Uncategorized

Cincinnati Financial Corporation Announces Preliminary Estimate for Third-Quarter Storm Losses

Cincinnati Financial Corporation Announces Preliminary Estimate for Third-Quarter Storm Losses

PR Newswire

CINCINNATI, Oct. 20, 2022

CINCINNATI, Oct. 20, 2022 /PRNewswire/ — Cincinnati Financial Corporation (Nasdaq: CINF) today announced that its …

Share this:

Cincinnati Financial Corporation Announces Preliminary Estimate for Third-Quarter Storm Losses

PR Newswire

CINCINNATI, Oct. 20, 2022

CINCINNATI, Oct. 20, 2022 /PRNewswire/ -- Cincinnati Financial Corporation (Nasdaq: CINF) today announced that its consolidated third-quarter results are expected to include pretax catastrophe losses of approximately $252 million – representing an impact on the third-quarter 2022 combined ratio of approximately 13.9 percentage points, based on estimated property casualty earned premiums. The company's 5‑year historical average contribution of catastrophe losses to the combined ratio is 11.6 percentage points for the third quarter.

The catastrophe loss estimate includes $220 million from Hurricane Ian, excluding any effects of reinstatement premiums assumed or ceded, in addition to less severe storms. Losses estimated for Hurricane Ian as of September 30, 2022, did not reach a level applicable to Cincinnati Insurance's property catastrophe treaty or Cincinnati Re's property catastrophe excess of loss coverage as both reinsurance arrangements include retention of the first $100 million of any loss. The estimate for total third-quarter 2022 catastrophe losses incurred includes approximately $46 million for the commercial lines insurance segment; $69 million for the personal lines insurance segment; $112 million for Cincinnati Re® and $25 million for Cincinnati Global Underwriting Ltdsm.

Steven J. Johnston, chairman and CEO, commented: "Our hearts go out to all those who found themselves in the path of Hurricane Ian. We have deployed storm teams – made up of our own associates who volunteer to serve extra during catastrophes so that we can quickly begin the restoration process for our policyholders. This is when our claims associates shine, delivering fast, fair and empathetic service.

"So far this year we've seen a variety of challenges – inflation, declining stock and bond markets and a Category 4 hurricane – reinforcing our belief in the importance of maintaining our long-term focus. Our solid financial position ensures our ability to continue executing on our strategic initiatives, growing our agency plant, introducing diversifying products and investing in our talented associates."

Estimated losses and expenses from catastrophe-related claims are expected to bring the company's third-quarter 2022 property casualty combined ratio to approximately 104%. The combined ratio before catastrophe losses continues to reflect increased uncertainty of estimated ultimate losses, due in part to elevated paid losses reflecting economic or other forms of inflation. Net written premium growth is estimated to be approximately 14% for the quarter.

Declining stock markets drove third-quarter 2022 earnings to a net loss estimated to be between $2.61 and $2.67 per share, with non-GAAP operating income ranging from $0.70 to $0.76 on a per share basis. To reconcile net income to operating income, net investment gains and losses on an after-tax basis is removed.

The unaudited loss estimates and other data presented in this release is preliminary, based upon management estimates and subject to the completion of the company's procedures for the preparation of its quarterly financial statements. As a result, further adjustments may be made between now and the time financial results for the quarter are finalized.

Cincinnati Financial plans to report final results for third-quarter 2022 on Monday, October 31, after the close of regular trading on the Nasdaq Stock Market. A conference call to discuss the results will be held at 11 a.m. ET on Tuesday, November 1, with a live, audio-only internet broadcast available at cinfin.com/investors.

Cincinnati Financial Corporation offers primarily business, home and auto insurance through The Cincinnati Insurance Company and its two standard market property casualty companies. The same local independent insurance agencies that market those policies may offer products of our other subsidiaries, including life insurance, fixed annuities and surplus lines property and casualty insurance. For additional information about the company, please visit cinfin.com.

Mailing Address | Street Address |

P.O. Box 145496 | 6200 South Gilmore Road |

Cincinnati, Ohio 45250-5496 | Fairfield, Ohio 45014-5141 |

This is our "Safe Harbor" statement under the Private Securities Litigation Reform Act of 1995. Our business is subject to certain risks and uncertainties that may cause actual results to differ materially from those suggested by the forward-looking statements in this report. Some of those risks and uncertainties are discussed in our 2021 Annual Report on Form 10-K, Item 1A, Risk Factors, Page 32.

Factors that could cause or contribute to such differences include, but are not limited to:

- Effects of the COVID-19 pandemic that could affect results for reasons such as:

- Securities market disruption or volatility and related effects such as decreased economic activity and continued supply chain disruptions that affect our investment portfolio and book value

- An unusually high level of claims in our insurance or reinsurance operations that increase litigation-related expenses

- An unusually high level of insurance losses, including risk of legislation or court decisions extending business interruption insurance in commercial property coverage forms to cover claims for pure economic loss related to the COVID-19 pandemic

- Decreased premium revenue and cash flow from disruption to our distribution channel of independent agents, consumer self-isolation, travel limitations, business restrictions and decreased economic activity

- Inability of our workforce, agencies or vendors to perform necessary business functions

- Ongoing developments concerning business interruption insurance claims and litigation related to the COVID-19 pandemic that affect our estimates of losses and loss adjustment expenses or our ability to reasonably estimate such losses, such as:

- The continuing duration of the pandemic and governmental actions to limit the spread of the virus that may produce additional economic losses

- The number of policyholders that will ultimately submit claims or file lawsuits

- The lack of submitted proofs of loss for allegedly covered claims

- Judicial rulings in similar litigation involving other companies in the insurance industry

- Differences in state laws and developing case law

- Litigation trends, including varying legal theories advanced by policyholders

- Whether and to what degree any class of policyholders may be certified

- The inherent unpredictability of litigation

- Unusually high levels of catastrophe losses due to risk concentrations, changes in weather patterns (whether as a result of global climate change or otherwise), environmental events, war or political unrest, terrorism incidents, cyberattacks, civil unrest or other causes

- Increased frequency and/or severity of claims or development of claims that are unforeseen at the time of policy issuance, due to inflationary trends or other causes

- Inadequate estimates or assumptions, or reliance on third-party data used for critical accounting estimates

- Declines in overall stock market values negatively affecting our equity portfolio and book value

- Prolonged low interest rate environment or other factors that limit our ability to generate growth in investment income or interest rate fluctuations that result in declining values of fixed-maturity investments, including declines in accounts in which we hold bank-owned life insurance contract assets

- Domestic and global events, such as Russia's invasion of Ukraine, resulting in capital market or credit market uncertainty, followed by prolonged periods of economic instability or recession, that lead to:

- Significant or prolonged decline in the fair value of a particular security or group of securities and impairment of the asset(s)

- Significant decline in investment income due to reduced or eliminated dividend payouts from a particular security or group of securities

- Significant rise in losses from surety or director and officer policies written for financial institutions or other insured entities

- Our inability to manage Cincinnati Global or other subsidiaries to produce related business opportunities and growth prospects for our ongoing operations

- Recession, prolonged elevated inflation or other economic conditions resulting in lower demand for insurance products or increased payment delinquencies

- Ineffective information technology systems or discontinuing to develop and implement improvements in technology may impact our success and profitability

- Difficulties with technology or data security breaches, including cyberattacks, that could negatively affect our or our agents' ability to conduct business; disrupt our relationships with agents, policyholders and others; cause reputational damage, mitigation expenses and data loss and expose us to liability under federal and state laws

- Difficulties with our operations and technology that may negatively impact our ability to conduct business, including cloud-based data information storage, data security, cyberattacks, remote working capabilities, and/or outsourcing relationships and third-party operations and data security

- Disruption of the insurance market caused by technology innovations such as driverless cars that could decrease consumer demand for insurance products

- Delays, inadequate data developed internally or from third parties, or performance inadequacies from ongoing development and implementation of underwriting and pricing methods, including telematics and other usage-based insurance methods, or technology projects and enhancements expected to increase our pricing accuracy, underwriting profit and competitiveness

- Intense competition, and the impact of innovation, technological change and changing customer preferences on the insurance industry and the markets in which we operate, could harm our ability to maintain or increase our ability to maintain or increase our business volumes and profitability

- Changing consumer insurance-buying habits and consolidation of independent insurance agencies could alter our competitive advantages

- Inability to obtain adequate ceded reinsurance on acceptable terms, amount of reinsurance coverage purchased, financial strength of reinsurers and the potential for nonpayment or delay in payment by reinsurers

- Inability to defer policy acquisition costs for any business segment if pricing and loss trends would lead management to conclude that segment could not achieve sustainable profitability

- Inability of our subsidiaries to pay dividends consistent with current or past levels

- Events or conditions that could weaken or harm our relationships with our independent agencies and hamper opportunities to add new agencies, resulting in limitations on our opportunities for growth, such as:

- Downgrades of our financial strength ratings

- Concerns that doing business with us is too difficult

- Perceptions that our level of service, particularly claims service, is no longer a distinguishing characteristic in the marketplace

- Inability or unwillingness to nimbly develop and introduce coverage product updates and innovations that our competitors offer and consumers expect to find in the marketplace

- Actions of insurance departments, state attorneys general or other regulatory agencies, including a change to a federal system of regulation from a state-based system, that:

- Impose new obligations on us that increase our expenses or change the assumptions underlying our critical accounting estimates

- Place the insurance industry under greater regulatory scrutiny or result in new statutes, rules and regulations

- Restrict our ability to exit or reduce writings of unprofitable coverages or lines of business

- Add assessments for guaranty funds, other insurance‑related assessments or mandatory reinsurance arrangements; or that impair our ability to recover such assessments through future surcharges or other rate changes

- Increase our provision for federal income taxes due to changes in tax law

- Increase our other expenses

- Limit our ability to set fair, adequate and reasonable rates

- Place us at a disadvantage in the marketplace

- Restrict our ability to execute our business model, including the way we compensate agents

- Adverse outcomes from litigation or administrative proceedings, including effects of social inflation on the size of litigation awards

- Events or actions, including unauthorized intentional circumvention of controls, that reduce our future ability to maintain effective internal control over financial reporting under the Sarbanes-Oxley Act of 2002

- Unforeseen departure of certain executive officers or other key employees due to retirement, health or other causes that could interrupt progress toward important strategic goals or diminish the effectiveness of certain longstanding relationships with insurance agents and others

- Our inability, or the inability of our independent agents, to attract and retain personnel in a competitive labor market, impacting the customer experience and altering our competitive advantages

- Events, such as an epidemic, natural catastrophe or terrorism, that could hamper our ability to assemble our workforce at our headquarters location or work effectively in a remote environment

Further, our insurance businesses are subject to the effects of changing social, global, economic and regulatory environments. Public and regulatory initiatives have included efforts to adversely influence and restrict premium rates, restrict the ability to cancel policies, impose underwriting standards and expand overall regulation. We also are subject to public and regulatory initiatives that can affect the market value for our common stock, such as measures affecting corporate financial reporting and governance. The ultimate changes and eventual effects, if any, of these initiatives are uncertain.

View original content to download multimedia:https://www.prnewswire.com/news-releases/cincinnati-financial-corporation-announces-preliminary-estimate-for-third-quarter-storm-losses-301655426.html

SOURCE Cincinnati Financial Corporation

Uncategorized

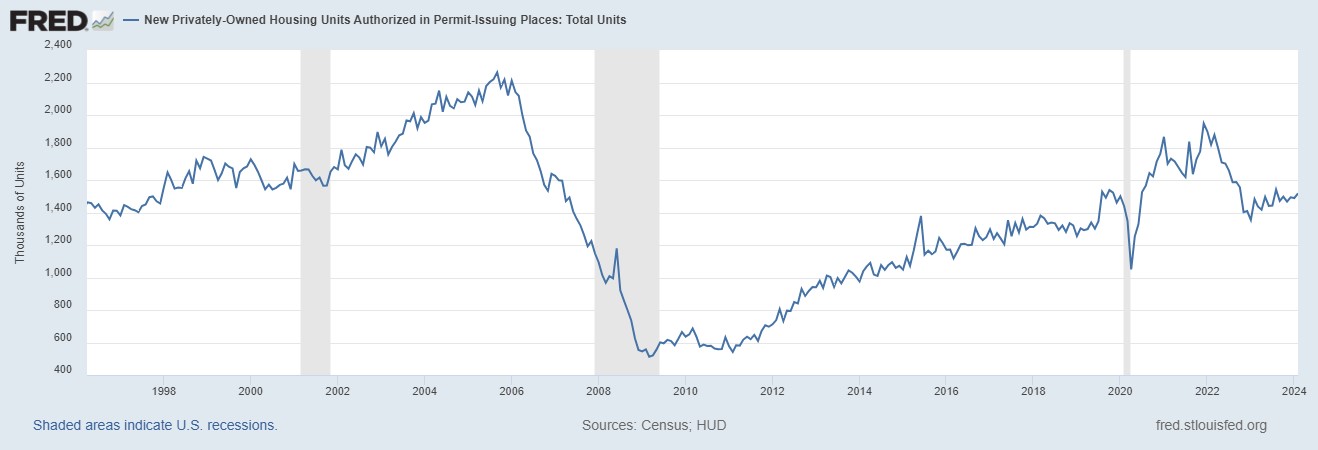

Apartment permits are back to recession lows. Will mortgage rates follow?

If housing leads us into a recession in the near future, that means mortgage rates have stayed too high for too long.

Share this:

In Tuesday’s report, the 5-unit housing permits data hit the same levels we saw in the COVID-19 recession. Once the backlog of apartments is finished, those jobs will be at risk, which traditionally means mortgage rates would fall soon after, as they have in previous economic cycles.

However, this is happening while single-family permits are still rising as the rate of builder buy-downs and the backlog of single-family homes push single-family permits and starts higher. It is a tale of two markets — something I brought up on CNBC earlier this year to explain why this trend matters with housing starts data because the two marketplaces are heading in opposite directions.

The question is: Will the uptick in single-family permits keep mortgage rates higher than usual? As long as jobless claims stay low, the falling 5-unit apartment permit data might not lead to lower mortgage rates as it has in previous cycles.

From Census: Building Permits: Privately‐owned housing units authorized by building permits in February were at a seasonally adjusted annual rate of 1,518,000. This is 1.9 percent above the revised January rate of 1,489,000 and 2.4 percent above the February 2023 rate of 1,482,000.

When people say housing leads us in and out of a recession, it is a valid premise and that is why people carefully track housing permits. However, this housing cycle has been unique. Unfortunately, many people who have tracked this housing cycle are still stuck on 2008, believing that what happened during COVID-19 was rampant demand speculation that would lead to a massive supply of homes once home sales crashed. This would mean the builders couldn’t sell more new homes or have housing permits rise.

Housing permits, starts and new home sales were falling for a while, and in 2022, the data looked recessionary. However, new home sales were never near the 2005 peak, and the builders found a workable bottom in sales by paying down mortgage rates to boost demand. The first level of job loss recessionary data has been averted for now. Below is the chart of the building permits.

On the other hand, the apartment boom and bust has already happened. Permits are already back to the levels of the COVID-19 recession and have legs to move lower. Traditionally, when this data line gets this negative, a recession isn’t far off. But, as you can see in the chart below, there’s a big gap between the housing permit data for single-family and five units. Looking at this chart, the recession would only happen after single-family and 5-unit permits fall together, not when we have a gap like we see today.

From Census: Housing completions: Privately‐owned housing completions in February were at a seasonally adjusted annual rate of 1,729,000.

As we can see in the chart below, we had a solid month of housing completions. This was driven by 5-unit completions, which have been in the works for a while now. Also, this month’s report show a weather impact as progress in building was held up due to bad weather. However, the good news is that more supply of rental units will mean the fight against rent inflation will be positive as more supply is the best way to deal with inflation. In time, that is also good news for mortgage rates.

Housing Starts: Privately‐owned housing starts in February were at a seasonally adjusted annual rate of 1,521,000. This is 10.7 percent (±14.2 percent)* above the revised January estimate of 1,374,000 and is 5.9 percent (±10.0 percent)* above the February 2023 rate of 1,436,000.

Housing starts data beat to the upside, but the real story is that the marketplace has diverged into two different directions. The apartment boom is over and permits are heading below the COVID-19 recession, but as long as the builders can keep rates low enough to sell more new homes, single-family permits and starts can slowly move forward.

If we lose the single-family marketplace, expect the chart below to look like it always does before a recession — meaning residential construction workers lose their jobs. For now, the apartment construction workers are at the most risk once they finish the backlog of apartments under construction.

Overall, the housing starts beat to the upside. Still, the report’s internals show a marketplace with early recessionary data lines, which traditionally mean mortgage rates should go lower soon. If housing leads us into a recession in the near future, that means mortgage rates have stayed too high for too long and restrictive policy by the Fed created a recession as we have seen in previous economic cycles.

The builders have been paying down rates to keep construction workers employed, but if rates go higher, it will get more and more challenging to do this because not all builders have the capacity to buy down rates. Last year, we saw what 8% mortgage rates did to new home sales; they dropped before rates fell. So, this is something to keep track of, especially with a critical Federal Reserve meeting this week.

recession covid-19 fed federal reserve home sales mortgage rates recessionUncategorized

One more airline cracks down on lounge crowding in a way you won’t like

Qantas Airways is increasing the price of accessing its network of lounges by as much as 17%.

Share this:

Over the last two years, multiple airlines have dealt with crowding in their lounges. While they are designed as a luxury experience for a small subset of travelers, high numbers of people taking a trip post-pandemic as well as the different ways they are able to gain access through status or certain credit cards made it difficult for some airlines to keep up with keeping foods stocked, common areas clean and having enough staff to serve bar drinks at the rate that customers expect them.

In the fall of 2023, Delta Air Lines (DAL) caught serious traveler outcry after announcing that it was cracking down on crowding by raising how much one needs to spend for lounge access and limiting the number of times one can enter those lounges.

Related: Competitors pushed Delta to backtrack on its lounge and loyalty program changes

Some airlines saw the outcry with Delta as their chance to reassure customers that they would not raise their fees while others waited for the storm to pass to quietly implement their own increases.

Shutterstock

This is how much more you'll have to pay for Qantas lounge access

Australia's flagship carrier Qantas Airways (QUBSF) is the latest airline to announce that it would raise the cost accessing the 24 lounges across the country as well as the 600 international lounges available at airports across the world through partner airlines.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

Unlike other airlines which grant access primarily after reaching frequent flyer status, Qantas also sells it through a membership — starting from April 18, 2024, prices will rise from $600 Australian dollars ($392 USD) to $699 AUD ($456 USD) for one year, $1,100 ($718 USD) to $1,299 ($848 USD) for two years and $2,000 AUD ($1,304) to lock in the rate for four years.

Those signing up for lounge access for the first time also currently pay a joining fee of $99 AUD ($65 USD) that will rise to $129 AUD ($85 USD).

The airline also allows customers to purchase their membership with Qantas Points they collect through frequent travel; the membership fees are also being raised by the equivalent amount in points in what adds up to as much as 17% — from 308,000 to 399,900 to lock in access for four years.

Airline says hikes will 'cover cost increases passed on from suppliers'

"This is the first time the Qantas Club membership fees have increased in seven years and will help cover cost increases passed on from a range of suppliers over that time," a Qantas spokesperson confirmed to Simple Flying. "This follows a reduction in the membership fees for several years during the pandemic."

The spokesperson said the gains from the increases will go both towards making up for inflation-related costs and keeping existing lounges looking modern by updating features like furniture and décor.

While the price increases also do not apply for those who earned lounge access through frequent flyer status or change what it takes to earn that status, Qantas is also introducing even steeper increases for those renewing a membership or adding additional features such as spouse and partner memberships.

In some cases, the cost of these features will nearly double from what members are paying now.

stocks pandemicUncategorized

Star Wars icon gives his support to Disney, Bob Iger

Disney shareholders have a huge decision to make on April 3.

Share this:

Disney's (DIS) been facing some headwinds up top, but its leadership just got backing from one of the company's more prominent investors.

Star Wars creator George Lucas put out of statement in support of the company's current leadership team, led by CEO Bob Iger, ahead of the April 3 shareholders meeting which will see investors vote on the company's 12-member board.

"Creating magic is not for amateurs," Lucas said in a statement. "When I sold Lucasfilm just over a decade ago, I was delighted to become a Disney shareholder because of my long-time admiration for its iconic brand and Bob Iger’s leadership. When Bob recently returned to the company during a difficult time, I was relieved. No one knows Disney better. I remain a significant shareholder because I have full faith and confidence in the power of Disney and Bob’s track record of driving long-term value. I have voted all of my shares for Disney’s 12 directors and urge other shareholders to do the same."

Related: Disney stands against Nelson Peltz as leadership succession plan heats up

Lucasfilm was acquired by Disney for $4 billion in 2012 — notably under the first term of Iger. He received over 37 million in shares of Disney during the acquisition.

Lucas' statement seems to be an attempt to push investors away from the criticism coming from The Trian Partners investment group, led by Nelson Peltz. The group, owns about $3 million in shares of the media giant, is pushing two candidates for positions on the board, which are Peltz and former Disney CFO Jay Rasulo.

Peltz and Co. have called out a pair of Disney directors — Michael Froman and Maria Elena Lagomasino — for their lack of experience in the media space.

Related: Women's basketball is gaining ground, but is March Madness ready to rival the men's game?

Blackwells Capital is also pushing three of its candidates to take seats during the early April shareholder meeting, though Reuters has reported that the firm has been supportive of the company's current direction.

Disney has struggled in recent years amid the changes in media and the effects of the pandemic — which triggered the return of Iger at the helm in late 2022. After going through mass layoffs in the spring of 2023 and focusing on key growth brands, the company has seen a steady recovery with its stock up over 25% year-to-date and around 40% for the last six months.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic recovery

Apartment permits are back to recession lows. Will mortgage rates follow?

Manufacturing and construction vs. the still-inverted yield curve

When words make you sick

How much stress is too much? A psychiatrist explains the links between toxic stress and poor health − and how to get help

Caitlin Clark, Coach Prime, and Linsanity: The Anatomy of a Viewership ‘Craze’

PR55α-controlled PP2A Inhibits p16 Expression and Blocks Cellular Senescence Induction

US Economic Conditions Scream “Buy Gold”

Wall Street Bonuses Fall For Second Year To 2019 Lows Amid Capital Markets Freeze

Half Of Downtown Pittsburgh Office Space Could Be Empty In 4 Years

Airline, travel companies face Chapter 11 bankruptcy, default risk

-

Spread & Containment7 days ago

Spread & Containment7 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International2 weeks ago

International2 weeks agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International2 weeks ago

International2 weeks agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex