Government

What Comes After The “Deepest Economic Crisis Since The Great Depression”

What Comes After The "Deepest Economic Crisis Since The Great Depression"

Share this:

Authored by Huge Erken, head of International Economics at Rabobank

Coronavirus causes deepest economic crisis since the Great Depression

Summary

-

COVID-19 is expected to result in contraction of the global economy by 4.1% in 2020

-

This means that the corona crisis will be the deepest economic crisis since the Great Depression in the 1930s

-

We expect a relatively limited recovery in 2021, as many countries will continue to be bound to a ‘six-foot economy’ for a long time

-

Businesses in these countries will not be able to offer as many goods and services as they did previously, and demand will remain low for a long time Political tensions between the US and China have flared up again, and we expect the truce in the trade war to come to an end

-

Downside risks such as a second wave of infections or a financial crisis continue to dominate

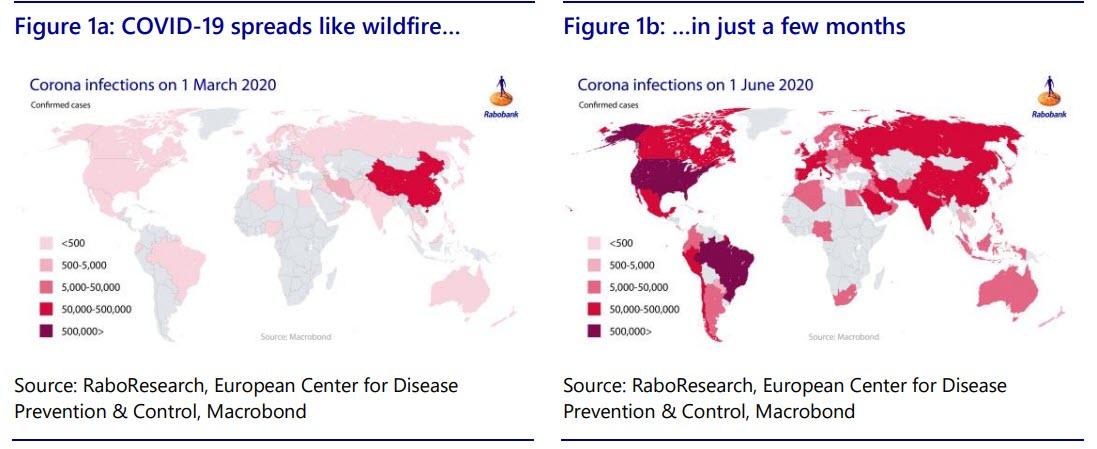

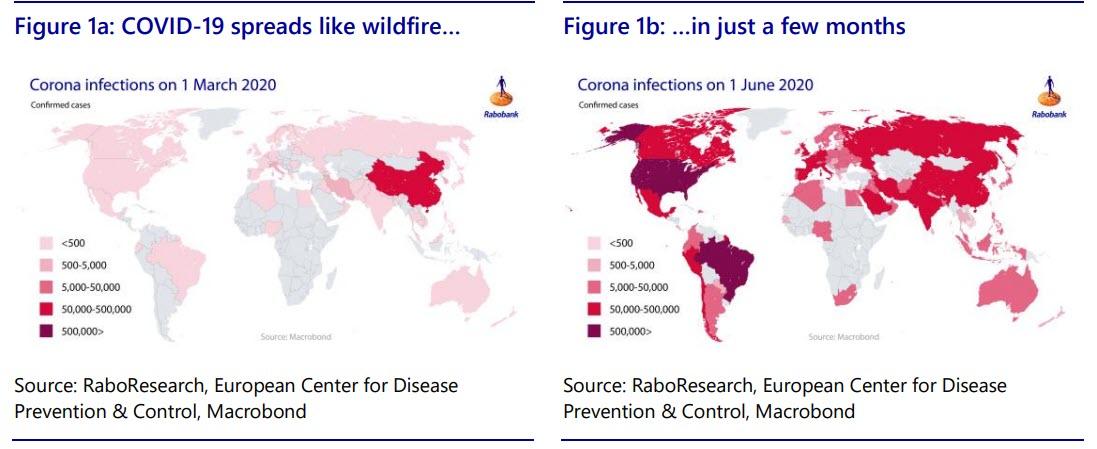

The global economy will contract by 4.1% The rapid succession of developments relating to the coronavirus (see Figure 1a and 1b) is leaving deep scars in the global economy. We have therefore had to downgrade our estimates several times (here and here and here).

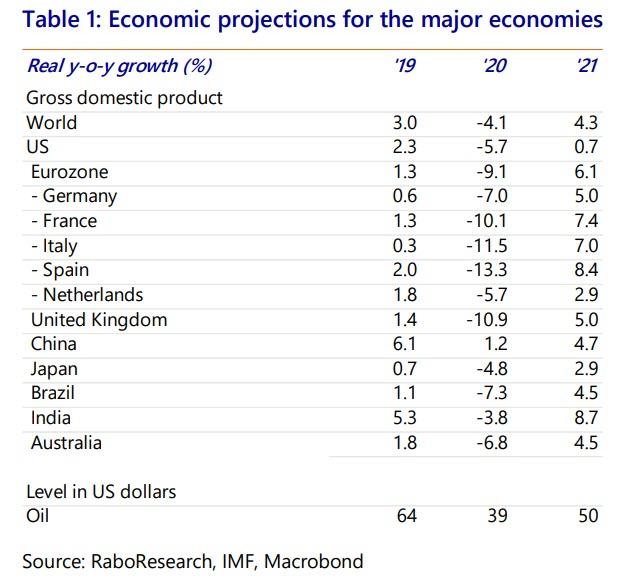

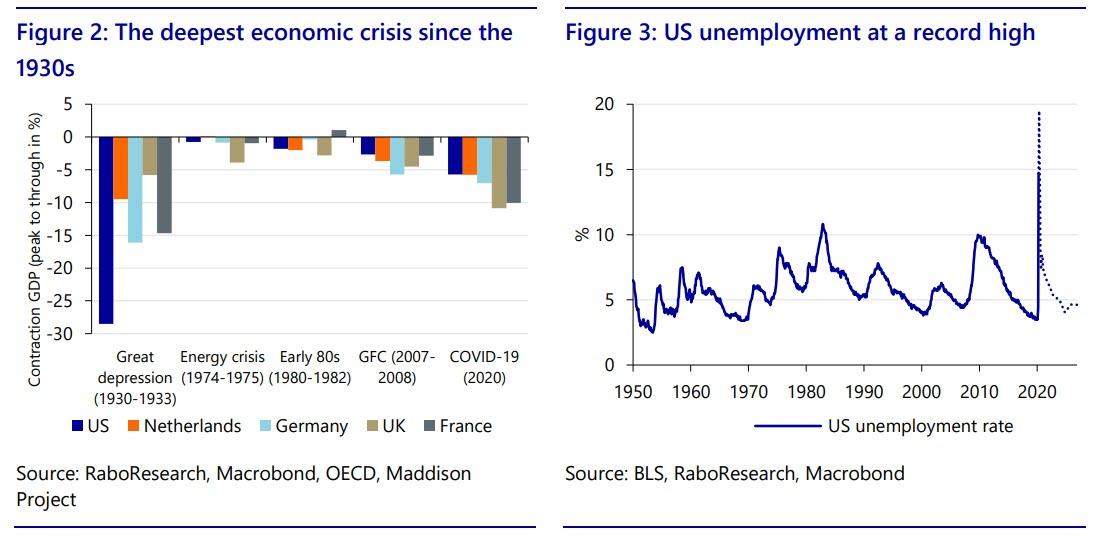

We are currently forecasting that the global economy will contract by 4.1% in 2020, and then grow by 4.3% in 2021 (Table 1). This means that the corona crisis will be the deepest economic crisis since the Great Depression in the 1930s (Figure 2). The sharp contraction in mainly Western Europe and Latin America will be offset by more moderate GDP declines in Asia, where stronger underlying growth in China in 2020 and in India in 2021 will go some way to limiting the damage.

The deepest economic crisis since the 1930s For France, Italy, Spain and the United Kingdom we are even forecasting a contraction in gross domestic product (GDP) of more than 10% in, mainly due to the long and stringent lockdowns in these countries. Another factor is that the sectors that are the worst hit by the corona crisis, such as tourism, recreation and hospitality, are relatively strongly represented in these countries compared to other eurozone countries.

In the United States, we expect a more limited contraction of 5.7%, again followed by a relatively modest recovery in 2021. In the US, this relates to the flexible labor market, which lead to a rapid rise in unemployment which started to come down again recently (Figure 3). April saw the highest post-war unemployment figure of 14.7%, although figures for May show that it is coming down again. Corrected for classification errors, unemployment was as much as 19.5%. With a fifth of the American working population temporarily out of work, private consumption will be slow to pick up after the hard lockdown period, and these effects will continue to be felt into 2021. This expected weakness in the demand side of the economy will be intensified by the fact that the US economy was already in pretty poor shape before the advent of the corona crisis, something we have been warning about since the beginning of 2019.

Reopening the economy is proving difficult

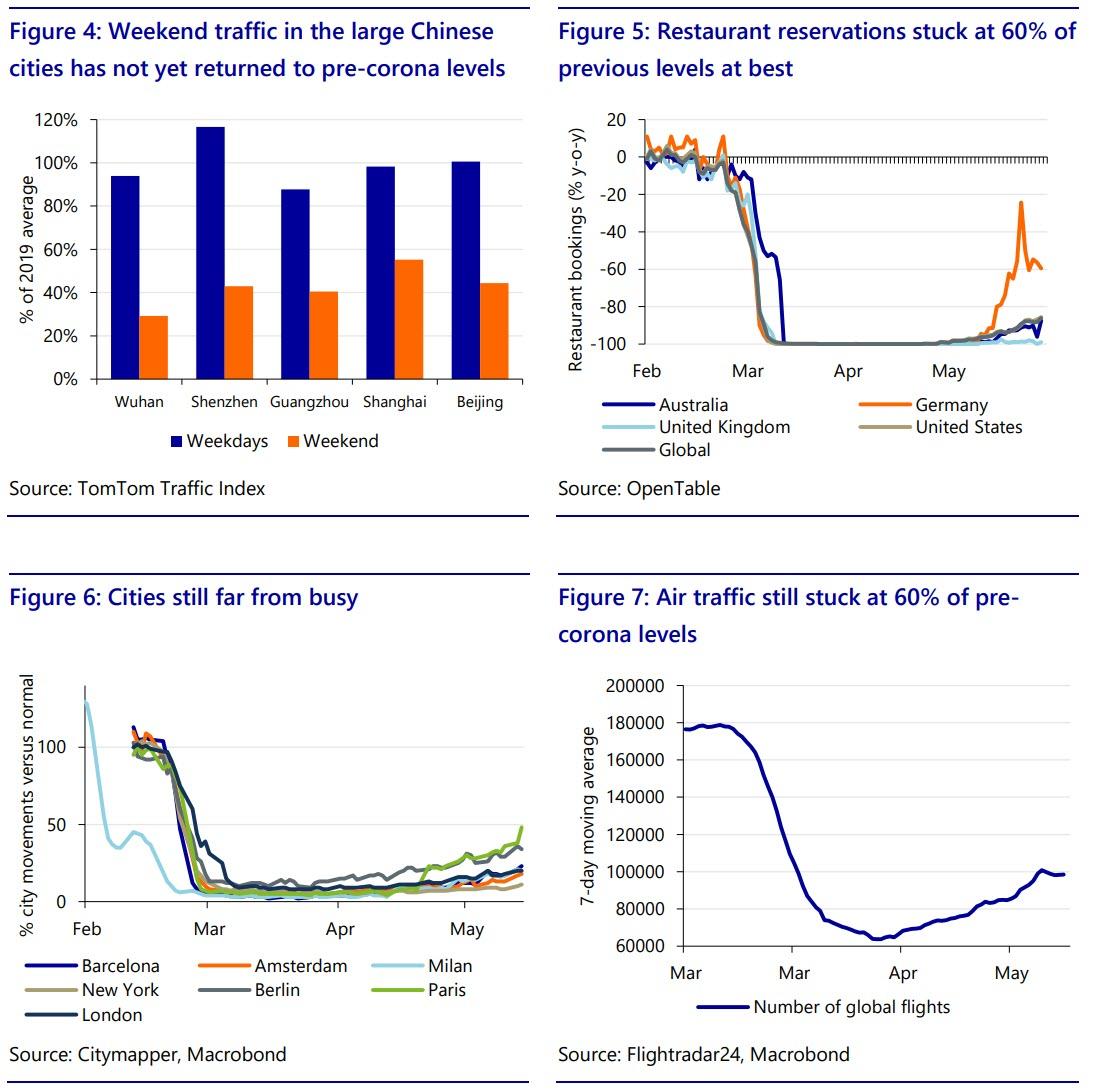

The US is not the only country where we expect lower growth in 2021 than we previously forecast. We currently expect the recovery to be more moderate in virtually all countries. Despite the easing of the lockdown in many countries, economic activity is increasing only marginally. On the one hand this is due to lack of demand, as people continue to avoid restaurants, cafés and stores, and also due to economic uncertainty and loss of income. On the other hand, there are limitations in the supply side of the economy as businesses and entrepreneurs are forced to adapt to the six-foot economy. A recent academic study argues that social distancing will be needed until 2022 to prevent a resurgence of the virus.

A lengthy period of social distancing and lower potential growth

Countries will be stuck with the six-foot economy for many months yet. For the Netherlands, we have calculated that there could be adaptation problems for 16% of jobs in this economy, while in the US this figure is 23% (see this report). In this situation a V-shaped economic recovery will be hard to achieve and a U-shaped recovery may be more likely (see this study for a detailed discussion on the possible shapes the recovery might take). We have calculated that the corona crisis could also damage the long-term growth potential of countries, so that the effects could continue to be felt even after 2022. For the Dutch economy, we forecast that annual potential economic growth in 2022-2030 will fall from 1.4% to 1.2%, and in the US we foresee a decline from 1.6% to 1.4%.

Political tensions between the US and China are flaring up again

Following the long-awaited truce between the US and China in the form of the ‘Phase 1 deal’ on January 13 and the subsequent outbreak of the corona virus, a period of quiet broke out in the trade war between the two superpowers. However, diplomatic relations between the US and China have now taken a rapid and serious turn for the worse. This started in March, with accusations from both sides regarding the approach to the virus.

US measures

The US is working on legislation to use grants and tax breaks to persuade foreign businesses in China to transfer their operations to the US and on measures to reduce dependence on China in areas such as medical and defense-related products. President Trump has also instructed his administration to remove Hong Kong’s special status in response to a Chinese security law that the Americans believe threatens Hong Kong’s autonomy. Withdrawing this status would mean that Hong Kong, which is a major trading hub in Asia, would face higher trade tariffs and that access to US dollars by businesses and banks in Hong Kong could be restricted. Finally, Trump has signed a presidential executive order, under which US businesses are no longer permitted to use products from the Chinese telecoms giant Huawei.

Anti-China rhetoric as a lightning conductor

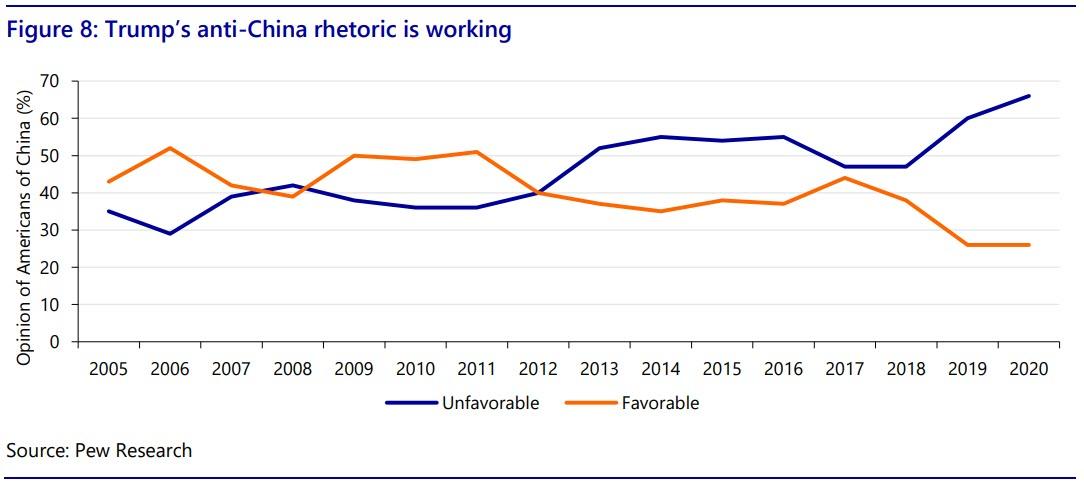

All these measures are part of President Trump’s ‘America First’ doctrine, and address what he sees as unfair trading practices on the part of China. This view is starting to gain traction with the US public (see Figure 8). Trump seems to be using anti-China rhetoric as a diversion from his domestic problems. Trump has lost much needed popularity in the polls due to his handling of the corona crisis, the rapidly worsening economy and his threat to deploy the military to subdue recent demonstrations and social unrest.

With the presidential elections upcoming in November, Trump is trying to make electoral gains with his tried and tested anti-China tactic. Trump is indeed not alone in this stance, as his Democratic opponent Joe Biden is also planning to act against China, albeit in cooperation with Europe.

Chinese measures

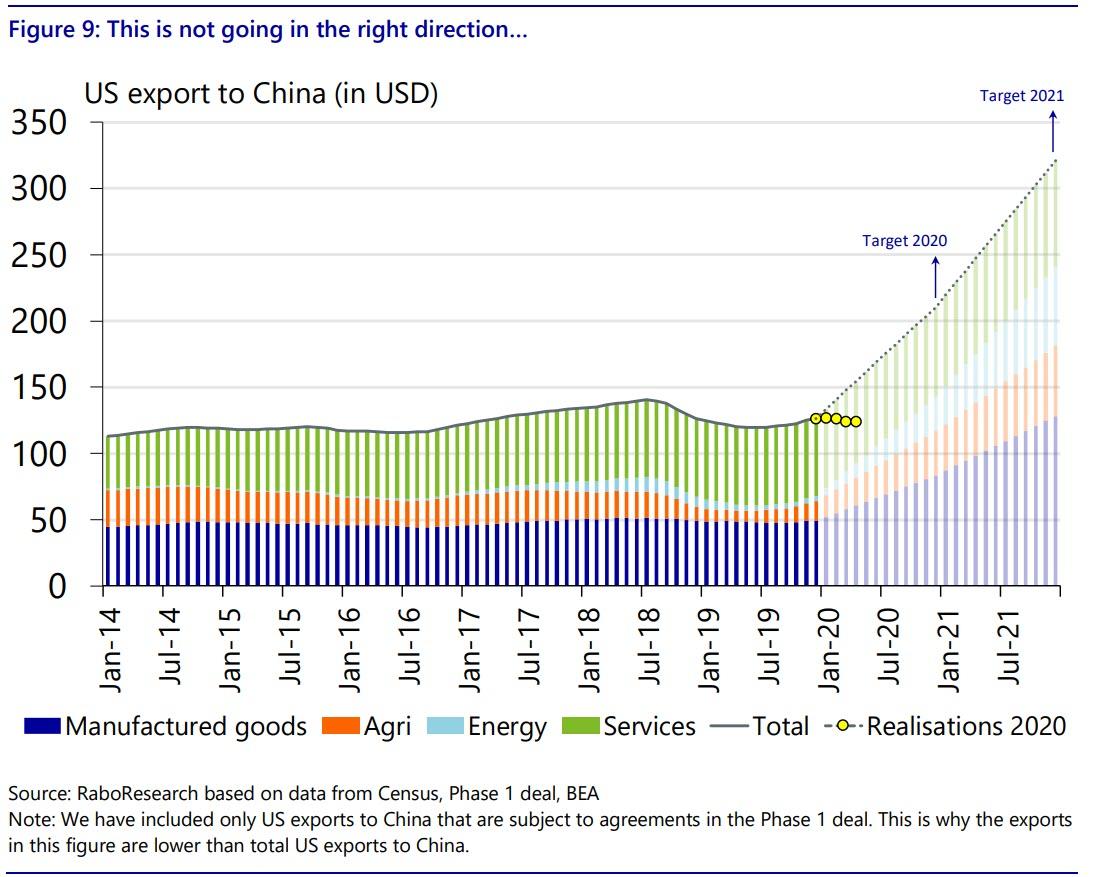

China has not been sitting on its hands either. It expelled several American journalists in March, and state-run food companies (Cofco and Sinograin) have been instructed to buy fewer products from the US. This fits the view that China is apparently not ready to observe the trade agreements in the Phase 1 deal, as available import data for the first three months of 2020 are showing a negative rather than a positive trend (see Figure 9). This also confirms that China’s import commitment was always highly unrealistic right from the start. In combination with the recent political tensions between the two countries, we believe the deal is likely to break down before the year is out.

Downside risks

Despite our heavily downgraded economic forecasts and rising geopolitical tensions, there are several risks that could make the outlook even worse. Four of these risks are discussed below. A second wave of infections Countries around the world are currently easing their lockdowns. There is a possibility that this easing will open the door to a new wave of infections, forcing countries to impose a new period of lockdowns to restrict the spread of the virus. Previously we published estimates of the additional economic damage if lockdowns were to be extended by a further three months. A return of the virus in emerging markets is potentially a much greater risk than in developed countries. It remains to be seen whether it is realistic that people in densely populated countries such as Indonesia, India and Brazil will be able to maintain adequate social distancing. There is also the question of whether these countries have sufficient testing capabilities to identify a resurgence of the virus at an early stage.

A financial crisis

The current economic crisis could turn into a financial crisis, in which financial institutions get into difficulties. For instance, if there is a second or third wave of infections that leads to a sharp increase in bankruptcies, a rapid deterioration in bank balance sheets and liquidity issues for banks themselves. The consequence could be that lending to businesses comes to a halt, putting more businesses in trouble and creating a vicious circle.

At this time we do not expect any friction in the financial system, partly because the banks have generally improved their buffers since the Great Financial Crisis and partly because central banks around the world are providing sufficient liquidity to the banks. The volatility in the financial markets that marked the start of the corona crisis has therefore also waned.

Zombie companies

Another risk in the longer term is that the proportion of what are known as ‘zombie companies’ will increase in some countries. Zombie companies are businesses that are barely profitable now and their outlook for future profitability is bleak. These companies thrive in an environment of low interest rates and a financial system that rolls over loans to loss-making companies. Even more loose monetary policy by central banks encourages this ‘zombification’ process. We saw the number of zombie companies increase rapidly in the wake of the Great Financial Crisis. In the US, the proportion of zombie companies among listed companies rose to 15% in 2019 (figure 10). In Japan as well, the proportion of zombie companies among SMEs is now 21% according to some estimates. Zombie companies represent a problem for the post-crisis recovery as they are less productive and innovative than healthy businesses. According to the BIS, a one percentage point increase in the proportion of zombie companies in a country leads to a decline of 0.3% in annual GDP growth.

International

Copper Soars, Iron Ore Tumbles As Goldman Says “Copper’s Time Is Now”

Copper Soars, Iron Ore Tumbles As Goldman Says "Copper’s Time Is Now"

After languishing for the past two years in a tight range despite recurring…

Share this:

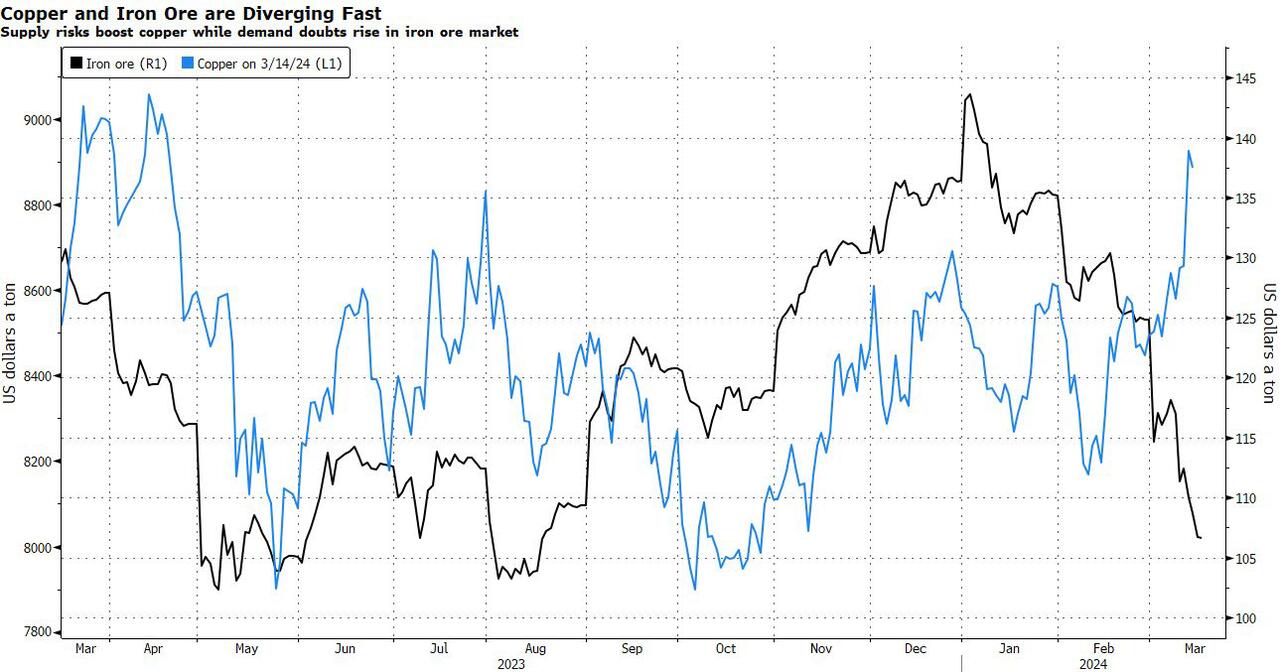

After languishing for the past two years in a tight range despite recurring speculation about declining global supply, copper has finally broken out, surging to the highest price in the past year, just shy of $9,000 a ton as supply cuts hit the market; At the same time the price of the world's "other" most important mined commodity has diverged, as iron ore has tumbled amid growing demand headwinds out of China's comatose housing sector where not even ghost cities are being built any more.

Copper surged almost 5% this week, ending a months-long spell of inertia, as investors focused on risks to supply at various global mines and smelters. As Bloomberg adds, traders also warmed to the idea that the worst of a global downturn is in the past, particularly for metals like copper that are increasingly used in electric vehicles and renewables.

Yet the commodity crash of recent years is hardly over, as signs of the headwinds in traditional industrial sectors are still all too obvious in the iron ore market, where futures fell below $100 a ton for the first time in seven months on Friday as investors bet that China’s years-long property crisis will run through 2024, keeping a lid on demand.

Indeed, while the mood surrounding copper has turned almost euphoric, sentiment on iron ore has soured since the conclusion of the latest National People’s Congress in Beijing, where the CCP set a 5% goal for economic growth, but offered few new measures that would boost infrastructure or other construction-intensive sectors.

As a result, the main steelmaking ingredient has shed more than 30% since early January as hopes of a meaningful revival in construction activity faded. Loss-making steel mills are buying less ore, and stockpiles are piling up at Chinese ports. The latest drop will embolden those who believe that the effects of President Xi Jinping’s property crackdown still have significant room to run, and that last year’s rally in iron ore may have been a false dawn.

Meanwhile, as Bloomberg notes, on Friday there were fresh signs that weakness in China’s industrial economy is hitting the copper market too, with stockpiles tracked by the Shanghai Futures Exchange surging to the highest level since the early days of the pandemic. The hope is that headwinds in traditional industrial areas will be offset by an ongoing surge in usage in electric vehicles and renewables.

And while industrial conditions in Europe and the US also look soft, there’s growing optimism about copper usage in India, where rising investment has helped fuel blowout growth rates of more than 8% — making it the fastest-growing major economy.

In any case, with the demand side of the equation still questionable, the main catalyst behind copper’s powerful rally is an unexpected tightening in global mine supplies, driven mainly by last year’s closure of a giant mine in Panama (discussed here), but there are also growing worries about output in Zambia, which is facing an El Niño-induced power crisis.

On Wednesday, copper prices jumped on huge volumes after smelters in China held a crisis meeting on how to cope with a sharp drop in processing fees following disruptions to supplies of mined ore. The group stopped short of coordinated production cuts, but pledged to re-arrange maintenance work, reduce runs and delay the startup of new projects. In the coming weeks investors will be watching Shanghai exchange inventories closely to gauge both the strength of demand and the extent of any capacity curtailments.

“The increase in SHFE stockpiles has been bigger than we’d anticipated, but we expect to see them coming down over the next few weeks,” Colin Hamilton, managing director for commodities research at BMO Capital Markets, said by phone. “If the pace of the inventory builds doesn’t start to slow, investors will start to question whether smelters are actually cutting and whether the impact of weak construction activity is starting to weigh more heavily on the market.”

* * *

Few have been as happy with the recent surge in copper prices as Goldman's commodity team, where copper has long been a preferred trade (even if it may have cost the former team head Jeff Currie his job due to his unbridled enthusiasm for copper in the past two years which saw many hedge fund clients suffer major losses).

As Goldman's Nicholas Snowdon writes in a note titled "Copper's time is now" (available to pro subscribers in the usual place)...

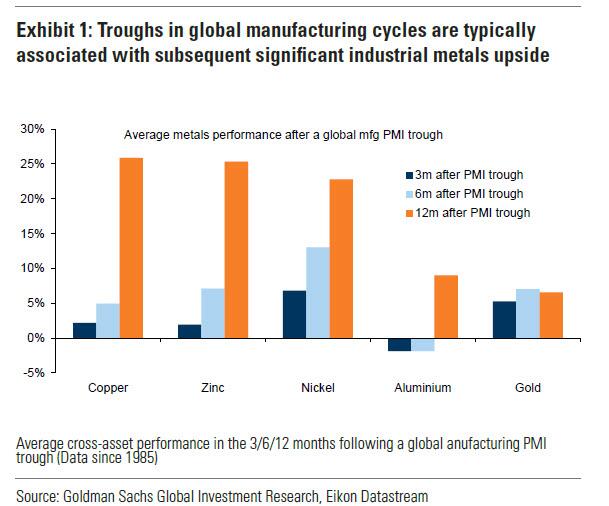

... there has been a "turn in the industrial cycle." Specifically according to the Goldman analyst, after a prolonged downturn, "incremental evidence now points to a bottoming out in the industrial cycle, with the global manufacturing PMI in expansion for the first time since September 2022." As a result, Goldman now expects copper to rise to $10,000/t by year-end and then $12,000/t by end of Q1-25.’

Here are the details:

Previous inflexions in global manufacturing cycles have been associated with subsequent sustained industrial metals upside, with copper and aluminium rising on average 25% and 9% over the next 12 months. Whilst seasonal surpluses have so far limited a tightening alignment at a micro level, we expect deficit inflexions to play out from quarter end, particularly for metals with severe supply binds. Supplemented by the influence of anticipated Fed easing ahead in a non-recessionary growth setting, another historically positive performance factor for metals, this should support further upside ahead with copper the headline act in this regard.

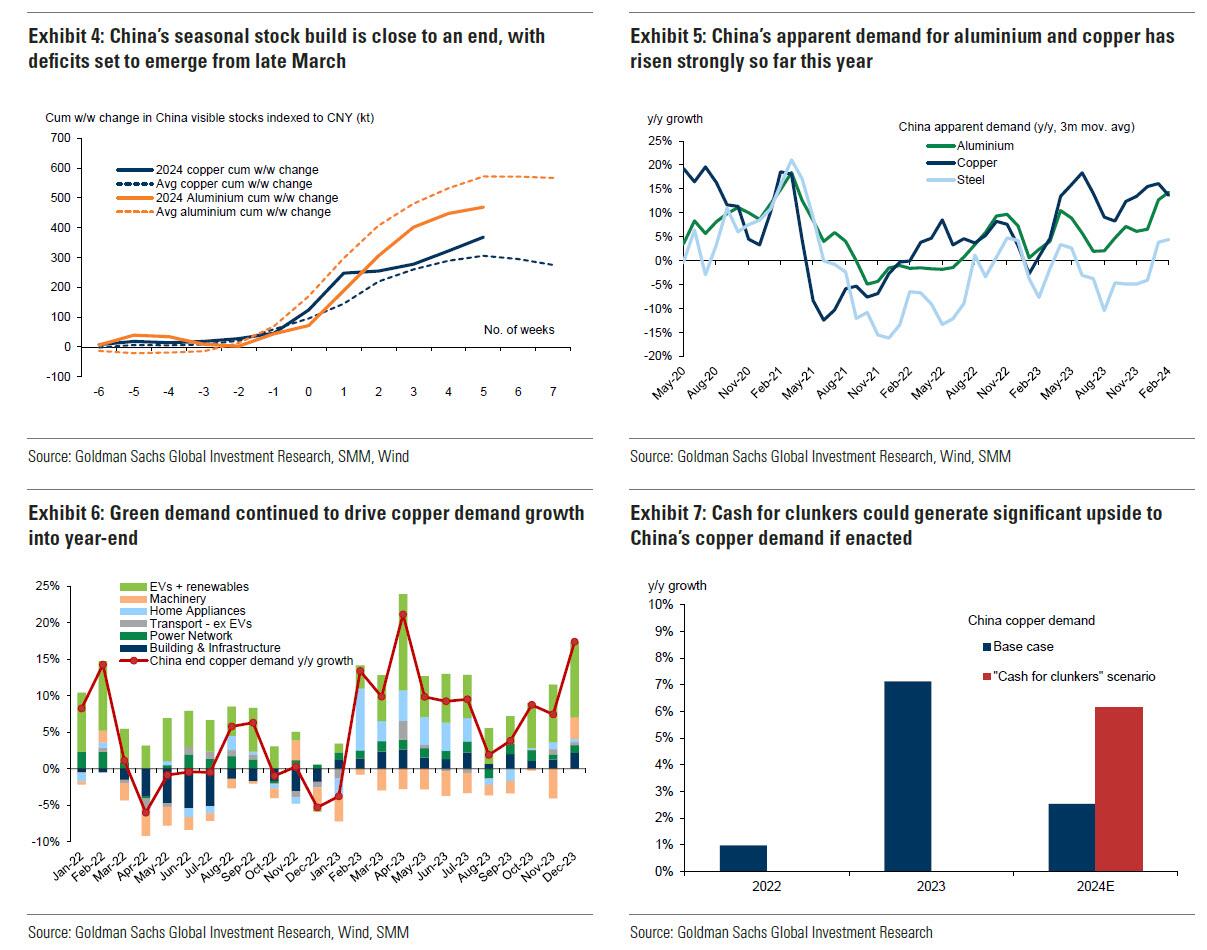

Goldman then turns to what it calls China's "green policy put":

Much of the recent focus on the “Two Sessions” event centred on the lack of significant broad stimulus, and in particular the limited property support. In our view it would be wrong – just as in 2022 and 2023 – to assume that this will result in weak onshore metals demand. Beijing’s emphasis on rapid growth in the metals intensive green economy, as an offset to property declines, continues to act as a policy put for green metals demand. After last year’s strong trends, evidence year-to-date is again supportive with aluminium and copper apparent demand rising 17% and 12% y/y respectively. Moreover, the potential for a ‘cash for clunkers’ initiative could provide meaningful right tail risk to that healthy demand base case. Yet there are also clear metal losers in this divergent policy setting, with ongoing pressure on property related steel demand generating recent sharp iron ore downside.

Meanwhile, Snowdon believes that the driver behind Goldman's long-running bullish view on copper - a global supply shock - continues:

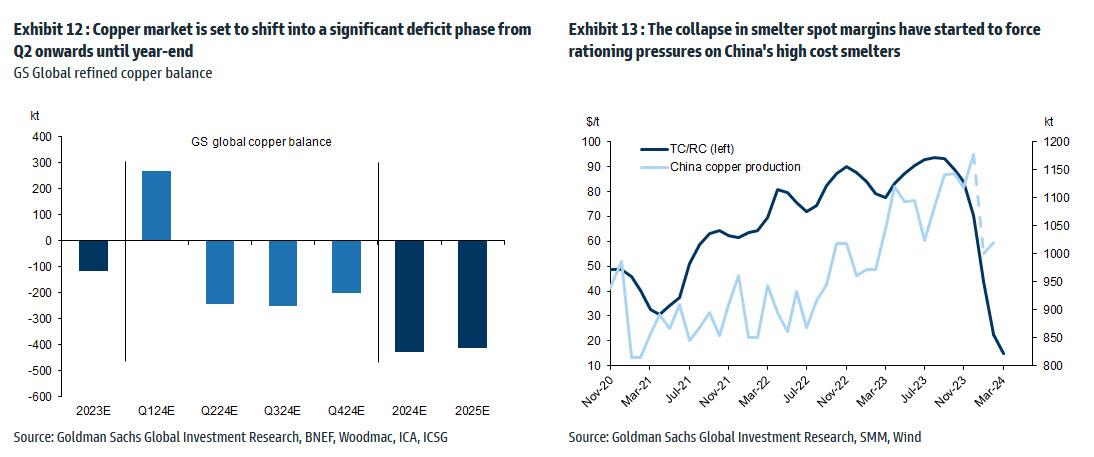

Copper’s supply shock progresses. The metal with most significant upside potential is copper, in our view. The supply shock which began with aggressive concentrate destocking and then sharp mine supply downgrades last year, has now advanced to an increasing bind on metal production, as reflected in this week's China smelter supply rationing signal. With continued positive momentum in China's copper demand, a healthy refined import trend should generate a substantial ex-China refined deficit this year. With LME stocks having halved from Q4 peak, China’s imminent seasonal demand inflection should accelerate a path into extreme tightness by H2. Structural supply underinvestment, best reflected in peak mine supply we expect next year, implies that demand destruction will need to be the persistent solver on scarcity, an effect requiring substantially higher pricing than current, in our view. In this context, we maintain our view that the copper price will surge into next year (GSe 2025 $15,000/t average), expecting copper to rise to $10,000/t by year-end and then $12,000/t by end of Q1-25’

Another reason why Goldman is doubling down on its bullish copper outlook: gold.

The sharp rally in gold price since the beginning of March has ended the period of consolidation that had been present since late December. Whilst the initial catalyst for the break higher came from a (gold) supportive turn in US data and real rates, the move has been significantly amplified by short term systematic buying, which suggests less sticky upside. In this context, we expect gold to consolidate for now, with our economists near term view on rates and the dollar suggesting limited near-term catalysts for further upside momentum. Yet, a substantive retracement lower will also likely be limited by resilience in physical buying channels. Nonetheless, in the midterm we continue to hold a constructive view on gold underpinned by persistent strength in EM demand as well as eventual Fed easing, which should crucially reactivate the largely for now dormant ETF buying channel. In this context, we increase our average gold price forecast for 2024 from $2,090/toz to $2,180/toz, targeting a move to $2,300/toz by year-end.

Much more in the full Goldman note available to pro subs.

Government

Moderna turns the spotlight on long Covid with new initiatives

Moderna’s latest Covid effort addresses the often-overlooked chronic condition of long Covid — and encourages vaccination to reduce risks. A digital…

Share this:

Moderna’s latest Covid effort addresses the often-overlooked chronic condition of long Covid — and encourages vaccination to reduce risks. A digital campaign debuted Friday along with a co-sponsored event in Detroit offering free CT scans, which will also be used in ongoing long Covid research.

In a new video, a young woman describes her three-year battle with long Covid, which includes losing her job, coping with multiple debilitating symptoms and dealing with the negative effects on her family. She ends by saying, “The only way to prevent long Covid is to not get Covid” along with an on-screen message about where to find Covid-19 vaccines through the vaccines.gov website.

“Last season we saw people would get a flu shot, but they didn’t always get a Covid shot,” said Moderna’s Chief Brand Officer Kate Cronin. “People should get their flu shot, but they should also get their Covid shot. There’s no risk of long flu, but there is the risk of long-term effects of Covid.”

It’s Moderna’s “first effort to really sound the alarm,” she said, and the debut coincides with the second annual Long Covid Awareness Day.

An estimated 17.6 million Americans are living with long Covid, according to the latest CDC data. About four million of them are out of work because of the condition, resulting in an estimated $170 billion in lost wages.

While HHS anted up $45 million in grants last year to expand long Covid support initiatives along with public health campaigns, the condition is still often ignored and underfunded.

“It’s not just about the initial infection of Covid, but also if you get it multiple times, your risks goes up significantly,” Cronin said. “It’s important that people understand that.”

grants covid-19 cdc hhsGovernment

Consequences Minus Truth

Consequences Minus Truth

Authored by James Howard Kunstler via Kunstler.com,

“People crave trust in others, because God is found there.”

-…

Share this:

{kind=link}

Authored by James Howard Kunstler via Kunstler.com,

“People crave trust in others, because God is found there.”

- Dom de Bailleul

The rewards of civilization have come to seem rather trashy in these bleak days of late empire; so, why even bother pretending to be civilized? This appears to be the ethos driving our politics and culture now. But driving us where? Why, to a spectacular sort of crack-up, and at warp speed, compared to the more leisurely breakdown of past societies that arrived at a similar inflection point where Murphy’s Law replaced the rule of law.

{kind=link}

The US Military Academy at West point decided to “upgrade” its mission statement this week by deleting the phrase Duty, Honor, Country that summarized its essential moral orientation. They replaced it with an oblique reference to “Army Values,” without spelling out what these values are, exactly, which could range from “embrace the suck” to “charlie foxtrot” to “FUBAR” — all neatly applicable to our country’s current state of perplexity and dread.

Are you feeling more confident that the US military can competently defend our country? Probably more like the opposite, because the manipulation of language is being used deliberately to turn our country inside-out and upside-down. At this point we probably could not successfully pacify a Caribbean island if we had to, and you’ve got to wonder what might happen if we have to contend with countless hostile subversive cadres who have slipped across the border with the estimated nine-million others ushered in by the government’s welcome wagon.

Momentous events await. This Monday, the Supreme Court will entertain oral arguments on the case Missouri, et al. v. Joseph R. Biden, Jr., et al. The integrity of the First Amendment hinges on the decision. Do we have freedom of speech as set forth in the Constitution? Or is it conditional on how government officials feel about some set of circumstances? At issue specifically is the government’s conduct in coercing social media companies to censor opinion in order to suppress so-called “vaccine hesitancy” and to manipulate public debate in the 2020 election. Government lawyers have argued that they were merely “communicating” with Twitter, Facebook, Google, and others about “public health disinformation and election conspiracies.”

You can reasonably suppose that this was our government’s effort to disable the truth, especially as it conflicted with its own policy and activities — from supporting BLM riots to enabling election fraud to mandating dubious vaccines. Former employees of the FBI and the CIA were directly implanted in social media companies to oversee the carrying-out of censorship orders from their old headquarters. The former general counsel (top lawyer) for the FBI, James Baker, slid unnoticed into the general counsel seat at Twitter until Elon Musk bought the company late in 2022 and flushed him out. The so-called Twitter Files uncovered by indy reporters Matt Taibbi, Michael Shellenberger, and others, produced reams of emails from FBI officials nagging Twitter execs to de-platform people and bury their dissent. You can be sure these were threats, not mere suggestions.

One of the plaintiffs joined to Missouri v. Biden is Dr. Martin Kulldorff, a biostatistician and professor at the Harvard Medical School, who opposed Covid-19 lockdowns and vaccine mandates. He was one of the authors of the open letter called The Great Barrington Declaration (October, 2020) that articulated informed medical dissent for a bamboozled public. He was fired from his job at Harvard just this past week for continuing his refusal to take the vaccine. Harvard remains among a handful of institutions that still require it, despite massive evidence that it is ineffective and hazardous. Like West Point, maybe Harvard should ditch its motto, Veritas, Latin for “truth.”

A society hostile to truth can’t possibly remain civilized, because it will also be hostile to reality. That appears to be the disposition of the people running things in the USA these days. The problem, of course, is that this is not a reality-optional world, despite the wishes of many Americans (and other peoples of Western Civ) who wish it would be.

Next up for us will be “Joe Biden’s” attempt to complete the bankruptcy of our country with $7.3-trillion proposed budget, 20 percent over the previous years spending, based on a $5-billion tax increase. Good luck making that work. New York City alone is faced with paying $387 a day for food and shelter for each of an estimated 64,800 illegal immigrants, which amounts to $9.15-billion a year. The money doesn’t exist, of course. New York can thank “Joe Biden’s” executive agencies for sticking them with this unbearable burden. It will be the end of New York City. There will be no money left for public services or cultural institutions. That’s the reality and that’s the truth.

A financial crack-up is probably the only thing short of all-out war that will get the public’s attention at this point. I wouldn’t be at all surprised if it happened next week. Historians of the future, stir-frying crickets and fiddleheads over their campfires will marvel at America’s terminal act of gluttony: managing to eat itself alive.

* * *

Support his blog by visiting Jim’s Patreon Page or Substack

Net Zero, The Digital Panopticon, & The Future Of Food

Illegal Immigrants Leave US Hospitals With Billions In Unpaid Bills

Sylvester researchers, collaborators call for greater investment in bereavement care

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Looking Back At COVID’s Authoritarian Regimes

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

MIPIM 2024 Reflects Mixed Feelings on CRE Recovery

Moderna turns the spotlight on long Covid with new initiatives

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex