International

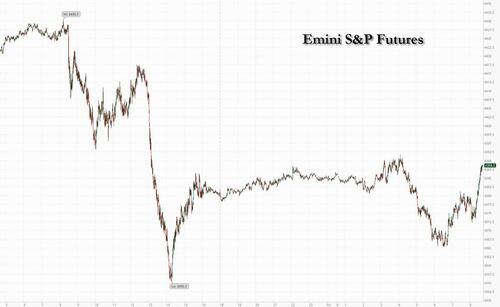

Futures Jump To Highs After Solid Bank Earnings As Gold, Treasuries Soar On Imminent Gaza Invasion

Futures Jump To Highs After Solid Bank Earnings As Gold, Treasuries Soar On Imminent Gaza Invasion

US equity futures reverased earlier losses,…

Share this:

US equity futures reverased earlier losses, thanks to solid results from JPM and Citi...

... while treasuries rallied with 10Y yields tumbling more than 10 basis point to session lows below 4.59% and paring almost all of Thursday’s sharp rise in the wake of hotter-than-expected US consumer price data.

... and while the dollar was largely flat...

... oil soared, with Brent about to rise above $90 again...

... and gold surged...

... as investors scramed to safe havens amid warnings that Israel is preparing for an imminent ground invasion of Gaza.

Helping nudge futures to session highs, JPMorgan, Citigroup and Wells Fargo all gained in premarket trading after earnings beats. Data showing that import prices rose less than expected in September also lifted the mood. Among other US premarket movers, Boeing fell after Ryanair Holdings Plc said delivery delays of 737 Max aircraft have worsened as the aircraft maker grapples with supplier quality-control issues. BlackRock declined after clients pulled a net $13 billion from long-term investment funds, the first outflows since the onset of the pandemic in 2020.

European bonds also gained, with the German 10-year yield falling seven basis points. Crude oil climbed more than 4% in New York, rising above $86 a barrel on fears the Israel-Hamas war could destabilize the Middle East and crimp global supply. “Bonds are rallying ahead of the weekend as traders likely want to hedge geopolitical risk,” said Christophe Barraud, chief economist and strategist at Market Securities LLP.

The Stoxx Europe 600 dropped about 0.8%, led by travel and leisure shares. The energy sector was the only one ini the green as oil majors gained. Among individual movers, Tryg A/S jumped after the Danish insurer reported an earnings beat. Ubisoft Entertainment advanced after the UK approved Microsoft Corp.’s deal to buy Activision Blizzard Inc., which will see the sale of some gaming rights to the French video-game maker. Here are the most notable European movers:

- Tryg gains as much as 6.7%, the most since March 2021, after the Danish insurance company reported 3Q earnings that beat estimates. Analysts notes that its DKK1 billion share buyback was larger and earlier than expected.

- Dufry shares climb as much as 2.1% after JPMorgan lifted its price target for the Swiss manager of airport duty-free shops to a new street high of CHF62, saying recent weakness in sentiment now presents a buy opportunity.

- Porsche rises as much as 1.8% after the luxury carmaker reported its global deliveries for the last nine months rose 10% year-on-year.

- Sabadell rises rise as much as 1.9% after loan management servicer doValue announced that the bank was among Spanish majors that it had secured €689 of new contracts from.

- CD Projekt climbs as much as 2.4% after the Polish video game developer said it used AI technology in its latest release to recreate the voice of an actor who passed away.

- BPER Banca shares advance as much as 4.3% to the highest since August after it was upgraded to overweight from equal-weight at Barclays, with the broker saying it’s getting more constructive on Italian banks.

- St James’s Place shares tumble 16% to the lowest since March 2020 as the UK wealth manager said it’s reviewing its fees and charges.

- Sartorius shares slide as much as 15% to the lowest since June 2020, while its French-listed subsidiary Sartorius Stedim Biotech drops as much as 19% after both cut guidance for the full year, with the companies citing lower volume expectations and product mix effects. Morgan Stanley says the magnitude of the profit warning is more significant than expected.

- Spirax drops as much as 4% to the lowest since May 2020 after Sartorius’s reduced sales forecast put pressure on the UK pumps manufacturer.

- Orsted drops as much as 8.3% as the stock is hit by New York State Public Service Commission’s unwillingness to support price increases for projects being developed alongside the state. The immediate implication for the Danish power generator is a greater likelihood of further write-down of Sunrise Wind, Citigroup says.

- Exor falls as much as 2.4%, the most since July, after the Agnelli family said a tender offer, part of its €1 billion buyback plan, went oversubscribed in a statement.

- British American Tobacco shares dip as much as 2.8% after the US Food and Drug Administration said it was prohibiting the marketing and distribution of some of its Vuse vape products.

Earlier in the session, Asian stocks fell for the first time in more than a week after brisk US inflation data bolstered rate-hike bets and weakness in China’s economy further soured sentiment. The MSCI Asia Pacific Index slid as much as 1.1%, with Chinese tech giants Tencent, Alibaba and JD.com among the biggest drags. Most markets were in the red as stronger-than-expected US inflation reading reinforced jitters about higher-for-longer rates. Gauges in Hong Kong were the worst performers after China’s consumer and producer prices came in below estimates, underscoring weak demand. Mainland shares only briefly pared losses following a report that China is considering forming a state-backed stabilization fund to shore up confidence in the stock market. The CSI 300 Index was back down more than 1%.

Hang Seng and Shanghai Comp. were lower with tech the worst hit in Hong Kong amid broker downgrades and as the US reportedly eyes closing a loophole that gives Chinese companies access to American AI chips via units located overseas. Furthermore, Chinese inflation data underwhelmed with consumer inflation flat and factory gate prices at a deeper-than-forecast decline, while participants digested mixed trade data in which exports beat expectations but remained in contractionary territory.

- Australia's ASX 200 was pressured with underperformance in real estate and tech alongside rising yields and as markets reflected on the latest gauges into the economic health of Australia’s largest trading partner.

- Japan's Nikkei 225 traded negatively but with price action choppy and downside stemmed as Japan plans to release an economy security plan to protect vital industries like semiconductors and with index heavyweight Fast Retailing boosted by earnings.

- India stocks closed lower, trimming their weekly gains, as bank stocks saw selling after UBS warned of rising default risks for unsecured retail loans. Index major Infosys slumped. The S&P BSE Sensex fell 0.2% to 66,282.74 in Mumbai, while the NSE Nifty 50 Index declined by a similar magnitude. The MSCI Asia Pacific Index was down 1.3%. Stock benchmarks eked out gains for the second week running as consumer-facing companies rallied on optimism

“Asia markets are facing a double whammy that casts significant doubt on the optimism-driven rally of the past few days,” said Hebe Chen, an analyst at IG Markets. “The earlier optimism, built on the assumption of a dovish turn by the Fed, now seems much vulnerable. Additionally, China’s disappointing zero CPI figures signal a yellow-light alarm.”

In FX, the Bloomberg Dollar Index falls 0.1%. The Swedish krona is the best performer among the G-10’s, rising 0.4% versus the greenback after CPI topped estimates.

In rates, treasuries held gains across the curve, unwinding a portion of Thursday’s sharp bear-steepening move, with yields richer by 4bp-8bp as US session begins. Intermediates lead, flattening 2s10s back to middle of Thursday’s range. US 10-year yields down more than 8bp at 4.60%, at session lows, outperforming gilts and bunds by ~3bp and ~1bp in the sector; front-end lags, with 2-year yields richer by ~4bp on the day. Haven demand is among the catalysts a ground invasion of Gaza by Israel appears likely. US session includes University of Michigan sentiment data, while 3Q earnings season starts with reports from JPMorgan, Citigroup and Wells Fargo. Meanwhile, the prospect of higher-for-longer US interest rates also weighed on risk appetite. Swap contracts pushed the odds of another quarter-point Federal Reserve hike to about 40% — from closer to 30% Wednesday. US economic data slate includes September import/export price index (8:30am) and October preliminary University of Michigan sentiment (10am).

In commodities, crude futures jumped over 4% to trade above $86. The risk-off tone has also benefited spot gold which adds 1%. An escalation of Israel’s war with Hamas, drawing in Iran, could send crude oil to $150 a barrel and cut about $1 trillion off world economic output, according to Bloomberg Economics.

Looking to the day ahead now, and data releases include Euro Area industrial production for August, whilst in the US we’ll get the University of Michigan’s preliminary consumer sentiment index for October. From central banks, we’ll hear from ECB President Lagarde, Bundesbank President Nagel, BoE Governor Bailey, Deputy Governor Cunliffe, and the Fed’s Harker. Finally, today’s earnings releases include JPMorgan, Citigroup, Wells Fargo and BlackRock.

Market Snapshot

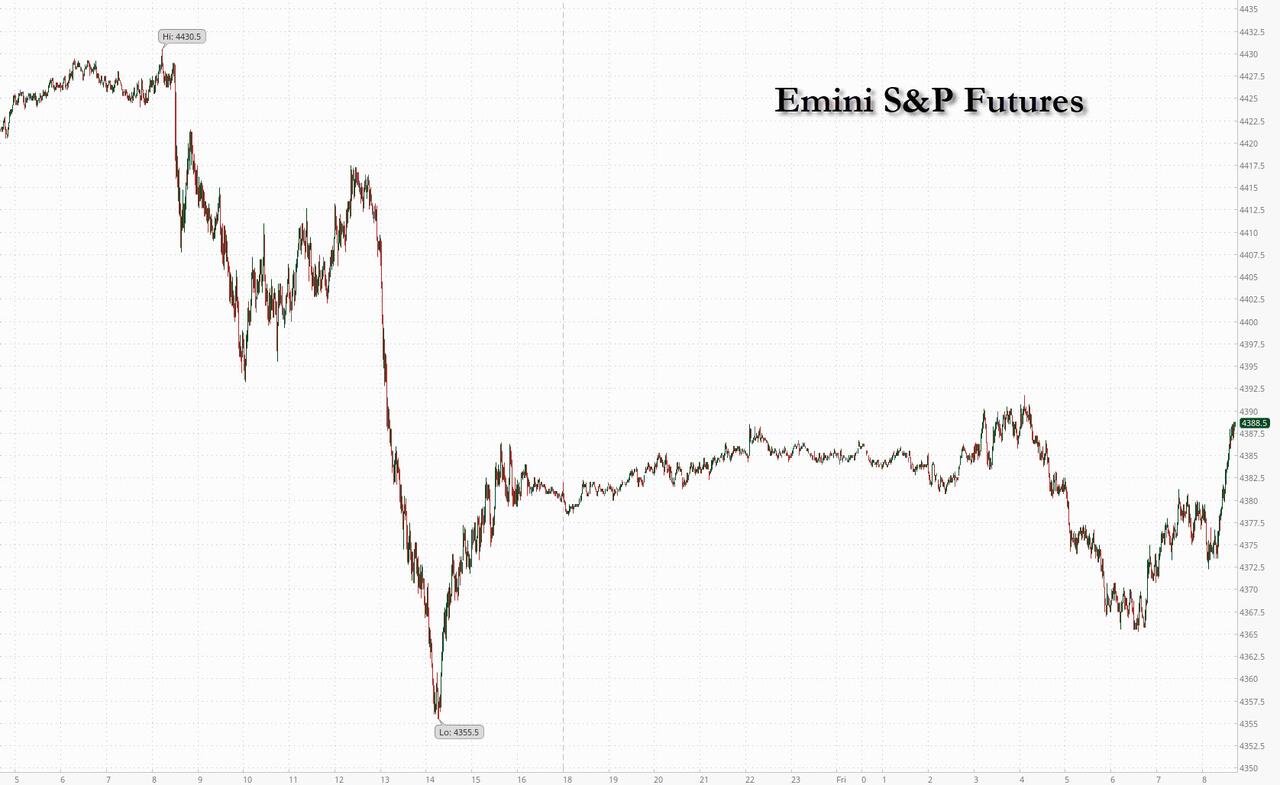

- S&P 500 futures little changed at 4,384.50

- MXAP down 1.2% to 157.23

- MXAPJ down 1.2% to 492.87

- Nikkei down 0.5% to 32,315.99

- Topix down 1.4% to 2,308.75

- Hang Seng Index down 2.3% to 17,813.45

- Shanghai Composite down 0.6% to 3,088.10

- Sensex down 0.2% to 66,272.36

- Australia S&P/ASX 200 down 0.6% to 7,051.03

- Kospi down 1.0% to 2,456.15

- STOXX Europe 600 down 0.4% to 451.95

- German 10Y yield little changed at 2.75%

- Euro up 0.3% to $1.0557

- Brent Futures up 2.6% to $88.24/bbl

- Gold spot up 0.8% to $1,884.33

- U.S. Dollar Index down 0.28% to 106.31

Top Overnight News

- China’s CPI for September was 0.0%, down from +0.1% in Aug and below the Street’s +0.2% forecast, while PPI deflation improved modestly to -2.5% (vs. -3% in Aug and vs. the Street forecast of -2.4%). FT

- China is considering forming a state-backed stabilization fund to shore up confidence in its $9.5 trillion stock market. After at least two rounds of consultation with industry participants over a period of months, financial regulators including the China Securities Regulatory Commission recently submitted a preliminary plan to the nation’s top leadership. BBG

- The Biden administration is considering closing a loophole that gives Chinese companies access to American artificial intelligence (AI) chips through units located overseas, according to four people familiar with the matter. RTRS

- Israel’s military warned more than 1mn Palestinians to leave Gaza City and its outskirts, in a move the UN said would cause a “calamitous” mass civilian displacement. FT

- Microsoft’s acquisition of videogame company Activision Blizzard won approval from U.K. competition authorities, clearing a path for the companies to close the $75 billion deal after a lengthy struggle with regulators. WSJ

- Americans didn’t pay an estimated $688 billion in taxes due on their 2021 returns—the largest shortfall ever. Audits and other enforcement will be stepped up to reduce the gap, the Internal Revenue Service said Thursday. WSJ

- Majority Leader Steve Scalise (R-La.) dropped out of the race for House speaker Thursday night, further throwing the House into chaos as Republicans openly ponder whether their fractured conference is capable of electing anyone as speaker. WaPo

- House Republicans are considering plans to give McHenry formal powers for a limited period so he can help pass a budget bill before the 11/17 deadline and deal with emergency spending requests. The Hill

- The biggest US banks face the worst write-offs in three years as JPMorgan, Citi and Wells Fargo kick off earnings today. They’re set to post combined net charge-offs almost twice last year’s levels. As well as deteriorating credit quality, analysts will be watching NII and investment banking revenue. BBG

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were mostly lower amid headwinds from the US where headline CPI data topped forecasts, while the region also digested softer-than-expected inflation and mixed trade data from China. ASX 200 was pressured with underperformance in real estate and tech alongside rising yields and as markets reflected on the latest gauges into the economic health of Australia’s largest trading partner. Nikkei 225 traded negatively but with price action choppy and downside stemmed as Japan plans to release an economy security plan to protect vital industries like semiconductors and with index heavyweight Fast Retailing boosted by earnings. Hang Seng and Shanghai Comp. were lower with tech the worst hit in Hong Kong amid broker downgrades and as the US reportedly eyes closing a loophole that gives Chinese companies access to American AI chips via units located overseas. Furthermore, Chinese inflation data underwhelmed with consumer inflation flat and factory gate prices at a deeper-than-forecast decline, while participants digested mixed trade data in which exports beat expectations but remained in contractionary territory.

Top Asian News

- PBoC set the USD/CNY mid-point at 7.1775 vs exp. 7.3179 (prev. 7.1776).

- PBoC Governor Pan met with Fed Chair Powell in Morocco on October 12th and exchanged views on cooperation, according to Reuters citing the PBoC.

- PBoC official said stable CNY has a solid foundation; and will resolutely prevent the risk of CNY overshooting; China will maintain a current account surplus, according to Reuters.

- PBoC said it will implement monetary policy in a precise and forceful manner. The official said the central bank still has ample room to support the economy. PBoC said recent interest rate reductions for the property sector have achieved significant results, and expects total social finance and credit to maintain steady growth in Q4, according to Reuters.

- China's NPC Standing Committee is to hold a meeting between Oct 20-24th; to discuss offer for new local government debt quota, according to Xinhua.

- Chinese Vice Premier Zhang called for efforts to vigorously develop advanced manufacturing and accelerate new industrialisation, according to Chinese press.

- China is said to weigh a new stabilisation fund to prop up the stock market with the plan calling for the fund to have access to up to hundreds of billions of yuan in capital, according to Bloomberg.

- US eyes closing loophole that gives Chinese companies access to American AI chips via units located overseas, according to Reuters sources

- China's Customs said China's trade still faces many difficulties and challenges, while it added that China's trade also faces a complex and severe external environment.

- Monetary Authority of Singapore maintained the width, centre and slope of the SGD NEER policy band, as expected, while it announced to shift to a quarterly schedule of policy reviews. MAS said it will closely monitor global and domestic economic developments amid uncertainty on inflation and growth, as well as noted that prospects for the Singapore economy are muted in the near term but should improve gradually in H2 2024.

- S&P said Japan is robust enough for rising JPY rates, expects a gradual increase in Japan's interest rates, and added that rates will rise from 2024, according to Reuters.

- IMF said BoJ's YCC tweak led to spillover in global bond market; could become larger in event of more substantial policy normalisation, according to Reuters.

European bourses have been tilting lower since the cash open despite a lack of major headlines during the European morning, with traders cognizant of geopolitical risks heading into the weekend. Sectors in Europe are mostly in the red with clear outperformance in energy as crude prices continue marching higher, while Banks, Financials and Healthcare lag. US futures have tilted lower alongside the European equity markets as broader sentiment deteriorates, albeit losses across US futures are modest.

Top European News

- German Chancellor Scholz reportedly faces renewed pressure to stem the property rout in a standoff with the industry, according to Reuters sources. Germany's building industry will present the chancellor with a new set of proposed measures this month to cushion the downside in the property sector.

- European Foreign Policy Commissioner Borrell says European investments in China have seen a sharp downturn and today they are at the lowest level since 2018, according to Reuters.

- Italian Economy Minister, when asked about a potential rating downgrade, said they have had discussions with rating agencies and cannot rule anything out, according to Reuters.

- ECB's Kazaks said he is quite happy with where rates currently are, via CNBC; would not close the door on further rate increases.

- ECB's Nagel said inflation has peaked in Germany, the labour market remains strong, and expects consumer demand to increase, according to Reuters.

- ECB's Visco said there are no signs that Italian spreads will be reaching levels for the ECB to take action, according to Bloomberg.

- BoE Governor Bailey said he is seeing progress that inflation is being tackled but there is work left to do, and added policy is restrictive and it needs to be, according to Reuters.

- UK Chancellor Hunt said the Autumn Budget statement will be "balanced with caution about the international situation"; needs to show in the statement that there is a path to lower taxation. He added the Autumn statement will lay out a plan to get out of the low growth trap, according to Reuters.

FX

- Dollar loses some inflation momentum as DXY slips from a double top into a softer 106.510-280 range.

- The Pound rebounds around the 1.2200 pivot vs Buck and the Euro steadies on the 1.0500 handle amidst massive EUR/USD option expiries.

- Franc holds above 0.9100 as yields retreat and the Loonie is over 1.3700 as oil recovers.

- Yen still defending 150.00 and the Kiwi in danger of losing 0.5900 on the eve of New Zealand election.

Fixed Income

- Bonds futures have extended their recovery from post-US CPI lows in what could be described as a risk revival given a marked downturn in equities.

- Bunds have reclaimed more than half of yesterday’s heavy losses to suggest more than a technical correction.

- Gilts have overcome a few wobbles to track their Eurozone counterpart.

- T-note is nudging new peaks amidst a return to bull-flattening regardless of a poor long bond auction to continue the run of weak sales this week.

Commodities

- Crude futures are on the grind higher on Friday despite a lack of fresh fundamentals, with traders likely wary to bet against crude heading into the weekend as geopolitical risk remains at the forefront for the complex.

- Dutch TTF is firmer intraday as prices for the Nov contract eye USD 54/MWh to the upside, potentially partially buoyed by action in the crude complex.

- Spot gold edged higher to eventually top yesterday’s USD 1,884.79/oz high, while the 50 DMA today coincides with the USD 1,900/oz psychological mark. Spot silver also benefits and is back on a USD 22/oz handle.

- Base metals are mixed with little reaction seen to the release of Chinese inflation and trade data overnight, with the data showing iron ore and copper imports fell in September.

- Australia union official said progress has been made with Chevron (CVX) in LNG labour talks, but there is no deal yet; further talks are planned for Monday, according to Reuters.

- Russian Deputy PM Novak says there are no discussions about an OPEC-like cartel for natural gas; says settlements in USD and EUR for Russian oil trade remain but have declined significantly. Discount to Russian oil on the global market to international benchmarks stabilised at USD 11-12/bbl from USD 35-38/bbl in early 2023, according to Reuters. Novak added that there is limited potential for further narrowing of the Urals prices discount.

Geopolitics

- Israel's ground military is building up on the Gaza Strip border, Sky News Arabia reports.

- The Israeli military called for an evacuation of all civilians in Gaza City from their homes southwards and said Gaza City is an area where military operations take place, while it will operate significantly in Gaza City in the coming days, according to Reuters.

- Israeli military informed the UN that all Palestinians north of Wadi Gaza should relocate to southern Gaza in the next 24 hours which amounts to approximately 1.1mln people, while the UN strongly appealed for any such order to be rescinded to avoid a calamitous situation, according to a UN spokesman. Furthermore, a Hamas official said the Gaza relocation warning is fake propaganda and it urged its citizens not to fall for it, according to Reuters.

- Iran's Foreign Minister said the continuation of war crimes will receive a response from the rest of the axes and 'the Zionist entity' will be responsible for that, while he added that the displacement of tens of thousands of Palestinians and cutting off water and electricity is considered a war crime.

- US, Japanese and South Korean officials are to discuss North Korean matters on October 17th in Jakarta, Indonesia, while it was separately reported that North Korea warned of the consequences of US drills in South Korea, according to KCNA.

- Indian Trade Secretary said a Free Trade Agreement with the UK is in an advanced stage of negotiations, according to Reuters.

- Russian President Putin proposes hosting peace talks between Azerbaijan and Armenia in Moscow, according to Reuters.

US Event Calendar

- 08:30: Sept. Import Price Index MoM, est. 0.5%, prior 0.5%

- Sept. Import Price Index YoY, est. -1.4%, prior -3.0%

- Sept. Export Price Index YoY, est. -4.0%, prior -5.5%

- Sept. Export Price Index MoM, est. 0.5%, prior 1.3%

- 10:00: Oct. U. of Mich. Sentiment, est. 67.0, prior 68.1

- Oct. U. of Mich. Current Conditions, est. 70.3, prior 71.4

- Oct. U. of Mich. Expectations, est. 65.7, prior 66.0

- Oct. U. of Mich. 1 Yr Inflation, est. 3.2%, prior 3.2%

- Oct. U. of Mich. 5-10 Yr Inflation, est. 2.8%, prior 2.8%

DB's Jim concludes the overnight wrap

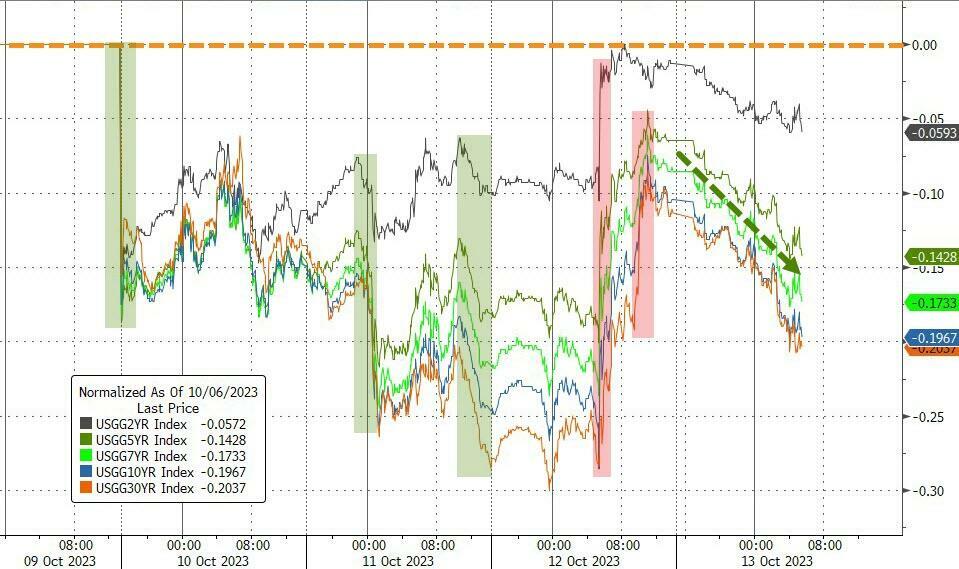

After a big rally for sovereign bonds at the start of the week, the sell-off resumed once again yesterday, thanks to an upside surprise in the latest US CPI print. The release showed that core CPI was at a 5-month high, and offered a fresh reminder that the road back to target is unlikely to be a smooth one. In turn, investors grew more confident that the Fed might raise rates again this year, and we even saw the 30yr Treasury yield experience its biggest daily rise since the Covid turmoil of March 2020, with a +16.0bps increase to 4.85%. That adjustment in rates meant that equities lost ground as well, with the S&P 500 ending its run of 4 consecutive gains to fall -0.62% .

Looking at the details of that CPI print, it was mostly bad news from a market perspective. The main story was that headline CPI came in at +0.40%, which was above the consensus of economists at 0.3%, along with market pricing via inflation swaps, which were expecting +0.25%. It wasn’t just the headline number that came in strong however, as the core CPI measure was running at +0.32%, with decent increases in some of the stickier categories as well. It was also a broad-based move, as the Cleveland Fed’s trimmed mean CPI measure that excludes the biggest outliers rose to +0.40%. So the data cemented the picture that inflation has been ticking up in recent months, and if you just look at the last 3 months, the annualised rate of CPI is now at +4.9%, which is the highest it’s been since August 2022. That’s offering some pushback against the more positive inflation narrative from a couple of months ago, and on the back of the release, our US economists have upgraded their near-term expectations for inflation, largely because of a stronger trajectory in rental inflation. See their reaction note here for details.

When it comes to the Fed, there’s still pretty strong scepticism about a hike in November, which is only priced as a 10% chance. But when it comes to December, futures raised the chance of a hike to 39% by that meeting, up from 30% the day before. That was also supported by the latest jobless claims data, which came in at 209k (vs. 210k expected) over the week ending October 7, in line with the lower levels of more recent weeks.

We didn’t hear much from Fed officials themselves, apart from Boston Fed President Collins, who echoed other recent Fedspeak in saying that if the recent rise in yields persists, it “likely reduces the need for further tightening”. But she wouldn’t take further tightening off the table and said that “today’s CPI release is a reminder that restoring price stability will take time”. Chair Powell is due to speak on Thursday next week, just before the pre-meeting blackout period begins, so that’ll be an important event on the calendar.

For sovereign bonds, the CPI proved to be a tough backdrop, and the 10yr yield was up +14.0bps by the close to 4.70%. That was its biggest daily increase since early May, back when the 10yr yield was still below 3.5%, and the move was led predominantly by higher real yields, which rose +10.8bps on the day. For the 30yr yield the move was even more dramatic, with a +16.0ps rise to 4.85%, which was the biggest daily rise since March 2020 at the height of the financial turmoil around the Covid-19 pandemic. That wasn’t helped by a 30yr auction, which was awarded at a post-2007 high of 4.837%, as weak end-investor demand led to the largest primarily dealer take up of a 30-year auction since December 2021. 30yr yields spiked by around 5bps following the auction results.

Over in Europe, the sell-off also had a clear impact, with yields on 10yr bunds (+6.8bps), OATs (+7.5bps) and BTPs (+9.8bps) all moving higher. That wasn’t helped by the latest rise in natural gas prices, which were up another +15.05% to €53.00 per megawatt-hour, which is the highest they’ve closed at since February. The latest moves follow several concerns about global supply over recent days, as well as forecasts showing much cooler weather in Europe over next week. Fortunately, gas prices are still some way beneath their levels from this time last year, and European gas storage is also fuller than at this point in 2021 and 2022, but this is still a concerning trend at a time when recent CPI prints have already been returning the focus back to inflationary pressures.

Whilst equities had initially been resilient, they took a tumble in the US after the 30yr auction, and the S&P 500 ended the day -0.62% lower. T he declines were fairly broad-based, but small-caps took a particular hit and the Russell 2000 ended the day -2.20% lower, which is its worst daily decline since April. By contrast, the FANG+ index of megacap tech stocks still lost ground, but was only down -0.28%, whilst European markets closed before the worst of the US losses, meaning the STOXX 600 ended the day up +0.10%. Today will see earnings season begin to get going, so plenty to keep an eye out for, including releases from several US financials.

That downbeat mood has continued overnight in Asia, where the major equity indices have all lost ground. The Hang Seng (-2.11%) is the biggest underperformer, but other indices including the CSI 300 (-1.11%), the KOSPI (-0.98%), the Shanghai Comp (-0.64%) and the Nikkei (-0.42%) have also declined. The moves come as China’s inflation data was weaker than expected, with CPI at 0.0% in September on a year-on-year basis (vs. +0.2% expected). Looking forward however, US equity futures have stabilised overnight, with those on the S&P 500 up +0.11%.

In the political sphere, the US House of Representatives remains without a speaker for the time being, and the latest news is that House Majority Leader Steve Scalise has withdrawn his name. He’d previously won the GOP nomination for speaker by a 113-99 vote, but there was clear opposition to his candidacy from some other Republicans, and to become Speaker, they would need to win a majority of the entire House of Representatives, meaning they could only lose a very small number of Republicans given their narrow majority. Currently, the House is unable to conduct business until a new speaker is elected.

Looking at yesterday’s other data, UK GDP grew by +0.2% in August, in line with expectations. Later on, we also heard from BoE chief economist Pill, who said that interest rate decisions were becoming “finely balanced”.

To the day ahead now, and data releases include Euro Area industrial production for August, whilst in the US we’ll get the University of Michigan’s preliminary consumer sentiment index for October. From central banks, we’ll hear from ECB President Lagarde, Bundesbank President Nagel, BoE Governor Bailey, Deputy Governor Cunliffe, and the Fed’s Harker. Finally, today’s earnings releases include JPMorgan, Citigroup, Wells Fargo and BlackRock.

International

United Airlines adds new flights to faraway destinations

The airline said that it has been working hard to "find hidden gem destinations."

Share this:

Since countries started opening up after the pandemic in 2021 and 2022, airlines have been seeing demand soar not just for major global cities and popular routes but also for farther-away destinations.

Numerous reports, including a recent TripAdvisor survey of trending destinations, showed that there has been a rise in U.S. traveler interest in Asian countries such as Japan, South Korea and Vietnam as well as growing tourism traction in off-the-beaten-path European countries such as Slovenia, Estonia and Montenegro.

Related: 'No more flying for you': Travel agency sounds alarm over risk of 'carbon passports'

As a result, airlines have been looking at their networks to include more faraway destinations as well as smaller cities that are growing increasingly popular with tourists and may not be served by their competitors.

Shutterstock

United brings back more routes, says it is committed to 'finding hidden gems'

This week, United Airlines (UAL) announced that it will be launching a new route from Newark Liberty International Airport (EWR) to Morocco's Marrakesh. While it is only the country's fourth-largest city, Marrakesh is a particularly popular place for tourists to seek out the sights and experiences that many associate with the country — colorful souks, gardens with ornate architecture and mosques from the Moorish period.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

"We have consistently been ahead of the curve in finding hidden gem destinations for our customers to explore and remain committed to providing the most unique slate of travel options for their adventures abroad," United's SVP of Global Network Planning Patrick Quayle, said in a press statement.

The new route will launch on Oct. 24 and take place three times a week on a Boeing 767-300ER (BA) plane that is equipped with 46 Polaris business class and 22 Premium Plus seats. The plane choice was a way to reach a luxury customer customer looking to start their holiday in Marrakesh in the plane.

Along with the new Morocco route, United is also launching a flight between Houston (IAH) and Colombia's Medellín on Oct. 27 as well as a route between Tokyo and Cebu in the Philippines on July 31 — the latter is known as a "fifth freedom" flight in which the airline flies to the larger hub from the mainland U.S. and then goes on to smaller Asian city popular with tourists after some travelers get off (and others get on) in Tokyo.

United's network expansion includes new 'fifth freedom' flight

In the fall of 2023, United became the first U.S. airline to fly to the Philippines with a new Manila-San Francisco flight. It has expanded its service to Asia from different U.S. cities earlier last year. Cebu has been on its radar amid growing tourist interest in the region known for marine parks, rainforests and Spanish-style architecture.

With the summer coming up, United also announced that it plans to run its current flights to Hong Kong, Seoul, and Portugal's Porto more frequently at different points of the week and reach four weekly flights between Los Angeles and Shanghai by August 29.

"This is your normal, exciting network planning team back in action," Quayle told travel website The Points Guy of the airline's plans for the new routes.

stocks pandemic south korea japan hong kong europeanInternational

Walmart launches clever answer to Target’s new membership program

The retail superstore is adding a new feature to its Walmart+ plan — and customers will be happy.

Share this:

It's just been a few days since Target (TGT) launched its new Target Circle 360 paid membership plan.

The plan offers free and fast shipping on many products to customers, initially for $49 a year and then $99 after the initial promotional signup period. It promises to be a success, since many Target customers are loyal to the brand and will go out of their way to shop at one instead of at its two larger peers, Walmart and Amazon.

Related: Walmart makes a major price cut that will delight customers

And stop us if this sounds familiar: Target will rely on its more than 2,000 stores to act as fulfillment hubs.

This model is a proven winner; Walmart also uses its more than 4,600 stores as fulfillment and shipping locations to get orders to customers as soon as possible.

Sometimes, this means shipping goods from the nearest warehouse. But if a desired product is in-store and closer to a customer, it reduces miles on the road and delivery time. It's a kind of logistical magic that makes any efficiency lover's (or retail nerd's) heart go pitter patter.

Walmart rolls out answer to Target's new membership tier

Walmart has certainly had more time than Target to develop and work out the kinks in Walmart+. It first launched the paid membership in 2020 during the height of the pandemic, when many shoppers sheltered at home but still required many staples they might ordinarily pick up at a Walmart, like cleaning supplies, personal-care products, pantry goods and, of course, toilet paper.

It also undercut Amazon (AMZN) Prime, which costs customers $139 a year for free and fast shipping (plus several other benefits including access to its streaming service, Amazon Prime Video).

Walmart+ costs $98 a year, which also gets you free and speedy delivery, plus access to a Paramount+ streaming subscription, fuel savings, and more.

If that's not enough to tempt you, however, Walmart+ just added a new benefit to its membership program, ostensibly to compete directly with something Target now has: ultrafast delivery.

Target Circle 360 particularly attracts customers with free same-day delivery for select orders over $35 and as little as one-hour delivery on select items. Target executes this through its Shipt subsidiary.

We've seen this lightning-fast delivery speed only in snippets from Amazon, the king of delivery efficiency. Who better to take on Target, though, than Walmart, which is using a similar store-as-fulfillment-center model?

"Walmart is stepping up to save our customers even more time with our latest delivery offering: Express On-Demand Early Morning Delivery," Walmart said in a statement, just a day after Target Circle 360 launched. "Starting at 6 a.m., earlier than ever before, customers can enjoy the convenience of On-Demand delivery."

Walmart (WMT) clearly sees consumers' desire for near-instant delivery, which obviously saves time and trips to the store. Rather than waiting a day for your order to show up, it might be on your doorstep when you wake up.

Consumers also tend to spend more money when they shop online, and they remain stickier as paying annual members. So, to a growing number of retail giants, almost instant gratification like this seems like something worth striving for.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic mexicoInternational

President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

President Biden Delivers The "Darkest, Most Un-American Speech Given By A President"

Having successfully raged, ranted, lied, and yelled through…

Share this:

{kind=link}

Having successfully raged, ranted, lied, and yelled through the State of The Union, President Biden can go back to his crypt now.

Whatever 'they' gave Biden, every American man, woman, and the other should be allowed to take it - though it seems the cocktail brings out 'dark Brandon'?

{kind=link}

Tl;dw: Biden's Speech tonight ...

-

Fund Ukraine.

-

Trump is threat to democracy and America itself.

-

Abortion is good.

-

American Economy is stronger than ever.

-

Inflation wasn't Biden's fault.

-

Illegals are Americans too.

-

Republicans are responsible for the border crisis.

-

Trump is bad.

-

Biden stands with trans-children.

-

J6 was the worst insurrection since the Civil War.

(h/t @TCDMS99)

Tucker Carlson's response sums it all up perfectly:

"that was possibly the darkest, most un-American speech given by an American president. It wasn't a speech, it was a rant..."

Carlson continued: "The true measure of a nation's greatness lies within its capacity to control borders, yet Bid refuses to do it."

"In a fair election, Joe Biden cannot win"

And concluded:

“There was not a meaningful word for the entire duration about the things that actually matter to people who live here.”

Victor Davis Hanson added some excellent color, but this was probably the best line on Biden:

"he doesn't care... he lives in an alternative reality."

— Tucker Carlson (@TuckerCarlson) March 8, 2024

* * *

Watch SOTU Live here...

* * *

Mises' Connor O'Keeffe, warns: "Be on the Lookout for These Lies in Biden's State of the Union Address."

On Thursday evening, President Joe Biden is set to give his third State of the Union address. The political press has been buzzing with speculation over what the president will say. That speculation, however, is focused more on how Biden will perform, and which issues he will prioritize. Much of the speech is expected to be familiar.

The story Biden will tell about what he has done as president and where the country finds itself as a result will be the same dishonest story he's been telling since at least the summer.

He'll cite government statistics to say the economy is growing, unemployment is low, and inflation is down.

Something that has been frustrating Biden, his team, and his allies in the media is that the American people do not feel as economically well off as the official data says they are. Despite what the White House and establishment-friendly journalists say, the problem lies with the data, not the American people's ability to perceive their own well-being.

As I wrote back in January, the reason for the discrepancy is the lack of distinction made between private economic activity and government spending in the most frequently cited economic indicators. There is an important difference between the two:

-

Government, unlike any other entity in the economy, can simply take money and resources from others to spend on things and hire people. Whether or not the spending brings people value is irrelevant

-

It's the private sector that's responsible for producing goods and services that actually meet people's needs and wants. So, the private components of the economy have the most significant effect on people's economic well-being.

Recently, government spending and hiring has accounted for a larger than normal share of both economic activity and employment. This means the government is propping up these traditional measures, making the economy appear better than it actually is. Also, many of the jobs Biden and his allies take credit for creating will quickly go away once it becomes clear that consumers don't actually want whatever the government encouraged these companies to produce.

On top of all that, the administration is dealing with the consequences of their chosen inflation rhetoric.

Since its peak in the summer of 2022, the president's team has talked about inflation "coming back down," which can easily give the impression that it's prices that will eventually come back down.

But that's not what that phrase means. It would be more honest to say that price increases are slowing down.

Americans are finally waking up to the fact that the cost of living will not return to prepandemic levels, and they're not happy about it.

The president has made some clumsy attempts at damage control, such as a Super Bowl Sunday video attacking food companies for "shrinkflation"—selling smaller portions at the same price instead of simply raising prices.

In his speech Thursday, Biden is expected to play up his desire to crack down on the "corporate greed" he's blaming for high prices.

In the name of "bringing down costs for Americans," the administration wants to implement targeted price ceilings - something anyone who has taken even a single economics class could tell you does more harm than good. Biden would never place the blame for the dramatic price increases we've experienced during his term where it actually belongs—on all the government spending that he and President Donald Trump oversaw during the pandemic, funded by the creation of $6 trillion out of thin air - because that kind of spending is precisely what he hopes to kick back up in a second term.

If reelected, the president wants to "revive" parts of his so-called Build Back Better agenda, which he tried and failed to pass in his first year. That would bring a significant expansion of domestic spending. And Biden remains committed to the idea that Americans must be forced to continue funding the war in Ukraine. That's another topic Biden is expected to highlight in the State of the Union, likely accompanied by the lie that Ukraine spending is good for the American economy. It isn't.

It's not possible to predict all the ways President Biden will exaggerate, mislead, and outright lie in his speech on Thursday. But we can be sure of two things. The "state of the Union" is not as strong as Biden will say it is. And his policy ambitions risk making it much worse.

* * *

The American people will be tuning in on their smartphones, laptops, and televisions on Thursday evening to see if 'sloppy joe' 81-year-old President Joe Biden can coherently put together more than two sentences (even with a teleprompter) as he gives his third State of the Union in front of a divided Congress.

President Biden will speak on various topics to convince voters why he shouldn't be sent to a retirement home.

The state of our union under President Biden: three years of decline. pic.twitter.com/Da1KOIb3eR

— Speaker Mike Johnson (@SpeakerJohnson) March 7, 2024

According to CNN sources, here are some of the topics Biden will discuss tonight:

Economic issues: Biden and his team have been drafting a speech heavy on economic populism, aides said, with calls for higher taxes on corporations and the wealthy – an attempt to draw a sharp contrast with Republicans and their likely presidential nominee, Donald Trump.

Health care expenses: Biden will also push for lowering health care costs and discuss his efforts to go after drug manufacturers to lower the cost of prescription medications — all issues his advisers believe can help buoy what have been sagging economic approval ratings.

Israel's war with Hamas: Also looming large over Biden's primetime address is the ongoing Israel-Hamas war, which has consumed much of the president's time and attention over the past few months. The president's top national security advisers have been working around the clock to try to finalize a ceasefire-hostages release deal by Ramadan, the Muslim holy month that begins next week.

An argument for reelection: Aides view Thursday's speech as a critical opportunity for the president to tout his accomplishments in office and lay out his plans for another four years in the nation's top job. Even though viewership has declined over the years, the yearly speech reliably draws tens of millions of households.

Sources provided more color on Biden's SOTU address:

The speech is expected to be heavy on economic populism. The president will talk about raising taxes on corporations and the wealthy. He'll highlight efforts to cut costs for the American people, including pushing Congress to help make prescription drugs more affordable.

Biden will talk about the need to preserve democracy and freedom, a cornerstone of his re-election bid. That includes protecting and bolstering reproductive rights, an issue Democrats believe will energize voters in November. Biden is also expected to promote his unity agenda, a key feature of each of his addresses to Congress while in office.

Biden is also expected to give remarks on border security while the invasion of illegals has become one of the most heated topics among American voters. A majority of voters are frustrated with radical progressives in the White House facilitating the illegal migrant invasion.

It is probable that the president will attribute the failure of the Senate border bill to the Republicans, a claim many voters view as unfounded. This is because the White House has the option to issue an executive order to restore border security, yet opts not to do so

Maybe this is why?

Most Americans are still unaware that the census counts ALL people, including illegal immigrants, for deciding how many House seats each state gets!

— Elon Musk (@elonmusk) March 7, 2024

This results in Dem states getting roughly 20 more House seats, which is another strong incentive for them not to deport illegals.

While Biden addresses the nation, the Biden administration will be armed with a social media team to pump propaganda to at least 100 million Americans.

"The White House hosted about 70 creators, digital publishers, and influencers across three separate events" on Wednesday and Thursday, a White House official told CNN.

Not a very capable social media team...

The State of Confusion https://t.co/C31mHc5ABJ

— zerohedge (@zerohedge) March 7, 2024

The administration's move to ramp up social media operations comes as users on X are mostly free from government censorship with Elon Musk at the helm. This infuriates Democrats, who can no longer censor their political enemies on X.

Meanwhile, Democratic lawmakers tell Axios that the president's SOTU performance will be critical as he tries to dispel voter concerns about his elderly age. The address reached as many as 27 million people in 2023.

"We are all nervous," said one House Democrat, citing concerns about the president's "ability to speak without blowing things."

The SOTU address comes as Biden's polling data is in the dumps.

BetOnline has created several money-making opportunities for gamblers tonight, such as betting on what word Biden mentions the most.

As well as...

We will update you when Tucker Carlson's live feed of SOTU is published.

Fuck it. We’ll do it live! Thursday night, March 7, our live response to Joe Biden’s State of the Union speech. pic.twitter.com/V0UwOrgKvz

— Tucker Carlson (@TuckerCarlson) March 6, 2024

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Catastrophic Risk: Investing and Business Implications

The Digest #187

Redefining Poverty: Towards a Transpartisan Approach

Deterra Royalties half-yearly result: stable performance and growth Initiatives

Deflationary pressures in China – be careful what you wish for

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Biden to call for first-time homebuyer tax credit, construction of 2 million homes

GBPINR: Analysis and Projections for 2024

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 hours ago

Walmart launches clever answer to Target’s new membership program

-

Government1 month ago

Government1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex