Government

Whither “Animal Spirits”?

Whither "Animal Spirits"?

Submitted by Elliott Middleton

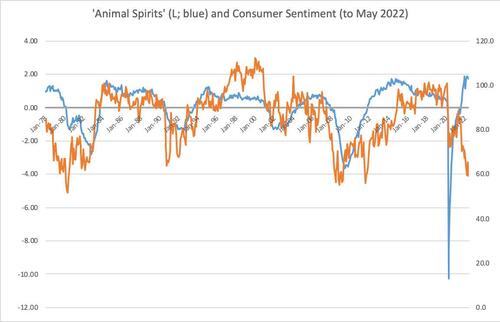

According to the Michigan Consumer Sentiment Series, confidence is at record lows….

Share this:

Submitted by Elliott Middleton

According to the Michigan Consumer Sentiment Series, confidence is at record lows. But a measure of confidence or “animal spirits,” as Keynes called it, that I developed in the 1990s — that was featured on the front page of the Wall Street Journal, February 20, 1998 — is now showing very healthy “animal spirits.” So which one is right?

Only time will tell. Read on to learn more.

In graduate school in the ‘Seventies I became fascinated with the implications of psychology for economics. I had been an English major at Yale as an undergraduate, and found the “psychology” of neoclassical utility theory ridiculous, at least when it came to things like the mood of the markets and consumers. Economics was in the grip of rational expectations theory at this time.

A Stanford economist by the name of Tibor Scitovsky had written a book called The Joyless Economy which explored the implications of adaptation level theory for economics. Our perceptions are always judged in the context of what we have experienced. The legendary Wundt curve showed that the pleasantness of stimuli followed an inverted U-shaped curve with respect to how novel a stimulus is to the subject. Moderate levels of subjective novelty are pleasant; very high levels unpleasant. Scitovsky harped on the then popular theme of the boringness of mass consumption. The importance of subjective novelty is now generally recognized in product design and marketing.

I spent some time on the complicated mathematics of subjective novelty before realizing that, in the majority of instances, some form of moving average of the relevant variable was all you needed to construct a measure of adaptation level, and of current variable value subjective novelty.

I had rediscovered moving averages! Traders feel good when the price is above the moving average, and they start to worry about losses one it veers below.

The next step was to apply this to the macro economy to solve the problem of “animal spirits.” What macro variable did people really care about? Stock prices? No, most people don't own enough stock to worry that much about stock prices. Industrial production? No, only economists are aware of that.

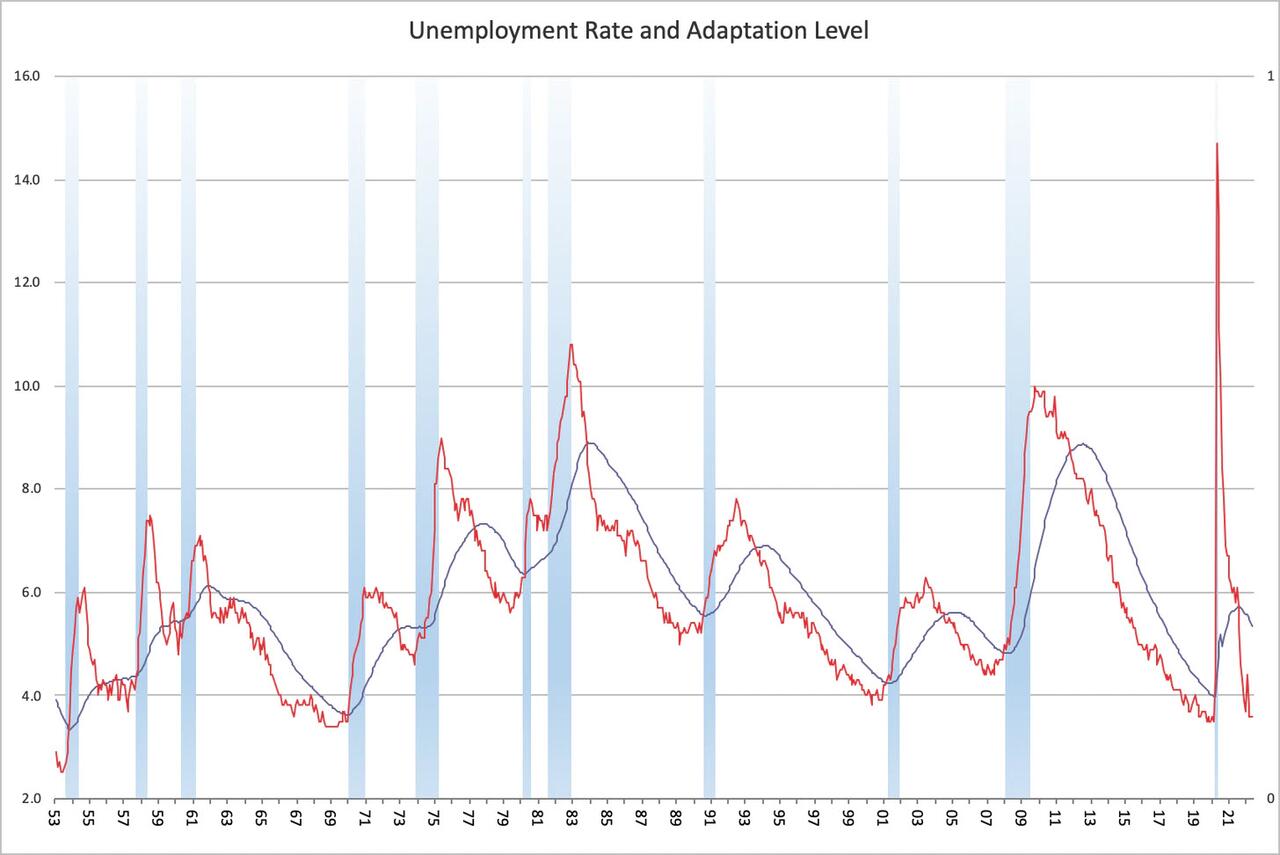

How about the unemployment rate? Given the rather tenuous attachment many people feel they have to their jobs, I thought this was a good candidate variable, sort of a personal unemployment risk indicator. Labor has never had much bargaining power with American business, and in the past few decades what it used to have was decimated.

Elliott Middleton says the main determinant of consumer confidence is the gap between the current unemployment rate of 4.6% and the rate that people consider normal. What's normal, according to Mr. Middleton, a professor at Metropolitan State University in Minneapolis, is a moving average of past unemployment rates, which he puts at about 5.2% now. The 4.6%-to-5.2% gap is what makes people euphoric, he contends, and if that gap closes, if the jobless rate goes above 5%, say, Americans would lose confidence. [https://www.wsj.com/articles/SB887928300124344000]

The recession began in April 2001 with the unemployment rate at 4.4% and adaptation level both at about 4.3%.

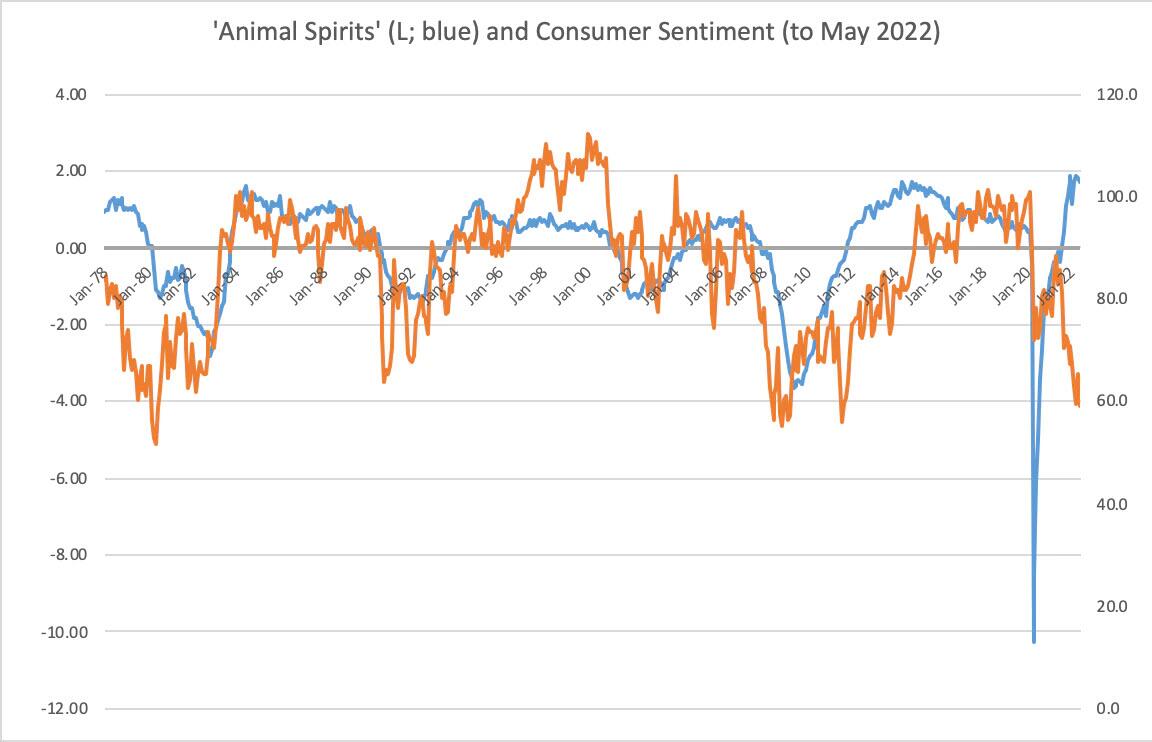

The editor of the European Journal of Economic Psychology had suggested using an exponential moving average whereby more recent observations are weighted more heavily than those more distant in the past; I used an exponential moving average over the past four years. An updated graph of the unemployment rate and adaptation level I proposed in “Adaptation Level and ‘Animal Spirits’” [1] is shown below.

As you can see, whenever the unemployment rate has risen above the adaptation level, a recession has ensued. I am counting the double dip recession in the early 1980s as one instance.

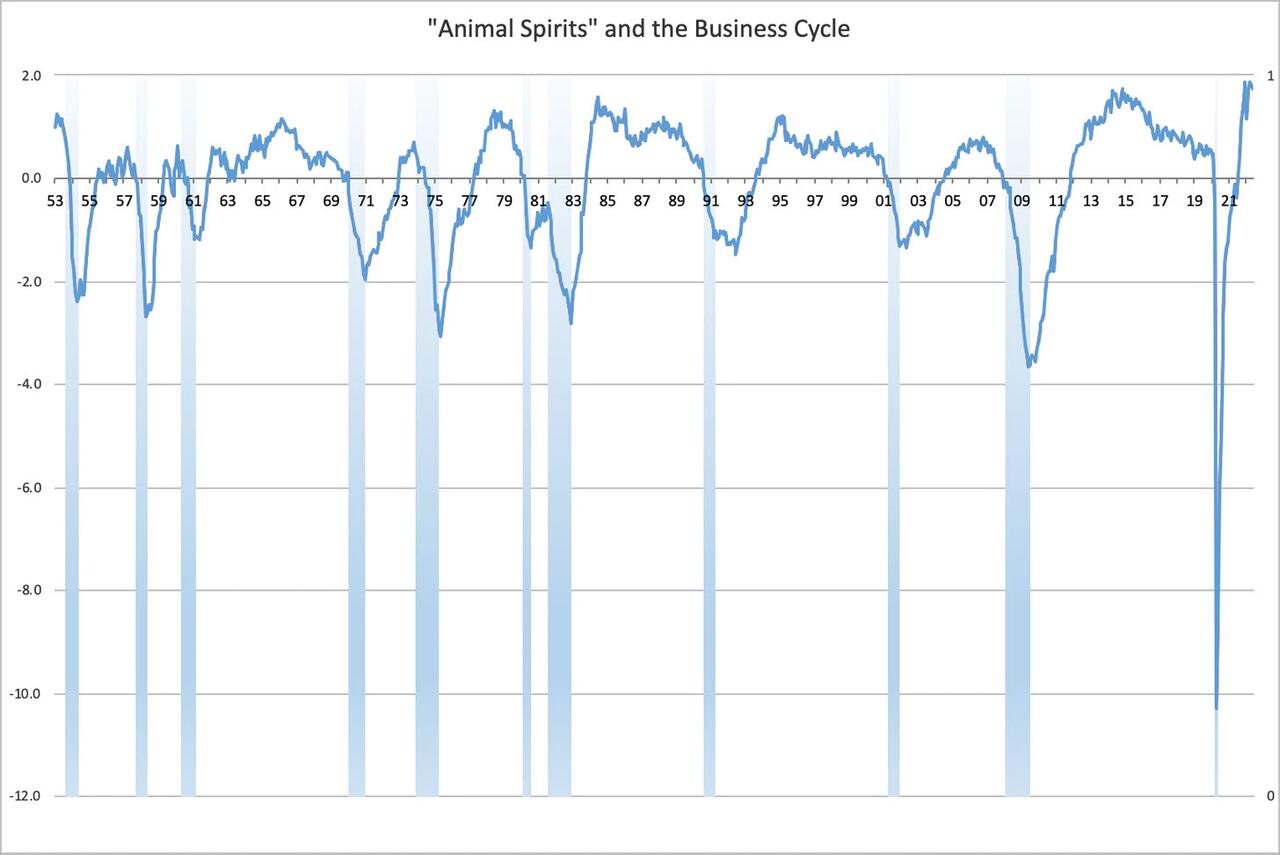

To create an "animal spirits” index I subtracted the unemployment rate from the adaptation level, so if unemployment was below the adaptation level, "animal spirits” would be positive; and conversely if the unemployment rate rose above the adaptation level. I ultimately abandoned attempts to scale this metric by the volatility of unemployment.

Figure 1 also includes the Michigan Sentiment series, showing the current divergence. The two measures track closely, and preliminary causality testing showed causality running from the “animal spirits” metric to the Michigan series.

So what is going on? The labor force participation rate suffered a huge involuntary blow during the pandemic that appears to have contributed to a “great resignation” from the labor force. Other things equal, this lowers the unemployment rate. The massive spike in the unemployment rate to over 14% in 2020, helped to raise the adaptation level, which peaked in the summer of 2021 at 5.7%, and is now at 5.3%, above the unemployment rate of 3.6%.

From the perspective of my model, recession becomes inevitable when the unemployment rate rises above the adaptation level, which is the same as the “animal spirits” index falling below zero. Because confidence is a form of psychological wealth, obeying the neoclassical precept that losses are discounted more steeply then gains, a form of self organized criticality sets in in the psychology of the labor market — as well as in the board rooms where investment decisions are made — and a self-reinforcing downward spiral of consumption and production decisions follows. At some point businesses stop laying off workers; the adaptation level rises to its peak with a lag; and as businesses hire workers back on, the unemployment rate drops below the adaptation level and “animal spirits” (confidence levels) become positive again.

It’s simplistic, but it works, which is why the academic economists have paid it no mind.

The problem facing the policymakers today is keeping the unemployment rate below the adaptation level. If we have a recession, and the unemployment rate jumps two percentage points, it will leap over the adaptation rate, engendering self-organized criticality. Keynes spoke direly about “the state of long-term expectation” as a critical determinant of an economy’s health, of its intrinsic “animal spirits.”

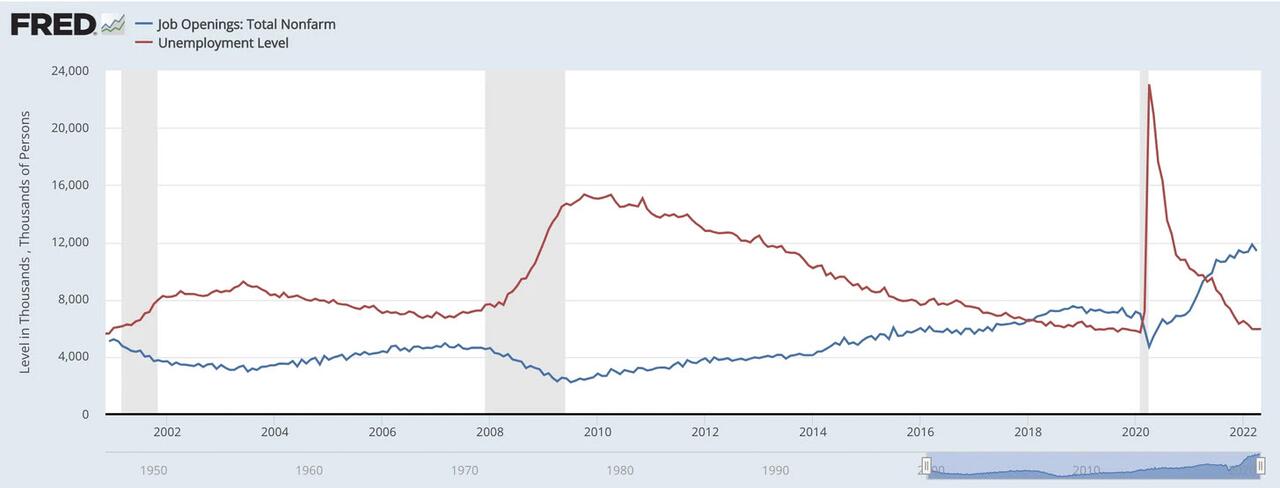

I believe the globalists want the West to give up hope, so we can all be happy owning nothing; that much of current policy is bent on self-destruction. Should the US be lucky enough and wise enough to rebalance national income toward labor with low-tax, hands-off policies for small business, always our greatest job producer, the spurt in domestic demand might be considerable. There are now more job openings than there are unemployed persons!

I believe the firehose of insulting, race-baiting woke propaganda about America emanating from the Democratic Party [CCP/WEF] has the majority of the country profoundly depressed about the prospects for their lives and businesses. This is why the Michigan index is at record lows. These feelings are strongest among small business people who have seen their businesses deemed “non-essential” and subject to termination upon the whim of a bureaucrat. A serious recession now might have very damaging effects on Americans’ long-term expectations.

I’m hoping that Americans are expressing more despair than they are demonstrating economically. Businesses may need to pay them more!

Ultimately, the West must deal with its long-term fiscal position that will involve some sort of bankruptcy negotiation with the rest of the world, that in its turn should also favor a domestic rebalancing to reduce inequalities, but that is another question.

Congress, not just the Fed, has the ability to begin revitalizing the economy with tax reductions on small business and energy production.

And instead of taxing excess profits and giving them to government, which will waste them, why doesn’t Congress require business to share profits with their employees, so they go back into the spending stream and the whole economy grows?

The forecast: the economy will enter recession when the unemployment rate reaches about 4.5%.

However, from psychophysical point of view, “animal spirits” may be stronger than the Michigan index suggests, meaning that appropriate stimulus now might reengage the engine of optimism and forestall the next recession.

[1] Middleton, E., Adaptation level and ‘animal spirits’, JEconPsych, Volume 17, Issue 4, August 1996, Pages 479-498.

International

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

The struggling chain has given up the fight and will close hundreds of stores around the world.

Share this:

It has been a brutal period for several popular retailers. The fallout from the covid pandemic and a challenging economic environment have pushed numerous chains into bankruptcy with Tuesday Morning, Christmas Tree Shops, and Bed Bath & Beyond all moving from Chapter 11 to Chapter 7 bankruptcy liquidation.

In all three of those cases, the companies faced clear financial pressures that led to inventory problems and vendors demanding faster, or even upfront payment. That creates a sort of inevitability.

Related: Beloved retailer finds life after bankruptcy, new famous owner

When a retailer faces financial pressure it sets off a cycle where vendors become wary of selling them items. That leads to barren shelves and no ability for the chain to sell its way out of its financial problems.

Once that happens bankruptcy generally becomes the only option. Sometimes that means a Chapter 11 filing which gives the company a chance to negotiate with its creditors. In some cases, deals can be worked out where vendors extend longer terms or even forgive some debts, and banks offer an extension of loan terms.

In other cases, new funding can be secured which assuages vendor concerns or the company might be taken over by its vendors. Sometimes, as was the case with David's Bridal, a new owner steps in, adds new money, and makes deals with creditors in order to give the company a new lease on life.

It's rare that a retailer moves directly into Chapter 7 bankruptcy and decides to liquidate without trying to find a new source of funding.

Image source: Getty Images

The Body Shop has bad news for customers

The Body Shop has been in a very public fight for survival. Fears began when the company closed half of its locations in the United Kingdom. That was followed by a bankruptcy-style filing in Canada and an abrupt closure of its U.S. stores on March 4.

"The Canadian subsidiary of the global beauty and cosmetics brand announced it has started restructuring proceedings by filing a Notice of Intention (NOI) to Make a Proposal pursuant to the Bankruptcy and Insolvency Act (Canada). In the same release, the company said that, as of March 1, 2024, The Body Shop US Limited has ceased operations," Chain Store Age reported.

A message on the company's U.S. website shared a simple message that does not appear to be the entire story.

"We're currently undergoing planned maintenance, but don't worry we're due to be back online soon."

That same message is still on the company's website, but a new filing makes it clear that the site is not down for maintenance, it's down for good.

The Body Shop files for Chapter 7 bankruptcy

While the future appeared bleak for The Body Shop, fans of the brand held out hope that a savior would step in. That's not going to be the case.

The Body Shop filed for Chapter 7 bankruptcy in the United States.

"The US arm of the ethical cosmetics group has ceased trading at its 50 outlets. On Saturday (March 9), it filed for Chapter 7 insolvency, under which assets are sold off to clear debts, putting about 400 jobs at risk including those in a distribution center that still holds millions of dollars worth of stock," The Guardian reported.

After its closure in the United States, the survival of the brand remains very much in doubt. About half of the chain's stores in the United Kingdom remain open along with its Australian stores.

The future of those stores remains very much in doubt and the chain has shared that it needs new funding in order for them to continue operating.

The Body Shop did not respond to a request for comment from TheStreet.

bankruptcy pandemic canadaGovernment

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

{kind=link}

{kind=link}

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

{kind=link}

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

Low Iron Levels In Blood Could Trigger Long COVID: Study

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

Angry Shouting Aside, Here’s What Biden Is Running On

Jack Smith Says Trump Retention Of Documents “Starkly Different” From Biden

Walmart joins Costco in sharing key pricing news

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex