Government

Futures Flat Ahead Of Closely Watched Powell Speech

Futures Flat Ahead Of Closely Watched Powell Speech

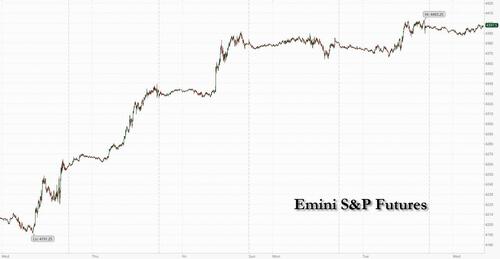

US equity futures are flat following a torrid 7-day rally, the longest since 2021, and…

Share this:

US equity futures are flat following a torrid 7-day rally, the longest since 2021, and global markets faltered as central bank officials in Europe pushed back against the prospect of speedy interest rate cuts, while investors were looking ahead to comments from Fed Chair Jerome Powell later in the day which could move markets. As of 7:45am US equity futures were unchanged at 4,397, erasing losses earlier in the session, while Europe’s Stoxx 600 traded near flat and yields on 10-year Treasuries climbed one basis point to 4.58%. The decline in oil prices also gained momentum, sending West Texas Intermediate crude futures below $77, near a three-month low. The dollar firmed for the third straight day.

In premarket trading, electric vehicle maker Rivian Automotive climbed 8.8% after raising its full-year production forecast, while smaller rival Lucid Group fell 5.8% after trimming its production forecast. Take-Two Interactive Software rose 9.1% on a report stating its Rockstar Games unit plans to announce the next "Grand Theft Auto" game as early as this week; ebay shares dropped after a lower-than-expected earnings forecast and another online retailer Coupang slid on weak quarterly profits. Here are the other notable premarket movers:

- Array shares fall 11% as the maker of renewable energy equipment cut its revenue guidance for the full year. Analysts note that order delays overshadowed otherwise strong Ebitda and margin.

- Datadog falls 1.1% as Mizuho Securities cut the recommendation on the cloud software company’s stock to neutral from buy. The broker said additional upside looks modest, following the company’s blowout report that propelled its stock up 28% on Tuesday.

- EBay shares fall 7.3% after the online auction company gave a fourth-quarter forecast that was lower than expected. Analysts attributed the weak guide to macro pressures.

- Lucid shares fall 4.9% after the electric-vehicle startup lowered its full-year production forecast to 8,000 to 8,500 vehicles, down from previous view of above 10,000 units. Third-quarter deliveries missed estimates as well.

- Nerdy shares tumble 25% after the online learning company widened its forecast for adjusted Ebitda loss for the full year and cut its projection for revenue.

- Rivian shares rise 7.0% after the electric-vehicle startup boosted its production guidance for the full year and also ended an exclusivity agreement to sell battery-electric vans to Amazon.com.

- Robinhood shares drop 7.9% after the online brokerage’s results fell short of estimates, with analysts pointing to slower-than-expected trading volumes in September, while Piper Sandler said that fourth-quarter guidance for net interest revenue was disappointing.

- Sleep Number shares plummet 33%, set to hit the lowest level since March 2011, after the air bed mattress manufacturer cut its outlook for the full year. It now sees a loss per share and plans to close stores in a restructuring effort. Analysts said that the moves show weakness in industry demand.

- Take-Two shares rise 8.5% after Bloomberg News reported that Rockstar Games, a division of the video game publisher, plans to announce the next highly anticipated Grand Theft Auto game as early as this week.

- Toast shares fall 19% after the restaurant-software company reported its third-quarter results and gave an outlook seen as disappointing.

- Upstart shares fall 23% after the AI lending marketplace firm reported third-quarter results that missed expectations and gave an outlook that was below the consensus estimate.

- Upwork shares jump 20% as the online-recruitment company boosted its revenue guidance for the full year. Analysts were positive about the execution amid continued macro headwinds.

- Under Armour added 1.9% on raising the annual gross margin forecast as the sports apparel maker benefited from cost cuts.

All eyes will be on Powell's opening remarks before the Federal Reserve Division of Research and Statistics Centennial Conference at 9:15 a.m. ET for more clues on how long U.S. monetary policy could stay restrictive. The Fed Chair is also due to speak at another conference on Thursday; his is widely expected to follow other policymakers in downplaying the likelihood of policy easing.

"Stocks may well pause for breath as investors balance the hope for rate cuts with building financial stresses in the economy," Derren Nathan, head of equity research at Hargreaves Lansdown, wrote in a note. "And it wouldn't be the first time ... that the market has been wrong about the timing of the Fed pivot."

Traders have been trying to gauge how hard global central bankers will push back against the drop in government bond yields, which potentially hinders efforts to keep a handle on inflation. Bank of England Governor Andrew Bailey warned Wednesday it is too early to discuss rate cuts, while three euro zone rate-setters also hinted policy would stay tight. Fed Governor Lisa Cook meanwhile said geopolitical tensions could trigger negative spillovers, including higher inflation.

“Fed speakers will attempt to jawbone and cool market expectations for rate cuts,” said Todd Schubert, Dubai-based senior fixed-income strategist at Bank of Singapore. “The market is underestimating the Fed’s resolve in bringing down inflation to 2% and we would not expect a sustained rally in risk assets until there is clearer evidence of a pronounced downward trajectory in inflation.”

Analysts have mixed views about the outlook for equities towards the end of the year, with some cautiously optimistic about the prospects of a rally, while others have highlighted the likelihood of economic growth concerns and tepid earnings forecasts keeping sentiment subdued.

European stocks also traded lower; the Stoxx 600 fell 0.1% with utilities, personal care and chemical names leading declines. Among individual stock movers on Wednesday, Britain’s Marks & Spencer was among the top gainers in Europe, surging 10% after the retailer posted robust profits and reinstated a dividend. ABN Amro fell as much as 8.9% to reach the lowest level since 2022, after the Dutch bank’s third quarter net interest income missed estimates, which analysts said was likely to disappoint despite an overall profit beat. Here are some other notable European movers:

- Vestas shares rise as much as 9.8%, most in a year as Ebit beat estimates. Analysts see 3Q results as an encouraging step in the right direction for the Danish wind turbine manufacturer

- Deutsche Post rises as much as 5.1% after the German courier services firm’s results were in line with expectations and show stock is well-positioned, according to Deutsche Bank

- Genmab shares climb as much as 8.9%, the most in three years, after the Danish biotechnology firm reported 3Q results that beat expectations

- Marks & Spencer rises as much as 10% following a strong first-half beat by the retailer, with analysts expecting significant upgrades to full-year consensus estimates

- Siemens Healthineers shares advance as much as 2.9% after the German medical technology firm reported sales and earnings for the fourth quarter that beat expectations

- Sampo advances as much as 3.5%, the most since August, after the Finnish insurance group reported better-than-expected third-quarter figures and a reassuring fall to claims inflation, analysts say

- Ahold Delhaize shares fall as much as 8.6%, dropping to the lowest level since October 2022, after the Amsterdam-listed grocer’s third-quarter margins and earnings missed estimates

- Legrand falls as much as 7.6%, the most in a year, after the maker of electrical devices like switches and plug sockets reports quarterly sales in North America that disappoint analysts

- E.On shares fall as much as 2.1% as investors are disappointed by the lack of a guidance upgrade. While the German utility reaffirmed its adjusted Ebitda forecast for the full year

- Adidas declines as much as 2%, after the company reported 3Q results in line with the pre-released figures from October. Despite the lack of surprises in the print, analysts highlighted the importance of Terrace-style sneakers to the company’s performance during the period

- ITV slumps as much as 7.2%, to the lowest intraday price since October 2022, after flagging a challenging advertising market. JPMorgan cut its full-year Ebit estimate for the broadcaster by 7%

Asian stocks fell ahead of a crucial speech by Fed Chairman Jerome Powell this week that could indicate how long US interest rates will remain elevated. The MSCI Asia Pacific Index fell as much as 0.4%, with financials the biggest drag. Key gauges in Japan and Singapore were among the biggest decliners. Korean stocks extended Tuesday’s decline further paring the big gain after a full ban on short-selling was reimposed. Asian stocks are trying to regain a foothold this month after the MSCI regional benchmark slid nearly 12% in the previous three months. Investors will parse a speech from Powell on Thursday after several of the central bank’s other policymakers on Tuesday signaled that tightening since July could hurt the economy.

- Hang Seng and Shanghai Comp moved between modest gains and losses with little action seen despite a slew of comments from the PBoC governor, while markets braced for next week’s Biden-Xi meeting in San Francisco, although no major breakthrough is expected.

- Australia's ASX 200 saw the tech sector leading the gains following a similar yield-driven sectoral performance on Wall Street.

- Japan's Nikkei 225 was initially supported by the Electronics sector with Nintendo shares rising over 6% post-earnings, whilst the Oil sector limited gains and the index eventually fell into losses as BoJ governor Ueda said the Bank doesn't necessarily need to wait until real wages actually turn positive in exiting YCC and negative rates, and if the BoJ thinks there is a strong chance real wages will turn positive in the future, that may be sufficient in making a decision on whether to continue with YCC and negative rate.

In FX, the greenback rose for a third day, with the Bloomberg Dollar Spot Index up 0.2% and back around levels seen before last Friday’s jobs report. The pound sits at the bottom of the G-10 table, falling 0.4% versus the dollar, despite BOE Governor Bailey arguing that it is too early to talk about rate cuts.

In rates, treasuries are mixed with the yield curve flatter for third straight day; the 10Y yield rose by 1 basis point to 4.58% and the 5s30s spread touched 14.4bp, lowest since Oct. 25. US yields are cheaper by 1bp-2bp on the day across front-end and belly of the curve with long-end yields little changed to lower on the day, flattening 2s10s by 1bp, 5s30s by more than 3bp. Sharper curve-flattening in bunds was spurred by IMF economic projections and comments by ECB’s Martins Kazaks. US curve-flattening complicates 10-year note auction at 1pm New York time. Likewise, Fed Chair Powell is slated to speak at 9:15am. The Treasury auction cycle resumes with $40BN 10-year note sale at 1pm, following good reception for 3-year note Tuesday; WI 10-year yield around 4.57% is ~4bp richer than October result, which had 1.8bp tail. Dollar IG issuance slate includes five names; eight borrowers priced $7.1b on Tuesday, taking weekly volume to $31b

In commodities, crude futures decline, with WTI falling 0.7% to trade near $76.80, the lowest since July as a forecast drop in US gasoline consumption added to a growing array of indicators suggesting the demand outlook is worsening. China, the world’s biggest importer, is also seeing dimming oil demand as winter approaches. Spot gold falls 0.5%.

Looking to the day ahead now, there is an array of central bank speakers, including Fed Chair Powell, Vice Chair Jefferson, Vice Chair for Supervision Barr, along with the Fed’s Cook and Williams. We’ll also hear from BoE Governor Bailey, and the ECB’s Lane, Kazaks, Wunsch, Makhlouf, Nagel, De Cos and Vujcic. Data releases include Euro Area retail sales for September, and we’ll also get the ECB’s Consumer Expectations Survey for September. Earnings releases include Walt Disney. And lastly, there’s a 10yr Treasury auction taking place.

Market Snapshot

- S&P 500 futures down 0.1% to 4,391.50

- MXAP down 0.6% to 156.62

- MXAPJ down 0.3% to 492.12

- Nikkei down 0.3% to 32,166.48

- Topix down 1.2% to 2,305.95

- Hang Seng Index down 0.6% to 17,568.46

- Shanghai Composite down 0.2% to 3,052.37

- Sensex little changed at 64,995.63

- Australia S&P/ASX 200 up 0.3% to 6,995.45

- Kospi down 0.9% to 2,421.62

- STOXX Europe 600 down 0.3% to 441.69

- German 10Y yield little changed at 2.65%

- Euro down 0.3% to $1.0665

- Brent Futures up 0.1% to $81.73/bbl

- Gold spot down 0.1% to $1,966.51

- U.S. Dollar Index up 0.27% to 105.83

Top Overnight News

- BOJ’s Ueda says there is “still some distance” toward the 2% inflation target, which is “why we are continuing with massive easing”, but he added that policy could be tightened before real wages rise. RTRS

- Recent high-level meetings have helped improve the China-US relationship, a top Beijing official said before an expected meeting between Xi Jinping and Joe Biden next week. The sitdowns “have sent out positive signals and raised the expectations of the international community on the improvement of China-US relations,” Vice President Han Zheng said. BBG

- Chinese authorities have asked Ping An Insurance Group to take a controlling stake in embattled Country Garden (2007.HK), the nation's biggest private property developer, four people family. China's State Council, which is headed by Premier Li Qiang, has instructed the local government of Guangdong province, where both companies are based, to help arrange a rescue of Country Garden by Ping An. RTRS

- Eurozone inflation expectations rise according to the latest ECB survey, creating a headache for Lagarde and her colleagues (median expectations for inflation over the next 12 months increased noticeably to 4.0%, from 3.5% in August and 3.4% in July, while those for inflation three years ahead remained unchanged at 2.5%). ECB

- Retail sales in the eurozone fell for the third consecutive month in September as consumers continued to rein in spending in response to rising interest rates, high inflation and stagnant economic growth. The 0.3 percent drop was slightly bigger than the 0.2 percent forecast by economists in a Reuters poll. Eurostat, the EU’s statistics arm, said the latest monthly decline took the year-on-year fall in retail goods sales to 2.9 percent. FT

- UBS is looking to raise its first additional tier 1 bond since $17bn worth of the risky debt instruments were wiped out when it took over rival lender Credit Suisse. The Swiss bank launched a deal to raise new dollar AT1 bonds on Wednesday, split between debt that can be redeemed in five years and 10 years. AT1 bonds have a perpetual maturity and are designed to take losses in times of crisis. FT

- Israeli troops stormed the “heart” of Gaza City, the country’s defense chief said. Saudi Arabia’s investment minister said talks toward a normalization of diplomatic ties with Israel will continue but are “contingent on a pathway to a peaceful resolution of the Palestinian question.” BBG

- Virginia Democrats won majorities in the state’s two legislative chambers, in a setback for Republican Governor Glenn Youngkin. The party also had success in Kentucky, Pennsylvania and Ohio, where voters approved a measure to enshrine abortion rights in the state’s constitution. Miami hosts the third GOP presidential debate tonight; Donald Trump will skip it. BBG

- Congress still hasn’t settled on a strategy for avoiding a gov’t shutdown on 11/17 amid ongoing divisions over spending, immigration, and funding for Israel/Ukraine. NYT

- A stubborn lack of growth and escalating political tensions with the U.S. are making investors rethink their China-oriented investments. They have pulled $1.6 billion from China-focused mutual and exchange-traded funds so far this year. WSJ

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed following a similar lead from Wall Street, with the breadth of the markets in early APAC hours particularly narrow. ASX 200 saw the tech sector leading the gains following a similar yield-driven sectoral performance on Wall Street. Nikkei 225 was initially supported by the Electronics sector with Nintendo shares rising over 6% post-earnings, whilst the Oil sector limited gains and the index eventually fell into losses as BoJ governor Ueda said the Bank doesn't necessarily need to wait until real wages actually turn positive in exiting YCC and negative rates, and if the BoJ thinks there is a strong chance real wages will turn positive in the future, that may be sufficient in making a decision on whether to continue with YCC and negative rate. Hang Seng and Shanghai Comp moved between modest gains and losses with little action seen despite a slew of comments from the PBoC governor, while markets braced for next week’s Biden-Xi meeting in San Francisco, although no major breakthrough is expected.

Top Asian News

- Chinese Vice Premier reiterated that the domestic economy is rebounding and improving as a whole, according to Bloomberg.

- PBoC Governor said PBoC will resolutely guard against overshooting risks of yuan exchange rate, and will resolutely deal with behaviours that disrupt market order, whilst preventing the formation of one-sided and self-reinforced mark, according to a Central Bank publication;

- PBoC Governor said shifting economic growth model is more important than pursuing high growth rate, via Securities Times. He added China's economy continues to improve, with the 5% growth target expected to be successfully achieved, and economic growth momentum has improved recently in China, production and consumption have recovered steadily, and employment and consumer prices are stable. He said monetary policy will pay more attention to cross-cyclical and counter-cyclical adjustments in the next stage, and the PBoC will always keep prudent monetary policy, and support stable growth of the real economy. He said they will strictly control new government-invested projects in areas with high debt burdens and will guide financial institutions to resolve debt risks through debt extension and replacement.

- China's top securities regulator vows to prevent excessive leverage, via state media.

- PBoC injected CNY 474bln via 7-day reverse repos with the rate at 1.80% for a CNY 83bln net daily injection.

- BoJ Governor Ueda said the BoJ doesn't necessarily need to wait until real wages actually turn positive in exiting YCC and negative rates, and if BoJ thinks there is a strong chance real wages will turn positive in the future, that may be sufficient in making a decision on whether to continue with YCC and negative rate, according to Reuters. Governor Ueda said it is desirable for FX to move stably reflecting fundamentals, according to Reuters. Governor Ueda says BoJ is continuing to buy huge amounts of govt bonds via market operations. Ueda said there is no statistical evidence that interest rate levels have a direct correlation with wage moves. BoJ Governor Ueda says the fact the central bank stands ready to step in to buy ETFs in times of market turbulence could be underpinning recent stock prices, and it may be possible to end ETF buying when there's no concern over the risk of a sharp rise in risk premia, according to Reuters.

- Japanese Finance Minister Suzuki sees June next year as the critical point where Japan can see inflation-adjusted real wages turn positive, according to Reuters.

- Japan is to reportedly include JPY 1.9tln in chip subsidies in its draft budget, according to NHK.

- Moody's affirms Japan's sovereign rating at A1; outlook stable, according to Reuters.

- Magnitude 6.8 earthquake strikes Banda Sea region near Indonesia; no tsunami warning, according to EMSC and PTWC.

European bourses are in the red, Euro Stoxx 50 -0.1%, in what has been a relatively choppy but ultimately contained session thus far with the focus firmly on earnings and upcoming speakers. Sectors are similarly mixed with Retail outperforming post-M&S while Banking is torn between Commerzbank and ABN AMRO; to the downside, Personal Care, Drug & Grocery lags after Ahold Delhaize's Q3 numbers. Stateside, futures are slightly softer with very modest underperformance in the RTY -0.2%, but with overall action similarly contained pre-Powell and others, ES -0.1%.

Top European News

- BoE's Bailey says the big shocks of last year and a bit before the unwinding; expects next inflation read to be quite a bit lower; expect it to be quite a bit lower by year-end, not down to 2%. We think policy is now restrictive and economic growth is very subdued. Basic message is that we believe policy will need to be restrictive for extended periods and there are upside risks.

- Norges Bank FSR: The financial system is marked by higher interest rates; Households draw on savings; Households draw on savings; Norwegian banks are well equipped to absorb higher losses.

FX

- Greenback continues to grind higher and claw back losses, DXY edged closer to 106.00 within firmer 105.51-87 range.

- Pound extends post-Pill declines as Cable probes 1.2250 and EUR/GBP pops back above 0.8700.

- Euro and Yen unable to evade Dollar recovery, with EUR/USD down towards base of 1.0660-1.0700 range and USD/JPY closer to 151.00 than 150.00.

- Loonie undermined by the ongoing plunge in oil as USD/CAD approaches 1.3800 head of Canadian building permits and BoC minutes.

- PBoC set USD/CNY mid-point at 7.1773 vs exp. 7.2839 (prev. 7.1776)

- Brazilian government will not ask Congress to alter fiscal target for now, according to Reuters sources.

Fixed Income

- Bonds mixed after a broad-based bounce on Tuesday, Bunds and Gilts remain above par within 130.73-25 and 95.96-42 respective ranges.

- T-note lags between 107-26+/108-06 + bounds awaiting Fed Chair Powell at a panel discussion and USD 40bln 10 year auction.

- 2033 German supply snapped up and PGBs regain some poise after PM resignation.

- Japan gov't bond issuance to total circa. JPY 44.5tln in FY23/24, via Reuters citing a draft; 9tln in second supplementary budget for FY23/24. Additionally, to maintain calendar-based annual JGBs to market unchanged at JPY 190.3tln following the FY23/24 second extra budget.

Commodities

- Crude benchmarks have recently slumped further into the red, in a continuation of the price action that was in play during yesterday’s session; slumping to current session troughs of USD 76.51/bbl and USD 80.87/bbl with fresh fundamentals limited but the move occurring alongside a further bout of USD upside.

- Most recently, it is worth pointing out that a magnitude 5 earthquake has occurred in western Texas, according to the EMSC. We are yet to see any updates as to what, if any, commodity activity in the region has been affected, but it is worth highlighting that the crude futures lifted slightly from the mentioned session lows on this update.

- Spot gold has similarly slipped to fresh lows, occurring alongside a fresh bout of USD upside with the DXY at session bests and moving ever closer to 106.00.

- Finally, base metals are slightly mixed but for the most part have not strayed significantly from relatively contained levels.

- US Private Energy Inventories (bbls): Crude +11.9mln (exp. -0.3mln), Gasoline -360k (exp. -0.8mln), Distillates +980k (exp. -1.5mln), Cushing +1.1mln.

- Nornickel says some clients who previously rejected purchasing from us are discussing metals purchases in 2024, via Ifx.

Geopolitics

- US President Biden told Israeli PM Netanyahu that a 3-day fighting pause could help secure the release of some hostages, according to Axios.

- Saudi Arabian investment minister says that discussions aimed at normalising ties with Israel will continue despite KSA's criticism of Israeli military actions in Gaza, according to Bloomberg. Adds will be contingent on a peaceful resolution to the Palestinian conflict.

US Event Calendar

- 07:00: Nov. MBA Mortgage Applications, prior -2.1%

- 10:00: Sept. Wholesale Trade Sales MoM, est. 0.9%, prior 1.8%

- 10:00: Sept. Wholesale Inventories MoM, est. 0%, prior 0%

Central Bank Speakers

- 05:15: Fed’s Cook Speaks on Financial Stability in Dublin

- 09:15: Fed’s Powell Delivers Opening Remarks

- 13:40: Fed’s Williams Delivers Keynote At Fed Research Conference

- 14:00: Fed’s Barr Speaks on Community Reinvestment Act

- 16:45: Fed’s Jefferson Delivers Closing Remarks

DB's Jim Reid concludes the overnight wrap

We're dealing with a suspected case of the nits at home, with all the required smelly shampoo. Rest assured if you have a meeting with me today, I'm highly unlikely to be a carrier. This is one of the advantages of being bald. In fact, this meant I was the one who had to go on the front line to administer the treatment.

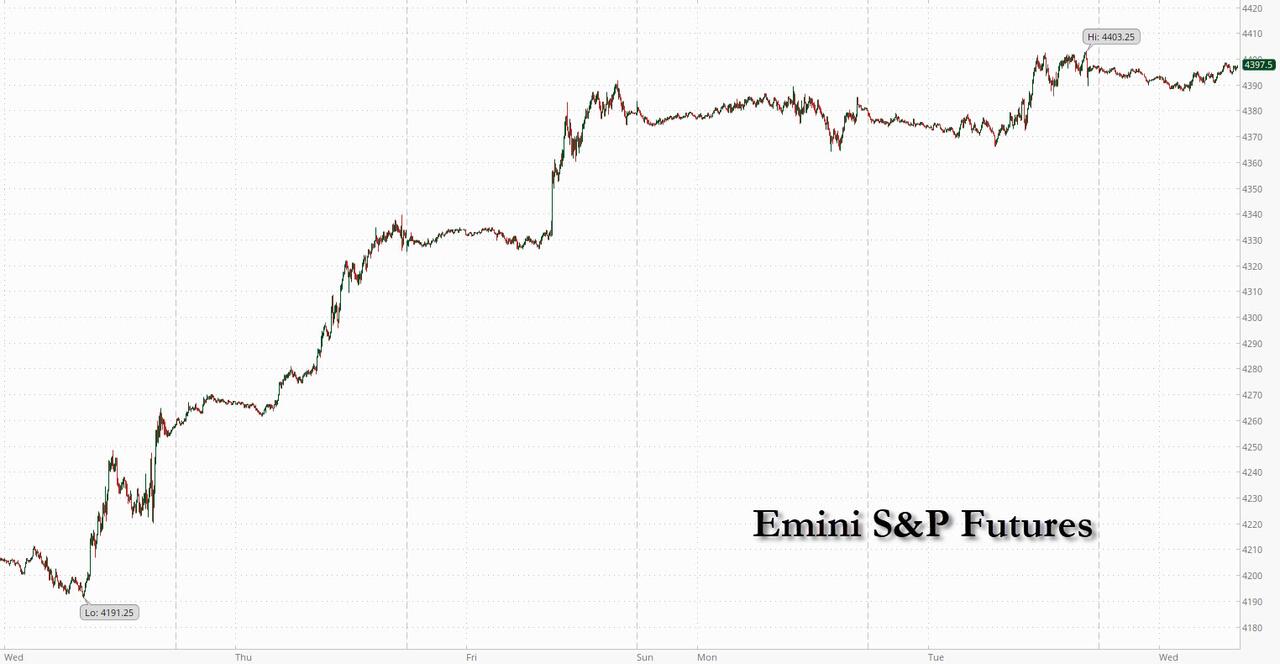

Hopefully it’ll go away as quickly as the bond sell-off did this week. Indeed yesterday saw Monday’s bond moves pretty much reversed at the longer-end yesterday with equities and fixed income both rallying together again. That saw the S&P 500 (+0.28%) post a 7th consecutive gain for the first time since late-2021, whilst the bond rally was helped by some dovish remarks from central bankers. Alongside that, we even saw oil prices fall to their lowest level since July, with Brent Crude (-4.19%) closing at $81.61/bbl, which added further support to the bond rally as inflation expectations moved lower.

When it came to bonds, the day had already got off to a strong start thanks to the “dovish hike” from the Reserve Bank of Australia. But we then heard from the Bank of England’s chief economist, who said that what financial markets were anticipating for rates “doesn’t seem totally unreasonable”, which were pricing in cuts later in 2024. That led investors to dial up the likelihood of rate cuts from the BoE next year, and it meant that gilts were the main outperformer yesterday, with the 2yr yield (-8.7bps) falling to its lowest level since June, whilst the 10yr yield was down -10.3bps .

Over at the Fed, we also heard from several speakers yesterday who held a broad range of views. Minneapolis Fed President Kashkari said that “I’m not seeing a lot of evidence that the economy is weakening”. But Chicago Fed President Goolsbee remained cautious, saying that he didn’t like “pre-committing what the rates are going to be at the next meeting when we still have weeks to go and a lot of information to gather”. Dallas Fed President Logan said that there’s been some “important cooling” in the labour market, but that "it still looks like we're trending to 3% instead of 2%” on inflation with continued tight financial conditions needed to bring inflation down. The generally hawkish Fed Governor Bowman was the only one to explicitly speak of additional hikes, as she continued “to expect that we will need to increase the federal funds rate further to bring inflation down to our 2% target in a timely way” .

Overall, the Fed commentary did little to derail the rates rally. Treasuries rallied across the curve, and the 10yr yield fell -7.6bps to 4.57%, with the 2yr yield down -1.7bps to 4.92%. The bond rally got some support from an auction of 3yr notes, which saw solid investor demand with the primary dealer takedown (16.3%) slightly below its 1-year average (17.0%). Today we have a 10yr auction which is the first big "proper duration" bond auction since last week's QRA. This morning in Asia, 10yr USTs (+1.3 bps) have edged back higher again.

Yesterday's rally was echoed in Europe too, where yields on 10yr bunds (-8.0bps), OATs (-8.5bps) and BTPs (-9.5bps) all moved lower as well. In part that was driven by a fresh move downwards for inflation expectations, with the German 10yr breakeven (-3.5bps) falling to its lowest level since February, at 2.15%. In addition, the 5y5y forward inflation swap for the Euro Area (-3.0bps) was also at its lowest level since May, at 2.44%, so there were growing signs that investors were becoming more confident about the inflation outlook.

One factor supporting that move in inflation expectations was a fresh decline in oil prices. Brent Crude fell by -4.19% to $81.61/bbl and WTI by -4.27% to $77.37/bbl. That’s the first time that Brent Crude has closed beneath its level prior to Hamas’ attack on Israel, having closed at $84.58/bbl on Friday October 6, with both Brent and WTI at their lowest levels since July. We've dipped another half percent in Asia. So despite the initial fears that oil markets would be disrupted by a broader escalation, it’s clear that investors remain relatively unconcerned by that risk for now. Amid the bearish catalysts for oil was the latest monthly EIA report, which now foresees an annual decline in US oil consumption this year.

This favourable backdrop proved supportive to other risk assets, which helped the S&P 500 (+0.28%) advance for a 7th consecutive day. Tech stocks led the advance, which meant the NASDAQ (+0.90%) and the FANG+ (+1.94%) both recorded an 8th consecutive advance for the first time since 2021, so lots of milestones for several indices. That said, the small-cap Russell 2000 (-0.28%) struggled for a second day, and there was also more weakness in Europe, where the STOXX 600 fell -0.16%. Portuguese stocks had a particularly bad day amidst the resignation of Prime Minister Costa, and the PSI 20 index fell -2.54%.

Risk appetite in Europe took a further hit from some fairly weak economic data from Germany. For instance, industrial production contracted by -1.4% in September (vs. -0.1% expected), whilst the construction PMI for October fell back to 38.3. For the construction PMI, the only month lower than that in the last decade was in April 2020, at the height of the Covid-19 pandemic, so this adds to the negative data surprises we’ve seen out of Europe in recent months.

As I check my screens in Asia, Chinese stocks are pretty flat with the Nikkei (-0.38%) and KOSPI (-0.39%) edging lower. In overnight trading, S&P 500 (-0.09%) and NASDAQ 100 (-0.12%) futures are trading slightly lower.

The Japanese yen (-0.11%) is edging lower again, trading at 150.53 against the dollar following some dovish signals from the BOJ. Looking ahead in the region, attention will turn to China’s inflation data tomorrow.

To the day ahead now, there is an array of central bank speakers, including Fed Chair Powell, Vice Chair Jefferson, Vice Chair for Supervision Barr, along with the Fed’s Cook and Williams. We’ll also hear from BoE Governor Bailey, and the ECB’s Lane, Kazaks, Wunsch, Makhlouf, Nagel, De Cos and Vujcic. Data releases include Euro Area retail sales for September, and we’ll also get the ECB’s Consumer Expectations Survey for September. Earnings releases include Walt Disney. And lastly, there’s a 10yr Treasury auction taking place.

International

Angry Shouting Aside, Here’s What Biden Is Running On

Angry Shouting Aside, Here’s What Biden Is Running On

Last night, Joe Biden gave an extremely dark, threatening, angry State of the Union…

Share this:

Last night, Joe Biden gave an extremely dark, threatening, angry State of the Union address - in which he insisted that the American economy is doing better than ever, blamed inflation on 'corporate greed,' and warned that Donald Trump poses an existential threat to the republic.

But in between the angry rhetoric, he also laid out his 2024 election platform - for which additional details will be released on March 11, when the White House sends its proposed budget to Congress.

To that end, Goldman Sachs' Alec Phillips and Tim Krupa have summarized the key points:

Taxes

While railing against billionaires (nothing new there), Biden repeated the claim that anyone making under $400,000 per year won't see an increase in their taxes. He also proposed a 21% corporate minimum tax, up from 15% on book income outlined in the Inflation Reduction Act (IRA), as well as raising the corporate tax rate from 21% to 28% (which would promptly be passed along to consumers in the form of more inflation). Goldman notes that "Congress is unlikely to consider any of these proposals this year, they would only come into play in a second Biden term, if Democrats also won House and Senate majorities."

Biden once again tells the complete lie that "nobody earning less than $400,000/year will pay additional penny in federal taxes."

— RNC Research (@RNCResearch) March 8, 2024

FACT: Biden has *already* raised the tax burden on Americans making as little as $20,000 per year. pic.twitter.com/VrZ1m0rzG3

Biden also called on Congress to restore the pandemic-era child tax credit.

Immigration

Instead of simply passing a slew of border security Executive Orders like the Trump ones he shredded on day one, Biden repeated the lie that Congress 'needs to act' before he can (translation: send money to Ukraine or the US border will continue to be a sieve).

As immigration comes into even greater focus heading into the election, we continue to expect the Administration to tighten policy (e.g., immigration has surged 20pp the last 7 months to first place with 28% in Gallup’s “most important problem” survey). As such, we estimate the foreign-born contribution to monthly labor force growth will moderate from 110k/month in 2023 to around 70-90k/month in 2024. -GS

SEE IT: Biden gets boo-ed while talking about his immigration bill. WATCH pic.twitter.com/O5FmkYx3xM

— Simon Ateba (@simonateba) March 8, 2024

Ukraine

Biden, with House Speaker Mike Johnson doing his best impression of a bobble-head, urged Congress to pass additional assistance for Ukraine based entirely on the premise that Russia 'won't stop' there (and would what, trigger article 5 and WW3 no matter what?), despite the fact that Putin explicitly told Tucker Carlson he has no further ambitions, and in fact seeks a settlement.

‼️ Breaking: Putin wants a negotiated settlement to what’s happening in Ukraine.

— Ed (@EdMagari) February 9, 2024

In a surprising turn of events, Tucker Carlson could be the key to peace, potentially playing a crucial role in ending the current conflict????️ pic.twitter.com/IKN8ajlEUX

As Goldman estimates, "While there is still a clear chance that such a deal could come together, for now there is no clear path forward for Ukraine aid in Congress."

China

Biden, forgetting about all the aggressive tariffs, suggested that Trump had been soft on China, and that he will stand up "against China's unfair economic practices" and "for peace and stability across the Taiwan Strait."

SOTU FACT CHECK:

— Wesley Hunt (@WesleyHuntTX) March 8, 2024

Biden claims we’re in a strong position to take on China.

No president in our lifetime has been WEAKER on China than Biden. pic.twitter.com/Y73JsIzmM3

Healthcare

Lastly, Biden proposed to expand drug price negotiations to 50 additional drugs each year (an increase from 20 outlined in the IRA), which Goldman said would likely require bipartisan support "even if Democrats controlled Congress and the White House," as such policies would likely be ineligible for the budget "reconciliation" process which has been used in previous years to pass the IRA and other major fiscal party when Congressional margins are just too thin.

So there you have it. With no actual accomplishments to speak of, Biden can only attack Trump, lie, and make empty promises.

Government

Jack Smith Says Trump Retention Of Documents “Starkly Different” From Biden

Jack Smith Says Trump Retention Of Documents "Starkly Different" From Biden

Authored by Catherine Yang via The Epoch Times (emphasis ours),

Special…

Share this:

Authored by Catherine Yang via The Epoch Times (emphasis ours),

Special counsel Jack Smith has argued the case he is prosecuting against former President Donald Trump for allegedly mishandling classified information is “starkly different” from the case the Department of Justice declined to bring against President Joe Biden over retention of classified documents.

Prosecutors, in responding to a motion President Trump filed to dismiss the case based on selective and vindictive prosecution, said on Thursday this is not the case of “two men ‘commit[ting] the same basic crime in substantially the same manner.”

They argue the similarities are only “superficial,” and that there are two main differences: that President Trump allegedly “engaged in extensive and repeated efforts to obstruct justice and thwart the return of documents” and the “evidence concerning the two men’s intent.”

Special counsel Robert Hur’s report found that there was evidence that President Biden “willfully” retained classified Afghanistan documents, but that evidence “fell short” of concluding guilt of willful retention beyond reasonable doubt.

Prosecutors argue the “strength of the evidence” is a crucial element showing these cases are not “similarly situated.”

“Trump may dispute the Hur Report’s conclusions but he should not be allowed to misrepresent them,” prosecutors wrote, arguing that the defense’s argument to dismiss the case fell short of legal standards.

They point to volume as another distinction: President Biden had 88 classified documents and President Trump had 337. Prosecutors also argued that while President Biden’s Delaware garage “was plainly an unsecured location ... whatever risks are posed by storing documents in a private garage” were “dwarfed” by President Trump storing documents at an “active social club” with 150 staff members and hundreds of visitors.

Defense attorneys had also cited a New York Times report where President Biden was reported to have held the view that President Trump should be prosecuted, expressing concern about his retention of documents at Mar-a-lago.

Prosecutors argued that this case was not “foisted” upon the special counsel, who had not been appointed at the time of these comments.

“Trump appears to contend that it was President Biden who actually made the decision to seek the charges in this case; that Biden did so solely for unconstitutional reasons,” the filing reads. “He presents no evidence whatsoever to show that Biden’s comments about him had any bearing on the Special Counsel’s decision to seek charges, much less that the Special Counsel is a ’stalking horse.'”

8 Other Cases

President Trump has argued he is being subjected to selective and vindictive prosecution, warranting dismissal of the case, but prosecutors argue that the defense has not “identified anyone who has engaged in a remotely similar battery of criminal conduct and not been prosecuted as a result.”

In addition to President Biden, defense attorneys offered eight other examples.

Former Vice President Mike Pence had, after 2023 reports about President Biden retaining classified documents surfaced, retained legal counsel to search his home for classified documents. Some documents were found, and he sent them to the National Archives and Records Administration (NARA).

Prosecutors say this was different from President Trump’s situation, as Vice President Pence returned the documents out of his own initiative and had fewer than 15 classified documents.

Former President Bill Clinton had retained a historian to put together “The Clinton Tapes” project, and it was later reported that NARA did not have those tapes years after his presidency. A court had ruled it could not compel NARA to try to recover the records, and NARA had defined the tapes as personal records.

Prosecutors argue those were tape diaries and the situation was “far different” from President Trump’s.

Former Secretary of State Hillary Clinton had “used private email servers ... to conduct official State Department business,” the DOJ found, and the FBI opened a criminal investigation.

Prosecutors argued this was a different situation where the secretary’s emails showed no “classified” markings and the deletion of more than 31,000 emails was done by an employee and not the secretary.

Former FBI Director James Comey had retained four memos “believing that they contained no classified information.” These memos were part of seven he authored addressing interactions he had with President Trump.

Prosecutors argued there was no obstructive behavior here.

Former CIA Director David Petraeus kept bound notebooks that contained classified and unclassified notes, which he allowed a biographer to review. The FBI later seized the notebooks and Mr. Petraeus took a guilty plea.

Prosecutors argued there was prosecution in Mr. Petraeus’s case, and so President Trump’s case is not selective.

Former national security adviser Sandy Berger removed five copies of a classified document and kept them at his personal office, later shredding three of the copies. When confronted by NARA, he returned the remaining two copies and took a guilty plea.

Former CIA director John Deutch kept a journal with classified information on an unclassified computer, and also took a guilty plea.

Prosecutors argued both Mr. Berger and Mr. Deutch’s behavior was “vastly less egregious than Trump’s” and they had been prosecuted.

Former White House coronavirus response coordinator Deborah Birx had possession of classified materials according to documents retrieved by NARA.

Prosecutors argued that there was no indication she knew she had classified information or “attempted to obstruct justice.”

International

United Airlines adds new flights to faraway destinations

The airline said that it has been working hard to "find hidden gem destinations."

Share this:

{kind=link}

{kind=link}

{kind=link}

Since countries started opening up after the pandemic in 2021 and 2022, airlines have been seeing demand soar not just for major global cities and popular routes but also for farther-away destinations.

Numerous reports, including a recent TripAdvisor survey of trending destinations, showed that there has been a rise in U.S. traveler interest in Asian countries such as Japan, South Korea and Vietnam as well as growing tourism traction in off-the-beaten-path European countries such as Slovenia, Estonia and Montenegro.

Related: 'No more flying for you': Travel agency sounds alarm over risk of 'carbon passports'

As a result, airlines have been looking at their networks to include more faraway destinations as well as smaller cities that are growing increasingly popular with tourists and may not be served by their competitors.

Shutterstock

United brings back more routes, says it is committed to 'finding hidden gems'

This week, United Airlines (UAL) announced that it will be launching a new route from Newark Liberty International Airport (EWR) to Morocco's Marrakesh. While it is only the country's fourth-largest city, Marrakesh is a particularly popular place for tourists to seek out the sights and experiences that many associate with the country — colorful souks, gardens with ornate architecture and mosques from the Moorish period.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

"We have consistently been ahead of the curve in finding hidden gem destinations for our customers to explore and remain committed to providing the most unique slate of travel options for their adventures abroad," United's SVP of Global Network Planning Patrick Quayle, said in a press statement.

The new route will launch on Oct. 24 and take place three times a week on a Boeing 767-300ER (BA) plane that is equipped with 46 Polaris business class and 22 Premium Plus seats. The plane choice was a way to reach a luxury customer customer looking to start their holiday in Marrakesh in the plane.

Along with the new Morocco route, United is also launching a flight between Houston (IAH) and Colombia's Medellín on Oct. 27 as well as a route between Tokyo and Cebu in the Philippines on July 31 — the latter is known as a "fifth freedom" flight in which the airline flies to the larger hub from the mainland U.S. and then goes on to smaller Asian city popular with tourists after some travelers get off (and others get on) in Tokyo.

United's network expansion includes new 'fifth freedom' flight

In the fall of 2023, United became the first U.S. airline to fly to the Philippines with a new Manila-San Francisco flight. It has expanded its service to Asia from different U.S. cities earlier last year. Cebu has been on its radar amid growing tourist interest in the region known for marine parks, rainforests and Spanish-style architecture.

With the summer coming up, United also announced that it plans to run its current flights to Hong Kong, Seoul, and Portugal's Porto more frequently at different points of the week and reach four weekly flights between Los Angeles and Shanghai by August 29.

"This is your normal, exciting network planning team back in action," Quayle told travel website The Points Guy of the airline's plans for the new routes.

stocks pandemic south korea japan hong kong european

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Catastrophic Risk: Investing and Business Implications

Redefining Poverty: Towards a Transpartisan Approach

The Digest #187

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

Deterra Royalties half-yearly result: stable performance and growth Initiatives

Deflationary pressures in China – be careful what you wish for

Biden to call for first-time homebuyer tax credit, construction of 2 million homes

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International10 hours ago

Walmart launches clever answer to Target’s new membership program

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex