Uncategorized

Futures Slide As Fed Pauses Rate Hikes, Regional Banks Resume Plunge

Futures Slide As Fed Pauses Rate Hikes, Regional Banks Resume Plunge

US stocks were set to open lower, reversing a modest gain earlier and…

Share this:

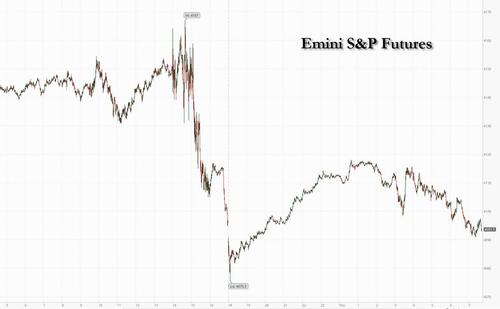

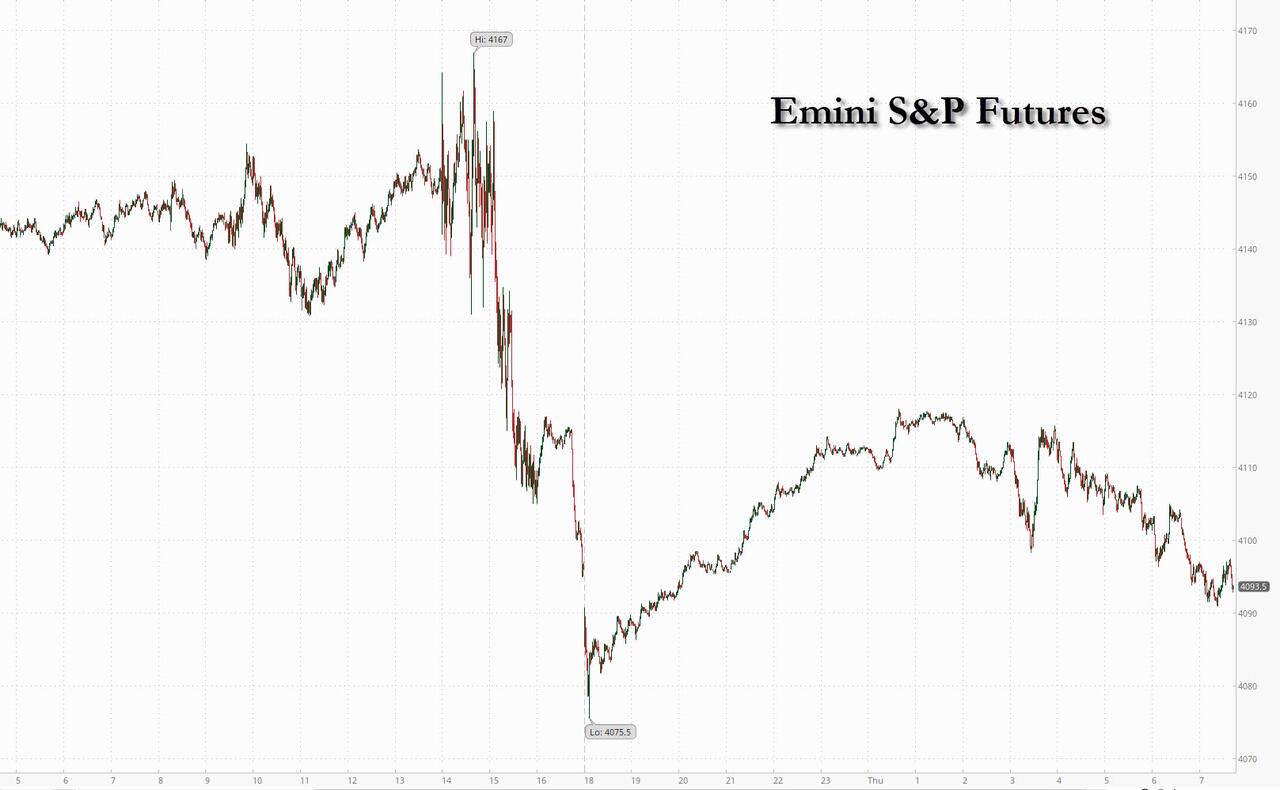

US stocks were set to open lower, reversing a modest gain earlier and extending a three-day selloff as investors weighed the possibility of more bank failures against a pause in rate hikes by the Federal Reserve as growth slows. Contracts on the S&P 500 were down 0.3% as of 7:45 a.m. ET while Nasdaq 100 futures were flat. The benchmark S&P 500 had slid on Wednesday, marking its longest losing streak in nearly two months even as the Fed signaled a possible pause in its most aggressive tightening campaign in decades. Sentiment was routed as US regional banks tumbled further even after PacWest said its deposits rose since March and confirmed a Bloomberg report that it’s talking with potential investors in a bid to calm markets. The stock slumped as much as 45% premarket. And Western Alliance was down 23%, though it claimed it hasn’t seen unusual deposit flows.

Treasury yields kneejerked higher but have also since reversed as worries over the impending debt-ceiling deadline weigh. A measure of the dollar is weakening as traders hike recession bets, and gold has steadied after jumping to just shy of record highs on news that the Fed may pause tightening. Iron ore is declining, while copper gains as concerns mount around global supply. Oil rose, recovering after a sudden dip early in the session on Thursday as Chinese traders returned after a break.

In premarket trading, PacWest Bancorp shares slumped as much as 46% with other regional lenders also plunging, after the Los Angeles-based bank confirmed that it is weighing strategic options. Western Alliance shares fell as much as 24%, headed for a fifth straight day of declines, as confidence in regional lenders remains shaky. The Arizona-based lender sought to reassure the market with an update on deposits after US markets closed, saying that it hasn’t seen unusual deposit flows following the sale of First Republic Bank. First Horizon stock was thrashed after TD terminated its planned $13.4 billion acquisition of the Memphis-based bank, citing uncertainty over a regulatory approval timeline. TD will fork out $200 million in cash to get out of the deal. TripAdvisor also dropped after the online travel company reported first-quarter adjusted earnings per share that missed consensus estimates. On the other end, Arconic surged 28% after a report that private equity firm Apollo Global Management was nearing a deal to buy the industrial-parts manufacturer. Here are all the notable premarket movers:

- Qualcomm falls as much as ~6.7% in premarket trading, after the chipmaker gave a third-quarter forecast that was weaker than expected. Analysts say the guidance shows that weakness in the smartphone market will persist until September.

- TripAdvisor shares drop 8.2% in premarket trading after the online travel company reported first-quarter adjusted earnings per share that missed consensus. Analysts flagged the performance of the company’s Viator business, which they said was the main driver behind the miss on adjusted Ebitda.

- Upwork shares drop as much as 14% in US premarket trading, set to hit a three-year low, after the online recruitment company cut its full-year revenue forecast. Analysts lowered their price targets on the stock, seeing an impact on spending from a tough macroeconomic backdrop, though some brokers were positive on the steps the company is taking to progress toward profitability.

- Etsy shares gained in extended trading, after the online retailer reported first- quarter results that beat expectations and gave an outlook that Bloomberg Intelligence sees as encouraging.

- Zillow Group advanced in extended trading, after the online real estate company gave a revenue outlook for the current period that at the midpoint of the forecast range topped the average analyst estimate. Analysts are positive on the report, and highlight the company’s Premier Agent offering as notably strong.

US stocks slumped to start the month of May as glum economic data has fueled concerns about a possible recession. The Fed on Wednesday hiked rates as expected, while pausing the tightening process even as Chair Jerome Powell said his forecast was for modest growth and not a recession, and said he disagrees with the staff's bearish consensus. But he reiterated that the process of getting inflation down had a long way to go.

Susannah Streeter, head of money and markets at Hargreaves Lansdown, said hopes that a rate cut might come before the end of the year faded after the Fed’s statement. “It’s clear inflation is still not coming down as fast as policymakers hoped,” she said. “It looks like the hiking cycle is now at an end, but the door to another rise is still slightly ajar and that’s still causing nervousness given that rates are already at the highest level for 16 years.”

“The tightening in credit conditions will put some significant downward pressure on the economy,” Michelle Girard, head of US for NatWest Markets, said on Bloomberg Television. “You will see the Fed in a position to move policy to a less restrictive stance sooner than what the Fed chairman today was suggesting.”

Meanwhile, strategists at UBS Global Wealth Management said even a pause in hikes by the Fed may not necessarily spur a rally in equities as those expectations should now be baked in. In past cycles, the S&P 500 typically didn’t bottom until after the Fed started to cut rates, the team led by Mark Haefele wrote in a note.

“The ECB meeting is expected to be a more complex one compared to that of the Federal Reserve,” said Erick Muller, director of product and investment strategy at Muzinich & Co. “If no one doubts the ECB will raise rates again at this week meeting, the magnitude of the rise and the tone of the communication are difficult to forecast.”

European stocks are on the back foot as investors count down to a rate decision from the European Central Bank later today. The Stoxx 600 is down 0.7% with media, real estate and autos the worst-performing sectors. Energy names have outperformed, led higher by Shell who maintained the pace of share buybacks after quarterly profit topped estimates. Here are the most notable European movers:

- Shell rises as much as 3.5%, the most since April 3, after the oil major’s quarterly profit beat expectations, with strong performances across divisions and particularly its gas business, analysts say

- Equinor rises as much as 4.4% after reporting 1Q profits that beat estimates. Analysts say the firm exceeded expectations across all key divisions as higher production offset lower oil and gas prices

- Hargreaves Lansdown shares rise as much as 4.5% after the investment platform’s net new business flows in its fiscal 3Q topped expectations, offsetting a small deterioration in asset retention

- Next shares rise as much as 2.7%, best performer in the Stoxx 600 Retail Index, after the UK clothing and furnishings seller’s 1Q sales beat estimates despite the cold weather

- Scout24 rises as much as 4.4% after digital marketplace operator reported better-than-expected revenue and Ebitda in 1Q thanks to strong growth in its core business as well as cost cuts

- Novo Nordisk falls as much as 6.5% after its blockbuster obesity drug Wegovy missed estimates due to supply woes. Analysts say their 1Q update, while beating expectations, otherwise held few surprises

- Airbus shares fell as much as 3.2% as analysts said the quarterly update indicates continued supply-chain challenges at the planemaker, which may weigh further on its delivery numbers for the year

- Zalando shares drop as much as 7.7% to the lowest since March after the online fast fashion retailer reported 1Q earnings, with Citigroup analysts noting caution around elevated inventory levels

- Leonardo falls as much as 7.5% and are the lead decliners on the FTSE MIB index after the Italian defense company reported what analysts called disappointing first-quarter results at the Ebita level

- Rheinmetall shares fall 3.8% after the German defense company’s first quarter operating profit misses estimates due to rising costs. Stifel says results were expected to be weak but “came in weaker”

- Virgin Money shares drop as much as 11%, the most since November 2020, as analysts flagged higher costs and impairments for the UK lender, which offset a small net interest income beat

- Casino shares plunge as much as 17% after the debt- laden French supermarket operator reported 1Q sales that missed the average analyst estimate

Earlier in the session, Asian stocks climbed as the dollar weakened on bets the Federal Reserve will pause interest-rate hikes, while Chinese shares ended flat as traders returned from the Golden Week holiday. The MSCI Asia Pacific Index advanced as much as 0.6%. The Fed hinted the latest hike could be the last one in its policy decision Wednesday, although pushed back against market expectations of rate cuts this year. Utilities and energy shares led broad-based gains. Onshore China stocks pared losses to close little changed as trading resumed following the Golden Week holidays. Concerns remain about the pace of China’s economic rebound despite strong holiday spending figures, as data showed factory activity struggled in April. Benchmarks in Hong Kong led gains in the region after falling in the previous session.

Expectations of lower US interest rates and a weaker dollar are boosting bets of outperformance for Asian equities as borrowing costs decline and US equities are weighed down by recession risks. The MSCI Asia Pacific Index is up about 3.6% this year, lagging the S&P 500. “While a lot of people are focused on the dollar smile theory, saying risk off is good for the dollar, when the epicenter is the US that’s not necessarily the case,” Steve Brice, group chief investment officer at Standard Chartered Wealth Management, told Bloomberg Television. “If you look at the growth differentials between the developed world and Asia, and also the dollar outlook, it paints a picture of Asian equity outperformance.”

In FX, the Bloomberg Dollar Index is flat having pared an earlier drop. The Swiss franc is the weakest among the G-10 currencies while the Norwegian krone sits atop the intraday rankings after the Norges Bank hiked 25bps and signaled more tightening ahead.

In rates, US yields have recouped some of Wednesday’s post-Fed losses with two-year borrowing costs initially rising 6bps to 3.86% but then sliding back to 3.81%. Treasuries are slightly cheaper across the curve along with European bond markets ahead of ECB rate decision at 8:15am New York time. US stock futures had opening gap lower as regional lenders continued to slump but have pared losses. US yields are higher by less than 2bp across the curve with spreads narrowly mixed after steepening sharply after Wednesday’s Fed rate increase and pause signal; 10-year yields around 3.34% outperforms bunds and gilts by ~1bp.

In commodities, crude futures advance with WTI rising 0.9% to trade near $69.20 after whipsawing at the open. Spot gold is down 0.2% around $2,035.

Bitcoin is essentially unchanged, pivoting the USD 29k mark in parameters that are even thinner than those seen at this time yesterday.

To the day ahead now, and the main highlight will be the ECB’s policy decision and President Lagarde’s press conference. We’ll also get the final services and composite PMIs from Europe for April, Euro Area PPI for March, and from the US there’s the weekly initial jobless claims, the March trade balance, and nonfarm productivity in Q1. Otherwise, earnings releases include Apple. And local elections will be taking place in the UK.

Market Wrap

- S&P 500 futures down 0.3% at 4,093.5

- STOXX Europe 600 down 0.4% to 460.71

- MXAP up 0.5% to 161.32

- MXAPJ up 0.6% to 514.21

- Nikkei up 0.1% to 29,157.95

- Topix down 0.1% to 2,075.53

- Hang Seng Index up 1.3% to 19,948.73

- Shanghai Composite up 0.8% to 3,350.46

- Sensex up 0.5% to 61,505.99

- Australia S&P/ASX 200 little changed at 7,193.11

- Kospi little changed at 2,500.94

- German 10Y yield little changed at 2.27%

- Euro down 0.2% to $1.1045

- Brent Futures up 1.2% to $73.23/bbl

- Gold spot down 0.2% to $2,033.95

- U.S. Dollar Index little changed at 101.37

Top Overnight News

- Chinese tourist spending during one of the country’s most important national holidays has exceeded pre-pandemic levels for the first time, authorities said, in a sign of economic momentum after China ended its coronavirus containment policies. FT

- China’s Caixin manufacturing PMI fell short of expectations in April, dipping into contraction territory at 49.5 (vs. the Street consensus of 50 and down from 50 in March). RTRS

- China's fight against a weaponized dollar puts the yuan front and center. Its use in contracts for everything from oil to nickel is gathering speed and its share of global trade finance has tripled since the end of 2019. The US remains the world's clear financial hegemon, but these moves help China play a bigger role in the international financial system. BBG

- The ECB is set to slow the pace of rate hikes, matching the Fed's 25-bp move yesterday and taking the key rate to 3.25%, after its preferred inflation measure eased for the first time in 10 months. BBG

- Regional banks remain in focus after PACW announced post-close they are weighing strategic options (deposits rose since March). FHN -40% pre mkt after TD scrapped its planned $13.4 billion acquisition of the Memphis-based bank, citing uncertainty over a regulatory approval timeline. TD will pay $200 million in cash to First Horizon. FT

- Leaders on both sides of the aisle in Washington insist they won’t enact a short-term debt ceiling fix to allow more time for negotiations on a larger fiscal package. Politico

- Bill Isaac, a former regulator credited with stabilizing the US banking system during the 1980s crisis has hit out at the decision to sell First Republic to JPMorgan Chase as he warned of “more problems” to come for regional lenders. “We are kidding ourselves if we think there are only four problem banks in the country,” Isaac said. “We have not gotten that smart. It’s been so long since we had a lot of problems, that I can’t help but think that there are going to be more problems.” FT

- Apple's sales may have dropped for a second quarter when it reports postmarket, though share buybacks may hold up. Analysts see revenue down 5% year on year, though Bloomberg Intelligence expects higher-end iPhone sales to help the gross margin as Mac sales underwhelm. In other earnings, Peloton is up before the bell, while Lyft and Carvana report later. BBG

- Biden's Fed picks. He's chosen current Governor Philip Jefferson for a promotion to vice chair and will nominate economist Adriana Kugler to an open board slot, people familiar said. The selections may be announced tomorrow. Jefferson voted to raise rates by 25 bps yesterday. Kugler is currently the World Bank's executive director for the US. BBG

- Almost half of US adults say they’re worried about the safety of their deposits in banks and other financial institutions — levels of concern as high or higher than during the 2008 financial crisis....(BBG)

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed in the aftermath of the FOMC meeting where the Fed delivered a widely expected 25bps rate hike and paved the way for a pause, although Fed Chair Powell pushed back against cutting rates this year and alluded to banks tightening lending standards and slowing the pace of lending. ASX 200 was lacklustre amid weakness in its top-weighted financial sector after big four bank NAB's H1 profit missed analysts’ estimates, although losses were cushioned by resilience in mining names and improved trade data. KOSPI was subdued as participants digested mixed earnings results, while Nikkei 225 remain closed. Hang Seng and Shanghai Comp. were firmer as mainland participants returned from the golden week break with Chinese markets shrugging off the surprise contraction in Caixin Manufacturing PMI and the PBoC’s significant liquidity drain, as well as the HKMA’s 25bps rate hike in lockstep with the Fed.

Top Asian News

- PBoC injected CNY 33bln via 7-day reverse repos with the rate at 2.00% for a CNY 529bln net drain.

- HKMA raised its base rate by 25bps to 5.50%, as expected.

- Chinese airlines will be allowed to expand their flights to the US, according to FT.

European equities, Euro Stoxx 50 -0.7%, trade mostly lower following the post-FOMC selling pressure in US indices. Equity sectors in Europe are mostly lower in what has been a busy morning for corporates. To the downside, Media and Auto names lag while Energy names are the clear outperformer in what has been a tough week for the sector amid declines in underlying crude prices, with upside also spurred by Shell's +1.8% update. US equity futures have spent the morning slightly better than flat in an attempted recovery following the Fed rate decision and further jitters on the regional banking front, with PACW's shares plunging over 50% in after hours trade. PacWest (PACW) has reportedly been approached by several potential partners and investors, according to Bloomberg.. -35% in the pre-market.

Top European News

- UK March Mortgage Approvals Unexpectedly Rise to 5-Month High

- UK April Composite PMI 54.9 vs Flash Reading 53.9

- Norway Hikes by Quarter-Point Again as Krone Woes Fester

- European Gas Prices Ease as IEA Sees Weaker Demand This Year

- Bud Light Brewer AB InBev Beats Forecasts on Strong Pricing

- Casino Plunges After 1Q Net Sales Misses Estimates

- European Stocks Retreat as Investors Await ECB After Fed Hike

FX

- DXY defends 101.000 in post-FOMC aftermath, as EUR/USD rejects 1.1100 in the run-up to the ECB amidst mixed EZ PMIs and a raft of hefty option expiries.

- Kiwi retains momentum above 0.6200 vs Buck and around 1.0700 vs Aussie as NZ building consents rebound firmly, AUD/USD underpinned within a 0.6699-41 band after export-led wider than forecast trade surplus.

- Pound perky near new YTD peak vs Buck just under 1.2600 with impetus from upgraded UK services and composite PMIs.

- PBoC set USD/CNY mid-point at 6.9054 vs exp. 6.9061 (prev. 6.9240)

- Norges Bank Key Policy Rate: 3.25% vs. Exp. 3.25% (Prev. 3.0%); policy rate will most likely be raised further in June. If NOK remains weaker than projected or pressures in the economy persist, a higher policy rate than envisaged earlier may be needed.

- Brazil Central Bank maintained the Selic rate at 13.75%, as expected. BCB said it will assess if the strategy of maintaining the Selic rate for a long period will be sufficient to ensure the convergence of inflation to the target and will persist in its strategy until consolidating disinflation and anchoring expectations around its targets.

Fixed Income

- Treasuries retain their bull-steepening trajectory post-Fed and ahead of several US data points, with T-notes holding above 116-00.

- Bunds probe 136.00 from 136.66 a peak as ECB looms and hawkish guidance is seen accompanying a 25 bp hike.

- Gilts teeter towards base of 101.37-93 range after upwardly revised UK services and composite PMIs.

Commodities

- WTI and Brent futures are firmer following the recent hefty losses in the complex. WTI June and Brent July slumped to lows of USD 63.64/bbl and USD 71.28/bbl respectively overnight as futures reopened amid banking sector woes.

- Spot gold shot higher by some USD 40/oz overnight, very briefly to a fresh all-time high on some charts, north of USD 2,080/oz. The yellow metal then immediately pulled back to levels under USD 2,050/oz and trades lower intraday in the European morning.

- Base metals are mostly firmer, underpinned by the return of the markets largest purchaser China from a five-day holiday.

- Shell (SHEL LN) CEO says they are getting close to Chinese levels of oil demand last seen in 2019; sees strong rebound in gas demand in China's services sectors, but less in the industrial sectors.

Geopolitics

- An oil refinery in Krasnodar Krai, southern Russia caught fire after a drone attack, according to TASS.

- The governor of the Russian Voronezh region announces that the air defenses shot down a drone over the city, according to Sky News Arabia citing Tass.

- Russian Foreign Ministry says "Moscow will quickly deal with Kiev's terrorist and subversive activities", via Al Jazeera.

- Indian and Russia suspend negotiations to settle bilateral trade in Rupees, Russia reportedly not willing to amass INR as trade gap remains large, via Reuters citing sources.

- Russia's Kremlin says we know decisions about such terrorist acts are taking in Washington and not Kyiv; Washington is definitely behind the attack, Kremlin is well aware of this; Russia has multiple response options, response will be thought-out.

US Event Calendar

- 07:30: April Challenger Job Cuts 175.9% YoY, prior 319.4%

- 08:30: April Initial Jobless Claims, est. 240,000, prior 230,000

- April Continuing Claims, est. 1.87m, prior 1.86m

- 08:30: March Trade Balance, est. -$63.1b, prior -$70.5b

- 08:30: 1Q Unit Labor Costs, est. 5.5%, prior 3.2%

- 08:30: 1Q Nonfarm Productivity, est. -2.0%, prior 1.7%

DB's Jim Reid concludes the overnight wrap

With the combination of a Fed that is now fully data dependent and further woes in the US regional banking sector before and after the closing bell, a decent survey question today might be, “when will the Fed next raise rates?”. I’d imagine the bid-offer would be somewhere between next month and only in 10 years’ time. Monetary policy clearly operates with a lag and the current US regional banking woes might be near the early stages of the fallout from this tighter policy rather than the end of it. That is a big worry. Before we recap the latest regional banking woes, let’s take a look at the Fed.

They delivered the expected 25bps hike last night with the upper bound of the target policy rate now 5.25%, the highest level it has been since 2007. The Fed also maintained their monthly pace of shrinking the balance sheet by $60bn for Treasuries and $35bn for MBS. It was a unanimous decision but the Fed dropped the phrase “some additional policy firming may be appropriate.” Fed Chair Powell called the removal of the phrase “meaningful”. The Fed pointed to inflation, labour-market strength, and credit conditions as factors they will be watching to decide future policy decisions. By doing away with forward guidance and transitioning to a more “data-dependent approach”, as Chair Powell said, the Fed opened the door to pausing rate hikes next meeting.

At the press conference, Chair Powell once again addressed the recent strains in the banking system following regulators seizing First Republic on Monday. He noted that the conditions in the banking sector “broadly improved” since early March and that the financial stability tools are not at odds with the monetary policy tools. Chair Powell noted that the banking system is “sound and resilient” but that the issues in the sector are further tightening lending conditions for small businesses and households. On credit conditions, Chair Powell – who received the Senior Loan Officer Survey data ahead of the meeting – said that “these tighter credit conditions are likely to weigh on economic activity, hiring and inflation.”

He also noted that the survey results are consistent with what policy makers have said and other data points have showed recently – namely that lending has grown in aggregate but the pace has slowed since 2H’22. When discussing a possible recession, Chair Powell acknowledged that a mild recession is possible as the Fed’s staff forecast shows, but that “the case of avoiding a recession is in (his) view more likely than that of having a recession.” On this he pointed to the excess demand in the labour market which seems to be cooling without a surge of unemployment seen in previous periods. Lastly on a question about the current market pricing of rate cuts in 2023, Chair Powell cautioned that the FOMC is not expecting inflation to come down that quickly and that rate cuts would not be appropriate, hence why it is not in their forecast. Fed futures are now pricing in a -11.5% chance of a rate cut in June and 82.7bps of cuts by year-end. However, before the after-market weakness in regional banks fed futures closed yesterday with a smaller chance of a cut next meeting (5%). See Matt Luzzetti’s review of the FOMC here. He continues to believe that the Fed is now done but that the first cut won’t come until Q1 2024.

Before the FOMC decision, US 2 year Treasury yields were down -2.9bps with 10 year yields down around -4.5bps. The S&P 500 was up +0.33%, with the USD index down -0.5%. As the statement came out, the dollar sold off initially whilst yields and equities rose. However there was a reversal during the last hour or so of US trading with equities selling off -1.4% from just after Powell started his presser to see the S&P 500 finish -0.70% lower on the day. US 10 year yields continued to fall after a brief rate selloff with yields finishing near their lows of the day down -8.8bps at 3.335%, as 2 year yields fell -15.6bps to 3.805. That’s the lowest the 2yr and 10yr yield has been in nearly a month and down an impressive -36bps and -27bps from their intra-day peaks on Monday just before the close.

Expanding on the equity moves, 20 of 24 industry sectors were lower on the day led by further weakness in cyclicals and banks. The KBW bank index was -1.89% lower as every member ended the day lower, as regionals were under pressure yet again. PacWest Bancorp, which was down -42% over the last 5 sessions and trading at its lowest share price since March 2009, announced after the US close that it has been approached by several partners and investors. The stock was down -52.49% in after-market trading. The news and weakness of the California-based lender caused fellow regional banks Western Alliance Bancorp to fall -22.42% after-hours and Zion Bank to decline -9.09%.

With the Fed now out of the way, attention will turn to the ECB today as they make their own policy decision. In terms of what to expect, both the consensus and DB view is that they’ll slow down their rate hikes to a 25bp pace, which would take the deposit rate up to 3.25%. However, as our European economists write in their preview (link here), it’s a close call between that and 50bps, since underlying inflation remains high and a rapid return to target is far from proven. So irrespective of how much they hike by, their view is that the underlying and conditional message will be that the tightening cycle isn’t over yet. Moreover, to stop financial conditions from overreacting to a slower hike, they expect the ECB to announce faster QT, with an increase in the roll-off of APP reinvestments from €15bn per month to €20bn per month from Q3.

As we look forward to the ECB decision, European markets had put in a decent performance ahead of the Fed as we got several positive data releases from both sides of the Atlantic. In the US, the ADP’s report of private payrolls showed growth of +296k in April (vs. 150k expected), which was the strongest print since July and also above every economist’s expectation on Bloomberg. Then the ISM services index came in at 51.9 (vs. 51.8 expected), and there was also upward movement in the new orders component, which rose to 56.1. Meanwhile in the Euro Area, unemployment hit a new record low in March at 6.5% (vs. 6.6% expected). That helped the STOXX 600 (+0.31%) to recover some of the previous day’s declines but it may well all change again this morning. 10yr yields also fell back, with those on bunds (-1.1bps), OATs (-1.9bps) and BTPs (-5.5bps) all moving lower.

Despite the positive data from yesterday, commodity prices took another hit from growing fears about a recession and what that would mean for energy demand. Indeed, Brent crude fell -3.97% to close at $72.33/bbl, which is its lowest level since December 2021. It was a similar story for European natural gas prices (-1.99%), which came down to their lowest since July 2021 at €36.78/MWh. So these are big positive tailwinds for the ECB as they make their decision today, and show how the prospect of a downturn has more than outweighed the effect from the OPEC+ group limiting output only a month earlier.

This morning in Asia equity markets are mixed. Across the region, the Hang Seng (+0.96%) is outperforming with the Shanghai Composite (+0.54%) also trading in positive territory while the CSI (-0.10%) and the KOSPI (-0.22%) are slightly lower in early trade. Elsewhere, markets in Japan are closed for a holiday. In overnight trading, US stock futures have recovered with those on the S&P 500 (+0.14%) and NASDAQ 100 (+0.40%) turning positive, indicating a recovery in risk appetite.

In early morning data, we have Chinese manufacturing activity slipping into contraction territory for the first time in 3 months as the Caixin manufacturing PMI fell to 49.5 in April from 50.0 in March, reflecting weakening market demand. Elsewhere, Australia’s trade surplus grew to a nine-month high of A$15.27 billion in March, surpassing market expectations for a surplus of A$13.0 billion, as well as February’s revised reading of A$14.15 billion, as commodity demand picked up.

On the political side, keep an eye out on the UK today, since local elections are taking place in England that will be the biggest electoral test for the main parties ahead of the next general election. In terms of where things currently stand, Politico’s polling average shows that the opposition Labour Party has a 16-point lead over the governing Conservatives, which is the biggest lead they’ve had going into a set of elections since the early 2000s. So Labour are widely expected to make gains at the Conservatives’ expense today. The more important question will be how many, and according to local election experts Rallings and Thrasher, Labour will be wanting to make gains in the high-hundreds of council seats to persuasively argue they’re on track to return to government. For the Conservatives, current polls imply they could lose over 1,000 council seats, but if they can limit that to around 750, it would suggest things aren’t as bad for them right now as the polls might suggest.

To the day ahead now, and the main highlight will be the ECB’s policy decision and President Lagarde’s press conference. We’ll also get the final services and composite PMIs from Europe for April, Euro Area PPI for March, and from the US there’s the weekly initial jobless claims, the March trade balance, and nonfarm productivity in Q1. Otherwise, earnings releases include Apple. And local elections will be taking place in the UK.

Uncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Uncategorized

Economic Earthquake Ahead? The Cracks Are Spreading Fast

Economic Earthquake Ahead? The Cracks Are Spreading Fast

Authored by Brandon Smith via Alt-Market.us,

One of my favorite false narratives…

Share this:

{kind=link}

{kind=link}

Authored by Brandon Smith via Alt-Market.us,

One of my favorite false narratives floating around corporate media platforms has been the argument that the American people “just don’t seem to understand how good the economy really is right now.” If only they would look at the stats, they would realize that we are in the middle of a financial renaissance, right? It must be that people have been brainwashed by negative press from conservative sources…

{kind=link}

I have to laugh at this notion because it’s a very common one throughout history – it’s an assertion made by almost every single political regime right before a major collapse. These people always say the same things, and when you study economics as long as I have you can’t help but throw up your hands and marvel at their dedication to the propaganda.

One example that comes to mind immediately is the delusional optimism of the “roaring” 1920s and the lead up to the Great Depression. At the time around 60% of the U.S. population was living in poverty conditions (according to the metrics of the decade) earning less than $2000 a year. However, in the years after WWI ravaged Europe, America’s economic power was considered unrivaled.

The 1920s was an era of mass production and rampant consumerism but it was all fueled by easy access to debt, a condition which had not really existed before in America. It was this illusion of prosperity created by the unchecked application of credit that eventually led to the massive stock market bubble and the crash of 1929. This implosion, along with the Federal Reserve’s policy of raising interest rates into economic weakness, created a black hole in the U.S. financial system for over a decade.

There are two primary tools that various failing regimes will often use to distort the true conditions of the economy: Debt and inflation. In the case of America today, we are experiencing BOTH problems simultaneously and this has made certain economic indicators appear healthy when they are, in fact, highly unstable. The average American knows this is the case because they see the effects everyday. They see the damage to their wallets, to their buying power, in the jobs market and in their quality of life. This is why public faith in the economy has been stuck in the dregs since 2021.

The establishment can flash out-of-context stats in people’s faces, but they can’t force the populace to see a recovery that simply does not exist. Let’s go through a short list of the most faulty indicators and the real reasons why the fiscal picture is not a rosy as the media would like us to believe…

The “miracle” labor market recovery

In the case of the U.S. labor market, we have a clear example of distortion through inflation. The $8 trillion+ dropped on the economy in the first 18 months of the pandemic response sent the system over the edge into stagflation land. Helicopter money has a habit of doing two things very well: Blowing up a bubble in stock markets and blowing up a bubble in retail. Hence, the massive rush by Americans to go out and buy, followed by the sudden labor shortage and the race to hire (mostly for low wage part-time jobs).

The problem with this “miracle” is that inflation leads to price explosions, which we have already experienced. The average American is spending around 30% more for goods, services and housing compared to what they were spending in 2020. This is what happens when you have too much money chasing too few goods and limited production.

The jobs market looks great on paper, but the majority of jobs generated in the past few years are jobs that returned after the covid lockdowns ended. The rest are jobs created through monetary stimulus and the artificial retail rush. Part time low wage service sector jobs are not going to keep the country rolling for very long in a stagflation environment. The question is, what happens now that the stimulus punch bowl has been removed?

Just as we witnessed in the 1920s, Americans have turned to debt to make up for higher prices and stagnant wages by maxing out their credit cards. With the central bank keeping interest rates high, the credit safety net will soon falter. This condition also goes for businesses; the same businesses that will jump headlong into mass layoffs when they realize the party is over. It happened during the Great Depression and it will happen again today.

Cracks in the foundation

We saw cracks in the narrative of the financial structure in 2023 with the banking crisis, and without the Federal Reserve backstop policy many more small and medium banks would have dropped dead. The weakness of U.S. banks is offset by the relative strength of the U.S. dollar, which lures in foreign investors hoping to protect their wealth using dollar denominated assets.

But something is amiss. Gold and bitcoin have rocketed higher along with economically sensitive assets and the dollar. This is the opposite of what’s supposed to happen. Gold and BTC are supposed to be hedges against a weak dollar and a weak economy, right? If global faith in the dollar and in the U.S. economy is so high, why are investors diving into protective assets like gold?

Again, as noted above, inflation distorts everything.

Tens of trillions of extra dollars printed by the Fed are floating around and it’s no surprise that much of that cash is flooding into the economy which simply pushes higher right along with prices on the shelf. But, gold and bitcoin are telling us a more honest story about what’s really happening.

Right now, the U.S. government is adding around $600 billion per month to the national debt as the Fed holds rates higher to fight inflation. This debt is going to crush America’s financial standing for global investors who will eventually ask HOW the U.S. is going to handle that growing millstone? As I predicted years ago, the Fed has created a perfect Catch-22 scenario in which the U.S. must either return to rampant inflation, or, face a debt crisis. In either case, U.S. dollar-denominated assets will lose their appeal and their prices will plummet.

“Healthy” GDP is a complete farce

GDP is the most common out-of-context stat used by governments to convince the citizenry that all is well. It is yet another stat that is entirely manipulated by inflation. It is also manipulated by the way in which modern governments define “economic activity.”

GDP is primarily driven by spending. Meaning, the higher inflation goes, the higher prices go, and the higher GDP climbs (to a point). Eventually prices go too high, credit cards tap out and spending ceases. But, for a short time inflation makes GDP (as well as retail sales) look good.

Another factor that creates a bubble is the fact that government spending is actually included in the calculation of GDP. That’s right, every dollar of your tax money that the government wastes helps the establishment by propping up GDP numbers. This is why government spending increases will never stop – It’s too valuable for them to spend as a way to make the economy appear healthier than it is.

The REAL economy is eclipsing the fake economy

The bottom line is that Americans used to be able to ignore the warning signs because their bank accounts were not being directly affected. This is over. Now, every person in the country is dealing with a massive decline in buying power and higher prices across the board on everything – from food and fuel to housing and financial assets alike. Even the wealthy are seeing a compression to their profit and many are struggling to keep their businesses in the black.

The unfortunate truth is that the elections of 2024 will probably be the turning point at which the whole edifice comes tumbling down. Even if the public votes for change, the system is already broken and cannot be repaired without a complete overhaul.

We have consistently avoided taking our medicine and our disease has gotten worse and worse.

People have lost faith in the economy because they have not faced this kind of uncertainty since the 1930s. Even the stagflation crisis of the 1970s will likely pale in comparison to what is about to happen. On the bright side, at least a large number of Americans are aware of the threat, as opposed to the 1920s when the vast majority of people were utterly conned by the government, the banks and the media into thinking all was well. Knowing is the first step to preparing.

The second step is securing your own financial future – that’s where physical precious metals can play a role. Diversifying your savings with inflation-resistant, uninflatable assets whose intrinsic value doesn’t rely on a counterparty’s promise to pay adds resilience to your savings. That’s the main reason physical gold and silver have been the safe haven store-of-value assets of choice for centuries (among both the elite and the everyday citizen).

* * *

As the world moves away from dollars and toward Central Bank Digital Currencies (CBDCs), is your 401(k) or IRA really safe? A smart and conservative move is to diversify into a physical gold IRA. That way your savings will be in something solid and enduring. Get your FREE info kit on Gold IRAs from Birch Gold Group. No strings attached, just peace of mind. Click here to secure your future today.

Wendy’s has a new deal for daylight savings time haters

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Wealth Inequality by Age in the Post‑Pandemic Era

These Are The 5 Charts The FDIC Does Not Want You Paying Attention To

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

Mortgage rates fall as labor market normalizes

People Who Received Ivermectin Were Better Off, Study Finds

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International23 hours ago

International23 hours agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges