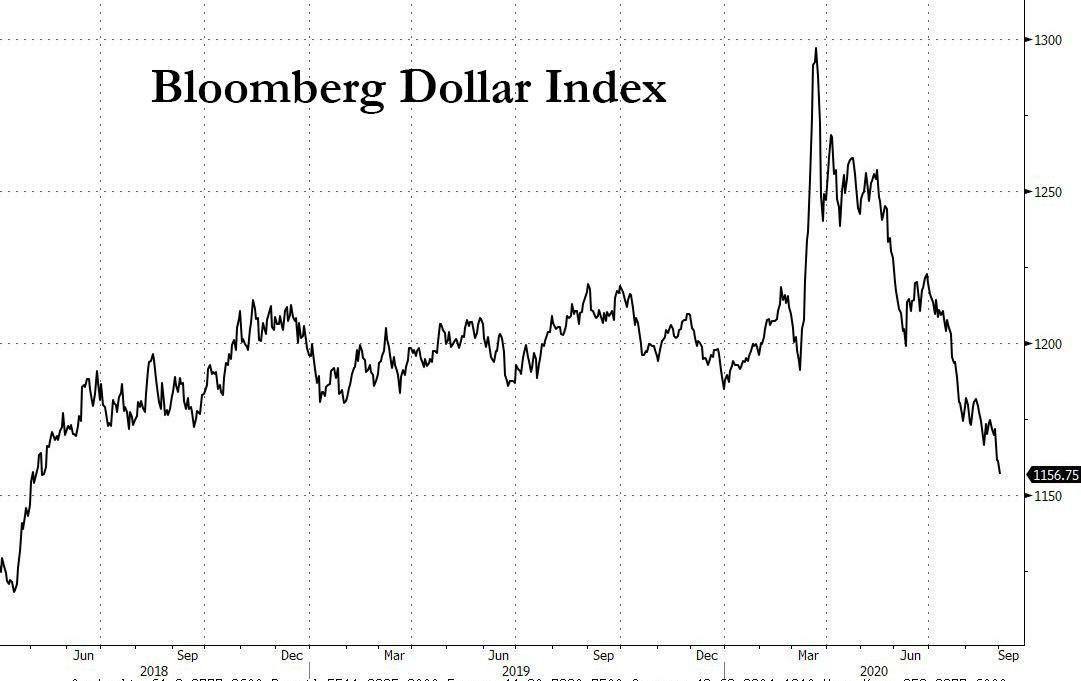

Futures Coiled Near All Time High As Dollar Tumbles To Fresh Two Year LowTyler DurdenTue, 09/01/2020 - 08:12

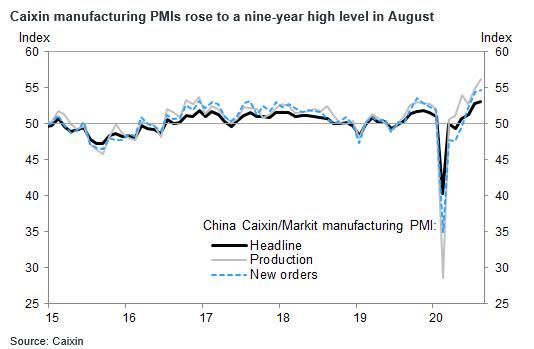

Stocks started September on a positive note on Tuesday, with S&P futures flat after fading earlier gains alongside shares in Europe as global indexes close to all-time highs as data in China and Europe showed manufacturing demand rebounding from coronavirus-induced lows. The dollar tumbled to a two-year low and the Yuan jumped after Chinese manufacturing data indicated that exports are underpinning a recovery.

The MSCI world equity index, which tracks shares in 49 countries, was close to recent highs, while the pan-European Stoxx 600 rose 0.3% in early trading with technology and basic resources climbing the most among sectors. France’s Cac 40 was up 0.2% and Germany’s Dax was up 0.7%. Britain’s FTSE 100 lagged, down 1.4%, hurt by a rising pound. Euro zone manufacturing activity grew last month, though factory managers remained wary about investing and hiring more workers. The French Mfg PMI beat expectations coming at 49.8, above the 49.0 consensus if down from 52.4, while Germany output grew at its fastest pace since February 2018, while in France it contracted.

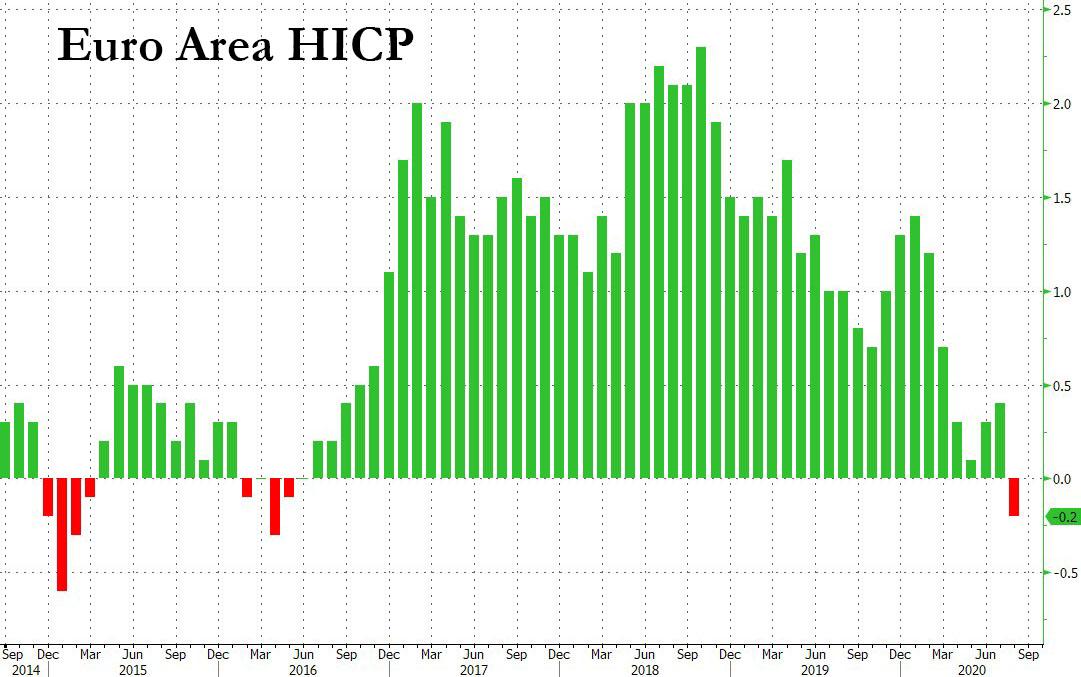

European stocks had opened even higher but pared gains after Germany cut its GDP forecast for 2021. Both shares and the euro, which rose to a two-year high of $1.19975 overnight in New York, were little changed after data showed annual euro zone inflation fell well below expectations in August, turning negative for the first time since May 2016, and a far cry from the European Central Bank’s inflation target of just under 2% (some have mused if the ECB will follow the Fed in announcing AIT as well).

“These numbers are clearly inconsistent with the ECB’s target,” said George Buckley, chief European economist at Nomura, who said the low reading will raise questions about whether the ECB should, like the Fed, adopt average inflation targeting. There were however credibility issues with such an approach, if the bank was unable to raise inflation to balance out the periods of lower inflation.

In Asia, China’s yuan touched the highest since 2019 and equities benchmarks in Hong Kong, Shanghai, Taipei and Seoul climbed. The Caixin PMI survey of China’s factory activity rose at the fastest pace in August since January 2011, helped by improving exports and continued domestic recovery, and boosted market sentiment overnight and into the European market open.

In rates, 10Y yields rose to 0.72% , up 2bps on the day with treasuries trading heavy led by the long end as month-end bid unwound. Yields were cheaper by up to 3bp at long end of the curve, steepening 2s10s, 5s30s by 1.6bp and 2.7bp; 10-year yields around 0.725%, cheaper by 1.8bp vs Monday’s close while gilts lag by ~1.5bp across the sector. Gilts underperformed, weighing on Treasuries along with a sharp selloff in Aussie bonds during Asia session. Core euro zone bond yields were up around 1 to 2 basis points, with the benchmark German 10-year yield at -0.387%.

In FX, the dollar continued to drop to a fresh two-year low and was down 0.4% at 91.826, dropping below 92 for the first time since May 2018 after a purchasing managers index for China beat estimates to raise optimism over Asia’s economic recovery.

"The weakness in the dollar is likely to continue and I suspect it will be substantially weaker from where it is against the euro by the end of the year," said Savvas Savouri, chief economist at Toscafund Asset Management. "We’ve got the Fed chairman clearly telling us he wants inflation to ratchet upwards, and the only reliable way to achieve this is through the channel of a weaker currency."

The euro climbed after German unemployment eased for a second month, though gains fell short of reaching $1.20 following the abovementioned deflationary print. At 1025 GMT, the single currency traded at $1.19835, up 0.4% since New York’s close as a dollar sell-off continued. Sterling rose to eight-month highs against the dollar, strengthening to as much as $1.3465 at 1028 GMT, and was up around 0.3% versus the euro.

In commodities, oil prices gained, reversing overnight losses. Brent climbed 56 cents to $45.84 a barrel while WTI futures rose 47 cents to $43.08 a barrel. Gold prices also rose, to their highest in two weeks.

Market Snapshot

S&P 500 futures up 0.3% to 3,510.75

STOXX Europe 600 up 0.2% to 367.28

MXAP up 0.4% to 173.35

MXAPJ up 0.5% to 574.03

Nikkei down 0.01% to 23,138.07

Topix down 0.2% to 1,615.81

Hang Seng Index up 0.03% to 25,184.85

Shanghai Composite up 0.4% to 3,410.61

Sensex up 0.8% to 38,948.09

Australia S&P/ASX 200 down 1.8% to 5,953.41

Kospi up 1% to 2,349.55

German 10Y yield rose 0.9 bps to -0.388%

Euro up 0.3% to $1.1971

Italian 10Y yield rose 5.0 bps to 0.968%

Spanish 10Y yield rose 0.8 bps to 0.417%

Brent futures up 1.2% to $45.82/bbl

Gold spot up 1.1% to $1,989.57

U.S. Dollar Index down 0.3% to 91.91

Top Overnight News from Bloomberg

A private gauge of China’s factory activity grew at the fastest rate in August since January 2011, helped by exports and domestic recovery

Global trade is expected to rebound faster than after the 2008 financial crisis, according to Germany’s Kiel Institute for the World Economy. The number of coronavirus cases approaches 25.5 million worldwide, while deaths surpass 850,000

The euro zone’s inflation rate went negative for the first time since 2016. Meanwhile Germany’s hit from the coronavirus will be less severe than feared, as the government’s efforts to kick start Europe’s largest economy show signs of bearing fruit

A closely-watched euro-area interbank borrowing rate fell to a record, dragged down by all the money sloshing around the economy

A quick look at global markets courtesy of NewsSquawk:

Asian equities traded cautiously as the region took its cue from the losses seen across most global counterparts despite Wall St. notching its biggest monthly gain since April and its best August performance in more than 3 decades, while participants also digested encouraging Chinese Caixin Manufacturing PMI data. ASX 200 (-1.8%) underperformed and briefly wiped out all of the prior month’s gains on a collapse below the 6,000 level with the downturn led by hefty losses in tech and energy, while the detention of a Chinese-Australian television anchor further highlighted the souring bilateral relations with China. Nikkei 225 (-0.1%) was indecisive but with downside stemmed by recent currency weakness and political continuity hopes with Chief Cabinet Secretary Suga said to be supported by the largest faction of the ruling LDP and is set to announce an intention to continue with Abenomics and the pandemic response when declaring his candidacy on Wednesday. Elsewhere, Hang Seng (U/C) and Shanghai Comp. (+0.4%) swung between gains and losses as mild support was seen following the strongest Caixin Manufacturing PMI reading since January 2011, but with upside also capped after the PBoC drained CNY 230bln from the interbank market and due to lingering US-China tensions after White House trade adviser Navarro stated the US will go after others not just TikTok and WeChat. Finally, 10yr JGBs were higher following the recent gains in T-notes and indecisive risk tone in the region, although some of the gains were reversed after all metrics pointed showed weaker results at the 10yr JGB auction.

Top Asian News

Total Enters Giant Korean Floating Wind Projects in Green Push

Samsung’s Heir Jay Y. Lee Indicted in Succession Probe

Supreme Court Approves 10-Year Rescue Plan for Indian Telcos

SoftBank Corp. Is ‘Surprise’ Addition to Japan’s Nikkei 225

Earlier gains across European equities have somewhat faded (Euro Stoxx 50 +0.4%) despite a lack of fresh macro catalysts, with the region now ultimately mixed, whilst losses in UK’s FTSE 100 (-1.3%) persist amid a catch-up play from its long weekend Bank holiday. Sectors performance is also varied with no clear risk profile to be derived: the IT sector outperforms as chip-makers cheer reports that Apple is aiming to launch four new iPhone models next month, with volumes in the 75mln region. Thus, the likes of STMicroelectronics (+1.1%), Dialog Semiconductor (+3.3%), Infineon (+1.2%) remain propped up. On the other side of the spectrum resides Travel & Leisure, alongside Banks and Oil & Gas. In terms of individual movers, Novartis (+3.0%) keeps the healthcare sector afloat on the back of a broker upgrade at Morgan Stanley coupled with an announcement that it has developed new ESG targets in order to ramp up access to medicines and achieve full carbon neutrality. Sticking with the healthcare sector, Sanofi (+0.6%) has largely brushed off its COVID-19 Kevzara vaccine failing to meet primary and key secondary endpoints in its Phase III trials. Meanwhile, AstraZeneca (-0.5%) succumbs to the weakness in the post-bank holiday UK markets but with downside somewhat cushioned by a positive update for its Farxiga, Imfinzi and COVID-19 vaccine deal with Canada. Elsewhere, Shell (-2.0%) and BP (-2.1%) are subdued despite higher oil prices, and with losses more pronounced that its cross-border counterparts amid catch-up play alongside reports UK Chancellor Sunak could increase fuel duty by 5p to help pay for the coronavirus in the Autumn budget.

Top European News

U.K. Manufacturing Output Expands at Fastest Pace in Six Years

European Factories Brace for Economic Rebound to Falter

Russia Passes 1 Million Covid-19 Cases as Epidemic Simmers

German Joblessness Falls Again Amid Revival of Economic Activity

In FX, the Dollar is suffering from a post-month end hangover as the DXY slips to a new 2020 low of 91.741 amidst broad losses vs G10 peers and most EM currencies. Confirmation of a firm US manufacturing PMI via the final release and ISM matching expectations for a pick-up in headline activity could conceivably provide the Greenback some respite, but the index remains toppy on rebounds over 92.000 as buoyant risk sentiment counters renewed bear-steepening along the Treasury curve.

NZD/CAD/GBP/EUR - The major beneficiaries of ongoing Buck weakness as the Kiwi pivots either side of 0.6750 awaiting NZ terms of trade for Q2 and the Loonie extends through the psychological 1.3000 level with some assistance from firm crude oil. Meanwhile, the Pound has scaled another big figure and briefly breached a mid-December 2019 peak (1.3422), as Eur/Gbp unwinds modest RHS demand for the August/September turn from circa 0.8950 towards 0.8900 irrespective of more negative sounding Brexit news (EU chief negotiator Barnier reportedly unwilling to discuss new UK fishing proposals unless Britain compromises on other contentious issues). Elsewhere, the Euro has tested round number resistance at 1.2000 vs the Dollar, but market contacts note heavy offers related to option expiries and on that note 1.1 bn rolling off between 1.1895-1.1900 at today’s NY cut may keep the headline pair supported given little net reaction to mixed Eurozone manufacturing PMIs and even weak, deflationary inflation.

JPY/AUD/CHF - Also firmer against the Greenback, albeit mildly as the Yen hovers midway within a 106.03-105.60 range, the Aussie fades after another 0.7400+ foray and Franc fails to breach 0.9000. For the record, the RBA stuck to the script overnight, though did extend and expand its Term Funding Facility, while July building approvals smashed estimates and the Q2 current account surplus was wider than forecast. However, relations with China are going from bad to worse as barley imports from Australia’s CBH Grain company are suspended.

SCANDI/EM - Not much response to rises in Swedish and Norwegian manufacturing PMIs, but China’s stronger than expected Caixin reading has helped the Yuan appreciate further vs the Dollar in contrast to a decline in the Turkish headline index that is weighing on the already lagging Try.

In commodities, WTI and Brent front month futures continue to ebb higher in early European trade, in what is a continuation of price action seen overnight as a function of the weakening Dollar, whilst the complex also remains underpinned by overall risk sentiment. Aside from that, pertinent news flow has been on the light side, although sources reported that UAE’s ADNOC pumped some 2.693mln BPD of crude in August in order to meet domestic demand – above its quota under the OPEC+ pact. That being said, sources added that the country will compensate for the undercompliance in the months ahead, whilst Iraq submitted a plan to OPEC that proposes additional cuts of 400k BPD in August and September and Kazakhstan plans additional cuts of 95k BPD over the same two-month period, according to sources. Further, Goldman Sachs raised 2020 Brent crude price forecast to USD 43.63/bbl from USD 40.51/bbl and raised 2021 forecast to USD 59.38/bbl from USD 55.63/bbl. WTI October holds its head above USD 43.00/bbl having found an overnight base around USD 42.75/bbl, whilst its Brent counterpart inches higher towards 46/bbl from a low of 45.47/bbl. Elsewhere, the weaker Buck keeps precious metals afloat with spot gold inching higher towards the USD 2000/oz mark (vs. low 1965/oz) whilst spot silver extends gains above USD 28.75/oz (vs. low 28.04/oz). Meanwhile, LME copper prices climbed to levels last seen over two years ago – bolstered by the Chinese Caixin Manufacturing beat coupled with the softer Dollar, whilst Dalian iron ore saw mild gains due to the same factors.

US Event Calendar

9:45am: Markit US Manufacturing PMI, est. 53.6, prior 53.6

10am: ISM Manufacturing, est. 54.8, prior 54.2

10am: Construction Spending MoM, est. 1.0%, prior -0.7%

Wards Total Vehicle Sales, est. 15m, prior 14.5m

DB's Jim Reid concludes the overnight wrap

Never has the restrictions of social distancing felt so liberating. As of today I can break the shackles of two weeks in quarantine. It’s been tedious, tiresome and ponderous. As least during full lockdown we went out for a nice walk once a day and I had heaps of work to occupy me. Of these past 14 days, 10 were spent on holiday at home (or weekends) and 4 at work in my home office. The latter were infinitely more enjoyable and less stressful for me. Much less for my wife. Every morning the twins repeatedly say “Go Mummy car”. They can’t work out why we don’t go out and are very confused. Hopefully they’ll squeal with delight when they realise their wish is finally going to come true.

So with a dull second half of August behind me we welcome in September today. To mark this we are launching our monthly survey this morning as a back to school special. This month’s includes plenty of questions about life around the virus including some questions on whether you will be first up volunteering to take any vaccine, whether you think they should be compulsory and how your understanding is on the effectiveness of vaccines generally. Also a number of other questions. It only takes 3 mins to fill in and results will come in the days ahead. Here is the link. All help filling in the survey very much appreciated.

This morning Henry is publishing the monthly performance review. It was another good month for risk especially for Silver (+15.39%) and the Nasdaq (+9.59%). It was also the best August for the S&P (+7.01%) since 1986 and the best individual month since April - just after the pandemic lows. See the full review in your inboxes soon for more.

Even with the good month, August ended with the S&P 500 slipping slightly, falling -0.16%, as even large gains in tech stocks were unable to keep the index in the green. Roughly 70% of the index was lower on the day after stocks dipped mid-session on reports of China blocking US companies from buying social media company TikTok. In a story that speaks to the power of retail investing in the current market, Apple and Tesla powered the Nasdaq +0.68% higher to another record after their pre-announced stock splits were enacted. The two stocks added +3.39% and +12.57% of value respectively by just lowering the sticker price.

In Europe with the UK markets closed, the Stoxx 600 fell -0.62% during the last session of August, reversing a gain of as much as +0.7% early in the session. This left the index up +2.86% on the month for its best August performance since 2009. Core sovereign bonds diverged much like equities with US 10yr Treasury yields down -1.6bps to finish at 0.705%, while 10yr Bund yields rose +1.2bps to -0.40%. The dollar resumed its slide as well (-0.25%), falling for the fifth session in a row.

Overnight Asian markets are a little directionless with the Nikkei (-0.07%) and Hang Seng (-0.02%) trading flat while the CSI (+0.12%) and Shanghai Comp (+0.04%) are posting modest advances. The Kospi (+1.06%) is leading the way on news that the government is preparing to boost its 2021 budget by 8.5%. In FX, all G-10 currencies are up (0.2-0.6%) against the greenback with the Euro trading closer to the 1.20 handle at 1.1992. Meanwhile the onshore Chinese yuan is up +0.42% to 6.8202, the highest level in over a year. Futures on the S&P 500 are up +0.11% while those on the Nasdaq are up +0.40%. Elsewhere, crude oil prices are trading up c.1% this morning while gold and silver are up +0.91% and +1.81% respectively.

It’s another round of global PMIs today and we’ve already kicked things off in Asia with China’s Caixin manufacturing PMI printing at 53.1 (vs. 52.5 expected and 52.8 last month), the highest reading since Jan 2011 and further emphasising the China recovery story. Yesterday, we saw China’s official August PMIs with manufacturing printing 0.2pts lower than expectations at 51.0 while services were at 55.2 (vs. 54.2 expected). Back to today and Japan’s final manufacturing PMI reading was confirmed at 47.2 (vs. 46.6 in flash). South Korea also showed an improvement at 48.5 (vs. 46.9 last month) while for Taiwan it was at 52.2 (vs. 50.6 last month), the highest reading in 2 years. However, readings for Vietnam (at 45.7 vs. 47.6 last month) and Australia (at 53.6 vs. 53.9 in flash and 54.0 last month) retreated on account of renewed lockdowns during the past month.

Following the policy framework changes laid out by Fed Chair Powell last week, yesterday Federal Reserve Vice Chair Clarida spoke to the possibility of using Treasury yield caps at some point, but suggested that it is not currently in the plans. He also noted that it is appropriate in many circumstances for inflation to overshoot the 2% goal. Markets also heard from the Fed's Bostic, who said that he was ‘very worried' about the drop in fiscal support for economy. Given that several participants argued for more accommodation in July, a lack of fiscal response and further gridlock may cause more committee members to opt for additional easing. With the next FOMC in two weeks this meeting will slowly come into the market’s view.

On the coronavirus, yesterday news came that Paris will now offer free testing at various locations throughout the city in order to identify and contain the spread of infections within the French capital. Cases in the country grew by 35,000 in the last week which is almost as many as seen at the country’s April peak, but there has not yet been a significant change in hospitalisations. The pace of new cases in the US continues to slow even as confirmed cases passed 6 million. Earlier this month New York City mayor said that indoor dining would be closed until June 2021, and then yesterday added that any resumption of indoor dining may hinge on a “huge step forward” such as a vaccine. With no guarantee of an effective or widely administered vaccine and colder months coming, this could lead to lower mobility and business output from the largest US city. Across the other side of world, India is now undoubtedly the global epicenter of the virus with the rise in new cases topping 70k on a daily basis. It also has the third highest fatalities now at 64,469. A reminder that we still publish our daily tables in the full pdf if you click on “view report”.

There was a good deal of attention on the US Presidential race this weekend after the conclusion of the Republican National Convention last Thursday night. We will see what kind of polling bounce President Trump receives, if any, by the end of the week as very few polls currently include the final, higher profile nights of the convention. In 2016, President Trump saw a nearly 5pt improvement in head-to-head polls against Secretary Clinton after the RNC. He even led her in polling averages for a small amount of time before seeing the bounce decline within a month. That said, Mr. Trump has seen his poll numbers vs Mr. Biden improve by nearly 2.8ps over the past 6 weeks. The RealClearPolitics polling average measures his nadir at 40pts in mid-summer. Mr. Trump is now back to the head-to-head polling range of 42-44pts he was sitting at following the first wave of outbreaks in the US. Overall RCP measures a +6.9pt spread for Mr. Biden (49.7%) over Mr. Trump (42.8%) but check in later this week to see how the RNC may change that.

Today we get final August manufacturing PMI’s from around the world, along with the ISM readings from the US, which will give us an indication of how the global economy has fared through the month as some economies opened up further and some became more restricted as viral patterns differed around the world. Note that the flash readings for the Euro Area saw a loss of momentum in the early part of August as its composite PMI fell from 54.9 to 51.6. Outside of the PMI’s, we will get July unemployment data out of the Euro Area, Italy and Japan, while seeing August unemployment change from Germany.

Back to this week’s calendar and later in the week the main highlights are the corresponding services and composite PMIs (Thursday) as well as the US jobs report on Friday. On payrolls, consensus on Bloomberg is currently expecting a further +1.518m increase in nonfarm payrolls last month, which would bring the total growth in nonfarm payrolls to 10.797m since April trough. However that would still be less than half of the 22.16m jobs lost in March and April. We have the day by day highlights for the rest of the week at the end.

To quickly recap last week for those on holiday yesterday, global equity markets continued to rise as the Federal Reserve’s new inflation targeting approach percolated through the financial system late in the week. The S&P 500 finished up +3.26% (+0.67% Friday) over the course of the week, having closed at record highs for 6 sessions in a row. The index has now risen 8 of the last 9 weeks since coronavirus cases rose quickly throughout the Southern and Western United States in June. The tech-focused Nasdaq rose +3.39% (+0.60% Friday) finishing at fresh highs as well and is now up over 30% YTD. In Europe, equities lagged behind their US counterparts, but the Stoxx 600 ended the week +1.02% (-0.52% Friday) higher.

Core sovereign bonds fell significantly on the week, before gaining on Friday with yields near their highest levels since June. The US yield curve steepened significantly following Fed Chair Powell’s statement on Thursday around the policy review and average inflation targeting. US 10yr Treasury yields rose +9.3bps (-3.1bps Friday) to finish at 0.721%, the highest weekly close since late March. Meanwhile 10yr Bund yields rose a similar +9.8bps (-0.2bps Friday) to -0.41% and 10yr Gilts rose +10.5bps (-2.5bps Friday) to 0.31%. The US 2y10y yield curve steepened +10.9bps to the highest levels since early June. In other markets, the dollar fell -0.94% on the week and is set to finish August lower for a fifth straight month.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}