International

“It Won’t Be Pleasant” – Mark Carney Unveils Dystopian New World To Combat Climate ‘Crisis’

"It Won’t Be Pleasant" – Mark Carney Unveils Dystopian New World To Combat Climate ‘Crisis’

Authored by Peter Foster via NationalPost.com,

What Carney ultimately wants is a technocratic dictatorship justified by climate alarmism…

In…

Share this:

Authored by Peter Foster via NationalPost.com,

What Carney ultimately wants is a technocratic dictatorship justified by climate alarmism...

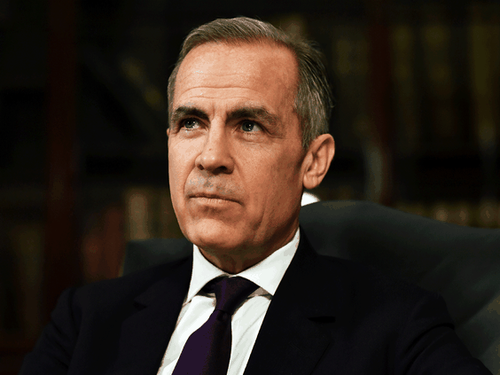

In his book Value(s): Building a Better World for All, Mark Carney, former governor both of the Bank of Canada and the Bank of England, claims that western society is morally rotten, and that it has been corrupted by capitalism, which has brought about a “climate emergency” that threatens life on earth. This, he claims, requires rigid controls on personal freedom, industry and corporate funding.

Carney’s views are important because he is UN Special Envoy on Climate Action and Finance. He is also an adviser both to British Prime Minister Boris Johnson on the next big climate conference in Glasgow, and to Canadian Prime Minister Justin Trudeau.

Since the advent of the COVID pandemic, Carney has been front and centre in the promotion of a political agenda known as the “Great Reset,” or the “Green New Deal,” or “Building Back Better.” All are predicated on the claim that COVID, and its disruption of the global economy, provides a once-in-a-lifetime opportunity not just to regulate climate, but to frame a more fair, more diverse, more inclusive, more safe and more woke world.

Carney draws inspiration from, among others, Marx, Engels and Lenin, but the agenda he promotes differs from Marxism in two key respects. First, the private sector is not to be expropriated but made a “partner” in reshaping the economy and society. Second, it does not make a promise to make the lives of ordinary people better, but worse. Carney’s Brave New World will be one of severely constrained choice, less flying, less meat, more inconvenience and more poverty: “Assets will be stranded, used gasoline powered cars will be unsaleable, inefficient properties will be unrentable,” he promises.

The agenda’s objectives are in fact already being enforced, not primarily by legislation but by the application of non-governmental — that is, non-democratic — pressure on the corporate sector via the ever-expanding dictates of ESG (environmental, social and corporate governance) and by “sustainable finance,” which is designed to starve non-compliant companies of funds, thus rendering them, as Carney puts it, “climate roadkill.” What ESG actually represents is corporate ideological compulsion. It is a key instrument of “stakeholder capitalism.”

Carney’s Agenda is promoted by the United Nations and other international bureaucracies and a vast and ever-growing array of non-governmental organizations and fora, especially the World Economic Forum (WEF), where Carney is a trustee. Also, perhaps most surprisingly, by its corporate victims. No one wants to become climate roadkill.

Carney clearly feels himself to be a man of destiny. “When I worked at the Bank of England,” he writes in Value(s), “I would remind myself each morning of Marcus Aurelius’ phrase ‘arise to do the work of humankind’.” One is reminded of French aristocrat and social reformer Henri de Saint-Simon, the “grand seigneur sans-culotte,” who ordered his valet to wake him with similar words: “Remember, monsieur le comte, that you have great things to do.”

That is not the only thing Carney has in common with Saint-Simon, who believed that society should be ruled by savants such as himself; an alliance of engineers and other technocratic intellectuals, along with bankers. Carney is very much a banker technocrat, not merely at ease gliding along the corridors of global bureaucratic power, but expert at framing arguments that support an ever-expanding role for his class.

His expansive pretensions first appeared at the Bank of Canada. If the economy is like a game of ice hockey, then central bankers should, ideally, be like Zamboni drivers, whose job is to keep the ice flat (Carney had in fact been a goalie during his academic years at both Harvard and Oxford). At the Bank of Canada, he often seemed like the Zamboni driver who thought he was Wayne Gretzky. He could never resist lecturing private businesses to stop sitting on “dead money,” or telling them they were too timid in the international arena, or advising consumers that they were spending too little, or borrowing too much. He promoted “macroprudence,” the idea that regulators, in their panoptic wisdom, would focus on the forest, not the trees. Now, he wants to establish himself as an intellectual.

Carney has a lot to put straight with the world. According to his new book, and the related BBC Reith Lectures that Carney delivered last year, the three great crises of credit (2008–09 version), COVID and climate are all rooted in a single problem: People in general, and markets in particular, are not as wise, moral or far-seeing as Mark Carney. He sums up this failing as the “Tragedy of the Horizon,” a phrase he concocted for a speech ahead of the 2015 Paris climate conference.

However, Carney is sophistic when it comes to the alleged moral shortcomings of capitalism. It has been one of the most tedious tropes of the left since at least The Communist Manifesto that the rise of commerce would drive out all that is virtuous in society, leaving nothing but the “cash nexus” of trade. One of Carney’s favourite philosophers is Harvard’s Michael Sandel, who produces endless trivial examples suggesting that we have moved from a “market economy” to a “market society.”

“Should sex be up for sale?” Carney thunders, following Sandel. “Should there be a market in the right to have children? Why not auction the right to opt out of military service? Why shouldn’t universities sell admission to raise money for worthy causes?” But the very fact that people reflexively feel uneasy about — or outright reject — such notions entirely disproves his point. People do not believe that everything is, or should be, for sale.

Carney notes the long debate, going back to classical times, on the nature of commercial value. This was theoretically resolved by the “marginalist revolution,” which put paid to the “paradox of value” that puzzled over the (usually) low price of useful water and the (usually) high price of useless diamonds. The marginalists pointed out that commercial value isn’t determined by usefulness or labour input. It is inevitably subjective, based on personal preferences and available resources. There is no paradox. Someone dying of thirst in the middle of the desert might be more than willing to offer a bucket of diamonds for a bucket of water.

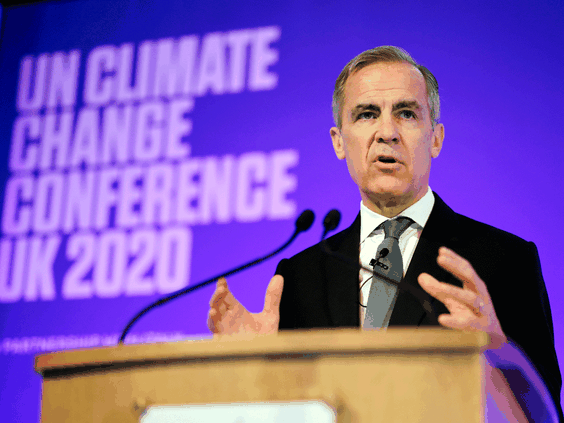

Mark Carney is a UN Special Envoy on Climate Action. PHOTO BY TOLGA AKMEN/POOL VIA REUTERS/FILE

However, market valuations are essentially different from moral values, a distinction Carney continually muddles. He misrepresents the marginalist/subjectivist perspective, claiming that it implies that anything not commercially priced is not considered valuable. “Market value,” he writes, “is taken to represent intrinsic value, and if a good or activity is not in the market, it is not valued.” But who holds such an idiotic view? Nobody “prices” their family, children, friends, community spirit or the beauties of nature, although there is certainly lots of calculation going on in the background. Carney constantly berates “market fundamentalist” straw men who employ “standard economic reasoning” and who believe that people are rational and markets perfect.

He incorrectly claims that Adam Smith — in his first great book, The Theory of Moral Sentiments— said that a sense of morality was “not inherent.” In fact, Smith believed that we are born with such a sense, which is then fine-tuned by the society in which we grow up. However, Carney — like all leftists — leans towards the blank slate, nurture-over-nature perspective because it suggests that human nature might be beneficially reformed under the right (that is, left) social arrangements.

Carney believes our moral sentiments started going astray around the time of the publication of Smith’s better-known book, The Wealth of Nations, in 1776, when the Industrial Revolution was beginning to take off. He rightly suggests that one should read both books to gain a full appreciation of Smith’s insights, but he seems to have missed the significance of Smith’s putdown of “whining and melancholy moralists,” his cynicism about “insidious and crafty” politicians, and his thoroughgoing skepticism about those who would “trade for the public good” (that is, the ESG crowd). Moreover, Smith noted that the greatest corrupter of moral sentiments was not commerce but “faction and fanaticism,” that is, politics and religion, which come together in the toxic stew of climate alarmism and ESG.

ESG used to be called Corporate Social Responsibility, or CSR. The Nobel economist Milton Friedman warned against its subversive nature 50 years ago. He noted that taking on externally dictated “social responsibilities” beyond those directly related to a company’s business opened the floodgates to endless pressure and interference. The big questions are responsibility to whom? And for what?

Carney also typically misrepresents Friedman, suggesting that he claimed that shareholders should rank “uber alles,” and to the exclusion of other legitimate stakeholders such as employees and local communities. Carney claims that “At times, large positive gains could accrue to society if small sacrifices were made on behalf of shareholders.” But by what right would management “sacrifice” shareholders, and who would decide which sacrifices should be made?

Carney admits that the “integrated reporting” required by ESG is a morass: “ESG ratings consider hundreds of metrics, with many of them qualitative in nature… Putting values to work is hard work, but as with virtue, it should become easier with sustained practice.” No need to ask whose version of values and virtue is to prevail.

* * *

Despite his thorough castigation of market society, Carney somehow also believes this “corroded” society is clamouring to make great personal sacrifices for draconian climate actions and the UN’s Sustainable Development Goals.

Carney has been a prime pusher of “net-zero,” the notion that climate-related human emissions must be entirely eradicated, buried or offset by 2050 if the world is to avoid climate Armageddon. He claims that net-zero is “highly valued by society.” In reality, the vast mass of people have no clue what it entails; when Carney talks about this version of “society,” he is talking about a small, radical element of it.

Carney peddles the non-sequitur that because the world wasn’t ready for COVID, this confirms that the world is being short-sighted about climate catastrophe. But COVID is an obvious reality; an existential climate catastrophe is a hypothesis (frequently promoted — admittedly with great success — by those with agendas). He claims that “A good introduction to this subject can be found in journalist David Wallace-Wells’ The Uninhabitable Earth,” a work heavily criticized even by prominent climate-change scientists for its factual errors and exaggerations. Indeed, even its author admitted its tendentious purpose.

Carney also commends the knowledge and wisdom of Swedish teenager Greta Thunberg: “The power of Greta Thunberg’s message lies in the way she drives home both the cold logic of climate physics and the fundamental unfairness of the climate crisis.”

Anybody who cites an anxious 17-year-old as an authority on climate science and moral philosophy should be an object of deep suspicion, but then, according to Carney, climate science is easy. Greta’s “basic calculations” are ones that she could “easily master and powerfully project.” (Carney says he once gave Greta a tour of the Bank of England’s gold vaults. One wonders if she also offered up tips on monetary policy.) But then, in early 2020, Greta demonstrated her complete disconnect from reality when, at the WEF in Davos, she called for an immediate cessation of emissions, which would tank the world economy and potentially kill millions. Even Carney admits deviating from her wisdom on that point.

Far from demonstrating a firm knowledge of the climate system himself, Carney cites scary but misleading statistics. “Since the 1980s,” he writes, “the number of registered weather-related loss events has tripled, and the inflation-adjusted losses have increased fivefold. Consistent with the accelerated pace of climate change, the cost of weather-related insurance losses has increased eightfold in real terms over the past decade to an annual average of $60 billion.”

I asked Professor Roger Pielke, Jr., an expert on climate and economics at the University of Colorado, to comment. He replied “(Carney) has confused economics with weather. The increase in losses he describes is well understood to occur for two main reasons: more wealth and property exposed to loss and better accounting of those losses. To assess trends in extreme weather one should look at weather data, not economic loss data.”

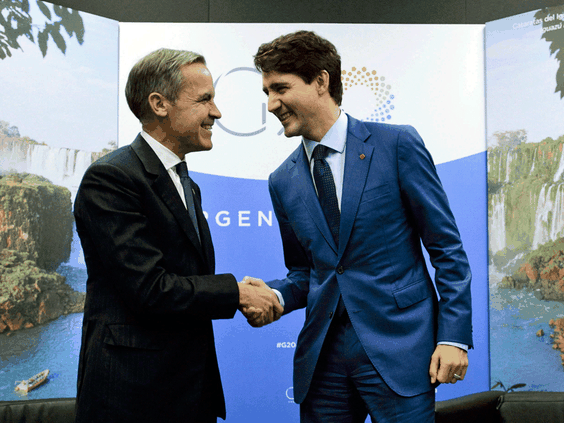

Among Mark Carney’s current responsibilities since leaving the Bank of England as its governor is advising Prime Minister Justin Trudeau. PHOTO BY SEAN KILPATRICK/THE CANADIAN PRESS/FILE

Carney’s confusion is hardly innocent since his Agenda depends on incessantly claiming that “What had been biblical is becoming commonplace.”

Fortunately, Carney has been making claims about worsening weather for long enough that we can assess some of his predictions. In his recent book Unsettled: What Climate Science Tells Us, What It Doesn’t, and Why It Matters, Steven Koonin, former undersecretary for science at the Obama-era U.S. Energy Department, cites the speech Carney made to Lloyd’s of London before the Paris climate conference in 2015. The speech was designed to frighten the insurance industry into divestment from fossil fuels, on the basis that many oil and gas reserves would be “stranded” as we exhaust our allowable carbon “budget.” Carney pointed out that the previous U.K. winter had been the “wettest since the time of King George III.” He went on to say, “forecasts suggest we can expect at least a further 10% increase in rainfall during future winters.” For support he cited the U.K. Met Office’s forecast for the next five years. It turned out to be dead wrong. The six winters after 2014 averaged 39-per-cent less rainfall than the 2014 record. Meanwhile a Met Office report in 2018 acknowledged that the “largest source of variability in U.K. extreme rainfalls during the winter months was the North Atlantic Oscillation mode of natural variability, not a changing climate.”

“(I)t’s surprising,” notes Koonin, “that someone with a PhD in economics and experience with the unpredictability of financial markets and economies as a whole doesn’t show a greater respect for the perils of prediction — and more caution in depending upon models.”

During his BBC Reith Lectures last year, on the topic of “How We Get What We Value,” Carney received few challenges from his handpicked questioners, but a couple came from eminent historian Niall Ferguson. Ferguson asked Carney why, in his discussion of the climate issue, he made no reference to Bjorn Lomborg (a much more knowledgeable Scandinavian than Greta), and in particular to Lomborg’s book, False Alarm, in which Lomborg establishes — using “official” science — that there is no existential climate crisis, that adapting to climate change is manageable, and that the kinds of policies promoted by Carney are likely to be far more costly than any impact from extreme weather.

Carney of course hadn’t read that book, but he dismissed Lomborg by saying that “it’s 15 or 20 years ago when he first came out with his ‘Don’t worry about the climate.’ How’s that working out for us?” But Lomborg never said “Don’t worry about the climate,” he just suggested that we had to put risks into perspective. Meanwhile Lomborg’s non-alarmist thesis is working out much better than that of doomsayers such as Carney.

This offhand rejection of someone as widely respected as Lomborg exposes the hypocrisy of Carney’s statement in Value(s) that “experts need to listen to all sides…All of us as individuals have a responsibility to be more open and to engage respectfully with different views if we want constructive political debates and to make progress on important issues.” Except, climate-catastrophe dissenters don’t make it into the debate. There can be zero diversity of views on net-zero.

Ferguson put another thorny question to Carney at that Reith lecture: He pointed out that since the 2015 Paris agreement, China had been responsible for almost half the increase in global carbon emissions, and it was building more coal capacity in the current year than existed in the entire United States. What did China’s promises of net-zero by 2060 mean, Ferguson asked, if it was “actually leading the pollution charge”? Carney’s non response was that China is the largest manufacturer of zero-emission cars, and the leading producer of renewable energy.

Koonin notes in his book that Carney “is probably the single most influential figure in driving investors and financial institutions around the world to focus on changes in climate and human influences upon it…. So it’s important to pay close attention to what he says.”

* * *

Mark Carney cries crocodile tears at the possible viability of the Marxist perspective in today’s political environment. But if there is one sure sign of a Marxist, it’s a belief that capitalism is — or is about to be – in “crisis.” His new book has an appendix on Marx’s theory of surplus value: that all profits are wrung from the hides of labour. He also cites Marx’s collaborator, Friedrich Engels. In particular he notes “Engels’ pause,” the one period in capitalist history, early in the 19th century, when workers may not have shared the increases in productivity brought about by industrialization.

Carney projects that the “Fourth Industrial Revolution” (a phenomenon much invoked by the WEF) might bring about a similar period, thus providing a source of political unrest. “(I)t could be generations before the gains of the Fourth Industrial Revolution are widely shared,” he writes. “In the interim, there could be a long period of technological unemployment, sharply rising inequalities and intensifying social unrest… If this world of surplus labour comes to pass, Marx and Engels could again become relevant.”

He rather seems to hope so.

Carney claims powerful parallels between Marx’s time and our own. “Substitute platforms for textile mills, machine learning for the steam engine, and Twitter for the telegraph, and current dynamics echo those of that era. Then, Karl Marx was scribbling the Communist Manifesto in the reading room of the British Library. Today, radical viral blogs and tweets voice similar outrage.”

In fact, Marx wrote The Communist Manifesto, based on a tract by Engels, in Brussels, not at the British Library, but it’s more important to remember where Marx’s misguided and immutable outrage led: to a disastrous economic and political model that generated poverty and mass murder on an unprecedented scale. Meanwhile “outrage” is surely a dubious basis for policy. The outraged are certainly a useful constituency for those seeking power, however, which brings us to the influence on Carney of the man who first tried to put Marxism into practice.

When it comes to the COVID crisis, writes Carney, “We are living Lenin’s observation that there are ‘decades when nothing happens and weeks when decades happen’.” Strange that Carney would cite one of the most ruthless murderers in history for this rather bland insight, but then Carney’s Agenda is not without its own parallels to Lenin (minus, one presumes, the precondition of rampant bloodshed).

Although Vladimir Lenin didn’t know much about business or economics, he declared that “’Communism is Soviet power plus the electrification of the whole country.” Carney’s plan is global. “We need,” he claims, “to electrify everything and turn electricity generation green.” The problem is that wind- and solar-powered electricity needs both hefty government subsidies and fossil-fuel backup for when the wind doesn’t blow and the sun doesn’t shine. Green electricity is inflexible, expensive and disruptive to grids.

Carney cites Joseph Schumpeter’s concept of “creative destruction,” but his own version involves not the metaphorical and benign process of market innovation making old technologies redundant, but a deliberate suppression of viable technologies to make way for less reliable and less economic alternatives.

When Lenin wrecked the Russian economy after brutally seizing power in 1917, he was forced to backtrack and allow some private enterprise to prevent people starving. However, he assured his radical comrades that he would retain control of “the commanding heights” of heavy industry. Carney’s plan is to control the global economy by seizing the commanding heights of finance, not by nationalization but by exerting non-democratic pressure to divest from, and stop funding, fossil fuels. The private sector is to become a partner in imposing its own bondage. This will be do-it-yourself totalitarianism. Indeed, companies in our one-party ESG state are already pleading like show-trial defendants, making suicidal net-zero commitments, lest banks cut them off.

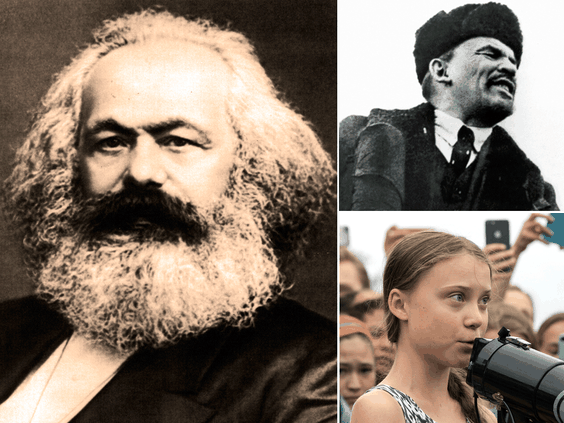

Left: A portrait of Karl Marx. Top right: Vladimir Lenin makes a speech in Red Square on the first anniversary of the Bolshevik Revolution. Below right: Teenage Swedish climate activist Greta Thunberg delivers brief remarkssurrounded by other student environmental advocates in 2019. Mark Carney draws on all three in his agenda to address the “climate emergency,” writes Peter Foster. PHOTO BY FILE; HULTON-DEUTSCH COLLECTION/CORBIS/CORBIS VIA GETTY IMAGES; SARAH SILBIGER/GETTY IMAGES/FILE

To further that end, Carney has helped to start a key organization, the Network for Greening the Financial System (NGFS), a collection of central banks and regulators. He has also signed up an ever-growing constituency of activist policy wonks who peddle emissions measurement and certification, eco audits and ESG rankings. This agenda is inevitably appealing to transnational organizations such as the International Energy Agency (IEA), the IMF, the World Bank and the OECD, whose empires are all lucratively intertwined with the global governance thrust. In May, the IEA issued a report calling for an immediate end to fossil fuel investment to get to net-zero.

Part of Carney’s strategy is to force “voluntary” standards on banking and industry, then have governments make those standards compulsory. The major accounting firms appear keen to promote the possibility of endless auditing extensions, under which the relatively straightforward metric of money is to be replaced by the infinitely malleable concepts of “purpose” and “impact.”

Carney has also helped turn the accounting screw though “carbon disclosure.” Companies are pressured to make explicit the kind of damage they might suffer if the alarmists’ worst nightmares are realized. Such disclosure is a variant on that famous loaded question “When did you stop beating your spouse?” Instead, carbon disclosure asks the climate equivalent of “If you were to beat your spouse, what sort of injuries might he/she suffer?” Companies must also disclose their plans to deal with the presumed crisis. No company dares to say “We do not believe your apocalyptic forecasts.” They meekly regurgitate the required climate porn about floods and droughts and hurricanes, and make elaborate fingers-crossed emissions-reductions commitments. This in turn leads them into arrangements such as buying emissions offsets, a complex scheme analogous to the medieval Catholic Church’s sale of indulgences. Carbon markets have inevitably led to a surge in work for offset generators, certifiers and auditors. Carney projects this market could be worth $100 billion.

Ironically, earlier this year Carney found himself tangled in the murky metrics of offsets. In 2020, he was appointed a vice chairman with Toronto-based Brookfield Asset Management, where he is in charge of “impact investing.” As historian Tammy Nemeth points out in her critical study of the “Transnational Progressive Movement,” of which Carney is a leading light: “(I)t is perhaps ethically murky for someone who is actively working within the UN and advising two different governments on how to change national and global financial rules to be working for a company that will be a direct beneficiary of those rule changes.” Still, who better to lead your company through a minefield than the person who planted the mines?

Except that Carney was hoist with his own petard when he claimed that Brookfield, which has major investments in fossil fuels and pipelines, was already “net-zero” due to emissions “avoided” as a result of its investing in renewable energy. Carney’s claim produced instant refutation and accusations of greenwashing. The Financial Times called it a “major stumble.” A representative of CDP (formerly the Carbon Disclosure Project) castigated those who attempt to hide “dirty coal issues.” Carney subsequently issued a qualified mea culpa on Twitter: “I have always been — and will continue to be — a strong advocate for net zero science-based targets, and I also recognize that avoided emissions do not count towards them.”

* * *

H. L. Mencken observed that “The urge to save humanity is almost always a false-front for the urge to rule.” So, just how big a threat is the agenda of Mark Carney and his fellow “transnational progressives”?

In his book, Value(s), Carney lays out rationalizations and autocratic pretensions, although he is less forthcoming about his motivations. He writes that “Leaders need to renounce power for its own sake and discern the power of service.” Mencken would be amused.

The shambolic response to COVID of many governments, not least in Canada, and the distinctly unsettled nature of pandemic “science,” have not done much for the credibility of either governments or experts. The Carney-backed agenda is not predicated on working through democratic institutions but on circumventing them. Still, he is also reported to have more conventional political aspirations, namely to join the federal Liberal party and rise within it, very possibly to prime minister. (Carney recently gave a speech at the Liberal national convention, where he pledged his full support.)

He thus has a rather ill-fitting section in Value(s) on “How Canada Can Build Value for All.” It reads like a Liberal party stump speech. According to Carney “We (in Canada) routinely transcend the limitations of our size to model values and policies for other countries.” It’s the old chestnut that no progressive Canadian leader ever seems to tire of: The world needs more Canada.

Carney is a classic example of what Friedrich Hayek called the “fatal conceit” of constructivist rationalism: the belief that the largely spontaneous institutions of the market order should be rejected in favour of more deliberately planned arrangements. Carney is undoubtedly an intelligent man, but Hayek stressed that the thing that intelligent people tend most to overestimate is the power of intelligence — particularly if they happen to be socialists.

Carney is also of the class that philosopher Karl Popper described as “enemies” of an “open society.” Popper noted that social upheavals tend to bring forth prophets who claim to understand the forces shaping the future, and promise salvation if they are given absolute power. Such was Plato’s model — in response to the upheavals of the Peloponnesian War and the first wave of democracy — of a necessary dictatorship in which the rulers lived as communists, using a specially bred military to control a cattle-like populace. Similarly, Marx’s communism was a response to the turmoil of the Industrial Revolution.

Considering the squalor of Manchester in the 1840s, one might forgive Marx and Engels for thinking a radical response was in order. But given the success of capitalism and the horrors of autocratic systems in the intervening period, it takes considerable chutzpah to be promoting net-zero totalitarianism.

Still, Carney claims that great crises demand great plans. He cites Timothy Geithner, secretary of the U.S. Treasury under president Obama, saying “plan beats no plan.” But Geithner was talking about the very real and immediate 2008–09 financial crisis. Carney’s climate plan is much closer to the notion of Soviet central long-term planning. Clearly, when it came to the subsequent welfare of the Russian people, “no plan” would certainly have beaten “plan.”

What Carney ultimately wants, like Saint-Simon, is a technocratic dictatorship justified by climate alarmism. He suggests that “governments can delegate certain aspects of the calibration of specific instruments… to Carbon Councils in order to improve the predictability, credibility and impact of climate policies.” These carbon councils will be able to demand that national governments “comply or explain” when they inevitably fall short of targets. How these commissars will bring governments into line is unclear, although Nobel economist William Nordhaus has suggested “Climate Clubs” that will punish recalcitrants with punitive tariffs.

The threat of punishment will clearly be necessary because governments are doing little more than hypocritical tinkering on climate policy. China and India are hardly even playing lip service to the “climate emergency.” Nevertheless, according to Carney “political technology” is needed to “build a broad consensus around the right goals.” No question of debating the goals, or the science, just building a consensus to support them.

Carney is a man on a mission to change global society. “Business as usual” — the most hated phrase in the socialist lexicon — is “ultimately catastrophic,” he writes. There is too much “misplaced acceptance of the status quo.” But somehow the new socialism will not be socialism as usual. This time it’s different. We can because we must. The threat is too great to permit any argument. It’s surprising that as he was picking out choice quotes from Lenin for his book, Carney missed this one: “No more opposition now, comrades! The time has come to put an end to opposition, to put the lid on it. We have had enough opposition!”

International

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Is there a light forming when it comes to the long, dark and…

Share this:

Is there a light forming when it comes to the long, dark and bewildering tunnel of social justice cultism? Global events have been so frenetic that many people might not remember, but only a couple years ago Big Tech companies and numerous governments were openly aligned in favor of mass censorship. Not just to prevent the public from investigating the facts surrounding the pandemic farce, but to silence anyone questioning the validity of woke concepts like trans ideology.

From 2020-2022 was the closest the west has come in a long time to a complete erasure of freedom of speech. Even today there are still countries and Europe and places like Canada or Australia that are charging forward with draconian speech laws. The phrase "radical speech" is starting to circulate within pro-censorship circles in reference to any platform where people are allowed to talk critically. What is radical speech? Basically, it's any discussion that runs contrary to the beliefs of the political left.

Open hatred of moderate or conservative ideals is perfectly acceptable, but don't ever shine a negative light on woke activism, or you might be a terrorist.

Riley Gaines has experienced this double standard first hand. She was even assaulted and taken hostage at an event in 2023 at San Francisco State University when leftists protester tried to trap her in a room and demanded she "pay them to let her go." Campus police allegedly witnessed the incident but charges were never filed and surveillance footage from the college was never released.

It's probably the last thing a champion female swimmer ever expects, but her head-on collision with the trans movement and the institutional conspiracy to push it on the public forced her to become a counter-culture voice of reason rather than just an athlete.

For years the independent media argued that no matter how much we expose the insanity of men posing as women to compete and dominate women's sports, nothing will really change until the real female athletes speak up and fight back. Riley Gaines and those like her represent that necessary rebellion and a desperately needed return to common sense and reason.

In a recent interview on the Joe Rogan Podcast, Gaines related some interesting information on the inner workings of the NCAA and the subversive schemes surrounding trans athletes. Not only were women participants essentially strong-armed by colleges and officials into quietly going along with the program, there was also a concerted propaganda effort. Competition ceremonies were rigged as vehicles for promoting trans athletes over everyone else.

The bottom line? The competitions didn't matter. The real women and their achievements didn't matter. The only thing that mattered to officials were the photo ops; dudes pretending to be chicks posing with awards for the gushing corporate media. The agenda took precedence.

Lia Thomas, formerly known as William Thomas, was more than an activist invading female sports, he was also apparently a science project fostered and protected by the athletic establishment. It's important to understand that the political left does not care about female athletes. They do not care about women's sports. They don't care about the integrity of the environments they co-opt. Their only goal is to identify viable platforms with social impact and take control of them. Women's sports are seen as a vehicle for public indoctrination, nothing more.

The reasons why they covet women's sports are varied, but a primary motive is the desire to assert the fallacy that men and women are "the same" psychologically as well as physically. They want the deconstruction of biological sex and identity as nothing more than "social constructs" subject to personal preference. If they can destroy what it means to be a man or a woman, they can destroy the very foundations of relationships, families and even procreation.

For now it seems as though the trans agenda is hitting a wall with much of the public aware of it and less afraid to criticize it. Social media companies might be able to silence some people, but they can't silence everyone. However, there is still a significant threat as the movement continues to target children through the public education system and women's sports are not out of the woods yet.

The ultimate solution is for women athletes around the world to organize and widely refuse to participate in any competitions in which biological men are allowed. The only way to save women's sports is for women to be willing to end them, at least until institutions that put doctrine ahead of logic are made irrelevant.

International

Congress’ failure so far to deliver on promise of tens of billions in new research spending threatens America’s long-term economic competitiveness

A deal that avoided a shutdown also slashed spending for the National Science Foundation, putting it billions below a congressional target intended to…

Share this:

Federal spending on fundamental scientific research is pivotal to America’s long-term economic competitiveness and growth. But less than two years after agreeing the U.S. needed to invest tens of billions of dollars more in basic research than it had been, Congress is already seriously scaling back its plans.

A package of funding bills recently passed by Congress and signed by President Joe Biden on March 9, 2024, cuts the current fiscal year budget for the National Science Foundation, America’s premier basic science research agency, by over 8% relative to last year. That puts the NSF’s current allocation US$6.6 billion below targets Congress set in 2022.

And the president’s budget blueprint for the next fiscal year, released on March 11, doesn’t look much better. Even assuming his request for the NSF is fully funded, it would still, based on my calculations, leave the agency a total of $15 billion behind the plan Congress laid out to help the U.S. keep up with countries such as China that are rapidly increasing their science budgets.

I am a sociologist who studies how research universities contribute to the public good. I’m also the executive director of the Institute for Research on Innovation and Science, a national university consortium whose members share data that helps us understand, explain and work to amplify those benefits.

Our data shows how underfunding basic research, especially in high-priority areas, poses a real threat to the United States’ role as a leader in critical technology areas, forestalls innovation and makes it harder to recruit the skilled workers that high-tech companies need to succeed.

A promised investment

Less than two years ago, in August 2022, university researchers like me had reason to celebrate.

Congress had just passed the bipartisan CHIPS and Science Act. The science part of the law promised one of the biggest federal investments in the National Science Foundation in its 74-year history.

The CHIPS act authorized US$81 billion for the agency, promised to double its budget by 2027 and directed it to “address societal, national, and geostrategic challenges for the benefit of all Americans” by investing in research.

But there was one very big snag. The money still has to be appropriated by Congress every year. Lawmakers haven’t been good at doing that recently. As lawmakers struggle to keep the lights on, fundamental research is quickly becoming a casualty of political dysfunction.

Research’s critical impact

That’s bad because fundamental research matters in more ways than you might expect.

For instance, the basic discoveries that made the COVID-19 vaccine possible stretch back to the early 1960s. Such research investments contribute to the health, wealth and well-being of society, support jobs and regional economies and are vital to the U.S. economy and national security.

Lagging research investment will hurt U.S. leadership in critical technologies such as artificial intelligence, advanced communications, clean energy and biotechnology. Less support means less new research work gets done, fewer new researchers are trained and important new discoveries are made elsewhere.

But disrupting federal research funding also directly affects people’s jobs, lives and the economy.

Businesses nationwide thrive by selling the goods and services – everything from pipettes and biological specimens to notebooks and plane tickets – that are necessary for research. Those vendors include high-tech startups, manufacturers, contractors and even Main Street businesses like your local hardware store. They employ your neighbors and friends and contribute to the economic health of your hometown and the nation.

Nearly a third of the $10 billion in federal research funds that 26 of the universities in our consortium used in 2022 directly supported U.S. employers, including:

A Detroit welding shop that sells gases many labs use in experiments funded by the National Institutes of Health, National Science Foundation, Department of Defense and Department of Energy.

A Dallas-based construction company that is building an advanced vaccine and drug development facility paid for by the Department of Health and Human Services.

More than a dozen Utah businesses, including surveyors, engineers and construction and trucking companies, working on a Department of Energy project to develop breakthroughs in geothermal energy.

When Congress shortchanges basic research, it also damages businesses like these and people you might not usually associate with academic science and engineering. Construction and manufacturing companies earn more than $2 billion each year from federally funded research done by our consortium’s members.

Jobs and innovation

Disrupting or decreasing research funding also slows the flow of STEM – science, technology, engineering and math – talent from universities to American businesses. Highly trained people are essential to corporate innovation and to U.S. leadership in key fields, such as AI, where companies depend on hiring to secure research expertise.

In 2022, federal research grants paid wages for about 122,500 people at universities that shared data with my institute. More than half of them were students or trainees. Our data shows that they go on to many types of jobs but are particularly important for leading tech companies such as Google, Amazon, Apple, Facebook and Intel.

That same data lets me estimate that over 300,000 people who worked at U.S. universities in 2022 were paid by federal research funds. Threats to federal research investments put academic jobs at risk. They also hurt private sector innovation because even the most successful companies need to hire people with expert research skills. Most people learn those skills by working on university research projects, and most of those projects are federally funded.

High stakes

If Congress doesn’t move to fund fundamental science research to meet CHIPS and Science Act targets – and make up for the $11.6 billion it’s already behind schedule – the long-term consequences for American competitiveness could be serious.

Over time, companies would see fewer skilled job candidates, and academic and corporate researchers would produce fewer discoveries. Fewer high-tech startups would mean slower economic growth. America would become less competitive in the age of AI. This would turn one of the fears that led lawmakers to pass the CHIPS and Science Act into a reality.

Ultimately, it’s up to lawmakers to decide whether to fulfill their promise to invest more in the research that supports jobs across the economy and in American innovation, competitiveness and economic growth. So far, that promise is looking pretty fragile.

This is an updated version of an article originally published on Jan. 16, 2024.

Jason Owen-Smith receives research support from the National Science Foundation, the National Institutes of Health, the Alfred P. Sloan Foundation and Wellcome Leap.

economic growth covid-19 grants congress vaccine chinaInternational

What’s Driving Industrial Development in the Southwest U.S.

The post-COVID-19 pandemic pipeline, supply imbalances, investment and construction challenges: these are just a few of the topics address by a powerhouse…

Share this:

{kind=link}

{kind=link}

The post-COVID-19 pandemic pipeline, supply imbalances, investment and construction challenges: these are just a few of the topics address by a powerhouse panel of executives in industrial real estate this week at NAIOP’s I.CON West in Long Beach, California. Led by Dawn McCombs, principal and Denver lead industrial specialist for Avison Young, the panel tackled some of the biggest issues facing the sector in the Western U.S.

Starting with the pandemic in 2020 and continuing through 2022, McCombs said, the industrial sector experienced a huge surge in demand, resulting in historic vacancies, rent growth and record deliveries. Operating fundamentals began to normalize in 2023 and construction starts declined, certainly impacting vacancy and absorption moving forward.

“Development starts dropped by 65% year-over-year across the U.S. last year. In Q4, we were down 25% from pre-COVID norms,” began Megan Creecy-Herman, president, U.S. West Region, Prologis, noting that all of that is setting us up to see an improvement of fundamentals in the market. “U.S. vacancy ended 2023 at about 5%, which is very healthy.”

Vacancies are expected to grow in Q1 and Q2, peaking mid-year at around 7%. Creecy-Herman expects to see an increase in absorption as customers begin to have confidence in the economy, and everyone gets some certainty on what the Fed does with interest rates.

“It’s an interesting dynamic to see such a great increase in rents, which have almost doubled in some markets,” said Reon Roski, CEO, Majestic Realty Co. “It’s healthy to see a slowing down… before [rents] go back up.”

Pre-pandemic, a lot of markets were used to 4-5% vacancy, said Brooke Birtcher Gustafson, fifth-generation president of Birtcher Development. “Everyone was a little tepid about where things are headed with a mediocre outlook for 2024, but much of this is normalizing in the Southwest markets.”

McCombs asked the panel where their companies found themselves in the construction pipeline when the Fed raised rates in 2022.

In Salt Lake City, said Angela Eldredge, chief operations officer at Price Real Estate, there is a typical 12-18-month lead time on construction materials. “As rates started to rise in 2022, lots of permits had already been pulled and construction starts were beginning, so those project deliveries were in fall 2023. [The slowdown] was good for our market because it kept rates high, vacancies lower and helped normalize the market to a healthy pace.”

A supply imbalance can stress any market, and Gustafson joked that the current imbalance reminded her of a favorite quote from the movie Super Troopers: “Desperation is a stinky cologne.” “We’re all still a little crazed where this imbalance has put us, but for the patient investor and owner, there will be a rebalancing and opportunity for the good quality real estate to pass the sniff test,” she said.

At Bircher, Gustafson said that mid-pandemic, there were predictions that one billion square feet of new product would be required to meet tenant demand, e-commerce growth and safety stock. That transition opened a great opportunity for investors to run at the goal. “In California, the entitlement process is lengthy, around 24-36 months to get from the start of an acquisition to the completion of a building,” she said. Fast forward to 2023-2024, a lot of what is being delivered in 2024 is the result of that chase.

“Being an optimistic developer, there is good news. The supply imbalance helped normalize what was an unsustainable surge in rents and land values,” she said. “It allowed corporate heads of real estate to proactively evaluate growth opportunities, opened the door for contrarian investors to land bank as values drop, and provided tenants with options as there is more product. Investment goals and strategies have shifted, and that’s created opportunity for buyers.”

“Developers only know how to run and develop as much as we can,” said Roski. “There are certain times in cycles that we are forced to slow down, which is a good thing. In the last few years, Majestic has delivered 12-14 million square feet, and this year we are developing 6-8 million square feet. It’s all part of the cycle.”

Creecy-Herman noted that compared to the other asset classes and opportunities out there, including office and multifamily, industrial remains much more attractive for investment. “That was absolutely one of the things that underpinned the amount of investment we saw in a relatively short time period,” she said.

Market rent growth across Los Angeles, Inland Empire and Orange County moved up more than 100% in a 24-month period. That created opportunities for landlords to flexible as they’re filling up their buildings. “Normalizing can be uncomfortable especially after that kind of historic high, but at the same time it’s setting us up for strong years ahead,” she said.

Issues that owners and landlords are facing with not as much movement in the market is driving a change in strategy, noted Gustafson. “Comps are all over the place,” she said. “You have to dive deep into every single deal that is done to understand it and how investment strategies are changing.”

Tenants experienced a variety of challenges in the pandemic years, from supply chain to labor shortages on the negative side, to increased demand for products on the positive, McCombs noted.

“Prologis has about 6,700 customers around the world, from small to large, and the universal lesson [from the pandemic] is taking a more conservative posture on inventories,” Creecy-Herman said. “Customers are beefing up inventories, and that conservatism in the supply chain is a lesson learned that’s going to stick with us for a long time.” She noted that the company has plenty of clients who want to take more space but are waiting on more certainty from the broader economy.

“E-commerce grew by 8% last year, and we think that’s going to accelerate to 10% this year. This is still less than 25% of all retail sales, so the acceleration we’re going to see in e-commerce… is going to drive the business forward for a long time,” she said.

Roski noted that customers continually re-evaluate their warehouse locations, expanding during the pandemic and now consolidating but staying within one delivery day of vast consumer bases.

“This is a generational change,” said Creecy-Herman. “Millions of young consumers have one-day delivery as a baseline for their shopping experience. Think of what this means for our business long term to help our customers meet these expectations.”

McCombs asked the panelists what kind of leasing activity they are experiencing as a return to normalcy is expected in 2024.

“During the pandemic, shifts in the ports and supply chain created a build up along the Mexican border,” said Roski, noting border towns’ importance to increased manufacturing in Mexico. A shift of populations out of California and into Arizona, Nevada, Texas and Florida have resulted in an expansion of warehouses in those markets.

Eldridge said that Salt Lake City’s “sweet spot” is 100-200 million square feet, noting that the market is best described as a mid-box distribution hub that is close to California and Midwest markets. “Our location opens up the entire U.S. to our market, and it’s continuing to grow,” she said.

The recent supply chain and West Coast port clogs prompted significant investment in nearshoring and port improvements. “Ports are always changing,” said Roski, listing a looming strike at East Coast ports, challenges with pirates in the Suez Canal, and water issues in the Panama Canal. “Companies used to fix on one port and that’s where they’d bring in their imports, but now see they need to be [bring product] in a couple of places.”

“Laredo, [Texas,] is one of the largest ports in the U.S., and there’s no water. It’s trucks coming across the border. Companies have learned to be nimble and not focused on one area,” she said.

“All of the markets in the southwest are becoming more interconnected and interdependent than they were previously,” Creecy-Herman said. “In Southern California, there are 10 markets within 500 miles with over 25 million consumers who spend, on average, 10% more than typical U.S. consumers.” Combined with the port complex, those fundamentals aren’t changing. Creecy-Herman noted that it’s less of a California exodus than it is a complementary strategy where customers are taking space in other markets as they grow. In the last 10 years, she noted there has been significant maturation of markets such as Las Vegas and Phoenix. As they’ve become more diversified, customers want to have a presence there.

In the last decade, Gustafson said, the consumer base has shifted. Tenants continue to change strategies to adapt, such as hub-and-spoke approaches. From an investment perspective, she said that strategies change weekly in response to market dynamics that are unprecedented.

McCombs said that construction challenges and utility constraints have been compounded by increased demand for water and power.

“Those are big issues from the beginning when we’re deciding on whether to buy the dirt, and another decision during construction,” Roski said. “In some markets, we order transformers more than a year before they are needed. Otherwise, the time comes [to use them] and we can’t get them. It’s a new dynamic of how leases are structured because it’s something that’s out of our control.” She noted that it’s becoming a bigger issue with electrification of cars, trucks and real estate, and the U.S. power grid is not prepared to handle it.

Salt Lake City’s land constraints play a role in site selection, said Eldridge. “Land values of areas near water are skyrocketing.”

The panelists agreed that a favorable outlook is ahead for 2024, and today’s rebalancing will drive a healthy industry in the future as demand and rates return to normalized levels, creating opportunities for investors, developers and tenants.

This post is brought to you by JLL, the social media and conference blog sponsor of NAIOP’s I.CON West 2024. Learn more about JLL at www.us.jll.com or www.jll.ca.

fed pandemic covid-19 real estate interest rates mexico

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Four Years Ago This Week, Freedom Was Torched

Red Candle In The Wind

The SNF Institute for Global Infectious Disease Research announces new advisory board

CDC Warns Thousands Of Children Sent To ER After Taking Common Sleep Aid

Analyst reviews Apple stock price target amid challenges

Economic Trends, Risks and the Industrial Market

Association of prenatal vitamins and metals with epigenetic aging at birth and in childhood

SoCal Industrial Prioritizes Speed, Power and Sustainability

Chronic stress and inflammation linked to societal and environmental impacts in new study

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges