From Sinatra to Katy Perry, celebrities have long sung about the power of a smile – how it picks you up, changes your outlook, and generally makes you feel better. But is it all smoke and mirrors, or is there a scientific backing to the claim?

Groundbreaking research from the University of South Australia confirms that the act of smiling can trick your mind into being more positive, simply by moving your facial muscles.

With the world in crisis amid COVID-19, and alarming rises of anxiety and depression in Australia and around the world, the findings could not be more timely.

The study, published in Experimental Psychology, evaluated the impact of a covert smile on perception of face and body expressions. In both scenarios, a smile was induced by participants holding a pen between their teeth, forcing their facial muscles to replicate the movement of a smile.

The research found that facial muscular activity not only alters the recognition of facial expressions but also body expressions, with both generating more positive emotions.

Lead researcher and human and artificial cognition expert, UniSA’s Dr Fernando Marmolejo-Ramos says the finding has important insights for mental health.

“When your muscles say you’re happy, you’re more likely to see the world around you in a positive way,” Dr Marmolejo-Ramos says.

“In our research we found that when you forcefully practise smiling, it stimulates the amygdala – the emotional centre of the brain – which releases neurotransmitters to encourage an emotionally positive state.

“For mental health, this has interesting implications. If we can trick the brain into perceiving stimuli as ‘happy’, then we can potentially use this mechanism to help boost mental health.”

The study replicated findings from the ‘covert’ smile experiment by evaluating how people interpret a range of facial expressions (spanning frowns to smiles) using the pen-in-teeth mechanism; it then extended this using point-light motion images (spanning sad walking videos to happy walking videos) as the visual stimuli.

Dr Marmolejo-Ramos says there is a strong link between action and perception.

“In a nutshell, perceptual and motor systems are intertwined when we emotionally process stimuli,” Dr Marmolejo-Ramos says.

“A ‘fake it ’til you make it’ approach could have more credit than we expect.”

###

NOTES TO EDITORS:

1-2 second video of point-light biological walking stimuli and emotional faces stimuli is available here: https://figshare.com/articles/media/stimuli/10269815

David Baker’s lab shows generative AI can design antibodies. But are they good enough to become drugs?

The promise of using artificial intelligence to design biologic drugs from scratch is starting to look a lot less abstract.

This week, scientists led by…

The promise of using artificial intelligence to design biologic drugs from scratch is starting to look a lot less abstract.

This week, scientists led by David Baker at the University of Washington revealed work showing that they have created therapeutically active proteins from scratch. Using the lab’s generative AI model they created an antibody that neutralizes a bacterial toxin and three that target the viruses responsible for Covid-19, RSV and the flu.

The study, which was posted Monday on bioRxiv and has not been peer-reviewed, showcases the potential power of using AI to make antibodies that target proteins just as their designers intended, rather than trawling through the blood of mice or humans in hopes of finding just the right one.

Yet it also suggests that AI-designed antibodies aren’t yet good enough to pass muster as drugs, at least not at the touch of a button. Scientists not involved in the study told Endpoints News that the work was a step in the right direction, but said the antibodies didn’t stick strongly enough to their targets to become real drug candidates, a point that Baker conceded.

“They’re just too weak for primetime,” Baker told Endpoints in an interview. “I think this is showing what the way of the future is going to be. But these things are not yet tight enough to be used as drugs.”

Making antibodies entirely on computers could become one of the most useful and lucrative applications of the growing de novo protein design field, in which scientists generate proteins never before seen in nature. While Baker’s Institute for Protein Design in Seattle has created other binding proteins before, they were simpler and more alien than the standard antibodies that pharma companies know and love.

Baker’s new preprint shows how his lab’s software, called RFdiffusion, can generate the structures of antibodies that mesh neatly with a specific surface on a bacterial or viral protein. It suggests that AI could help target the Achilles heel of such proteins. “Normally, you can’t really control that,” Baker said. “But in our approach, you specify where on the target you want to bind.”

When the lab tested its antibodies on the viral proteins and used high-powered microscopes to see the results, the structures and interactions were “basically identical” to what their computer program predicted, Baker said. “That was the wow moment.”

Big investments and blockbuster dreams

Many of biopharma’s best-selling drugs are antibodies, and the race is on to tap the AI technologies underpinning text and image generators like ChatGPT to create antibodies. Generate:Biomedicines, an AI startup just outside of Boston, has raised nearly $750 million to make therapeutic proteins, with an initial focus on antibodies. Absci, BigHat Biosciences, and Nabla Bio are also focused on making antibodies with AI.

Nicholas Polizzi

“Deep learning is making previously difficult design problems now tractable,” Nicholas Polizzi, a protein scientist at Dana-Farber Cancer Institute told Endpoints in an email. But like many problems in using AI for biology, “we are running up against a wall of not-enough-training-data,” he said.

The four targets chosen for Baker’s paper weren’t especially tough nuts to crack, since there are already many existing antibodies for those bacteria and viruses. Polizzi noted that the antibodies also targeted surfaces of those proteins for which strong binders already exist, a lower-hanging fruit than targeting a novel surface.

But Baker said that the structures of the antibodies were different enough from existing ones found in the Protein Data Bank — used as the training source for RFdiffusion — that he’s confident the model is coming up with new solutions and not just regurgitating what it’s been fed.

In addition to improving the AI model to make better antibodies, the lab is also working towards making antibodies against more difficult drug targets. Although RFdiffusion is open source, he also wants to make an easier-to-use text interface where scientists can ask the program to generate the amino acid sequence of an antibody that binds to specific sites of a protein.

“We’re not there yet,” Baker said. “But I don’t think we’re far away.”

Visionary $15 million gift from Wayne & Wendy Holman to NYU Langone Health ensures continued excellence in newly named Holman Division of Endocrinology, Diabetes & Metabolism

NYU Langone Health has received a $15 million gift from innovators and philanthropists Wayne G. Holman, MD, and Wendy Holman to further elevate the world-class…

NYU Langone Health has received a $15 million gift from innovators and philanthropists Wayne G. Holman, MD, and Wendy Holman to further elevate the world-class treatment and study of endocrine disorders in the newly named and endowed Holman Division of Endocrinology, Diabetes & Metabolism.

Credit: Mateo Salcedo / NYU Langone Health

NYU Langone Health has received a $15 million gift from innovators and philanthropists Wayne G. Holman, MD, and Wendy Holman to further elevate the world-class treatment and study of endocrine disorders in the newly named and endowed Holman Division of Endocrinology, Diabetes & Metabolism.

“Wayne and Wendy’s generosity in this important area of medicine will help NYU Langone further enhance our exceptional research, education and clinical care within the Holman Division of Endocrinology, Diabetes & Metabolism,” said Robert I. Grossman, MD, dean and CEO, NYU Langone. “NYU Langone has a rich history of developing novel treatment options to provide superior outcomes for the most complex cases, and thanks to this endowment, we can sustain these efforts over time.”

“This impactful gift will propel the division into its next phase of growth by establishing new translational research, clinical trials, academic forums, and advancing clinical care, among other initiatives,” said Steven Abramson, MD, Frederick H. King Professor of Internal Medicine and chair of the Department of Medicine at NYU Grossman School of Medicine. “I am excited for the medical advances that will undoubtedly come about because of the Holmans’ deep investment.”

The Holman Division of Endocrinology, Diabetes, & Metabolism, part of the Department of Medicine at NYU Grossman School of Medicine, is among the best in the country, ranked No. 2 U.S. News & World Report’s specialty rankings for 2023-24. The division’s robust research program has made major contributions to the studies of diabetes care, thyroid disease, obesity, neuroendocrinology, lipid disorders, and bone health.

Dr. Holman was recently elected to NYU Langone’s Board of Trustees. His gift is the largest ever given to the NYU Grossman School of Medicine by an alumnus.

“NYU Langone and its medical school gave me the gifts of knowledge, experience, and lifelong friendships. Wendy and I are happy to give back by supporting the dedicated and innovative researchers, physicians, and caregivers in the Holman Division of Endocrinology, Metabolism, and Diabetes who care for patients and advance work toward new treatments and cures,” said Dr. Holman. “We look forward to the achievements. Many thanks to those working so hard on these endeavors.”

For more than 18 years, Dr. Holman has served as founder and CEO of Ridgeback Capital, a private investment firm focusing on the life sciences. Dr. Holman’s work at Ridgeback Capital has provided funding to companies that have developed medicines for various cancers, infectious diseases, rare pediatric diseases, and more. In 2016, the Holmans founded Ridgeback Biotherapeutics, a biotech company focused on developing life-saving medications to treat diseases with limited or no treatment options. Ridgeback Biotherapeutics has brought two medicines—for Ebola and COVID-19—to regulatory approvals around the world. For decades, Dr. Holman and Mrs. Holman have leveraged their own success to help vulnerable populations, facilitating drug research and development at over a hundred biopharmaceutical companies.

“Wayne and I are happy to support advancements in collaboration with NYU Langone that will have a tangible positive effect on health and alleviate human suffering,” said Mrs. Holman. “We are confident the division will continue to make a significant impact on the field and benefit countless individuals, and we are proud to be part of that.”

“Wendy and Wayne are people who have dedicated every aspect of their lives to helping others. They see NYU Langone as an institution with the ability to magnify every dollar, and through which they can have exponential impact,” said Kenneth G. Langone, chair of the NYU Langone Board of Trustees. “And they’re right.”

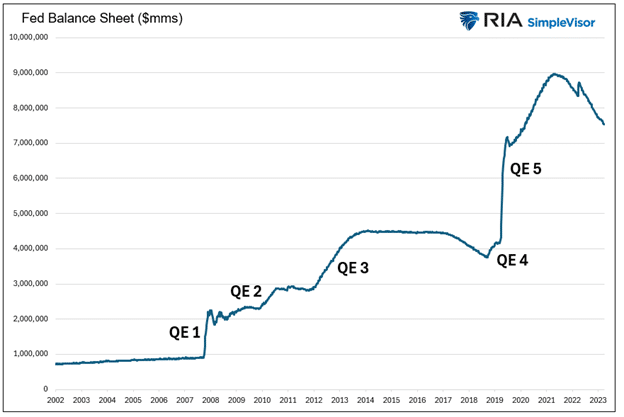

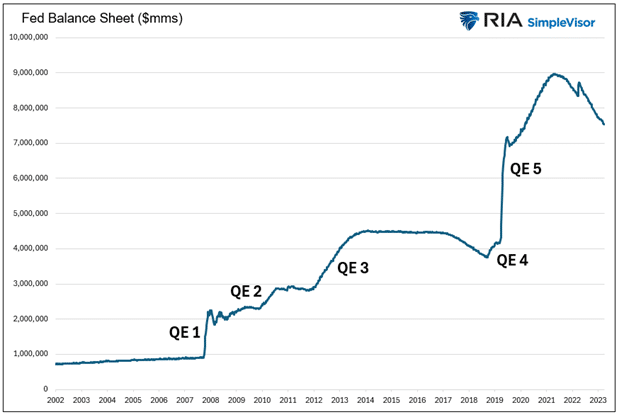

The Fed added Quantitative Easing (QE) to its monetary policy toolbox in 2008. At the time, the financial system was imploding. Fed Chair Ben Bernanke…

The Fed added Quantitative Easing (QE) to its monetary policy toolbox in 2008. At the time, the financial system was imploding. Fed Chair Ben Bernanke bought $1.5 trillion U.S. Treasury and mortgage-backed securities to staunch a financial disaster. The drastic action was sold to the public as a one-time, emergency operation to stabilize the banking system and economy. Since the initial round of QE, there have been four additional rounds, culminating with the mind-boggling $5 trillion operation in 2020 and 2021.

QE is no longer a tool for handling a crisis. It has morphed into a policy to ensure the government can fund itself. However, as we are learning today, QE has its faults. For example, it’s not an appropriate policy in times of high inflation like we have.

That doesn’t mean the Fed can’t provide liquidity to help the Treasury fund the government’s deficits. They just need to be more creative. To that end, rumors are floating around that a new variation of QE will help bridge potential liquidity shortfalls.

The Sad Fiscal Situation

The Federal government now pays over $1 trillion in interest expenses annually. Before they spend a dime on the military, social welfare, or the tens of thousands of other expenditures, one-third of the government’s tax revenue pays for the interest on the $34 trillion in debt, representing deficits of years and decades past.

There are many ways to address deficits and overwhelming debt, such as spending cuts or higher taxes. While logical approaches, politicians favor more debt. Let’s face it: winning an election on the promise of spending cuts and tax increases is hard. It’s even harder to keep your seat in Congress if you try to enact such changes.

More recently, the Federal Reserve has been forced to help fund today’s deficits and those of years past. We can debate the merits of such irresponsible behavior all day, but for investors, it’s much more critical to assess how the Fed and Treasury might keep the debt scheme going when QE is not an option.

Borrowing For Deficits

Before spreading rumors about a new variation of QE, let’s review the problem. The graph below shows the widening gap between federal spending and tax receipts. Literally, the gap between the two lines amounts to the cumulative Federal deficit. Instead of plotting deficit data, we prefer outstanding total federal debt as it better represents the cumulative onus of deficits.

The graph below shows the Treasury debt has grown annually for the last 57 years by about 1.5% more than the interest expense. Such may not seem like a lot, but 57 years of compounding makes a big difference.

Declining interest rates for the last 40+ years are to thank for the differential. The green line shows the effective interest rate has steadily dropped until recently. Even with the current instance of higher interest rates, the effective interest rate is only 3.00%.

Fiscal Dominance

The Fed has been increasingly pressed to help the U.S. Treasury maintain the ability to fund its debt at reasonable interest rates. In addition to presiding over lower-than-normal interest rates for the last 30 years, QE helps the cause. By removing Treasury and mortgage-backed securities from the market, the market can more easily absorb new Treasury issuance.

Fiscal dominance, as we are experiencing, occurs when monetary policy helps the Treasury fund its debts. Per The CATO Institute:

Fiscal dominance occurs when central banks use their monetary powers to support the prices of government securities and to peg interest rates at low levels to reduce the costs of servicing sovereign debt.

2019 Revisited

In 2019, before the massive pandemic-related deficits, government spending ramped up over the prior few years due to higher spending and tax cuts. In September 2019, the repo markets strained under the pressure of the growing Treasury demands. The banks had plenty of securities but no cash to lend. For more information on the incident and the importance of liquidity in maintaining financial stability, please read our article, Liquidity Problems.

When a bank, broker, or investor can’t borrow money despite being willing to post U.S. Treasury collateral, that is a clear sign that the banking system lacks liquidity. That is exactly what happened in 2019.

The Fed came to the rescue, offering QE and lowering interest rates.

Shortly later, in March 2020, government spending blossomed with the pandemic, and the Fed was quick to help. As we shared earlier, the Fed, via QE, removed over $5 trillion of assets from the financial markets. That amount was on par with the surge of government debt.

The Fed is mandated to manage policy to achieve maximum employment and stable prices. Mandated or not, recent experiences demonstrate the Fed has become the de facto lender to the Treasury, albeit indirectly.

The Fed Is In Handcuffs

While Jerome Powell and the Fed might like to help the government meet their exorbitant funding needs with lower interest rates and QE, they are shackled. Higher inflation resulting from the pandemic and fiscal and monetary policies force them to reduce their balance sheet and keep rates abnormally high.

Unfortunately, as we wrote in Liquidity Problems, the issuance of Treasury debt rapidly drains excess liquidity from the system.

While the Fed hesitates to cut rates or do QE, they may have another trick up their sleeve.

Spreading Rumors

The following is based on rumors from numerous sources about what the Fed and banking regulators may do to alleviate funding pressures and liquidity shortfalls.

Banks have regulatory limits on the amount of leverage they can employ. The amount is set by the type and riskiness of assets they hold. For instance, U.S. Treasuries can be leveraged more than a loan to small businesses. A dollar of a bank deposit may allow a bank to buy $5 of a Treasury note but only lend $3 to a riskier borrower.

The regulatory structure currently recognizes eight Global Systematically Important Banks (GSIB). They are as follows: Bank of America, The Bank of New York, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley, State Street, and Wells Fargo & Company.

Rumor has it that the regulators could eliminate leverage requirements for the GSIBs. Doing so would infinitely expand their capacity to own Treasury securities. That may sound like a perfect solution, but there are two problems: the banks must be able to fund the Treasury assets and avoid losing money on them.

BTFP To The Rescue Again

A year ago, the Fed created the Bank Term Funding Program (BTFP) to bail out banks with underwater securities. The program allowed banks to pledge underwater Treasury assets to the Fed. In exchange, the Fed would loan them money equal to the bond’s par value, even though the bonds were trading at discounts to par.

Remember, since 2008, banks no longer have to book gains or losses on assets unless they are impaired or sold.

In a new scheme, bank regulators could eliminate the need for GSIBs to hold capital against Treasury securities while the Fed reenacts some version of BTFP. Under such a regime, the banks could buy Treasury notes and fund them via the BTFP. If the borrowing rate is less than the bond yield, they make money and, therefore, should be very willing to participate, as there is potentially no downside.

The Fed still uses its balance sheet in this scheme, but it could sell it to the public as a non-inflationary action, as it did in March 2023 when the BTFP was introduced.

Summary

The federal government’s escalating debt and interest expenses underscore the challenges posed by prolonged deficit spending. The problem has forced the Fed to help the Treasury meet its burgeoning needs. The situation becomes more evident with each passing day.

The recently closed BTFP program and rumors about leverage requirements provide insight into how the Fed might accomplish this tall task while maintaining its hawkish anti-inflationary policy stance.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}