Uncategorized

First Reliance Bancshares Reports Third Quarter 2022 Results

First Reliance Bancshares Reports Third Quarter 2022 Results

PR Newswire

FLORENCE, S.C., Nov. 1, 2022

FLORENCE, S.C., Nov. 1, 2022 /PRNewswire/ — First Reliance Bancshares, Inc. (OTC:FSRL), the holding company for First Reliance Bank (collectively…

Share this:

First Reliance Bancshares Reports Third Quarter 2022 Results

PR Newswire

FLORENCE, S.C., Nov. 1, 2022

FLORENCE, S.C., Nov. 1, 2022 /PRNewswire/ -- First Reliance Bancshares, Inc. (OTC:FSRL), the holding company for First Reliance Bank (collectively, "First Reliance" or the "Company"), today announced its financial results for the third quarter of 2022.

Third Quarter 2022 Highlights

- Net income for the third quarter of 2022 increased 95.8% to $2.5 million, or $0.31 per diluted share, compared to $1.3 million, or $0.16 per diluted share, for the third quarter of 2021.

- Return on average assets increased to 1.06% for September 30, 2022 compared to 0.45% at June 30, 2022 and 0.60% for the third quarter of 2021. Return on average equity increased to 15.60% for September 30, 2022 compared to 6.60% at June 30, 2022 and 7.29% for the third quarter of 2021.

- Net interest income for the quarter was $8.2 million, which represents an increase of $0.9 million, or 12.4%, on a linked quarter basis and an increase of $2.0 million, or 31.6% compared to the same period in 2021.

- Net interest margin expanded during the quarter to 3.71% at September 30, 2022 compared to 3.39% for the second quarter of 2022.

- In the third quarter, $4.9 million of the mortgage servicing right assets were sold for a net gain of $632 thousand.

- Total loans increased $8.7 million, or 5.4% annualized, to $646.6 million at September 30, 2022 from $638.0 million at June 30, 2022.

- Total deposits increased $9.4 million, or 4.5% annualized, to $840.4 million at September 30, 2022 from $831.0 million at June 30, 2022. This growth was primarily driven by noninterest-bearing deposits and transaction accounts.

- The Company had net charge-offs of $34 thousand, or annualized 0.02% of average loans during the quarter compared to net recoveries of $178 thousand, or annualized 0.12% of average loans, for the quarter ended June 30, 2022. Asset quality remains unchanged with nonperforming assets as a percentage of total assets of 0.06% at September 30, 2022 and June 30, 2022.

- Cost of funds for the third quarter of 2022 increased to 0.33% from 0.21% on a linked quarter basis and from 0.24% for the same period in 2021.

Rick Saunders, Chief Executive Officer, remarked: "We had another quarter of increased core bank profitability, highlighted by a 32 basis point expansion in Net Interest Margin and improving expense management. In the face of rising interest rates, we have benefited from the strong deposit franchise that our team has cultivated. As we continue to execute our growth strategies, we are committed to ensuring that we remain disciplined in our approach to credit underwriting and pricing."

Financial Summary | ||||||||

Three Months Ended | Nine Months Ended | |||||||

Sep 30 | Jun 30 | Mar 31 | Dec 31 | Sept 30 | Sep 30 | Sep 30 | ||

($ in thousands, except per share data) | 2022 | 2022 | 2022 | 2021 | 2021 | 2022 | 2021 | |

Earnings: | ||||||||

Net income available to common shareholders | $ 2,522 | $ 1,064 | $ 852 | $ 932 | $ 1,288 | $ 4,438 | $ 4,344 | |

Earnings per common share, diluted | 0.31 | 0.13 | 0.11 | 0.12 | 0.16 | 0.55 | 0.53 | |

Total revenue(1) | 11,103 | 9,404 | 9,097 | 9,253 | 9,570 | 29,604 | 29,655 | |

Net interest margin | 3.71 % | 3.39 % | 3.12 % | 3.10 % | 3.12 % | 3.41 % | 3.30 % | |

Return on average assets(2) | 1.06 % | 0.45 % | 0.37 % | 0.41 % | 0.60 % | 0.63 % | 0.72 % | |

Return on average equity(2) | 15.60 % | 6.60 % | 4.85 % | 5.28 % | 7.29 % | 8.91 % | 8.34 % | |

Efficiency ratio(3) | 69.40 % | 84.49 % | 87.50 % | 88.45 % | 83.83 % | 79.76 % | 80.98 % | |

As of | |||||

Sep 30 | Jun 30 | Mar 31 | Dec 31 | Sept 30 | |

(dollars in thousands) | 2022 | 2022 | 2022 | 2021 | 2021 |

Balance Sheet: | |||||

Total assets | $ 946,437 | $ 946,853 | $ 953,784 | $ 910,797 | $ 911,057 |

Total loans receivable | 646,634 | 637,953 | 592,089 | 586,446 | 564,738 |

Total deposits | 840,392 | 830,992 | 837,663 | 780,833 | 787,501 |

Total transaction deposits(4) to total deposits | 51.42 % | 51.14 % | 52.71 % | 50.19 % | 48.25 % |

Loans to deposits | 76.94 % | 76.77 % | 70.68 % | 75.11 % | 71.71 % |

Bank Capital Ratios: | |||||

Total risk-based capital ratio | 13.47 % | 12.97 % | 13.67 % | 14.07 % | 15.80 % |

Tier 1 risk-based capital ratio | 12.45 % | 11.98 % | 12.65 % | 13.03 % | 14.64 % |

Tier 1 leverage ratio | 9.84 % | 9.66 % | 9.67 % | 9.66 % | 10.24 % |

Common equity tier 1 capital ratio | 12.45 % | 11.98 % | 12.65 % | 13.03 % | 14.64 % |

Asset Quality Ratios: | |||||

Nonperforming assets as a percentage of | 0.06 % | 0.06 % | 0.11 % | 0.10 % | 0.15 % |

Allowance for loan losses as a percentage of | 1.18 % | 1.17 % | 1.22 % | 1.20 % | 1.23 % |

Footnotes to table located at the end of this release. | |||||

CONDENSED CONSOLIDATED INCOME STATEMENTS – Unaudited | ||||||||

Three Months Ended | Nine Months Ended | |||||||

Sep 30 | Jun 30 | Mar 31 | Dec 31 | Sept 30 | Sep 30 | |||

($ in thousands, except per share data) | 2022 | 2022 | 2022 | 2021 | 2021 | 2022 | 2021 | |

Interest income | ||||||||

Loans | $ 7,555 | $ 6,781 | $ 6,380 | $ 6,663 | $ 6,382 | $ 20,716 | $ 18,623 | |

Investment securities | 1,097 | 840 | 571 | 359 | 294 | 2,508 | 844 | |

Other interest income | 321 | 176 | 73 | 79 | 58 | 570 | 155 | |

Total interest income | 8,973 | 7,797 | 7,024 | 7,101 | 6,734 | 23,794 | 19,622 | |

Interest expense | ||||||||

Deposits | 446 | 212 | 197 | 224 | 257 | 855 | 798 | |

Other interest expense | 283 | 252 | 252 | 256 | 213 | 787 | 740 | |

Total interest expense | 729 | 464 | 449 | 480 | 470 | 1,642 | 1,538 | |

Net interest income | 8,244 | 7,333 | 6,575 | 6,621 | 6,264 | 22,152 | 18,084 | |

Provision for loan losses | 170 | 110 | 85 | 95 | 100 | 365 | 208 | |

Net interest income after provision for loan | 8,074 | 7,223 | 6,490 | 6,526 | 6,164 | 21,787 | 17,876 | |

Noninterest income | ||||||||

Mortgage banking income | 1,721 | 897 | 1,420 | 1,407 | 2,151 | 4,038 | 8,124 | |

Service fees on deposit accounts | 343 | 357 | 362 | 356 | 315 | 1,062 | 865 | |

Debit card and other service charges, | 536 | 559 | 498 | 543 | 532 | 1,593 | 1,495 | |

Income from bank owned life insurance | 91 | 89 | 88 | 93 | 94 | 268 | 281 | |

Gain on sale of securities, net | - | - | - | - | 42 | - | 81 | |

Gain on sale of loans | - | - | - | - | - | - | 326 | |

(Loss) Gain on disposal of fixed assets | (10) | - | 10 | 69 | - | (1) | - | |

Other income | 178 | 168 | 144 | 164 | 172 | 492 | 399 | |

Total noninterest income | 2,859 | 2,070 | 2,522 | 2,632 | 3,306 | 7,452 | 11,571 | |

Noninterest expense | ||||||||

Compensation and benefits | 4,505 | 5,059 | 5,079 | 4,965 | 5,268 | 14,642 | 15,777 | |

Occupancy and equipment | 923 | 890 | 893 | 862 | 784 | 2,707 | 2,359 | |

Data processing, technology, and communications | 846 | 789 | 837 | 920 | 852 | 2,473 | 2,634 | |

Professional fees | 185 | 180 | 180 | 202 | 234 | 544 | 715 | |

Marketing | 206 | 184 | 74 | 150 | 113 | 464 | 270 | |

Other | 1,040 | 843 | 897 | 1,085 | 772 | 2,781 | 2,259 | |

Total noninterest expense | 7,705 | 7,945 | 7,960 | 8,184 | 8,023 | 23,611 | 24,014 | |

Income before provision for income taxes | 3,228 | 1,348 | 1,052 | 974 | 1,447 | 5,628 | 5,433 | |

Income tax expense | 706 | 284 | 200 | 42 | 159 | 1,190 | 1,089 | |

Net income available to common shareholders | $ 2,522 | $ 1,064 | $ 852 | $ 932 | $ 1,288 | $ 4,438 | $ 4,344 | |

Weighted average common shares - basic | 7,777 | 7,782 | 7,784 | 7,785 | 7,750 | 7,781 | 7,737 | |

Weighted average common shares - diluted | 8,073 | 8,094 | 8,100 | 8,096 | 8,084 | 8,088 | 8,160 | |

Basic income per common share | $ 0.32 | $ 0.14 | $ 0.11 | $ 0.12 | $ 0.17 | $ 0.57 | $ 0.56 | |

Diluted income per common share | $ 0.31 | $ 0.13 | $ 0.11 | $ 0.12 | $ 0.16 | $ 0.55 | $ 0.53 | |

Net income for the three months ended September 30, 2022 was $2.5 million, or $0.31 per diluted common share, compared to $1.3 million, or $0.16 per diluted common share, for the three months ended September 30, 2021. Net income for the nine months ended September 30, 2022 totaled $4.4 million, or $0.55 per diluted common share, compared to $4.3 million, or $0.53 per diluted common share for the nine months ended September 30, 2021.

Noninterest income for the three months ended September 30, 2022 was $2.9 million, a decrease of $0.4 million from $3.3 million for the same period in 2021. Noninterest income is largely driven by the Company's mortgage banking division, which produced net revenue of $1.7 million during the three months ended September 30, 2022. During the third quarter, the Company sold mortgage servicing rights related to approximately $503.8 million of underlying mortgages for a $0.6 million net gain on sale mortgage servicing rights. Additionally, mortgage sales volume decreased $67.4 million to $56.6 million compared to third quarter 2021 due to the effect of rising mortgage rates.

Noninterest expense for the three months ended September 30, 2022 was $7.7 million, a decrease of $0.3 million from $8.0 million for the same period in 2021. This decrease was primarily driven by a decrease in core bank and mortgage compensation and benefits somewhat offset by an increase in other noninterest expense compared to third quarter 2021.

NET INTEREST INCOME AND MARGIN – Unaudited | |||||||

For the Three Months Ended | |||||||

September 30, 2022 | September 30, 2021 | ||||||

Average | Income/ | Yield/ | Average | Income/ | Yield/ | ||

(dollars in thousands) | Balance | Expense | Rate | Balance | Expense | Rate | |

Assets | |||||||

Interest-earning assets | |||||||

Federal funds sold and interest-bearing deposits | $ 66,503 | $ 317 | 1.89 % | $ 159,307 | $ 51 | 0.13 % | |

Investment securities | 163,843 | 1,097 | 2.66 % | 55,049 | 294 | 2.12 % | |

Nonmarketable equity securities | 522 | 4 | 3.61 % | 837 | 7 | 3.38 % | |

Loans held for sale | 10,073 | 152 | 5.98 % | 32,181 | 244 | 3.01 % | |

Loans | 639,929 | 7,403 | 4.59 % | 548,028 | 6,138 | 4.44 % | |

Total interest-earning assets | 880,870 | 8,973 | 4.04 % | 795,402 | 6,734 | 3.36 % | |

Allowance for loan losses | (7,570) | (6,764) | |||||

Noninterest-earning assets | 81,448 | 75,650 | |||||

Total assets | $ 954,748 | $ 864,288 | |||||

Liabilities and Shareholders' Equity | |||||||

Interest-bearing liabilities | |||||||

NOW accounts | $ 152,444 | $ 29 | 0.08 % | $ 133,577 | $ 16 | 0.05 % | |

Savings & money market | 304,629 | 321 | 0.42 % | 246,212 | 101 | 0.16 % | |

Time deposits | 108,258 | 95 | 0.35 % | 132,972 | 140 | 0.42 % | |

Total interest-bearing deposits | 565,331 | 445 | 0.31 % | 512,761 | 257 | 0.20 % | |

FHLB advances and other borrowings | 11,264 | 5 | 0.16 % | 19,839 | 48 | 0.96 % | |

Subordinated debentures | 25,679 | 279 | 4.31 % | 18,144 | 165 | 3.61 % | |

Total interest-bearing liabilities | 602,274 | 729 | 0.48 % | 550,744 | 470 | 0.34 % | |

Noninterest bearing deposits | 274,832 | 231,993 | |||||

Other liabilities | 12,967 | 10,903 | |||||

Shareholders' equity | 64,675 | 70,648 | |||||

Total liabilities and shareholders' equity | $ 954,748 | $ 864,288 | |||||

Net interest income (tax equivalent) / interest | $ 8,244 | 3.56 % | $ 6,264 | 3.02 % | |||

Net Interest Margin | 3.71 % | 3.12 % | |||||

For the Nine Months Ended | |||||||

September 30, 2022 | September 30, 2021 | ||||||

Average | Income/ | Yield/ | Average | Income/ | Yield/ | ||

(dollars in thousands) | Balance | Expense | Rate | Balance | Expense | Rate | |

Assets | |||||||

Interest-earning assets | |||||||

Federal funds sold and interest-bearing deposits | $ 97,344 | $ 552 | 0.76 % | $ 128,926 | $ 109 | 0.11 % | |

Investment securities | 141,479 | 2,508 | 2.37 % | 50,139 | 844 | 2.25 % | |

Nonmarketable equity securities | 552 | 17 | 4.16 % | 909 | 46 | 6.75 % | |

Loans held for sale | 17,402 | 564 | 4.33 % | 34,653 | 740 | 2.85 % | |

Loans | 611,679 | 20,153 | 4.40 % | 517,512 | 17,883 | 4.62 % | |

Total interest-earning assets | 868,456 | 23,794 | 3.66 % | 732,139 | 19,622 | 3.58 % | |

Allowance for loan losses | (7,331) | (6,478) | |||||

Noninterest-earning assets | 80,919 | 74,404 | |||||

Total assets | $ 942,044 | $ 800,065 | |||||

Liabilities and Shareholders' Equity | |||||||

Interest-bearing liabilities | |||||||

NOW accounts | $ 161,932 | $ 69 | 0.06 % | $ 129,834 | $ 45 | 0.05 % | |

Savings & money market | 288,708 | 507 | 0.23 % | 210,738 | 263 | 0.17 % | |

Time deposits | 113,460 | 280 | 0.33 % | 136,221 | 490 | 0.48 % | |

Total interest-bearing deposits | 564,100 | 856 | 0.20 % | 476,793 | 798 | 0.22 % | |

FHLB advances and other borrowings | 13,044 | 34 | 0.35 % | 17,665 | 141 | 1.06 % | |

Subordinated debentures | 25,671 | 752 | 3.92 % | 19,901 | 599 | 4.03 % | |

Total interest-bearing liabilities | 602,815 | 1,642 | 0.36 % | 514,359 | 1,538 | 0.40 % | |

Noninterest bearing deposits | 260,426 | 205,531 | |||||

Other liabilities | 12,376 | 10,695 | |||||

Shareholders' equity | 66,427 | 69,480 | |||||

Total liabilities and shareholders' equity | $ 942,044 | $ 800,065 | |||||

Net interest income (tax equivalent) / interest | $ 22,152 | 3.30 % | $ 18,084 | 3.18 % | |||

Net Interest Margin | 3.41 % | 3.30 % | |||||

Net interest income for the three months ended September 30, 2022 was $8.2 million compared to $6.3 million for the three months ended September 30, 2021. This increase was primarily driven by an increase in interest-earning assets, as well as an increase in interest rates. Yield on interest-earning assets increased to 4.04% for the three months ended September 30, 2022 from 3.36% for the same period in 2021. The company expects deposit betas to increase beginning in the fourth quarter of 2022 from historically low levels thus far in the rate tightening cycle which should be at least partially offset by continued increases in interest earning asset yields.

Net interest income was $22.2 million for the nine months ended September 30, 2022, an increase of $4.1 million over the same period in 2021. Increases in average loans and investments contributed to a majority of the increase in interest income as well as a reduction in yield on interest bearing liabilities.

CONDENSED CONSOLIDATED BALANCE SHEETS – Unaudited | |||||

As of | |||||

Sept 30 | June 30 | Mar 31 | Dec 31 | Sept 30 | |

(dollars in thousands) | 2022 | 2022 | 2022 | 2021 | 2021 |

Assets | |||||

Cash and cash equivalents: | |||||

Cash and due from banks | $ 4,147 | $ 7,702 | $ 4,672 | $ 5,299 | $ 4,930 |

Interest-bearing deposits with banks | 60,537 | 45,683 | 116,192 | 144,825 | 184,739 |

Total cash and cash equivalents | 64,684 | 53,385 | 120,864 | 150,124 | 189,669 |

Time deposits in other banks | 257 | 257 | 257 | 257 | |

Investment securities: | |||||

Investment securities available for sale | 160,504 | 164,440 | 144,422 | 81,917 | 58,470 |

Other investments | 917 | 657 | 521 | 837 | 837 |

Total investment securities | 161,421 | 165,097 | 144,943 | 82,754 | 59,307 |

Mortgage loans held for sale | 4,599 | 19,648 | 23,528 | 23,844 | 33,667 |

Loans receivable: | |||||

Loans | 646,634 | 637,953 | 592,089 | 586,446 | 564,738 |

Less allowance for loan losses | (7,630) | (7,494) | (7,206) | (7,040) | (6,934) |

Loans receivable, net | 639,004 | 630,459 | 584,883 | 579,406 | 557,804 |

Property and equipment, net | 22,868 | 23,100 | 23,222 | 22,805 | 22,364 |

Mortgage servicing rights | 10,182 | 14,893 | 14,536 | 14,057 | 13,785 |

Bank owned life insurance | 18,744 | 18,653 | 18,564 | 18,476 | 18,383 |

Deferred income taxes | 8,629 | 7,376 | 5,862 | 4,128 | 2,798 |

Other assets | 16,306 | 13,985 | 17,125 | 14,946 | 13,023 |

Total assets | 946,437 | 946,853 | 953,784 | 910,797 | 911,057 |

Liabilities | |||||

Deposits | $ 840,392 | $ 830,992 | $ 837,663 | $ 780,833 | $ 787,501 |

Federal Home Loan Bank advances | - | - | - | 10,000 | 10,000 |

Federal funds and repurchase agreements | 3,726 | 13,805 | 11,886 | 11,372 | 6,353 |

Subordinated debentures | 15,373 | 15,365 | 15,357 | 15,349 | 15,498 |

Junior subordinated debentures | 10,310 | 10,310 | 10,310 | 10,310 | 10,310 |

Other liabilities | 14,472 | 12,412 | 11,937 | 12,131 | 10,983 |

Total liabilities | 884,273 | 882,884 | 887,153 | 839,995 | 840,645 |

Shareholders' equity | |||||

Preferred stock - Series D non-cumulative, no par | 1 | 1 | 1 | 1 | 1 |

Common Stock - $.01 par value; 20,000,000 shares | 88 | 88 | 88 | 88 | 88 |

Treasury stock, at cost | (4,364) | (4,333) | (4,419) | (4,323) | (4,281) |

Nonvested restricted stock | (2,291) | (2,500) | (2,572) | (2,668) | (2,737) |

Additional paid-in capital | 54,013 | 54,088 | 53,980 | 53,856 | 53,765 |

Retained earnings | 28,423 | 25,901 | 24,837 | 23,985 | 23,053 |

Accumulated other comprehensive income (loss) | (13,706) | (9,276) | (5,284) | (137) | 523 |

Total shareholders' equity | 62,164 | 63,969 | 66,631 | 70,802 | 70,412 |

Total liabilities and shareholders' equity | $ 946,437 | $ 946,853 | $ 953,784 | $ 910,797 | $ 911,057 |

COMMON STOCK SUMMARY - Unaudited | |||||

As of | |||||

30-Sep | June 30 | Mar 31 | Dec 31 | Sept 30 | |

(shares in thousands) | 2022 | 2022 | 2022 | 2021 | 2021 |

Voting common shares outstanding | 8,793 | 8,801 | 8,782 | 8,793 | 8,784 |

Treasury shares outstanding | (575) | (571) | (545) | (535) | (530) |

Total common shares outstanding | 8,218 | 8,230 | 8,237 | 8,258 | 8,254 |

Tangible book value per common share(5) | $ 7.46 | $ 7.66 | $ 7.98 | $ 8.46 | $ 8.41 |

Stock price: | |||||

High | $ 10.20 | $ 10.20 | $ 10.20 | $ 10.74 | $ 10.50 |

Low | $ 9.00 | $ 9.25 | $ 9.75 | $ 9.95 | $ 9.80 |

Period end | $ 9.14 | $ 9.25 | $ 9.85 | $ 10.20 | $ 10.30 |

ASSET QUALITY MEASURES – Unaudited | |||||

As of | |||||

Sept 30 | June 30 | Mar 31 | Dec 31 | Sept 30 | |

(dollars in thousands) | 2022 | 2022 | 2022 | 2021 | 2021 |

Nonperforming Assets | |||||

Commercial | |||||

Owner occupied RE | $ 135 | $ 140 | $ 144 | $ 152 | $ 526 |

Non-owner occupied RE | - | - | 295 | - | - |

Construction | - | - | - | - | - |

Commercial business | 146 | 81 | - | - | - |

Consumer | |||||

Real estate | 2 | 3 | 343 | 341 | 346 |

Home equity | - | - | - | - | - |

Construction | - | - | - | - | - |

Other | 130 | 160 | 104 | 84 | 121 |

Nonaccruing troubled debt restructurings | 160 | 173 | 190 | 205 | 220 |

Total nonaccrual loans | $ 573 | $ 557 | $ 1,076 | $ 782 | $ 1,213 |

Other real estate owned | - | - | - | 135 | 150 |

Total nonperforming assets | $ 573 | $ 557 | $ 1,076 | $ 917 | $ 1,363 |

Nonperforming assets as a percentage of: | |||||

Total assets | 0.06 % | 0.06 % | 0.11 % | 0.10 % | 0.15 % |

Total loans receivable | 0.09 % | 0.09 % | 0.18 % | 0.16 % | 0.24 % |

Accruing troubled debt restructurings | $ 1,312 | $ 1,349 | $ 1,393 | $ 1,405 | $ 1,444 |

Three Months Ended | |||||

Sept 30 | June 30 | Mar 31 | Dec 31 | Sept 30 | |

(dollars in thousands) | 2022 | 2022 | 2022 | 2021 | 2021 |

Allowance for Loan Losses | |||||

Balance, beginning of period | $ 7,494 | $ 7,206 | $ 7,040 | $ 6,934 | $ 6,323 |

Loans charged-off | 76 | 11 | 19 | 5 | 72 |

Recoveries of loans previously charged-off | 42 | 189 | 100 | 16 | 583 |

Net charge-offs (recoveries) | 34 | (178) | (81) | (11) | (511) |

Provision for loan losses | 170 | 110 | 85 | 95 | 100 |

Balance, end of period | $ 7,630 | $ 7,494 | $ 7,206 | $ 7,040 | $ 6,934 |

Allowance for loan losses to gross loans receivable | 1.18 % | 1.17 % | 1.22 % | 1.20 % | 1.23 % |

Allowance for loan losses to nonaccrual loans | 1331.59 % | 1345.42 % | 669.70 % | 900.26 % | 571.64 % |

Footnotes to table located at the end of this release. | |||||

Our asset quality remained strong through September 30, 2022, with nonperforming assets remaining at $0.6 million, which represents 0.06% of total assets. The allowance for loan losses as a percentage of total loans receivable increased slightly to 1.18% at September 30, 2022, compared to 1.17% at June 30, 2022. The Company had net charge-offs of $34 thousand for the three months ended September 30, 2022 compared to net recoveries of $0.5 million for the same period in 2021.

LOAN COMPOSITION – Unaudited | |||||

As of | |||||

Sept 30 | June 30 | Mar 31 | Dec 31 | Sept 30 | |

(dollars in thousands) | 2022 | 2022 | 2022 | 2021 | 2021 |

Commercial real estate | $ 378,589 | $ 368,316 | $ 334,508 | $ 333,060 | $ 318,849 |

Consumer real estate | 147,110 | 142,711 | 123,908 | 120,079 | 107,651 |

Commercial and industrial | 67,200 | 67,239 | 66,285 | 60,687 | 61,778 |

Consumer and other | 53,735 | 59,687 | 67,388 | 72,620 | 76,460 |

Total loans, net of deferred fees | 646,634 | 637,953 | 592,089 | 586,446 | 564,738 |

Less allowance for loan losses | 7,630 | 7,494 | 7,206 | 7,040 | 6,934 |

Total loans, net | $ 639,004 | $ 630,459 | $ 584,883 | $ 579,406 | $ 557,804 |

DEPOSIT COMPOSITION – Unaudited | |||||

As of | |||||

Sept 30 | June 30 | Mar 31 | Dec 31 | Sept 30 | |

(dollars in thousands) | 2022 | 2022 | 2022 | 2021 | 2021 |

Noninterest-bearing | $ 277,587 | $ 265,049 | $ 273,118 | $ 238,019 | $ 246,534 |

Interest-bearing: | |||||

DDA and NOW accounts | 154,550 | 159,939 | 168,401 | 153,889 | 133,474 |

Money market accounts | 232,711 | 230,840 | 217,812 | 204,432 | 216,243 |

Savings | 71,929 | 66,727 | 61,246 | 58,566 | 59,941 |

Time, less than $250,000 | 76,530 | 78,735 | 84,874 | 99,059 | 103,126 |

Time, $250,000 and over | 27,085 | 29,702 | 32,212 | 26,868 | 28,183 |

Total deposits | $ 840,392 | $ 830,992 | $ 837,663 | $ 780,833 | $ 787,501 |

Footnotes to tables: | |

(1) | Total revenue is the sum of net interest income and noninterest income. |

(2) | Annualized for the respective period. |

(3) | Noninterest expense divided by the sum of net interest income and noninterest income. |

(4) | Includes noninterest-bearing and interest-bearing DDA and NOW accounts. |

(5) | The tangible book value per share is calculated as total shareholders' equity less intangible assets, divided by period-end outstanding common shares. |

ABOUT FIRST RELIANCE

Founded in 1999, First Reliance Bancshares, Inc. (OTC: FSRL.OB), is based in Florence, South Carolina and has assets of approximately $946 million. The company employs more than 175 professionals and has locations throughout South Carolina and central North Carolina. First Reliance has redefined community banking with a commitment to making customers' lives better, its founding principle. Customers of the company have given it a 93% customer satisfaction rating well above the bank industry average of 81%. First Reliance is also one of two companies throughout South Carolina to receive the Best Places to Work in South Carolina award all 17 years since the program began. We believe that this recognition confirms that our associates are engaged and committed to our brand and the communities we serve. In addition to offering a full range of personalized community banking products and services for individuals, small businesses and corporations, First Reliance offers two unique community-customers programs, which include: Hometown Heroes, a package of benefits for those serving our communities and Check N Save, an outreach program for the unbanked or under-banked. The company also offers a full suite of digital banking services, Treasury Services, a Customer Service Guaranty, a Mortgage Service Guaranty, and First Reliance Wealth Strategies.

FORWARD-LOOKING STATEMENTS

Certain statements in this news release contain "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995, such as statements relating to future plans and expectations, and are thus prospective. Such forward-looking statements include, but are not limited to, statements with respect to our plans, objectives, expectations and intentions and other statements that are not historical facts, and other statements identified by words such as "believes," "expects," "anticipates," "estimates," "intends," "plans," "targets," and "projects," as well as similar expressions. Such statements are subject to risks, uncertainties, and other factors which could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. Although we believe that the assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove to be inaccurate. Therefore, we can give no assurance that the results contemplated in the forward-looking statements will be realized. The inclusion of this forward-looking information should not be construed as a representation by the Company or any person that the future events, plans, or expectations contemplated by the Company will be achieved.

The following factors, among others, could cause actual results to differ materially from the anticipated results or other expectations expressed in the forward-looking statements: (1) competitive pressures among depository and other financial institutions may increase significantly and have an effect on pricing, spending, third-party relationships and revenues; (2) the strength of the United States economy in general and the strength of the local economies in which we conduct operations may be different than expected resulting in, among other things, a deterioration in the credit quality or a reduced demand for credit, including the resultant effect on the Company's loan portfolio and allowance for loan losses; (3) the rate of delinquencies and amounts of charge-offs, the level of allowance for loan loss, the rates of loan growth, or adverse changes in asset quality in our loan portfolio, which may result in increased credit risk-related losses and expenses; (4) the risk that the preliminary financial information reported herein and our current preliminary analysis will be different when our review is finalized; (5) changes in the U.S. legal and regulatory framework including, but not limited to, the Dodd-Frank Act and regulations adopted thereunder; (6) adverse conditions in the stock market, the public debt market and other capital markets (including changes in interest rate conditions) could have a negative impact on the Company, including the value of its MSR asset; (7) the business related to acquisitions may not be integrated successfully or such integration may take longer to accomplish than expected; (8) the expected cost savings and any revenue synergies from acquisitions may not be fully realized within expected timeframes; and (9) disruption from acquisitions may make it more difficult to maintain relationships with clients, associates or suppliers. Moreover, a trade war or other governmental action related to tariffs or international trade agreements or policies, as well as Covid-19 or other potential epidemics or pandemics, have the potential to negatively impact ours and/or our customers' costs, demand for our customers' products, and/or the U.S. economy or certain sectors thereof and, thus, adversely affect our business, financial condition, and results of operations. All subsequent written and oral forward-looking statements concerning the Company or any person acting on its behalf are expressly qualified in their entirety by the cautionary statements above. We do not undertake any obligation to update any forward-looking statement to reflect circumstances or events that occur after the date the forward-looking statements are made.

Contact:

Robert Haile

SEVP & Chief Financial Officer

(843) 656-5000

rhaile@firstreliance.com

View original content to download multimedia:https://www.prnewswire.com/news-releases/first-reliance-bancshares-reports-third-quarter-2022-results-301665287.html

SOURCE First Reliance Bancshares

Uncategorized

Q4 Update: Delinquencies, Foreclosures and REO

Today, in the Calculated Risk Real Estate Newsletter: Q4 Update: Delinquencies, Foreclosures and REO

A brief excerpt: I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened followi…

Share this:

A brief excerpt:

I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble). The two key reasons are mortgage lending has been solid, and most homeowners have substantial equity in their homes..There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ mortgage rates real estate mortgages pandemic interest rates

...

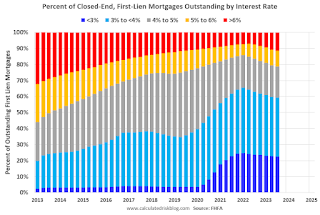

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023 (Q4 2023 data will be released in a two weeks).

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 22.6% of loans are under 3%, 59.4% are under 4%, and 78.7% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

Uncategorized

‘Bougie Broke’ – The Financial Reality Behind The Facade

‘Bougie Broke’ – The Financial Reality Behind The Facade

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Social media users claiming…

Share this:

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive restaurants. Yet they complain about living paycheck to paycheck and lacking the means to support their lifestyle.

Bougie broke is like “keeping up with the Joneses,” spending beyond one’s means to impress others.

Bougie Broke gives us a glimpse into the financial condition of a growing number of consumers. Since personal consumption represents about two-thirds of economic activity, it’s worth diving into the Bougie Broke fad to appreciate if a large subset of the population can continue to consume at current rates.

The Wealth Divide Disclaimer

Forecasting personal consumption is always tricky, but it has become even more challenging in the post-pandemic era. To appreciate why we share a joke told by Mike Green.

Bill Gates and I walk into the bar…

Bartender: “Wow… a couple of billionaires on average!”

Bill Gates, Jeff Bezos, Elon Musk, Mark Zuckerberg, and other billionaires make us all much richer, on average. Unfortunately, we can’t use the average to pay our bills.

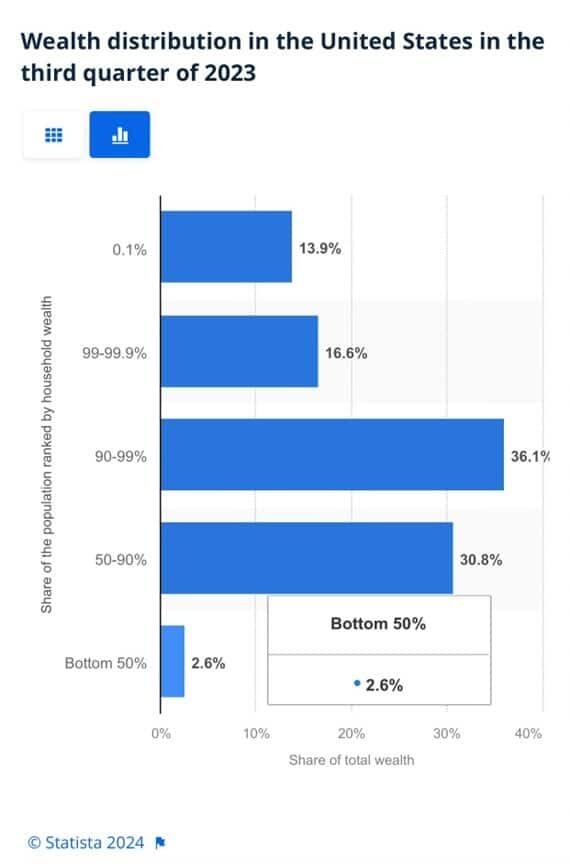

According to Wikipedia, Bill Gates is one of 756 billionaires living in the United States. Many of these billionaires became much wealthier due to the pandemic as their investment fortunes proliferated.

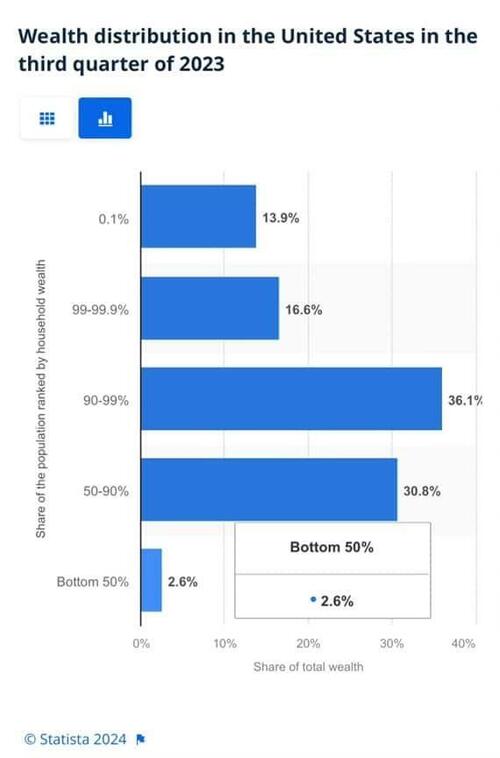

To appreciate the wealth divide, consider the graph below courtesy of Statista. 1% of the U.S. population holds 30% of the wealth. The wealthiest 10% of households have two-thirds of the wealth. The bottom half of the population accounts for less than 3% of the wealth.

The uber-wealthy grossly distorts consumption and savings data. And, with the sharp increase in their wealth over the past few years, the consumption and savings data are more distorted.

Furthermore, and critical to appreciate, the spending by the wealthy doesn’t fluctuate with the economy. Therefore, the spending of the lower wealth classes drives marginal changes in consumption. As such, the condition of the not-so-wealthy is most important for forecasting changes in consumption.

Revenge Spending

Deciphering personal data has also become more difficult because our spending habits have changed due to the pandemic.

A great example is revenge spending. Per the New York Times:

Ola Majekodunmi, the founder of All Things Money, a finance site for young adults, explained revenge spending as expenditures meant to make up for “lost time” after an event like the pandemic.

So, between the growing wealth divide and irregular spending habits, let’s quantify personal savings, debt usage, and real wages to appreciate better if Bougie Broke is a mass movement or a silly meme.

The Means To Consume

Savings, debt, and wages are the three primary sources that give consumers the ability to consume.

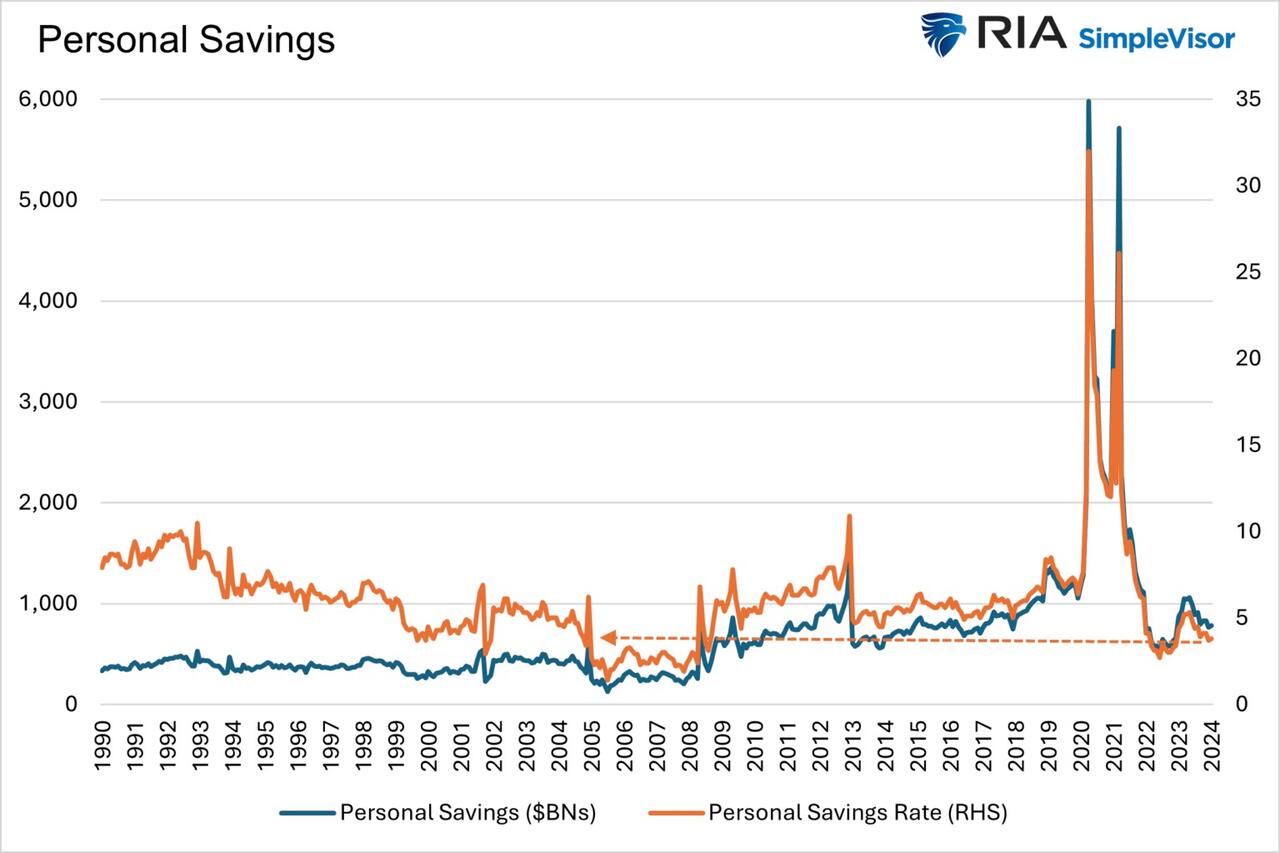

Savings

The graph below shows the rollercoaster on which personal savings have been since the pandemic. The savings rate is hovering at the lowest rate since those seen before the 2008 recession. The total amount of personal savings is back to 2017 levels. But, on an inflation-adjusted basis, it’s at 10-year lows. On average, most consumers are drawing down their savings or less. Given that wages are increasing and unemployment is historically low, they must be consuming more.

Now, strip out the savings of the uber-wealthy, and it’s probable that the amount of personal savings for much of the population is negligible. A survey by Payroll.org estimates that 78% of Americans live paycheck to paycheck.

More on Insufficient Savings

The Fed’s latest, albeit old, Report on the Economic Well-Being of U.S. Households from June 2023 claims that over a third of households do not have enough savings to cover an unexpected $400 expense. We venture to guess that number has grown since then. To wit, the number of households with essentially no savings rose 5% from their prior report a year earlier.

Relatively small, unexpected expenses, such as a car repair or a modest medical bill, can be a hardship for many families. When faced with a hypothetical expense of $400, 63 percent of all adults in 2022 said they would have covered it exclusively using cash, savings, or a credit card paid off at the next statement (referred to, altogether, as “cash or its equivalent”). The remainder said they would have paid by borrowing or selling something or said they would not have been able to cover the expense.

Debt

After periods where consumers drained their existing savings and/or devoted less of their paychecks to savings, they either slowed their consumption patterns or borrowed to keep them up. Currently, it seems like many are choosing the latter option. Consumer borrowing is accelerating at a quicker pace than it was before the pandemic.

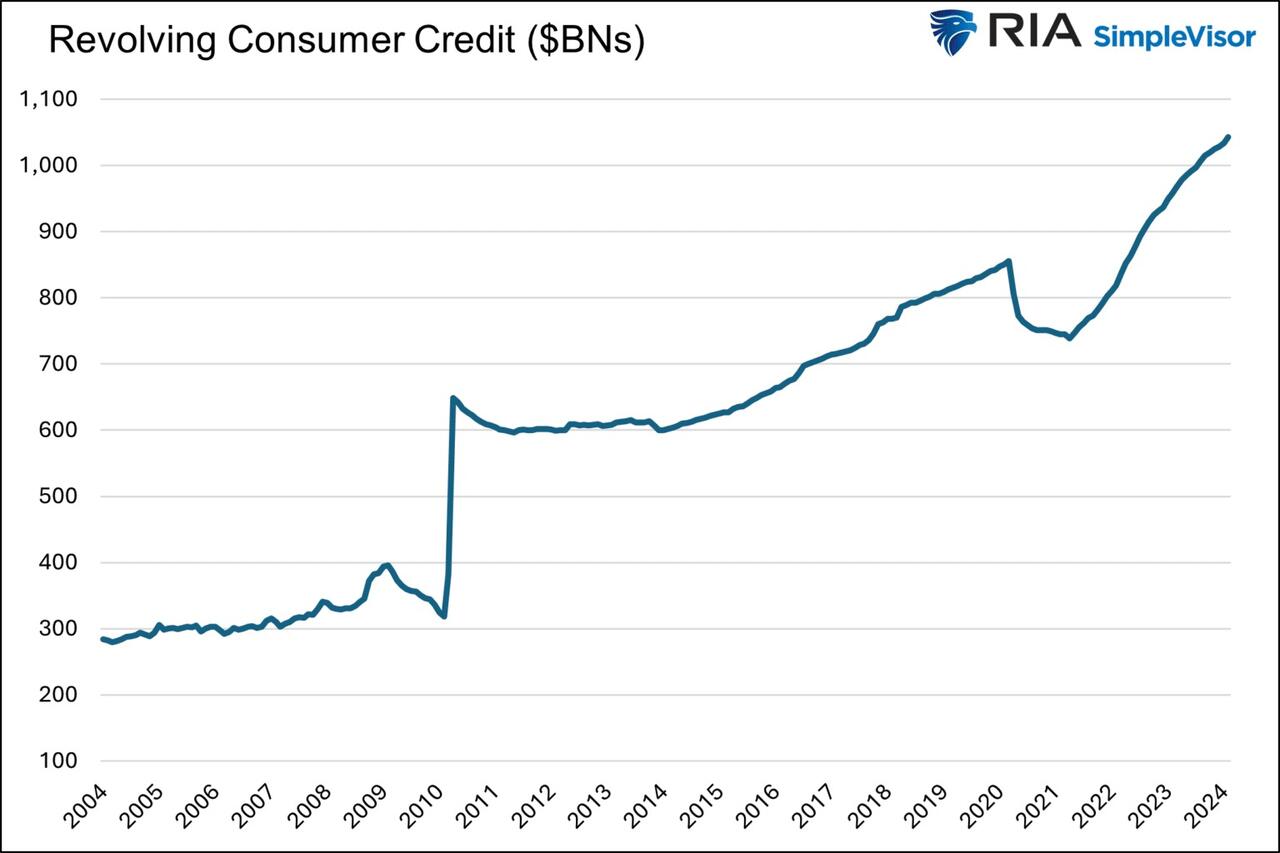

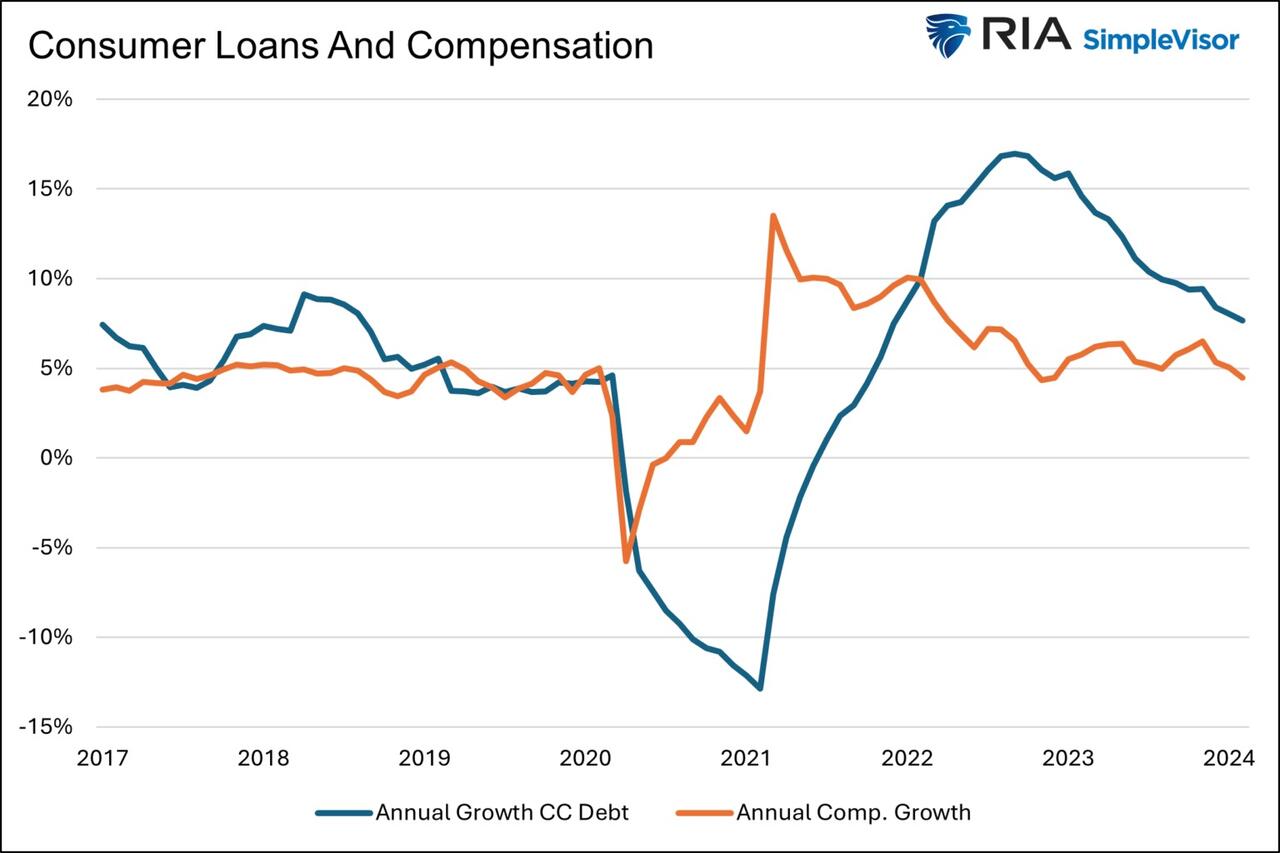

The first graph below shows outstanding credit card debt fell during the pandemic as the economy cratered. However, after multiple stimulus checks and broad-based economic recovery, consumer confidence rose, and with it, credit card balances surged.

The current trend is steeper than the pre-pandemic trend. Some may be a catch-up, but the current rate is unsustainable. Consequently, borrowing will likely slow down to its pre-pandemic trend or even below it as consumers deal with higher credit card balances and 20+% interest rates on the debt.

The second graph shows that since 2022, credit card balances have grown faster than our incomes. Like the first graph, the credit usage versus income trend is unsustainable, especially with current interest rates.

With many consumers maxing out their credit cards, is it any wonder buy-now-pay-later loans (BNPL) are increasing rapidly?

Insider Intelligence believes that 79 million Americans, or a quarter of those over 18 years old, use BNPL. Lending Tree claims that “nearly 1 in 3 consumers (31%) say they’re at least considering using a buy now, pay later (BNPL) loan this month.”More telling, according to their survey, only 52% of those asked are confident they can pay off their BNPL loan without missing a payment!

Wage Growth

Wages have been growing above trend since the pandemic. Since 2022, the average annual growth in compensation has been 6.28%. Higher incomes support more consumption, but higher prices reduce the amount of goods or services one can buy. Over the same period, real compensation has grown by less than half a percent annually. The average real compensation growth was 2.30% during the three years before the pandemic.

In other words, compensation is just keeping up with inflation instead of outpacing it and providing consumers with the ability to consume, save, or pay down debt.

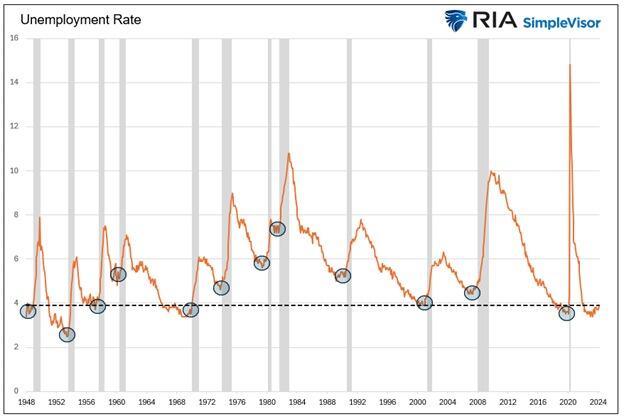

It’s All About Employment

The unemployment rate is 3.9%, up slightly from recent lows but still among the lowest rates in the last seventy-five years.

The uptick in credit card usage, decline in savings, and the savings rate argue that consumers are slowly running out of room to keep consuming at their current pace.

However, the most significant means by which we consume is income. If the unemployment rate stays low, consumption may moderate. But, if the recent uptick in unemployment continues, a recession is extremely likely, as we have seen every time it turned higher.

It’s not just those losing jobs that consume less. Of greater impact is a loss of confidence by those employed when they see friends or neighbors being laid off.

Accordingly, the labor market is probably the most important leading indicator of consumption and of the ability of the Bougie Broke to continue to be Bougie instead of flat-out broke!

Summary

There are always consumers living above their means. This is often harmless until their means decline or disappear. The Bougie Broke meme and the ability social media gives consumers to flaunt their “wealth” is a new medium for an age-old message.

Diving into the data, it argues that consumption will likely slow in the coming months. Such would allow some consumers to save and whittle down their debt. That situation would be healthy and unlikely to cause a recession.

The potential for the unemployment rate to continue higher is of much greater concern. The combination of a higher unemployment rate and strapped consumers could accentuate a recession.

Uncategorized

The most potent labor market indicator of all is still strongly positive

– by New Deal democratOn Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently…

Share this:

{kind=link}

{kind=link}

- by New Deal democrat

On Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently than not indicated a recession was near or underway. But I concluded by noting that this survey has historically been noisy, and I thought it would be resolved away this time. Specifically, there was strong contrary data from the Establishment survey, backed up by yesterday’s inflation report, to the contrary. Today I’ll examine that, looking at two other series.

{kind=link}

Digital Currency And Gold As Speculative Warnings

Bougie Broke The Financial Reality Behind The Facade

Q4 Update: Delinquencies, Foreclosures and REO

NY Fed Finds Medium, Long-Term Inflation Expectations Jump Amid Surge In Stock Market Optimism

Aging at AACR Annual Meeting 2024

Bitcoin on Wheels: The Story of Bitcoinetas

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

The most potent labor market indicator of all is still strongly positive

‘Bougie Broke’ – The Financial Reality Behind The Facade

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges