Uncategorized

Can We Get A 5th All-Time High In A Row: Futures Flat Ahead Of ECB, GDP Report

Can We Get A 5th All-Time High In A Row: Futures Flat Ahead Of ECB, GDP Report

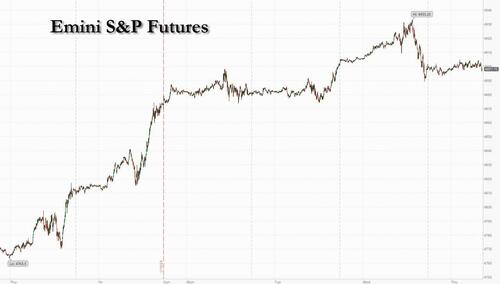

After the S&P eeked out modst gains yesterday despite an…

Share this:

After the S&P eeked out modst gains yesterday despite an intraday swoon, which helped it close for a 4th consecutive, the question is whether we can get a five-peat: for now, it's on the fence, with S&P 500 futures flate ahead of a slew of US economic data and a meeting of the European Central Bank.while Nasdaq 100 futures inched up 0.1% as the market tried to shake off the gloom from Tesla’s disappointing earnings late on Wednesday. While shares in the electric carmaker dropped 8% in US premarket trading, those in IBM gained 7% after it delivered a positive revenue outlook. American Airlines Group Inc. and Blackstone Inc. also rose after reporting profits.

In premarket trading, Tesla shares tumbled 8% after the EV maker’s 2024 delivery guidance failed to soothe investor concerns about slowing demand. Here are some of the most notable premarket movers:

- American Airlines (AAL) gains 4% after forecasting full year profit that’s above analyst expectations.

- Boeing (BA) slips 2% after the FAA halted planned increases in production of the 737 Max.

- Comcast Corp. (CMCSA) gains 2% after posting better-than-expected earnings and sales.

- Hertz (HTZ) falls 2% after JPMorgan cut the recommendation on the car-rental company to neutral, citing few near-term catalysts.

- Humana (HUM) plunges 13% after the company withdrew its 2025 earnings target and forecast 2024 profit far lower than Wall Street’s estimates.

- IBM (IBM) rallies 7% after the IT services company reported fourth-quarter results that beat expectations.

- Las Vegas Sands (LVS) advances 2% after posting sales that beat Wall Street’s expectations as Chinese travel to Macau continued its recovery, defying concerns of an economic slowdown.

- Paramount Global (PARA) advances 3% after Bloomberg reported that Skydance Media’s David Ellison made an offer to buy National Amusements, the holding company of the Redstone family that controls 77% of the voting stock in the media giant.

- Sherwin-Williams (SHW) falls 5% after providing a 2024 profit forecast that disappointed.

- Virtu Financial (VIRT) slumps 5% after the financial services firm reported adjusted Ebitda for the fourth quarter that missed the average analyst estimate.

Elsewhere, Intel rose ahead of its own report later in the day. Thursday also brought some disappointing reports from the likes of European chipmaker STMicroelectronics NV dropped and South Korea’s SK Hynix Inc., the world’s no. 2 maker of memory chips, yest investors are confident interest rates will fall this year and that economic growth is likely to stay resilient.

“We are still in a bad-news-is-good-news environment and that if earnings drop a bit and margins tick down, it would be a further guarantee that interest rates will go down,” said Frederic Leroux, head of cross asset at Carmignac Gestion.

As noted in our preview, the ECB is expected to keep rates on hold at 4% later in the day, and its statement and post-meeting news conference will be parsed for clues on the path forward. While markets are leaning toward an April rate cut, ECB officials seem to be penciling in June for their first move.

Similarly, US GDP data is expected to show the economy expanded at a 2% annualized rate in the fourth quarter. A slew of other figures will also emerge, including inventories, new home sales and weekly unemployment claims, which should offer a snapshot of the economy before the next Federal Reserve meeting.

A key focal point for risk assets is the Treasury market, where long-dated yields have been on the rise. The 30-year yield eased about 2 basis points, having risen on Wednesday to its highest level this year, while 10-year yields are around 4.16%, up more than 20 basis points so far this year.

European stocks edge lower as traders look ahead to the ECB meeting later on Thursday. The Stoxx 600 is down 0.2% as investors await a meeting from the European Central Bank for further clues about interest rates. Chemicals, media and energy sectors are the best performers, while the autos sector falls after Tesla missed its earnings estimates. Among individual movers, STMicroelectronics falls as its sales outlook for the current quarter misses estimates and Nokia Oyj climbs after a better-than-expected fourth quarter. Here are some of the biggest movers on Thursday:

- Shares in Tryg jump as much as 6.2%, the most in three months, after the Danish insurance company reported 4Q results that beat analyst estimates.

- Shares in SEB advance as much as 3.7%, erasing earlier declines of as much as 2.7%, after Sweden’s largest lender missed earnings estimates, but posted higher-than-expected capital returns.

- Shares in Givaudan rise as much as 5.4%, the most since November 2022, after the Swiss specialty chemicals firm reported full year like-for-like sales above estimates. Analysts highlighted strength in fine fragrances, while Morgan Stanley says the sequential improvement in like-for-like sales, especially in North America, in the fourth quarter is positive for other ingredient peers into 2024.

- Shares in Dr. Martens gain as much as 7.9% to erase an earlier decline after the footwear maker maintained its full-year guidance in a third-quarter update. Investec said the company’s longer-term growth opportunities “have not gone away.”

- Shares in Tod’s rise as much as 5.8% after analysts said the Italian luxury footwear firm’s preliminary full-year results imply strong fourth-quarter sales, driven by its retail channel, as well as strength in the Americas and Greater China. The final full-year results are due in March.

- Shares in Publicis gain as much as 2.4%, touching a record high, after the advertising firm reported preliminary fourth-quarter organic revenue growth which beat estimates and announced plans to invest €300 million over the next three years in AI, including €100 million in 2024.

- Shares in Sandvik rise as much as 2.2% after the Swedish industrial and mining equipment firm reported fourth-quarter results that mostly met expectations, with Jefferies seeing a cost-cutting program adding to earnings next year.

- Shares in STMicro drop as much as 5.7% in Paris after the chipmaker’s guidance for FY24 revenue and gross margin missed estimates. STMicro said customer orders decreased in 4Q versus a quarter earlier. The outlook showed a deeper decline in demand for chips used in industrial applications, while demand for chips used in cars remains robust, analysts said. Peers including Infineon and Melexis also trade lower.

- Shares in Wizz Air slide as much as 8.1% after the budget airline reported third-quarter sales and profits that missed estimates, saying that its results were affected by the cancellation of Israel flights. Analysts at Citi said that pricing weakness was a key negative, and sees risks to full-year guidance.

- Shares in IG Group fall as much as 11%, the steepest drop since September 2021, after the online-trading company’s half-year trading update missed estimates, with analysts highlighting soft market conditions.

- Shares in St. James’s Place drop as much 10%, the most in more than three months, after the UK wealth manager reported net inflows for the full year that missed the average analyst estimate.

- Shares in Fevertree drop as much as 5.3%, biggest decline in almost four months, after the high-end tonic maker reported full-year revenue that missed estimates, with Morgan Stanley citing disappointing international sales.

Earlier in the session, Asian stocks were mostly higher as Chinese shares continued to climb on bets that the latest stimulus measures from Beijing will provide a floor for the cratering market.

The MSCI Asia Pacific Index rose 0.2% after swinging in a narrow range earlier in the session. TSMC and Tencent were among the biggest boosts while SK Hynix fell, paring a sliver of last year’s gains. Stocks rose in Australia and Taiwan as Indian equities retreated.

Shares in Hong Kong and mainland China climbed for a third day after the People’s Bank of China said it would cut the reserve requirement ratio for banks and hinted at more. Investors are still trying to gauge how long gains might be sustained after news earlier this week of a $278 billion market rescue package from the government.

- Hang Seng and Shanghai Comp were boosted with outperformance in the latter as mainland participants took their first opportunity to react to the latest support measures by China including the 50bps RRR cut which will release CNY 1tln of funds.

- Nikkei 225 eventually turned positive but lagged behind regional peers and briefly dipped below the 36,000 level.

- ASX 200 notched mild gains as strength in the commodity-related sectors picked up the slack in the rate-sensitive industries.

- Indian stocks resumed losses on Thursday with key gauges erasing half of the previous session’s gains, dragged by declines in the banking and technology shares. A key measure of lenders plunging to its lowest level in almost two months and today’s expiry of monthly derivative contracts also weighed on investor sentment. The S&P BSE Sensex fell 0.5% to 70,700.67 in Mumbai, while the NSE Nifty 50 Index slipped by a similar measure. HDFC Bank contributed the most to the index’s decline, decreasing 1.4%. BSE Ltd.’s banking index fell 0.6% to its lowest since Dec. 1.

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The Norwegian krone extended gains after the Norges Bank stood pat and said high rates will likely be needed for some time ahead. USD/NOK is down 0.5%.

In rates, Treasuries rise, with US 10-year yields falling 2bps to 4.16%. Bunds and gilts are lower ahead of the European Central Bank meeting, while US session includes first estimate of 4Q GDP and weekly jobless claims data, as well as a 7-year note auction, last coupon sale until Feb. 6. US yields richer by ~2bp across long-end of the curve vs little-changed front-end and belly; 10-year yields around 4.16% outperform bunds and gilts by ~3bp on the day. Treasury auction cycle concludes with $41b 7-year note sale at 1pm; Wednesday’s sloppy 5-year note sale tailed by 2bp. WI 7-year yield around 4.115% is ~25.5bp cheaper than December’s result

In commodities, oil prices advance, with WTI rising 1.6% to trade near $76.30. Spot gold adds 0.2%.

To the day ahead now, and the main highlight will be the ECB’s monetary policy decision, and President Lagarde’s press conference. Data releases from the US include the advance reading of Q4 GDP, along with the weekly initial jobless claims and new home sales for December. Meanwhile in Germany, there’s the Ifo Institute’s business climate indicator for January. Finally, earnings releases include Visa, Intel and LVMH.

Market Snapshot

- S&P 500 futures little changed at 4,902.25

- STOXX Europe 600 little changed at 476.69

- MXAP up 0.3% to 166.51

- MXAPJ up 0.7% to 508.28

- Nikkei little changed at 36,236.47

- Topix up 0.1% to 2,531.92

- Hang Seng Index up 2.0% to 16,211.96

- Shanghai Composite up 3.0% to 2,906.11

- Sensex down 0.7% to 70,586.84

- Australia S&P/ASX 200 up 0.5% to 7,555.36

- Kospi little changed at 2,470.34

- German 10Y yield little changed at 2.36%

- Euro little changed at $1.0893

- Brent Futures up 1.0% to $80.86/bbl

- Gold spot up 0.0% to $2,014.81

- US Dollar Index little changed at 103.21

Top Overnight News

- More and more Chinese investors are using creative ways to own bitcoin and other crypto assets that they believe are safer than investing in crumbling stock and property markets at home. While cryptocurrency is banned in mainland China and there are strict controls on capital movement across the border, people are still able to trade tokens such as bitcoin on crypto exchanges such as OKX and Binance, or through other over-the-counter channels. RTRS

- Surging freight rates provide another reason for the ECB to temper hopes for early rate cuts. Red Sea chaos has pushed the Rotterdam-to-Shanghai container benchmark to $975 as of Jan. 18, from $466 a month earlier. That’s threatening to add upward pressure to euro-area inflation. BBG

- Expect more ECB pushback against bets for rate cuts as early as April, after an anticipated hold for a third meeting. Christine Lagarde is poised to double down on her cautious data-dependence after last week’s signal that a summer reduction is “likely.” BBG

- McConnell suggested the Senate could look to split Ukraine from the border given ongoing controversy around the latter topic (the odds of anything happening on the border are fading fast). The Hill

- Fed says the Bank Term Funding Program will stop making new loans on Mar 11, and the rate on new BTFP loans has been increased to eliminate an arbitrage opportunity for banks (“the interest rate applicable to new BTFP loans has been adjusted such that the rate on new loans extended from now through program expiration will be no lower than the interest rate on reserve balances”). Fed

- The economic agenda Trump would bring to a 2nd term will be very different from the first. Then, as now, Trump’s strongest economic conviction is in protectionism. In his first term, though, that was overshadowed by a sweeping tax overhaul Republican allies muscled through Congress. In his second term, no such tax plan is waiting in the wings. Instead, Trump wants to expand the trade war he started six years ago by hitting a range of trading partners with steep new tariffs. The tit-for-tat retaliation, higher costs, and supply-chain disruptions make for a less benign landscape than what prevailed before the Covid-19 pandemic hit in 2020. WSJ

- More than 21 million people have signed up for health plans through the Affordable Care Act’s health insurance marketplaces, the Biden administration announced Wednesday. The record level of enrollment comes as former president Donald Trump, seeking the GOP nomination, is again vowing to repeal the program if elected. WaPo

- Bank of America has sent “letters of education” to employees who have not been showing up at the office, warning them of disciplinary action, in the latest move from a large company to push staff back to the workplace. FT

- TSLA down 8% pre mkt after company reported a miss on Q4 EPS due to weak margins, and mgmt. warns that vehicle volume growth in ’24 may be “notably lower” than ’23. BBG

- GSPB: Overall Gross exposure has risen to new record highs, while Net exposure is now in the 50th percentile on a 3-year lookback (vs. 3rd percentile at the start of November). Importantly, both Long and Short exposures are now at their respective multi-year highs, a sharp contrast vs. the start of 2023 when Long exposure fell to post-Covid lows.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive but with gains capped as markets digested a slew of earnings releases and with the recent upside in global yields partially offsetting the Chinese stimulus euphoria. ASX 200 notched mild gains as strength in the commodity-related sectors picked up the slack in the rate-sensitive industries. Nikkei 225 eventually turned positive but lagged behind regional peers and briefly dipped below the 36,000 level. Hang Seng and Shanghai Comp were boosted with outperformance in the latter as mainland participants took their first opportunity to react to the latest support measures by China including the 50bps RRR cut which will release CNY 1tln of funds.

Top Asian News

- Australian PM Albanese said every taxpayer will get a tax cut from July 1st as his government made changes to planned tax cuts including reducing benefits for the wealthy and providing low-income earners with more breaks, while Albanese commented that tax cuts have no implication on RBA's inflation forecast.

- Moody's downgrades the rating of 17 Chinese local government financing vehicles by one notch; revises outlooks to negative

European bourses, Stoxx600 (-0.2%) are taking a breather from yesterday’s gains induced by the PBoC RRR cut & the Tech sector. Indices are marginally weaker, with the exception of the AEX (+0.4%), which continues to benefit from gains in ASML after earnings earlier in the week. European sectors hold a negative tilt; though, Energy is at the top of the pile amid higher crude prices. Chemicals and Media are both propped up by strong earnings results within the sector; Givaudan (+4.4%) and Publicis (+1.9%) assisting respectively. US equity futures are mixed; ES and NQ are trading on either side of the unchanged mark, whilst the RTY outperforms as it attempts to pare back the underperformance seen in the prior session. Tesla (-7.9%) is significantly lower in the pre-market after its results missed noting that 2024 vehicle growth will be lower than the prior year.

Top European News

- Red Sea attacks reportedly push BHP to divert shipping from Asia to Europe, via WSJ citing sources; adding around nine days to transit time, according to experts cited.

- Norges Bank maintains its Key Policy Rate at 4.50% as expected; "the policy rate will likely be kept at that level for some time ahead". Click here for full analysis on the announcement.

Earnings

- Tesla Inc (TSLA) - Q4 2023 (USD): Adj. EPS 0.71 (exp. 0.74), Revenue 25.17bln (exp. 25.59bln); 2024 vehicle volume growth may be notably lower than 2023. KEY METRICS: Free cash flow 2.06bln (exp. .1.45bln). Gross margin 17.6% (exp. 18.1%). CapEx 2.31bln (exp. 2.32bln). COMMENTARY: Cybertruck production and deliveries ramp throughout the year. One-time non-cash tax benefit of USD 5.9bln recorded. CEO Musk says very far along with next-generation product development Co. is to first produce next-generation vehicles in Texas followed by Mexico, while Co. expects capital spending to exceed USD 10bln in 2024. Says: Will start production of next-generation vehicle towards end-2025. Will ramp up battery cell orders from suppliers. The production ramp-up of next-generation vehicles will be challenging. Wants 25% control of the company to be an effective steward of very powerful technology. A dual class of stock would be ideal. Co. has a chance of shipping some Optimus units next year. Chinese car companies will demolish rivals without trade barriers. (Tesla) Shares -7.8% premarket.

- International Business Machines Corp (IBM) - Q4 2023 (USD): oper. EPS 3.87 (exp. 3.78), Revenue 17.4bln (exp. 17.3bln). Sees FY free cash flow of about USD 12bln (exp. 10.9bln). Sees FY constant currency revenue growth consistent with the company’s mid-single digit model. (Newswires). Shares +7.4% premarket.

- Nokia (NOKIA FH) - Q4 (EUR): Revenue 5.71bln (exp. 6.10bln), EPS 0.10 (exp. 0.13), Adj. EBIT 846mln (exp. 767.5mln), initiates a 2-year EUR 600mln share repurchase program; raises dividend to EUR 0.13/shr (prev. 0.12/shr). COMMENTARY: "In Q4 the environment remained challenging however there are now signs of stabilization with improving order trends.". "Nokia expects Q1 net sales in its networks businesses (consisting of Network Infrastructure, Mobile Networks and Cloud and Network Services) to show an approximately normal seasonal decline sequentially." GUIDANCE: Sees FY comparable operating profit between EUR 2.3-2.9bln (exp. 2.449bln). "Company decided to lower its comparable operating margin target to be achieved by 2026 from the prior at least 14% to at least 13%." "Nokia still sees a path to achieving the at least 14% comparable operating margin target but considering the current market conditions in Mobile Networks, this was deemed a prudent change". (Nokia/Newswires) +7.2% in European trade

- STMicroelectronics (STM FP) - Q4 (USD): Revenue 4.28bln (exp. 4.31bln), Net 1.08bln (exp. 0.9bln), EPS 1.14 (exp. 0.95), Operating Income 1.02bln (exp. 1.04bln). OTHER METRICS: Intend to invest circa. 2.5bln in net CapEx during 2024. Q1 GUIDANCE: Revenue 3.6bln (exp. 4.06bln). Gross Margin 42.3%. COMMENTARY: “In Q4, our customer order bookings decreased compared to Q3. We continued to see stable end-demand in Automotive, no significant increase in Personal Electronics, and further deterioration in Industrial.” "In Q4, ST delivered revenues and gross margin slightly below the mid-point of the guidance, with higher revenues in Personal Electronics offset by a softer growth rate in Automotive.” (STMicroelectronics/Newswires) -3.0% in European trade

FX

- Uneventful trade for the USD with the DXY back on a 103 handle awaiting key US data releases; peak for today is at 103.40, just shy of its 200DMA at 103.47.

- EUR is steady vs. the USD with the pair unable to reclaim 1.09 status ahead of the ECB. Well contained within yesterday's 1.0848-1.0932 parameters, with a raft of EUR/USD Opex also in focus.

- JPY is the marginal laggard across the majors vs. the USD but sticking to a 147 handle for now. Yesterday's 146.65-148.39 range very much in place, and awaiting impetus from Tokyo CPI.

- NOK inching slight gains vs. the EUR after the Norges Bank stood pat on rates whilst offering some hawkish guidance; next downside target comes via the 16th Jan low at 11.3230.

- PBoC sets USD/CNY mid-point at 7.1044 vs exp. 7.1620 (prev. 7.1053).

Fixed Income

- USTs contained with specifics limited thus far and perhaps given the marked hawkish cross-asset reaction seen after the disappointing 5yr outing on Wednesday.

- Bunds hold a bearish tone; softer German Ifo provided fleeting respite, but Bunds have since reverted back towards their 133.58 trough.

- Gilts continue to exude hawkish action with a fresh 97.57 WTD trough bringing into play 97.43 (8th Dec) & 97.39 (11th Dec) lows.

Commodities

- A firmer session for the crude complex in a continuation of the upside seen yesterday whereby futures settled with gains of USD 0.72/bbl for WTI and USD 0.49/bbl for Brent; currently, Brent (+1.4%) and back above USD 81.00/bbl.

- Precious metals are firmer to varying degrees with horizontal price action for spot gold while spot silver continues grinding higher despite a lack of obvious catalysts; XAU in a narrow USD 2,012.20-2,018.19/oz range. Base metals are also mostly firmer though with the breadth of the market fairly narrow.

- Ukraine hits a Russian oil refinery in Tuapse with drones in operation by SBU agency, via Reuters citing Ukrainian sources; to continue attacking facilities providing fuel for the Russian military.

- China's 2023 gold consumption rose 8.78% Y/Y to 1089.7 tonnes and China's gold output rose 0.84% Y/Y to 375.2 tonnes, according to the Gold Association.

Geopolitics

- US President Biden sent a letter to congressional leaders informing them of his intention to formally notify Congress of the sale of F-16s to Turkey as soon as Ankara completes Sweden's NATO ratification process, while he urged Congress to proceed with the F-16 sale without delay, according to Reuters.

- China's military said it organised troops to follow and monitor a US destroyer that transited through the Taiwan Strait, while it added that the US openly "hyped" up the passage, according to Reuters.

- Taiwan's President-elect Lai said he will continue to defend the cross-strait status quo of peace and stability, while he hopes the US can continue to firmly support Taiwan and hopes US Congress can continue to support Taiwan in bolstering self-defence capabilities.

- Chinese Defence Ministry says US warships and planes have "caused trouble and provocations at China's doorstep" and carried out large-scale high-frequency activities in waters and airspace around China. Says on patrols in the Taiwan Strait, says the PLA continues to train/prepare for war and will continue organising relevant military operations regularly.

US Event Calendar

- 08:30: Jan. Initial Jobless Claims, est. 200,000, prior 187,000

- Jan. Continuing Claims, est. 1.82m, prior 1.81m

- 08:30: 4Q GDP Annualized QoQ, est. 2.0%, prior 4.9%

- Personal Consumption, est. 2.5%, prior 3.1%

- GDP Price Index, est. 2.2%, prior 3.3%

- Core PCE Price Index QoQ, est. 2.0%, prior 2.0%

- 08:30: Dec. Durable Goods Orders, est. 1.5%, prior 5.4%

- Durables-Less Transportation, est. 0.2%, prior 0.4%

- Cap Goods Ship Nondef Ex Air, est. 0%, prior -0.2%

- Cap Goods Orders Nondef Ex Air, est. 0.1%, prior 0.8%

- 08:30: Dec. Wholesale Inventories MoM, est. -0.2%, prior -0.2%

- Dec. Retail Inventories MoM, est. 0%, prior -0.1%

- 08:30: Dec. Advance Goods Trade Balance, est. -$88.7b, prior -$90.3b, revised -$89.3b

- 08:30: Dec. Chicago Fed Nat Activity Index, est. 0.06, prior 0.03, revised 0.01

- 10:00: Dec. New Home Sales, est. 649,000, prior 590,000

- Dec. New Home Sales MoM, est. 10.0%, prior -12.2%

- 11:00: Jan. Kansas City Fed Manf. Activity, est. -3, prior -1

DB's Jim Reid concludes the overnight wrap

Risk assets kept up their positive momentum over the last 24 hours, with the S&P 500 (+0.08%) just about reaching a record high for a 4th consecutive session, whilst US IG spreads fell to their tightest level in over two years. And in turn, Bloomberg’s index of US financial conditions eased to its most accommodative level in the last two years. The latest advance came as US data continued to surprise on the upside, with the January flash PMIs coming in stronger than expected, just as positive earnings releases offered further support. However, the rally began to turn later in the session after a challenging 5-year Treasury auction, which also meant 10yr Treasury yields (+4.7bps) ended the day at their highest level since the December FOMC meeting, at 4.18%. So a mixed but still mostly positive backdrop as we head into today’s ECB meeting.

When it came to yesterday’s flash PMIs, there was good news across the board in the US, with the services PMI up to a 7-month high of 52.9, whilst the manufacturing PMI hit a 15-month high of 50.3. Moreover, the releases contained more positive news on the inflation side, since the output prices component in the services PMI fell to its lowest since May 2020, so that offered more evidence that a soft landing could still be achieved. Looking outside the US, there were further signs of improvement, as the UK composite PMI hit a 7-month high of 52.5, and even though the Euro Area composite PMI was still in contractionary territory, it did hit a 6-month high of 47.9.

That data offered a sizeable boost to markets, which were further supported by several earnings releases. In particular, the Euro Stoxx 50 (+2.20%) hit its highest level since 2001 thanks to surges from ASML (+9.72%) and SAP (+7.63%) after their earnings results, and there was a record high for the DAX (+1.58%) as well. Back in the US, the S&P 500 had been trading +0.8% up on the day shortly after the European close, but sentiment softened during the US afternoon, with the index only just eking out another record by the close (+0.08%). Big tech stocks led the way again, with a +0.89% gain for the Magnificent 7, while the Philadelphia semiconductor index advanced +1.54% amidst the strong results from ASML. That said, a key point of caution is that this remains an unusually narrow rally. Only 28% of the S&P 500 constituents moved higher yesterday, with the equal-weighted S&P 500 down -0.54% on the day. So the equal-weighted index is now down -1.24% since the start of the year, even as the overall S&P 500 has hit successive records.

After the US market close, we saw Tesla’s results miss earnings and revenue expectations for Q4, with the company also warning that 2024 volume growth may be “notably lower” than last year. Its shares fell as much as 6% in after-market trading. By contrast, shares of IBM gained more than 6% in extended trading as it issued an upbeat outlook for 2024 revenue and free cash flow. Overnight, US stock futures are struggling to gain traction with those on the S&P 500 (+0.01%) basically flat ahead of today’s Q4 GDP report.

As mentioned at start, the trigger for the negative turn in US equities was a weak 5yr Treasury auction. The bonds were issued 2.0bps above the when-issued yield, and the bid-to-cover ratio and share of primary dealer take up were the lowest and highest respectively for a 5yr auction since September 2022. The auction results boosted the Treasury selloff that started after the strong flash PMI data, and the 10yr yield (+4.7bps) ended the day at 4.18%, which is its highest level since the Fed’s last meeting in December. The 2yr yield also rose by +1.0bps as the size of Fed rate cuts priced by the December meeting declined by -4.3bps to 132bps, the fewest so far in 2024. It was a similar story for gilts, with yields on 2yr gilts (+4.0bps) and 10yr gilts (+2.4bps) at their highest level in over a month. However in the Euro Area, the ongoing contraction in the PMIs meant that sovereign bonds had a better performance, with yields on 10yr bunds (-1.0bps), OATs (-0.8bps) and BTPs (-1.6bps) all moving lower.

Looking forward, the focus will be back on central banks today, as the ECB are announcing their latest policy decision. It’s widely expected that there’ll be no change in rates today, so the bigger question will be what they signal about any cuts at future meetings. In their preview (link here), our European economists are not expecting a change in messaging, and they expect President Lagarde to repeat that it’s too soon for the ECB to lower its guard on inflation. That said, investors still see a 64% chance of a cut by the April meeting, so it’ll be interesting to see if there’s any weight given to the idea they could cut that soon.

Otherwise from central banks, the main headline yesterday was from the Bank of Canada, which left rates unchanged again. In addition, Governor Macklem said that “there was a clear consensus to maintain our policy rate at 5%, and that the “discussion about future policy is shifting from whether monetary policy is restrictive enough to how long to maintain the current restrictive stance”. So this echoes what we’ve seen elsewhere, with central banks keeping rates on hold for the time being rather than raising them. In turn, markets interpreted that in a dovish light, and the Canadian dollar was the weakest-performing G10 currency yesterday, down -0.47% against the US Dollar.

Overnight in Asia, equities have got some fresh momentum after fresh stimulus announcements from China. That included the news that the reserve requirement ratio will be lowered by 50bps on February 5, along with other measures. In turn, that’s supported substantial gains this morning, with the Shanghai Composite up by +2.59% currently, which leaves it on track for its best daily performance since November 2022. Separately, there’ve also been gains for the Hang Seng (+1.89%) and the CSI 300 (+1.63%), although the Nikkei (+0.11%) and the KOSPI (-0.04%) have struggled to gain much traction this morning. Separately in Japan, 10yr government bond yields (+3.1bps) rose to a 6-week high of 0.74% after weak demand in a 40-year auction.

In other overnight news, the Fed raised the interest rate it will charge banks on the BTFP liquidity facility it launched during the banking stress last March. It also confirmed that the facility will not be extended beyond March, in line with earlier comments by Fed officials. The change will eliminate the arbitrage that banks have been able to take advantage of as rates cuts got priced, due to BTFP borrowing being priced off the 1y OIS rate.

To the day ahead now, and the main highlight will be the ECB’s monetary policy decision, and President Lagarde’s press conference. Data releases from the US include the advance reading of Q4 GDP, along with the weekly initial jobless claims and new home sales for December. Meanwhile in Germany, there’s the Ifo Institute’s business climate indicator for January. Finally, earnings releases include Visa, Intel and LVMH.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Wealth Inequality by Age in the Post‑Pandemic Era

Is the biotech market rally real? Data suggest comeback in private, public markets

Mortgage rates fall as labor market normalizes

People Who Received Ivermectin Were Better Off, Study Finds

Interest rates, the best it gets. It’s time to deploy cash

COVID-19 May Lead To Persistent Cognitive Impairment, Brain Fog, And Lower IQ Scores

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 day ago

International1 day agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges