Varo’s bank charter milestone, more corporate cards and BNPL under a microscope

Welcome to The Interchange! If you received this in your inbox, thank you for signing up and your vote of confidence. If you’re reading this as a post…

Welcome to The Interchange! If you received this in your inbox, thank you for signing up and your vote of confidence. If you’re reading this as a post on our site, sign up here so you can receive it directly in the future. Every week, I’ll take a look at the hottest fintech news of the previous week. This will include everything from funding rounds to trends to an analysis of a particular space to hot takes on a particular company or phenomenon. There’s a lot of fintech news out there and it’s my job to stay on top of it — and make sense of it — so you can stay in the know. — Mary Ann

First off, I have to say that this past week was one of the busiest fintech news weeks I have experienced in a long while. Whoa. So.much.going.on. While I couldn’t obviously cover it all, I attempted to fit as much of it as I could into this newsletter.

Before we get into the various news items from the past week, let’s talk about bank charters.

For the unacquainted, according to Investopedia: “A chartered bank is a financial institution (FI) whose primary roles are to accept and safeguard monetary deposits from individuals and organizations, as well as to lend money out. Chartered bank specifics vary from country to country. However, in general, a chartered bank in operation has obtained a form of government permission to do business in the financial services industry. A chartered bank is often associated with a commercial bank.”

In 2020, digital bank Varo became the first-ever all-digital nationally chartered U.S. consumer bank — meaning it received approval from the Office of the Comptroller of the Currency to become an actual bank, as opposed to partnering with one as most digital banks do.

It was a bold, and risky, move. So I talked to Varo CEO and founder Colin Walsh to find out if it was worth it. His answer? 100%.

To read my full interview with Walsh on just how things have been going since, head here.

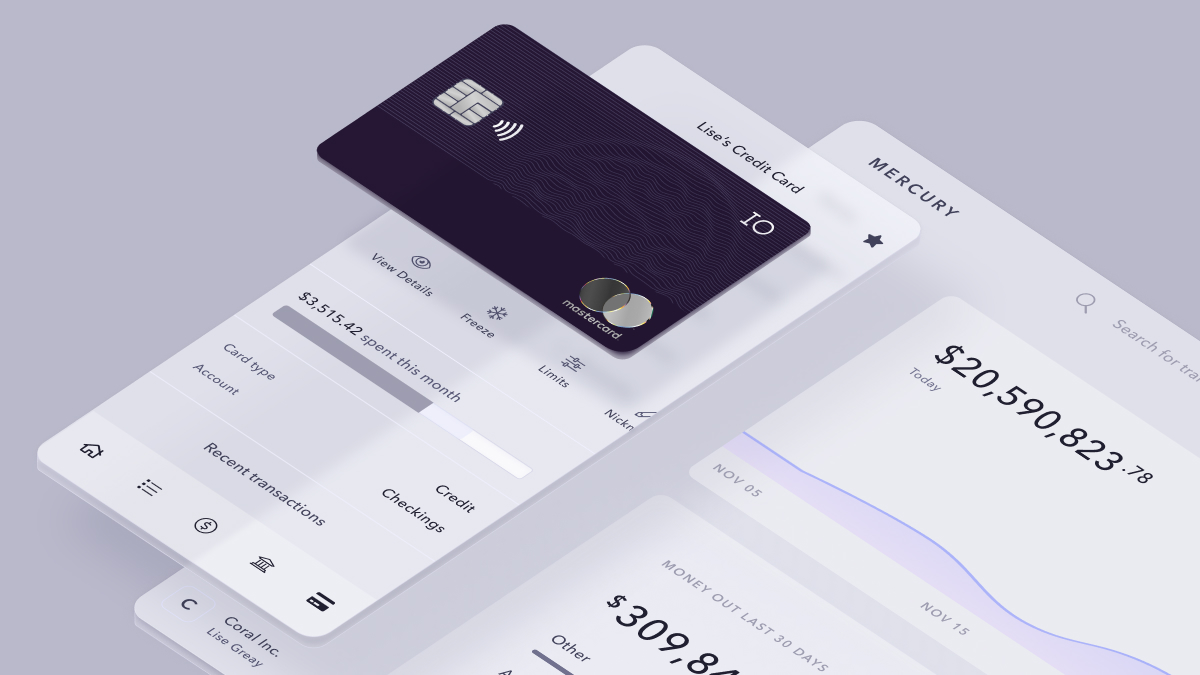

The corporate cards just keep on coming

Mercury announced last week that it launched a new corporate credit card. Via email, a spokesperson told me that the IO Mastercard is designed to help startups scale their business. “It’s straightforward 1.5% cashback on everything, no personal credit check and the first step to qualifying for the card is having just $50,000 in a Mercury account.”

The company added that a corporate credit card has been one of the most requested features from customers since Mercury launched in 2019. In fact, Mercury actually considered launching with a credit card as its first product but instead chose to start with creating a bank account instead since “every founder needs a bank account to run their business…and [they] are the ideal foundation from which to build additional financial features.” The move is admittedly an effort to carve out its own space against the likes of Brex and Ramp.

Meanwhile, European fintech Payhawk announced that it is launching in the U.S. with a focus on enterprise customers. As part of that move, it is also launching its — you guessed it — first credit card product in the U.S. The move follows what a spokesperson describes as “a huge year” for the company: Over the last 12 months, it grew revenue by over 520%. The company achieved unicorn status after extending its Series B round to $215 million.

We’re not done yet! Center, which was co-founded by former Concur CEO and co-founder Steve Singh and launched its own corporate card and expense software offering aimed at small- and medium-sized enterprises, recently shared that in the last year, it tripled its customer base “while retaining 94% of existing customers” and doubled the company size. This is particularly interesting because many of the existing corporate card players often point to Concur as an incumbent that they are trying to replace.

These companies, of course, join a plethora of others in the U.S. already offering corporate cards, including — but not limited to — Brex, Ramp, Airbase, Mesh Payments and Rho.

Image Credits: Mercury

Weekly News

Adyen announced on September 15 that it has become the first fintech to partner with Cash App (Block) to offer Cash App Pay, a mobile payment method, to its U.S. customers. Adyen said its businesses will be giving customers a way to pay using their Cash App balance or linked debit card. Cash App COO Owen Jennings said in a written statement: “As the first financial technology platform outside of the Square ecosystem to launch Cash App Pay, we look forward to seeing the value this partnership brings to our customers and Adyen’s businesses.” An Adyen spokesperson told me via email: “The partnership will provide Adyen business customers access to over 80 million active customers that make up a third of Millennial and Gen Z consumers in the U.S. Their customers, in turn, will be provided with another convenient, seamless way to pay at checkout that fits their unique financial needs and habits.”

Speaking of Block, the company formerly known as (and still goes by sometimes) Square announced last week that its entire ecosystem of more than 35 products and services is now available in Spanish to sellers in the United States. This means that millions of Hispanic-owned businesses in the U.S. will have the ability to use Square in English or Spanish, “including key products like Square Banking to unlock access to financial services and Square for Restaurants to enable seamless, bilingual communication between front- and back-of-house staff.”

While we’re on the topic of payments, Goldman Sachs and Modern Treasury announced they are partnering “to accelerate the shift to embedded payments, helping joint customers embed and scale payments into products.” Via email, a Goldman Sachs spokesperson told me that the partnership furthers “Goldman’s push to better serve mid-market companies that have long wanted to bank with Goldman.” In a written statement, Eduardo Vergara, head of product and sales at Goldman Sachs Transaction Banking, said, “Embedding payments into software products is increasingly the trajectory of commerce, and by partnering with Modern Treasury, we are creating new opportunities for clients to seamlessly leverage our payments capabilities within their own platforms.”

In other Goldman Sachs news, Bloomberg reported that the investment banking and financial services giant is “embarking on its biggest round of jobs cuts since the start of the pandemic.” The publication cited people with knowledge of the matter who said that Goldman “plans to eliminate several hundred roles starting this month.”

Buy now, pay later made headlines several times last week. First, the Associated Press reported that (unsurprisingly, and sadly) while “Americans have grown fond of ‘buy now, pay later’ services… the “pay later” part is becoming increasingly difficult for some borrowers.” Meanwhile, TechCrunch’s Kyle Wiggers reported that the U.S. Consumer Financial Protection Bureau (CFPB) on September 15 “issued a report suggesting that companies like Klarna and Afterpay, which allow customers to pay for products and services in installments, must be subjected to stricter oversight.” Meanwhile, Affirm CEO Max Levchin told Bloomberg Law in an interview: “A fair amount of what the report has called for we have chosen to do. We have always seen this as a lending activity subject to all the lending rules and regulations.”

Proptechs continue to take a hit. Residential real estate marketplace Sundae last week conducted its second layoff this year. About 28% of the team — mostly sales and support staff — were laid off. Specifically, about 106 employees were let go. I reached out to the company for confirmation and a spokesperson told me via email that “Sundae is focusing on creating a more streamlined customer experience so that we can get offers to sellers even faster. The market remains volatile and we saw layoffs as an opportunity to use data and technology to streamline our approach and improve our customer experience. We also saw these decisions as an opportunity to build a longer runway.” I covered the company’s 2021 raise here.

In more uplifting personnel news, Forage — a payments processor that aims to make it easier for grocers to accept SNAP EBT payments online — revealed that Kristina Herrmann is joining the company in the new role of chief business officer. She comes to Forage after nearly 16 years at Amazon, where she most recently built out and led the company’s underserved populations team as its founder and general manager. Earlier this year, I wrote about how Ofek Lavian left his role as Instacart’s head of payments to join Forage. Today, he serves as the startup’s CEO.

FIS has launched Worldpay for Platforms, an embedded finance solution aimed at SMBs. Businesses that use the offering, FIS told me via email, “eliminate the need for SMBs to pay separate partners to help with card issuance, cash advances or faster access to cash flow.” Obviously, this has implications for companies such as Stripe or Plaid, or other embeddable products that target the small business marketplace.

ICYMI: Revolut recently announced a new online checkout feature, Revolut Pay, that “lets consumers pay at an online checkout with just one click.”

Whew. That was a lot, and if this week was any indication, the fourth quarter is going to be crazy. I’m heading out now in an attempt to refresh this weekend. Hope you’re doing the same! See you next week! xoxoxo Mary Ann

In case you have been hiding under a rock and haven’t heard, TechCrunch Disrupt is coming to San Francisco October 18–20! I would absolutely love to see you there. Use the code INTERCHANGE to get 15% off passes (excluding online and expo), or simply click here.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}