Uncategorized

No Asset Class Is Remotely Ready For More Inflation

No Asset Class Is Remotely Ready For More Inflation

Authored by Simon White, Bloomberg macro strategist,

Stocks, bonds, commodities and other…

Share this:

Authored by Simon White, Bloomberg macro strategist,

Stocks, bonds, commodities and other real assets are dramatically unpriced for a resurgence in inflation.

If fortune favors the prepared, then no market is going to have much luck. A re-acceleration in inflation is increasingly on the cards (see here), an eventuality that is materially underpriced across asset classes. That means portfolios are cheap to hedge, as well as leaving markets subject to outsized moves when they do price in inflation’s return.

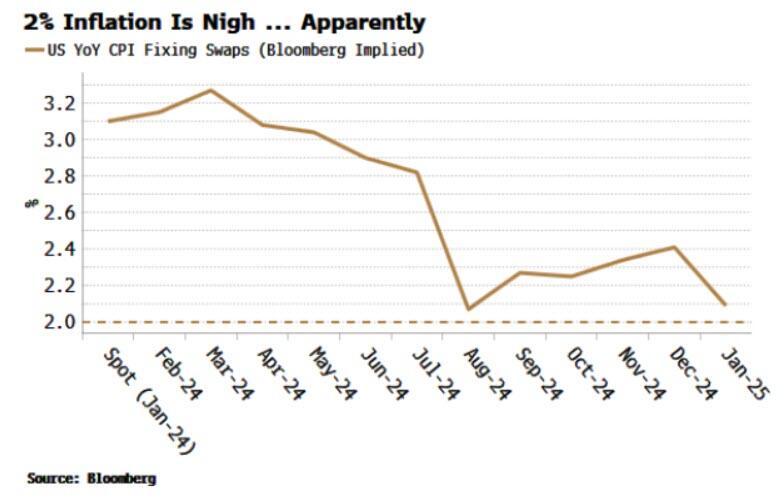

Inflation complacency can be seen clearly in one chart. CPI fixing swaps foresee a continued steady decline in headline inflation in the US back toward 2% through this year. Not only that, most of the swaps have been falling in recent months as spot inflation has eased. The implied probability of a return of inflation is dwindling to zero.

But it’s not just fixing swaps predicting a return to inflation utopia. Across markets, there are indications that are not only underpricing a revival in price growth, they appear to be ignoring the possibility altogether:

-

nominal yields with negative inflation risk premium

-

real yields with low downside skew

-

low expectation of much higher short-term rates

-

high exposure to equity sectors with steep duration

-

low exposure to the sectors best placed to weather inflation

-

commodity volatility that’s very subdued

-

ownership in commodities that is at histrocial lows

The charts will do most of the talking. Start with nominal yields. We can decompose them (via the DKW model) into a real expected short-rate, real term-premium, expected inflation and inflation term-premium (aka risk premium).

The drop in the 10-year yield from its October high has been driven by a fall in the real expected short-rate, as well as a decline in expected inflation. But there is nothing built into the price for inflation’s volatility rising again, as it typically does when price pressures increase. In fact, the inflation risk-premium is more negative than it was in the years leading up to the pandemic.

Real yields too are bereft of any risk premium for inflation. If the Federal Reserve does not immediately react to rising inflation (as happened in 2021, and I suspect will happen this year if and when inflation starts to pick back up), real yields are likely to experience downside volatility, i.e. call skew for TIPS should rise. Again there is no sign of market nerves here.

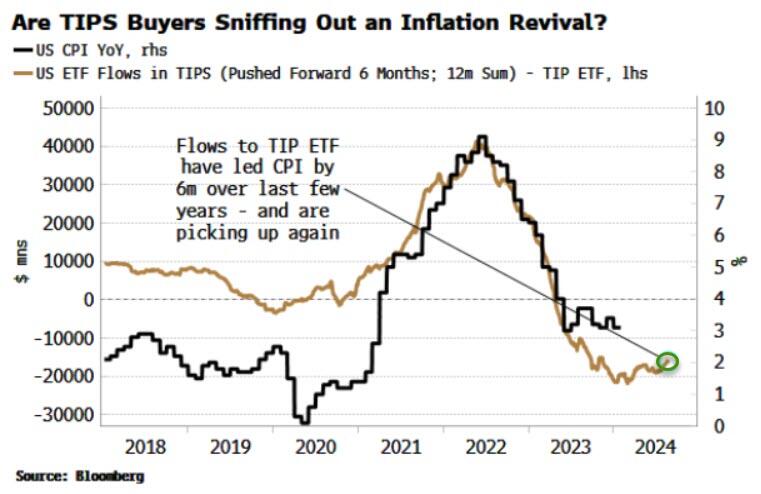

As the chart above shows, TIPS call skew has tended to lead inflation over the last few years, and thus there is little in the way of rising price growth expected soon. The inflation-bond market may have this one wrong.

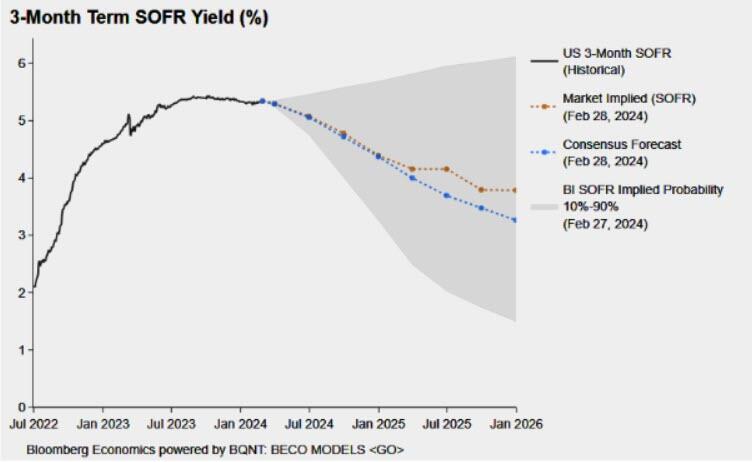

Short-term rates don’t look any better. The market is still expecting lower rates over the next year, which might make sense from a weighted-average perspective given that when things go wrong (e.g. a recession) they go violently wrong. But there is little likelihood priced in for much higher rates – the distribution for SOFR rates has a clear downwards skew.

Overall, bond investors just aren’t anticipating more inflation, with the number of investors who say they are short USTs in JPMorgan’s Treasury survey plumbing its series lows.

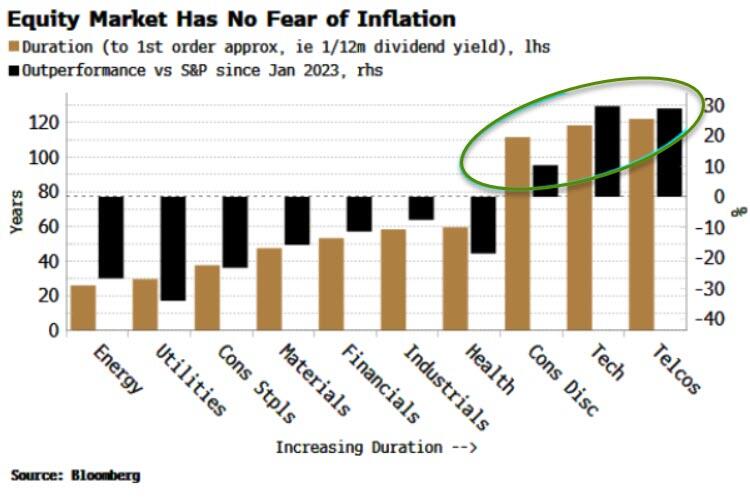

Stocks are also very much on Team Transitory (and we can make similar arguments for credit). There continues to be a bias toward high-duration sectors (which are more likely to fare worse when inflation is high), such as tech and telcos, with these strongly outperforming the index.

On the flipside, the sectors with historically the best record when inflation is elevated are those with low duration such as energy and staples, which continue to lag heavily behind.

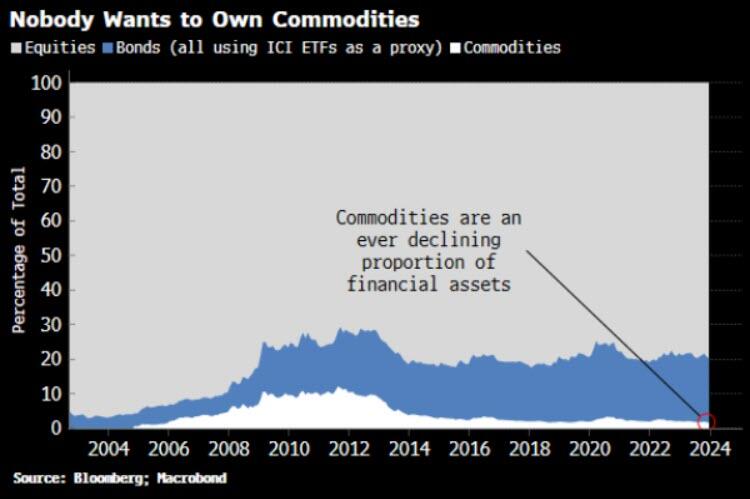

Bonds, and stocks in the main, are assets to avoid (or short) when inflation is troublesome, but commodities and other real assets are havens. But here as well, there is no sign investors are making hay while the disinflation sun is shining. Commodity ownership relative to stocks and bonds continues to fall, and now represents only a measly 1.7% of the total.

That’s not just down to valuation effects, given commodities are now 30% lower than their 2022 peak, but due to real outflows from the asset class (using commodity ETFs as a proxy).

It could be the calm before the storm. Implied volatility in several commodities, mainly in metals, has been falling and is near 10-year lows. Lead, copper, nickel and most notably gold and silver are within ten percentage points of their vol troughs over the last decade.

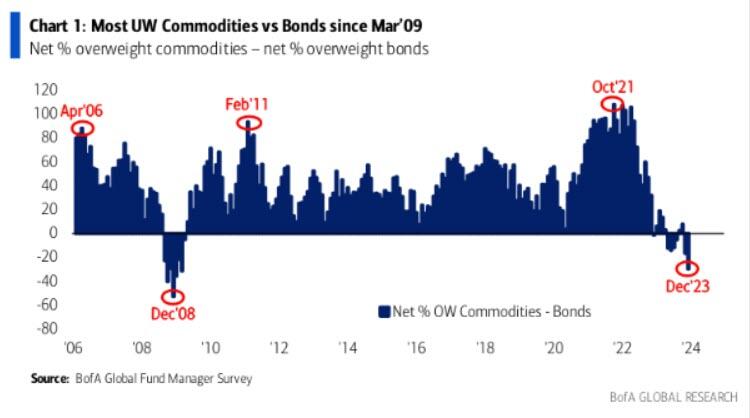

Again, why own real assets over financial assets when you think inflation is yesterday’s story? That’s reflected in BofA’s Global Fund Manager Survey from December, showing the biggest underweight in commodities versus bonds since the post-GFC equity-market bottom in March 2009.

Source: Bank of America

Just maybe though there is one market sensing price growth is returning and is moving to hedge it. I mentioned above TIPS skew did not appear to be anticipating an inflation-driven lurch lower in real yields. But inflows into TIPS ETFs as a whole are slowly picking up. This had a good call in the pandemic, starting to rise about three months before CPI started its ascent in 2020 (when inflation leading indicators were already rising, as they are today).

Either way, there are precious few signs a re-acceleration in inflation is being priced in even as much of a tail-risk across markets. Fortune favors the hedged — and at the moment, that’s exceedingly cheap to do.

Uncategorized

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Today, in the Calculated Risk Real Estate Newsletter: Part 1: Current State of the Housing Market; Overview for mid-March 2024

A brief excerpt: This 2-part overview for mid-March provides a snapshot of the current housing market.

I always like to star…

Share this:

A brief excerpt:

This 2-part overview for mid-March provides a snapshot of the current housing market.There is much more in the article.

I always like to start with inventory, since inventory usually tells the tale!

...

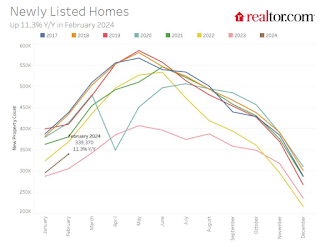

Here is a graph of new listing from Realtor.com’s February 2024 Monthly Housing Market Trends Report showing new listings were up 11.3% year-over-year in February. This is still well below pre-pandemic levels. From Realtor.com:

However, providing a boost to overall inventory, sellers turned out in higher numbers this February as newly listed homes were 11.3% above last year’s levels. This marked the fourth month of increasing listing activity after a 17-month streak of decline.Note the seasonality for new listings. December and January are seasonally the weakest months of the year for new listings, followed by February and November. New listings will be up year-over-year in 2024, but we will have to wait for the March and April data to see how close new listings are to normal levels.

There are always people that need to sell due to the so-called 3 D’s: Death, Divorce, and Disease. Also, in certain times, some homeowners will need to sell due to unemployment or excessive debt (neither is much of an issue right now).

And there are homeowners who want to sell for a number of reasons: upsizing (more babies), downsizing, moving for a new job, or moving to a nicer home or location (move-up buyers). It is some of the “want to sell” group that has been locked in with the golden handcuffs over the last couple of years, since it is financially difficult to move when your current mortgage rate is around 3%, and your new mortgage rate will be in the 6 1/2% to 7% range.

But time is a factor for this “want to sell” group, and eventually some of them will take the plunge. That is probably why we are seeing more new listings now.

Uncategorized

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45%…

Share this:

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45% of US respondents in 2023, according to the latest Harris Poll data. That’s exactly the same as the previous year.

Pharma’s highest point was in February 2021 — as Covid vaccines began to roll out — with a 62% positive US perception, and helping the industry land at an average 55% positive sentiment at the end of the year in Harris’ 2021 annual assessment of industries. The pharma industry’s reputation hit its most recent low at 32% in 2019, but it had hovered around 30% for more than a decade prior.

“Pharma has sustained a lot of the gains, now basically one and half times higher than pre-Covid,” said Harris Poll managing director Rob Jekielek. “There is a question mark around how sustained it will be, but right now it feels like a new normal.”

The Harris survey spans 11 global markets and covers 13 industries. Pharma perception is even better abroad, with an average 58% of respondents notching favorable sentiments in 2023, just a slight slip from 60% in each of the two previous years.

Pharma’s solid global reputation puts it in the middle of the pack among international industries, ranking higher than government at 37% positive, insurance at 48%, financial services at 51% and health insurance at 52%. Pharma ranks just behind automotive (62%), manufacturing (63%) and consumer products (63%), although it lags behind leading industries like tech at 75% positive in the first spot, followed by grocery at 67%.

The bright spotlight on the pharma industry during Covid vaccine and drug development boosted its reputation, but Jekielek said there’s maybe an argument to be made that pharma is continuing to develop innovative drugs outside that spotlight.

“When you look at pharma reputation during Covid, you have clear sense of a very dynamic industry working very quickly and getting therapies and products to market. If you’re looking at things happening now, you could argue that pharma still probably doesn’t get enough credit for its advances, for example, in oncology treatments,” he said.

vaccine pandemic covid-19Uncategorized

Q4 Update: Delinquencies, Foreclosures and REO

Today, in the Calculated Risk Real Estate Newsletter: Q4 Update: Delinquencies, Foreclosures and REO

A brief excerpt: I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened followi…

Share this:

{kind=link}

{kind=link}

A brief excerpt:

I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble). The two key reasons are mortgage lending has been solid, and most homeowners have substantial equity in their homes..There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ mortgage rates real estate mortgages pandemic interest rates

...

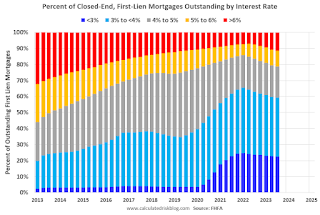

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023 (Q4 2023 data will be released in a two weeks).

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 22.6% of loans are under 3%, 59.4% are under 4%, and 78.7% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

{kind=link}

Q4 Update: Delinquencies, Foreclosures and REO

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Digital Currency And Gold As Speculative Warnings

Bougie Broke The Financial Reality Behind The Facade

‘Bougie Broke’ – The Financial Reality Behind The Facade

Bitcoin on Wheels: The Story of Bitcoinetas

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

The most potent labor market indicator of all is still strongly positive

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges