International

Futures Extend Rebound As Nike Soars, Tesla Tumbles; Powell On Deck For 2nd Day

Futures Extend Rebound As Nike Soars, Tesla Tumbles; Powell On Deck For 2nd Day

Share this:

S&P futures and global stocks rose on Wednesday for the second day as Tuesday's global rebound extended after the recent correction, ahead of data that would throw light on the pace of an economic recovery from a coronavirus-driven recession. Investors also waited for a second speech from Fed Chair Jerome Powell who will appear before the House Select Subcommittee on the coronavirus to discuss the central bank’s response. The dollar extended its impressive Tuesday gains while 10Y yields were fractionally higher.

Nike was set for a record open after a stunning quarterly earnings report. Shares of the world's largest athletic shoe maker surged 13.2% in premarket trading as its digital sales, especially in North America, helped offset a fall in sales at traditional brick-and-mortar stores. The Dow constituent was set to drive the blue-chip index higher for a second straight day, clawing back more of the sharp declines from Monday that were driven by fears of another round of lockdowns to contain a global surge in COVID-19 cases.

On the other end, Tesla fell 4.8% in premarket trading as the goals announced at Tuesday’s “Battery Day” event was a dud and Musk failed to impress with his promise to cut electric vehicle costs. Oracle headed lower after a report by a state-backed Chinese newspaper said Beijing was unlikely to approve a proposed deal by the software maker and Walmart for ByteDance's TikTok.

Meanwhile, Russia’s largest internet company Yandex surged 9.2% in premarket after it said it’s in talks to buy TCS Group Holding Plc for about $5.48 billion. Elsewhere, the FAANGs edged higher before the bell. The group has borne the brunt of the declines this month after fuelling a Wall Street rally since March.

Overall sentiment remains skittish as doubts about more U.S. fiscal stimulus and growing political uncertainty in the run-up to the Nov. 3 presidential elections have kept investors from making big stock market bets.

"We are seeing a solid bounce, but it’s in the context of a very sharp pullback on Monday, which was a reset,” said Neil Wilson, chief market analyst in London for Markets.com. “We had bulls just tipping their toes back in the water, and the higher closes -- as small as they were -- seems to have been enough to cue today’s gains.”

"If we get a second (COVID-19) wave, it could have a significant impact on the election itself and that’s why markets have been wobbly in the last few days,” said Andrea Cicione, head of strategy at TS Lombard in London.

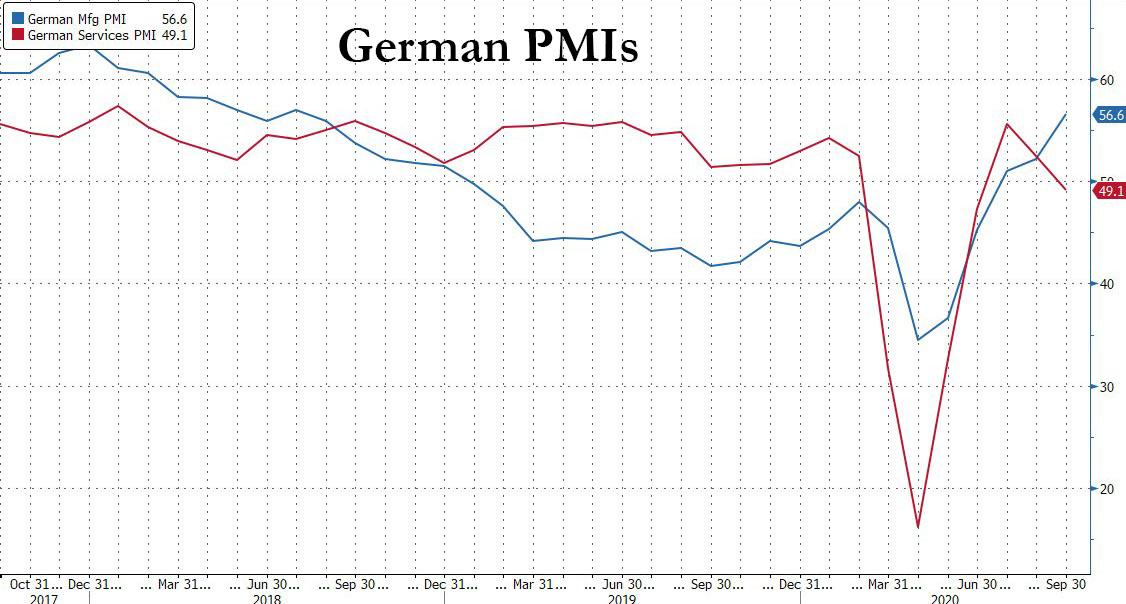

In Europe, the Stoxx 600 Index climbed 1.5%, the biggest gain in two weeks, helped by a jump German stocks after manufacturing data rose to a two-year high. Auto companies and travel stocks led the advance in Europe, with gains of 2.8% for both. Despite stronger German mfg PMI, the service sector stumbled and broader Eurozone data showed eurozone business growth ground to a halt this month with the post-Covid economic recovery stumbling this month, as the latest Euro area composite PMI declined by 1.8pt to 50.1 in September, notably below expectations. Across sectors, the overall decline was concentrated in the service sector, with the pace of recovery in manufacturing reaccelerating from August:

- Euro Area Composite PMI: 50.1, consensus 51.9, last 51.9.

- Euro Area Manufacturing PMI: 53.7, consensus 51.9, last 51.7.

- Euro Area Services PMI: 47.6, consensus 50.6, last 50.5.

And the sharp divergence in Germany:

- Germany Composite PMI: 53.7, consensus 54.0, last 54.4.

- German Services PMI: 49.1, consensus 53.0, last 52.5

- German Manufacturing PMI: 56.6, consensus 52.5

Earlier in the session, Asian stocks were fractionally higher, with health care rising and energy falling, after falling in the last. Markets in the region were mixed, with Australia's S&P/ASX 200 and Singapore's Straits Times Index rising, and India's S&P BSE Sensex Index and Taiwan's Taiex Index falling. The Topix declined 0.1%, with Daiichi Kigenso and Land Co falling the most. The Shanghai Composite Index rose 0.2%, with EGing Photovoltaic Technology and Jinko Power Technology posting the biggest advances

Chinese state-run media decounced the TikTok deal as "an American trap" and a "dirty and underhanded trick" as sentiment in Beijing swings against the proposal. TikTok owner ByteDance said it would remain in control of the new entity that would be created in the agreement, pushing back on President Donald Trump's assertions that Oracle Corp. would be in control. The wider context of resistance from China is that the country's leaders do not want to be seen to be pushed around by unilateral U.S. actions.

Looking at today's main event in markets, Fed Chair Powell is in Congress again testifying to a House select subcommittee on the coronavirus response from 10:00 a.m. Yesterday he said the U.S. economy has a long way to go before it is fully recovered and that more support will be needed.

In other overnight news, while there is still very little progress on reaching a new stimulus deal, there was some relief late yesterday when an agreement to keep the government funded through Dec. 11 was reached, avoiding a shutdown just before the election. More importantly, Republican moves to get a confirmation hearing for Trump's Supreme Court nominee in the coming weeks now seem unstoppable, after Democrats gained little support in the Senate for a delay.In FX, the dollar advanced a fourth day - its best run since June - after breaking above a key technical resistance level. The Bloomberg dollar index was up as much as 0.3% to highest since Aug. 12, but pared some advance as the euro erased losses. The euro erased losses, after falling to 1.1672 in early London trading, after mixed PMI data out of the region weighed initially yet as European equities extended gains, but then the common currency reversed course. The pound also steadied after dropping following comments by Foreign Secretary Dominic Raab on not being able to rule out a nationwide shutdown. The Australian dollar led declines after influential Westpac Banking Corp. economist Bill Evans predicted the central bank would cut interest rates at its Oct. 6 meeting; the New Zealand dollar also slipped, with the central bank maintaining the size of its quantitative easing program and keeping rates unchanged.

MSCI’s index of developing-nation stocks was little changed on Wednesday after falling more than 2% in the previous two days. The gauge for currencies dropped to its lowest level since Sept. 14, with the rand among the worst-hit as outflows from South Africa’s bond market surged. The average emerging-market sovereign-risk premium was unchanged, according to JPMorgan indexes. Central banks remain in focus, with policy makers in the Czech Republic forecast to follow their Thai counterparts and keep rates on hold. China’s yuan fixing was weaker than expected for a second day, reinforcing speculation that the central bank wants to slow the currency’s biggest quarterly rally since 2008.

In rates, treasury yields are slightly cheaper in early U.S. trading as Asia-session gains - led by steep gains for Aussie bonds - eroded ahead of 5-year note auction. Yields are cheaper by about 0.5bp from intermediates to long end with 10-year around 0.675%, trading broadly in line with bunds; gilts outperform slightly, about 0.5bp richer vs. Treasuries. Treasury auction cycle resumes with $53b 5-year note at 1pm ET, concludes with 7-year Thursday. Italian bonds rallied to send 30-year yields to an all-time low with investors continuing to snap up the securities on fading domestic political risk and support from European institutions. Elsewhere, Zambia became the first African country to ask bondholders for relief since the onset of the coronavirus.

In commodities oil was unchanged after fluctuating earlier, while gold continues to slide, dropping below $1,900 earlier and sliding below the 50DMA.

Looking at the day ahead, in addition to Powell speaking in the House, there is a slew of Fed speakers today, including Cleveland Fed President Loretta Mester, Chicago Fed President Charles Evans, Boston Fed President Eric Rosengren, Minneapolis Fed President Neel Kashkari, Atlanta Fed President Raphael Bostic, Fed Vice Chair for Supervision Randal Quarles and San Francisco Fed President Mary Daly. Latest U.S. government crude stockpile data is at 10:30 a.m. President Trump is due to speak to state attorneys general on social media abuses. The UN General Assembly continues.

Market Snapshot

- S&P 500 futures up 0.5% to 3,314.00

- STOXX Europe 600 up 1.3% to 362.11

- MXAP up 0.09% to 171.12

- MXAPJ up 0.2% to 557.55

- Nikkei down 0.06% to 23,346.49

- Topix down 0.1% to 1,644.25

- Hang Seng Index up 0.1% to 23,742.51

- Shanghai Composite up 0.2% to 3,279.71

- Sensex down 1% to 37,353.04

- Australia S&P/ASX 200 up 2.4% to 5,923.93

- Kospi up 0.03% to 2,333.24

- German 10Y yield fell 0.8 bps to -0.513%

- Euro down 0.2% to $1.1689

- Italian 10Y yield fell 5.2 bps to 0.661%

- Spanish 10Y yield fell 1.8 bps to 0.217%

- Brent futures up 0.4% to $41.87/bbl

- Gold spot down 1.1% to $1,879.89

- U.S. Dollar Index little changed at 93.94

Top Overnight News from Bloomberg

- The European Central Bank risks legal trouble if it tries to extend the “emergency powers” of its pandemic bond-buying plan to its other asset-purchase program, according to Executive Board member Yves Mersch

- SNB President Thomas Jordan has taken his foot off the pedal after the most aggressive currency intervention in five years early in the outbreak of the coronavirus pandemic

- The euro area’s economic recovery stalled this month as consumers fretted about a resurgence of the coronavirus and governments reinstated restrictions to control the spread of the disease

- Banks from Goldman Sachs Group Inc. to HSBC Holdings Plc have hit pause on plans to return workers in London after Prime Minister Boris Johnson appealed to Britons to work from home to help tame a resurgent coronavirus

- JPMorgan Chase & Co. is moving about 200 billion euros ($230 billion) from the U.K. to Frankfurt as a result of Britain’s exit from the European Union

A quick look at global markets courtesy of NewsSquawk

Asian equity markets traded mixed and failed to take full impetus from the rebound across their global peers, with the region tentative amid ongoing US-China tensions and with Japan suffering post-holiday blues on return from the extended weekend. Nonetheless, ASX 200 (+2.4%) outperformed and is on track for its best day in seven weeks as tech names led the broad advances after they found inspiration from the resurgence of the sector stateside, with sentiment also buoyed by increasing calls for the RBA to cut rates at next month’s meeting after RBA Deputy Governor Debelle recently outlined policy options. Nikkei 225 (U/C) was subdued as it played catch up to the recent days’ weakness and with Panasonic shares pressured alongside fellow Tesla supplier LG Chem after the EV-maker’s Battery Day Event fell flat where Elon Musk announced plans for a reduction in costs and to manufacture its own batteries, while he also showcased the Model S Plaid which is to be available next year. Conversely, Fujifilm Holdings was at the other side of the spectrum after announcing its Avigan drug met the primary endpoint in Phase 3 COVID trials. Hang Seng (+0.1%) and Shanghai Comp. (+0.2%) were indecisive as the continued PBoC liquidity efforts were offset by ongoing US-China tensions after US President Trump put China on blast for the spread of the coronavirus at the virtual UN meeting, while Beijing later criticized President Trump of spreading “political virus”. In addition, the uncertainty regarding the TikTok deal persists and the US House also overwhelmingly passed the forced labour bill which would ban imports from China’s Xinjiang region that were produced using forced labour. Finally, 10yr JGBs were higher amid the risk averse tone in Japan and with the BoJ also in the market for nearly JPY 1.3tln of JGBs in up to 10yr maturities, while it also offered to purchase 3yr-5yr corporate bonds.

Top Asian News

- Hong Kong’s BEA Is Said to Press Ahead With Life Insurance Sale

- Richard Li’s FWD Said to Plan Up to $3 Billion Hong Kong IPO

- Malaysia Leader Calls for Stability After Anwar Claims Majority

- Hong Kong Traders Chased 1,600-1 Odds to Buy IPO That Flopped

European equities are back on the grind higher (Euro Stoxx 50 +1.7%) after experience a fleeting blip lower on the back of French Services PMI dipping back into contractionary territory on second wave woes. The region picked up the baton from a mixed APAC handover, with reports also noting that the ECB as called upon Brussels to make the EU Recovery Fund a permanent measure. Bourses in the EU are seeing broad-based gains, whilst UK’s FTSE (+2.2%) ploughs ahead initially with the aid of a softer Sterling. Meanwhile UBS Wealth Management sees UK domestic banks falling 15-20% and insurance stocks decline by 7-10% in a no-deal Brexit scenario, but expects double digit positive returns from UK equities over the next 9-12 months in the event of a deal. Sectors in Europe are higher across the board with a slight cyclical/value bias, although material names do not fare so well amid the USD-induced declines across the metals complex. Consumer Discretionary meanwhile tops the charts with the aid of Nike (+13% pre-mkt) post-earnings, who beat on both top and bottom lines whilst reporting digital sales +82% YY – thus bolstering the likes of Adidas (+5.7%), Puma (+4.6%) and JD Sports (+5.1%). In terms of the breakdown, Travel & Leisure leads the gains, closely followed by Autos and Banks. Turning to individual movers, Osram Licht (+14.6%) is the top Stoxx 600 gainer after ASM (+1.4%) has signed a denomination and profit and loss transfer agreement with Osram as part of the takeover process.

Top European News

- Europe’s Economic Revival Put on Hold by Virus Resurgence

- U.K. Recovery Slows as Households Start to Rein In Spending

- Sunak Urged to Save U.K. Firms From ‘Ruin’ of Covid Curbs

- Merkel Resists Full Ban on Huawei, Making Germany an Outlier

In FX, the Dollar has extended its impressive recovery rally, partly in relief that the House finally passed the stopgap spending bill to avert a Government shutdown, but mainly as the Greenback continues to regain its global safe-haven and reserve status amidst the ongoing resurgence in COVID-19 that is accelerating outside the US and notably across Europe again. As a result, the index breached 94.000 and topped out just above 94.250, with several Buck/major pairings looking very vulnerable near or through psychological/round number levels.

- AUD/NZD - Dovish RBA calls via Westpac and NAB both looking for 15 bp cuts at the October meeting, plus a dovish RBNZ hold overnight, leaving the door wide open for more easing and in the offing or in the pipeline, an FLP by the end of 2020, according to the accompanying statement, have all added further pressure on the Aussie and Kiwi, with the former struggling to stay above 0.7100 and latter even less assured around 0.6600 ahead of NZ trade data.

- CAD - Some solace for the Loonie from relative stability in oil prices, but not enough momentum to convincingly reclaim 1.3300+ status within a 1.3345-1.3294 range awaiting the reopening of Canadian Parliament by PM Trudeau.

- CHF/EUR/GBP/JPY - All narrowly mixed vs the Dollar, but not before losing grip of 0.9200, 1.1700, 1.2700 and 105.00 handles respectively in advance of Thursday’s quarterly SNB policy review and following mixed Eurozone/UK prelim PMIs where services sector weakness outweighed manufacturing strength to keep the composite readings compressed. However, Sterling was undermined by domestic factors related to the coronavirus and warnings from Foreign Minister Raab about latest restrictions not going far enough to rule out the risk of reverting to full lockdown. Cable plumbed fresh lows around 1.2677 and Eur/Gbp retested recent peaks circa 0.9220 in response, but the Pound has subsequently received a reprieve from EU’s Barnier expressing determination to strike a Brexit trade deal. Elsewhere, pretty standard commentary from BoJ Governor Kuroda has marked the return of Japanese markets from their 4-day break, but not really the Yen between 104.91-105.19 parameters eyeing mega option expiries for tomorrow that span 105.00 in an even tighter band (104.90-105.10).

- SCANDI/EM - The Norwegian Crown continues to slip closer towards the sentimental if not technically significant 11.0000 level vs the Euro regardless of crude finding a base as noted above, but the Swedish Krona is still benefiting from Riksbank rigidity on the repo staying at the zero lower bound until this time in 2023. On that note, the Turkish Lira will be looking for continuity and some much needed support from the CBRT on Thursday via a form of indirect tightening as it plumbs almost daily record lows, and more immediately the Czech Koruna has the CNB to provide direction, albeit with no change in rates expected.

In commodities, WTI and Brent front month futures have nursed the losses seen in APAC hours, as sentiment in Europe picks back up after the EZ Services PMI fell back contraction but manufacturing topped estimates across the board. The initial weakness in the crude markets stemmed from a surprise build in the Private Inventory data (+0.7mln vs. Exp. -2.3mln), whilst concern remains over the demand implications from the reimposition of lockdowns and quarantine travel rules, with the Gazprom CEO also noting that we are seeing global oil demand recovery slowing down due to pandemic, and expects global oil consumption to return to pre-crisis level in H2 2021. In terms of the reopening supply from Libya, reports yesterday noted that next week could see output of some 260k BPD (vs. 1mln BPD pre-blockade), although analysts at ING downplay the relevance, noting that “In the current environment, where there are clear concerns over demand, additional supply will do little to help rebalance the market.” Something else to be aware of: reports noted that Chinese refiners are requesting additional import quotas for the fourth quota, having had taken advantage of the lower oil prices earlier this year. Desks note that further quota allocation could support the physical market. Aside from that, news-flow has remained relatively light for the complex thus far, WTI Nov meanders around USD 39.85/bbl (vs. low USD 39.26/bbl), while its Brent counterpart resides around 41.85/bbl (vs. low 41.21/bbl), awaiting the weekly EIA inventory data – with headline crude stocks seen drawing 2.325mln barrels. Elsewhere, precious metals initially succumb to the firmer Dollar and broader gains in stocks. Spot gold moves further below the USD 1900/oz mark to find support at USD 1875/oz, and has picked up given the most recent slip in the USD, whilst spot silver found a current base around the USD 23/oz level. Base metals are also mostly lower – with LME copper weighed on by the firmer Buck and lackluster China performance, whilst Dalian iron ore futures fell for a third straight days as higher shipments from mainstream miners weighed on prices.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -2.5%

- 9am: FHFA House Price Index MoM, est. 0.45%, prior 0.9%

- 9:45am: Markit US Manufacturing PMI, est. 53.5, prior 53.1; Services PMI, est. 54.5, prior 55; Composite PMI, prior 54.6

Fed Speakers:

- 9am: Fed’s Mester Discusses Payments and the Pandemic

- 10am: Powell Appears before House Panel on Covid-19

- 11am: Fed’s Evans Discusses the U.S. Economy and Monetary Policy

- 12pm: Fed’s Rosengren Discusses U.S. Economy

- 1pm: Fed’s Kashkari Discusses Public Health

- 1pm: Fed’s Bostic Speaks to Hale County Chamber of Commerce

- 2pm: Fed’s Quarles Gives Speech on the Economic Outlook

- 3pm: Fed’s Daly Discusses Labor Force Implications of Covid-19

DB's Jim Reid concludes the overnight wrap

I suspect this won’t be the last Zoom call I do from home after the U.K. yesterday effectively encouraged those who can work from home to do so - and possibly for the next 6 months. Today also sees a big change in the weather here as the Indian Summer has come to an abrupt end. Winter is coming in more ways than one. On the virus we’ve revamped our daily cases and fatality tables that appear in the PDF (click view report above) and given they are sorted worst to best they show that the U.K. is certainly not at the top of the second wave, but restrictions are nonetheless being tightened as case numbers build (4,926 yesterday and the highest since early May). In addition to WFH guidance, all hospitality venues must now close at 10pm daily from Thursday. In a nationwide address Johnson stressed the desire to avoid a full lockdown scenarios saying, “we must do all we can to avoid going down that road again.” Though if the infections continue to rise the government naturally left the option on the table. Meanwhile in Scotland, First Minister Nicola Sturgeon went even further, with a ban on households visiting other households indoors.

In Europe, the summit of EU leaders planned for this Thursday and Friday has now been postponed to the following week, after the President of the European Council, Charles Michel, went into quarantine because a security officer had tested positive. We also heard from German Chancellery Minister Braun that it is not the country’s ‘first choice’ to close borders to neighboring countries with high level of infections, citing the economic challenges. So here again we see a level of moderation in policy enactment during the second wave. Can this continue as the virus spreads? Cases are also rising in the US again, with the daily rate of people testing positive for the first time jumping to 5.9% in Florida after being under 5% for the better part of the last 2 weeks. We also saw some vaccine related news yesterday with the Washington Post reporting that the US FDA is expected to spell out a tough, new standard for an emergency authorisation of a coronavirus vaccine as soon as this week that will make it exceedingly difficult for any vaccine to be cleared before Election Day.

The virus news flow has been a difficult backdrop for markets this week but US markets started to gather some momentum after Europe went home last night. There was a particular reversal in US technology stocks, which continued to outperform after the late-session rally on Monday. The S&P 500 broke a four-day slide and gained +1.05%, however cyclicals sectors like Banks (-1.89%), Autos (-1.13%) and Energy (-1.03%) continued to lag. Retail (+3.64%), Media (+2.24%) and Software (+1.94%) all the led the S&P higher as the tech gains saw the NASDAQ rally +1.71%. This could again signal that the stay-at-home trade is coming back into vogue with further restrictions being seen in Europe. Europe still saw a slight recovery from Monday’s worst day for three months as the STOXX 600 climbed +0.20% higher.

Asian markets are mixed this morning with the Nikkei (-0.36%) and Kospi (-0.25%) both down while the Hang Seng (-0.01%) and Shanghai Comp (+0.02%) are trading broadly flat and the Asx (+2.15%) is up partly helped by stronger preliminary PMIs (more below). Japanese markets have reopened post 2 days of holiday. In overnight news, Tesla’s “Battery Day” event came short of expectations for a blockbuster leap forward as the company laid out a roadmap to build a $25,000 car only by 2023 which disappointed some. The stock was down -7% in aftermarket trading. This is also weighing on Nasdaq futures (-0.38%) while those on the S&P 500 are trading broadly flat.In fx, the US dollar index is up a further +0.25% this morning after yesterday’s +0.47% advance.

In other news, the US House passed a stopgap funding bill to keep the government operating through Dec. 11 after both parties in Congress and officials at the White House struck a deal to provide aid to farmers and food assistance for low-income families. The temporary spending bill will now move to the Senate for a vote.

Today, investors will be watching out for the flash PMIs for September, which will give us an early indication of how the global economy has fared this month. Overnight we’ve already had readings from Japan and Australia, with Japan struggling to recover further as manufacturing PMI rose by just 0.1 pt to 47.3 while the services reading improved to 45.6 (vs. 45.0 last month). Australia’s readings were a bit more robust with manufacturing PMI climbing to 55.5 (vs. 53.6 last month) and the services reading printing at 50.0 (vs. 49.0 last month). Australia’s reading seem to be helped partly by the easing of lockdown in Victoria, the second largest state. With infections rising again in Europe, not least in the UK, France and Spain, the question is to what extent this will impact on economic activity there as well. DB’s Peter Sidorov put out a piece yesterday (link here) in which he writes that his analysis points to a slight upside risk to the Euro Area PMI because of mobility trends, which has been rising in September. We’ll get those releases this morning.

Back to yesterday, and Fed Chair Powell appeared before the House Financial Services panel, where he again stressed the need to keep the virus under control and for further policy actions from “all levels of government.” Secretary Mnuchin who testified alongside the Fed Chair said that he and the President he would continue to seek Congressional agreement on further fiscal stimulus. Though now Congress seems like it will be more focused on a supreme court confirmation than fiscal stimulus in the short term. The Fed Chair said the Fed has only purchased $1.5 billion in loans so far through its Main Street Lending Program. The program is a $600 billion facility backed by Treasury funds, which aims to provide credit to small-mid sized companies. Mnuchin did bring up the idea of reallocating some of the unused money in Fed facilities to other uses, though it would require congressional approval.

There were a few other central bank headlines. From the ECB, we had Fabio Panetta of the Executive Board saying that “the risks of a policy overreaction are much smaller than the risks of policy being too slow or too shy to react and the worst-case scenarios materialising.” And over in the UK, Bank of England Governor Bailey downplayed the prospect of an imminent move to negative rates after last week’s MPC minutes showed that they were exploring the operational considerations of such a move.

In fixed income, there was a sharp narrowing of sovereign bond spreads in Europe, particularly following the regional election results in Italy that were regarded as positive for the government’s stability. Yields on 10yr BTPs fell -5.2bps to their lowest levels in almost a year, moving below the levels they were at before the pandemic hit the country in late February. And with the selloff for bunds, that sent the BTP-bund spread down -7.7bps to 1.37%, its lowest level in 7 months. Elsewhere, US Treasury yields saw a slight +0.5bps move higher, as the dollar index climbed a further +0.35% to reach its highest level in nearly 2 months.

Staying on the US, and with less than 6 weeks now until the election, President Trump said that he’d announce his choice this Saturday at 5pm (Washington Time) on who would replace Justice Ruth Bader Ginsburg on the Supreme Court. In a positive development for Trump, Senator Mitt Romney said that he’s in favour of moving forward with a confirmation vote on Trump’s choice, which leaves just 2 Republican senators out of the 53-member caucus who have opposed going ahead with a vote. With Trump’s choice on Saturday and the first debate between himself and Biden this Tuesday, the coming week will be one of the most important yet ahead of election day on November 3rd.

Looking at yesterday’s data, existing home sales in the US rose to an annualised rate of 6.00m in August, in line with expectations, and the most since 2006. Meanwhile the Richmond Fed’s manufacturing survey rose to 21 (vs. 12 expected). Finally, the advance consumer confidence reading from the Euro Area in September rose to -13.9 (vs. -14.7 expected). This was its highest level since March, but still some way below the -6.6 reading back in February before the full impact of the pandemic became apparent.

To the day ahead now, and the aforementioned flash PMIs will be one of the key highlights. Otherwise, there are an array of Fed speakers, including Chair Powell before the House Select Subcommittee on the Coronavirus Crisis, as well as the Vice Chair Quarles, Mester, Evans, Rosengren, Kashkari, Bostic and Daly. The ECB’s Hernandez de Cos will also be speaking.

International

Congress’ failure so far to deliver on promise of tens of billions in new research spending threatens America’s long-term economic competitiveness

A deal that avoided a shutdown also slashed spending for the National Science Foundation, putting it billions below a congressional target intended to…

Share this:

Federal spending on fundamental scientific research is pivotal to America’s long-term economic competitiveness and growth. But less than two years after agreeing the U.S. needed to invest tens of billions of dollars more in basic research than it had been, Congress is already seriously scaling back its plans.

A package of funding bills recently passed by Congress and signed by President Joe Biden on March 9, 2024, cuts the current fiscal year budget for the National Science Foundation, America’s premier basic science research agency, by over 8% relative to last year. That puts the NSF’s current allocation US$6.6 billion below targets Congress set in 2022.

And the president’s budget blueprint for the next fiscal year, released on March 11, doesn’t look much better. Even assuming his request for the NSF is fully funded, it would still, based on my calculations, leave the agency a total of $15 billion behind the plan Congress laid out to help the U.S. keep up with countries such as China that are rapidly increasing their science budgets.

I am a sociologist who studies how research universities contribute to the public good. I’m also the executive director of the Institute for Research on Innovation and Science, a national university consortium whose members share data that helps us understand, explain and work to amplify those benefits.

Our data shows how underfunding basic research, especially in high-priority areas, poses a real threat to the United States’ role as a leader in critical technology areas, forestalls innovation and makes it harder to recruit the skilled workers that high-tech companies need to succeed.

A promised investment

Less than two years ago, in August 2022, university researchers like me had reason to celebrate.

Congress had just passed the bipartisan CHIPS and Science Act. The science part of the law promised one of the biggest federal investments in the National Science Foundation in its 74-year history.

The CHIPS act authorized US$81 billion for the agency, promised to double its budget by 2027 and directed it to “address societal, national, and geostrategic challenges for the benefit of all Americans” by investing in research.

But there was one very big snag. The money still has to be appropriated by Congress every year. Lawmakers haven’t been good at doing that recently. As lawmakers struggle to keep the lights on, fundamental research is quickly becoming a casualty of political dysfunction.

Research’s critical impact

That’s bad because fundamental research matters in more ways than you might expect.

For instance, the basic discoveries that made the COVID-19 vaccine possible stretch back to the early 1960s. Such research investments contribute to the health, wealth and well-being of society, support jobs and regional economies and are vital to the U.S. economy and national security.

Lagging research investment will hurt U.S. leadership in critical technologies such as artificial intelligence, advanced communications, clean energy and biotechnology. Less support means less new research work gets done, fewer new researchers are trained and important new discoveries are made elsewhere.

But disrupting federal research funding also directly affects people’s jobs, lives and the economy.

Businesses nationwide thrive by selling the goods and services – everything from pipettes and biological specimens to notebooks and plane tickets – that are necessary for research. Those vendors include high-tech startups, manufacturers, contractors and even Main Street businesses like your local hardware store. They employ your neighbors and friends and contribute to the economic health of your hometown and the nation.

Nearly a third of the $10 billion in federal research funds that 26 of the universities in our consortium used in 2022 directly supported U.S. employers, including:

A Detroit welding shop that sells gases many labs use in experiments funded by the National Institutes of Health, National Science Foundation, Department of Defense and Department of Energy.

A Dallas-based construction company that is building an advanced vaccine and drug development facility paid for by the Department of Health and Human Services.

More than a dozen Utah businesses, including surveyors, engineers and construction and trucking companies, working on a Department of Energy project to develop breakthroughs in geothermal energy.

When Congress shortchanges basic research, it also damages businesses like these and people you might not usually associate with academic science and engineering. Construction and manufacturing companies earn more than $2 billion each year from federally funded research done by our consortium’s members.

Jobs and innovation

Disrupting or decreasing research funding also slows the flow of STEM – science, technology, engineering and math – talent from universities to American businesses. Highly trained people are essential to corporate innovation and to U.S. leadership in key fields, such as AI, where companies depend on hiring to secure research expertise.

In 2022, federal research grants paid wages for about 122,500 people at universities that shared data with my institute. More than half of them were students or trainees. Our data shows that they go on to many types of jobs but are particularly important for leading tech companies such as Google, Amazon, Apple, Facebook and Intel.

That same data lets me estimate that over 300,000 people who worked at U.S. universities in 2022 were paid by federal research funds. Threats to federal research investments put academic jobs at risk. They also hurt private sector innovation because even the most successful companies need to hire people with expert research skills. Most people learn those skills by working on university research projects, and most of those projects are federally funded.

High stakes

If Congress doesn’t move to fund fundamental science research to meet CHIPS and Science Act targets – and make up for the $11.6 billion it’s already behind schedule – the long-term consequences for American competitiveness could be serious.

Over time, companies would see fewer skilled job candidates, and academic and corporate researchers would produce fewer discoveries. Fewer high-tech startups would mean slower economic growth. America would become less competitive in the age of AI. This would turn one of the fears that led lawmakers to pass the CHIPS and Science Act into a reality.

Ultimately, it’s up to lawmakers to decide whether to fulfill their promise to invest more in the research that supports jobs across the economy and in American innovation, competitiveness and economic growth. So far, that promise is looking pretty fragile.

This is an updated version of an article originally published on Jan. 16, 2024.

Jason Owen-Smith receives research support from the National Science Foundation, the National Institutes of Health, the Alfred P. Sloan Foundation and Wellcome Leap.

economic growth covid-19 grants congress vaccine chinaInternational

What’s Driving Industrial Development in the Southwest U.S.

The post-COVID-19 pandemic pipeline, supply imbalances, investment and construction challenges: these are just a few of the topics address by a powerhouse…

Share this:

The post-COVID-19 pandemic pipeline, supply imbalances, investment and construction challenges: these are just a few of the topics address by a powerhouse panel of executives in industrial real estate this week at NAIOP’s I.CON West in Long Beach, California. Led by Dawn McCombs, principal and Denver lead industrial specialist for Avison Young, the panel tackled some of the biggest issues facing the sector in the Western U.S.

Starting with the pandemic in 2020 and continuing through 2022, McCombs said, the industrial sector experienced a huge surge in demand, resulting in historic vacancies, rent growth and record deliveries. Operating fundamentals began to normalize in 2023 and construction starts declined, certainly impacting vacancy and absorption moving forward.

“Development starts dropped by 65% year-over-year across the U.S. last year. In Q4, we were down 25% from pre-COVID norms,” began Megan Creecy-Herman, president, U.S. West Region, Prologis, noting that all of that is setting us up to see an improvement of fundamentals in the market. “U.S. vacancy ended 2023 at about 5%, which is very healthy.”

Vacancies are expected to grow in Q1 and Q2, peaking mid-year at around 7%. Creecy-Herman expects to see an increase in absorption as customers begin to have confidence in the economy, and everyone gets some certainty on what the Fed does with interest rates.

“It’s an interesting dynamic to see such a great increase in rents, which have almost doubled in some markets,” said Reon Roski, CEO, Majestic Realty Co. “It’s healthy to see a slowing down… before [rents] go back up.”

Pre-pandemic, a lot of markets were used to 4-5% vacancy, said Brooke Birtcher Gustafson, fifth-generation president of Birtcher Development. “Everyone was a little tepid about where things are headed with a mediocre outlook for 2024, but much of this is normalizing in the Southwest markets.”

McCombs asked the panel where their companies found themselves in the construction pipeline when the Fed raised rates in 2022.

In Salt Lake City, said Angela Eldredge, chief operations officer at Price Real Estate, there is a typical 12-18-month lead time on construction materials. “As rates started to rise in 2022, lots of permits had already been pulled and construction starts were beginning, so those project deliveries were in fall 2023. [The slowdown] was good for our market because it kept rates high, vacancies lower and helped normalize the market to a healthy pace.”

A supply imbalance can stress any market, and Gustafson joked that the current imbalance reminded her of a favorite quote from the movie Super Troopers: “Desperation is a stinky cologne.” “We’re all still a little crazed where this imbalance has put us, but for the patient investor and owner, there will be a rebalancing and opportunity for the good quality real estate to pass the sniff test,” she said.

At Bircher, Gustafson said that mid-pandemic, there were predictions that one billion square feet of new product would be required to meet tenant demand, e-commerce growth and safety stock. That transition opened a great opportunity for investors to run at the goal. “In California, the entitlement process is lengthy, around 24-36 months to get from the start of an acquisition to the completion of a building,” she said. Fast forward to 2023-2024, a lot of what is being delivered in 2024 is the result of that chase.

“Being an optimistic developer, there is good news. The supply imbalance helped normalize what was an unsustainable surge in rents and land values,” she said. “It allowed corporate heads of real estate to proactively evaluate growth opportunities, opened the door for contrarian investors to land bank as values drop, and provided tenants with options as there is more product. Investment goals and strategies have shifted, and that’s created opportunity for buyers.”

“Developers only know how to run and develop as much as we can,” said Roski. “There are certain times in cycles that we are forced to slow down, which is a good thing. In the last few years, Majestic has delivered 12-14 million square feet, and this year we are developing 6-8 million square feet. It’s all part of the cycle.”

Creecy-Herman noted that compared to the other asset classes and opportunities out there, including office and multifamily, industrial remains much more attractive for investment. “That was absolutely one of the things that underpinned the amount of investment we saw in a relatively short time period,” she said.

Market rent growth across Los Angeles, Inland Empire and Orange County moved up more than 100% in a 24-month period. That created opportunities for landlords to flexible as they’re filling up their buildings. “Normalizing can be uncomfortable especially after that kind of historic high, but at the same time it’s setting us up for strong years ahead,” she said.

Issues that owners and landlords are facing with not as much movement in the market is driving a change in strategy, noted Gustafson. “Comps are all over the place,” she said. “You have to dive deep into every single deal that is done to understand it and how investment strategies are changing.”

Tenants experienced a variety of challenges in the pandemic years, from supply chain to labor shortages on the negative side, to increased demand for products on the positive, McCombs noted.

“Prologis has about 6,700 customers around the world, from small to large, and the universal lesson [from the pandemic] is taking a more conservative posture on inventories,” Creecy-Herman said. “Customers are beefing up inventories, and that conservatism in the supply chain is a lesson learned that’s going to stick with us for a long time.” She noted that the company has plenty of clients who want to take more space but are waiting on more certainty from the broader economy.

“E-commerce grew by 8% last year, and we think that’s going to accelerate to 10% this year. This is still less than 25% of all retail sales, so the acceleration we’re going to see in e-commerce… is going to drive the business forward for a long time,” she said.

Roski noted that customers continually re-evaluate their warehouse locations, expanding during the pandemic and now consolidating but staying within one delivery day of vast consumer bases.

“This is a generational change,” said Creecy-Herman. “Millions of young consumers have one-day delivery as a baseline for their shopping experience. Think of what this means for our business long term to help our customers meet these expectations.”

McCombs asked the panelists what kind of leasing activity they are experiencing as a return to normalcy is expected in 2024.

“During the pandemic, shifts in the ports and supply chain created a build up along the Mexican border,” said Roski, noting border towns’ importance to increased manufacturing in Mexico. A shift of populations out of California and into Arizona, Nevada, Texas and Florida have resulted in an expansion of warehouses in those markets.

Eldridge said that Salt Lake City’s “sweet spot” is 100-200 million square feet, noting that the market is best described as a mid-box distribution hub that is close to California and Midwest markets. “Our location opens up the entire U.S. to our market, and it’s continuing to grow,” she said.

The recent supply chain and West Coast port clogs prompted significant investment in nearshoring and port improvements. “Ports are always changing,” said Roski, listing a looming strike at East Coast ports, challenges with pirates in the Suez Canal, and water issues in the Panama Canal. “Companies used to fix on one port and that’s where they’d bring in their imports, but now see they need to be [bring product] in a couple of places.”

“Laredo, [Texas,] is one of the largest ports in the U.S., and there’s no water. It’s trucks coming across the border. Companies have learned to be nimble and not focused on one area,” she said.

“All of the markets in the southwest are becoming more interconnected and interdependent than they were previously,” Creecy-Herman said. “In Southern California, there are 10 markets within 500 miles with over 25 million consumers who spend, on average, 10% more than typical U.S. consumers.” Combined with the port complex, those fundamentals aren’t changing. Creecy-Herman noted that it’s less of a California exodus than it is a complementary strategy where customers are taking space in other markets as they grow. In the last 10 years, she noted there has been significant maturation of markets such as Las Vegas and Phoenix. As they’ve become more diversified, customers want to have a presence there.

In the last decade, Gustafson said, the consumer base has shifted. Tenants continue to change strategies to adapt, such as hub-and-spoke approaches. From an investment perspective, she said that strategies change weekly in response to market dynamics that are unprecedented.

McCombs said that construction challenges and utility constraints have been compounded by increased demand for water and power.

“Those are big issues from the beginning when we’re deciding on whether to buy the dirt, and another decision during construction,” Roski said. “In some markets, we order transformers more than a year before they are needed. Otherwise, the time comes [to use them] and we can’t get them. It’s a new dynamic of how leases are structured because it’s something that’s out of our control.” She noted that it’s becoming a bigger issue with electrification of cars, trucks and real estate, and the U.S. power grid is not prepared to handle it.

Salt Lake City’s land constraints play a role in site selection, said Eldridge. “Land values of areas near water are skyrocketing.”

The panelists agreed that a favorable outlook is ahead for 2024, and today’s rebalancing will drive a healthy industry in the future as demand and rates return to normalized levels, creating opportunities for investors, developers and tenants.

This post is brought to you by JLL, the social media and conference blog sponsor of NAIOP’s I.CON West 2024. Learn more about JLL at www.us.jll.com or www.jll.ca.

fed pandemic covid-19 real estate interest rates mexicoInternational

Analyst reviews Apple stock price target amid challenges

Here’s what could happen to Apple shares next.

Share this:

They said it was bound to happen.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

Big plans for China

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

Related: Tech News Now: OpenAI says Musk contract 'never existed', Xiaomi's EV, and more

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

More Tech Stocks:

- Analyst unveils new Facebook stock price target after earnings

- Billionaire George Soros sold this popular semiconductor stock

- Ark’s Cathie Wood just traded 3 popular tech stocks

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic recovery european europe eu china

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Four Years Ago This Week, Freedom Was Torched

Red Candle In The Wind

Analyst reviews Apple stock price target amid challenges

The SNF Institute for Global Infectious Disease Research announces new advisory board

CDC Warns Thousands Of Children Sent To ER After Taking Common Sleep Aid

Economic Trends, Risks and the Industrial Market

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

Chronic stress and inflammation linked to societal and environmental impacts in new study

SoCal Industrial Prioritizes Speed, Power and Sustainability

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges