Government

Low to moderate-income families are losing ground: How to save their homeownership dreams

Widespread vaccinations and relaxed CDC restrictions have stimulated a robust economic rebound. Since the start of the pandemic, the U.S. unemployment rate declined dramatically from a peak of 14.8% to roughly 5.8% at the time of this writing. Employers..

Share this:

By Makada Henry-Nickie, Tim Lucas, Radha Seshagiri, Samantha Elizondo

Widespread vaccinations and relaxed CDC restrictions have stimulated a robust economic rebound. Since the start of the pandemic, the U.S. unemployment rate declined dramatically from a peak of 14.8% to roughly 5.8% at the time of this writing. Employers have added roughly 14.7 million jobs. Still, 9.3 million workers remain suspended in a state of joblessness and financial fragility, including low-to moderate-income-class families worried about preserving their homes.

For homeowners facing COVID-related hardships, the CARES Act’s mortgage forbearance protection has been a crucial lifeline: an unprecedented payment deferral program allowing struggling borrowers to delay or reduce their mortgage payments, creating an essential safe harbor that temporarily secured their claim to the American Dream. According to the Federal Reserve Bank of New York, forbearance plans disproportionately benefitted low-income borrowers, especially those holding FHA-insured loans or living in disadvantaged neighborhoods.

Despite evidence that many low-income borrowers remain in distress, this crucial policy shield will disappear on June 30 when the federal forbearance program is set to expire. This development has serious implications for the roughly 2.1 million borrowers still under the protective ambit of COVID forbearance programs. On the surface, steady increases in forbearance exits suggest that borrowers’ financial circumstances have improved. These national trends, however, mask significant financial weaknesses plaguing financially stressed households, and financial stress tends to be geographically and demographically concentrated among communities of color. The looming forbearance cliff threatens to expose millions of unemployed and underemployed homeowners to foreclosure, bankruptcy, or pressure to sell prematurely. These escape routes will undoubtedly exacerbate the racial wealth gap; each option represents a retreat from homeownership that communities of color are ill-prepared to absorb. Homeownership is integral to generational wealth creation, home equity is the largest component of asset-driven wealth for Black and Hispanic accounting for nearly 40% of their balance sheet on average

Policies aimed at stabilizing distressed communities should be informed by the well-being of COVID-impacted homeowners, not artificial deadlines. We partnered with SaverLife, a fintech non-profit, to explore the financial well-being of low- and moderate-income homeowners. Like Tenesha, who lives in Washington with two daughters. She has never missed a mortgage payment but worries about losing her home when her unemployment benefits end. This blog highlights the financial constraints and foreclosure fears among distressed borrowers and offers pointed recommendations to preserve their homes.

Upended households struggle to regain their footing

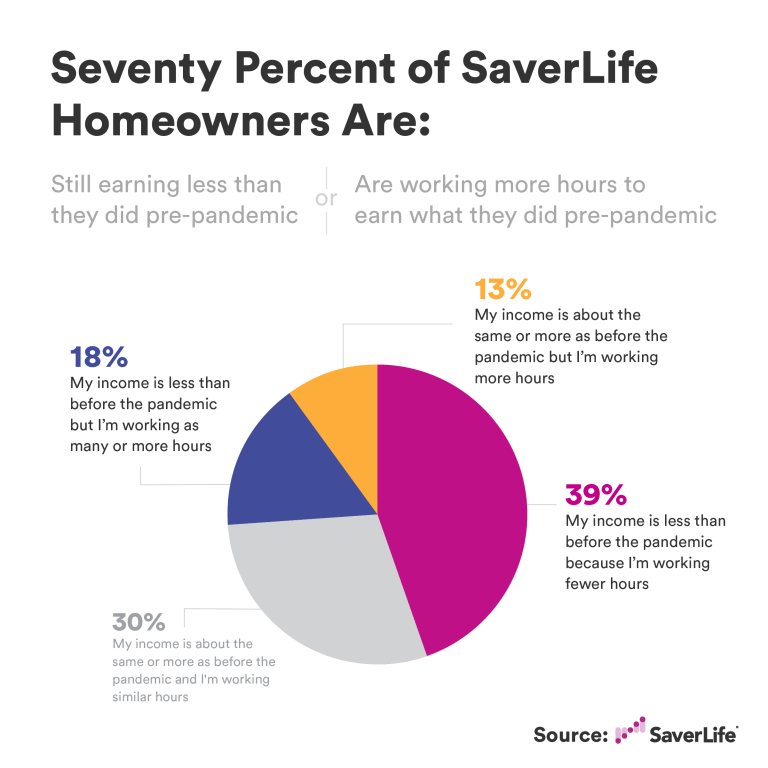

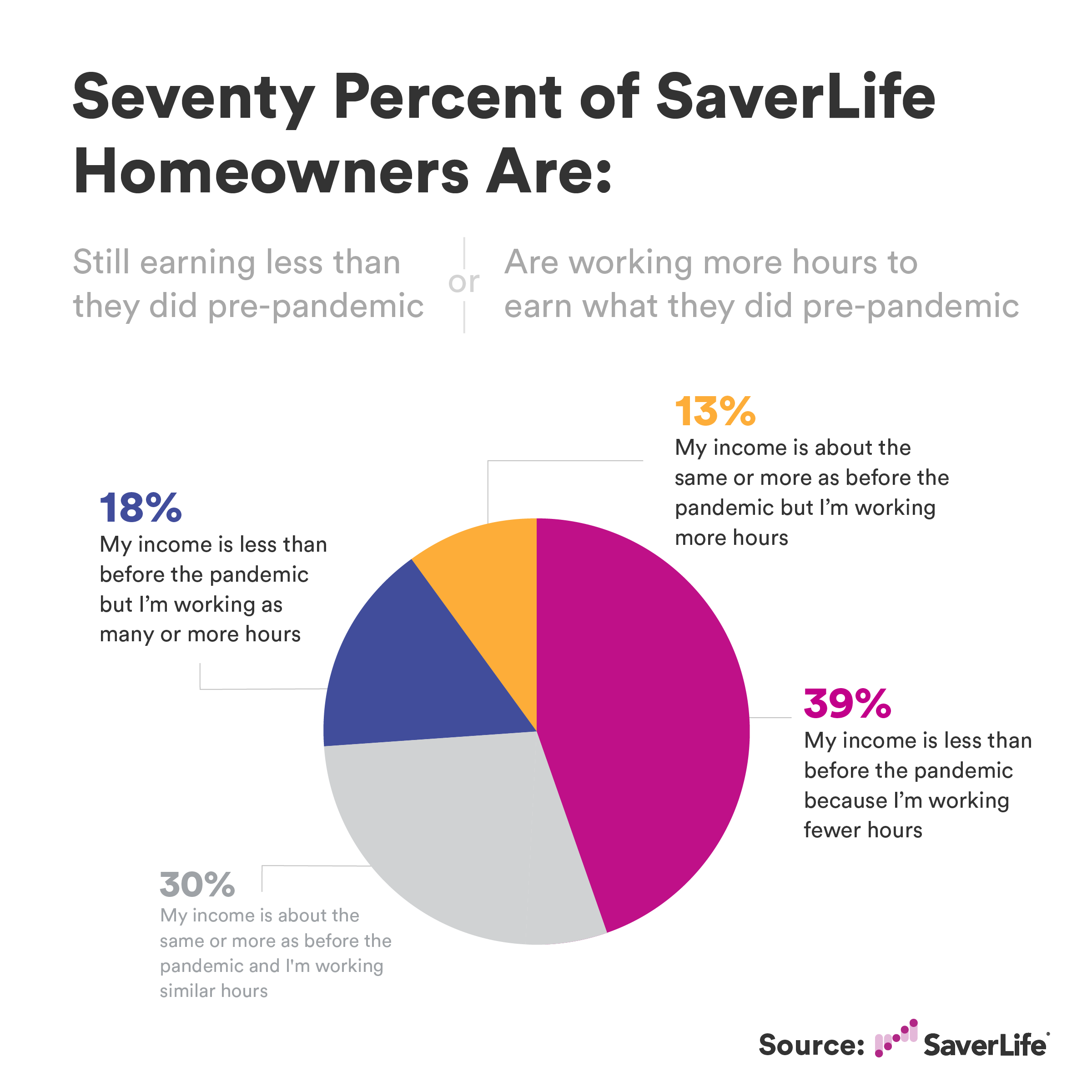

Homeowners hit hard by the pandemic are falling behind, with many struggling to find quality jobs that pay a living wage. Fifty-seven percent of respondents said their post-pandemic income declined. Of those who reported being employed, about 4 in 10 (39%) earned less income because they worked fewer hours. Another 18% reported working more hours but not earning enough to replace their pre-pandemic income. Notably, men were far more likely (23%) than women (11%) to report working more hours; this result is consistent with widespread reports on structural hurdles, such as disproportionate parental and elder care responsibilities, that continue to delay women’s return to the job market.

Tenesha lost her job as a server in March 2020 because her restaurant closed permanently. She’s still searching for work. The enormous financial burden facing this demographic is severe and possibly deeper than the barriers facing 37.5% of US adults, who, according to the Census Bureau’s Household Pulse Survey, experienced income declines.

The over-representation of minorities and women in SaverLife’s sample provides an important snapshot of the pronounced adversity facing homeowners of color. This real-time pulse check suggests that premature withdrawal of critical federal and state subsidies would exacerbate the hardships faced by communities of color and undermine recovery for other economically disadvantaged groups, including women and younger Americans.

Many homeowners were unaware of and missed the forbearance window

The CARES Act circumvented an epic housing instability crisis for both renters and homeowners. Since last spring, more than 6 million borrowers have sought payment relief through forbearance. Although forbearance provided millions of distressed borrowers with vital breathing room, a substantial share of COVID-impacted homeowners missed the chance to participate in a forbearance program.

Participation in forbearance plans was remarkably low—just 8% of respondents reported having received a forbearance plan. This rate is unexpectedly low given respondents’ reportedly high rate of income disruption and the trend of working longer hours to keep up. Michelle, a Wisconsin resident, heard that forbearance could have negative consequences down the road, and opted not to apply even though she struggles to pay her mortgage. Unlike Michelle, borrowers who opted into forbearance plans did so out of necessity; the majority of those who froze their mortgages (55%) experienced some form of income disruption. This finding is consistent with studies from JP Morgan and others showing that most borrowers did not engage in opportunistic moral hazard behaviors such as opting into forbearance plans even though there was no change in their financial circumstances.

Despite reaching its target market, the CARES Act failed to protect many. Tenesha was unaware of forbearance relief and didn’t apply. A significant share of polled participants (40%) said they were unaware of forbearance as an option for mortgage relief. Nearly half of these respondents (49%) reported being worried about foreclosure. Additionally, 14% of survey participants believed they were ineligible for a COVID-payment deferral program. Among them, 8 out of 10 reported earning less than their pre-pandemic income—a key qualifying characteristic for the program.

Notable differences emerged across racial and ethnic groups as well. For instance, Hispanic homeowners were twice as likely as Black and white homeowners to receive a forbearance plan. However, on average, Hispanics reported being unaware of relief options at moderately higher rates (44%) than Blacks (38%) and whites (40%) who were unaware of forbearance plans.

Early on, Fannie Mae raised concerns that familiarity with forbearance relief was alarmingly low among homeowners with incomes below $50,000: 56% were unaware of payment deferrals. A confluence of factors, including widespread misinformation about eligibility, fees, credit score penalties, and lump sum repayment obligations, could explain this frustrating pattern. Unfortunately, these racial disparities transcend the survey sample: a corroborating study by the Federal Reserve Bank of Philadelphia found that non-whites and Hispanics were more likely than whites to cite these concerns as reasons for forgoing forbearance protections. Together, the evidence suggests that critical information asymmetries suppressed participation rates in many corners of hard-hit communities of color.

Homeowners are increasingly fearful of losing ground

The protracted COVID recession has placed mounting pressure on stressed homeowners who are struggling to recover and are increasingly concerned about losing their homes. Nearly a third (30%) of respondents feared losing their homes to foreclosure, and individual financial circumstances were a key driver of this sentiment. The 40% of homeowners who reported earning less were twice as likely to be concerned about a possible foreclosure than the 20% of respondents whose financial conditions remained relatively stable.

The 24% of respondents who worked fewer hours were three times more likely to be extremely anxious about foreclosure than those who had experienced virtually no change in their employment situation (8%). Fear of foreclosure was particularly high among Hispanics with lower incomes: more than half (54%) of this homeowner segment stated they were worried about losing their homes to foreclosure. Despite racial disparities, white respondents were hardly immune to this dynamic: more than a third (37%) were equally worried about foreclosure. Such concerns were not unique to this particular segment; nationally, Freddie Mac estimates that 2 in 5 homeowners (41%) are concerned about their ability to make mortgage payments in the near future.

Some have argued that concern about foreclosure is irrational. However, SaverLife’s homeowners’ experiences contradict this claim and make one fact painfully obvious: many homeowners are currently employed but do not earn nearly enough to maintain mortgage payments alongside other monthly expenses. According to Upjohn Institute’s New Hires Quality Index, which tracks occupational-adjusted wages of new hires, Blacks and Hispanics are returning to the job market through lower-paying occupations with average hourly wages of $16.01 and $15.47, respectively. That’s just $32,740 per year—far short of the minimum annual salary necessary to pay basic living expenses, including a mortgage.

The data show that low-wage and part-time work, not irrationality, drives the foreclosure fears of financially strained homeowners. Shay’s forbearance application never made it through her mortgage servicer’s backlog; she relies on her unemployment benefits to continue making mortgage payments. Quelling Shay’s anxieties, and others like her, will largely depend on her ability to access jobs paying above subsistence wages, which is unlikely to materialize before the foreclosure moratorium expires.

It’s too early to pull the plug: Struggling homeowners need more support, not less

The extreme disruptive effects of the pandemic have begun to wane. Of course, policymakers are eager to normalize the economy, including withdrawing or reducing subsidies such as unemployment benefits. But it would be a mistake to pursue this strategy. Nearly 40% of workers with incomes below $50,000 reported losing their jobs or being laid off, according to the latest Survey of Household and Economic Decisionmaking (SHED) data—more, not less, support is needed to bolster their recovery.

There is an enormous opportunity to avert a foreclosure crisis if states strategically invest the $10 billion 2021 Homeowners Assistance Fund (HAF). The HAF provides states with a wide range of options to mitigate borrower hardships. While resolving backward-looking obligations (such as overdue utility and property tax bills) is a critical aspect of home preservation, the benefits will likely be too short-lived to have a measurable long-term impact. Instead, states should prioritize relief options that make mortgage payments affordable, including making refinancing more accessible. States should provide distressed borrowers with HAF grants to lower the costs of refinancing.

Importantly, these subsidies should cover any cash required to bring down interest rates to an affordable expense-to-income ratio or to ensure that replacement loans conform to loan-to-value overlays. Moreover, states should make corresponding investments in community-based organizations to educate impacted borrowers about available options. Closing information gaps is crucial to improving participation in mortgage relief schemes. Therefore, states must strengthen the capacity of counselors and navigators to empower distressed borrowers and launch public information campaigns that target platforms where those who would most benefit from relief options can be informed.

HAF is an exemplary racial equity paradigm that recognizes the singularity of homeownership in creating wealth for Blacks and Hispanics. HAF marks a commendable start to encouraging inclusive economic recovery, but it is not nearly enough to meet the needs of jobless individuals. Millions of low-income and minority homeowners remain unemployed. This is morally unacceptable. The Biden administration must extend the foreclosure moratorium and continue to make federal forbearance available to unemployed homeowners. Failure to expand these accommodations compromises the immense amount of equity minority families have invested in their pursuit of homeownership and undermines conscious efforts to close the racial wealth gap.

recession unemployment bankruptcy foreclosure pandemic economic recovery subsidies federal reserve grants cdc recession recovery interest rates unemploymentInternational

There will soon be one million seats on this popular Amtrak route

“More people are taking the train than ever before,” says Amtrak’s Executive Vice President.

Share this:

While the size of the United States makes it hard for it to compete with the inter-city train access available in places like Japan and many European countries, Amtrak trains are a very popular transportation option in certain pockets of the country — so much so that the country’s national railway company is expanding its Northeast Corridor by more than one million seats.

Related: This is what it's like to take a 19-hour train from New York to Chicago

Running from Boston all the way south to Washington, D.C., the route is one of the most popular as it passes through the most densely populated part of the country and serves as a commuter train for those who need to go between East Coast cities such as New York and Philadelphia for business.

Veronika Bondarenko

Amtrak launches new routes, promises travelers ‘additional travel options’

Earlier this month, Amtrak announced that it was adding four additional Northeastern routes to its schedule — two more routes between New York’s Penn Station and Union Station in Washington, D.C. on the weekend, a new early-morning weekday route between New York and Philadelphia’s William H. Gray III 30th Street Station and a weekend route between Philadelphia and Boston’s South Station.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

According to Amtrak, these additions will increase Northeast Corridor’s service by 20% on the weekdays and 10% on the weekends for a total of one million additional seats when counted by how many will ride the corridor over the year.

“More people are taking the train than ever before and we’re proud to offer our customers additional travel options when they ride with us on the Northeast Regional,” Amtrak Executive Vice President and Chief Commercial Officer Eliot Hamlisch said in a statement on the new routes. “The Northeast Regional gets you where you want to go comfortably, conveniently and sustainably as you breeze past traffic on I-95 for a more enjoyable travel experience.”

Here are some of the other Amtrak changes you can expect to see

Amtrak also said that, in the 2023 financial year, the Northeast Corridor had nearly 9.2 million riders — 8% more than it had pre-pandemic and a 29% increase from 2022. The higher demand, particularly during both off-peak hours and the time when many business travelers use to get to work, is pushing Amtrak to invest into this corridor in particular.

To reach more customers, Amtrak has also made several changes to both its routes and pricing system. In the fall of 2023, it introduced a type of new “Night Owl Fare” — if traveling during very late or very early hours, one can go between cities like New York and Philadelphia or Philadelphia and Washington. D.C. for $5 to $15.

As travel on the same routes during peak hours can reach as much as $300, this was a deliberate move to reach those who have the flexibility of time and might have otherwise preferred more affordable methods of transportation such as the bus. After seeing strong uptake, Amtrak added this type of fare to more Boston routes.

The largest distances, such as the ones between Boston and New York or New York and Washington, are available at the lowest rate for $20.

stocks pandemic japan europeanInternational

The next pandemic? It’s already here for Earth’s wildlife

Bird flu is decimating species already threatened by climate change and habitat loss.

Share this:

I am a conservation biologist who studies emerging infectious diseases. When people ask me what I think the next pandemic will be I often say that we are in the midst of one – it’s just afflicting a great many species more than ours.

I am referring to the highly pathogenic strain of avian influenza H5N1 (HPAI H5N1), otherwise known as bird flu, which has killed millions of birds and unknown numbers of mammals, particularly during the past three years.

This is the strain that emerged in domestic geese in China in 1997 and quickly jumped to humans in south-east Asia with a mortality rate of around 40-50%. My research group encountered the virus when it killed a mammal, an endangered Owston’s palm civet, in a captive breeding programme in Cuc Phuong National Park Vietnam in 2005.

How these animals caught bird flu was never confirmed. Their diet is mainly earthworms, so they had not been infected by eating diseased poultry like many captive tigers in the region.

This discovery prompted us to collate all confirmed reports of fatal infection with bird flu to assess just how broad a threat to wildlife this virus might pose.

This is how a newly discovered virus in Chinese poultry came to threaten so much of the world’s biodiversity.

The first signs

Until December 2005, most confirmed infections had been found in a few zoos and rescue centres in Thailand and Cambodia. Our analysis in 2006 showed that nearly half (48%) of all the different groups of birds (known to taxonomists as “orders”) contained a species in which a fatal infection of bird flu had been reported. These 13 orders comprised 84% of all bird species.

We reasoned 20 years ago that the strains of H5N1 circulating were probably highly pathogenic to all bird orders. We also showed that the list of confirmed infected species included those that were globally threatened and that important habitats, such as Vietnam’s Mekong delta, lay close to reported poultry outbreaks.

Mammals known to be susceptible to bird flu during the early 2000s included primates, rodents, pigs and rabbits. Large carnivores such as Bengal tigers and clouded leopards were reported to have been killed, as well as domestic cats.

Our 2006 paper showed the ease with which this virus crossed species barriers and suggested it might one day produce a pandemic-scale threat to global biodiversity.

Unfortunately, our warnings were correct.

A roving sickness

Two decades on, bird flu is killing species from the high Arctic to mainland Antarctica.

In the past couple of years, bird flu has spread rapidly across Europe and infiltrated North and South America, killing millions of poultry and a variety of bird and mammal species. A recent paper found that 26 countries have reported at least 48 mammal species that have died from the virus since 2020, when the latest increase in reported infections started.

Not even the ocean is safe. Since 2020, 13 species of aquatic mammal have succumbed, including American sea lions, porpoises and dolphins, often dying in their thousands in South America. A wide range of scavenging and predatory mammals that live on land are now also confirmed to be susceptible, including mountain lions, lynx, brown, black and polar bears.

The UK alone has lost over 75% of its great skuas and seen a 25% decline in northern gannets. Recent declines in sandwich terns (35%) and common terns (42%) were also largely driven by the virus.

Scientists haven’t managed to completely sequence the virus in all affected species. Research and continuous surveillance could tell us how adaptable it ultimately becomes, and whether it can jump to even more species. We know it can already infect humans – one or more genetic mutations may make it more infectious.

At the crossroads

Between January 1 2003 and December 21 2023, 882 cases of human infection with the H5N1 virus were reported from 23 countries, of which 461 (52%) were fatal.

Of these fatal cases, more than half were in Vietnam, China, Cambodia and Laos. Poultry-to-human infections were first recorded in Cambodia in December 2003. Intermittent cases were reported until 2014, followed by a gap until 2023, yielding 41 deaths from 64 cases. The subtype of H5N1 virus responsible has been detected in poultry in Cambodia since 2014. In the early 2000s, the H5N1 virus circulating had a high human mortality rate, so it is worrying that we are now starting to see people dying after contact with poultry again.

It’s not just H5 subtypes of bird flu that concern humans. The H10N1 virus was originally isolated from wild birds in South Korea, but has also been reported in samples from China and Mongolia.

Recent research found that these particular virus subtypes may be able to jump to humans after they were found to be pathogenic in laboratory mice and ferrets. The first person who was confirmed to be infected with H10N5 died in China on January 27 2024, but this patient was also suffering from seasonal flu (H3N2). They had been exposed to live poultry which also tested positive for H10N5.

Species already threatened with extinction are among those which have died due to bird flu in the past three years. The first deaths from the virus in mainland Antarctica have just been confirmed in skuas, highlighting a looming threat to penguin colonies whose eggs and chicks skuas prey on. Humboldt penguins have already been killed by the virus in Chile.

How can we stem this tsunami of H5N1 and other avian influenzas? Completely overhaul poultry production on a global scale. Make farms self-sufficient in rearing eggs and chicks instead of exporting them internationally. The trend towards megafarms containing over a million birds must be stopped in its tracks.

To prevent the worst outcomes for this virus, we must revisit its primary source: the incubator of intensive poultry farms.

Diana Bell does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

genetic pandemic mortality spread deaths south korea south america europe uk chinaInternational

This is the biggest money mistake you’re making during travel

A retail expert talks of some common money mistakes travelers make on their trips.

Share this:

{kind=link}

Travel is expensive. Despite the explosion of travel demand in the two years since the world opened up from the pandemic, survey after survey shows that financial reasons are the biggest factor keeping some from taking their desired trips.

Airfare, accommodation as well as food and entertainment during the trip have all outpaced inflation over the last four years.

Related: This is why we're still spending an insane amount of money on travel

But while there are multiple tricks and “travel hacks” for finding cheaper plane tickets and accommodation, the biggest financial mistake that leads to blown travel budgets is much smaller and more insidious.

This is what you should (and shouldn’t) spend your money on while abroad

“When it comes to traveling, it's hard to resist buying items so you can have a piece of that memory at home,” Kristen Gall, a retail expert who heads the financial planning section at points-back platform Rakuten, told Travel + Leisure in an interview. “However, it's important to remember that you don't need every souvenir that catches your eye.”

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

According to Gall, souvenirs not only have a tendency to add up in price but also weight which can in turn require one to pay for extra weight or even another suitcase at the airport — over the last two months, airlines like Delta (DAL) , American Airlines (AAL) and JetBlue Airways (JBLU) have all followed each other in increasing baggage prices to in some cases as much as $60 for a first bag and $100 for a second one.

While such extras may not seem like a lot compared to the thousands one might have spent on the hotel and ticket, they all have what is sometimes known as a “coffee” or “takeout effect” in which small expenses can lead one to overspend by a large amount.

‘Save up for one special thing rather than a bunch of trinkets…’

“When traveling abroad, I recommend only purchasing items that you can't get back at home, or that are small enough to not impact your luggage weight,” Gall said. “If you’re set on bringing home a souvenir, save up for one special thing, rather than wasting your money on a bunch of trinkets you may not think twice about once you return home.”

Along with the immediate costs, there is also the risk of purchasing things that go to waste when returning home from an international vacation. Alcohol is subject to airlines’ liquid rules while certain types of foods, particularly meat and other animal products, can be confiscated by customs.

While one incident of losing an expensive bottle of liquor or cheese brought back from a country like France will often make travelers forever careful, those who travel internationally less frequently will often be unaware of specific rules and be forced to part with something they spent money on at the airport.

“It's important to keep in mind that you're going to have to travel back with everything you purchased,” Gall continued. “[…] Be careful when buying food or wine, as it may not make it through customs. Foods like chocolate are typically fine, but items like meat and produce are likely prohibited to come back into the country.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic france

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Is the National Guard a solution to school violence?

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Vaccine-skeptical mothers say bad health care experiences made them distrust the medical system

Are Voters Recoiling Against Disorder?

The Great Replacement Loophole: Illegal Immigrants Score 5-Year Work Benefit While “Waiting” For Deporation, Asylum

Survey Shows Declining Concerns Among Americans About COVID-19

Chinese migration to US is nothing new – but the reasons for recent surge at Southern border are

The Grinch Who Stole Freedom

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International3 days ago

International3 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

International3 days ago

International3 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex