Government

Coronavirus – weekly update – 20 May 2020

Coronavirus – weekly update – 20 May 2020

Share this:

- Exits from lockdown proceed with no major mishaps

- Stock markets still trading sideways

- Slow progress in implementing fiscal support a potential risk and source of volatility.

Worldwide COVID-19 cases crossed the 5 million mark, while deaths topped 325,000, as of 20 May.

- More and more economies are easing their lockdown measures, as data on the human impact of Covid-19 continues to improve, albeit slowly. This is helping sentiment and expectations. So far, in countries that have lifted, or that had light lockdowns, the increase in the number of new Covid-19 cases is not significant, and the infection management is under control.

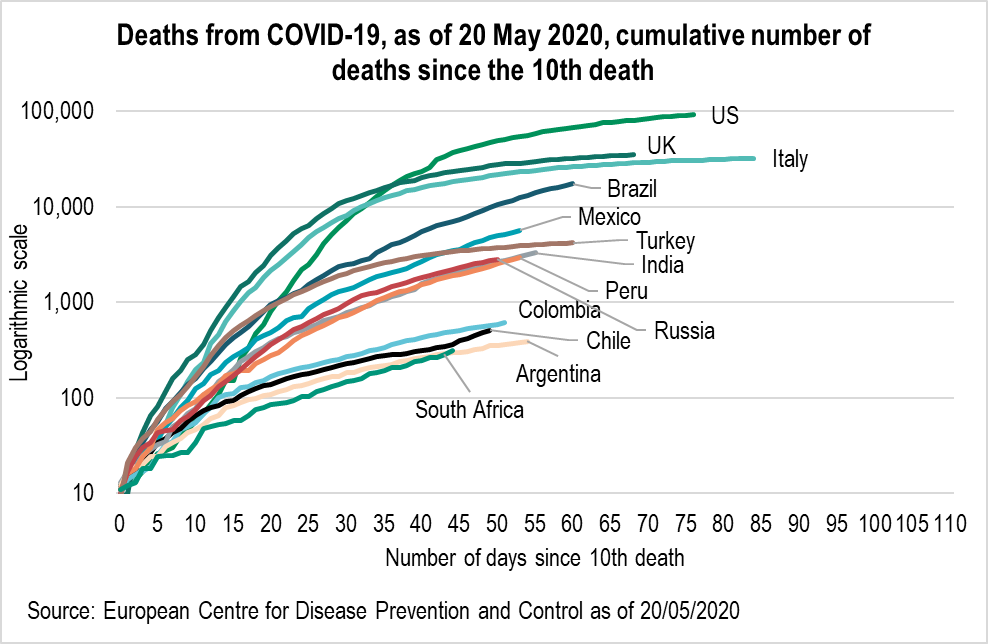

- The development of the pandemic in Brazil however, is worrying, as the death toll continues to climb fast. With over 17,000 deaths Brazil is, by some distance, the hardest hit among emerging economies. The shape of the curve implies Brazil is still weeks away from the likely peak (see Exhibit 1 below). The absence of a nationwide lockdown in Brazil, combined with conflicting messaging from the federal government, has aggravated the situation.

Exhibit 1:

For us, the key issue remains that in the absence of vaccine, this virus will be with us for a long time. For this reason, there can be no rapid return to normality. Levels of acquired immunity remain low according to recent serology studies. The capacity of nation states to conduct mass testing and contact tracing remains limited, with the exception of a few countries in Asia. This, in turn, limits the pace at which re-opening can proceed and sows the seeds of a potential second wave.

A vaccine would be obviously be a game changer. As we have seen this week, with the positive news from Moderna’s vaccine trial, the market enthusiastically responds to every bit of good news about vaccines, no matter how tentative and preliminary the results. Nonetheless, the consensus among experts remains that a vaccine will not arrive until 2021 at the earliest. The logistics required to support mass manufacture and delivery of the vaccine could further lengthen the timeline.

Economic news

On the data front, the major news is arguably the US data on activity and expenditure for April. The data for the first quarter of 2020 show a far more modest contraction in the US economy than in continental Europe. One plausible explanation is that lockdown measures came in to force later in the United States so the resultant contraction in activity occurred later and therefore had a smaller impact on the March data for the United States. The April data for the United States corroborate this hypothesis somewhat with retail sales, excluding autos, falling over 17% on the month and industrial production falling over 11% on the month. Nonetheless, it still seems likely that the absolute contraction in activity was larger in Europe. In Italy, for example, industrial production in March fell by almost 30%.

Policy measures – a pivotal moment for the European Union?

The major news this week was the Franco-German proposal for the EU Recovery Fund. If anything the size of the proposed fund is a slight disappointment – the EUR 500 billions figure is significantly lower than that discussed in an earlier plan, produced by the Spanish government. The proposal does however favour grants over loans. There is hope that this Franco-German plan could prove a pivotal moment in the creation of a genuine federal state.

The proposal has however not yet been adopted. It has already run into resistance from a familiar set of northern European countries. It may require diluting down in order to win the support of all countries. Moreover, we do not yet know how exactly the scheme will work and whether in particular, it will lead to the EU gaining tax revenue streams of its own.

There have been other significant development this week regarding the policy response to the crisis:

- As the focus shifts from nursing the economy through lock-down to supporting the recovery in demand, we believe that the case for further fiscal stimulus will build. In the United States, the Democrat-controlled House of Representatives has passed another USD 3 trillion stimulus package – called the Heroes Act – but it will not pass the Republican-controlled Senate. However, the Senate Majority Leader, Mitch McConnell has indicated a “high likelihood” that another stimulus bill will eventually pass after negotiation with the Democrats.

- The crisis will inevitably lead to a significant increase in government debt. Borrowing will automatically rise as the economy contracts and then the combined cost of socialising losses through the lockdown and stimulating demand in the recovery phase will lead to additional borrowing. This inevitably raises questions about how this additional debt-load will be serviced. The Governor of the Bank of England has signalled that his central bank will engage in persistent monetary financing to help the UK Government manage the huge cost of fighting the pandemic by “smoothing the profile of government borrowing and the impact that might have on financial markets”.

- Central banks will also need to provide sustained and significant monetary stimulus to the economy to support a recovery in demand once the social distancing measures are removed. One of the most contentious issues here is whether that stimulus should involve negative interest rates. Central banks have sent mixed messages on this point in the last week: Chair Powell continues to signal his discomfort with negative rates as a tool of monetary policy but several members of the Bank of England’s Monetary Policy Committee seem open to the idea in the United Kingdom.

Market outlook

- Activity data in China is showing a marked improvement as lockdowns are lifted and recovery gains ground. In our view, China points the way forward for those economies coming out of lockdown. In turn, this should be positive for oil prices as demand starts to pick up.

- In the short run, the current glass is half-full backdrop should continue for now with slightly lower volatility and markets drifting sideways. This cautious positive tone is supported by the expectation of more fiscal/monetary stimulus. However, the lack of implementation of fiscal support remains a risk and a source of volatility.

- The key headwind to implementation of additional fiscal support, is political fragmentation. This is currently delaying the introduction of broad-based fiscal initiatives in both Europe and the US.

- Whilst the market is pricing in a broad-based recovery, we see the risk that this recovery as being more uneven, pushing earnings and credit dispersion up, with entire sectors or even countries coming under significant pressure. Asset selection and risk allocation are likely to be more important than outright market calls in such an environment.

Denis Panel, Chief Investment Officer Multi Assets & Quantitative Solutions, and Marina Chernyak, senior economist and coordinator of COVID-19 research.

Any views expressed here are those of the author as of the date of publication, are based on available information, and are subject to change without notice. Individual portfolio management teams may hold different views and may take different investment decisions for different clients.

The value of investments and the income they generate may go down as well as up and it is possible that investors will not recover their initial outlay. Past performance is no guarantee for future returns.

Investing in emerging markets, or specialised or restricted sectors is likely to be subject to a higher-than-average volatility due to a high degree of concentration, greater uncertainty because less information is available, there is less liquidity or due to greater sensitivity to changes in market conditions (social, political and economic conditions).

Writen by Marina Chernyak. The post Coronavirus – weekly update – 20 May 2020 appeared first on Investors' Corner - The official blog of BNP Paribas Asset Management.

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Government

Walmart joins Costco in sharing key pricing news

The massive retailers have both shared information that some retailers keep very close to the vest.

Share this:

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trumpGovernment

Walmart has really good news for shoppers (and Joe Biden)

The giant retailer joins Costco in making a statement that has political overtones, even if that’s not the intent.

Share this:

{kind=link}

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trump

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

When Military Rule Supplants Democracy

Catastrophic Risk: Investing and Business Implications

Dropping Like a Stone: ON RRP Take‑up in the Second Half of 2023

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

The Digest #187

The Coming Of The Police State In America

Redefining Poverty: Towards a Transpartisan Approach

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 day ago

Walmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire