense attributable to higher salary and benefits expense attributable to general, annual compensation adjustments and higher staffing levels to support expanded business activity across the Bank, as well as higher costs related to investments in the Bank's business development initiatives.

Digital Banking Operations

Net Interest Margin – Net interest margin (or spread) for the quarter increased to 2.83% from 2.81% for the first quarter of fiscal 2023 and 2.77% for the same period of fiscal 2022. The sequential and year-over-year increases were primarily the result of higher yields earned on the Bank's lending and treasury assets attributable to higher interest rates offset partially by higher cost of funds.

Net Interest Margin on Loans – Net interest margin on loans for the quarter remained unchanged sequentially, and decreased 20 bps, or 6%, year-over-year and to 3.03%, due primarily to a shift in the Bank's funding mix and the Bank successfully executing on its strategy to grow its POS Financing portfolio offset partially by higher yields earned on the Bank's lending portfolio due to higher interest rates.

Net Interest Income – Net interest income for the quarter increased to a record $24.3 million from $22.5 million for the fourth quarter of 2022 and $16.9 million for the same period of fiscal 2022. The sequential and year-over year increases were due primarily to higher interest income earned on a higher loan balances attributable to strong growth in both the Bank's POS Financing and CRE Mortgage portfolios, higher yields earned on floating-rate lending assets as a result of higher interest rates, and the redeployment of available cash into higher-yielding, low-risk securities offset partially by higher interest expense attributable to higher deposit balances.

Non-Interest Expenses – Non-interest expenses for the quarter were $12.3 million compared with $13.8 million for the fourth quarter of 2022 and $10.6 million for the same period of fiscal 2022. The sequential trend was a function primarily of lower costs attributable to investments in the Bank's business development initiatives including, but not limited to, the acquisition of a US national bank, the development of the US RPP and preparation for commercial launch of the Canadian-dollar version of VersaBank's Digital Deposit Receipts and lower capital tax expense, offset partially by higher salary and benefits expense attributable to general, annual compensation adjustments and higher staffing levels to support expanded business activity across the Bank . Notwithstanding the favourable sequential trend investments associated with the acquisition of the US bank are anticipated to continue over the first half of fiscal 2023 but will be substantially lower than the amounts invested over the course of fiscal 2022 and will be related primarily to the Bank ensuring that it is in compliance with all necessary US banking regulatory requirements. The year-over-year increase was a function primarily of higher salary and benefits expense attributable to higher staffing levels to support expanded business activity across VersaBank and higher costs associated with employee retention as well as higher costs related to investments in the Bank's business development initiatives, noted above, offset partially by lower insurance premiums attributable to VersaBank's listing on the Nasdaq in September 2021 and lower capital tax expense.

Provision for/Recovery of Credit Losses – Provision for credit losses for the quarter was $385,000 compared to a provision for credit losses of $205,000 for the fourth quarter of 2022 and a provision for credit losses of $2,000 for the same period of fiscal 2022. The sequential and year-over-year changes were a function primarily of changes in the forward-looking information used by the Bank in its credit risk models and higher lending asset balances.

Capital – At January 31, 2023, VersaBank's total regulatory capital was $447 million compared with $449 million at October 31, 2022 and $426 million at January 31, 2022. The Bank's total capital ratio at January 31, 2023 was 15.34%, compared 16.52% at October 31, 2022 and 20.34% at January 31, 2022. The sequential and year-over-year capital ratio trends were a function primarily of retained earnings growth, the purchase and cancellation of common shares through the Bank's NCIB and changes to the Bank's risk-weighted asset balances and composition over the same periods.

Credit Quality – Gross impaired loans at January 31, 2023 were $1.7 million, compared with $0.3 million last quarter and $nil a year ago. The Bank's allowance for expected credit losses, ("ECL") at January 31, 2023 was $2.3 million compared with $1.9 million last quarter and $1.5 million a year ago. The quarter-over-quarter and year-over-year changes were a function primarily of the factors set out in the Provision for/Recovery of Credit Losses section above. VersaBank's Provision for Credit Losses ratio continues to be one of the lowest in the Canadian banking industry, reflecting the very low risk profile of the Bank's lending portfolio, enabling it to generate superior net interest margins by offering innovative, high-value deposit and lending solutions that address unmet needs in the banking industry through a highly efficient partner model.

Lending Operations: POS Financing – POS Financing portfolio balances for the quarter increased 9% sequentially and 68% year-over-year to $2.4 billion as a function primarily of continued strong demand for home finance, home improvement/HVAC receivable financing, and auto financing. Consumer spending and business investment in Canada are expected to slow during the first half of 2023 due primarily to higher interest rates combined with higher inflation relative to recent historical levels. Notwithstanding these factors, given the continuing strength of the labour market management anticipates that consumers will continue to spend in the various sectors to which the Bank provides POS financing although at levels measurably lower than the outsized spending of 2022. This consumer behaviour, combined with the anticipated addition of new origination partners in Canada, is expected to contribute to continued meaningful growth in the Bank's POS Financing portfolio throughout fiscal 2023 that is more consistent with pre-fiscal 2022 levels.

U.S. Receivable Purchase Program - Despite higher interest rates, elevated inflation, higher gas prices and supply chain disruptions in the US continued momentum in the job market and higher wages are expected to mitigate material declines in consumer spending, which in turn will support stable demand for durable goods and agricultural products which is expected to continue to stimulate transportation and manufacturing equipment purchases. Additionally, despite a cooling of the residential home market in the US overall construction activity is expected to continue to expand modestly in fiscal 2023 which is anticipated to support demand for construction equipment in the near term. Management believes that the anticipated US macroeconomic and industry trends described above will support growth in the Bank's RPP portfolio in the US throughout fiscal 2023, which will be focused on the provision of commercial equipment financing over the course of the same period. The Bank's RPP launched in a limited manner in the second quarter of fiscal 2022 with a large, North American, commercial transportation financing business focused on independent owner/operators and added a second commercial equipment financing partner over the course of the first quarter of fiscal 2023.

Lending Operations: Commercial Lending – The Commercial Lending portfolio for the quarter increased 6% sequentially and 5% year-over-year to $807 million. Management anticipates modest growth in the commercial mortgage sector related to financing for residential housing properties, which is expected to result in healthy demand for the Bank's construction and term financing products for which the Bank is currently experiencing and expects to continue to experience high quality deal flow, throughout at least fiscal 2023. Notwithstanding the highly effective risk mitigation strategies that are employed in managing the Bank's CRE portfolios, including working with well-established, well-capitalized partners and maintaining modest loan-to-value ratios on individual transactions, management has taken a cautionary stance with respect to its broader CRE portfolios due to the anticipation of volatility in CRE asset valuations in a rising interest rate environment and the potential impact of same on borrowers' ability to service debt, as well as due to concerns related to inflation and higher input costs, which continue to have the potential to drive higher construction costs. Additionally, management anticipates more meaningful participation in the B-20 compliant conventional, uninsured mortgage financing space, however, does not expect this lending activity to impact the Bank's balance sheet until mid-fiscal 2023.

Deposit Funding – Cost of funds for the first quarter was 2.95%, an increase of 50 bps sequentially and 166 bps year-over-year attributable to a shift in the Bank's funding mix and a higher interest rate environment. Commercial deposits at January 31, 2023 were $586 million, down 2% year-over-year and down 2% sequentially. Personal deposits at January 31, 2023 were $2.3 billion, up 87% year-over-year and up 14% sequentially. Management expects that commercial deposit volumes raised via VersaBank's Trustee Integrated Banking ("TIB") program will return to growth in the second half of fiscal 2023 as a function of an increase in the volume of consumer and commercial bankruptcy and proposal restructuring proceedings over the same timeframe, attributable primarily to a more challenging current and forecasted economic environment as evidenced by increasing Canadian consumer bankruptcy filing volumes. Further, VersaBank continues to pursue a number of initiatives to grow and expand its well-established, diverse deposit broker network through which it sources personal deposits, consisting primarily of guaranteed investment certificates.

DRTC (Cybersecurity Services and Banking and Financial Technology Development)

DRTC revenue (including that from services provided to the Digital Banking operations) increased 3% sequentially to $1.8 million and 29% year-over-year, as a function primarily of higher gross profit from DBG. Notwithstanding this positive trend DRTC recorded a net loss of $516,000 compared to a net loss of $486,000 in the sequential quarter and net income of $148,000 a year ago. The sequential trend was function primarily of DRTC recognizing an income tax recovery in the comparative period related to tax adjustments in fiscal 2022, while the year-over-year trend was function primarily of higher non-interest expenses attributable to higher salary and benefits expense due to higher staffing levels to support expanded business activity and higher costs associated with employee retention amidst the current challenging labour market.

DBG revenue decreased 3% as a function of lower service work volume in the current quarter while gross profit increased 17% as a function primarily of improved operational efficiency achieved by DBG over the course of the year. DRTC's DBG services revenue and gross profit decreased 19% and 6% to $2.3 million and $1.6 million respectively as a function of lower engagements in the current quarter. DBG's gross profit amounts are included in DRTC's consolidated revenue which is reflected in non-interest income in VersaBank's consolidated statements of income and comprehensive income.

FINANCIAL HIGHLIGHTS

(unaudited) | For the three months ended | ||||||

January 31 | October 31 | January 31 | |||||

(thousands of Canadian dollars except per share amounts) | 2023 | 2022 | 2022 | ||||

Results of operations | |||||||

Interest income | $ 49,561 | $ 42,072 | $ 24,720 | ||||

Net interest income | 24,274 | 22,477 | 16,885 | ||||

Non-interest income | 1,644 | 1,775 | 1,381 | ||||

Total revenue | 25,918 | 24,252 | 18,266 | ||||

Provision (recovery) for credit losses | 385 | 205 | 2 | ||||

Non-interest expenses | 12,335 | 13,774 | 10,636 | ||||

Digital Banking | 10,169 | 11,456 | 9,504 | ||||

DRTC | 2,357 | 2,359 | 1,173 | ||||

Net income | 9,417 | 6,429 | 5,566 | ||||

Income per common share: | |||||||

Basic | $ 0.34 | $ 0.23 | $ 0.19 | ||||

Diluted | $ 0.34 | $ 0.23 | $ 0.19 | ||||

Dividends paid on preferred shares | $ 247 | $ 247 | $ 247 | ||||

Dividends paid on common shares | $ 663 | $ 680 | $ 687 | ||||

Yield* | 5.78 % | 5.26 % | 4.06 % | ||||

Cost of funds* | 2.95 % | 2.45 % | 1.29 % | ||||

Net interest margin* | 2.83 % | 2.81 % | 2.77 % | ||||

Net interest margin on loans* | 3.03 % | 3.03 % | 3.23 % | ||||

Return on average common equity* | 10.79 % | 7.32 % | 6.58 % | ||||

Book value per common share* | $ 12.77 | $ 12.37 | $ 11.78 | ||||

Efficiency ratio* | 48 % | 57 % | 58 % | ||||

Efficiency ratio - Digital banking* | 42 % | 51 % | 56 % | ||||

Return on average total assets* | 1.07 % | 0.77 % | 0.87 % | ||||

Gross impaired loans to total loans* | 0.05 % | 0.01 % | 0.00 % | ||||

Provision (recovery) for credit losses as a % of average loans* | 0.05 % | 0.03 % | 0.00 % | ||||

As at | |||||||

Balance Sheet Summary | |||||||

Cash | $ 201,372 | $ 88,581 | $ 155,239 | ||||

Securities | 49,847 | 141,564 | - | ||||

Loans, net of allowance for credit losses | 3,235,083 | 2,992,678 | 2,215,638 | ||||

Average loans | 3,113,881 | 2,903,400 | 2,159,344 | ||||

Total assets | 3,531,690 | 3,265,998 | 2,415,346 | ||||

Deposits | 2,925,452 | 2,657,540 | 1,847,003 | ||||

Subordinated notes payable | 102,765 | 104,951 | 97,726 | ||||

Shareholders' equity | 351,177 | 350,675 | 336,951 | ||||

Capital ratios** | |||||||

Risk-weighted assets | $ 2,917,048 | $ 2,714,902 | $ 2,095,335 | ||||

Common Equity Tier 1 capital | 326,411 | 325,657 | 310,825 | ||||

Total regulatory capital | 447,472 | 448,575 | 426,237 | ||||

Common Equity Tier 1 (CET1) capital ratio | 11.19 % | 12.00 % | 14.83 % | ||||

Tier 1 capital ratio | 11.66 % | 12.50 % | 15.49 % | ||||

Total capital ratio | 15.34 % | 16.52 % | 20.34 % | ||||

Leverage ratio | 9.21 % | 9.84 % | 12.69 % | ||||

* This is a non-GAAP measure. See definition under 'Non-GAAP and Other Financial Measures' in the | |||||||

Q1 2023 Management's Discussion and Analysis. | |||||||

** Capital management and leverage measures are in accordance with OSFI's Capital Adequacy Requirements | |||||||

and Basel III Accord. | |||||||

VersaBank is a Canadian Schedule I chartered (federally licensed) bank with a difference. VersaBank became the world's first fully digital financial institution when it adopted its highly efficient business-to-business model in 1993 using its proprietary state-of-the-art financial technology to profitably address underserved segments of the Canadian banking market in the pursuit of superior net interest margins while mitigating risk. VersaBank obtains all of its deposits and provides the majority of its loans and leases electronically, with innovative deposit and lending solutions for financial intermediaries that allow them to excel in their core businesses. In addition, leveraging its internally developed IT security software and capabilities, VersaBank established wholly owned, Washington, DC-based subsidiary, DRT Cyber Inc. to pursue significant large-market opportunities in cyber security and develop innovative solutions to address the rapidly growing volume of cyber threats challenging financial institutions, multi-national corporations and government entities on a daily basis.

VersaBank's Common Shares trade on the Toronto Stock Exchange ("TSX") and Nasdaq under the symbol VBNK. Its Series 1 Preferred Shares trade on the TSX under the symbol VBNK.PR.A.

VersaBank's public communications often include written or oral forward-looking statements. Statements of this type are included in this document and may be included in other filings and with Canadian securities regulators or the US Securities and Exchange Commission, or in other communications. All such statements are made pursuant to the "safe harbor" provisions of, and are intended to be forward-looking statements under, the United States Private Securities Litigation Reform Act of 1995 and any applicable Canadian securities legislation. The statements in this management's discussion and analysis that relate to the future are forward-looking statements. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, many of which are out of VersaBank's control. Risks exist that predictions, forecasts, projections, and other forward-looking statements will not be achieved. Readers are cautioned not to place undue reliance on these forward-looking statements as a number of important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include, but are not limited to, the strength of the Canadian and US economy in general and the strength of the local economies within Canada and the US in which VersaBank conducts operations; the effects of changes in monetary and fiscal policy, including changes in interest rate policies of the Bank of Canada and the US Federal Reserve; global commodity prices; the effects of competition in the markets in which VersaBank operates; inflation; capital market fluctuations; the timely development and introduction of new products in receptive markets; the impact of changes in the laws and regulations pertaining to financial services; changes in tax laws; technological changes; unexpected judicial or regulatory proceedings; unexpected changes in consumer spending and savings habits; the impact of wars or conflicts including the crisis in Ukraine and the impact of the crisis on global supply chains; the impact of potential new variants of COVID-19; the possible effects on our business of terrorist activities; natural disasters and disruptions to public infrastructure, such as transportation, communications, power or water supply; and VersaBank's anticipation of and success in managing the risks implicated by the foregoing. For a detailed discussion of certain key factors that may affect VersaBank's future results, please see VersaBank's annual MD&A for the year ended October 31, 2022.

The foregoing list of important factors is not exhaustive. When relying on forward-looking statements to make decisions, investors and others should carefully consider the foregoing factors and other uncertainties and potential events. The forward-looking information contained in the management's discussion and analysis is presented to assist VersaBank shareholders and others in understanding VersaBank's financial position and may not be appropriate for any other purposes. Except as required by securities law, VersaBank does not undertake to update any forward-looking statement that is contained in this management's discussion and analysis or made from time to time by VersaBank or on its behalf.

VersaBank will be hosting a conference call and webcast today, Wednesday, March 8, 2023, at 9:00 a.m. (EDT) to discuss its first quarter results, featuring a presentation by David Taylor, President & CEO, and other VersaBank executives, followed by a question and answer period.

Dial-in Details

Toll-free dial-in number: | 1 (888) 664-6392 (Canada/U.S.) |

Local dial-in number: | (416) 764-8659 |

Please call between 8:45 a.m. and 8:55 a.m. (EDT).

To join the conference call by telephone without operator assistance, you may register and enter your phone number in advance at https://bit.ly/3JKSPJv to receive an instant automated call back.

Webcast Access: For those preferring to listen to the conference call via the Internet, a webcast of Mr. Taylor's presentation will be available via the internet, accessible here https://app.webinar.net/x8GVZWDBk1P or from the Bank's web site.

Instant Replay

Toll-free dial-in number: | 1 (888) 390-0541 (Canada/U.S.) |

Local dial-in number: | (416) 764-8677 |

Passcode: | 158247# |

Expiry Date: | April 8th, 2023, at 11:59 p.m. (EDT) |

The archived webcast presentation will also be available via the Internet for 90 days following the live event at https://app.webinar.net/x8GVZWDBk1P and on the Bank's web site.

Visit our website at: www.versabank.com

Follow VersaBank on Facebook, Instagram, LinkedIn and Twitter

View original content to download multimedia:https://www.prnewswire.com/news-releases/versabank-reports-continued-strong-results-for-first-quarter-2023-highlighted-by-69-year-over-year-growth-in-net-income-to-record-9-4-million-301765146.html

SOURCE VersaBank

Uncategorized

Q4 Update: Delinquencies, Foreclosures and REO

Today, in the Calculated Risk Real Estate Newsletter: Q4 Update: Delinquencies, Foreclosures and REO

A brief excerpt: I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened followi…

Share this:

A brief excerpt:

I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble). The two key reasons are mortgage lending has been solid, and most homeowners have substantial equity in their homes..There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ mortgage rates real estate mortgages pandemic interest rates

...

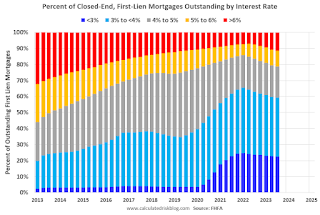

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023 (Q4 2023 data will be released in a two weeks).

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 22.6% of loans are under 3%, 59.4% are under 4%, and 78.7% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

Uncategorized

‘Bougie Broke’ – The Financial Reality Behind The Facade

‘Bougie Broke’ – The Financial Reality Behind The Facade

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Social media users claiming…

Share this:

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive restaurants. Yet they complain about living paycheck to paycheck and lacking the means to support their lifestyle.

Bougie broke is like “keeping up with the Joneses,” spending beyond one’s means to impress others.

Bougie Broke gives us a glimpse into the financial condition of a growing number of consumers. Since personal consumption represents about two-thirds of economic activity, it’s worth diving into the Bougie Broke fad to appreciate if a large subset of the population can continue to consume at current rates.

The Wealth Divide Disclaimer

Forecasting personal consumption is always tricky, but it has become even more challenging in the post-pandemic era. To appreciate why we share a joke told by Mike Green.

Bill Gates and I walk into the bar…

Bartender: “Wow… a couple of billionaires on average!”

Bill Gates, Jeff Bezos, Elon Musk, Mark Zuckerberg, and other billionaires make us all much richer, on average. Unfortunately, we can’t use the average to pay our bills.

According to Wikipedia, Bill Gates is one of 756 billionaires living in the United States. Many of these billionaires became much wealthier due to the pandemic as their investment fortunes proliferated.

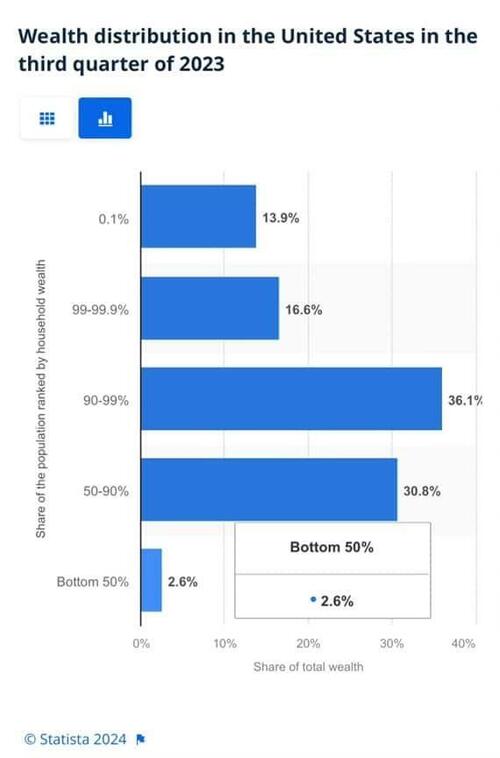

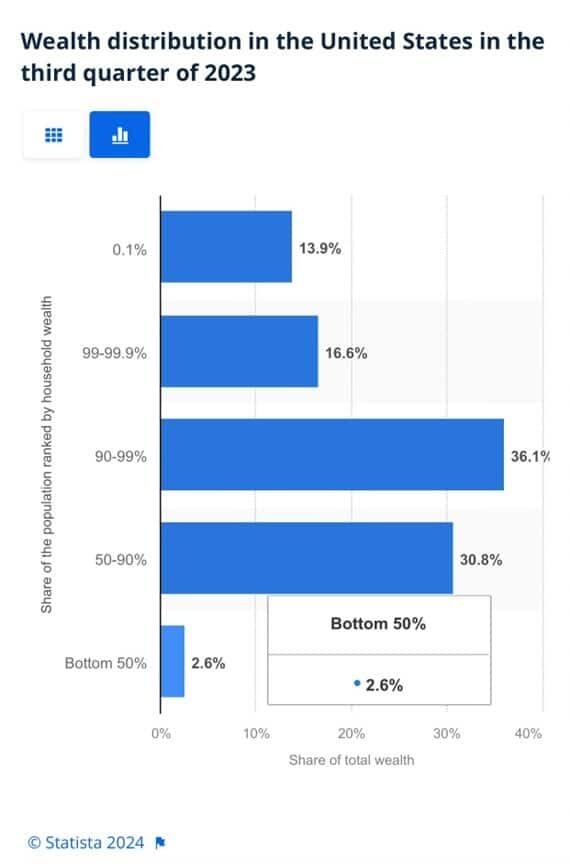

To appreciate the wealth divide, consider the graph below courtesy of Statista. 1% of the U.S. population holds 30% of the wealth. The wealthiest 10% of households have two-thirds of the wealth. The bottom half of the population accounts for less than 3% of the wealth.

The uber-wealthy grossly distorts consumption and savings data. And, with the sharp increase in their wealth over the past few years, the consumption and savings data are more distorted.

Furthermore, and critical to appreciate, the spending by the wealthy doesn’t fluctuate with the economy. Therefore, the spending of the lower wealth classes drives marginal changes in consumption. As such, the condition of the not-so-wealthy is most important for forecasting changes in consumption.

Revenge Spending

Deciphering personal data has also become more difficult because our spending habits have changed due to the pandemic.

A great example is revenge spending. Per the New York Times:

Ola Majekodunmi, the founder of All Things Money, a finance site for young adults, explained revenge spending as expenditures meant to make up for “lost time” after an event like the pandemic.

So, between the growing wealth divide and irregular spending habits, let’s quantify personal savings, debt usage, and real wages to appreciate better if Bougie Broke is a mass movement or a silly meme.

The Means To Consume

Savings, debt, and wages are the three primary sources that give consumers the ability to consume.

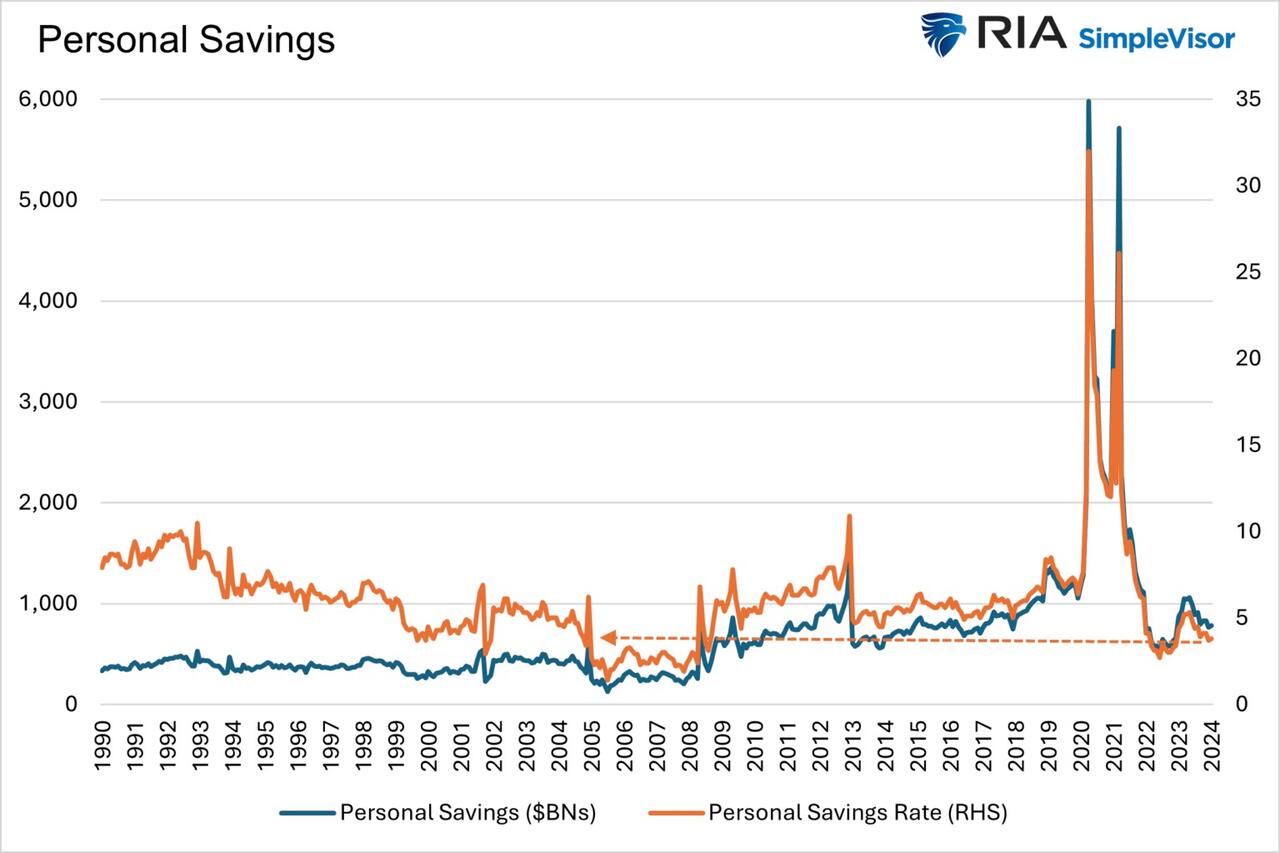

Savings

The graph below shows the rollercoaster on which personal savings have been since the pandemic. The savings rate is hovering at the lowest rate since those seen before the 2008 recession. The total amount of personal savings is back to 2017 levels. But, on an inflation-adjusted basis, it’s at 10-year lows. On average, most consumers are drawing down their savings or less. Given that wages are increasing and unemployment is historically low, they must be consuming more.

Now, strip out the savings of the uber-wealthy, and it’s probable that the amount of personal savings for much of the population is negligible. A survey by Payroll.org estimates that 78% of Americans live paycheck to paycheck.

More on Insufficient Savings

The Fed’s latest, albeit old, Report on the Economic Well-Being of U.S. Households from June 2023 claims that over a third of households do not have enough savings to cover an unexpected $400 expense. We venture to guess that number has grown since then. To wit, the number of households with essentially no savings rose 5% from their prior report a year earlier.

Relatively small, unexpected expenses, such as a car repair or a modest medical bill, can be a hardship for many families. When faced with a hypothetical expense of $400, 63 percent of all adults in 2022 said they would have covered it exclusively using cash, savings, or a credit card paid off at the next statement (referred to, altogether, as “cash or its equivalent”). The remainder said they would have paid by borrowing or selling something or said they would not have been able to cover the expense.

Debt

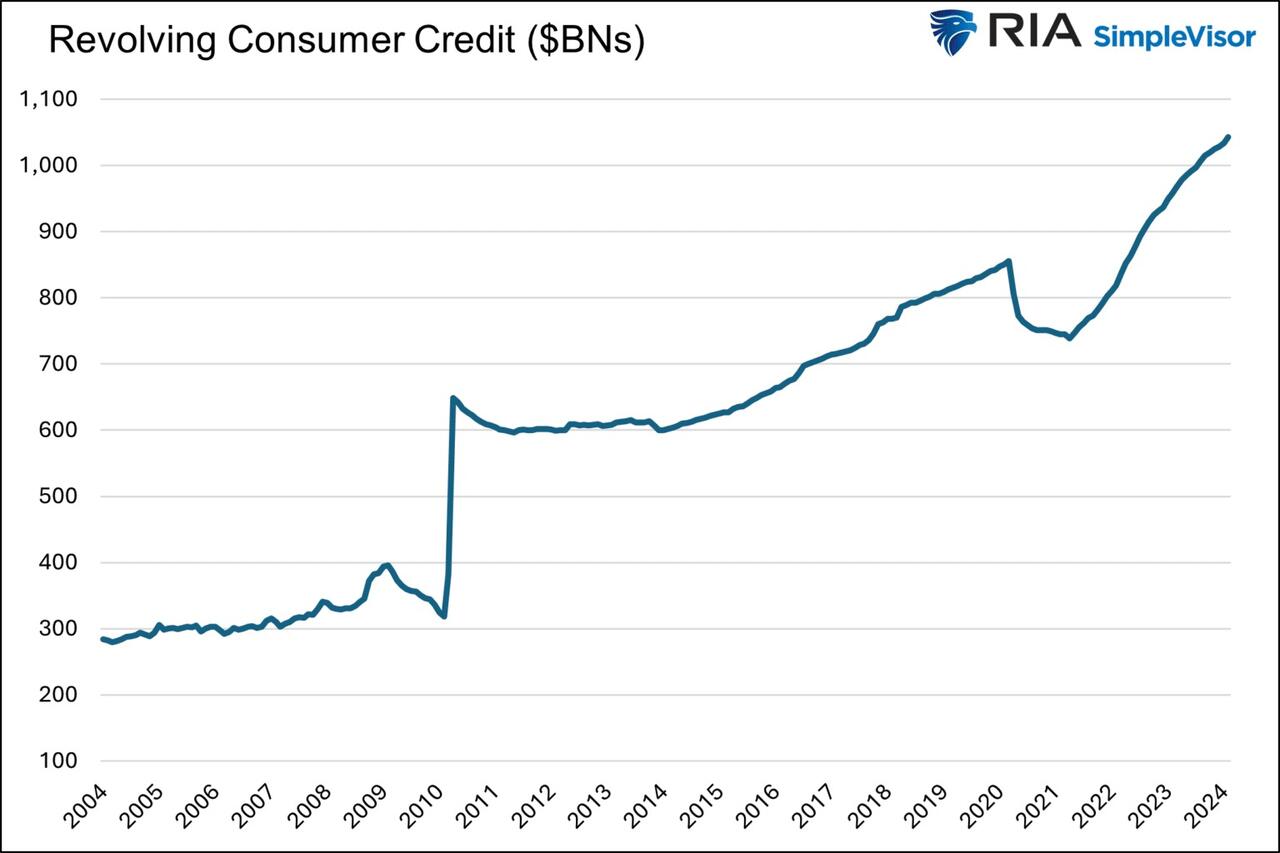

After periods where consumers drained their existing savings and/or devoted less of their paychecks to savings, they either slowed their consumption patterns or borrowed to keep them up. Currently, it seems like many are choosing the latter option. Consumer borrowing is accelerating at a quicker pace than it was before the pandemic.

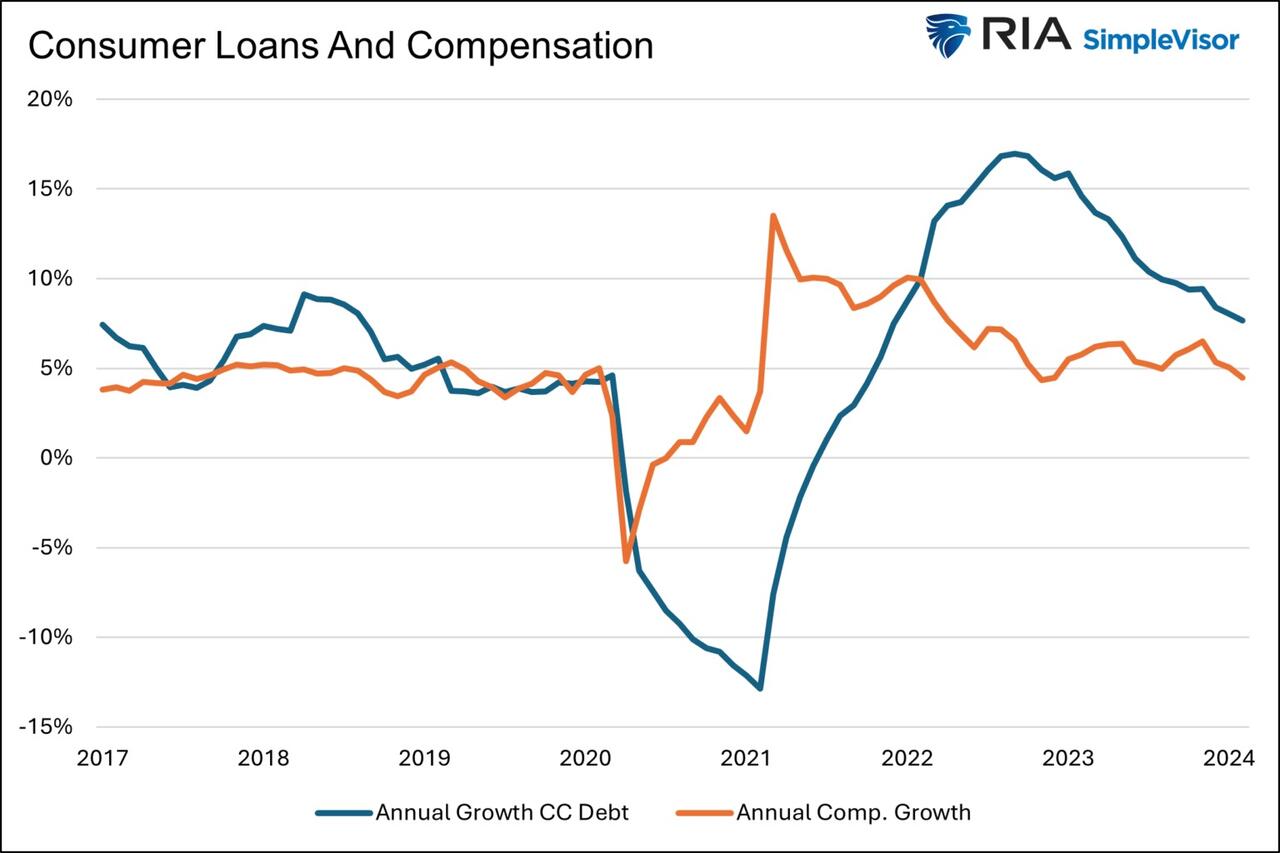

The first graph below shows outstanding credit card debt fell during the pandemic as the economy cratered. However, after multiple stimulus checks and broad-based economic recovery, consumer confidence rose, and with it, credit card balances surged.

The current trend is steeper than the pre-pandemic trend. Some may be a catch-up, but the current rate is unsustainable. Consequently, borrowing will likely slow down to its pre-pandemic trend or even below it as consumers deal with higher credit card balances and 20+% interest rates on the debt.

The second graph shows that since 2022, credit card balances have grown faster than our incomes. Like the first graph, the credit usage versus income trend is unsustainable, especially with current interest rates.

With many consumers maxing out their credit cards, is it any wonder buy-now-pay-later loans (BNPL) are increasing rapidly?

Insider Intelligence believes that 79 million Americans, or a quarter of those over 18 years old, use BNPL. Lending Tree claims that “nearly 1 in 3 consumers (31%) say they’re at least considering using a buy now, pay later (BNPL) loan this month.”More telling, according to their survey, only 52% of those asked are confident they can pay off their BNPL loan without missing a payment!

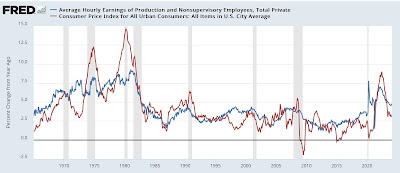

Wage Growth

Wages have been growing above trend since the pandemic. Since 2022, the average annual growth in compensation has been 6.28%. Higher incomes support more consumption, but higher prices reduce the amount of goods or services one can buy. Over the same period, real compensation has grown by less than half a percent annually. The average real compensation growth was 2.30% during the three years before the pandemic.

In other words, compensation is just keeping up with inflation instead of outpacing it and providing consumers with the ability to consume, save, or pay down debt.

It’s All About Employment

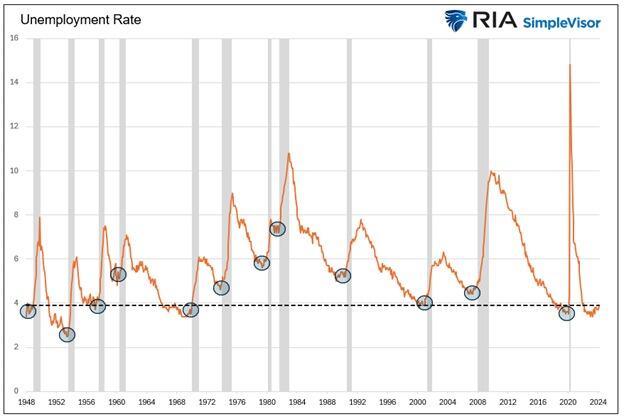

The unemployment rate is 3.9%, up slightly from recent lows but still among the lowest rates in the last seventy-five years.

The uptick in credit card usage, decline in savings, and the savings rate argue that consumers are slowly running out of room to keep consuming at their current pace.

However, the most significant means by which we consume is income. If the unemployment rate stays low, consumption may moderate. But, if the recent uptick in unemployment continues, a recession is extremely likely, as we have seen every time it turned higher.

It’s not just those losing jobs that consume less. Of greater impact is a loss of confidence by those employed when they see friends or neighbors being laid off.

Accordingly, the labor market is probably the most important leading indicator of consumption and of the ability of the Bougie Broke to continue to be Bougie instead of flat-out broke!

Summary

There are always consumers living above their means. This is often harmless until their means decline or disappear. The Bougie Broke meme and the ability social media gives consumers to flaunt their “wealth” is a new medium for an age-old message.

Diving into the data, it argues that consumption will likely slow in the coming months. Such would allow some consumers to save and whittle down their debt. That situation would be healthy and unlikely to cause a recession.

The potential for the unemployment rate to continue higher is of much greater concern. The combination of a higher unemployment rate and strapped consumers could accentuate a recession.

Uncategorized

The most potent labor market indicator of all is still strongly positive

– by New Deal democratOn Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently…

Share this:

{kind=link}

{kind=link}

- by New Deal democrat

On Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently than not indicated a recession was near or underway. But I concluded by noting that this survey has historically been noisy, and I thought it would be resolved away this time. Specifically, there was strong contrary data from the Establishment survey, backed up by yesterday’s inflation report, to the contrary. Today I’ll examine that, looking at two other series.

{kind=link}

Q4 Update: Delinquencies, Foreclosures and REO

Digital Currency And Gold As Speculative Warnings

Bougie Broke The Financial Reality Behind The Facade

NY Fed Finds Medium, Long-Term Inflation Expectations Jump Amid Surge In Stock Market Optimism

Aging at AACR Annual Meeting 2024

Bitcoin on Wheels: The Story of Bitcoinetas

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

The most potent labor market indicator of all is still strongly positive

‘Bougie Broke’ – The Financial Reality Behind The Facade

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges