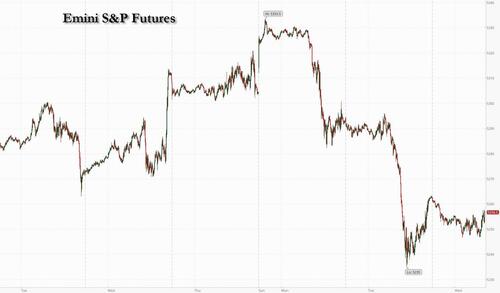

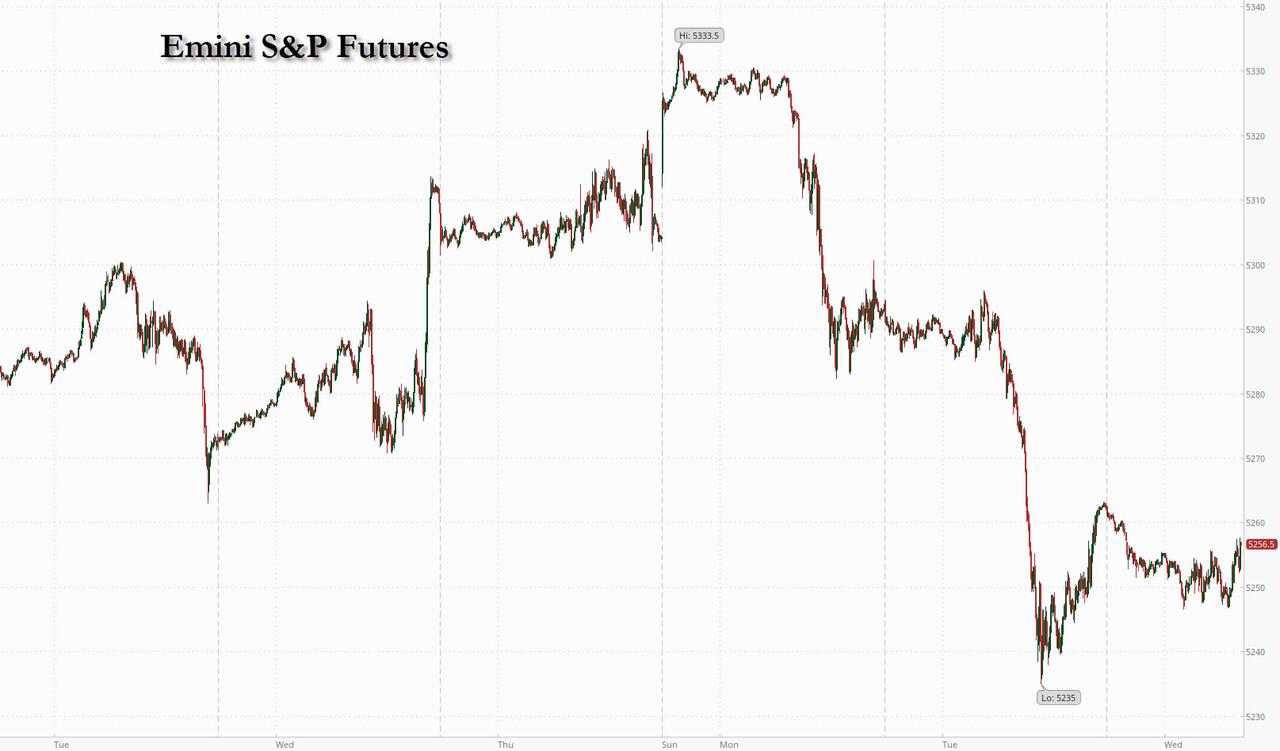

Futures Drop As Rates Continue Rising With Brent Back To $90

US futures are down small with Tech underperforming and small-caps flat, as rates held at 4 month highs, and Brent is about to rise above $90. As of 8:00am, both S&P and Nasdaq futures are down -0.2%, with yields higher pre-market ahead of Powell’s 12.10pm ET speech; despite his dovish rhetoric at the Mar 20 Fed Meeting press conference investors are nervous of a hawkish pivot according to JPM. This comes amid a surge a commodity prices and a spike in geopolitical tensions; pre-market all 3 commodity complexes are higher with gold the notable laggard despite USD being flat (although gold lagging these days means it hasn't hit a new all time high in the past 15 minutes). Today’s macro focus is on ADP (has not been predictive of the brutally manipulated NFP print), ISM Services and 2x Fedspeakers, including Powell.

In premarket trading, Mag7 and Semis are under pressure with Intel tumbling over 5% after the chipmaker said losses have deepened at its factory business and the unit may not reach a break-even point for several years. Here are some other notable premarket movers:

Ally Financial shares fall 2.6% in thin premarket trading after JPMorgan cut its recommendation to underweight from neutral. The broker also revisited its ratings on other consumer finance companies, downgrading Guild Holdings and Essent Group, while raising Navient.

Dave & Buster’s shares rise 7.1% after the restaurant chain reported fourth-quarter Ebitda that was ahead of consensus estimates. The company also announced an additional $100 million share-buyback program.

Vanda Pharmaceuticals shares rise 23% after the biopharmaceutical company said it got FDA approval for Fanapt (iloperidone) tablets for treating manic or mixed episodes associated with bipolar I disorder in adults.

Wolfspeed shares fall 2.2% as Wells Fargo Securities cut the recommendation on the semiconductor device company to equal-weight from overweight.

Global stocks are suddenly struggling to extend the previous quarter’s strong gains, with MSCI’s all-country index down for a third straight day, and Wall Street also heading for a weaker open, with contracts on the S&P Global index down 0.2% as 10-year Treasury yields crept higher again, rising to about 4.37%, up more than 15 basis points from last week’s close, after traders pared expectations for the timing and scope of US rate cuts this year and as commodity prices soared. The dollar held near seven-week highs against a basket of Group-of-Ten currencies.

The spotlight now is on Fed Chair Jerome Powell, who last week said the central bank is awaiting more evidence that inflation is in check and who speaks again today at 12:10pm ET. A strong monthly US jobs print on Friday, coming on top of a robust reading on US manufacturing, could further dent policy-easing expectations.

"Given the risk that payrolls data may affirm a higher-for-longer outlook for Fed rates, it is not surprising that risk appetite has taken a step back,” said Jane Foley, head of FX strategy at Rabobank in London.

Swap traders currently price less than three Fed rate cuts in 2024, with a high chance that policy easing is delayed beyond June. Pacific Investment Management Co. is among the asset managers that are positioning for the Fed to deliver fewer cuts than other major central banks. That’s despite comments Tuesday from San Francisco President Mary Daly and the Cleveland Fed’s Loretta Mester, who threw their weight behind three cuts this year.

Rising commodity prices, meanwhile, are fanning inflation expectations, with Brent crude futures holding above $89 a barrel. Copper advanced for a third day, while palm oil is at the highest since November 2022, raising the risk of higher global food inflation. Adding to the concerns, Taiwan’s strongest earthquake in 25 years cast uncertainty over chip production, as the world’s largest chipmaker, Taiwan Semiconductor, evacuated factory areas. Shares in the firm slipped 1.3%.

In Europe, the Stoxx 600 equity index held flat and bond yields slipped after a below-forecast inflation print. That cemented expectations that the European Central Bank will kick off its policy-easing campaign in June, possibly ahead of the Federal Reserve. European markets rebounded as bonds caught a bid following yesterday’s global rates selloff after the latest Euro area CPI data came in cooler than expected. Baskets tied to a recovery/reflation scenario continue to perform well. Rising Yields/Value are leading, Momentum/Quality are lagging; Cyclicals over Defensives. UKX -0.4%, SX5E +0.5%, SXXP +0.1%, DAX +0.3%.

Earlier in the session, Asian equities declined, driven by losses in technology stocks, amid speculation that major global central banks will keep interest rates higher for longer. The MSCI Asia Pacific Index fell as much as 0.8%, to a two-week low, with virtually all markets in the red. Chip-related stocks were among the biggest drags on the region after Intel posted widening foundry losses and TSMC evacuated production lines following Taiwan’s biggest earthquake in 25 years. EV makers led a gauge of tech stocks lower in Hong Kong after Tesla missed expectations for deliveries.

“I think people are just mindful of what happens with rates, especially with the Fed,” Catherine Yeung, investment director at Fidelity International, told Bloomberg TV. “Investors are treading water and looking for opportunity,” she said.

Asian equities have struggled in the first week of the new quarter, with Japan and China failing to build on recent gains. Pessimism returned following Tuesday’s strong rally in Hong Kong, as a recent slew of upbeat Chinese economic data failed to provide further momentum. The yuan slid to a four-month low against the dollar in onshore trading Tuesday.

Hang Seng and Shanghai Comp. conformed to the downbeat mood across the region amid tech weakness and mixed US-China headlines with the US asking South Korea to toughen controls on semiconductor technology exports to China. However, the losses in the mainland were cushioned after an improvement in Caixin Services PMI data and Biden-Xi phone talks.

Nikkei 225 briefly dipped beneath 39,500 with index heavyweight Fast Retailing among the worst hit after lower Uniqlo same-store sales, while Japan also issued a tsunami warning after a powerful earthquake struck Taiwan.

TAIEX was pressured after Taiwan's most powerful earthquake in 25 years which collapsed at least 26 buildings.

ASX 200 was led lower by tech and real estate as the rate-sensitive sectors suffered from firmer yields.

In FX, the Bloomberg Dollar Spot Index is little changed in another quiet session for FX. The onshore yuan fell toward the weak end of its allowed trading band.

In rates, treasuries fell and kept US equity futures subdued as investors awaited another batch of economic data and a flurry of Fed speakers later today including Powell. US 10-year yields rise 2bps to 4.37%, close to Tuesday’s year-to-date high of 4.40%. ISM services will be closely watched after the manufacturing gauge topped estimates on Monday. Fed Chair Powell is also due to deliver remarks on the economic outlook. Bunds rise as data showed euro-area inflation slowed more than expected in March. European stocks inch higher.

In commodities, oil prices advance, with WTI rising 0.3% to trade near $85.40 and Brent just shy of $90. Spot gold falls 0.3%.

The Bitcoin sell-off from the prior day has cooled, with the coin now holding around USD 66.5k after the latest ETF flows data showed a reversal to yesterday's GBTC-driven outflow.

Looking to the day ahead now, data releases in the US include the ADP’s report of private payrolls for March, and the ISM services index for March. Otherwise from central banks, we’ll hear from Fed Chair Powell, along with the Fed’s Bowman, Goolsbee, Barr and Kugler, as well as the ECB’s De Cos.

Market Snapshot

S&P 500 futures down 0.2% to 5,251.00

STOXX Europe 600 little changed at 508.19

MXAP down 0.8% to 175.21

MXAPJ down 0.9% to 536.40

Nikkei down 1.0% to 39,451.85

Topix down 0.3% to 2,706.51

Hang Seng Index down 1.2% to 16,725.10

Shanghai Composite down 0.2% to 3,069.30

Sensex up 0.1% to 73,999.33

Australia S&P/ASX 200 down 1.3% to 7,782.54

Kospi down 1.7% to 2,706.97

German 10Y yield little changed at 2.40%

Euro little changed at $1.0775

Brent Futures down 0.1% to $88.82/bbl

Gold spot down 0.4% to $2,270.51

US Dollar Index little changed at 104.76

Top Overnight News

Taiwan was hit by its strongest earthquake in 25 years, leveling dozens of buildings on the eastern side of the island. At least nine people died, Taiwan’s emergency service said. TSMC halted some chipmaking and evacuated plants. BBG

Nato is drawing up plans to secure a five-year military aid package of up to $100bn, in an attempt to shield Ukraine from “winds of political change” that could usher in a second Trump presidency. FT

In meetings in Guangzhou and Beijing, Yellen is expected to tell her Chinese counterparts to stop relying on exports to prop up their underperforming economy and instead boost their own consumer market. The warning from Yellen is a sign that the Biden administration is moving toward raising Trump-era tariffs on some Chinese products, including electric vehicles. Such a move could reignite tensions between the world’s two largest economies, which have tried to stabilize relations in recent months. WSJ

Eurozone CPI for Mar falls a bit short of expectations, coming in at +2.4% on the headline (down from +2.6% in Feb and below the Street’s +2.5% forecast) and +2.9% core (down from +3.1% in Feb and below the Street’s +3% forecast). BBG

Joe Biden rebuked Israel for not doing enough to protect civilians and aid workers in Gaza, some of his sternest criticism yet of the country’s conduct. The remarks echo reprimands from the UK and Australia as Israel’s global isolation grows. BBG

Auto sales in the US Mar came in at an annualized rate of 15.5M last month, down from 15.8M in Feb and below the consensus forecast of 15.9M, while average sales prices tumbled 3.6% Y/Y (the largest recorded decline in the month of March) and discounts surged by ~66%. Marketwatch

The rally in crude prompted the US to cancel plans to buy up to 3 million barrels for its strategic reserve. Separately, US stockpiles fell by 2.3 million barrels last week, the API is said to have reported, and OPEC+ may today affirm its current supply curbs. BBG

Loretta Mester, president of the Cleveland Federal Reserve and a voting member of the Federal Open Market Committee, revealed in a speech on Tuesday that she had raised her estimate of the longer-run federal funds rate from 2.5% to 3%. FT

Disney secured enough votes before today’s shareholder meeting to defeat a challenge against its board by Nelson Peltz’s Trian, Reuters reported. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks followed suit to losses in the US where treasuries bear-steepened and oil prices ramped up. ASX 200 was led lower by tech and real estate as the rate-sensitive sectors suffered from firmer yields. Nikkei 225 briefly dipped beneath 39,500 with index heavyweight Fast Retailing among the worst hit after lower Uniqlo same-store sales, while Japan also issued a tsunami warning after a powerful earthquake struck Taiwan. TAIEX was pressured after Taiwan's most powerful earthquake in 25 years which collapsed at least 26 buildings. Hang Seng and Shanghai Comp. conformed to the downbeat mood across the region amid tech weakness and mixed US-China headlines with the US asking South Korea to toughen controls on semiconductor technology exports to China. However, the losses in the mainland were cushioned after an improvement in Caixin Services PMI data and Biden-Xi phone talks.

Top Asian News

US Treasury Secretary Yellen is to travel to China on April 3rd-9th to continue economic dialogue with top Chinese officials and is to meet with Vice Premier He Lifeng, the Guangdong province Governor and US business executives in Guangzhou. Furthermore, Yellen is to meet with PBoC's Governor Pan Gongsheng and former Vice President Liu He on April 8th, while she is to underscore global economic consequences of Chinese industrial overcapacity in meetings with Chinese officials.

A strong earthquake was felt in Taipei and parts of the city experienced a power outage, while the Taiwan Central Weather Administration said the earthquake registered a 7.2 magnitude and was Taiwan's most powerful earthquake in 25 years. Taipei city government said it had not yet received any reports of major damage following the earthquake and it was later reported that Taipei’s MRT resumed operations although there were reports of collapsed buildings in the city of Hualien with people reportedly trapped in the buildings, while Taiwan announced the earthquake caused 26 buildings to collapse.

Japan issued an evacuation advisory for Okinawa coastal areas and a tsunami warning after the initial announcement of a preliminary magnitude 7.5 earthquake off southwestern Japan but later revised the Taiwan earthquake magnitude up to 7.7 and lifted the tsunami warnings.

China March prelim car sales +7% Y/Y (vs -21% in Feb).

Foxonn (2354 TT) says Co. shut down some of its production lines in Taiwan for inspection following the earthquake; currently normal production operations have gradually resumed; no damage to manufacturing equipment.

European bourses, Stoxx600 (+0.2%), were mostly but modestly firmer at the open, and trade remained directionless up until the EZ CPI; following the print, stocks trudged higher. European sectors hold a negative tilt, though with no overarching theme or bias. Banks and Tech take the top spots, whilst Real Estate continues to be hampered by the yield environment. US Equity Futures (ES -0.2%, NQ -0.2%, RTY -0.3%) are all marginally lower continuing the downside seen in the prior session. Intel (-4.6%) suffers pre-market after reporting its Foundry had an op. loss for 2023 at USD 7bln.

Top European news

ECB's Holzmann says he has no in-principle objection to a June rate cut, but wants to see more supportive data. Holzmann added that cutting out-of-sync with the Fed would diminish the impact of easing, whilst also noting that a 3.0% deposit rate could prove too tight over the longer-term, given weak EZ productivity.

Italian Finance Minister Giorgetti says the EU is to open a deficit infringement procedure against Italy and several other countries. Adds, Italy is already in line with the EU requirements to cut deficit below 3% of GDP over time

Barclays raises Eurostoxx600 target to 540 (prev. target 510, current 508); upgrades Europe to overweight.

Norwegian Parliament received a bomb threat, according to local reports; debate continues in Norway's parliament despite bomb threat

FX

USD on net steady vs. peers after failing to hold above the 105 mark, within a tight 104.84-70 range; topped out at 105.10 yesterday.

EUR is contained vs. the USD as post-CPI downside proved to be fleeting. The data may accelerate calls for a move next week but June still firmly the base case. EUR/USD holding above yesterday's 1.0724 low.

USD/JPY remains in consolidation mode around recent highs as recent Fed repricing provides support. Upside targets include the YTD high at 151.97 and the psych 152 mark, above which, there is clean air.

Antipodeans are both a touch softer vs. the USD after yesterday's session of gains. AUD able to hold onto a 0.65 handle and above yesterday's 0.6482 low.

PBoC set USD/CNY mid-point at 7.0949 vs exp. 7.2282 (prev. 7.0957).

Chile Central Bank cut its benchmark interest rate by 75bps to 6.50%, as expected, with the decision unanimous. Chile Central Bank said the board will continue cutting rates, while the size and timing of rates will consider the trajectory of inflation and the macroeconomic scenario.

Fixed Income

USTs were contained during APAC trade as participants took a slight breather from Tuesday's pronounced bear-steepening, though overnight Fed speak was on the hawkish side of things. Modest pressure emerged in the European morning, USTs down to a 109-18 base before Tuesday's 109-14+ trough.

Bunds were initially contained, in-fitting with USTs, before experiencing modest upside on Holzmann's remarks which had an uncharacteristic dovish-tilt. A dovish but fleeting reaction was seen following the cooler than expected EZ HICP print. Currently near session peaks around 132.50.

BTPs were dented after Economy Minister Giorgetti announced that the EU is likely to begin deficit infringement procedures against the nation and others, sending BTPs down from 117.90 to 117.50 where they currently reside.

Commodities

Horizontal trade in the crude complex overnight and in early European hours ahead of the OPEC+ JMMC at 12:00BST, although no recommendations are expected. Brent holds around USD 88.20/bbl.

Mixed trade for precious metals with some potential profit-taking (ahead of US ADP and a slew of Fed speakers) in the yellow metal after hitting a fresh ATH this morning at USD 2,288.43/oz; XAU has pulled back towards the bottom of a USD 2,269.27-2,288.82/oz intraday range.

Flat/mixed picture across base metals amid quiet newsflow and with the complex taking a breather after yesterday's data-induced rally.

US Energy Inventory Data (bbls): Crude -2.3mln (exp. -1.5mln), Gasoline -1.5mln (exp. -0.8mln), Distillate -2.5mln (exp. -0.6mln), Cushing -0.8mln.

Mexico's Pemex requested trading unit PMI to cancel up to 436k bpd of Mexican crude exports in April which would increase the availability of crude for domestic use including for a new refinery, according to a document cited by Reuters.

US President Biden is reportedly open to ending LNG export pause for Ukraine aid, according to Reuters.

Russian Deputy PM Novak said gasoline and diesel fuel stocks remain high in Russia.

Kazahkstan's Kashagan oil field operator says output was fully restored on April 2 after brief stoppage on April 1.

Indian oil secretary says higher oil prices are a cause of concern; oil prices reflect geopolitical premium; firms will take appropriate decision on fuel prices if global oil prices stay high for more than a month.

Spot premiums for US Mars crude exports to Asia reportedly jump after Mexico cuts supply, according to Reuters sources.

Some Japanese aluminium buyers agree April-June premium at USD 148/ton, +64% from prev. quarter.

BofA research increases 2024 Brent and WTI crude forecasts to USD 86 and USD 81/bbl respectively; sees prices peaking at around USD 95/bbl in the summer

OPEC's JMMC will meet at 12:00BST on April 3rd, according to Energy Intel's Bakr.

Geopolitics: Middle East

US President Biden criticised Israel for failing to adequately protect civilians and is pushing for an immediate ceasefire as part of a hostage deal, while Biden said he is outraged over the deaths of World Central Kitchen staff in Gaza, according to Bloomberg and AFP.

Deep divisions between the US and Israel over an operation in Rafah were evident in a virtual meeting between senior officials, according to three sources cited by Axios. Furthermore, the parties agreed there will be separate virtual meetings of four expert working groups in the next 10 days that will focus on different aspects of a possible Rafah operation.

Geopolitics: Other

NATO Foreign Ministers will meet on Wednesday to discuss how to put military support for Ukraine on long-term footing including a proposal for a EUR 100bln five-year military fund, according to Reuters.

North Korea said it successfully test-fired a new mid- to long-range hypersonic missile, while its leader Kim said they completely turned all missiles to solid fuel with warhead control and capable of nuclear weaponisation, according to Yonhap.

UK FCDO said North Korea's ballistic missile launch on April 2nd is a breach of multiple UN Security Council resolutions and the UK urges North Korea to refrain from further provocations, return to dialogue and take credible steps towards denuclearisation.

Philippine National Security Council spokesperson said the commitment to maintain the grounded warship in Second Thomas Shoal will always be there and any attempt by China to interfere with resupply missions will be met by the Philippines in a fashion that protects its troops, while the spokesperson added that resupply missions to Second Thomas Shoal will never stop.

US Event Calendar

07:00: March MBA Mortgage Applications, prior -0.7%

08:15: March ADP Employment Change, est. 150,000, prior 140,000

09:45: March S&P Global US Services PMI, est. 51.7, prior 51.7

March ISM Services Prices Paid, est. 58.4, prior 58.6

March ISM Services Employment, est. 49.0, prior 48.0

March ISM Services New Orders, est. 55.5, prior 56.1

March ISM Services Index, est. 52.8, prior 52.6

Central Bank Speakers

08:30: Fed’s Bostic Speaks on CNBC

09:45: Fed’s Bowman Speaks on Bank Liquidity, Fed

12:00: Fed’s Goolsbee Gives Opening Remarks

12:10: Fed’s Powell Speaks on Economic Outlook

13:10: Fed’s Barr Speaks on Community Reinvestment Act

16:30: Fed’s Kugler Speaks on Economic, Monetary Policy Outlook

DB's Jim Reid concludes the overnight wrap

Markets continued their rocky start to Q2 yesterday, with bonds and equities both selling off for a second day running. That’s been driven by a succession of hawkish developments, which have led to growing questions about how soon the Fed will be cutting rates, particularly given the resilience of both growth and inflation. All eyes will now be on Fed Chair Powell’s remarks today, but in the meantime, the 10yr Treasury yield was up another +4.0bps yesterday to 4.35%, marking its highest level since November. And equities also struggled in response, with the S&P 500 (-0.72%) posting its worst daily performance in 4 weeks.

These moves have come on the back of several headlines in recent days, which have seen investors price out the number of rate cuts likely to happen this year. On Friday, we had the latest PCE inflation print for February, which is the measure the Fed officially targets. And even though the monthly print was broadly as the consensus expected, it still meant that core PCE over the previous 3 months was running at an annualised rate of 3.5%. Then on Monday, the ISM manufacturing was back in expansionary territory for the first time since October 2022, whilst the prices paid indicator was the highest since July 2022. Yesterday, that was then followed up by a fresh rise in oil prices, which saw Brent Crude close at nearly $89/bbl, its highest since October, and Bloomberg’s Commodity Spot Index (+0.79%) also hit a 4-month high. And with all that happening, there’ve been clear signs that investors are raising their inflation expectations as well. For instance, 5yr US inflation swaps were up another +2.5bps yesterday to 2.53%, closing at their highest level since November.

This backdrop has led to a significant selloff for sovereign bonds around the world, with a sharp rise in yields. In the US, it saw the 10yr Treasury yield rise +3.9bps to 4.35%, which built on its +10.9bps move the previous day. And 30yr yields were up +4.7bps to 4.50%, with both reaching their highest levels since November. Meanwhile in Europe, there were even bigger moves as they caught up from the previous day’s holiday. For example, yields on 10yr bunds (+10.0bps), OATs (+11.1bps), BTPs (+12.5bps) all saw significant rises. And here in the UK, 10yr gilts (+15.1bps) saw the biggest rise in yields after multiple data releases came in stronger than expected. That included mortgage approvals, which were up to a 17-month high in February of 60.4k (vs. 56.5k expected). Moreover, the final UK manufacturing PMI for March was revised up to 50.3 (vs. flash 49.9), which is the first in expansionary territory since July 2022.

The main exception to that bond selloff came at the front-end of the US Treasury curve, where the 2yr yield was down -1.6bps to 4.69%. That came as market pricing for a June cut moved up slightly relative to Monday, with futures now pricing in a 66% chance of a cut by June. In part, that followed fairly balanced remarks from Fed speakers. San Francisco Fed President Daly said that three cuts this year was “a very reasonable baseline” but that as of now “growth is going strong, so there’s really no urgency to adjust the rate”. Cleveland Fed President Mester also said she still saw three cuts in 2024 but that “it’s a close call” whether fewer cuts would be needed, and noting earlier that “At this point, I think the bigger risk would be to begin reducing the funds rate too early.”

Today, we’ll hear from Fed Chair Powell who’s giving a speech on the economic outlook, so the focus will be on whether he offers any new commentary about the timing of potential rate cuts. We’ve also got the ISM services index today, along with the jobs report on Friday, so there’s still plenty of data this week that will shape the market narrative.

For equities, the concern about rates staying higher for longer led to a sizeable selloff, with the major indices losing ground on both sides of the Atlantic. That meant the S&P 500 (-0.72%) saw its worst daily performance in 4 weeks, and the STOXX 600 (-0.80%) saw its worst performance in 7 weeks. The decline was a broad-based one, with almost 80% of the S&P 500 losing ground on the day. Small caps underperformed for the second session in a row, with the Russell 2000 down -1.80%. But losses among US tech stocks were also a factor, and the Magnificent 7 (-0.90%) fell to a two-week low. That came as Tesla fell -4.90% after it reported lower-than-expected sales, with its first year-on-year decline in vehicle deliveries since 2020.

That negative tone has continued overnight, with all the major indices in Asia moving lower this morning. That includes the Nikkei (-0.64%), the KOSPI (-1.19%), the Hang Seng (-0.74%), the CSI 300 (-0.28%) and the Shanghai Comp (-0.24%). And over in the US, futures on the S&P 500 (-0.17%) are pointing towards further losses today. Alongside that, Taiwan has been hit by an earthquake overnight of 7.4 magnitude, the strongest there in 25 years. Separately on the PMIs, the final composite PMI in Japan was up to a 6-month high of 51.7 in March, whilst the Caixin composite PMI from China was up to a 10-month high of 52.7.

Whilst there was a lot of focus on the hawkish narrative yesterday, we did get a downside inflation surprise from Germany yesterday, which follows other downside surprises from Europe over recent days. The release showed CPI was down to +2.3% using the EU-harmonised measure (vs. +2.4% expected), and using the national definition, it was down to its lowest since May 2021, at +2.2%. So adding some encouraging signs ahead of the Euro Area March inflation print this morning. Alongside that, we also got some positive news from the final Euro Area manufacturing PMI, which was revised up four-tenths from the flash reading to 46.1.

Finally in the US, there were several data prints for February out yesterday, including the JOLTS report of job openings. That showed openings were at 8.756m (vs. 8.73m expected), which was basically in line with the downwardly-revised 8.748m in January. Indeed, it was the smallest monthly change in job openings since the pandemic. Elsewhere, the report showed that the quits rate of those voluntarily leaving their job was stable at 2.2%, where it’s been since November.

To the day ahead now, and data releases from the Euro Area include the flash CPI print for March, along with the unemployment rate for February. Meanwhile in the US, there’s the ADP’s report of private payrolls for March, and the ISM services index for March. Otherwise from central banks, we’ll hear from Fed Chair Powell, along with the Fed’s Bowman, Goolsbee, Barr and Kugler, as well as the ECB’s De Cos.

As the global economy continues to take new shape in its recovery from the Covid-19 pandemic, many companies are still reeling from the high costs and supply shortages the health crisis triggered.

And a significant number of them are filing for bankruptcy.

Major bankruptcy filings in 2023 included the working space company WeWork in November, drug store retailer Rite Aid in October, and Bed, Bath & Beyond in April.

The trend has continued in 2024. In fact, telecom company Airspan Networks Holdings (MIMO) filed for a prepackaged Chapter 11 bankruptcy in Delaware on March 31.

A lot of the news around bankruptcies involves how companies are restructuring their debts or going out of business entirely. But if a company that files for bankruptcy has a stock that is publicly traded, the question of what happens to shareholders is worth examining.

In Airspan's case, existing holders of stock have been given two options. One is to receive their pro rata share of $450,000. The other is to elect for warrants instead of cash. But if more than 150 shareholders decide to take the warrants, no warrants at all will be given.

A pro rata share is the cash value of a proportionate number of owned shares based on the determined total value.

A warrant is similar to an option, where the holder can purchase a security at a specific price and quantity at a future time. But unlike options, warrants are issued by a company rather than a central exchange.

What bankruptcy means for the people affected

The thought of bankruptcy is scary for companies, their employees and shareholders.

The companies themselves would enter a reality where they are forced to ponder their very survival.

Employees, naturally, wonder about the security of their jobs.

The impact on shareholders of a company filing for bankruptcy has a few layers of complexity.

In Chapter 7 bankruptcy, a company is simply going out of business. It sells its assets to pay off debts. Shareholders are left to split what's left, if there is anything remaining at all. If there is not, shareholders can get nothing.

When a company is considering filing for Chapter 11 bankruptcy, it is likely looking to restructure and stage a comeback. If shareholders are brave enough to hold onto their shares during this process, which is risky, they at least stand the chance of making some money back.

For example, car rental company Hertz (HTZ) filed for Chapter 11 in May 2020 as the Covid-19 pandemic wounded the travel business generally. While the stock has struggled recently, the company did come out of bankruptcy in July 2021.

Employees are pictured pondering the bankruptcy of their company, peering out the window of a building.

Shutterstock

In bankruptcy events, shareholders are last in line

When a company goes bankrupt, hanging on to its shares is dicey business. Shareholders could wind up with little or nothing, but they may be rewarded for their patience.

In the short term, the stock is probably already down at the filing and is destined to stay that way for a while. But in the long term, there may be hope for a revival.

Shareholders are the last ones to be considered for payouts. First to get any money from liquidated assets or cash advancements are secured creditors such as banks holding mortgage or equipment loans, for example. Unsecured creditors, including banks, suppliers and bondholders are next. Then come the shareholders.

"The stock could very well become completely worthless," writes The Balance. "But there’s always a chance that the company could emerge from bankruptcy stronger and stock prices may rise. In the short-term, however, the stock price is likely to stay very low during bankruptcy and immediately after."

As the global economy continues to take new shape in its recovery from the Covid-19 pandemic, many companies are still reeling from the high costs and supply shortages the health crisis triggered.

And a significant number of them are filing for bankruptcy.

Major bankruptcy filings in 2023 included the working space company WeWork in November, drug store retailer Rite Aid in October, and Bed, Bath & Beyond in April.

The trend has continued in 2024. In fact, telecom company Airspan Networks Holdings (MIMO) filed for a prepackaged Chapter 11 bankruptcy in Delaware on March 31.

A lot of the news around bankruptcies involves how companies are restructuring their debts or going out of business entirely. But if a company that files for bankruptcy has a stock that is publicly traded, the question of what happens to shareholders is worth examining.

In Airspan's case, existing holders of stock have been given two options. One is to receive their pro rata share of $450,000. The other is to elect for warrants instead of cash. But if more than 150 shareholders decide to take the warrants, no warrants at all will be given.

A pro rata share is the cash value of a proportionate number of owned shares based on the determined total value.

A warrant is similar to an option, where the holder can purchase a security at a specific price and quantity at a future time. But unlike options, warrants are issued by a company rather than a central exchange.

What bankruptcy means for the people affected

The thought of bankruptcy is scary for companies, their employees and shareholders.

The companies themselves would enter a reality where they are forced to ponder their very survival.

Employees, naturally, wonder about the security of their jobs.

The impact on shareholders of a company filing for bankruptcy has a few layers of complexity.

In Chapter 7 bankruptcy, a company is simply going out of business. It sells its assets to pay off debts. Shareholders are left to split what's left, if there is anything remaining at all. If there is not, shareholders can get nothing.

When a company is considering filing for Chapter 11 bankruptcy, it is likely looking to restructure and stage a comeback. If shareholders are brave enough to hold onto their shares during this process, which is risky, they at least stand the chance of making some money back.

For example, car rental company Hertz (HTZ) filed for Chapter 11 in May 2020 as the Covid-19 pandemic wounded the travel business generally. While the stock has struggled recently, the company did come out of bankruptcy in July 2021.

Employees are pictured pondering the bankruptcy of their company, peering out the window of a building.

Shutterstock

In bankruptcy events, shareholders are last in line

When a company goes bankrupt, hanging on to its shares is dicey business. Shareholders could wind up with little or nothing, but they may be rewarded for their patience.

In the short term, the stock is probably already down at the filing and is destined to stay that way for a while. But in the long term, there may be hope for a revival.

Shareholders are the last ones to be considered for payouts. First to get any money from liquidated assets or cash advancements are secured creditors such as banks holding mortgage or equipment loans, for example. Unsecured creditors, including banks, suppliers and bondholders are next. Then come the shareholders.

"The stock could very well become completely worthless," writes The Balance. "But there’s always a chance that the company could emerge from bankruptcy stronger and stock prices may rise. In the short-term, however, the stock price is likely to stay very low during bankruptcy and immediately after."

East Hanover, NJ – April 2, 2024 – A recent commentary published in The Journal of Spinal Cord Medicine highlights the unprecedented upward trend in employment for people with disabilities, accelerated by the COVID-19 pandemic’s economic recovery phase.

Credit: Disability: In/ Jordan Nicholson

East Hanover, NJ – April 2, 2024 – A recent commentary published in The Journal of Spinal Cord Medicine highlights the unprecedented upward trend in employment for people with disabilities, accelerated by the COVID-19 pandemic’s economic recovery phase.

In ”Employment and people with disabilities: Reframing the dialogue in the post-pandemic era,” (DOI: 10.1080/10790268.2024.2315927) published on February 22, 2024, the authors examine the confluence of factors contributing to the recent record-high employment levels among people with disabilities. This trend has been supported by a favorable labor market, evolving employer attitudes, and the adoption of inclusive workplace practices. A series of National Trends in Disability Employment (nTIDE) reports issued by Kessler Foundation and the University of New Hampshire Institute on Disability explored the contributions of diverse subgroups within the disability community to this positive shift.

A contributing factor was the rapid adaptation by employers to the acute labor shortages caused by the pandemic. Innovations in recruiting, hiring, training, and employee retention have expanded opportunities for people with disabilities. Notably, a 2022 Kessler Foundation survey revealed significant shifts in supervisors’ perceptions towards more inclusive hiring practices and accommodations, signaling a sustainable change in workplace culture.

The authors also address the uncertainties about the longevity of these gains as the pandemic’s direct impact wanes. The widespread adoption of remote work, recognized as beneficial for many employees including those with disabilities, faces a future of mixed prospects as workplaces readjust and offices reopen. Yet, evidence suggests remote and hybrid work arrangements as viable, ongoing options that will continue to support employment equity for people with disabilities.

The article underscores the importance of continued research and policy development to extend the upward trend for employment of people with disabilities. By recognizing the achievements and challenges highlighted during the post-pandemic recovery, stakeholders can work towards further narrowing the employment gap and fostering a more inclusive economy.

About the Journal of Spinal Cord Medicine

The Journal of Spinal Cord Medicine (JSCM) serves the international community of professionals dedicated to improving the lives of people with injuries/disorders of the spinal cord. JSCM is the peer-reviewed official journal of the Academy of Spinal Cord Injury Professionals (ASCIP), a U.S.-based multidisciplinary organization serving scientists, physicians, psychologists, nurses, therapists and social workers in the field of spinal cord injury care and research. JSCM, a member benefit of ASCIP, is published six times a year by Taylor & Francis Publishing. The editor-in-chief is Dr. Florian Thomas of Hackensack University Medical Center, Hackensack Meridian School of Medicine, Hackensack, NJ, USA.

About Kessler Foundation

Kessler Foundation, a major nonprofit organization in the field of disability, is a global leader in rehabilitation research. Our scientists seek to improve cognition, mobility, and long-term outcomes, including employment, for adults and children with neurological and developmental disabilities of the brain and spinal cord including traumatic brain injury, spinal cord injury, stroke, multiple sclerosis, and autism. Kessler Foundation also leads the nation in funding innovative programs that expand opportunities for employment for people with disabilities. We help people regain independence to lead full and productive lives. For more information, visit KesslerFoundation.org.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}