Government

Merck 2022: The three towers

Merck’s exceptional revenue growth in 2021 and the first half of 2022 came thanks to three big brands, one of which is not even approved by the FDA …

Share this:

Merck’s exceptional revenue growth in 2021 and the first half of 2022 came thanks to three big brands, one of which is not even approved by the FDA yet.

By Joshua Slatko • josh.slatko@medadnews.com

126 East Lincoln Avenue

Rahway, NJ 07065

908-740-4000 • merck.com

| Financial Performance | ||||

| 2021 | 2020 | 1H 2022 | 1H 2021 | |

| Revenue | $48,704 | $41,518 | $30,494 | $22,029 |

| Net income | $13,049 | $7,067 | $8,254 | $4,724 |

| Diluted EPS | $5.14 | $2.78 | $3.25 | $1.86 |

| R&D expense | $12,245 | $13,397 | $5,374 | $6,732 |

|

All figures are in millions of dollars, except EPS. |

||||

Best-selling products

All sales are in millions of dollars.

2021 sales

- Keytruda $17,186

- Gardasil $5,673

- Januvia $3,324

- ProQuad/MMR II/Varivax $2,135

- Janumet $1,964

- Bridion $1,532

- Lynparza $989

- Lagevrio $952

- Pneumovax 23 $893

- Simponi $825

- RotaTeq $807

- Isentress $769

- Lenvima $704

1H 2022 sales

- Keytruda $10,061

- Lagevrio $4,424

- Gardasil $3,133

- Januvia $1,535

- ProQuad/MMR II/Varivax $1,047

- Janumet $931

- Bridion $821

- Lynparza $541

- Lenvima $459

- RotaTeq $389

- Simponi $366

- Pneumovax 23 $325

- Isentress $305

Outcomes Creativity Index Score: 9

- Manny Awards — N/A

- Cannes Lions — N/A

- Clio Health — N/A

- Creative Floor Awards — 4

- London International Awards – N/A

- MM+M Awards — 4

- One Show — 1

Merck in 2022 looks like a company of three towers. The first, Keytruda, continues to break sales records and add indications at a furious pace, with $20 billion in sales for the year not out of the question. The second, Gardasil, has been around a long time but is enjoying a late-career bounce as the COVID pandemic fades. And the third, a tower that did not even exist just a year ago, is the COVID treatment Lagevrio, a drug that has not even been finally approved by the FDA yet, which went from launch via EUA in December 2021 to second place in the company’s portfolio through two quarters of 2022. The three towers together accounted for the large majority of Merck’s top-line growth in 2021, and nearly all of it in the first half of 2022.

“I continue to be immensely proud of how the Merck team is performing in all facets of our business — scientifically, commercially and operationally,” said Robert M. Davis, CEO and president, in the company’s Q2 2022 earnings announcement. “Our strategy is working and our future is bright. I am very confident that we are well-positioned to achieve our near- and long-term goals, anchored by our commitment to deliver innovative medicines and vaccines to patients and value to all of our stakeholders, including shareholders.”

Merck’s top-line revenue in 2021 was $48.7 billion, up 17.3 percent for the year. Nearly all of that growth fell right into the bottom line, with net income rising 84.6 percent to $13.05 billion and earnings per share nearly doubling from $2.78 to $5.14. The trend continued into 2022, with top-line revenue for the first two quarters up 38.4 percent to $30.49 billion, net income up another 74.7 percent to $8.25 billion, and EPS rising by $1.39 to $3.25 per share. Merck leaders project that the company’s full-year EPS for 2022 will fall between $5.89 and $5.99.

Acquisitions and partnerships

In July, Merck and Orion Corp. announced a global development and commercialization agreement for Orion’s investigational candidate ODM-208 and other drugs targeting cytochrome P450 11A1 (CYP11A1), an enzyme important in steroid production. ODM-208 is an oral, non-steroidal inhibitor of CYP11A1 being evaluated in a Phase II clinical trial for the treatment of patients with metastatic

castration-resistant prostate cancer.

Under the terms of the agreement, Orion and Merck will jointly develop and commercialize ODM-208. Merck made an upfront payment to Orion of $290 million. Orion is responsible for the manufacture of clinical and commercial supply of ODM-208. In addition, the contract provides both parties with an option to convert the initial joint development and commercialization agreement into a global exclusive license to Merck. If the option is exercised, Merck would assume full responsibility for all accrued and future development and commercialization expenses associated with the program. Orion would be eligible to receive milestone payments associated with progress in the development and commercialization of ODM-208 as well as tiered double-digit royalties on sales if the product is approved.

In August, Merck and Orna Therapeutics, a biotechnology company pioneering a new investigational class of engineered circular RNA (oRNA) therapies, announced a collaboration agreement to discover, develop, and commercialize multiple programs, including vaccines and therapeutics in the areas of infectious disease and oncology.

Under the terms of the agreement, Merck made an upfront payment to Orna of $150 million. In addition, Orna is eligible to receive up to $3.5 billion in development, regulatory, and sales milestones associated with the progress of the multiple vaccine and therapeutic programs, as well as royalties on any approved products derived from the collaboration. Orna will retain rights to its

oRNA-LNP technology platform and will continue to advance other wholly owned programs in areas such as oncology and genetic disease. Merck will also invest $100 million of equity in Orna’s recently completed Series B financing round.

Orna’s proprietary oRNA technology creates oRNAs from linear RNAs by self-circularization. oRNA molecules have been shown to have greater stability in vivo than linear mRNA and have the potential to produce larger quantities of therapeutic proteins inside the body. Newly synthesized oRNA molecules are more compactly packaged into custom lipid nanoparticles, which Orna has engineered to target key tissues in the body. Preclinical data have demonstrated the potential of oRNA expression and delivery as an approach for further development in multiple areas, including vaccines and oncology therapeutics.

Product performance

Keytruda is tracking towards $20 billion in sales for 2022, as well as adding a long list of new approvals from the European Commission.

Firming up its place as the world’s best-selling oncologic medicine, Keytruda generated $17.19 billion in sales for Merck in 2021, an improvement of 19.5 percent over the previous year. According to company leaders, sales in the United States continued to build across the multiple approved indications, in particular for the treatment of advanced NSCLC as monotherapy, and in combination with chemotherapy for both nonsquamous and squamous metastatic NSCLC, along with continued uptake in the TNBC, RCC, HNSCC, MSI-H cancer, and esophageal cancer indications. Keytruda sales growth in international markets reflected continued uptake predominately for the NSCLC, HNSCC, and RCC indications, particularly in Europe. In the first half of 2022, sales of Keytruda grew another 24.6 percent to $10.06 billion.

In January, the European Commission approved Keytruda as monotherapy for the adjuvant treatment of adults with renal cell carcinoma at increased risk of recurrence following nephrectomy, or following nephrectomy and resection of metastatic lesions. This approval was based on results from the Phase III KEYNOTE-564 trial, in which Keytruda demonstrated a statistically significant improvement in disease-free survival, reducing the risk of disease recurrence or death by 32 percent after a median follow-up of 23.9 months compared to placebo, in patients at increased risk of recurrence (defined in the clinical trial protocol as intermediate-high or high risk following nephrectomy and those with resected advanced disease). Updated efficacy results with a median follow-up time of 29.7 months demonstrated Keytruda reduced the risk of disease recurrence or death by 37 percent compared with placebo.

Also in January, Merck announced the final results from the Phase III KEYNOTE-394 trial investigating Keytruda plus best supportive care in patients in Asia with advanced hepatocellular carcinoma previously treated with sorafenib. KEYNOTE-394 is the first trial with an anti-PD-1/L1 as a second-line monotherapy treatment to show an improvement in overall survival, progression-free survival, and objective response rate versus placebo plus BSC for these patients.

Keytruda plus BSC demonstrated a statistically significant and clinically meaningful improvement in the primary endpoint of OS, reducing the risk of death by 21 percent compared to placebo plus BSC for patients with previously treated advanced HCC. For patients treated with Keytruda plus BSC, median OS was 14.6 months compared to 13.0 months for patients treated with placebo plus BSC. The percentage of patients who were alive at two years was 34.3 percent for Keytruda plus BSC compared to 24.9 percent for placebo plus BSC.

That same month, Merck and Eisai announced the publication of results from the Phase III KEYNOTE-775/Study 309 trial evaluating the combination of Keytruda plus Lenvima, versus chemotherapy (treatment of physician’s choice of doxorubicin or paclitaxel) for patients with advanced endometrial carcinoma following at least one prior platinum-based regimen in any setting. Results showed that the Keytruda plus Lenvima combination demonstrated statistically significant improvements in the dual primary endpoints of overall survival and progression-free survival compared to chemotherapy.

In March, FDA approved Keytruda as a single agent for the treatment of patients with advanced endometrial carcinoma that is microsatellite instability-high (MSI-H) or mismatch repair deficient (dMMR), as determined by an FDA-approved test, who have disease progression following prior systemic therapy in any setting and are not candidates for curative surgery or radiation. The approval was based on new data from Cohorts D and K of the KEYNOTE-158 trial. The objective response rate was 46 percent for patients who received Keytruda, including a complete response rate of 12 percent and a partial response rate of 33 percent, at a median follow-up time of 16.0 months. Of the responding patients, 68 percent had responses lasting 12 months or longer, and 44 percent had responses lasting 24 months or longer. Median duration of response was not reached.

Additionally in March, Merck announced results from the pivotal Phase III KEYNOTE-091 trial, also known as EORTC-1416-LCG/ETOP-8-15 – PEARLS. The study found that adjuvant treatment with Keytruda significantly improved disease-free survival, one of the dual primary endpoints, reducing the risk of disease recurrence or death by 24 percent compared to placebo in patients with stage IB (≥4 centimeters) to IIIA non-small cell lung cancer following surgical resection regardless of PD-L1 expression. Median DFS was 53.6 months for Keytruda versus 42.0 months for placebo, an improvement of nearly one year.

There was also an improvement in DFS for patients whose tumors express PD-L1 (tumor proportion score [TPS] ≥50%) treated with Keytruda compared to placebo, the other dual primary endpoint; these results did not reach statistical significance per the pre-specified statistical plan. Among these patients, median DFS was not reached in either arm. Additionally, a favorable trend in overall survival, a key secondary endpoint, was observed for Keytruda versus placebo regardless of PD-L1 expression; these OS data were not mature and did not reach statistical significance at the time of this interim analysis. The trial will continue to evaluate DFS in patients whose tumors express high levels of PD-L1 (TPS ≥50%) and OS.

Lynparza is looking to crack the blockbuster barrier for the first time for Merck in 2022 as the drug earned a new approval in breast cancer from the FDA in March.

That same month, Merck stopped the Phase III KEYLYNK-010 trial investigating Keytruda in combination with Lynparza for the treatment of patients with metastatic castration-resistant prostate cancer who progressed after treatment with chemotherapy and either abiraterone acetate or enzalutamide. Merck discontinued the study following the recommendation of an independent Data Monitoring Committee after the DMC reviewed data from a planned interim analysis. At the interim analysis, the combination of Keytruda and Lynparza did not demonstrate a benefit in overall survival, one of the study’s dual primary endpoints, compared to the control arm of either abiraterone acetate or enzalutamide. The trial’s other dual primary endpoint, radiographic progression free survival, was evaluated at an earlier interim analysis and did not demonstrate improvement compared to the control arm.

In April, the European Commission approved Keytruda as monotherapy for the treatment of microsatellite instability-high (MSI-H) or deficient mismatch repair (dMMR) tumors in adults with unresectable or metastatic colorectal cancer after previous

fluoropyrimidine-based combination therapy; advanced or recurrent endometrial carcinoma, who have disease progression on or following prior treatment with a platinum-containing therapy in any setting and who are not candidates for curative surgery or radiation; unresectable or metastatic gastric, small intestine or biliary cancer, who have disease progression on or following at least one prior therapy.

The approvals were based on data from KEYNOTE-164 (NCT02460198) and KEYNOTE-158 (NCT02628067), multicenter, non-randomized, open-label Phase II trials evaluating Keytruda in patients with advanced MSI-H or dMMR solid tumors. In colorectal cancer, the ORR was 34 percent, including a complete response rate of 10 percent and a partial response rate of 24 percent, at a median follow-up time of 37.3 months. Median DOR was not reached, and of responding patients, 92 percent had responses lasting at least three years.

In endometrial cancer, the ORR was 51 percent, including a CR rate of 16 percent and a PR rate of 35 percent, at a median follow-up time of 21.9 months. Median DOR was not reached, and of responding patients, 85 percent had responses lasting at least one year, and 60 percent had responses lasting at least three years.

In gastric cancer, the ORR was 37 percent, including a CR rate of 14 percent and a PR rate of 24 percent, at a median follow-up time of 13.9 months. Median DOR was not reached, and of responding patients, 90 percent had responses lasting at least one year, and 81 percent had responses lasting at least three years.

In small intestine cancer, the ORR was 56 percent, including a CR rate of 15 percent and a PR rate of 41 percent, at a median follow-up time of 29.1 months. Median DOR was not reached, and of responding patients, 93 percent had responses lasting at least one year, and 73 percent had responses lasting at least three years.

In biliary cancer, the ORR was 41 percent, including a CR rate of 14 percent and a PR rate of 27 percent, at a median follow-up time of 19.4 months. Median DOR was 30.6 months, and of responding patients, 89 percent had responses lasting at least one year, and 42 percent had responses lasting at least three years.

Also in April, the European Commission approved Keytruda in combination with chemotherapy, with or without bevacizumab, for the treatment of persistent, recurrent or metastatic cervical cancer in adults whose tumors express PD-L1 (Combined Positive Score [CPS] ≥1). This approval was based on results from the Phase III KEYNOTE-826 trial, in which Keytruda plus chemotherapy with or without bevacizumab demonstrated a statistically significant improvement in overall survival and progression-free survival compared to chemotherapy with or without bevacizumab in this patient population. Additionally, more patients responded to the Keytruda regimen, with an objective response rate of 68 percent versus 50 percent, respectively.

In the KEYNOTE-826 trial, median OS in patients whose tumors express PD-L1 CPS ≥1 was not reached for the Keytruda regimen versus 16.3 months for the chemotherapy regimen. Median PFS in patients whose tumors express PD-L1 CPS ≥1 was 10.4 months for the Keytruda regimen versus 8.2 months for the chemotherapy regimen. The ORR in patients whose tumors express PD-L1 CPS ≥1 was 68 percent, including a complete response rate of 23 percent and a partial response rate of 45 percent for patients receiving the Keytruda regimen versus 50 percent, including a CR rate of 13 percent and a PR rate of 37 percent for patients receiving the chemotherapy regimen.

In May, the European Commission approved Keytruda in combination with chemotherapy as neoadjuvant treatment, and then continued as monotherapy as adjuvant treatment after surgery for adults with locally advanced or early-stage triple-negative breast cancer (TNBC) at high risk of recurrence. The approval was based on results from the pivotal Phase III KEYNOTE-522 trial, in which Keytruda in combination with chemotherapy before surgery and continued as a single agent after surgery prolonged event-free survival, reducing the risk of EFS events or death by 37 percent compared to neoadjuvant chemotherapy alone in this patient population. Median follow-up time for all patients was 37.8 months. KEYNOTE-522 was the first large, randomized Phase III study to report a statistically significant and clinically meaningful EFS result among patients with stage II and III TNBC. With this decision, this Keytruda combination became the first immunotherapy option approved for patients in the European Union in this setting.

In June, the European Commission approved Keytruda as monotherapy for the adjuvant treatment of adults and adolescents aged 12 years and older with stage IIB or IIC melanoma and who have undergone complete resection. Additionally, the EC approved expanding the indications for Keytruda in advanced (unresectable or metastatic) melanoma and stage III melanoma (as adjuvant treatment following complete resection) to include adolescent patients aged 12 years and older.

The approval of Keytruda for the adjuvant treatment of patients with resected stage IIB or IIC melanoma was based on results from the Phase III KEYNOTE-716 trial, in which Keytruda significantly prolonged recurrence-free survival, reducing the risk of disease recurrence or death by 39 percent compared to placebo in this patient population at a median follow-up of 20.5 months. Keytruda in this adjuvant setting also significantly prolonged distant metastasis-free survival, reducing the risk of distant metastasis by 36 percent compared to placebo in this patient population at a median follow-up of 26.9 months.

In July, Merck announced that the Phase III KEYNOTE-412 trial evaluating Keytruda with concurrent chemoradiation therapy (CRT) followed by Keytruda as maintenance therapy (the Keytruda regimen), did not meet its primary endpoint of event-free survival for the treatment of patients with unresected locally advanced head and neck squamous cell carcinoma. At the final analysis of the study, there was an improvement in EFS for patients who received the Keytruda regimen compared to placebo plus CRT; however, these results did not meet statistical significance per the pre-specified statistical plan.

In August, Merck and Eisai announced that the Phase III LEAP-002 trial investigating Keytruda plus Lenvima versus Lenvima monotherapy did not meet its dual primary endpoints of overall survival and progression-free survival as a first-line treatment for patients with unresectable hepatocellular carcinoma (uHCC). There were trends toward improvement in OS and PFS for patients who received Keytruda plus Lenvima versus Lenvima monotherapy; however, these results did not meet statistical significance per the pre-specified statistical plan. The median OS of the Lenvima monotherapy arm in LEAP-002 was longer than that observed in previously reported clinical trials evaluating Lenvima monotherapy in uHCC. Merck and Eisai are studying the Keytruda plus Lenvima combination through the LEAP (LEnvatinib And Pembrolizumab) clinical program in more than 10 different tumor types (endometrial carcinoma, hepatocellular carcinoma, melanoma, non-small cell lung cancer, renal cell carcinoma, head and neck cancer, biliary tract cancer, colorectal cancer, gastric cancer, esophageal cancer, glioblastoma, and pancreatic cancer) across more than 15 clinical trials.

Also in August, Merck announced that the Phase III KEYNOTE-921 trial evaluating Keytruda in combination with chemotherapy (docetaxel) compared to chemotherapy alone did not meet its dual primary endpoints of overall survival and radiographic progression-free survival for the treatment of patients with metastatic castration-resistant prostate cancer (mCRPC). In the study, there were modest trends toward an improvement in both OS and rPFS for patients who received Keytruda plus chemotherapy compared with chemotherapy alone; however, these results did not meet statistical significance per the pre-specified statistical plan.

Gardasil sales rose by 44.1 percent to $5.67 billion in 2021, driven primarily by strong global demand, particularly in China.

The HPV vaccine Gardasil brought in $5.67 billion in sales for Merck in 2021, enjoying impressive growth of 44.1 percent. According to company leaders, this was driven primarily by strong global demand, particularly in China, as well as increased supply. Higher pricing in China and the United States also contributed to sales growth in 2021. In the first half of 2022, sales of Gardasil were up another 45.7 percent to $3.13 billion.

Sales of the type 2 diabetes products Januvia and Janumet were both relatively flat in 2021, with Januvia up 0.5 percent to $3.32 billion and Janumet down 0.4 percent to $1.96 billion. Merck leaders say this reflected continued pricing pressure and lower demand in the United States, largely offset by higher demand in certain international markets, particularly in China. Januvia and Janumet were set to lose market exclusivity in the United States in January 2023, in the EU in September 2022, and in China in July 2022. In the first half of 2022, Januvia sales fell 3.6 percent to $1.54 billion, while sales of Janumet declined 3.2 percent to $931 million.

Merck’s ProQuad/MMR II/Varivax family of vaccines generated sales of $2.14 billion in 2021, an improvement of 13.7 percent over the previous year. According to company executives, this was due to higher sales in the United States reflecting higher demand driven by the ongoing COVID-19 pandemic recovery, as well as higher pricing. In the first half of 2022, ProQuad/MMR II/Varivax sales rose another 8.5 percent to $1.05 billion.

The neuromuscular blocking agent reversal drug Bridion brought in sales of $1.53 billion in 2021, up 27.9 percent compared with 2020. Merck leaders said this was due to higher demand globally, particularly in the United States and Europe, attributable to the COVID-19 pandemic recovery, as well as increased usage of neuromuscular blockade reversal agents and Bridion’s growing share within the class. Bridion was also approved by FDA in June 2021 for pediatric patients aged 2 years and older undergoing surgery. First-half 2022 Bridion sales were up by another 12.9 percent to $821 million.

Developed and marketed in partnership with AstraZeneca, the oncologic Lynparza generated sales of $989 million for Merck in 2021, enjoying growth of 36.4 percent. Company executives say this was due to continued uptake across the multiple approved indications in the United States, Europe, Japan, and China. In the first half of 2022 Lynparza sales rose another 13.9 percent to $541 million.

In March, the FDA approved Lynparza for the adjuvant treatment of adult patients with deleterious or suspected deleterious germline BRCA-mutated (gBRCAm), human epidermal growth factor receptor 2 (HER2)-negative high-risk early breast cancer who have been treated with neoadjuvant or adjuvant chemotherapy. The approval was based on results from the Phase III OlympiA trial, including data for the trial’s primary endpoint of invasive disease-free survival. In the OlympiA trial, Lynparza demonstrated a statistically significant improvement in IDFS, reducing the risk of invasive breast cancer recurrences, second cancers, or death by 42 percent versus placebo. Updated results from the OlympiA trial showed Lynparza reduced the risk of death by 32 percent versus placebo, a statistically significant improvement in OS, a key secondary endpoint. The European Commission subsequently approved Lynparza for a similar indication in August.

In August, the FDA accepted and granted priority review to an sNDA for Lynparza in combination with abiraterone and prednisone or prednisolone for the treatment of adult patients with metastatic castration-resistant prostate cancer. The sNDA was based on results from the Phase III PROpel trial. In PROpel, Lynparza in combination with abiraterone and prednisone or prednisolone reduced the risk of disease progression or death by 34 percent versus placebo plus abiraterone and prednisone or prednisolone. Median radiographic progression-free survival was 24.8 months for the Lynparza plus abiraterone arm versus 16.6 months for the placebo plus abiraterone arm.

In September, AstraZeneca and Merck announced long-term follow-up results from the Phase III PAOLA-1 and SOLO-1 trials in first-line advanced ovarian cancer, which represent the longest-term data for any PARP inhibitor in this setting. The Phase III PAOLA-1 trial evaluated Lynparza in combination with bevacizumab as first-line maintenance therapy in patients with advanced ovarian cancer, who were without evidence of disease after surgery or following response to platinum-based chemotherapy. Final overall survival, a key secondary endpoint, in those who received Lynparza plus bevacizumab was 56.5 months versus 51.6 months with bevacizumab alone in patients with newly diagnosed advanced ovarian cancer. These OS results were not statistically significant.

In an exploratory subgroup analysis of HRD-positive patients, Lynparza plus bevacizumab provided a clinically meaningful improvement in OS, reducing the risk of death by 38 percent versus bevacizumab alone. Reportedly, 65.5 percent of patients who received Lynparza plus bevacizumab were still alive at five years versus 48.4 percent who received bevacizumab alone. Lynparza plus bevacizumab also improved median progression-free survival to nearly four years (46.8 months) versus 17.6 months with bevacizumab plus placebo, and 46.1 percent of patients who received Lynparza in combination with bevacizumab remain progression free versus 19.2 percent of patients who received bevacizumab alone. The safety and tolerability profile of Lynparza in this trial was in line with that observed in prior clinical trials, with no new safety signals. Adverse events of special interest for Lynparza in combination with bevacizumab versus bevacizumab alone included myelodysplastic syndrome/acute myeloid leukemia/aplastic anemia (1.7 percent versus 2.2 percent), new primary malignancies (4.1 percent versus 3.0 percent) and pneumonitis/interstitial lung disease/bronchiolitis (1.3 percent versus 0.7 percent).

The Phase III SOLO-1 trial evaluated Lynparza as monotherapy as first-line maintenance therapy in patients with advanced ovarian cancer, who were without evidence of disease after surgery or following response to platinum-based chemotherapy. In the trial, Lynparza demonstrated a clinically meaningful improvement in OS versus placebo in patients with germline BRCA-mutated (gBRCAm) newly diagnosed advanced ovarian cancer, reducing the risk of death by 45 percent versus placebo (not statistically significant). Median OS was not reached with Lynparza versus 75.2 months with placebo. At the seven-year descriptive OS analysis, 67 percent of Lynparza patients were alive versus 47 percent of placebo patients (44 percent of whom had a subsequent PARP inhibitor), and 45 percent of Lynparza patients versus 21 percent of placebo patients were alive and had not received a first subsequent treatment. Additional data showed median time to first subsequent therapy (TFST) was 64.0 months with Lynparza versus 15.1 months with placebo.

The Merck/Ridgeback COVID drug Lagevrio went from zero to about $5.37 billion in sales from December 2021 through June 2022.

The COVID treatment molnupiravir, now known as Lagevrio, received an emergency use authorization from FDA in December 2021 and managed to generate $952 million in sales for Merck through the end of the year from a standing start. In the first half of 2022, sales of Lagevrio totaled $4.42 billion, pushing it quickly to second in sales in Merck’s entire portfolio.

In April, Merck and partner developer Ridgeback Biotherapeutics announced final analyses evaluating virologic outcomes throughout and following a five-day course of Lagevrio as part of the Phase III MOVe-OUT trial, which studied Lagevrio versus placebo for the treatment of COVID-19 in non-hospitalized adults with mild-to-moderate COVID-19 who were at high risk for progressing to severe disease. In participants with infectious virus isolated at baseline and for whom post-baseline infectivity data were available, Lagevrio was associated with more rapid elimination of infectious virus than placebo. At Day 3 of treatment, among patients with infectious virus at baseline, infectious SARS-CoV-2 was detected in 0.0 percent of patients who received Lagevrio, compared with 20.8 percent of patients who received placebo. At Day 5, infectious virus was detected in 0.0 percent of patients in the Lagevrio arm compared with 2.2 percent in the placebo arm. At Day 10, no infectious virus was detected in either arm for patients with infectious virus at baseline. Lagevrio was also associated with greater mean reductions from baseline in SARS-CoV-2 RNA than placebo from Days 3 through 10, though Lagevrio and placebo were associated with comparable rates of viral RNA clearance through Day 29.

In June, Merck and Ridgeback announced additional data from the Phase III MOVe-OUT trial evaluating Lagevrio in non-hospitalized adults with mild-to-moderate COVID-19 who were at high risk for progressing to severe disease. Analyses of pre-specified exploratory endpoints indicate that a lower proportion of Lagevrio-treated participants in the modified intent-to-treat (MITT) population had an acute care visit or a COVID-19-related acute care visit versus placebo-treated participants in the MITT population: 7.2 percent of participants who received Lagevrio reported an acute care visit through Day 29, versus 10.6 percent of placebo participants, with a relative risk reduction of 32.1 percent; 6.6 percent of participants who received Lagevrio reported a COVID-19-related acute care visit, versus 10.0 percent of placebo participants, with a RRR of 33.8 percent.

Based on a post hoc analysis, fewer Lagevrio-treated participants in the MITT population required respiratory interventions (including conventional oxygen therapy, a high-flow heated and humidified device, noninvasive mechanical ventilation, or invasive mechanical ventilation) versus placebo-treated participants, with a RRR of 34.3 percent for all respiratory interventions. Based on additional post hoc analyses, participants in the safety population who received Lagevrio showed earlier and larger reductions in mean C-reactive protein (CRP) values, and earlier and larger improvements in mean change from baseline oxygen saturation (SpO2) values, compared with participants who received placebo. The safety population consisted of all participants who had undergone randomization and had received at least one dose of Lagevrio.

Post hoc analyses also suggest that among the subgroup of participants who were hospitalized after randomization in MOVe-OUT, the median time to hospital discharge was nine days for participants who received Lagevrio, versus 12 days in the placebo group. Consistent with the full MITT population data, post hoc analyses also suggest that fewer Lagevrio-treated participants who were hospitalized after randomization required respiratory interventions versus placebo-treated participants, with a RRR of 21.3 percent for all respiratory interventions.

Sales of the oncologic Lenvima rose 21.4 percent in 2021 to $704 million.

Being developed as part of a collaboration with Eisai, the oncologic Lenvima produced $704 million in sales for Merck in 2021, an improvement of 21.4 percent. Company leaders credited this to higher demand in the United States and China. In the first half of 2022, Lenvima sales rose another 48.1 percent to $459 million.

In the pipeline

In January, the FDA issued a Complete Response Letter regarding Merck’s New Drug Application for gefapixant, an investigational, non-narcotic, orally administered selective P2X3 receptor antagonist, under development for the treatment of refractory chronic cough or unexplained chronic cough in adults. In the CRL, FDA requested additional information related to measurement of efficacy. The CRL was not related to the safety of gefapixant.

In March, Merck announced the presentation of findings from a systematic literature review and meta-analysis of data from real-world observational studies of Prevymis for primary prophylaxis of cytomegalovirus infection and disease in patients undergoing allogeneic hematopoietic cell transplantation (alloHCT) who were CMV-seropositive. In the analysis of 48 real-world observational studies, compared to controls (mostly preemptive therapy), primary prophylaxis with Prevymis was associated at 100 days of follow-up after alloHCT with 87 percent lower odds of CMV reactivation; 91 percent lower odds for clinically significant CMV infection; 69 percent lower odds of CMV disease; 94 percent lower odds of CMV-related hospitalization; and 48 percent lower odds of Grade 2 or greater graft versus host disease. Consistent results were observed at 200 days of follow-up with respect to CMV reactivation, clinically significant CMV infection, and CMV disease.

In June, FDA approved an expanded indication for Vaxneuvance to include children 6 weeks through 17 years of age. Vaxneuvance is now indicated for active immunization for the prevention of invasive disease caused by Streptococcus pneumoniae serotypes 1, 3, 4, 5, 6A, 6B, 7F, 9V, 14, 18C, 19A, 19F, 22F, 23F and 33F in individuals 6 weeks of age and older.

FDA’s approval was based on data from seven randomized, double-blind clinical studies assessing safety, tolerability and immunogenicity of Vaxneuvance in infants, children, and adolescents. Clinical data from the pivotal study showed that immune responses elicited by Vaxneuvance following a four-dose pediatric series were non-inferior to the currently available 13-valent pneumococcal conjugate vaccine (PCV13) for the 13 shared serotypes based on serotype-specific immunoglobulin G (IgG) geometric mean concentrations (GMCs).

In a secondary analysis, immune responses for Vaxneuvance following a four-dose pediatric series were superior to PCV13 for shared serotype 3 and the two serotypes unique to Vaxneuvance, 22F and 33F. Randomized controlled trials assessing the clinical efficacy of Vaxneuvance compared to PCV13 have not been conducted. Data from the clinical program also support the use of Vaxneuvance concomitantly with other commonly administered routine pediatric vaccines, and in a variety of clinical settings, such as interchangeable use following initiation of an infant vaccination schedule with PCV13 or in a catch-up setting for older children who are either pneumococcal vaccine-naïve or who previously received an incomplete series of another PCV. Additionally, data support the use of Vaxneuvance in special populations, such as in preterm infants and children living with HIV infection or sickle cell disease.

In August, the FDA granted Fast Track designation for Merck’s investigational anticoagulant therapy MK-2060 for the reduction in risk of major thrombotic cardiovascular events in patients with end-stage renal disease. MK-2060 is an investigational monoclonal antibody designed to inhibit Factor XI and its ability to activate downstream proteins involved in the blood coagulation cascade. MK-2060 is being evaluated in a Phase II study for the treatment of patients with ESRD receiving hemodialysis.

emergency use authorization pandemic covid-19 vaccine treatment fda clinical trials preclinical genetic therapy rna recovery japan european europe eu chinaInternational

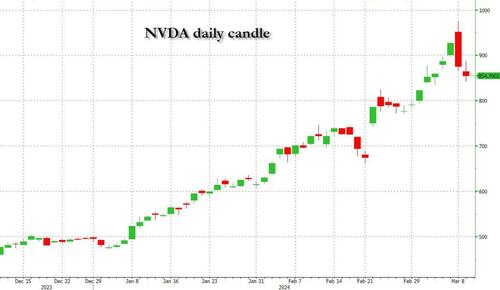

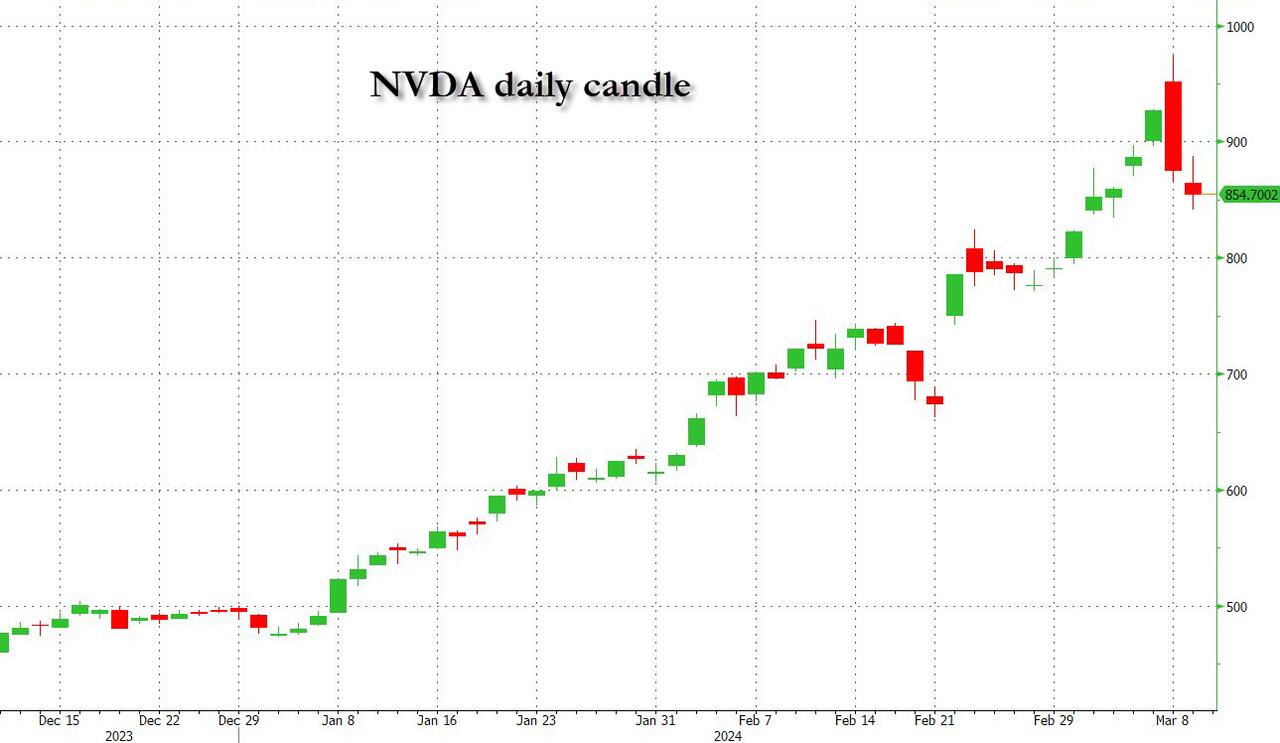

Red Candle In The Wind

Red Candle In The Wind

By Benjamin PIcton of Rabobank

February non-farm payrolls superficially exceeded market expectations on Friday by…

Share this:

By Benjamin PIcton of Rabobank

February non-farm payrolls superficially exceeded market expectations on Friday by printing at 275,000 against a consensus call of 200,000. We say superficially, because the downward revisions to prior months totalled 167,000 for December and January, taking the total change in employed persons well below the implied forecast, and helping the unemployment rate to pop two-ticks to 3.9%. The U6 underemployment rate also rose from 7.2% to 7.3%, while average hourly earnings growth fell to 0.2% m-o-m and average weekly hours worked languished at 34.3, equalling pre-pandemic lows.

Undeterred by the devil in the detail, the algos sprang into action once exchanges opened. Market darling NVIDIA hit a new intraday high of $974 before (presumably) the humans took over and sold the stock down more than 10% to close at $875.28. If our suspicions are correct that it was the AIs buying before the humans started selling (no doubt triggering trailing stops on the way down), the irony is not lost on us.

The 1-day chart for NVIDIA now makes for interesting viewing, because the red candle posted on Friday presents quite a strong bearish engulfing signal. Volume traded on the day was almost double the 15-day simple moving average, and similar price action is observable on the 1-day charts for both Intel and AMD. Regular readers will be aware that we have expressed incredulity in the past about the durability the AI thematic melt-up, so it will be interesting to see whether Friday’s sell off is just a profit-taking blip, or a genuine trend reversal.

AI equities aside, this week ought to be important for markets because the BTFP program expires today. That means that the Fed will no longer be loaning cash to the banking system in exchange for collateral pledged at-par. The KBW Regional Banking index has so far taken this in its stride and is trading 30% above the lows established during the mini banking crisis of this time last year, but the Fed’s liquidity facility was effectively an exercise in can-kicking that makes regional banks a sector of the market worth paying attention to in the weeks ahead. Even here in Sydney, regulators are warning of external risks posed to the banking sector from scheduled refinancing of commercial real estate loans following sharp falls in valuations.

Markets are sending signals in other sectors, too. Gold closed at a new record-high of $2178/oz on Friday after trading above $2200/oz briefly. Gold has been going ballistic since the Friday before last, posting gains even on days where 2-year Treasury yields have risen. Gold bugs are buying as real yields fall from the October highs and inflation breakevens creep higher. This is particularly interesting as gold ETFs have been recording net outflows; suggesting that price gains aren’t being driven by a retail pile-in. Are gold buyers now betting on a stagflationary outcome where the Fed cuts without inflation being anchored at the 2% target? The price action around the US CPI release tomorrow ought to be illuminating.

Leaving the day-to-day movements to one side, we are also seeing further signs of structural change at the macro level. The UK budget last week included a provision for the creation of a British ISA. That is, an Individual Savings Account that provides tax breaks to savers who invest their money in the stock of British companies. This follows moves last year to encourage pension funds to head up the risk curve by allocating 5% of their capital to unlisted investments.

As a Hail Mary option for a government cruising toward an electoral drubbing it’s a curious choice, but it’s worth highlighting as cash-strapped governments increasingly see private savings pools as a funding solution for their spending priorities.

Of course, the UK is not alone in making creeping moves towards financial repression. In contrast to announcements today of increased trade liberalisation, Australian Treasurer Jim Chalmers has in the recent past flagged his interest in tapping private pension savings to fund state spending priorities, including defence, public housing and renewable energy projects. Both the UK and Australia appear intent on finding ways to open up the lungs of their economies, but government wants more say in directing private capital flows for state goals.

So, how far is the blurring of the lines between free markets and state planning likely to go? Given the immense and varied budgetary (and security) pressures that governments are facing, could we see a re-up of WWII-era Victory bonds, where private investors are encouraged to do their patriotic duty by directly financing government at negative real rates?

That would really light a fire under the gold market.

Spread & Containment

Fauci Deputy Warned Him Against Vaccine Mandates: Email

Fauci Deputy Warned Him Against Vaccine Mandates: Email

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

Mandating COVID-19…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

Mandating COVID-19 vaccination was a mistake due to ethical and other concerns, a top government doctor warned Dr. Anthony Fauci after Dr. Fauci promoted mass vaccination.

“Coercing or forcing people to take a vaccine can have negative consequences from a biological, sociological, psychological, economical, and ethical standpoint and is not worth the cost even if the vaccine is 100% safe,” Dr. Matthew Memoli, director of the Laboratory of Infectious Diseases clinical studies unit at the U.S. National Institute of Allergy and Infectious Diseases (NIAID), told Dr. Fauci in an email.

“A more prudent approach that considers these issues would be to focus our efforts on those at high risk of severe disease and death, such as the elderly and obese, and do not push vaccination on the young and healthy any further.”

Employing that strategy would help prevent loss of public trust and political capital, Dr. Memoli said.

The email was sent on July 30, 2021, after Dr. Fauci, director of the NIAID, claimed that communities would be safer if more people received one of the COVID-19 vaccines and that mass vaccination would lead to the end of the COVID-19 pandemic.

“We’re on a really good track now to really crush this outbreak, and the more people we get vaccinated, the more assuredness that we’re going to have that we’re going to be able to do that,” Dr. Fauci said on CNN the month prior.

Dr. Memoli, who has studied influenza vaccination for years, disagreed, telling Dr. Fauci that research in the field has indicated yearly shots sometimes drive the evolution of influenza.

Vaccinating people who have not been infected with COVID-19, he said, could potentially impact the evolution of the virus that causes COVID-19 in unexpected ways.

“At best what we are doing with mandated mass vaccination does nothing and the variants emerge evading immunity anyway as they would have without the vaccine,” Dr. Memoli wrote. “At worst it drives evolution of the virus in a way that is different from nature and possibly detrimental, prolonging the pandemic or causing more morbidity and mortality than it should.”

The vaccination strategy was flawed because it relied on a single antigen, introducing immunity that only lasted for a certain period of time, Dr. Memoli said. When the immunity weakened, the virus was given an opportunity to evolve.

Some other experts, including virologist Geert Vanden Bossche, have offered similar views. Others in the scientific community, such as U.S. Centers for Disease Control and Prevention scientists, say vaccination prevents virus evolution, though the agency has acknowledged it doesn’t have records supporting its position.

Other Messages

Dr. Memoli sent the email to Dr. Fauci and two other top NIAID officials, Drs. Hugh Auchincloss and Clifford Lane. The message was first reported by the Wall Street Journal, though the publication did not publish the message. The Epoch Times obtained the email and 199 other pages of Dr. Memoli’s emails through a Freedom of Information Act request. There were no indications that Dr. Fauci ever responded to Dr. Memoli.

Later in 2021, the NIAID’s parent agency, the U.S. National Institutes of Health (NIH), and all other federal government agencies began requiring COVID-19 vaccination, under direction from President Joe Biden.

In other messages, Dr. Memoli said the mandates were unethical and that he was hopeful legal cases brought against the mandates would ultimately let people “make their own healthcare decisions.”

“I am certainly doing everything in my power to influence that,” he wrote on Nov. 2, 2021, to an unknown recipient. Dr. Memoli also disclosed that both he and his wife had applied for exemptions from the mandates imposed by the NIH and his wife’s employer. While her request had been granted, his had not as of yet, Dr. Memoli said. It’s not clear if it ever was.

According to Dr. Memoli, officials had not gone over the bioethics of the mandates. He wrote to the NIH’s Department of Bioethics, pointing out that the protection from the vaccines waned over time, that the shots can cause serious health issues such as myocarditis, or heart inflammation, and that vaccinated people were just as likely to spread COVID-19 as unvaccinated people.

He cited multiple studies in his emails, including one that found a resurgence of COVID-19 cases in a California health care system despite a high rate of vaccination and another that showed transmission rates were similar among the vaccinated and unvaccinated.

Dr. Memoli said he was “particularly interested in the bioethics of a mandate when the vaccine doesn’t have the ability to stop spread of the disease, which is the purpose of the mandate.”

The message led to Dr. Memoli speaking during an NIH event in December 2021, several weeks after he went public with his concerns about mandating vaccines.

“Vaccine mandates should be rare and considered only with a strong justification,” Dr. Memoli said in the debate. He suggested that the justification was not there for COVID-19 vaccines, given their fleeting effectiveness.

Julie Ledgerwood, another NIAID official who also spoke at the event, said that the vaccines were highly effective and that the side effects that had been detected were not significant. She did acknowledge that vaccinated people needed boosters after a period of time.

The NIH, and many other government agencies, removed their mandates in 2023 with the end of the COVID-19 public health emergency.

A request for comment from Dr. Fauci was not returned. Dr. Memoli told The Epoch Times in an email he was “happy to answer any questions you have” but that he needed clearance from the NIAID’s media office. That office then refused to give clearance.

Dr. Jay Bhattacharya, a professor of health policy at Stanford University, said that Dr. Memoli showed bravery when he warned Dr. Fauci against mandates.

“Those mandates have done more to demolish public trust in public health than any single action by public health officials in my professional career, including diminishing public trust in all vaccines.” Dr. Bhattacharya, a frequent critic of the U.S. response to COVID-19, told The Epoch Times via email. “It was risky for Dr. Memoli to speak publicly since he works at the NIH, and the culture of the NIH punishes those who cross powerful scientific bureaucrats like Dr. Fauci or his former boss, Dr. Francis Collins.”

Government

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

Trump "Clearly Hasn’t Learned From His COVID-Era Mistakes", RFK Jr. Says

Authored by Jeff Louderback via The Epoch Times (emphasis ours),

President…

Share this:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Authored by Jeff Louderback via The Epoch Times (emphasis ours),

President Joe Biden claimed that COVID vaccines are now helping cancer patients during his State of the Union address on March 7, but it was a response on Truth Social from former President Donald Trump that drew the ire of independent presidential candidate Robert F. Kennedy Jr.

{kind=link}

During the address, President Biden said: “The pandemic no longer controls our lives. The vaccines that saved us from COVID are now being used to help beat cancer, turning setback into comeback. That’s what America does.”

President Trump wrote: “The Pandemic no longer controls our lives. The VACCINES that saved us from COVID are now being used to help beat cancer—turning setback into comeback. YOU’RE WELCOME JOE. NINE-MONTH APPROVAL TIME VS. 12 YEARS THAT IT WOULD HAVE TAKEN YOU.”

An outspoken critic of President Trump’s COVID response, and the Operation Warp Speed program that escalated the availability of COVID vaccines, Mr. Kennedy said on X, formerly known as Twitter, that “Donald Trump clearly hasn’t learned from his COVID-era mistakes.”

“He fails to recognize how ineffective his warp speed vaccine is as the ninth shot is being recommended to seniors. Even more troubling is the documented harm being caused by the shot to so many innocent children and adults who are suffering myocarditis, pericarditis, and brain inflammation,” Mr. Kennedy remarked.

“This has been confirmed by a CDC-funded study of 99 million people. Instead of bragging about its speedy approval, we should be honestly and transparently debating the abundant evidence that this vaccine may have caused more harm than good.

“I look forward to debating both Trump and Biden on Sept. 16 in San Marcos, Texas.”

Mr. Kennedy announced in April 2023 that he would challenge President Biden for the 2024 Democratic Party presidential nomination before declaring his run as an independent last October, claiming that the Democrat National Committee was “rigging the primary.”

Since the early stages of his campaign, Mr. Kennedy has generated more support than pundits expected from conservatives, moderates, and independents resulting in speculation that he could take votes away from President Trump.

Many Republicans continue to seek a reckoning over the government-imposed pandemic lockdowns and vaccine mandates.

President Trump’s defense of Operation Warp Speed, the program he rolled out in May 2020 to spur the development and distribution of COVID-19 vaccines amid the pandemic, remains a sticking point for some of his supporters.

Operation Warp Speed featured a partnership between the government, the military, and the private sector, with the government paying for millions of vaccine doses to be produced.

President Trump released a statement in March 2021 saying: “I hope everyone remembers when they’re getting the COVID-19 Vaccine, that if I wasn’t President, you wouldn’t be getting that beautiful ‘shot’ for 5 years, at best, and probably wouldn’t be getting it at all. I hope everyone remembers!”

President Trump said about the COVID-19 vaccine in an interview on Fox News in March 2021: “It works incredibly well. Ninety-five percent, maybe even more than that. I would recommend it, and I would recommend it to a lot of people that don’t want to get it and a lot of those people voted for me, frankly.

“But again, we have our freedoms and we have to live by that and I agree with that also. But it’s a great vaccine, it’s a safe vaccine, and it’s something that works.”

On many occasions, President Trump has said that he is not in favor of vaccine mandates.

An environmental attorney, Mr. Kennedy founded Children’s Health Defense, a nonprofit that aims to end childhood health epidemics by promoting vaccine safeguards, among other initiatives.

Last year, Mr. Kennedy told podcaster Joe Rogan that ivermectin was suppressed by the FDA so that the COVID-19 vaccines could be granted emergency use authorization.

He has criticized Big Pharma, vaccine safety, and government mandates for years.

Since launching his presidential campaign, Mr. Kennedy has made his stances on the COVID-19 vaccines, and vaccines in general, a frequent talking point.

“I would argue that the science is very clear right now that they [vaccines] caused a lot more problems than they averted,” Mr. Kennedy said on Piers Morgan Uncensored last April.

“And if you look at the countries that did not vaccinate, they had the lowest death rates, they had the lowest COVID and infection rates.”

Additional data show a “direct correlation” between excess deaths and high vaccination rates in developed countries, he said.

President Trump and Mr. Kennedy have similar views on topics like protecting the U.S.-Mexico border and ending the Russia-Ukraine war.

COVID-19 is the topic where Mr. Kennedy and President Trump seem to differ the most.

Former President Donald Trump intended to “drain the swamp” when he took office in 2017, but he was “intimidated by bureaucrats” at federal agencies and did not accomplish that objective, Mr. Kennedy said on Feb. 5.

Speaking at a voter rally in Tucson, where he collected signatures to get on the Arizona ballot, the independent presidential candidate said President Trump was “earnest” when he vowed to “drain the swamp,” but it was “business as usual” during his term.

John Bolton, who President Trump appointed as a national security adviser, is “the template for a swamp creature,” Mr. Kennedy said.

Scott Gottlieb, who President Trump named to run the FDA, “was Pfizer’s business partner” and eventually returned to Pfizer, Mr. Kennedy said.

Mr. Kennedy said that President Trump had more lobbyists running federal agencies than any president in U.S. history.

“You can’t reform them when you’ve got the swamp creatures running them, and I’m not going to do that. I’m going to do something different,” Mr. Kennedy said.

During the COVID-19 pandemic, President Trump “did not ask the questions that he should have,” he believes.

President Trump “knew that lockdowns were wrong” and then “agreed to lockdowns,” Mr. Kennedy said.

He also “knew that hydroxychloroquine worked, he said it,” Mr. Kennedy explained, adding that he was eventually “rolled over” by Dr. Anthony Fauci and his advisers.

MaryJo Perry, a longtime advocate for vaccine choice and a Trump supporter, thinks votes will be at a premium come Election Day, particularly because the independent and third-party field is becoming more competitive.

Ms. Perry, president of Mississippi Parents for Vaccine Rights, believes advocates for medical freedom could determine who is ultimately president.

She believes that Mr. Kennedy is “pulling votes from Trump” because of the former president’s stance on the vaccines.

“People care about medical freedom. It’s an important issue here in Mississippi, and across the country,” Ms. Perry told The Epoch Times.

“Trump should admit he was wrong about Operation Warp Speed and that COVID vaccines have been dangerous. That would make a difference among people he has offended.”

President Trump won’t lose enough votes to Mr. Kennedy about Operation Warp Speed and COVID vaccines to have a significant impact on the election, Ohio Republican strategist Wes Farno told The Epoch Times.

President Trump won in Ohio by eight percentage points in both 2016 and 2020. The Ohio Republican Party endorsed President Trump for the nomination in 2024.

“The positives of a Trump presidency far outweigh the negatives,” Mr. Farno said. “People are more concerned about their wallet and the economy.

“They are asking themselves if they were better off during President Trump’s term compared to since President Biden took office. The answer to that question is obvious because many Americans are struggling to afford groceries, gas, mortgages, and rent payments.

“America needs President Trump.”

Multiple national polls back Mr. Farno’s view.

As of March 6, the RealClearPolitics average of polls indicates that President Trump has 41.8 percent support in a five-way race that includes President Biden (38.4 percent), Mr. Kennedy (12.7 percent), independent Cornel West (2.6 percent), and Green Party nominee Jill Stein (1.7 percent).

A Pew Research Center study conducted among 10,133 U.S. adults from Feb. 7 to Feb. 11 showed that Democrats and Democrat-leaning independents (42 percent) are more likely than Republicans and GOP-leaning independents (15 percent) to say they have received an updated COVID vaccine.

The poll also reported that just 28 percent of adults say they have received the updated COVID inoculation.

The peer-reviewed multinational study of more than 99 million vaccinated people that Mr. Kennedy referenced in his X post on March 7 was published in the Vaccine journal on Feb. 12.

It aimed to evaluate the risk of 13 adverse events of special interest (AESI) following COVID-19 vaccination. The AESIs spanned three categories—neurological, hematologic (blood), and cardiovascular.

The study reviewed data collected from more than 99 million vaccinated people from eight nations—Argentina, Australia, Canada, Denmark, Finland, France, New Zealand, and Scotland—looking at risks up to 42 days after getting the shots.

Three vaccines—Pfizer and Moderna’s mRNA vaccines as well as AstraZeneca’s viral vector jab—were examined in the study.

Researchers found higher-than-expected cases that they deemed met the threshold to be potential safety signals for multiple AESIs, including for Guillain-Barre syndrome (GBS), cerebral venous sinus thrombosis (CVST), myocarditis, and pericarditis.

A safety signal refers to information that could suggest a potential risk or harm that may be associated with a medical product.

The study identified higher incidences of neurological, cardiovascular, and blood disorder complications than what the researchers expected.

President Trump’s role in Operation Warp Speed, and his continued praise of the COVID vaccine, remains a concern for some voters, including those who still support him.

Krista Cobb is a 40-year-old mother in western Ohio. She voted for President Trump in 2020 and said she would cast her vote for him this November, but she was stunned when she saw his response to President Biden about the COVID-19 vaccine during the State of the Union address.

“I love President Trump and support his policies, but at this point, he has to know they [advisers and health officials] lied about the shot,” Ms. Cobb told The Epoch Times.

“If he continues to promote it, especially after all of the hearings they’ve had about it in Congress, the side effects, and cover-ups on Capitol Hill, at what point does he become the same as the people who have lied?” Ms. Cobb added.

“I think he should distance himself from talk about Operation Warp Speed and even admit that he was wrong—that the vaccines have not had the impact he was told they would have. If he did that, people would respect him even more.”

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Is the National Guard a solution to school violence?

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Red Candle In The Wind

The next pandemic? It’s already here for Earth’s wildlife

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

Mathematicians use AI to identify emerging COVID-19 variants

The Great Replacement Loophole: Illegal Immigrants Score 5-Year Work Benefit While “Waiting” For Deporation, Asylum

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

International4 days ago

International4 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International3 days ago

International3 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges