Spread & Containment

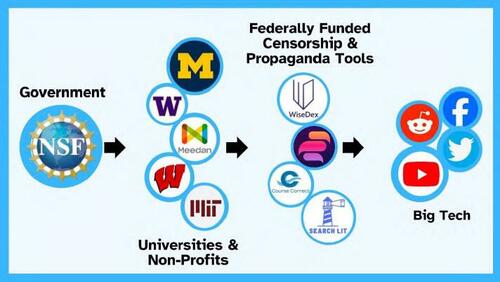

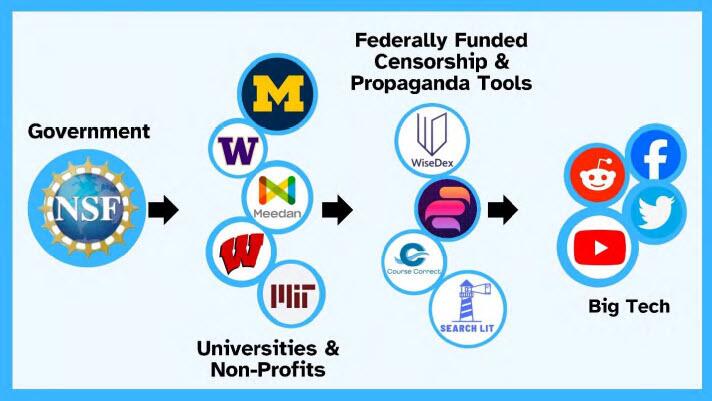

NSF Paid Universities To Develop AI Censorship Tools For Social Media

NSF Paid Universities To Develop AI Censorship Tools For Social Media

By Daniel Nuccio of The College Fix

"Used by governments and Big Tech…

Share this:

By Daniel Nuccio of The College Fix

"Used by governments and Big Tech to shape public opinion by restricting certain viewpoints or promoting others’: report

The National Science Foundation is paying universities using taxpayer money to create AI tools that can be used to censor Americans on various social media platforms, according to members of the House.

University of Michigan, the University of Wisconsin-Madison, and MIT are among the universities cited in the House Judiciary Committee and the Select Subcommittee on the Weaponization of the Federal Government interim report.

It details the foundation’s “funding of AI-powered censorship and propaganda tools, and its repeated efforts to hide its actions and avoid political and media scrutiny.”

“NSF has been issuing multi-million-dollar grants to university and non-profit research teams” for the purpose of developing AI-powered technologies “that can be used by governments and Big Tech to shape public opinion by restricting certain viewpoints or promoting others,” states the report, released last month.

Funding for the projects began in 2021 and was issued through the NSF’s Convergence Accelerator grant program, which was initially launched in 2019 to develop interdisciplinary solutions to major challenges of national and societal importance such as those pertaining to AI and quantum technology, it states.

In 2021, however, the NSF introduced “Track F: Trust & Authenticity in Communication Systems.”

The NSF’s 2021 Convergence Accelerator program solicitation stated the goal of Track F projects was to “develop prototype(s) of novel research platforms forming integrated collection(s) of tools, techniques, and educational materials and programs to support increased citizen trust in public information of all sorts (health, climate, news, etc.), through more effectively preventing, mitigating, and adapting to critical threats in our communications systems.”

Specifically, the grant solicitation singled out the threats posed by hackers and misinformation.

That September, the select subcommittee report notes, the NSF awarded “twelve Track F teams $750,000 each (a total of $9 million) to develop and refine their project ideas and build partnerships.” The following year, the NSF selected six of the 12 teams to receive an additional $5 million each for their respective projects, according to the report.

Projects from the University of Michigan, University of Wisconsin-Madison, MIT, and Meedan, a nonprofit that specializes in developing software to counter misinformation, are highlighted by the select subcommittee.

Collectively, these four projects received $13 million from the NSF, it states.

“The University of Michigan intended to use the federal funding to develop its tool ‘WiseDex,’ which could use AI technology to assess the veracity of content on social media and assist large social media platforms with what content should be removed or otherwise censored,” it states.

The University of Wisconsin-Madison’s Course Correct, which was featured in an article from The College Fix last year, was “intended to aid reporters, public health organizations, election administration officials, and others to address so-called misinformation on topics such as U.S. elections and COVID-19 vaccine hesitancy.”

MIT’s Search Lit, as described in the select subcommittee’s report, was developed as an intervention to help educate groups of Americans the researchers believed were most vulnerable to misinformation such as conservatives, minorities, rural Americans, older adults, and military families.

Meedan, according to its website, used its funding to develop “easy-to-use, mobile-friendly tools [that] will allow AAPI [Asian-American and Pacific Islander] community members to forward potentially harmful content to tiplines and discover relevant context explainers, fact-checks, media literacy materials, and other misinformation interventions.”

According to the select committee’s report, “Once empowered with taxpayer dollars, the pseudo-science researchers wield the resources and prestige bestowed upon them by the federal government against any entities that resist their censorship projects.”

“In some instances,” the report states, “if a social media company fails to act fast enough to change a policy or remove what the researchers perceive to be misinformation on its platform, disinformation researchers will issue blogposts or formal papers to ‘generate a communications moment’ (i.e., negative press coverage) for the platform, seeking to coerce it into compliance with their demands.”

Efforts were made via email to contact senior members of the three university research teams, as well as a representative from Meedan, regarding the portrayal of their work in the select subcommittee’s report.

Paul Resnick, who serves as the WiseDex project director at the University of Michigan, referred The College Fix to the WiseDex website.

“Social media companies have policies against harmful misinformation. Unfortunately, enforcement is uneven, especially for non-English content,” states the site. “WiseDex harnesses the wisdom of crowds and AI techniques to help flag more posts [than humans can]. The result is more comprehensive, equitable, and consistent enforcement, significantly reducing the spread of misinformation.”

A video on the site presents the tool as a means to help social media sites flag posts that violate platform policies and subsequently attach warnings to or remove the posts. Posts portraying approved COVID-19 vaccines as potentially dangerous are used as an example.

Michael Wagner from the University of Wisconsin-Madison also responded to The Fix, writing, “It is interesting to be included in a report that claims to be about censorship when our project censors exactly no one.”

According to the select subcommittee report, some of the researchers associated with Track F and similar projects, however, privately acknowledged efforts to combat misinformation were inherently political and a form of censorship.

Yet, following negative coverage of Track F projects, depicting them as politically motivated and their products as government-funded censorship tools, the report notes, the NSF began discussing media and outreach strategy with grant recipients.

Notes from a pair of Track F media strategy planning sessions included in Appendix B of the select subcommittee’s report recommended researchers, when interacting with the media, focus on the “pro-democracy” and “non-ideological” nature of their work, “Give examples of both sides,” and “use sports metaphors.”

The select subcommittee report also highlights that there were discussions of having a media blacklist, although at least one researcher from the University of Michigan objected to this, citing the potential optics.

Spread & Containment

Chapter 11 bankruptcy on table for nationwide restaurant chain

The popular chain has made some devastating mistakes that put its future in doubt and its owner wants out.

Share this:

Restaurant chains that built their brands around a dine-in experience have suffered since the Covid pandemic. During the period where social distancing required eateries to close their dining rooms (or greatly limit their capacities), some companies simply weren't set up to pivot to an all-delivery model.

That left a number of restaurant operators taking on added debt that they have not been able to recover from once the pandemic-related rules were relaxed. In addition, restaurants have been dealing with inflation, higher ingredient prices, and consumers who are worried about the economy.

Related: Fast-food chain nears end after failed Chapter 11 bankruptcy filings

People have generally been eating out less at least partially because supermarket prices have fallen from inflation and supply chain problem-driven highs while restaurant prices have inched up.

"Historically, when commodity inflation runs ahead of labor inflation, grocery pricing pushes ahead of restaurants," Citi analyst Jon Tower wrote in a not to clients. "When labor inflation runs ahead of commodity inflation, restaurant prices tend to outpace grocery pricing."

Restaurants have been spending more on labor as 22 states raised their minimum wage on Jan. 1, 2024 while a tight labor market has generally pushed service industry wages higher. It's a difficult situation for restaurant operators with one popular brand that operates 650 restaurants globally showing signs that it might be in real trouble.

Red Lobster brings in a restructuring expert

Red Lobster, a sit-down seafood chain, has seen multiple chief executives make the same mistake. Edna Morris lost her job as president of the chain after she misjudged how much customers would eat during a $22.99 all-you-can-eat crab promotion.

The chain lost millions on her miscalculation.

“It wasn’t the second helping on all-you-can-eat but the third,” then Chairman Joe R. Lee told analysts, during a Darden earnings call back when that brand owned Red Lobster.

“And maybe the fourth,” added former Chief Operating Officer Dick Rivera.

Amazingly, the company repeated the same mistake under Its current owner Thai Union Group.

The seafood chain used an all-you-can-eat shrimp offer as a way to bring people into the restaurant. It worked, but at $20, it was priced too low for the company to make money on the deal. That deal is still on the menu, but the price has been raised to $25.

Now, the struggling chain has replaced its CEO Horace Dawson, who is retiring, with Jonathan Tibus, managing director of management consultant Alvarez & Marsal. Tibus is considered a turnaround expert who helped Kona Grill and Krystal through their Chapter 11 bankruptcy filings.

Chapter 11 filing looms for "zombie" brand

Thai Union Group has already shared that it intends to divest itself of the Red Lobster brand.

“During the past years, the combination of Covid-19 pandemic, sustained industry headwinds, higher interest rates and rising material and labor costs have impacted to Red Lobster business resulting in prolonged negative financial contributions to the company and its shareholders,” Thai Union said in a Jan. 16 media release. “...After detailed analysis, the board of directors has determined that Red Lobster’s ongoing financial requirements no longer align with our capital allocation priorities and therefore the company is pursuing an exit of the minority investment.”

FoodserviceResults CEO Darren Tristano believes the company is headed toward a resolution.

“It appears that Red Lobster is planning for a turnaround, bankruptcy, or fire sale,” he told SeafoodSource.

Red Lobster is now considered a “zombie brand,” Tristano said.

“[Red Lobster] continues to wander aimlessly looking for direction,” he said.

Thai Union Group has said it does not expect to make any money on a sale of the brand and has already taken a $650 million writedown.

"Because Red Lobster has not yet named a new buyer, it would appear that bankruptcy would be the best option followed by a sale after the balance sheet gets cleaned up," Tristano added.

Red Lobster has been operating since 1968. The company started as a single, family-owned restaurant in Lakeland, Fla., and later grew to nearly 800 locations worldwide.

Thai Union, one of the largest seafood companies in the world, did not immediately respond to a request for comment.

bankruptcy pandemic covid-19 social distancing interest ratesSpread & Containment

In the fog of the video streaming wars, job losses and business closures are imminent

The video streaming industry has reached a tipping point.

Share this:

Prussian general and military theorist Carl von Clausewitz presented the concept of the “fog of war” in 1832. It is a phrase that has become synonymous with the uncertainty and confusion of military battle.

But this expression also acts as a useful metaphor to describe the industry and market dynamics that subscription video-on-demand streaming firms find themselves operating in – that is, uncertainty.

This uncertainty is demonstrated by the performance of American streaming platform Disney+. Since 2019, the platform has received US$10 billion (£7.9 billion) of investment. But, over the same period, it has lost roughly 12 million customers, and it posted staggering losses of more than US$1.6 billion in 2023.

In November, its parent company, Walt Disney, introduced a new “cost-reduction strategy” that will aim to cut 7,000 jobs and save US$7.5 billion in the face of weakening economic conditions and tougher competition.

Five year share price comparison: Walt Disney v New York Stock Exchange

The COVID pandemic supercharged the on-demand streaming business as consumers sought to entertain themselves during the numerous lockdowns. The streaming industry experienced a period of rapid growth, attracting a flood of new entrants lured by market growth rates of 40% per year and potentially high profits from surging consumer demand.

Companies such as Netflix, Amazon, Disney+ and Apple TV gained millions of customers in a matter of months and invested billions of dollars on new content, infrastructure and marketing. It all seemed too good to be true as the “land grab” for subscriber growth and market share continued into 2022.

However, an easing of lockdown restrictions saw consumers vacate their sofas and give up their binge-watching TV habits, ready to explore the great outdoors again.

The shakeout

The streaming industry is currently characterised by an oversupply of service providers. This has led to aggressive competitive pricing where businesses set their prices based on what their competitors are charging.

For example, instead of Netflix basing its subscription price solely on production costs and a desired profit margin, it will consider the prevailing prices offered by its rivals in the market and find a strategic price point that allows it to be competitive while also maintaining profitability.

Platforms with less efficient operations or inferior offerings are starting to struggle and an “industry shakeout” is inevitable. This is where a significant number of businesses are eliminated or acquired through competition in a period of intense consolidation.

Think of it as a metaphorical earthquake. The ground shifts beneath established players, forcing some to adapt, some to crumble, and others to emerge even stronger.

Take, for instance, the Swedish streaming platform, Viaplay. Despite being much smaller than its US counterparts, it adopted an expensive international expansion strategy that was fuelled by the pandemic. This strategic approach failed and Viaplay could not expand profitably outside its home market.

The cost of living crisis then resulted in subscriber price increases and higher customer churn as a result. Uncertainty surrounding the firm has also been made worse by the sacking of its CEO and the introduction of a plan to significantly cut operating costs. It’s no great surprise then that the company has withdrawn its long-term guidance for sales revenue and its share price has slumped by a remarkable 99% over the past 12 months.

This shakeout phase of industry development will result in job losses and business closures until a situation develops where a smaller number of stronger, more efficient players dominate the industry through “scale advantage”.

A good example of consolidation occurred in the social media industry in the early 2000s. Platforms such as MySpace, Friendster and Friends Reunited gained early popularity with consumers, but then ceased trading or became a competitive insignificance as Facebook emerged as a dominant force. To maintain its market-leading position and access new users, Facebook went on to acquire smaller competitors including Instagram and WhatsApp in 2012 and 2014 respectively.

The benefits of this “scale advantage” are more efficient access to international markets, higher profitability and the ability to deliver lower subscription prices due to the economies of scale. This is particularly beneficial to consumers at a time of inflationary pressure on discretionary spend.

The outlook

So, who is at risk on the battlefield of streaming wars? Even household favourites such as Netflix, with a global market share of 24%, 260 million subscribers and best-in-class content are not safe.

Five year share price comparison: Netflix v Nasdaq

Given the current focus on corporate profitability in an industry likely to consolidate, Netflix’s ability to produce a net profit of more than US$5 billion and an impressive operating margin of 21% in 2023 will make it a potential target for acquisition. This is particularly the case given that the size of the company, at US$264 billion, is relatively small compared to larger competitors such as Apple (US$2.75 trillion) and Amazon (US$1.84 trillion).

The “fog of streaming war” will clear and the strategic uncertainty caused by lower market growth rates, inflationary pressure and economic weakness will decrease. As such, competitive industry positions will become more established, normalised and defended.

The key question facing most media companies in the future will be how to make subscription video-on-demand streaming a profitable part of their business.

John J Oliver does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

nasdaq pandemic lockdownSpread & Containment

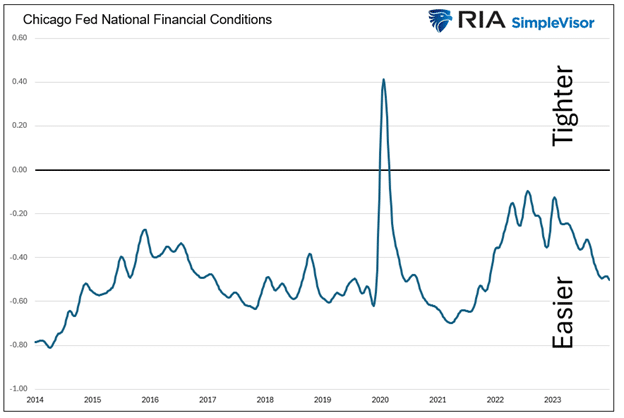

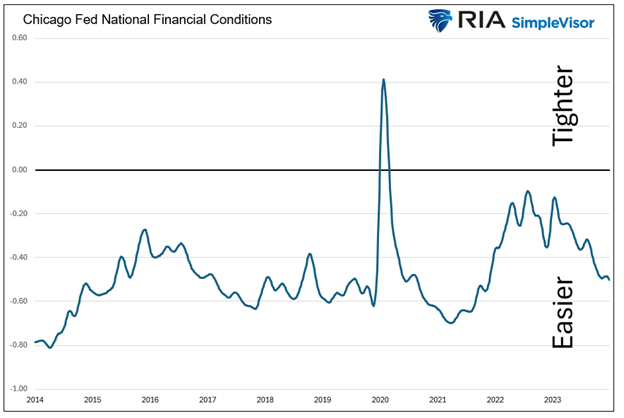

Financial Conditions Butt Heads With Borrowing Conditions

At last week’s FOMC meeting, Jerome Powell said, "We think financial conditions are weighing on the economy."

His comments seem sensible, given the following:

The…

Share this:

{kind=link}

At last week’s FOMC meeting, Jerome Powell said, “We think financial conditions are weighing on the economy.”

His comments seem sensible, given the following:

- The Fed is reducing its balance sheet (QT).

- The Fed Funds rate is at its highest level in over 15 years.

- Mortgage rates are about 7%, 3-4% above pre-pandemic levels.

- Credit card interest rates are 20% or more.

- Auto loans range between 7% and 10%

- Consumer loan growth, excluding the pandemic, is down to levels last seen over ten years ago.

- Outstanding Commercial & Industrial (C&I) loans are declining.

Powell’s statement indicates that financial conditions are tight. However, they are easy based on the Fed’s definition of financial conditions. If Powell doesn’t appreciate the difference between financial and borrowing conditions, we must assume most investors do not either.

{kind=link}

As we will explain, there is a big difference between financial and borrowing conditions. Equally worth considering is that the current combination of easy financial conditions and tight borrowing conditions makes monetary policy difficult for the Fed to balance.

What Are Financial Conditions?

The St. Louis Federal Reserve defines financial conditions as follows:

“Measures of equity prices (also commonly referred to as stock prices), the strength of the U.S. dollar, market volatility, credit spreads, long-term interest rates, and other variables.”

Financial conditions tend to be easy when investors are optimistic and speculative. Let’s look at the four critical measures in the St. Louis Fed definition to understand why financial conditions are easy today.

Equity Prices: The S&P 500 is up 38% since 2023 and 10% through the first three months of 2024.

U.S. Dollar: The dollar index has been relatively flat since 2023 and the year to date.

Market Volatility: The VIX volatility index has been hovering between 12 and 15 this year. That is about one standard deviation below the average VIX reading of 19.32 over the last 35 years.

Credit Spreads: The BBB investment grade yield is only 1% above a comparable maturity Treasury. Such is the tightest spread since the 1990s.

Long-Term Interest Rates: Long-term interest rates have been significantly higher than average over the past few years and at levels last seen before the financial crisis in 2008. However, they are about 1% lower than their peak last year.

Equity prices, market volatility, and credit spreads point to very easy financial conditions, and we might also characterize their levels as speculative.

The dollar has had little effect on financial conditions as it has been relatively stable.

Long-term interest rates point to tighter financial conditions, albeit easing over the past six months.

The bottom line is that financial conditions are easy in large part because robust sentiment in the equity and credit markets more than offsets higher interest rates.

As shown below, our proprietary SimpleVisor Sentiment indicator is at its maximum level, and the CNN Fear & Greed Index is closing in on extreme greed.

What Are Borrowing Conditions?

Unlike financial conditions, borrowing conditions are far from easy. The two graphs below highlight the financial stress on consumer and corporate borrowers.

Credit card interest rates are over 20% and about 5% above the highest in the past 24 years. Mortgage and auto loan interest rates are up to levels not seen in at least fifteen years.

The following graph shows that 90-day commercial paper loans and yields on BBB-rated corporate bonds are at their highest levels since the financial crisis.

What Can And Can’t The Fed Manage?

The Fed plays a crucial role in directing financial and borrowing conditions. At times, like today, financial and borrowing conditions can be at odds with each other, which makes the Fed’s job of managing monetary policy more difficult.

The market’s perception of the Fed’s stance, hawkish or dovish, and more importantly, forecasts of how they may change policy can heavily impact market sentiment and financial conditions.

For instance, a strong correlation exists between QE and higher stock returns, lower volatility, and tighter credit spreads. The relationship occurs in part due to the psychology of investors. However, it’s also a function of the liquidity the Fed creates when conducting QE. For similar reasons, lower rates are thought to be beneficial for markets.

The Fed has a heavier hand in determining borrowing conditions. By managing its Fed Funds rate, the Fed sets the tone for long-term interest rates and significantly influences shorter-term rates. Further, QE and QT can add or subtract liquidity from the markets, directly affecting the supply and demand of liquidity available to all markets.

Powell’s Predicament

Financial conditions have eased considerably as investors priced out the odds of rate increases and have started pricing in rate cuts. The combination of lower interest rates and possibly less QT, coupled with robust economic growth, is the goldilocks scenario driving investors’ sentiment higher. This occurs despite extremely tight borrowing conditions and a hawkish monetary policy.

Currently, the Fed does not want financial conditions to ease further as the wealth effect of strong markets can have an inflationary impulse. They could hike rates or even talk of increasing rates to weigh on financial conditions. However, with tight borrowing conditions and the potential that the lag effect of prior rate hikes will ultimately cause a recession, they appear to be in no man’s land.

As we share below, on a real basis, the Fed’s policy stance is the tightest it has been in fifteen years.

Another Fed Predicament Coming Soon

Sentiment and liquidity drive markets in the short run. Both have supported higher stock prices and mania-like trading in AI stocks and cryptocurrencies.

However, that could be changing. As we note in Liquidity Problems, excess liquidity is rapidly draining from the financial system. The Fed knows the situation and may be called upon to deal with a liquidity shortfall. QT reductions and/or lower rates would ease liquidity concerns. But, doing so, especially if the economy stays robust and market sentiment is strong, would risk further easing of financial conditions, which in turn may keep inflation sticky at current levels.

Summary

The Goldilocks economy, coupled with the end of the rate hiking cycle, has investors giddy, which eases financial conditions. Ironically, while some of the easiest financial conditions in the last ten years have existed, borrowing conditions remain very tight.

The Fed must balance these two conditions, which is difficult as they can counteract each other. Threading the eye of this needle may prove problematic given that inflation remains too high and, more recently, is showing some signs of being sticky.

The post Financial Conditions Butt Heads With Borrowing Conditions appeared first on RIA.

recession pandemic economic growth bonds corporate bonds credit markets sp 500 stocks monetary policy fomc qe fed federal reserve mortgage rates spread interest rates

Lockdown’s Fourth Birthday

ARPA-H awards Columbia researchers nearly $39M to develop a living knee replacement

Financial Conditions Butt Heads With Borrowing Conditions

In the fog of the video streaming wars, job losses and business closures are imminent

The Canaries In America’s Coal Mine

Chapter 11 bankruptcy on table for nationwide restaurant chain

NSF Paid Universities To Develop AI Censorship Tools For Social Media

-

Spread & Containment2 weeks ago

Spread & Containment2 weeks agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized1 month ago

Uncategorized1 month agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International6 days ago

International6 days agoParexel CEO to retire; CAR-T maker AffyImmune promotes business leader to chief executive

-

International3 weeks ago

International3 weeks agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoApparel Retailer Express Moving Toward Bankruptcy

-

International3 weeks ago

International3 weeks agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoKey Events This Week: All Eyes On Core PCE Amid Deluge Of Fed Speakers

-

Uncategorized1 month ago

Uncategorized1 month agoA Blue State Exodus: Who Can Afford To Be A Liberal