Wells Tumbles As Revenues Plunge, NIM Hits Record Low, Warns On Payment Deferrals

Wells Tumbles As Revenues Plunge, NIM Hits Record Low, Warns On Payment Deferrals

Share this:

If there is one constant during earnings season, it is that no matter what the other banks do, Wells Fargo will always shit the bed, and this time was no different, with the stock sliding after reporting that Q3 earnings missed again as its Net Interest Margin dropped to a fresh all time low, while issuing an ominous warning that customer payment deferrals in the wake of the pandemic may delay the recognition of net charge-offs and delinquencies.

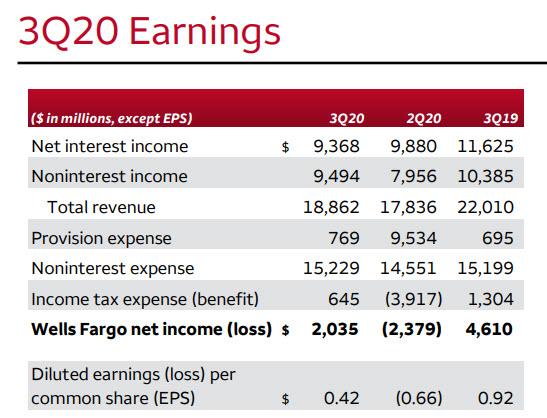

Wells reported Q3 EPS of just $0.42, down more than 50% from the 0.92 a year ago, and missing expectations of $0.45 even as Revenue of $18.862BN beat estimates of $18.0BN, but plunged 14% from $22BN a year ago. The bank reported Q3 net income of $2 billion, which was up $4.4 billion from the previous quarter, but down 56% from $4.6BN a year ago, on "lower provision expense and higher non-interest income on broad-based growth including higher mortgage banking income, partially offset by lower net interest income and higher noninterest expense, which included restructuring charges."

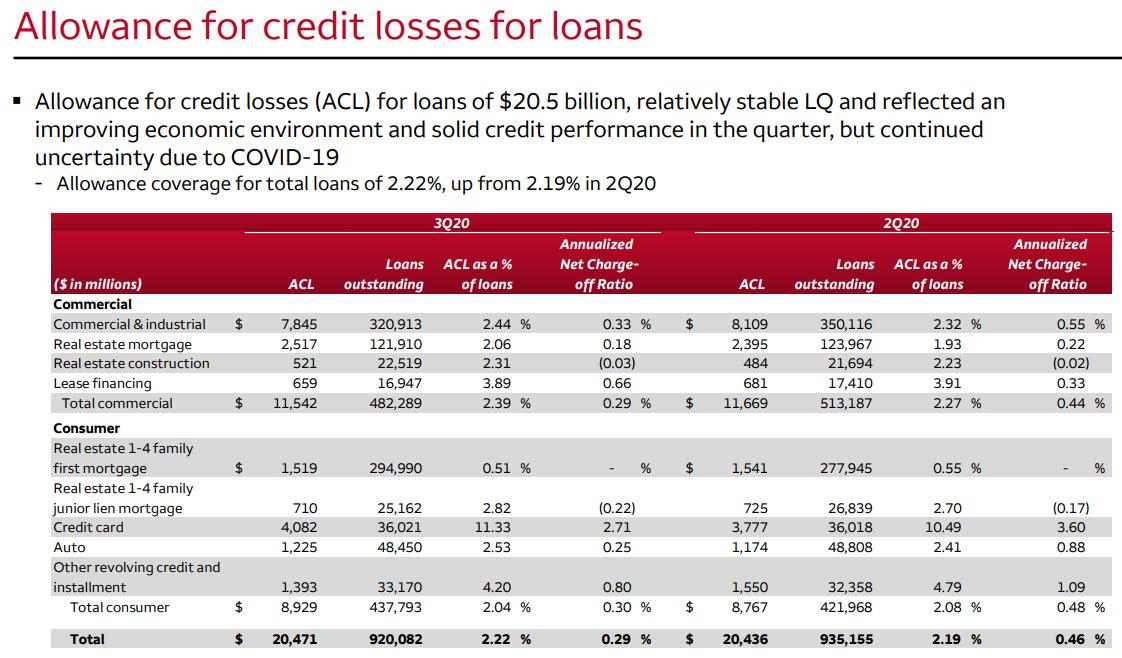

The bank missed EPS even though - like all the other banks - it set aside only $769MM in loan-loss provisions, far less than the $1.65BN expected, and charged off just $683MM (up 5.9% Y/Y, but down $430MM from Q2), also below the $1.38BN expected. Non-performing assets increased again, rising by $378 million, or 5%, to $8.2 billion, of which $417MM was due to an increase in nonaccrual loans at $8BN. Commercial nonaccruals increased $113 million "on higher commercial real estate nonaccruals" while consumer nonaccrual loans increased $304 million driven by higher consumer real estate and auto nonaccruals.

Wells also said that the net charge-off ratio of 0.29% was down 17 bps from Q2, as commercial losses of 29 bps, were down 15 bps "reflecting lower C&I losses driven by lower losses in oil and gas, as well as lower CRE losses" while "consumer losses of 30 bps, down 18 bps LQ driven by lower losses in credit card and auto loans."

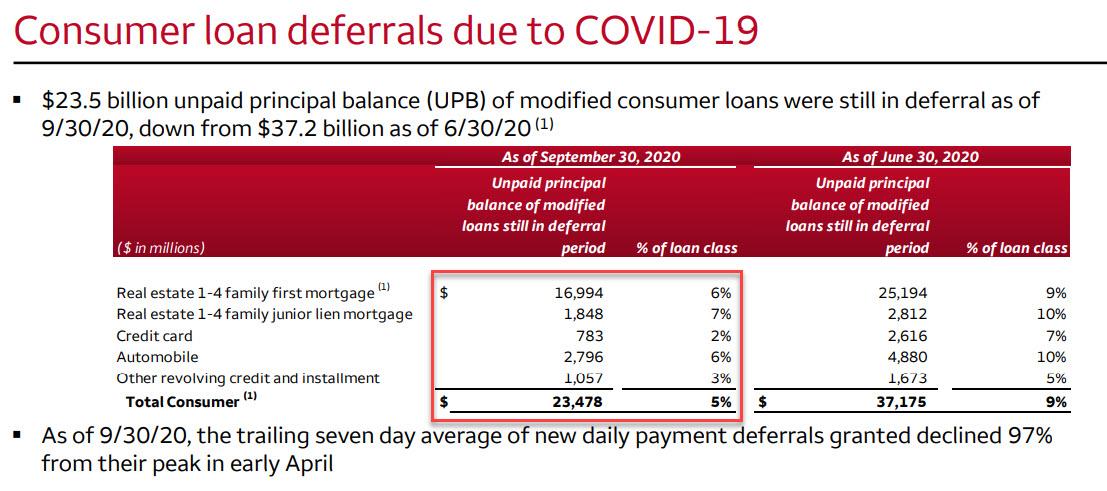

Expect these numbers to get far worse, as the bank implicit admitted when it warned that "customer forbearance and payment deferral activities instituted in response to the COVID-19 pandemic could delay the recognition of net charge-offs, delinquencies, and nonaccrual status for those customers who would have otherwise moved into past due or nonaccrual status."

Specifically, Wells revealed that $23.5 billion in unpaid principal balance of modified consumer loans were still in deferral as of 9/30/20, which while down from $37.2 billion as of 6/30/20, suggests that the charge-offs could get far worse especially since those who remain in forbearance are unlikely to revert to non-deferral.

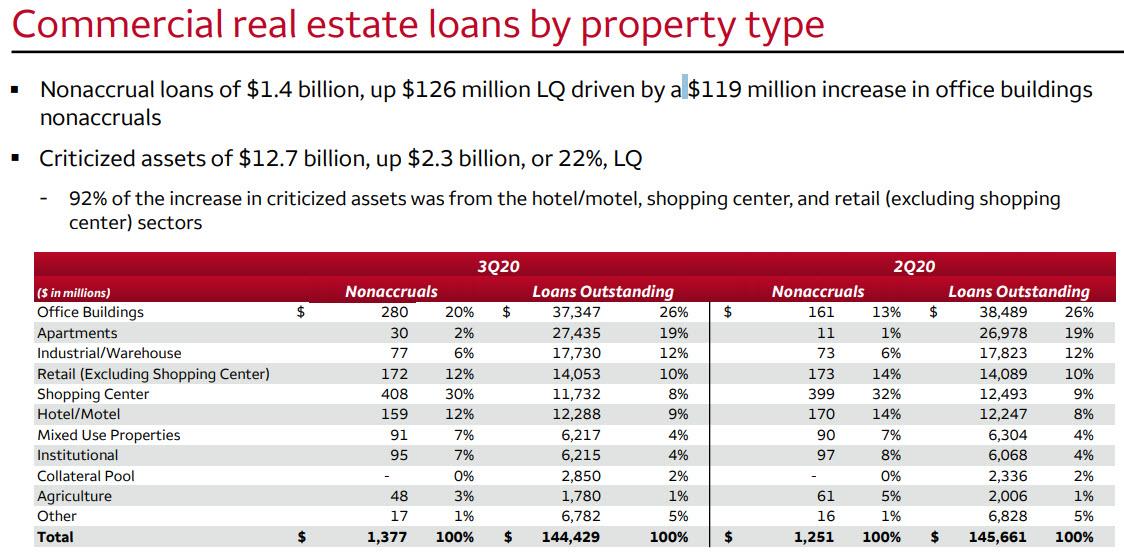

Wells Fargo was also kind enough to break out its exposure of loans by type, starting with CRE, where nonaccrual loans of $1.4 billion, rose by $126 million driven by a $119 million increase in office buildings nonaccruals as criticized assets of $12.7 billion, rose $2.3 billion, or 22%...

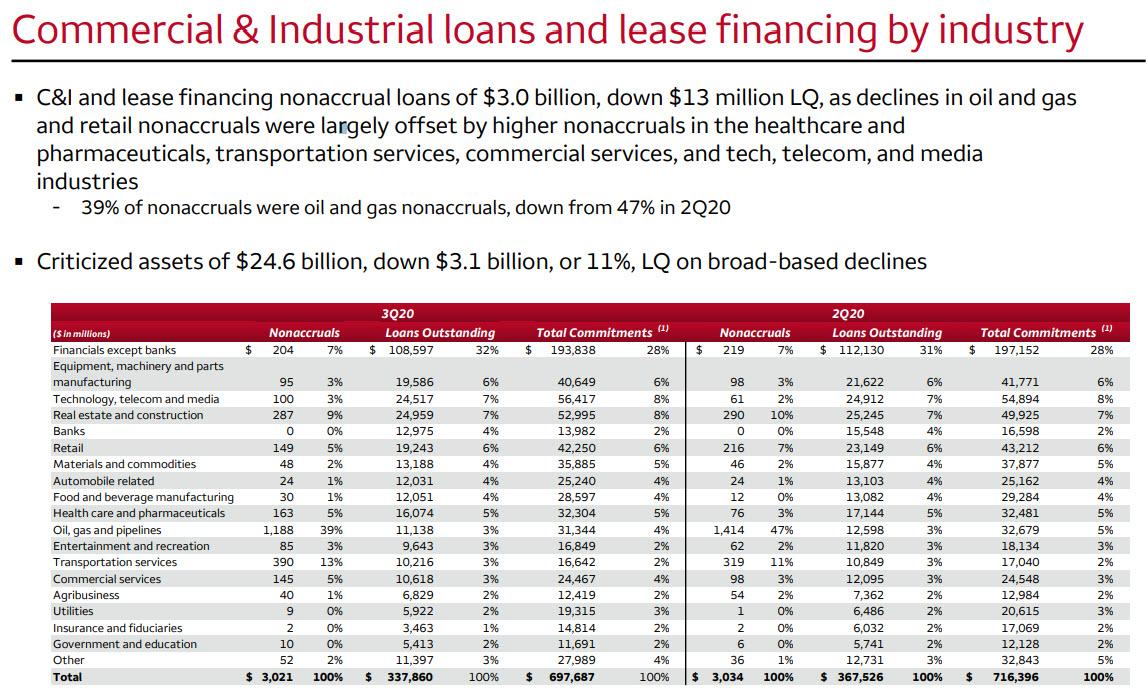

... while C&I and lease financing nonaccrual loans of $3.0 billion, were down $13 million Q/Q as declines in oil and gas and retail nonaccruals (39% of nonaccruals were oil and gas nonaccruals, down from 47% in 2Q20) were largely offset by higher nonaccruals in the healthcare and pharmaceuticals, transportation services, commercial services, and tech, telecom, and media industries. Total C&I criticized assets of $24.6 billion, were down $3.1 billion.

In total, Wells' allowance for credit losses (ACL) for loans was $20.5 billion, unchanged from last quarter, and "reflected an improving economic environment and solid credit performance in the quarter, but continued uncertainty due to COVID-19." On a percentage basis, the allowance coverage for total loans was 2.22%, up from 2.19% in 2Q20, due to a decline in total loans.

In short, Wells' headaches on its massive loan book are nowhere near over.

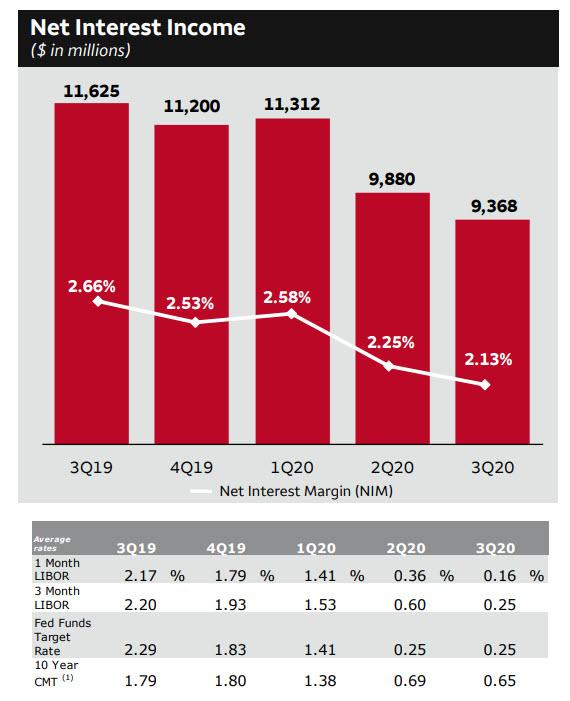

And unfortunately, this was visible in its Net Interest Income, which plunged by 19% Y/Y, or $2.3 billion, to just $9.4BN, missing expectations of $9.6BBN, and "reflecting the lower interest rate environment." Net interest income also decreased $512 million, or 5%, Q/Q "reflecting balance sheet repricing resulting from the lower interest rate environment, balance sheet mix shifts into lower yielding earning assets including the impact of lower commercial loans."

And, as expected at a time of record low rates, Wells' Net Interest Margin tumbled to a new all time lows of 2.13%, down 12bps Q/Q, and missing the estimate of 2.19% due to i) (11) bps from balance sheet repricing and mix; ii) (3) bps from MBS premium amortization; iii) (1) bp from hedge ineffectiveness accounting results; and iv) 3 bps from variable sources of income.

Noninterest income was slightly better, rising $1.5BN Q/Q but down nearly $900MM Y/Y, due to the following:

- Deposit-related fees up $157 million, or 14%, Q/Q on higher transaction volumes, one additional day in the quarter, and higher treasury management fees; Consumer was 56% and commercial was 44% of total

- Trust and investment fees up $163 million, or 5%, Q/Q on brokerage advisory, commissions and other fees up $219 million on higher retail brokerage advisory fees (priced at the beginning of the quarter); Trust and investment management fees up $50 million on higher asset-based fees; Investment banking fees down $106 million from record 2Q20 investment grade results.

- Card fees up $115 million, or 14%, Q/Q on higher interchange income driven by higher debit and credit card POS volumes

- Mortgage banking up $1.3 billion Q/Q as net gains on mortgage loan originations were up $243 million and included higher origination volumes and a higher gain on sale margin, while Servicing income was up $1.0 billion from a 2Q20 that included negative market-related MSR valuation changes.

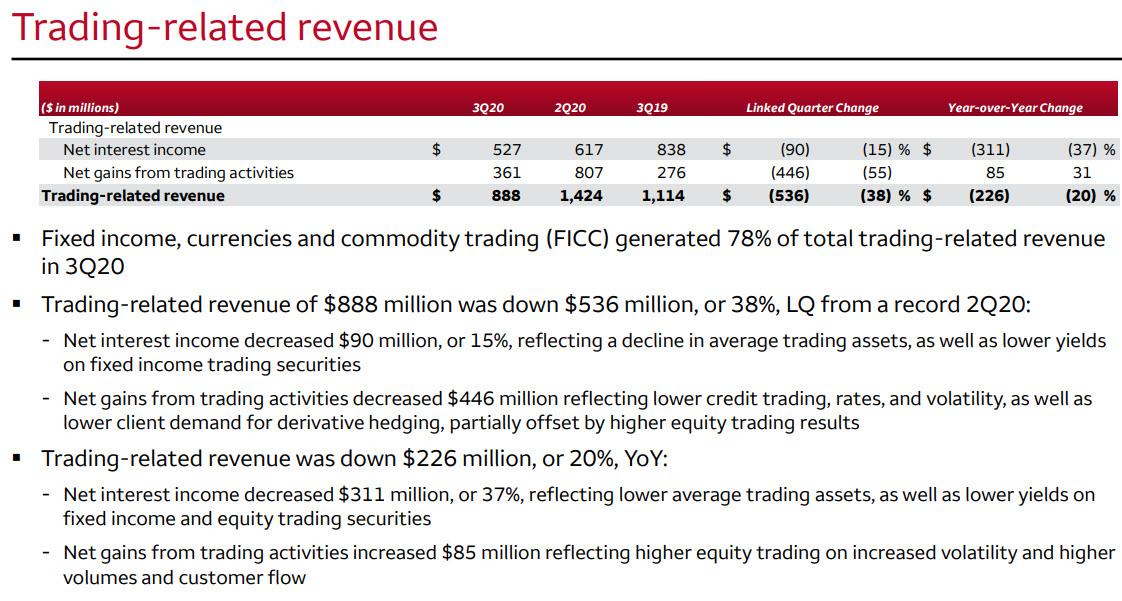

One remarkable - and recurring - aspect of Wells' revenues is just how poor its sales and trading performs compared to other banks. Perhaps Wells should hire the 50 best Robinhood traders to beef it up? Here are the details:

- Fixed income, currencies and commodity trading (FICC) generated 78% of total trading-related revenue in 3Q20;

- Trading-related revenue of $888 million was down $536 million, or 38%, Q/Q from a record 2Q20: Net interest income decreased $90 million, or 15%, reflecting a decline in average trading assets, as well as lower yields on fixed income trading securities; Net gains from trading activities decreased $446 million reflecting lower credit trading, rates, and volatility, as well as lower client demand for derivative hedging, partially offset by higher equity trading results

- Trading-related revenue was down $226 million, or 20%, YoY: Net interest income decreased $311 million, or 37%, reflecting lower average trading assets, as well as lower yields on fixed income and equity trading securities; Net gains from trading activities increased $85 million reflecting higher equity trading on increased volatility and higher volumes and customer flow.

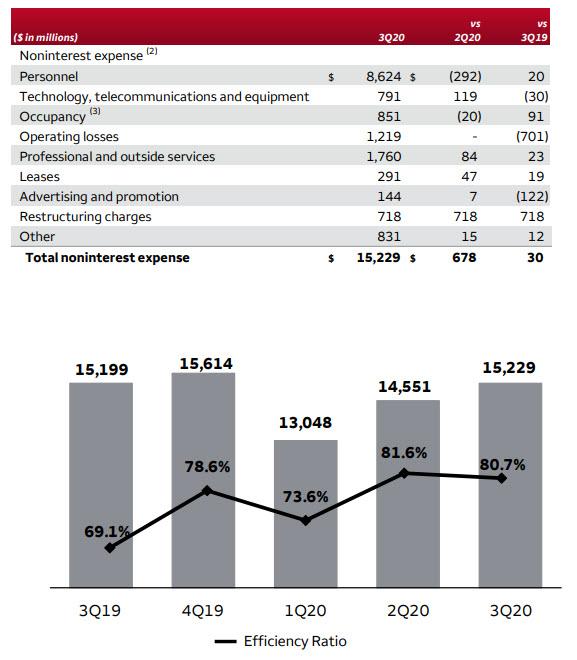

Away from revenues, the bank posted a surprise increase in third-quarter expenses which rose by $30MM Y/Y even as total revenues tumbles, as it set aside $961 million for customer remediation and $718 million in restructuring charges. That countered the abovementioned sharp drop loan-loss provisions that came in at less than half what analysts had expected. Some more details:

- Personnel expense down $292 million and included: i) $344 million lower deferred compensation expense; ii) $163 million decline in expenses in response to COVID-19 from a 2Q20 that included bonus payments and premium pay for certain customer-facing and support employees, as well as child care services benefits; iii) Higher salaries expense driven by one additional day in the quarter, and higher revenue-based incentive compensation.

- Technology, telecommunications and equipment expense up $119 million from a 2Q20 that included the reversal of an accrual for software expense.

- Operating losses remained at an elevated level and included $961 million of customer remediation accruals for a variety of matters reflecting expansion of populations, time periods, and/or amount of reimbursement

- Restructuring charges of $718 million, predominantly severance expense associated with expense reduction initiatives

As Bloomberg notes, in his first year atop Wells Fargo, CEO Charlie Scharf has been working to move the firm past a series of scandals. He’s tasked with making harmed customers whole, repairing relations in Washington and improving the firm’s earnings. He’s repeatedly lamented the firm’s high costs, pledging to ultimately shave $10 billion off annual expenses.

Quarterly results "reflect the impact of aggressive monetary and fiscal stimulus on the U.S. economy,” and were helped by “strong mortgage banking fees, higher equity markets, and declining sequential charge-offs,” CEO Charlie Scharf said in the bank’s statement. At the same time, "historically low interest rates reduced our net interest income and our expenses continued to remain elevated."

"The trajectory of the economic recovery remains unclear as the negative impact of Covid continues and further fiscal stimulus is uncertain." He added that Wells Fargo’s "top priority continues to be the implementation of our risk, control, and regulatory work", as he clearly wants to avoid any more trips for Wells Fargo to the Capitol.

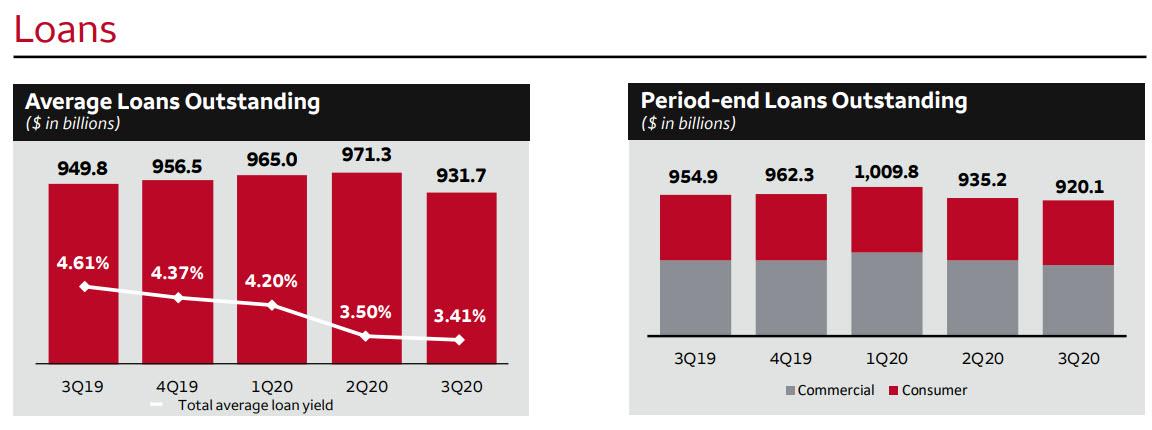

Finally, and perhaps the last nail in the coffin, Wells period-end loans continued to shrink, tumbling to $920.1 billion, down 4% or $34.8 billion year-over-year (YoY) "driven by lower commercial and industrial loans"...

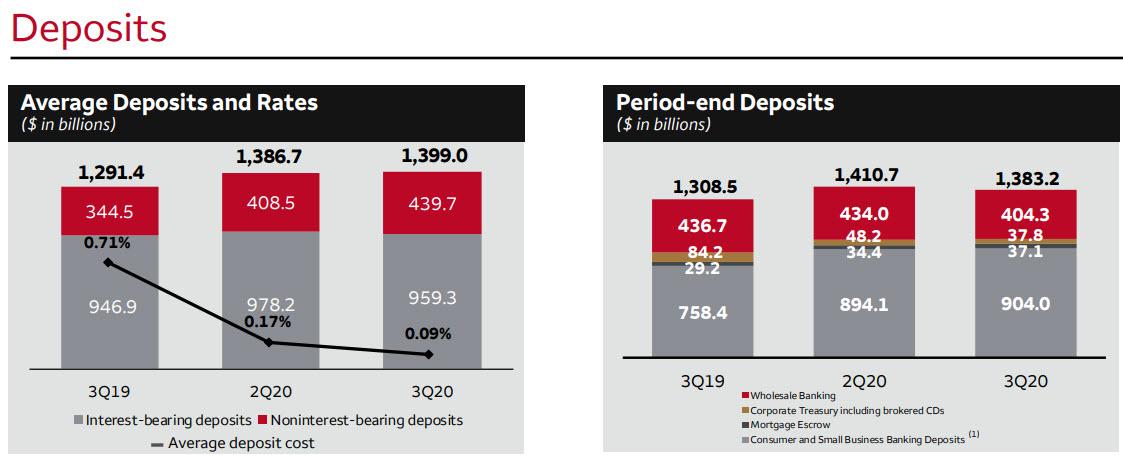

... meanwhile as we noted yesterday, deposits across the banking sector continued to rise, and hit $1.4TN on an average basis (if declining slightly to $1.383TN on a period end-basis largely due to a decline in Wholesale Banking deposits of $29.7 billion, or 7%,

due to actions taken to manage under the Asset Cap) due to an increase in consumer and small business banking deposits "reflecting customers’ preferences for liquidity due to COVID-19."

Not surprising after all this, the stock was sharply lower on the latest dismal earnings report by Wells. Wells shares have plunged 54% so far in 2020, worse than the 31% drop in the KBW Bank Index.

The full Wells earnings report is below (pdf link)

Uncategorized

Key shipping company files Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Tight inventory and frustrated buyers challenge agents in Virginia

With inventory a little more than half of what it was pre-pandemic, agents are struggling to find homes for clients in Virginia.

Share this:

No matter where you are in the state, real estate agents in Virginia are facing low inventory conditions that are creating frustrating scenarios for their buyers.

“I think people are getting used to the interest rates where they are now, but there is just a huge lack of inventory,” said Chelsea Newcomb, a RE/MAX Realty Specialists agent based in Charlottesville. “I have buyers that are looking, but to find a house that you love enough to pay a high price for — and to be at over a 6.5% interest rate — it’s just a little bit harder to find something.”

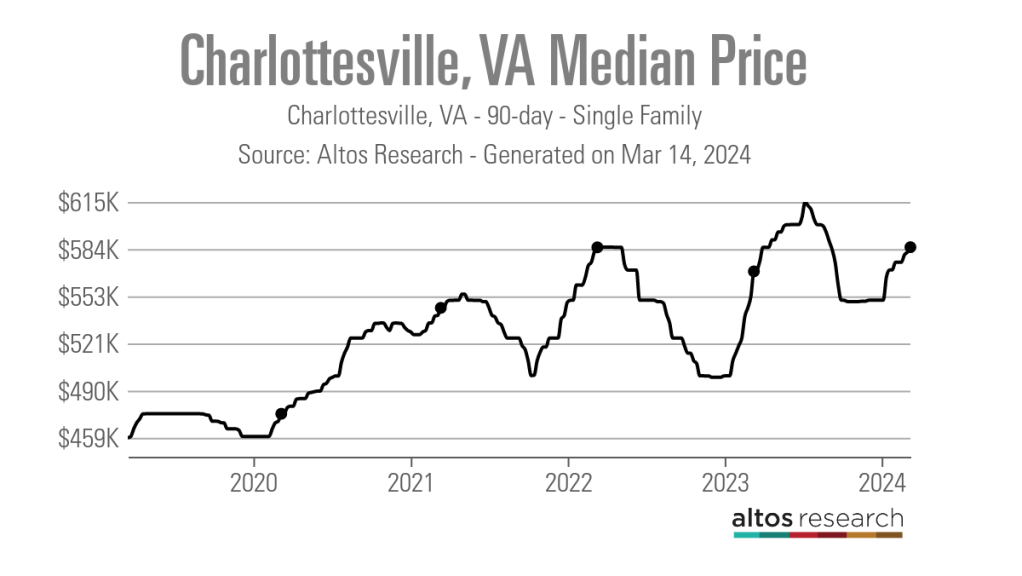

Newcomb said that interest rates and higher prices, which have risen by more than $100,000 since March 2020, according to data from Altos Research, have caused her clients to be pickier when selecting a home.

“When rates and prices were lower, people were more willing to compromise,” Newcomb said.

Out in Wise, Virginia, near the westernmost tip of the state, RE/MAX Cavaliers agent Brett Tiller and his clients are also struggling to find suitable properties.

“The thing that really stands out, especially compared to two years ago, is the lack of quality listings,” Tiller said. “The slightly more upscale single-family listings for move-up buyers with children looking for their forever home just aren’t coming on the market right now, and demand is still very high.”

Statewide, Virginia had a 90-day average of 8,068 active single-family listings as of March 8, 2024, down from 14,471 single-family listings in early March 2020 at the onset of the COVID-19 pandemic, according to Altos Research. That represents a decrease of 44%.

In Newcomb’s base metro area of Charlottesville, there were an average of only 277 active single-family listings during the same recent 90-day period, compared to 892 at the onset of the pandemic. In Wise County, there were only 56 listings.

Due to the demand from move-up buyers in Tiller’s area, the average days on market for homes with a median price of roughly $190,000 was just 17 days as of early March 2024.

“For the right home, which is rare to find right now, we are still seeing multiple offers,” Tiller said. “The demand is the same right now as it was during the heart of the pandemic.”

According to Tiller, the tight inventory has caused homebuyers to spend up to six months searching for their new property, roughly double the time it took prior to the pandemic.

For Matt Salway in the Virginia Beach metro area, the tight inventory conditions are creating a rather hot market.

“Depending on where you are in the area, your listing could have 15 offers in two days,” the agent for Iron Valley Real Estate Hampton Roads | Virginia Beach said. “It has been crazy competition for most of Virginia Beach, and Norfolk is pretty hot too, especially for anything under $400,000.”

According to Altos Research, the Virginia Beach-Norfolk-Newport News housing market had a seven-day average Market Action Index score of 52.44 as of March 14, making it the seventh hottest housing market in the country. Altos considers any Market Action Index score above 30 to be indicative of a seller’s market.

Further up the coastline on the vacation destination of Chincoteague Island, Long & Foster agent Meghan O. Clarkson is also seeing a decent amount of competition despite higher prices and interest rates.

“People are taking their time to actually come see things now instead of buying site unseen, and occasionally we see some seller concessions, but the traffic and the demand is still there; you might just work a little longer with people because we don’t have anything for sale,” Clarkson said.

“I’m busy and constantly have appointments, but the underlying frenzy from the height of the pandemic has gone away, but I think it is because we have just gotten used to it.”

While much of the demand that Clarkson’s market faces is for vacation homes and from retirees looking for a scenic spot to retire, a large portion of the demand in Salway’s market comes from military personnel and civilians working under government contracts.

“We have over a dozen military bases here, plus a bunch of shipyards, so the closer you get to all of those bases, the easier it is to sell a home and the faster the sale happens,” Salway said.

Due to this, Salway said that existing-home inventory typically does not come on the market unless an employment contract ends or the owner is reassigned to a different base, which is currently contributing to the tight inventory situation in his market.

Things are a bit different for Tiller and Newcomb, who are seeing a decent number of buyers from other, more expensive parts of the state.

“One of the crazy things about Louisa and Goochland, which are kind of like suburbs on the western side of Richmond, is that they are growing like crazy,” Newcomb said. “A lot of people are coming in from Northern Virginia because they can work remotely now.”

With a Market Action Index score of 50, it is easy to see why people are leaving the Washington-Arlington-Alexandria market for the Charlottesville market, which has an index score of 41.

In addition, the 90-day average median list price in Charlottesville is $585,000 compared to $729,900 in the D.C. area, which Newcomb said is also luring many Virginia homebuyers to move further south.

“They are very accustomed to higher prices, so they are super impressed with the prices we offer here in the central Virginia area,” Newcomb said.

For local buyers, Newcomb said this means they are frequently being outbid or outpriced.

“A couple who is local to the area and has been here their whole life, they are just now starting to get their mind wrapped around the fact that you can’t get a house for $200,000 anymore,” Newcomb said.

As the year heads closer to spring, triggering the start of the prime homebuying season, agents in Virginia feel optimistic about the market.

“We are seeing seasonal trends like we did up through 2019,” Clarkson said. “The market kind of soft launched around President’s Day and it is still building, but I expect it to pick right back up and be in full swing by Easter like it always used to.”

But while they are confident in demand, questions still remain about whether there will be enough inventory to support even more homebuyers entering the market.

“I have a lot of buyers starting to come off the sidelines, but in my office, I also have a lot of people who are going to list their house in the next two to three weeks now that the weather is starting to break,” Newcomb said. “I think we are going to have a good spring and summer.”

real estate housing market pandemic covid-19 interest ratesInternational

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

As the global pandemic unfolded, government-funded…

Share this:

As the global pandemic unfolded, government-funded experimental vaccines were hastily developed for a virus which primarily killed the old and fat (and those with other obvious comorbidities), and an aggressive, global campaign to coerce billions into injecting them ensued.

{kind=link}

Then there were the lockdowns - with some countries (New Zealand, for example) building internment camps for those who tested positive for Covid-19, and others such as China welding entire apartment buildings shut to trap people inside.

It was an egregious and unnecessary response to a virus that, while highly virulent, was survivable by the vast majority of the general population.

Oh, and the vaccines, which governments are still pushing, didn't work as advertised to the point where health officials changed the definition of "vaccine" multiple times.

Tucker Carlson recently sat down with Dr. Pierre Kory, a critical care specialist and vocal critic of vaccines. The two had a wide-ranging discussion, which included vaccine safety and efficacy, excess mortality, demographic impacts of the virus, big pharma, and the professional price Kory has paid for speaking out.

Keep reading below, or if you have roughly 50 minutes, watch it in its entirety for free on X:

Ep. 81 They’re still claiming the Covid vax is safe and effective. Yet somehow Dr. Pierre Kory treats hundreds of patients who’ve been badly injured by it. Why is no one in the public health establishment paying attention? pic.twitter.com/IekW4Brhoy

— Tucker Carlson (@TuckerCarlson) March 13, 2024

"Do we have any real sense of what the cost, the physical cost to the country and world has been of those vaccines?" Carlson asked, kicking off the interview.

"I do think we have some understanding of the cost. I mean, I think, you know, you're aware of the work of of Ed Dowd, who's put together a team and looked, analytically at a lot of the epidemiologic data," Kory replied. "I mean, time with that vaccination rollout is when all of the numbers started going sideways, the excess mortality started to skyrocket."

When asked "what kind of death toll are we looking at?", Kory responded "...in 2023 alone, in the first nine months, we had what's called an excess mortality of 158,000 Americans," adding "But this is in 2023. I mean, we've had Omicron now for two years, which is a mild variant. Not that many go to the hospital."

'Safe and Effective'

Tucker also asked Kory why the people who claimed the vaccine were "safe and effective" aren't being held criminally liable for abetting the "killing of all these Americans," to which Kory replied: "It’s my kind of belief, looking back, that [safe and effective] was a predetermined conclusion. There was no data to support that, but it was agreed upon that it would be presented as safe and effective."

Tucker Carlson Asks the Forbidden Question

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

He wants to know why the people who made the claim “safe and effective” aren’t being held to criminal liability for abetting the “killing of all these Americans.”

DR. PIERRE KORY: “It’s my kind of belief, looking back, that [safe and… pic.twitter.com/Icnge18Rtz

Carlson and Kory then discussed the different segments of the population that experienced vaccine side effects, with Kory noting an "explosion in dying in the youngest and healthiest sectors of society," adding "And why did the employed fare far worse than those that weren't? And this particularly white collar, white collar, more than gray collar, more than blue collar."

Kory also said that Big Pharma is 'terrified' of Vitamin D because it "threatens the disease model." As journalist The Vigilant Fox notes on X, "Vitamin D showed about a 60% effectiveness against the incidence of COVID-19 in randomized control trials," and "showed about 40-50% effectiveness in reducing the incidence of COVID-19 in observational studies."

Dr. Pierre Kory: Big Pharma is ‘TERRIFIED’ of Vitamin D

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

Why?

Because “It threatens the DISEASE MODEL.”

A new meta-analysis out of Italy, published in the journal, Nutrients, has unearthed some shocking data about Vitamin D.

Looking at data from 16 different studies and 1.26… pic.twitter.com/q5CsMqgVju

Professional costs

Kory - while risking professional suicide by speaking out, has undoubtedly helped save countless lives by advocating for alternate treatments such as Ivermectin.

Kory shared his own experiences of job loss and censorship, highlighting the challenges of advocating for a more nuanced understanding of vaccine safety in an environment often resistant to dissenting voices.

"I wrote a book called The War on Ivermectin and the the genesis of that book," he said, adding "Not only is my expertise on Ivermectin and my vast clinical experience, but and I tell the story before, but I got an email, during this journey from a guy named William B Grant, who's a professor out in California, and he wrote to me this email just one day, my life was going totally sideways because our protocols focused on Ivermectin. I was using a lot in my practice, as were tens of thousands of doctors around the world, to really good benefits. And I was getting attacked, hit jobs in the media, and he wrote me this email on and he said, Dear Dr. Kory, what they're doing to Ivermectin, they've been doing to vitamin D for decades..."

"And it's got five tactics. And these are the five tactics that all industries employ when science emerges, that's inconvenient to their interests. And so I'm just going to give you an example. Ivermectin science was extremely inconvenient to the interests of the pharmaceutical industrial complex. I mean, it threatened the vaccine campaign. It threatened vaccine hesitancy, which was public enemy number one. We know that, that everything, all the propaganda censorship was literally going after something called vaccine hesitancy."

Money makes the world go 'round

Carlson then hit on perhaps the most devious aspect of the relationship between drug companies and the medical establishment, and how special interests completely taint science to the point where public distrust of institutions has spiked in recent years.

"I think all of it starts at the level the medical journals," said Kory. "Because once you have something established in the medical journals as a, let's say, a proven fact or a generally accepted consensus, consensus comes out of the journals."

"I have dozens of rejection letters from investigators around the world who did good trials on ivermectin, tried to publish it. No thank you, no thank you, no thank you. And then the ones that do get in all purportedly prove that ivermectin didn't work," Kory continued.

"So and then when you look at the ones that actually got in and this is where like probably my biggest estrangement and why I don't recognize science and don't trust it anymore, is the trials that flew to publication in the top journals in the world were so brazenly manipulated and corrupted in the design and conduct in, many of us wrote about it. But they flew to publication, and then every time they were published, you saw these huge PR campaigns in the media. New York Times, Boston Globe, L.A. times, ivermectin doesn't work. Latest high quality, rigorous study says. I'm sitting here in my office watching these lies just ripple throughout the media sphere based on fraudulent studies published in the top journals. And that's that's that has changed. Now that's why I say I'm estranged and I don't know what to trust anymore."

Vaccine Injuries

Carlson asked Kory about his clinical experience with vaccine injuries.

"So how this is how I divide, this is just kind of my perception of vaccine injury is that when I use the term vaccine injury, I'm usually referring to what I call a single organ problem, like pericarditis, myocarditis, stroke, something like that. An autoimmune disease," he replied.

"What I specialize in my practice, is I treat patients with what we call a long Covid long vaxx. It's the same disease, just different triggers, right? One is triggered by Covid, the other one is triggered by the spike protein from the vaccine. Much more common is long vax. The only real differences between the two conditions is that the vaccinated are, on average, sicker and more disabled than the long Covids, with some pretty prominent exceptions to that."

Watch the entire interview above, and you can support Tucker Carlson's endeavors by joining the Tucker Carlson Network here...

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Tight inventory and frustrated buyers challenge agents in Virginia

The Question You Should Ask Whenever You’re Wrong

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International7 days ago

International7 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International6 days ago

International6 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges