Uncategorized

Why crypto remittance companies are flocking to Mexico

Mexico has a burgeoning crypto remittance market that has immense potential.

Mexico is the second-largest recipient of remittances…

Share this:

Mexico has a burgeoning crypto remittance market that has immense potential.

Mexico is the second-largest recipient of remittances in the world, according to 2021 World Bank statistics. Remittances to the nation jumped to a record $5.3 billion in July, which is a 16.5% increase year-over-year compared to the same period last year. The steady growth presents myriad opportunities for fintech companies.

Not surprisingly, droves of crypto companies are setting up shop in Mexico to claim a share of the burgeoning remittance market.

Over the past year alone, about half a dozen crypto giants, including Coinbase, have set up operations in the country.

In February, Coinbase unveiled a crypto transfer service tailored to United States-based clients looking to send crypto remittances to Mexico. The product enabled recipients in Mexico to withdraw their money in pesos.

Other companies have since joined the foray. In August, the Malaysia-based Belfrics digital currency exchange announced plans to open crypto transfer operations in Mexico. According to the published communique, the firm will start by launching blockchain wallet and remittance service solutions.

Another notable company that is jostling for a share of the Mexican crypto remittance market is Tether. In May, the crypto company launched the MXNT stablecoin, which is pegged to the Mexican peso. According to the enterprise, the collateralized digital currency will help customers to navigate volatility and use cryptocurrencies as a store of value.

Besides the new entrants, local Mexican crypto companies such as Bitso, which is one of the largest crypto exchanges in the Latin American nation, are already making moves to enhance their reach in an increasingly competitive market.

In November 2021, the Mexican firm established an alliance with U.S.-based Circle Solutions. The collaboration allowed the agency to use Circle’s payment system to facilitate U.S.-to-Mexico crypto remittances.

Cointelegraph had the opportunity to speak with Eduardo Cruz, head of business operations and enterprise solutions at Bitso, about the factors driving the crypto remittance trend in Mexico. He cited high bank transaction costs, slow settlement times and the lack of access to banking facilities as some of the factors pushing the masses toward crypto remittances.

He also highlighted recent alliances that have helped Mexican crypto companies bring crypto remittance services closer to nationals around the world, thereby boosting their adoption.

“For example, Bitso’s clients such as Africhange, which recently integrated Canada–Mexico crypto-powered remittance services to Bitso, and Everest, which enables remittances from the United States, Europe and Singapore into Mexico, are offering a cheaper and faster way to send money to Mexico,” he said.

Factors driving the Mexican crypto remittance sector

One of the biggest factors driving the Mexican crypto remittance sector today is the huge Mexican population residing in the diaspora. Presently, the U.S. and Canada have the highest number of Mexican immigrants.

According to data released by the U.S. Census Bureau in 2020, there are approximately 62.1 million Hispanic people residing in the U.S. today, with Mexicans comprising 61.6% of this population.

Going by 2021 numbers, money sent to Mexico from the U.S. accounted for about 94.9% of all remittances, while Mexicans residing in Canada sent $231 million in the second quarter of 2022.

In a nutshell, the rising number of Mexicans migrating to the U.S. and Canada is pushing remittances to new levels, and the high demand is spilling over to the crypto payments industry.

The decline of the Mexican peso and the emergence of a strong dollar have also contributed to the spike in remittances over the past couple of years.

Recent: Smart contract-enabled insurance holds promise, but can it be scaled?

This phenomenon has occurred in previous crises, such as the 2008 financial crisis, which plunged the Mexican economy into turmoil. In times like this, Mexican institutions and investors usually tend to seek refuge in the greenback, which typically has a higher buying power.

In March 2020, when coronavirus lockdowns began, the U.S. dollar’s purchasing power jumped by approximately 30% in Mexico. At the same time, the average remittance transfer to Mexico increased from $315 to $343.

Today, the availability of dollar-pegged cryptocurrencies allows Mexicans living in the diaspora to leverage the heightened buying power of the USD to make investments and purchases in their home country, hence the higher remittance rates.

Greater convenience

Blockchain technology eliminates third-party mediators from transaction processes, which leads to lower transaction costs and less time used when undertaking remittance transactions.

Cointelegraph caught up with Structure.fi president and co-founder Bryan Hernandez to discuss the impact of these factors on the Mexican remittance market. His company operates a mobile trading platform that gives investors exposure to traditional and crypto financial markets:

“Crypto businesses see a huge opportunity here to streamline (conventional money transfer) processes using blockchain technology. Using crypto, cross-border payments can be made directly with little or no fees instantaneously.”

In Mexico, many financial institutions are also located far away from rural areas, and this makes it hard for the locals to access financial services. Crypto remittance solutions are beginning to close this gap by enabling citizens in such areas to access their money without having to travel long distances.

Moreover, they are able to serve the unbanked. As things stand, over 50% of Mexicans lack a bank account. This makes crypto remittance solutions convenient for citizens in this demographic, as all that’s needed to receive funds is a crypto wallet address.

Another reason why more Mexicans are embracing the crypto remittance fad is their distrust of banks. Mexicans living in the diaspora are sometimes subjected to redlining practices, and this has led to more people using crypto remittance solutions.

Dmitry Ivanov, chief marketing officer at CoinsPaid — a crypto payments firm — told Cointelegraph that the wider use of crypto remittance networks in Mexico was bound to boost adoption overall.

“The clear advantage of digital currencies is what is paving the way for their broad-based adoption in the country and the Latin American world as a whole,” he said, adding:

“The benefits derived from digital currencies have made Mexicans see how exploitative banks have been thus far with their charges, and the general comparative inefficiency has made them distrust traditional financial institutions in general. With a little more regulatory push, the country’s remittance inflow may be dominated by cryptocurrencies.”

A few hurdles

Blockchain remittance solutions provide a raft of important benefits to Mexican users, such as fast transfers and lower transaction fees.

However, they have to overcome some fundamental challenges to dominate the cross-border payments market. The technical nature of crypto platforms, and limited local currency withdrawal options, for example, present some unique challenges that are likely to slow down adoption.

Mexican citizens also still prefer using cash to make payments. According to the 2021 McKinsey Global Payments Report, Mexico was ranked top among countries projected to have high cash usage over the next couple of years.

Recent: To HODL or have kids? The IVF Bitcoin Babies paid for with BTC profits

The research report forecasts that consumer cash payments will account for about 81.5% of all transactions in Mexico by 2025.

This presents a major hurdle for crypto adoption in the country, despite rising crypto remittance figures.

Going forward, it will be interesting to see how the tech-savvy and crypto evangelists navigate the challenges facing adoption and take advantage of the momentum provided by the growing remittances industry.

bitcoin blockchain crypto btc coronavirus currencies cryptoUncategorized

Q4 Update: Delinquencies, Foreclosures and REO

Today, in the Calculated Risk Real Estate Newsletter: Q4 Update: Delinquencies, Foreclosures and REO

A brief excerpt: I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened followi…

Share this:

A brief excerpt:

I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble). The two key reasons are mortgage lending has been solid, and most homeowners have substantial equity in their homes..There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ mortgage rates real estate mortgages pandemic interest rates

...

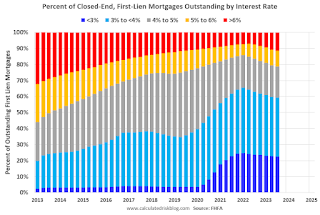

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023 (Q4 2023 data will be released in a two weeks).

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 22.6% of loans are under 3%, 59.4% are under 4%, and 78.7% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

Uncategorized

‘Bougie Broke’ – The Financial Reality Behind The Facade

‘Bougie Broke’ – The Financial Reality Behind The Facade

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Social media users claiming…

Share this:

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive restaurants. Yet they complain about living paycheck to paycheck and lacking the means to support their lifestyle.

Bougie broke is like “keeping up with the Joneses,” spending beyond one’s means to impress others.

Bougie Broke gives us a glimpse into the financial condition of a growing number of consumers. Since personal consumption represents about two-thirds of economic activity, it’s worth diving into the Bougie Broke fad to appreciate if a large subset of the population can continue to consume at current rates.

The Wealth Divide Disclaimer

Forecasting personal consumption is always tricky, but it has become even more challenging in the post-pandemic era. To appreciate why we share a joke told by Mike Green.

Bill Gates and I walk into the bar…

Bartender: “Wow… a couple of billionaires on average!”

Bill Gates, Jeff Bezos, Elon Musk, Mark Zuckerberg, and other billionaires make us all much richer, on average. Unfortunately, we can’t use the average to pay our bills.

According to Wikipedia, Bill Gates is one of 756 billionaires living in the United States. Many of these billionaires became much wealthier due to the pandemic as their investment fortunes proliferated.

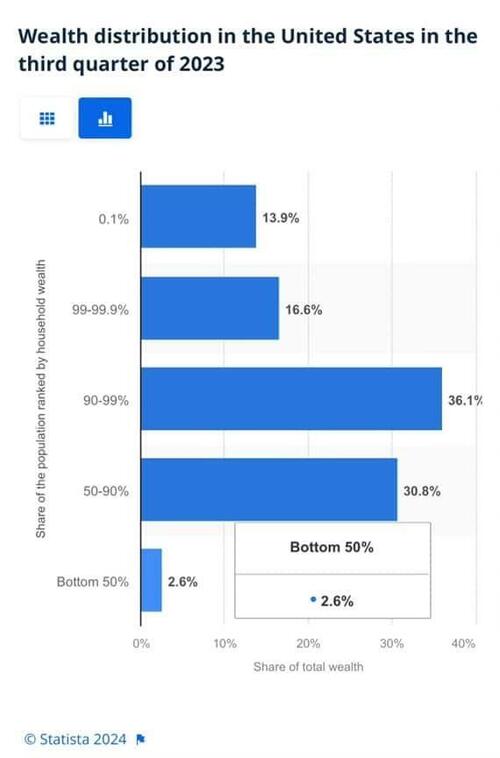

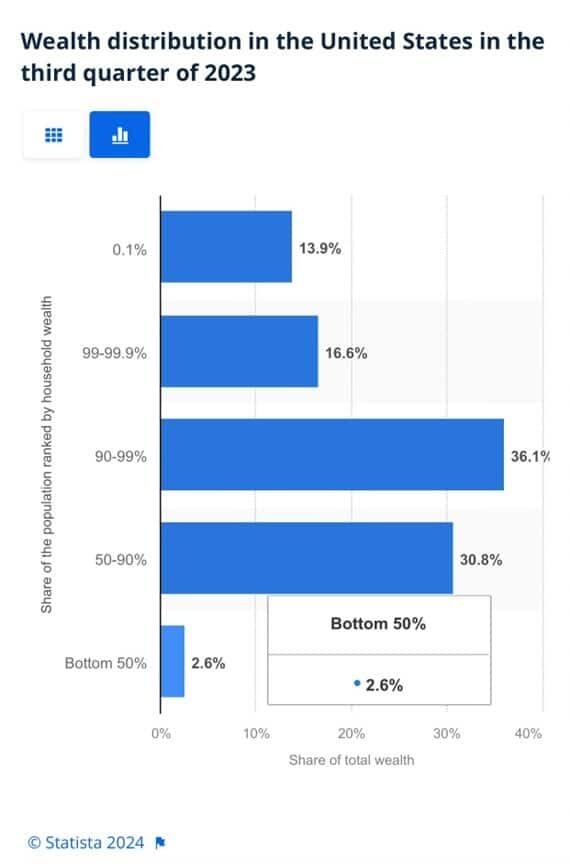

To appreciate the wealth divide, consider the graph below courtesy of Statista. 1% of the U.S. population holds 30% of the wealth. The wealthiest 10% of households have two-thirds of the wealth. The bottom half of the population accounts for less than 3% of the wealth.

The uber-wealthy grossly distorts consumption and savings data. And, with the sharp increase in their wealth over the past few years, the consumption and savings data are more distorted.

Furthermore, and critical to appreciate, the spending by the wealthy doesn’t fluctuate with the economy. Therefore, the spending of the lower wealth classes drives marginal changes in consumption. As such, the condition of the not-so-wealthy is most important for forecasting changes in consumption.

Revenge Spending

Deciphering personal data has also become more difficult because our spending habits have changed due to the pandemic.

A great example is revenge spending. Per the New York Times:

Ola Majekodunmi, the founder of All Things Money, a finance site for young adults, explained revenge spending as expenditures meant to make up for “lost time” after an event like the pandemic.

So, between the growing wealth divide and irregular spending habits, let’s quantify personal savings, debt usage, and real wages to appreciate better if Bougie Broke is a mass movement or a silly meme.

The Means To Consume

Savings, debt, and wages are the three primary sources that give consumers the ability to consume.

Savings

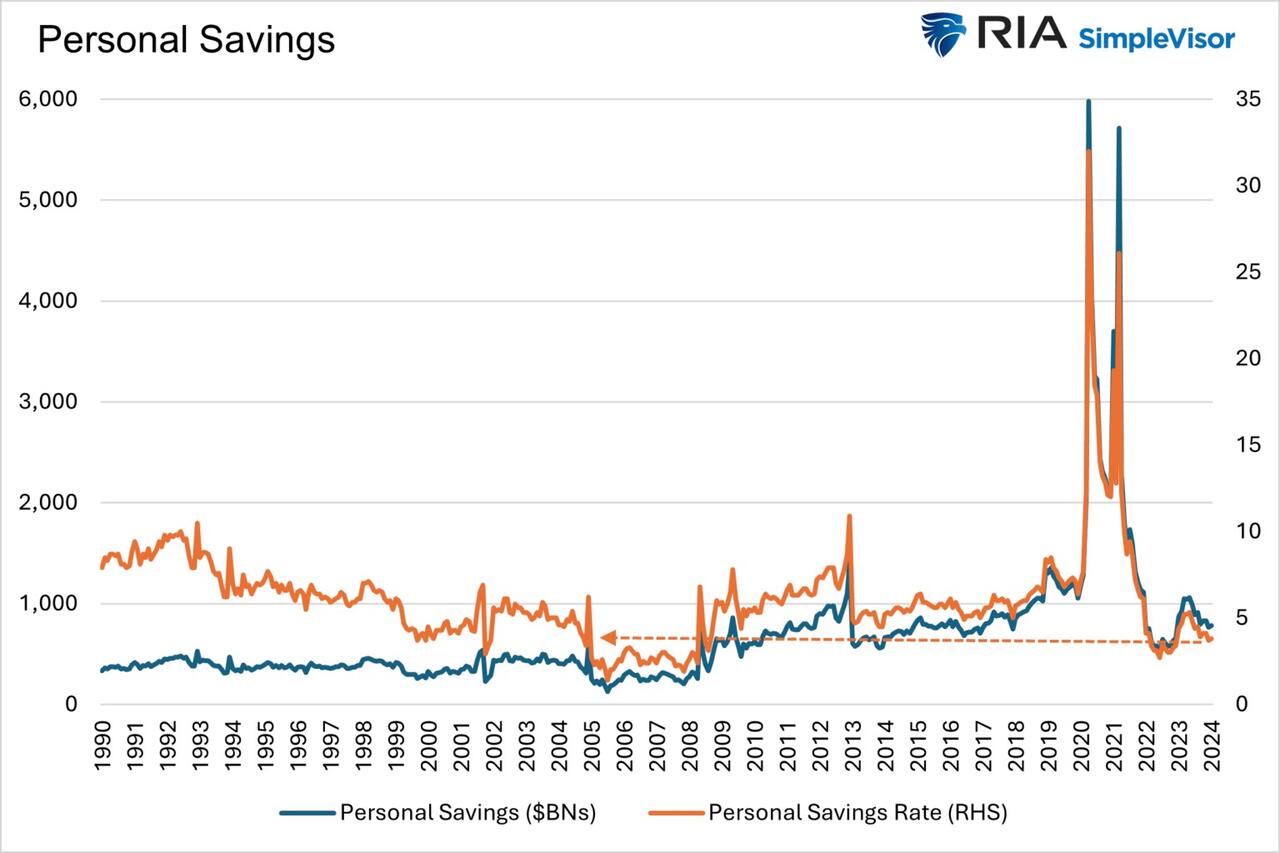

The graph below shows the rollercoaster on which personal savings have been since the pandemic. The savings rate is hovering at the lowest rate since those seen before the 2008 recession. The total amount of personal savings is back to 2017 levels. But, on an inflation-adjusted basis, it’s at 10-year lows. On average, most consumers are drawing down their savings or less. Given that wages are increasing and unemployment is historically low, they must be consuming more.

Now, strip out the savings of the uber-wealthy, and it’s probable that the amount of personal savings for much of the population is negligible. A survey by Payroll.org estimates that 78% of Americans live paycheck to paycheck.

More on Insufficient Savings

The Fed’s latest, albeit old, Report on the Economic Well-Being of U.S. Households from June 2023 claims that over a third of households do not have enough savings to cover an unexpected $400 expense. We venture to guess that number has grown since then. To wit, the number of households with essentially no savings rose 5% from their prior report a year earlier.

Relatively small, unexpected expenses, such as a car repair or a modest medical bill, can be a hardship for many families. When faced with a hypothetical expense of $400, 63 percent of all adults in 2022 said they would have covered it exclusively using cash, savings, or a credit card paid off at the next statement (referred to, altogether, as “cash or its equivalent”). The remainder said they would have paid by borrowing or selling something or said they would not have been able to cover the expense.

Debt

After periods where consumers drained their existing savings and/or devoted less of their paychecks to savings, they either slowed their consumption patterns or borrowed to keep them up. Currently, it seems like many are choosing the latter option. Consumer borrowing is accelerating at a quicker pace than it was before the pandemic.

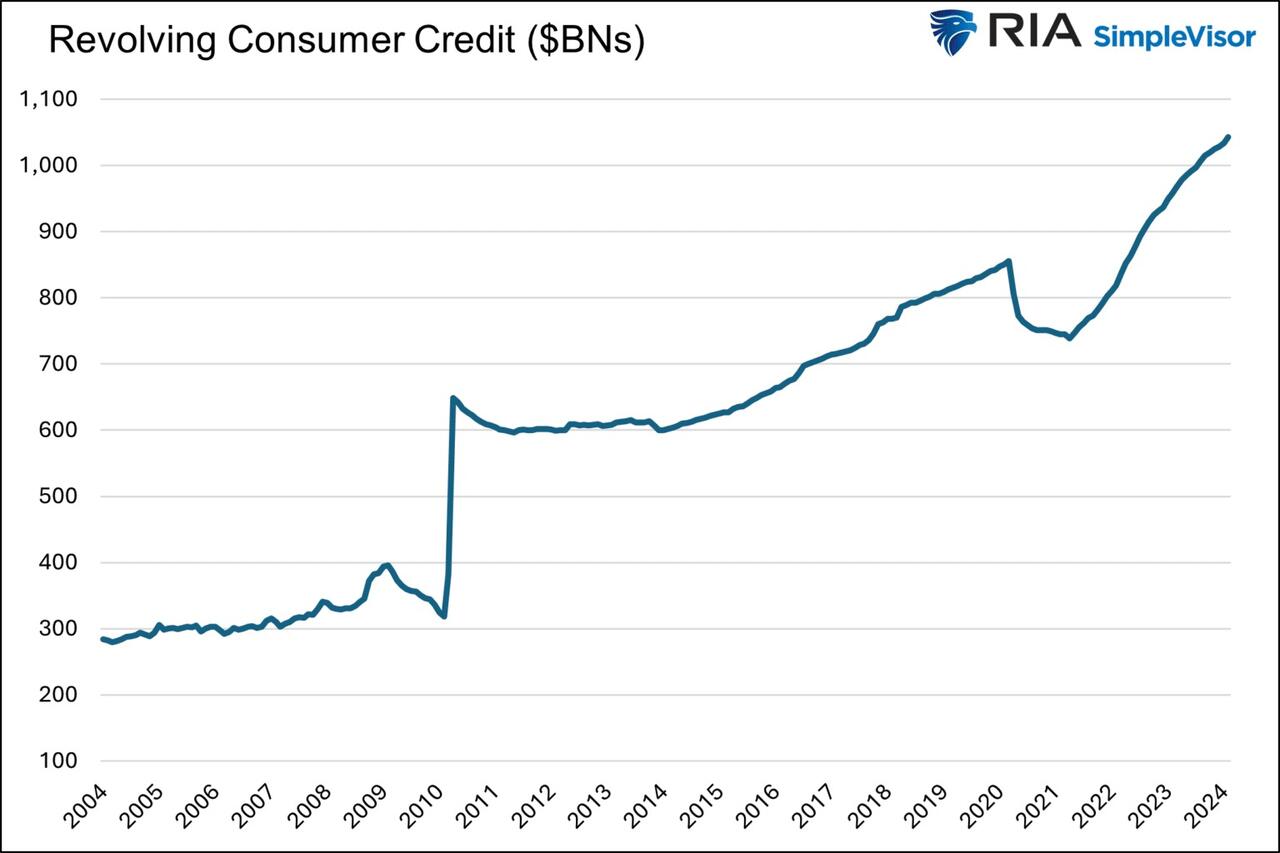

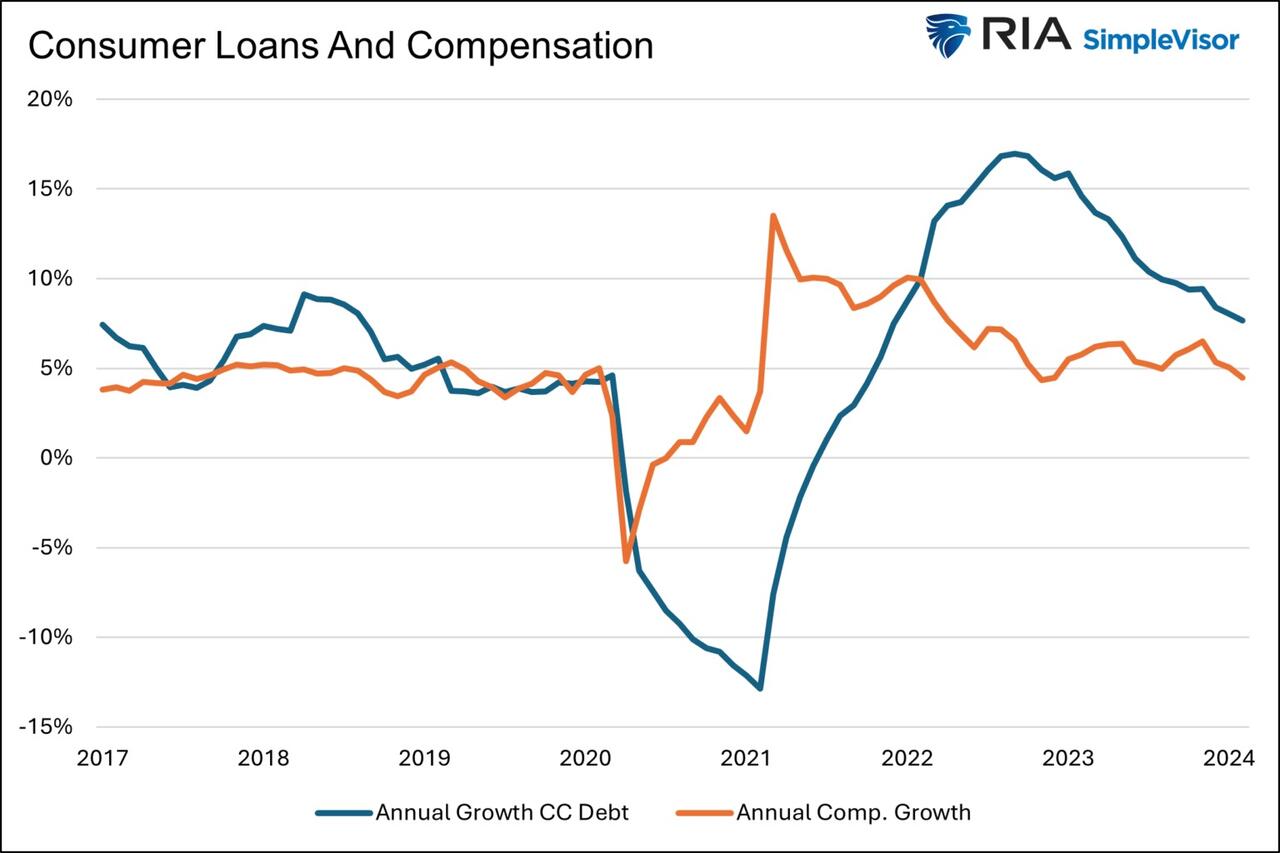

The first graph below shows outstanding credit card debt fell during the pandemic as the economy cratered. However, after multiple stimulus checks and broad-based economic recovery, consumer confidence rose, and with it, credit card balances surged.

The current trend is steeper than the pre-pandemic trend. Some may be a catch-up, but the current rate is unsustainable. Consequently, borrowing will likely slow down to its pre-pandemic trend or even below it as consumers deal with higher credit card balances and 20+% interest rates on the debt.

The second graph shows that since 2022, credit card balances have grown faster than our incomes. Like the first graph, the credit usage versus income trend is unsustainable, especially with current interest rates.

With many consumers maxing out their credit cards, is it any wonder buy-now-pay-later loans (BNPL) are increasing rapidly?

Insider Intelligence believes that 79 million Americans, or a quarter of those over 18 years old, use BNPL. Lending Tree claims that “nearly 1 in 3 consumers (31%) say they’re at least considering using a buy now, pay later (BNPL) loan this month.”More telling, according to their survey, only 52% of those asked are confident they can pay off their BNPL loan without missing a payment!

Wage Growth

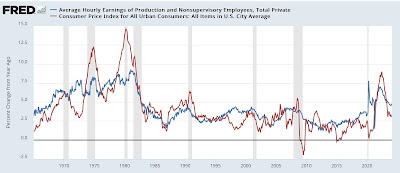

Wages have been growing above trend since the pandemic. Since 2022, the average annual growth in compensation has been 6.28%. Higher incomes support more consumption, but higher prices reduce the amount of goods or services one can buy. Over the same period, real compensation has grown by less than half a percent annually. The average real compensation growth was 2.30% during the three years before the pandemic.

In other words, compensation is just keeping up with inflation instead of outpacing it and providing consumers with the ability to consume, save, or pay down debt.

It’s All About Employment

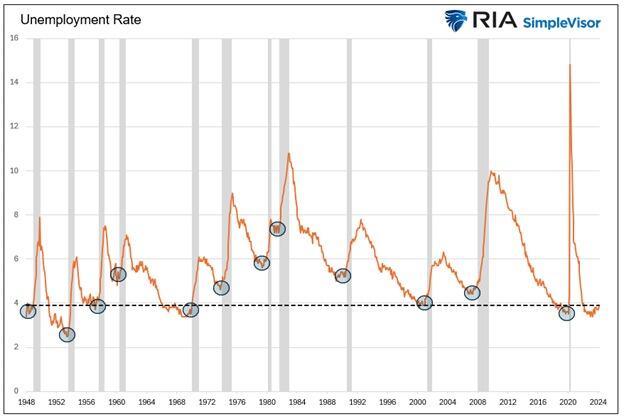

The unemployment rate is 3.9%, up slightly from recent lows but still among the lowest rates in the last seventy-five years.

The uptick in credit card usage, decline in savings, and the savings rate argue that consumers are slowly running out of room to keep consuming at their current pace.

However, the most significant means by which we consume is income. If the unemployment rate stays low, consumption may moderate. But, if the recent uptick in unemployment continues, a recession is extremely likely, as we have seen every time it turned higher.

It’s not just those losing jobs that consume less. Of greater impact is a loss of confidence by those employed when they see friends or neighbors being laid off.

Accordingly, the labor market is probably the most important leading indicator of consumption and of the ability of the Bougie Broke to continue to be Bougie instead of flat-out broke!

Summary

There are always consumers living above their means. This is often harmless until their means decline or disappear. The Bougie Broke meme and the ability social media gives consumers to flaunt their “wealth” is a new medium for an age-old message.

Diving into the data, it argues that consumption will likely slow in the coming months. Such would allow some consumers to save and whittle down their debt. That situation would be healthy and unlikely to cause a recession.

The potential for the unemployment rate to continue higher is of much greater concern. The combination of a higher unemployment rate and strapped consumers could accentuate a recession.

Uncategorized

The most potent labor market indicator of all is still strongly positive

– by New Deal democratOn Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently…

Share this:

{kind=link}

{kind=link}

- by New Deal democrat

On Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently than not indicated a recession was near or underway. But I concluded by noting that this survey has historically been noisy, and I thought it would be resolved away this time. Specifically, there was strong contrary data from the Establishment survey, backed up by yesterday’s inflation report, to the contrary. Today I’ll examine that, looking at two other series.

{kind=link}

Q4 Update: Delinquencies, Foreclosures and REO

Digital Currency And Gold As Speculative Warnings

Bougie Broke The Financial Reality Behind The Facade

Aging at AACR Annual Meeting 2024

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

The most potent labor market indicator of all is still strongly positive

‘Bougie Broke’ – The Financial Reality Behind The Facade

Bitcoin on Wheels: The Story of Bitcoinetas

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges