Futures Jump On China Trade-Deal Optimism Ahead Of Quad-Witch FridayTyler DurdenFri, 06/19/2020 - 07:46

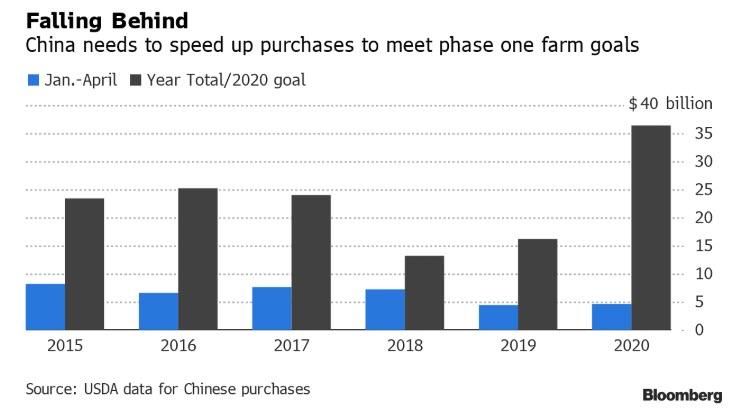

What do you get when you mix reopening optimism with stimulus hopes and throw in some good old "2019-style" US-China trade optimism? You get a session like overnight, where headed into what is usually an especially volatile quad-expiration day, at the curious time of 2:34am ET, or just before the European open, Bloomberg reported that with the Phase 1 trade deal largely forgotten, China planned to accelerate purchases of American farm goods to comply with the phase one trade deal with the U.S. following talks in Hawaii this week: "the world’s top soybean importer intends to step up buying of everything from soybeans to corn and ethanol after purchases fell behind due to coronavirus disruptions" Bloomberg reported citing sources, and that's all last year's trade war algos needed to push futures to overnight highs.

As a result of the report promising a "return" to the trade deal, which is laughably unachievable...

... but was enough to fool the algos, S&P index futures rose about 1% on Friday as investors also bet on a bounce back in post-pandemic economic activity, shrugging off the daily increase in new coronavirus infections in several states. Oil major Exxon Mobil rose 1.7% in premarket trading and Chevron gained 0.4% as Brent crude rose above $42 a barrel amid signs of gradual recovery in demand and oil producers’ promise to meet supply cuts. AMC Entertainment jumped 7.6% on plans to reopen theaters at about 450 locations in the United States next month and the company expects returning to full-seating capacity around Thanksgiving.

Meanwhile, on the virus front, on Thursday California, Florida and North Carolina imposed a mandatory mask use on Thursday as at least six states set daily records for new coronavirus cases. Mainland China also reported 32 new cases of infections, an uptick from a day earlier. Risk of a resurgence of the virus outbreak has led to choppy trading sessions this week, but the three main stock indexes are set to wrap up the week higher after a strong retail sales report for May and signs of additional official stimulus.

The S&P 500 ended marginally higher on Thursday while the Nasdaq posted its sixteenth rise in the past 19 sessions. The benchmark S&P 500 and the blue-chip Dow are now about 8% and 12% below their respective record closing highs hit in February, while the Nasdaq is about 0.5% below its all-time closing high on June 10.

In Europe, attention turned to negotiations over the EU’s proposed €750 billion program to help economies rebound from lockdowns, which sent the Stoxx 600 Index up as much as 1%. Wirecard AG shares bucked the trend, continuing their free-fall as the German payments company faced a potential cash crunch.

Attention will turn to the European Council summit of EU leaders, which will be taking place via videoconference from this morning. One of the main items on the agenda is the EU recovery fund, while there’ll also be discussions on the bloc’s long-term budget for the next 7 years. In terms of what to expect, hopes of a breakthrough on the recovery fund have been managed downwards recently, and the signs are instead pointing to an agreement no sooner than an as-yet unscheduled summit meeting in July. And with unanimity between the member states required for an agreement, the question will be how the so-called ‘Frugal Four’ of Sweden, the Netherlands, Denmark and Austria (all of which ran budget surpluses going into the pandemic) can move on board with the proposals. In an FT article on Tuesday, their four PMs said that they “support the creation of a time-limited emergency recovery fund”, so the question is whether they’ll be on board with grants as opposed to loans to the different member states. A negative outcome would be if there were a bunch of red lines or if we saw signs of reduced commitment to a large fund as the economic indicators recover. A more positive outcome would be if there were flexibility between the various positions.

Asian stocks also gained, led by energy and IT, after ending flat in the last session. Most markets in the region were up, with India's S&P BSE Sensex Index gaining 1.1% and Shanghai Composite rising 1%, while Singapore's Straits Times Index dropped 0.7%. Trading volume for MSCI Asia Pacific Index members was 18% above the monthly average for this time of the day. The Topix was little changed, with Management Solutions rising and Alpha Systems falling the most. The Shanghai Composite Index rose 1%, with Maoye Commercial Co Ltd and Hangzhou Jiebai Group posting the biggest advances.

While the overnight ramp has eased potential downside pressures somewhat, markets are expected to become more volatile during Friday’s session on account of quad witching, as investors unwind interests in futures and options contracts prior to expiration.

"Investors need to be prepared,” said Chris Gaffney, president of world markets at TIAA Bank. “When we see the run-up like we’ve seen and you have investors trying to protect their portfolios, protect the gains and having the uncertainty still out there, you’ve got some big options positions in the markets right now and the decisions to roll them or not on that day is what drives the volatility."

In FX, the Bloomberg dollar index slipped following news that China plans to accelerate purchases of American farm goods to comply with the phase one trade deal with the US,yet still headed for gains this week, supported by investors seeking haven currencies on rising concern that a second wave of coronavirus infections will delay a global economic recovery. G-10 currencies moved within tight ranges on Friday; the yen was little changed on the day but rose against almost all its major peers on the week amid a resurgence of the virus outbreak in Beijing and a jump in hospitalizations in some U.S. states. Mexico reported a record daily rise in cases in data released Thursday night.

In rates, Treasuries are lower led by long end, leaving 20- to 30-year yields cheaper by ~1bp vs Thursday’s close. Session lows were reached during Asia session as U.S. stock futures advanced. Market continues to show signs of fatigue with futures volumes still well below par.

In commodities, WTI and Brent future continues marching higher in early European trade as the complex was buoyed by overall risk appetite following reports that China will be stepping up purchase of US farms goods, whilst the contracts are also supported after yesterday’s JMMC meeting where Iraq and Kazakhstan submitted their proposals to compensate for overproduction, although the committee have delayed the press conference to next week as Nigeria and Angola have not yet submitted their compliance proposals.

Looking at the day ahead now, the main highlight will probably be the aforementioned European Council meeting. Otherwise, the data highlights include UK retail sales and public finance data for May, Germany’s PPI reading for May, along with April data on the Euro Area current account balance and Canadian retail sales. From central banks, the Russian central bank will be deciding on rates, while the Fed’s Powell, Quarles, Mester and Rosengren will be speaking. CarMax is reporting earnings.

Market Snapshot

S&P 500 futures up 0.6% to 3,128.75

STOXX Europe 600 up 0.5% to 365.27

MXAP up 0.2% to 159.33

MXAPJ up 0.5% to 513.91

Nikkei up 0.6% to 22,478.79

Topix down 0.02% to 1,582.80

Hang Seng Index up 0.7% to 24,643.89

Shanghai Composite up 1% to 2,967.63

Sensex up 1% to 34,546.83

Australia S&P/ASX 200 up 0.1% to 5,942.60

Kospi up 0.4% to 2,141.32

German 10Y yield rose 0.3 bps to -0.404%

Euro up 0.1% to $1.1218

Italian 10Y yield fell 3.6 bps to 1.251%

Spanish 10Y yield unchanged at 0.516%

Brent futures up 2.9% to $42.72/bbl

Gold spot up 0.4% to $1,729.41

U.S. Dollar Index little changed at 97.41

Top Overnight News

European Central Bank President Christine Lagarde and German Chancellor Angela Merkel warned European Union leaders meeting Friday by video conference that if they fail to agree on a stimulus package the consequences could be dire

China plans to accelerate purchases of American farm goods to comply with the phase one trade deal with the U.S. following talks in Hawaii this week

U.K. government debt rose above 100% of gross domestic product in May for the first time since 1963, reflecting a precipitous drop in economic output and a surge in spending to counter the fallout from the coronavirus pandemic.

Globally, companies are rushing to the bond market to raise more money than ever before.

Asian equity markets attempted to shrug-off Wall Street’s pre-quadruple witching indecision with a slightly upbeat tone seen in the region. ASX 200 (+0.1%) was higher with initial outperformance in Australia spearheaded by a surge in the consumer discretionary sector following a record jump in preliminary sales data, while advances in the Nikkei 225 (+0.5%) were limited by uninspiring currency moves and after early momentum was stalled by resistance around the 22550 level. Hang Seng (+0.7%) and Shanghai Comp. (+1.0%) were mixed amid the overall non-committal tone seen across global markets and as US-China frictions lingered with US President suggesting the US maintains the option of a complete decoupling from China and US Assistant Secretary of State Stilwell noted China’s attitude in Hawaii talks cannot be described as forthcoming and that the relationship between the sides is said to be tense overall, although the mainland indices remained afloat following the PBoC’s liquidity efforts in which it utilized both 7-day and 14-day reverse repos for a 2nd consecutive day. Finally, 10yr JGBs are flat with demand hampered as Japanese stocks remained afloat and amid the lack of BoJ presence in the market, although downside was also stemmed by a floor just above the 152.00 level.

Stocks in Europe continue to gain ground on the final trading session of the week [Euro Stoxx 50 +1.3%] as the region mimic the positive APAC performance overnight – whilst sentiment was bolstered amid reports China will be accelerating its US ag purchases under the Phase One trade deal. As a reminder, today marks the Q2 quad witching (full schedule on the newsquawk headline feed), and thus the stock markets could see increased volume and volatility – with analysts at Goldman Sachs suggesting S&P 500 option expiries of almost USD 2bln in the pipeline. Back to Europe, major bourses see broad-based gains with UK’s FTSE (+1.2%) the marginal top performer on Sterling dynamics, having initially kicked the session off as a laggard. Sectors are in the green across the with clear outperformance in Energy amid as the sector benefits from the gains in the complex, whilst Material names see notable underperformance. The breakdown meanwhile provides little by way of a clear risk tone. In terms of individual movers, focus remains on Wirecard (-50%) as shares continue to erode having opened with losses deeper than 20% amid news Management Board Member Jan Marsalek has been suspended on a revocable basis, couple with reports of a rogue employee falsified documents which were related to Wirecard. Lufthansa (+1.2%) eased off best levels after pilot union VC stated the state aid package is needed for the Co’s survival, following reports that the aid envelop could be rolled back.

Top European News

Lagarde Warns EU Leaders of Market Risks if No Stimulus Deal

Investors Fear BOE Slowed Crisis Response Too Soon as Risks Loom

A $21 Billion Debt Program in Denmark Has Bankers Confused

Mask Maker GVS Surges in Milan Debut After $558 Million IPO

In FX, not quite the biggest G10 movers, but marginally divergent against the buoyant US Dollar as the DXY remains elevated near 97.500 after rebounding to a fresh mtd high on Thursday at 97.586. The Aussie is hovering just above 0.6870 in wake of a record rise in retail sales that almost reversed April’s steep decline and compensating for more angst between the nation and China amidst accusations over cyber-attacks. However, the Pound remains depressed despite UK consumption exceeding expectations in May, with Cable teetering on the 1.2400 handle and Eur/Gbp towards the upper end of a 0.9007-39 range as Government debt tops 100% of GDP for the first time since 1963.

CHF/EUR/CAD/JPY/NZD - All rangy vs the Greenback, as the Franc continues to straddle 0.9600, while the Euro has tentatively reclaimed 1.1200+ status and may derive underlying support ahead of yesterday’s 1.1186 low given decent 1.1200-1.1195 option expiry interest (1.2 bn) in the run up to the post-EC Recovery Fund videoconference press statement (for more on this see our primer on the headline feed at 8.20BST). Elsewhere, the Loonie is gleaning traction within 1.3615-1.3569 parameters from a firmer rebound in crude prices awaiting Canadian retail sales data and the Yen is still relatively restrained either side of 107.00 as it maintains a tight inverse correlation with the Buck on risk factors offset against JGB-UST yield differentials/curve dynamics. Back down under, the Kiwi is lagging in the low 0.6400 zone and facing Aud/Nzd headwinds on the aforementioned modest Aussie outperformance as the cross trades near top of a 1.0700-1.0656 band.

SCANDI/EM - Some support for the Nok, Rub and Mxn via the oil complex with WTI and Brent back over Usd 40 and approaching Usd 43/brl respectively, but the Rouble will be eyeing the CBR for rate guidance beyond the looming 100 bp cut anticipated and well telegraphed by the Governor before turning attention to May economic indicators at 11.30BST and 17.00BST respectively. Meanwhile, the Cnh is firmer and testing 7.0650 vs the Usd following reports that China has agreed to revert to Phase 1 trade deal compliant levels of US farm imports.

In commodities, WTI and Brent crude future continue marching higher in early European trade as the complex is buoyed by overall risk appetite following reports that China will be stepping up purchase of US farms goods, whilst the contracts are also supported after yesterday’s JMMC meeting where Iraq and Kazakhstan submitted their proposals to compensate for overproduction, although the committee have delayed the press conference to next week as Nigeria and Angola have not yet submitted their compliance proposals. That being said, Energy Intel stated that the mood at the JMMC wasn’t very positive according to delegates. News-flow has been light for the complex during European trade but traders will be eyeing further COVID-19, US-China or OPEC-related headlines. In the absence of that, the weekly Baker Hughes rig count rounds off the schedule. WTI July has reclaimed a USD 40/bbl handle (vs. low 38.75/bbl), whilst Brent August extended its footing over USD 42/bbl (vs. low 41.50/bbl) and currently eyes the next round number to the upside. Elsewhere, spot gold gained impetus early-doors as the DXY retreated in early trade, but the yellow metal has since waned off highs to stabilise around USD 1730/oz from a low of 1721/oz. Meanwhile, copper prices rise with the overall risk appetite and as copper front-month futures surpass the USD 2.6/lb mark to a current high of USD 2.6340/lb.

US Event Calendar

8:30am: Current Account Balance, est. $102.9b deficit, prior $109.8b deficit

DB's Jim Reid concludes the overnight wrap

There’s been an element of Groundhog Day about this week with the same themes looping over like a stuck radio station. It’s clear that the virus is still spreading in some important areas but at the same time the market’s technicals continue to be strong, especially with all the liquidity around.

In terms of the pandemic, the main news continues to be the possible Covid-19 resurgence in the US. California and Florida both registered their largest one day rise yesterday with 3649 and 3207 respectively. The rise in California amounts to a 2.2% pickup, higher than the 7 day average of 2%, but the state continues to have better figures under the surface with hospitilisations only rising by 0.5%. The Florida case rise corresponds to a 3.9% increase, above the previous 7-day average of 3%. In a reversal of sorts, NY Governor Cuomo floated an idea of a quarantine for all travelers from Florida. NY residents have been asked to self-quarantine for 14 days when traveling to Florida since early in the pandemic. In Texas, the number of hospitalisations rose for a 7th straight day, up by a further 5%, while cases rose by 3.6%, well above the 7-day average of 3.0%.

Outside of the US, Germany reported 908 new cases (up 0.5%), the largest one day rise since 19 May, though it is unknown whether this is related to the meat plant that we mentioned yesterday. Highlighting just how low German case growth has been over the last month, only 2 days (including yesterday) in the last 30 have seen cases rise more than 700 in a day. Elsewhere, daily increases in LatAm and India have been mired in the 3-4% range for weeks now. Thankfully these countries have registered lower recorded deaths per million of the population even if data recording may not be as thorough in all places. See the “view report” button for the global/main US states case and fatality tables.

The data releases out yesterday didn’t provide much optimism either, with the weekly initial jobless claims from the US (one of the most up-to-date pieces of high-frequency data we have right now) declining to 1.508m in the week ending June 13, well above the 1.290m reading expected. Though this was the 11th week in a row that the numbers have fallen, the decline of just -58k from the previous week is the smallest since the numbers peaked back in late March, posing a concerning sign that progress in the labour market could be slowing. Meanwhile the number of continuing claims in the week ending June 6 were also higher than expected, falling to 20.544m (vs. 19.850m expected), with the insured unemployment rate remaining at 14.1%, thanks to the previous week’s numbers being revised down by three-tenths. Overall, it paints a picture of rather slower improvements in the labour market than many hoped for after the unexpectedly good jobs report for May.

Against this backdrop of lingering virus concerns and ambivalent data, global equities continued to tread water in low volume markets. The S&P 500 just barely rose on the day (+0.06%), while the STOXX 600 in Europe fell by -0.71%. Tech stocks held up well though, with the NASDAQ managing to eke out a +0.33% advance. For the second day in a row S&P volumes were well below average, yesterday was nearly 25% below the last month’s daily average. This drops comes as options and futures contracts are set to expire today, in what is colloquially known as the “quadruple witching”. Elsewhere, sovereign bonds rallied for the most part as investors looked for safe havens, with yields on 10yr Treasuries falling by -3.0bp, as bunds (-1.5bps), OATs (-2.7bps), and BTPs (-3.7bps) also advanced. Meanwhile the dollar strengthened +0.27% to a 2-week high.

Today, attention will turn to the European Council summit of EU leaders, which will be taking place via videoconference from this morning. One of the main items on the agenda is the EU recovery fund, while there’ll also be discussions on the bloc’s long-term budget for the next 7 years. In terms of what to expect, hopes of a breakthrough on the recovery fund have been managed downwards recently, and the signs are instead pointing to an agreement no sooner than an as-yet unscheduled summit meeting in July. And with unanimity between the member states required for an agreement, the question will be how the so-called ‘Frugal Four’ of Sweden, the Netherlands, Denmark and Austria (all of which ran budget surpluses going into the pandemic) can move on board with the proposals. In an FT article on Tuesday, their four PMs said that they “support the creation of a time-limited emergency recovery fund”, so the question is whether they’ll be on board with grants as opposed to loans to the different member states. A negative outcome would be if there were a bunch of red lines or if we saw signs of reduced commitment to a large fund as the economic indicators recover. A more positive outcome would be if there were flexibility between the various positions.

Overnight it’s been another fairly uneventful session in Asia with newsflow fairly light. The Nikkei (+0.46%), Shanghai Comp (+0.39%) and ASX (+0.75%) have all posted gains – the latter boosted by strong retail sales numbers - while the Hang Seng (-0.07%) and Kospi (-0.37%) are flat to slightly down. S&P 500 futures have posted modest gains, while bond markets have been muted. The only other data this morning came from Japan where the May CPI print came at +0.1% yoy (vs. +0.2% yoy expected), core CPI printed at -0.2% yoy (vs. -0.1% yoy expected) and core-core CPI printed in line with expectations at +0.4% yoy.

Back to yesterday and here in the UK, the main news was that the Bank of England decided to expand their QE programme by a further £100bn, in line with consensus expectations. However, in contrast to sovereign debt in the rest of Europe, gilts sold off in the aftermath, with 10yr yields up +3.8bps as there were a number of hawkish takeaways from the decision. For starters, the BoE said that since liquidity conditions had stabilised, “purchases could now be conducted at a slower pace than during the earlier period of dysfunction.” There also wasn’t a discussion of negative rates at the meeting, while the Chief Economist Andy Haldane dissented from the majority and voted to keep QE unchanged. Nevertheless, downside risks to the growth outlook remain, and looking forward our UK economists think more action from the BoE might be needed to ensure financial conditions remain easy and gilt yields stable, not least as the post-Brexit transition period concludes at the end of the year. As a result, their view is that the chance of further easing – via more QE in Q4 – remains high.

In terms of yesterday’s other data, the Philadelphia Fed’s business outlook survey surprised to the upside, with the general business activity indicator rising to 27.5 (vs. -21.4 expected). Meanwhile the Conference Board’s leading economic index rose +2.8% in May (vs. +2.4% expected).

Before we look at what today will bring, we’ve just released a new podcast from the latest edition of Konzept (link here). The title is Online Grocery – Fad or fate? Before the pandemic, online food ordering (both grocery delivery and meal kits) was already seeing steady growth, but since the outbreak, it’s taken off. While some people may revert back to their old habits when the pandemic recedes, many have been introduced to the concept and will continue to enjoy the benefits. You can listen to the podcast here, and can also subscribe to Podzept on Spotify, Google and Apple Podcasts.

To the day ahead now, and the main highlight will probably be the aforementioned European Council meeting. Otherwise, the data highlights include UK retail sales and public finance data for May, Germany’s PPI reading for May, along with April data on the Euro Area current account balance and Canadian retail sales. From central banks, the Russian central bank will be deciding on rates, while the Fed’s Powell, Quarles, Mester and Rosengren will be speaking.

As the industrial market sees some cooling from pandemic-era highs and financing tightens, what should owners and investors expect over the next 12-18…

As the industrial market sees some cooling from pandemic-era highs and financing tightens, what should owners and investors expect over the next 12-18 months? Four national experts took the stage at I.CON West to discuss what lies ahead for this popular asset class.

Capital Raising is Down, Cash is King

Overall, institutional capital raising was down 30-40% in 2023. Institutional investors have been wary of open-ended funds, portfolios have been trimmed and deals are happening increasingly in cash. Considering the current lending environment, more investors prefer unlevered deals.

“I’m always surprised how many groups out there are willing to buy all cash,” said Christy Gahr, director of capital markets, North America, Realterm. “It’s taken off over the last year, especially when the cost of debt is 6%.”

The private equity market is active, and panelists said they see more investment coming from end users. On the debt side, banks are shying away from speculative development projects and focused on smaller transactions last year. Some investors are taking more of a “rifle shot” approach by focusing on targeted, specific projects rather than casting a wide net. There is also interest from life companies that have some liquidity to invest in stabilized industrial product in first-tier markets.

Not Much Distress, But More Scrutiny

PJ Charlton, chief investment officer, CenterPoint Properties, commented he wasn’t seeing much distress and certainly not at 2009 levels. However, there are motivated sellers. It is a suitable time to sell assets out of a fund due to the high leasing rates and spectacular rent growth. “Most sellers today have a reason,” said Tim Walsh, chief investment officer, Dermody, “whether it’s a balance sheet-motivated, whether it’s related to some sort of tax structuring or promises they’ve made to investors.”

What has changed over the past 2-3 years is the approach of investment committees. “Back then it was about aggregation,” said Charlton. “It was all in on industrial… rents were growing 15% a year, cap rates are down another 50 basis points. Interest rates are 3%… Investment committees are reading every page and scrutinizing every word now. It’s a much more discerning buyer than it was three years ago,” he said. Investment committees are focusing on projects in healthy rent growth markets such as New Jersey, Los Angeles and Miami with $50-$150 million deal ranges.

“There is a thesis that there’s a slowdown in developments in all our markets,” said Walsh. “Everyone sees it. There are some submarkets where there weren’t any groundbreakings in the first quarter.” However, there will be an overall return to a balanced supply and demand dynamic.

Embracing ESG

Investors and tenants are increasingly recognizing the importance of ESG, and the panel agreed bigger credit and quality tenants tend to be more environmentally focused. Dermody has increased its environmental standards, making sure each of their building roofs can structurally support solar panels and installing piping and wiring the parking lots for electric charging. “There is a lot of noise out there when it comes to NIMBYism,” said Walsh, “And I think we need to do more to promote the modern environmentally sensitive product that we’re all building.”

Additionally, power supply is becoming more of a concern. “Several years ago, everyone was talking about having the right amount of parking. Now the hot topic is having access to power supply,” said Charlton. Several Fortune 500 companies, including FedEx, have promised to reduce their carbon footprint quickly and that means access to electrified parking. “What we’re seeing is that parking is even more important because now you have fleets that need to be able to charge two or three times a day in last-mile distribution facilities,” said Gahr. “It will change aspects of how we invest and how we underwrite and think about what our properties need to be able to provide our users.”

Nearshoring and Onshoring

Jack Fraker, president and global head of industrial and logistics capital markets for Newmark, turned the discussion to what is happening near the U.S.-Mexico border and asked the panelists what they are seeing in terms of nearshoring. Gahr commented that so much has changed in a short period and cited several statistics. For example, since 2019, China alone has invested in more than 120 projects in Mexico and in over 18 million square feet of industrial space. U.S.-Mexico trade is now outpacing U.S.-China trade by more than 40%.

“During the first half of 2023, $461 billion of goods passed through the U.S.-Mexico border, which is 44% higher than the value of goods between U.S. and China,” said Gahr. More than 150 foreign companies said in 2023 that they will open a new operation or expand into Mexico. These sectors include automotive, energy, manufacturing and IT.

Texas cities Laredo and El Paso were identified as active border markets, and the panelists agreed the best-performing assets are going to be as close to the border as possible. In 2023, El Paso had over three million square feet in total net absorption with a market wide vacancy of less than 4%, according to CBRE. The panelists also discussed the tremendous amount of opportunity in Mexico, although many U.S. development companies have not yet chosen to invest there. Onshoring activity, such as a Samsung project in Austin, is also on the rise.

Overall, the panel remained optimistic about investments, the economy and interest rates. Unemployment is below 4% and the economy is still growing. Additionally, the level of capital that’s sitting in money markets right now is “at $6 trillion – and that’s $2 trillion higher than it was five years ago,” according to Walsh. “So, the giant pile of money persists. And it’s available as soon as people are comfortable coming off the sidelines.”

This post is brought to you by JLL, the social media and conference blog sponsor of NAIOP’s I.CON West 2024. Learn more about JLL at www.us.jll.com or www.jll.ca.

Centre for Doctoral Training in Diversity in Data Visualization awarded over £9m funding from the EPSRC

Announced today, a new Centre for Doctoral Training (CDT) has been funded by a grant of over £9 million from the Engineering and Physical Sciences Research…

Announced today, a new Centre for Doctoral Training (CDT) has been funded by a grant of over £9 million from the Engineering and Physical Sciences Research Council (EPSRC) to help train the next, diverse generation of research leaders in data visualization.

A collaboration between City, University of London and the University of Warwick, the EPSRC Centre for Doctoral Training in Diversity in Data Visualization (DIVERSE CDT) will train 60 PhD students, in cohorts of 12 students, beginning in October 2025. The set-up phase will begin in July 2024.

The funding announcement is part of a wider UK Research & Innovation (UKRI) announcement of the UK’s biggest-ever investment in engineering and physical sciences postgraduate skills, totalling more than £1 billion.

DIVERSE CDT will be supported by 19 partner organisations, including the Natural History Museum, the Ordnance Survey, and the Centre for Applied Education Research.

Data Visualization is the practice of designing, developing and evaluating representations of complex data – the kinds of data that lie at the heart of every organization – to enable more people to make real-world use of a source of information which is otherwise challenging to access.

Data visualization can be used to synthesise complex data into a clear story upon which actions can be based. From illustrating how the Covid-19 pandemic made countries poorer, to showing how the processing-power of cryptocurrencies may have driven up the price of high-street graphics cards; data visualization is crucial to society obtaining meaning from data.

However, no current CDT focuses upon training its students in data visualization. This is despite government’s Department of Digital, Media, Culture and Sport listing data visualization as one of the top five skills needed by businesses – with 23% of businesses saying that their sector has insufficient capacity. Likewise, Wiley’s Digital Skills Gap Index, 2021, listed data visualization as the third most needed business and organisational skill for employees to succeed in the workplace in the next five years.

Key innovations of DIVERSE CDT will include students:

Credit: Alex Kachkaev and Jo Wood, City, University of London

Announced today, a new Centre for Doctoral Training (CDT) has been funded by a grant of over £9 million from the Engineering and Physical Sciences Research Council (EPSRC) to help train the next, diverse generation of research leaders in data visualization.

A collaboration between City, University of London and the University of Warwick, the EPSRC Centre for Doctoral Training in Diversity in Data Visualization (DIVERSE CDT) will train 60 PhD students, in cohorts of 12 students, beginning in October 2025. The set-up phase will begin in July 2024.

The funding announcement is part of a wider UK Research & Innovation (UKRI) announcement of the UK’s biggest-ever investment in engineering and physical sciences postgraduate skills, totalling more than £1 billion.

DIVERSE CDT will be supported by 19 partner organisations, including the Natural History Museum, the Ordnance Survey, and the Centre for Applied Education Research.

Data Visualization is the practice of designing, developing and evaluating representations of complex data – the kinds of data that lie at the heart of every organization – to enable more people to make real-world use of a source of information which is otherwise challenging to access.

Data visualization can be used to synthesise complex data into a clear story upon which actions can be based. From illustrating how the Covid-19 pandemic made countries poorer, to showing how the processing-power of cryptocurrencies may have driven up the price of high-street graphics cards; data visualization is crucial to society obtaining meaning from data.

However, no current CDT focuses upon training its students in data visualization. This is despite government’s Department of Digital, Media, Culture and Sport listing data visualization as one of the top five skills needed by businesses – with 23% of businesses saying that their sector has insufficient capacity. Likewise, Wiley’s Digital Skills Gap Index, 2021, listed data visualization as the third most needed business and organisational skill for employees to succeed in the workplace in the next five years.

Key innovations of DIVERSE CDT will include students:

undertaking and relating a series of applied studies with world-leading industrial and academic partners through a structured internship programme and an exchange programme with 18 leading international labs

using an interactive digital notebook for recording, reflection and reporting which becomes a “thesis” for examination, in lieu of the traditional doctoral thesis, and in line with current best practice in data visualization methodology

being provided with tools that mitigate against the dreaded isolation that PhD students fear, including opportunities for cohort reflection and supportive inclusion via enriching and inclusive processes for admissions, support, and a research environment that addresses barriers for students from under-represented backgrounds; specifically students who identify as female, students from ethnic minority backgrounds and students from lower socio-economic groups.

DIVERSE CDT will be led by Professor Stephanie Wilson, Co-Director of the Centre for HCI Design (HCID) and Professor Jason Dykes, Professor of Visualization and Co-Director of the giCentre, both of the School of Science & Technology at City, University of London.

Members of DIVERSE CDT’s interdisciplinary team include:

Professor Cagatay Turkay and Dr Gregory McInerny from the Centre for Interdisciplinary Methodologies, University of Warwick

Dr Sara Jones, Reader in Creative Interactive System Design, Bayes Business School at City

Professor Rachel Cohen, Professor in Sociology, Work and Employment, School of Policy & Global Affairs at City

Professor Jo Wood, Professor of Visual Analytics, and Dr Marjahan Begum, Lecturer in Computer Science, School of Science & Technology at City

Ian Gibbs, Head of Academic Enterprise at City.

Reflecting on DIVERSE CDT, Co-Principal Investigator, Professor Stephanie Wilson said:

“This funding represents a significant investment from the EPSRC and partner organisations in our vision of an innovative approach to doctoral training. We are delighted to have the opportunity to train a new and diverse generation of PhD students to become future leaders in data visualization.”

Professor Cagatay Turkay said:

“I am thrilled to see this investment for this exciting initiative that brings City and Warwick together to train the next generation of data visualization leaders. Together with our stellar partner organisations, DIVERSE CDT will deliver a transformative training programme that will underpin pioneering interdisciplinary data visualization research that not only innovates in methods and techniques but also delivers meaningful change in the world.”

Dr Sara Jones said:

“I’m really excited to be part of this great new initiative, sharing some of the innovative approaches we’ve developed through the interdisciplinary Centre for Creativity in Professional Practice and Masters in Innovation, Creativity and Leadership, and applying them in this important field.”

Professor Rachel Cohen said:

“DIVERSE CDT puts City at the heart of interdisciplinary data visualization. Data are increasingly part of the social science and policy agenda and it is imperative that those charged with visualizing data understand both the technical and social implications of visualization”

“The CDT is committed to developing and widening the group of people who have the cutting-edge skills needed to visualize, interpret and represent key aspects of our everyday lives. As such it marks a huge step forward both in terms of skill development and representation.”

Professor Leanne Aitken, Vice-President (Research), City, University of London, said:

“Growing the number of doctoral students we prepare in the interdisciplinary field of data visualization is core to our research strategy at City. Doctoral students represent the future of research and expand the capacity and impact of our research. The strength of the DIVERSE CDT is that it draws together our commitment to providing a supportive environment for students from all backgrounds to undertake applied research that challenges current practices in partnership with a range of commercial, public and third sector organisations. This represents an exciting expansion in our doctoral training provision.”

Professor Charlotte Deane, Executive Chair of the EPSRC, part of UKRI, said:

“The Centres for Doctoral Training announced today will help to prepare the next generation of researchers, specialists and industry experts across a wide range of sectors and industries.

“Spanning locations across the UK and a wide range of disciplines, the new centres are a vivid illustration of the UK’s depth of expertise and potential, which will help us to tackle large-scale, complex challenges and benefit society and the economy.

“The high calibre of both the new centres and applicants is a testament to the abundance of research excellence across the UK, and EPSRC’s role as part of UKRI is to invest in this excellence to advance knowledge and deliver a sustainable, resilient and prosperous nation.”

Science and Technology Secretary, Michelle Donelan, said:

“As innovators across the world break new ground faster than ever, it is vital that government, business and academia invests in ambitious UK talent, giving them the tools to pioneer new discoveries that benefit all our lives while creating new jobs and growing the economy.

“By targeting critical technologies including artificial intelligence and future telecoms, we are supporting world class universities across the UK to build the skills base we need to unleash the potential of future tech and maintain our country’s reputation as a hub of cutting-edge research and development.”

ENDS

Notes to editors

Contact details:

To speak to City, University of London collaborators, contact Dr Shamim Quadir, Senior Communications Officer, School of Science & Technology, City, University of London. Tel: +44(0) 207 040 8782 Email: shamim.quadir@city.ac.uk.

To speak to University of Warwick collaborators contact Annie Slinn, Communications Officer, University of Warwick. Tel: +44 (0)7392 125 605 Email: annie.slinn@warwick.ac.uk

Further information

Example data visualization (image)

Bridges – Alex Kachaev and Jo Wood.

Link to image:bit.ly/3Iy3BRz Credit: Alex Kachkaev and Jo Wood, City, University of London

Data visualization for the Museum of London by Alex Kachkaev (a PhD student) with supervisor Joseph Wood, illustrating where people in London congregate in both inside and outside spaces, showing how a creative use of data can be used to build a picture of human behaviour.

Collaborating labs

Collaborators on the international exchange programme comprise the world’s leading visualization research labs, including the Visualization Group at Massachusetts Institute of Technology (MIT), USA, the Embodied Visualisation Group, Monash University, Australia; Georgia Tech, USA; AVIZ, France; the DataXExperience Lab, University of Calgary, Canada, and the ixLab, Simon Fraser University, Canada.

About the funder

The Engineering and Physical Sciences Research Council (EPSRC) is the main funding body for engineering and physical sciences research in the UK. Our portfolio covers a vast range of fields from digital technologies to clean energy, manufacturing to mathematics, advanced materials to chemistry.

EPSRC invests in world-leading research and skills, advancing knowledge and delivering a sustainable, resilient and prosperous UK. We support new ideas and transformative technologies which are the foundations of innovation, improving our economy, environment and society. Working in partnership and co-investing with industry, we deliver against national and global priorities.

About City, University of London

City, University of London is the University of business, practice and the professions.

City attracts around 20,000 students (over 40 per cent at postgraduate level) from more than 150 countries and staff from over 75 countries. In recent years City has made significant investments in its academic staff, its infrastructure, and its estate.

City’s academic range is broadly-based with world-leading strengths in business; law; health sciences; mathematics; computer science; engineering; social sciences; and the arts including journalism, dance and music.

Our research is impactful, engaged and at the frontier of practice. In the last REF (2021) 86 per cent of City research was rated as world leading 4* (40%) and internationally excellent 3* (46%).

We are committed to our students and to supporting them to get good jobs. City was one of the biggest improvers in the top half of the table in the Complete University Guide (CUG) 2023 and is 15th in UK for ‘graduate prospects on track’.

Over 150,000 former students in 170 countries are members of the City Alumni Network.

Under the leadership of our new President, Professor Sir Anthony Finkelstein, we have developed an ambitious new strategy that will direct the next phase of our development.

By a show of hands, I.CON West keynote speaker Christine Cooper, Ph.D., managing director and chief U.S. economist with CoStar Group, polled attendees…

By a show of hands, I.CON West keynote speaker Christine Cooper, Ph.D.,managing director and chief U.S. economist with CoStar Group, polled attendees on their economic outlook – was it bright or bleak? The group responded largely positively, with most indicating they felt the economy was doing better than not.

Four years ago, the World Health Organization declared COVID-19 a global pandemic, seemingly halting life as we knew it. And although those early days of the pandemic seem like a long time ago, we’re still in recovery from two of its major consequences: 1) the $4 trillion in economic stimulus that the U.S. government showered on consumers; and 2) the aggressive monetary policies that have created ripple effects on the industrial markets.

Cooper began with an overview of the economic environment, which she called “the good news.” The nation’s GDP is strong, and the economy gained momentum in the second half of 2023 – we saw economic growth of 4.9% and 3.2% in Q3 and Q4 respectively — much higher than expected. “The reason is consumers,” Cooper said. “When things get tough, we go shopping. This generates sales and economic activity. But how long can it last?”

Consumer sentiment continues to be healthy, and employment is good, although a shortage of workers could impact that moving forward. The U.S. added 275,000 jobs in January, far exceeding expectations. “The Fed raising interest rates hasn’t done what it normally does – slow job growth and the economy,” said Cooper. In addition, the $4 trillion given to keep households afloat during the pandemic has simply padded checking accounts, she said, as consumers couldn’t immediately spend the money because everyone was staying home, and the supply chain was clogged. The money was banked, and there’s still a lot of it to be spent.

Cooper addressed economic risks and the weak points that industrial real estate professionals should be mindful of right now, including mortgage rates that remain at 20-year highs, stalling the housing market, particularly for new home buyers. Mid-pandemic years of 2020-2021 had strong home sales, driven by people moving out of the city or roommates dividing into two properties for more space and protection against the virus. Homeowners who refinanced in the early stages of the pandemic were fortunate and aren’t willing to list their houses for sale quite yet.

“The housing market is a big driver of industrial demand – think furniture, appliances and all the durable goods that go into a home. This equates to warehouse space demand,” said Cooper.

Interest rates on consumer credit are spiking and leading economic indexes are still signaling a recession ahead. Financial markets are indicating the same, with a current probability of 61.5% that we will be in a recession by 2025. However, Cooper said, while all signs point to a recession, economists everywhere say the same thing as the economy seemingly continues to surprise us: “This time is different.”

Consumers are still holding the economy up with solid job and wage gains, yet higher borrowing costs are weighing on business activity and the housing market. Inflation has eased meaningfully but remains a bit too high for comfort. We’ve so far avoided the recession that everyone predicted, and the Federal Reserve appears ready to cut rates this year.

For the industrial markets, the good news is that retailer corporate profits are beginning to bounce back after slowing in 2021 and 2022, with retail sales accelerating.

A slowdown in industrial space absorption was reflected in all the key markets – Atlanta, Chicago, Columbus, Dallas-Fort Worth, Houston, the Inland Empire, Los Angeles, New Jersey and Phoenix – but was worst in the southern California markets, which have since been rebounding.

“Supply responded to strong demand,” Cooper said. “In 2021, 307 million square feet were delivered, followed by 395 million in 2022. In 2023, we saw 534 million square feet delivered – that’s almost 33% higher than the year before.”

The top 20 markets for 2023 deliveries measured by square feet are the expected hot spots: Dallas-Fort Worth (71 million square feet) leads the pack by almost double its follower of Chicago (37 million), then Houston (35 million), Phoenix (30 million) and Atlanta (29 million). Measured by share of inventory, emerging markets like Spartanburg, Pennsylvania, topped the list at 15 million square feet, followed by Austin (10 million), Phoenix and Dallas-Fort Worth (7 million), and Columbus (6 million).

“Developers are more focused on big box distribution projects, and 90% of what’s being delivered is 100,000 square feet or more,” Cooper said. Around 400 million square feet of space currently under construction is unleased, in addition to the around 400,000 square feet that remained unleased in 2023. “Putting supply and demand together, industrial vacancy rate is rising and could peak at 6-7% in 2024,” she said.

In conclusion, Cooper said that industrial real estate is rebalancing from its boom-and-bust years. Pandemic-related demands and accelerated e-commerce growth created a surge in 2021 and 2022, and the strong supply response that began in 2022 will continue to unfold through 2024. With rising interest rates putting a damper on demand in 2023, vacancies began to move higher and will continue to rise this year.

“Consumers are spending and will continue to do so, and interest rates are likely to fall this year,” said Cooper. “We can hope for a recovery from the full effects of the pandemic in 2025.”

This post is brought to you by JLL, the social media and conference blog sponsor of NAIOP’s I.CON West 2024. Learn more about JLL at www.us.jll.com or www.jll.ca.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.