US Futures Dip From Record As Chinese Stocks Soar

US Futures Dip From Record As Chinese Stocks Soar

US equity futures slipped from record highs, European stocks held steady at the start of a new week and Chinese stocks soared the most in five weeks, as investors awaited a fresh round of…

Share this:

US equity futures slipped from record highs, European stocks held steady at the start of a new week and Chinese stocks soared the most in five weeks, as investors awaited a fresh round of corporate earnings with global shares sitting at record highs. The dollar slid following the crypto rout over the weekend. Gold rose and oil was flat.

At 07:30 a.m. ET, Dow E-minis were down 81points, or 0.24%, S&P 500 E-minis were down 10.75 points, or 0.26%, and Nasdaq 100 E-minis were down 46points, or 0.3% after briefly rising above Friday’s close during the European morning. Notable movers included Activision Blizzard and PayPal which fell in premarket trading. Tesla slid 1.6% following a deadly crash involving a 2019 Model S that no one appeared to be driving. IBM and United Airlines are due to report.

Looking at global markets, the MSCI world equity index climbed to a new peak, up 0.2% despite the weakness in US futures. Blockbuster economic data from China and the US last week pushed the MSCI All-Country World Index to another record despite concerns surrounding the spread of Covid-19 variants. New infections in the past week surpassed 5.2 million, the most since the pandemic began, with emerging markets (i.e. India, Brazil) getting hit the hardest.

A pullback in 10-year bond yield from 14-month highs in April has also eased worries about higher borrowing costs, renewing interest in richly valued technology stocks. As Goldman explained over the weekend, the risk of another destabilizing increase in borrowing costs has also subsided, as bond yields have pulled back from recent highs amid rising investor concerns that the peak of the stimulus surge is now behind us. This week traders will look for further confirmation of the private sector’s recovery from the pandemic as the earnings season gathers pace.

And speaking of economic data, it takes a back seat this week to earnings as 79 S&P 500 companies report results this week including Johnson & Johnson, Netflix Inc, Intel Corp, Honeywell and Schlumberger.

"Our current view is that with short-term interest rates set to remain low for the medium term and our expectation that earnings will continue to increase, it is unlikely that the increase in long-term interest rates will trigger an equity market fall," Russel Chesler, head of investments and capital markets at VanEck Australia, said in a note.

Europe’s STOXX 600 rose to a record high before easing some gains, and was flat at last check erasing earlier gains. Here are some of the biggest European movers today:

- Juventus shares rise as much as 14%, the most in a year after the Italian soccer club joins some of the game’s wealthiest teams in announcing plans for a new “super league” that could transform revenue streams at the top level of the sport.

- Arjo shares rise as much as 9.6% to a record high, as Swedish business daily Dagens Industri reiterates its recommendation to buy the shares of the medical-equipment maker.

- Danone shares rise 1.2% after Bernstein notes that a sector rotation from consumer staples to those benefiting from economic reopening appears to be finished. The firm also raises the price target for the French food-processing company.

- L’Oreal shares rise 1.3%. The company’s progress with e-commerce will help margins in the years to come, according to Goldman Sachs, which boosts the French beauty-products maker’s PT to a Street high while adding the stock to its “Conviction List.”

- Pantheon Resources shares fall as much as 54%, the most since April 2018, after saying that the Kuparuk formation in Alaska was more “geologically complex” than expected.

- Piraeus shares fall 30% to a record low as it resumes trading after reverse split and par value adjustment, with EU4.784 adjusted opening price.

Matthias Scheiber, global head of portfolio management at Wells Fargo Asset Management cited low interest rates, the rollout of COVID-19 vaccines and the fiscal stimulus package in the United States as reasons for his bullish stance on equities.

“Risk is coming down, volatility is coming down … we see the slow reopening of global economies, the rollout of the vaccine and the huge catch-up in demand so from that perspective it should be positive for economic growth. We had a strong rally in cyclical and value stocks since the start of this year - we would like to see confirmation in the earnings.”

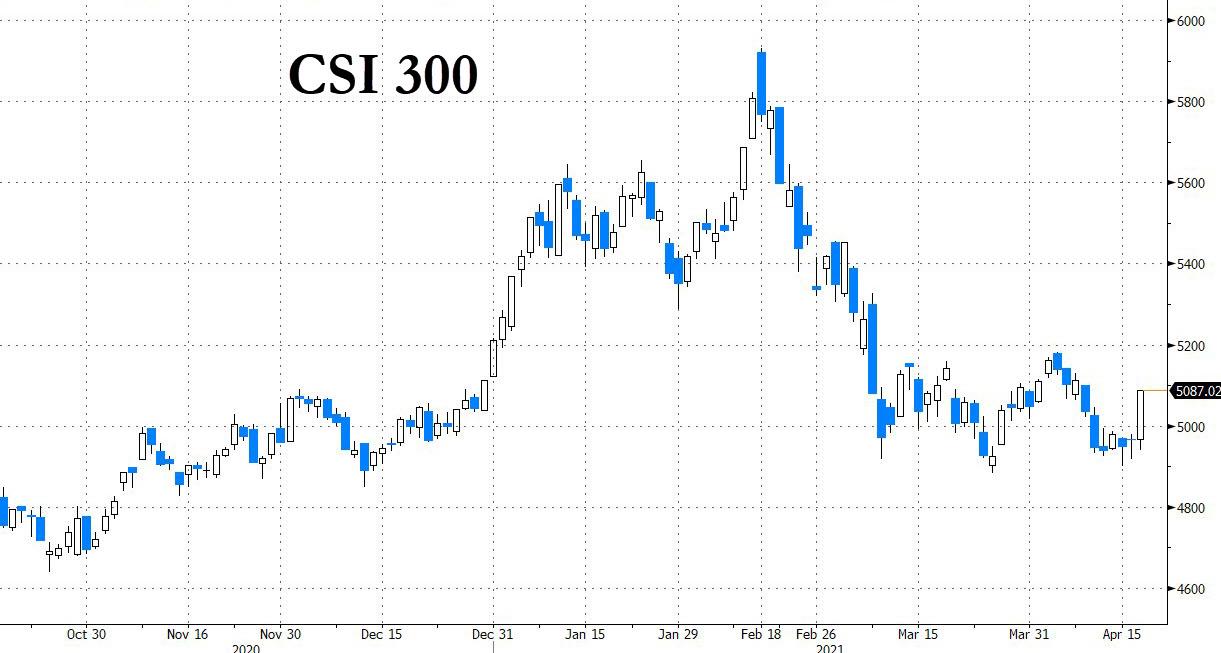

Earlier in the session, Asian stocks rose after a dip in early trading, led by Chinese stocks that had their best day in five weeks. The MSCI Asia Pacific Index is set to climb for the fifth straight session, its longest winning streak in more than two months, amid lower longer-term U.S. Treasury yields. Health care and materials led gains for the gauge, which was up as much as 0.5%.

China’s CSI 300 Index closed 2.4% higher to become the region’s best performing major national benchmark amid easing concerns about the health of state enterprise China Huarong Asset Management, the country's iconic distressed-debt manager which itself is so distressed many speculated Beijing will let if fail. China’s financial regulator on Friday said Huarong had ample liquidity, the first official comments since the company missed a deadline to report earnings. Ebbing fears of contagion drove a rally in Huarong bonds.

Also in China, shares of automakers jumped on Huawei’s plan to invest in car technologies, while electronics firms rose ahead of Apple’s first product unveiling of 2021. Japan’s Topix ended the day down 0.2% as the governors of Tokyo and Osaka considered declaring another virus emergency as infections surge. The country posted a double-digit gain in exports for the first time in more than three years in March, official data showed Monday. India’s Sensex index slid 1.8%, the worst performer in Asia, as daily new coronavirus infections continue to top previous highs.

Wells Fargo Asset Management’s Matthias Scheiber said “We believe we are in the ‘buy the dip’ environment at this moment given that both fiscal and monetary policy are very supportive, so if we would see a correction … we would probably increase the equity position.”

In rates, the benchmark U.S. Treasury yield, which dropped as low as 1.528% last Thursday, was at 1.5782%. Yields were lower by less than 1bp across the curve within spreads likewise little changed; 10-year TSY outperforming bunds by ~2bp while broadly keeping pace with gilts. Treasuries held small gains with S&P 500 futures under pressure despite strong gains for Chinese stocks. Options activity picked up during Asia session, including large trades in 5- and 10-year tenors. Overnight UST options activity included large bearish block trade via Jun21 10-year put spread and 5-year blocks re-jigging a big short position. Another heavy corporate new-issue slate is expected this week, a possible source of hedging flows.

In FX, the greenback fell against all of its G10 peers while the euro rose beyond $1.2030, the highest since March 4, amid news that Pfizer and BioNTech will supply the EU with an additional 100 million vaccine doses this year; Treasuries gained, outperforming bunds. The pound rose for a sixth straight session against the U.S. dollar, as the U.K.’s swift vaccination program and reopening schedule continued to bolster investor confidence. The yen also advanced as renewed tensions between U.S. and Russia spurred demand for haven assets; China rejected criticism from U.S. and Japanese leaders, adding to the risk-off sentiment. Australia’s dollar erased a drop as a rally in iron-ore prices offset weakness fueled by rising U.S.-China tensions.

“We have been highlighting over the past two months that USD could bottom out, in contrast to consensus, and believed that this would be a tactical problem for EM and for certain commodity trades,” wrote JP Morgan’s head of global and European equity strategy, Mislav Matejka, in a note to clients. “We think the risk of a firmer USD, through rising US-Europe interest rate differential, is not finished.”

Matejka also said that, although there is the technical potential for a correction in equities, he would not cut stocks exposure on the six- to nine-month horizon: “We think that it is more likely that we will be raising our year-end targets, rather than reducing them, as we move through the summer,” he said.

In commodities, oil prices fell as rising COVID-19 infections in India prompted concern than stronger measures to contain the pandemic would hurt economic activity. A recent surge in COVID-19 cases could see major parts of Japan slide back into states of emergency, with authorities in Tokyo and Osaka looking at renewed curbs.

Bitcoin was up 1% at around $56,850, nursing losses from Sunday, when it plunged as much as 14% to $51,541.

Looking at the week's events, economic data is sparse and no Fed speakers scheduled ahead of April 28 FOMC meeting. Instead attention will be on earnings from IBM which are due later in the session. Netflix reports on Tuesday. Later in the week, American Airlines and Southwest will be the first major post-COVID cyclicals to post results. The European Central Bank meeting on Thursday will also be in focus this week. ECB President Christine Lagarde said last week that the euro zone economy is still standing on the “two crutches” of monetary and fiscal stimulus and these cannot be taken away until it makes a full recovery.

Market Snapshot

- S&P 500 futures down 0.1% to 4,172.00

- MXAP up 0.3% to 209.28

- MXAPJ up 0.3% to 697.59

- Nikkei little changed at 29,685.37

- Topix down 0.2% to 1,956.56

- Hang Seng Index up 0.5% to 29,106.15

- Shanghai Composite up 1.5% to 3,477.55

- Sensex down 1.7% to 47,982.83

- Australia S&P/ASX 200 little changed at 7,065.64

- Kospi little changed at 3,198.84

- German 10Y yield fell 0.6bps to -0.268%

- Euro up 0.3% to 1.2024

- Brent Futures down 0.1% to $66.70/bbl

- Gold spot up 0.5% to $1,785.97

- U.S. Dollar Index down 0.40% to 91.19

Top Overnight News from Bloomberg

- Markus Soeder’s bid to lead Angela Merkel’s conservative bloc into September’s German election is gathering pace, with Monday’s imminent announcement by the Greens of their chancellor candidate adding to pressure to end the deadlock

- Russia hit back defiantly after the U.S. warned of “consequences” if jailed opposition leader Alexey Navalny dies on hunger strike, deepening the conflict over the dissident who’s already survived an alleged assassination attempt

- China sought to allay fears it wants to topple the dollar as the world’s main reserve currency as Beijing makes bigger strides in creating its own digital yuan

- Deutsche Bank AG is replacing its global pricing engine for emerging-market currencies in London with one in Singapore, drawn by surging trading in Asia and the increasing importance of the Chinese yuan

- The mania that drove crypto assets to records as Coinbase Global Inc. went public last week turned on itself on the weekend, sending Bitcoin tumbling the most since February

- U.K. house prices surged to a record this month with a tax break on purchases and rock-bottom interest rates prompting a “buying frenzy,” the property website Rightmove said

- The unprecedented oil inventory glut that amassed during the coronavirus pandemic is almost gone, underpinning a price recovery that’s rescuing producers but vexing consumers.

A quick look at global markets courtesy of Newsquawk

Asian equity markets began the week with mostly cautious gains and US equity futures marginally pulled back from record highs with participants tentative ahead of further earning updates this week, and as COVID-19 uncertainty lingered after the number of global cases last week increased by over 5.2mln, which was a record despite the ongoing vaccination drive. However, there were comments from NIH's Dr Fauci that a decision on whether to resume administering the Johnson & Johnson COVID-19 vaccine could occur as soon as Friday and that he would not be surprised if it is resumed in some form. ASX 200 (+0.2%) was positive with the kept afloat by outperformance in mining-related sectors and with M&A developments providing encouragement following news of a merger between Galaxy Resources and Orocobre, as well as reports that Crown Resorts received an unsolicited proposal on behalf of funds managed by Oaktree Capital. Nikkei 225 (+0.2%) initially swung between gains and losses as pressure from currency inflows was offset by stronger than expected trade data - including the largest increase in exports since November 2017 - and although Japanese stocks eventually improved, Toshiba shares were left in the lurch after CVC was said to plan a delay in submitting a formal proposal to acquire the Co. Hang Seng (+0.8%) and Shanghai Comp. (+1.3%) shrugged off the flat open and the continued US-China verbal jousting, to outperform their regional peers with the Hang Seng extending above the 29k level and strength seen in Chinese automakers after Huawei unveiled its intelligent driving system. There were also constructive comments regarding China Huarong Asset Management in which the CBIRC Vice Head stated the Co. is currently operating normally with ample liquidity and Chinese regulators were also said to have asked some banks not to withhold loans to the Co., while India's NIFTY (-2.4%) was heavily pressured amid ongoing rampant COVID-19 cases which hit a fresh record high and with the capital of New Delhi said to have less than 100 ICU beds available in the entire city. Finally, 10yr JGBs were slightly higher amid the mild gains in T-notes and a relatively tepid BoJ purchase announcement totalling JPY 500bln mostly concentrated in 3yr-5yr maturities, while Aussie yields were also relatively unmoved after the RBA announcement to purchase AUD 2bln of government bonds.

Top Asian News

- Packer Gets Crown Exit Path With $2.3 Billion Oaktree Offer

- China Stocks Book Best Day in 5 Weeks as Tech, Car Firms Gain

- Top India Homebuilder Drops in Debut After Decade-Long IPO Wait

- Chinese Travel Site Trip.com Rises 4.6% in Hong Kong Debut

European equities kick off the trading week with another mixed/directionless session thus far (Euro Stoxx 50 -0.1%) despite the positive APAC handover, and amidst a lack of fresh catalysts as participants continue to ponder over the rising COVID cases globally alongside the broader recovery with the vast fiscal and monetary support present. US equity futures meanwhile are somewhat varied and have a negative bias, with the ES and NQ flat whilst the cyclically-driven RTY narrowly lags. Analysts at JPM noted that some technical and sentiment indicators are becoming stretched after the recent run higher across stocks. That being said, the analysts say they would not be reducing stocks exposure on a six-to-nine month horizon whilst acknowledging the potential for a technical correction - JPM continue to see dips as buys. Back to Europe, cash markets see no major outlier in terms of performance whilst sectors are similarly mixed, with outperformance seen Travel & Leisure whilst the early gains in the Auto sector, following the 2021 Shanghai Motor Show, faded with the sector now the laggard. Overall the sectors do now portray and over-arching theme. In terms of individual movers, ABN AMRO (+1.4%) trades firmer after the Co. has accepted the payment of EUR 480mln to settle an anti-money laundering investigation. Bayer (+1.4%) is also supported as the US FDA granted Orphan Drug status for Co's Aliqopa for chronic lymphocytic leukaemia and small lymphocytic lymphoma. Conversely, CNH Industrial (-5.1%) sits at the foot of the Stoxx after it terminated discussions with FAW Jiefang around the On-Highway business, but will still continue with plans to spin-off the unit from 2022 onwards.

Top European News

- HSBC Top Staff to Hot Desk After Scrapping Executive Floor

- Juventus Stock Jumps Most in a Year Amid Super League Plan

- Pfizer, BioNTech to Supply EU With 100M Additional Doses in 2021

- Piraeus Bank Falls 30% After Share Capital Increase Terms

In FX, the Dollar and index have extended declines across the board as US Treasury yields maintain a mild bull-flattening bias, but also on increasingly bearish technical momentum as several Buck/major pairings breach key and psychological levels and the DXY itself breaches 91.500 to probe support around 91.300 within a 91.748-125 band. However, the index and Greenback in general may benefit from underlying bids into 91.000 given that the 100 DMA is in very close proximity at 91.019 today.

- JPY/NZD/AUD - Better than expected Japanese trade data could be helping the Yen compound gains vs its US counterpart, and at this stage 108.00 appears far more achievable than a rebound towards 108.50 where the base of decent option expiry interest resides (1.9 bn from the half round number up to 109.65 to be precise). Meanwhile, the Kiwi and Aussie are taking advantage of their US peer’s predicament to form firmer bases above 0.7150 and 0.7750 respectively ahead of RBA minutes and NZ Q1 CPI on Tuesday.

- CHF/EUR/GBP/CAD - Little sign of Franc buyers getting twitchy about a relatively big rise in Swiss sight deposit balances at domestic banks, as Usd/Chf tests 0.9150 and Eur/Chf eyes 1.1000 even though the single currency has made light work of breaching supposed option barriers at 1.2000 against the Dollar. Elsewhere, Cable is approaching 1.3900 after holding just above the big figure below and the Pound is starting the new week in a much better position vs the Euro after the cross reached circa 0.8719 last Friday, with Eur/Gbp now pivoting 0.8650. Similarly, the Loonie has turned the tables on its US rival to regain 1.2500+ status in advance of Canada’s first Federal Budget since 2019 then CPI and the BoC on Wednesday.

- SCANDI/EM/PM - The Nok and Sek have picked up where they left off last week, on the front foot, with the former outperforming through 10.0000 vs the Eur and latter straddling 10.1000, while most EM currencies are benefiting from Usd weakness bar the Rub that remains below 76.0000 amidst ongoing investor jitters about Russia’s deteriorating international relations and stand-off with Ukraine. Turning to commodities, Xau has taken a bit of a breather before continuing its march to just over Usd 1788/oz with bullish chart impulses embellished by China reportedly allowing banks to import some 150 tonnes of Gold this month and in May.

In commodities, yet another choppy European morning for WTI and Brent front-month futures and within relatively tight ranges as markets await a concrete fundamental catalyst to latch onto. Participants in the interim will continue to balance the geopolitics with vaccination hurdles and rising COVID cases across some economies - with India and Canada recently telegraphing a worsening situation, with the former cancelling UK PM Johnson's visit whilst its capital New Delhi announce fresh lockdown measures alongside some speculation pointing to India being put on the UK's travel red list. Note that this comes ahead of next week's JMMC/OPEC+ meeting in which eyes will be on any need to alter the output quotas set through July, with production set to steadily increase amid a projected rise in summer demand. The geopolitical landscape meanwhile remains mixed but fluid as ever, with sanguine rhetoric initially emanating from the Iranian JCPOA talks, although Tehran later suggested that negotiations still remain difficult. Elsewhere, developments regarding Russia have been abundant with Kremlin-critic Navalny now seemingly attended to by doctors after US has warned Russia there will be "consequences" if the opposition activist Alexei Navalny dies in jail, whilst EU expressed concern regarding Navalny's health. Further, Russia is reportedly bolstering its warship presence in the Black Sea amid ongoing tensions with Ukraine and Moscow is also poised to announce a US sanctions list. WTI trades on either side of USD 63/bbl (62.67-63.42/bbl range) whilst its Brent counterpart holds its head above USD 66.50/bbl (66.17-95/bbl range). Spot gold and silver meanwhile glean support from the deteriorating Buck with the former now north of USD 1,775/oz (vs low 1,773/oz) whilst spot silver reclaimed USD 26/oz. In terms of base metals, LME copper has been bolstered further above USD 9,000/t amid the softer Buck, reaching a current peak of USD 9,430/t. Overnight, Singapore iron ore futures surged overnight with traders citing demand from the Chinese steel sector.

US Event Calendar

- Nothing major scheduled

DB's Jim Reid concludes the overnight wrap

It’s quite a strange feeling of pride that I feel today given I’m going to get my first Covid jab this afternoon. Maybe its pride at the human achievement, maybe its pride at doing my civic duty. I’m not 100% sure. By tomorrow morning when I’m likely feeling really groggy I’m sure that pride will fade. I nearly became a vaccine refuser as I tried to drive my car yesterday only to find the battery was dead. A call to the breakdown service has fixed this but its a consequence of lockdown as I’ve hardly used my car for 13 months. Thankfully I needed to make rare use of it yesterday or I wouldn’t have discovered the battery problem until just before my 20 mile drive to the vaccination centre. Anyway lets hope I’ll be well enough to be on EMR duties tomorrow.

In terms of markets a more successful vaccination campaign in Europe over the last couple of week has certainty helped the Goldilocks theme for now and the continent looks on surer footing now. In terms of wider markets even risk parity type trades have seemingly made a comeback of late. Indeed Bloomberg data suggests that the S&P 500 and 30yr Treasuries have now both rallied for a fourth week together for the first time since August 2008. So markets are back to being a bit dull for now but pretty buoyant. However positioning is becoming more stretched which should be watched. Our equity strategists reported over the weekend (link here) that their composite measure of US equity positioning is close to record highs (98th percentile). There remains a notable divide between the positioning of discretionary investors, which has moved up to a new peak (100th percentile), while systematic strategies exposure has also risen, but remains near historical median levels (46th percentile). A reminder that they think there is likely to be a 6-10% pull back (link here) when growth peaks which they think will occur over the next 3 months.

While we wait for such excitement we can all live vicariously through the big moves in Bitcoin over the weekend. After being as high as $64,869.78 this past Wednesday it traded as low as $51,707.51 yesterday down around 15% from Friday’s close. As we type its now at $56,987. It’s difficult to work out exactly why the sudden reversal occurred but the online chatter is linking it to speculation that the US Treasury may soon crack down on money laundering that uses digital assets. The market remains in a frenzy though as Dogecoin rose over 110% on Friday. Remember this coin was set up as a joke and was worth more than $50bn at one point over the weekend.

Asian markets have started the week on the front foot with the Nikkei (+0.24%), Hang Seng (+0.80%), Shanghai Comp (+1.30%) and Kospi (+0.26%) all up. Futures on the S&P 500 are down -0.14% while those on the Nasdaq are up +0.11% benefitting form a decline in 10y UST yields (-1.3bps) this morning. In Fx, the Russian rouble (-0.61%) is under fresh pressure this morning after the US warned Russia of “consequences” if jailed opposition leader Alexey Navalny dies. Indeed the geopolitical risks from the Russia story last week did seep into wider markets a little so certainly one to watch

There’s a reasonably eventful calendar for markets this week, with the highlights including Thursday’s ECB meeting and Friday’s release of the April flash PMIs from around the world. Investors will also be paying attention to the latest earnings releases, with a further 80 S&P 500 companies reporting, as well as the continued path of the pandemic as a number of places such as India have faced a big surge in cases. There have been around 5.1mn cases reported across the globe over the past 7 days, the highest weekly increase since the pandemic began. India contributed north of 1.4mn cases to this increase which is also its largest weekly gain and continues to remain the current epicentre of the virus. Elsewhere both Osaka and Tokyo may go into fresh state of emergency conduction as soon as today. On a more positive note, Dr Fauci has said that he expects a decision on how to resume vaccinating Americans with the J&J COVID-19 vaccine will probably come by Friday and added that “I doubt very seriously if they just cancel” the J&J vaccine. We are also expecting that the European Medicines Agency will issue their recommendation on the J&J vaccine over the week ahead.

From central banks, this week’s highlight will be the latest ECB decision on Thursday, along with President Lagarde’s subsequent press conference. In their preview (link here), our European economists write that a change in the policy stance is unlikely, and that a decision on whether or not to maintain the new faster pace of PEPP purchases will be made after a joint assessment of financing conditions and the inflation outlook at the Governing Council’s next monetary policy meeting in June. However, at this point it’s unclear whether they will maintain that higher pace beyond June. Our economists say that although a latent recovery is building and ‘net-net’ issuance (net issuance, net of ECB purchases) ought to turn favourable for rates markets following the Q1 spike, the ECB consensus is cautious and determined to avoid a premature tightening in financing conditions.

Staying on Europe, another important event will take place in Germany today, as the Green party present their first chancellor candidate in the 41-year history of their party. This is an important one to look out for, as the CDU/CSU’s slump in the polls has put them only a few points ahead of the second-place Greens, so it’s no longer implausible that the next German chancellor could come from the Greens following September’s federal election. Our German economists’ full preview can be found here, but their view is that the odds appear slightly tilted towards co-leader Annalena Baerbock being selected. In terms of the election result, our economists still see a CDU-CSU/Green coalition as their baseline scenario, as they expect the Conservatives to regain polling momentum. Talking of which, it’s also possible that the CDU/CSU will agree on who will be their candidate over the next day as Armin Laschet and Markus Soeder have been having behind close door discussions since Friday to hammer out which of them will be on the ticket come September. Overnight, the headlines have leaned more favourably towards Markus Soeder with CDU lawmaker Christian von Stetten suggesting in an interview yesterday that Laschet’s leadership bid would be rejected by the CDU/CSU caucus in a vote on Tuesday if the issue isn’t resolved before then.

On the data front, it’s a lighter week ahead, with the main highlight likely to be at the end of the week with the flash PMIs for April. This will give us an initial indication of how global economic performance has fared at the start of Q2, and there’ll be particular attention on the price gauges as well as investors stay attuned to any signs of growing inflationary pressures. In terms of central banks, there are a few other decisions alongside the ECB, with Canada, Russia and Indonesia all deciding on rates. However, there won’t be any Fed speakers as they’re now in a blackout period ahead of their own meeting the week after.

Earnings season kicks up another gear this week, as 80 companies from the S&P 500 report along with a further 54 from the STOXX 600. Among the highlights include Coca-Cola and IBM today, before tomorrow sees reports from Johnson & Johnson, Procter & Gamble, Netflix, Abbott Laboratories, Philip Morris International and Lockheed Martin. Then on Wednesday we’ll hear from ASML, Verizon, NextEra Energy, and Thursday sees releases from Intel, AT&T, Danaher, Union Pacific and Credit Suisse. Finally on Friday, there’s Honeywell International, American Express and Daimler.

To quickly recap last week, risk markets in Europe and the US continued to set new records as US government yields fell but Europe’s mostly rose possibly due to being past peak European pessimism now vaccine deployment is accelerating. The S&P 500 rose +1.37% on the week (+0.36% Friday), finishing at yet another record high. The index has risen for four straight weeks, the first time that has happened since August. The weekly move was broad based as sectors such as materials, healthcare, and real estate all led gains while technology shares also continued to improve as the NASDAQ rose +1.01% on the week. The tech-concentrated index is within a third of a per cent of its all-time highs. Market volatility has calmed over the last few weeks and this past week the VIX volatility index fell -0.4pts to 16.3 – the lowest levels since the pandemic started. European stocks rose to their own record highs as the STOXX 600 gained +1.20% over the week, with the CAC (+1.91%) and FTSE 100 (+1.50%) outperforming other bourses.

US 10yr yields finished the week -7.9bps lower (+0.4bps Friday) at 1.580% - the third weekly drop in yields over the last four weeks. 30yrs are four in four as discussed at their top. The week’s move was driven by the drop in real yields (-12.4bps) which overcame the increase in inflation expectations (+4.5bps). European rates were more mixed with 10yr bund yields gaining +4.1bps last week and UK gilts falling -1.0bps. There was also a tightening of peripheral spreads in parts of southern Europe as Italian BTPs (-2.1bps) and Spanish bonds (-2.5bps) tightened against 10yr bunds, while Portuguese bonds (+7.9bps) widened.

In terms of economic data from Friday, US housing starts in March was ahead of schedule with 1.739mn (vs 1.613mn expected) new construction after 1.457mn recorded in February. The preliminary University of Michigan consumer sentiment index for April showed a less-than-expected rise to 86.5pts (vs. 89.0pts expected) from 84.9pts. Meanwhile in Europe, new EU car registrations for March was up +87.3% after being down -19.3% in February. The final Euro Area CPI reading for February was +0.9% m/m and +1.3% y/y in-line with earlier estimates.

International

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

The crisis in NHS dentistry is driving increasing numbers abroad for treatment. Here are some of their stories.

Share this:

It’s a hot summer day in the Turkish city of Antalya, a Mediterranean resort with golden beaches, deep blue sea and vibrant nightlife. The pool area of the all-inclusive resort is crammed with British people on sun loungers – but they aren’t here for a holiday. This hotel is linked to a dental clinic that organises treatment packages, and most of these guests are here to see a dentist.

From Norwich, two women talk about gums and injections. A man from Wales holds a tissue close to his mouth and spits blood – he has just had two molars extracted.

The dental clinic organises everything for these dental “tourists” throughout their treatment, which typically lasts from three to 15 days. The stories I hear of what has caused them to travel to Turkey are strikingly similar: all have struggled to secure dental treatment at home on the NHS.

“The hotel is nice and some days I go to the beach,” says Susan*, a hairdresser in her mid-30s from Norwich. “But really, we aren’t tourists like in a proper holiday. We come here because we have no choice. I couldn’t stand the pain.”

This is Susan’s second visit to Antalya. She explains that her ordeal started two years earlier:

I went to an NHS dentist who told me I had gum disease … She did some cleaning to my teeth and gums but it got worse. When I ate, my teeth were moving … the gums were bleeding and it was very painful. I called to say I was in pain but the clinic was not accepting NHS patients any more.

The only option the dentist offered Susan was to register as a private patient:

I asked how much. They said £50 for x-rays and then if the gum disease got worse, £300 or so for extraction. Four of them were moving – imagine: £1,200 for losing your teeth! Without teeth I’d lose my clients, but I didn’t have the money. I’m a single mum. I called my mum and cried.

Susan’s mother told her about a friend of hers who had been to Turkey for treatment, then together they found a suitable clinic:

The prices are so much cheaper! Tooth extraction, x-rays, consultations – it all comes included. The flight and hotel for seven days cost the same as losing four teeth in Norwich … I had my lower teeth removed here six months ago, now I’ve got implants … £2,800 for everything – hotel, transfer, treatments. I only paid the flights separately.

In the UK, roughly half the adult population suffers from periodontitis – inflammation of the gums caused by plaque bacteria that can lead to irreversible loss of gums, teeth, and bone. Regular reviews by a dentist or hygienist are required to manage this condition. But nine out of ten dental practices cannot offer NHS appointments to new adult patients, while eight in ten are not accepting new child patients.

Some UK dentists argue that Britons who travel abroad for treatment do so mainly for cosmetic procedures. They warn that dental tourism is dangerous, and that if their treatment goes wrong, dentists in the UK will be unable to help because they don’t want to be responsible for further damage. Susan shrugs this off:

Dentists in England say: ‘If you go to Turkey, we won’t touch you [afterwards].’ But I don’t worry because there are no appointments at home anyway. They couldn’t help in the first place, and this is why we are in Turkey.

‘How can we pay all this money?’

As a social anthropologist, I travelled to Turkey a number of times in 2023 to investigate the crisis of NHS dentistry, and the journeys abroad that UK patients are increasingly making as a result. I have relatives in Istanbul and have been researching migration and trading patterns in Turkey’s largest city since 2016.

In August 2023, I visited the resort in Antalya, nearly 400 miles south of Istanbul. As well as Susan, I met a group from a village in Wales who said there was no provision of NHS dentistry back home. They had organised a two-week trip to Turkey: the 12-strong group included a middle-aged couple with two sons in their early 20s, and two couples who were pensioners. By going together, Anya tells me, they could support each other through their different treatments:

I’ve had many cavities since I was little … Before, you could see a dentist regularly – you didn’t even think about it. If you had pain or wanted a regular visit, you phoned and you went … That was in the 1990s, when I went to the dentist maybe every year.

Anya says that once she had children, her family and work commitments meant she had no time to go to the dentist. Then, years later, she started having serious toothache:

Every time I chewed something, it hurt. I ate soups and soft food, and I also lost weight … Even drinking was painful – tea: pain, cold water: pain. I was taking paracetamol all the time! I went to the dentist to fix all this, but there were no appointments.

Anya was told she would have to wait months, or find a dentist elsewhere:

A private clinic gave me a list of things I needed done. Oh my God, almost £6,000. My husband went too – same story. How can we pay all this money? So we decided to come to Turkey. Some people we know had been here, and others in the village wanted to come too. We’ve brought our sons too – they also need to be checked and fixed. Our whole family could be fixed for less than £6,000.

By the time they travelled, Anya’s dental problems had turned into a dental emergency. She says she could not live with the pain anymore, and was relying on paracetamol.

In 2023, about 6 million adults in the UK experienced protracted pain (lasting more than two weeks) caused by toothache. Unintentional paracetamol overdose due to dental pain is a significant cause of admissions to acute medical units. If left untreated, tooth infections can spread to other parts of the body and cause life-threatening complications – and on rare occasions, death.

In February 2024, police were called to manage hundreds of people queuing outside a newly opened dental clinic in Bristol, all hoping to be registered or seen by an NHS dentist. One in ten Britons have admitted to performing “DIY dentistry”, of which 20% did so because they could not find a timely appointment. This includes people pulling out their teeth with pliers and using superglue to repair their teeth.

In the 1990s, dentistry was almost entirely provided through NHS services, with only around 500 solely private dentists registered. Today, NHS dentist numbers in England are at their lowest level in a decade, with 23,577 dentists registered to perform NHS work in 2022-23, down 695 on the previous year. Furthermore, the precise division of NHS and private work that each dentist provides is not measured.

The COVID pandemic created longer waiting lists for NHS treatment in an already stretched public service. In Bridlington, Yorkshire, people are now reportedly having to wait eight-to-nine years to get an NHS dental appointment with the only remaining NHS dentist in the town.

In his book Patients of the State (2012), Argentine sociologist Javier Auyero describes the “indignities of waiting”. It is the poor who are mostly forced to wait, he writes. Queues for state benefits and public services constitute a tangible form of power over the marginalised. There is an ethnic dimension to this story, too. Data suggests that in the UK, patients less likely to be effective in booking an NHS dental appointment are non-white ethnic groups and Gypsy or Irish travellers, and that it is particularly challenging for refugees and asylum-seekers to access dental care.

This article is part of Conversation Insights

The Insights team generates long-form journalism derived from interdisciplinary research. The team is working with academics from different backgrounds who have been engaged in projects aimed at tackling societal and scientific challenges.

In 2022, I experienced my own dental emergency. An infected tooth was causing me debilitating pain, and needed root canal treatment. I was advised this would cost £71 on the NHS, plus £307 for a follow-up crown – but that I would have to wait months for an appointment. The pain became excruciating – I could not sleep, let alone wait for months. In the same clinic, privately, I was quoted £1,300 for the treatment (more than half my monthly income at the time), or £295 for a tooth extraction.

I did not want to lose my tooth because of lack of money. So I bought a flight to Istanbul immediately for the price of the extraction in the UK, and my tooth was treated with root canal therapy by a private dentist there for £80. Including the costs of travelling, the total was a third of what I was quoted to be treated privately in the UK. Two years on, my treated tooth hasn’t given me any more problems.

A better quality of life

Not everyone is in Antalya for emergency procedures. The pensioners from Wales had contacted numerous clinics they found on the internet, comparing prices, treatments and hotel packages at least a year in advance, in a carefully planned trip to get dental implants – artificial replacements for tooth roots that help support dentures, crowns and bridges.

In Turkey, all the dentists I speak to (most of whom cater mainly for foreigners, including UK nationals) consider implants not a cosmetic or luxurious treatment, but a development in dentistry that gives patients who are able to have the procedure a much better quality of life. This procedure is not available on the NHS for most of the UK population, and the patients I meet in Turkey could not afford implants in private clinics back home.

Paul is in Antalya to replace his dentures, which have become uncomfortable and irritating to his gums, with implants. He says he couldn’t find an appointment to see an NHS dentist. His wife Sonia went through a similar procedure the year before and is very satisfied with the results, telling me: “Why have dentures that you need to put in a glass overnight, in the old style? If you can have implants, I say, you’re better off having them.”

Most of the dental tourists I meet in Antalya are white British: this city, known as the Turkish Riviera, has developed an entire economy catering to English-speaking tourists. In 2023, more than 1.3 million people visited the city from the UK, up almost 15% on the previous year.

Read more: NHS dentistry is in crisis – are overseas dentists the answer?

In contrast, the Britons I meet in Istanbul are predominantly from a non-white ethnic background. Omar, a pensioner of Pakistani origin in his early 70s, has come here after waiting “half a year” for an NHS appointment to fix the dental bridge that is causing him pain. Omar’s son had been previously for a hair transplant, and was offered a free dental checkup by the same clinic, so he suggested it to his father. Having worked as a driver for a manufacturing company for two decades in Birmingham, Omar says he feels disappointed to have contributed to the British economy for so long, only to be “let down” by the NHS:

At home, I must wait and wait and wait to get a bridge – and then I had many problems with it. I couldn’t eat because the bridge was uncomfortable and I was in pain, but there were no appointments on the NHS. I asked a private dentist and they recommended implants, but they are far too expensive [in the UK]. I started losing weight, which is not a bad thing at the beginning, but then I was worrying because I couldn’t chew and eat well and was losing more weight … Here in Istanbul, I got dental implants – US$500 each, problem solved! In England, each implant is maybe £2,000 or £3,000.

In the waiting area of another clinic in Istanbul, I meet Mariam, a British woman of Iraqi background in her late 40s, who is making her second visit to the dentist here. Initially, she needed root canal therapy after experiencing severe pain for weeks. Having been quoted £1,200 in a private clinic in outer London, Mariam decided to fly to Istanbul instead, where she was quoted £150 by a dentist she knew through her large family. Even considering the cost of the flight, Mariam says the decision was obvious:

Dentists in England are so expensive and NHS appointments so difficult to find. It’s awful there, isn’t it? Dentists there blamed me for my rotten teeth. They say it’s my fault: I don’t clean or I ate sugar, or this or that. I grew up in a village in Iraq and didn’t go to the dentist – we were very poor. Then we left because of war, so we didn’t go to a dentist … When I arrived in London more than 20 years ago, I didn’t speak English, so I still didn’t go to the dentist … I think when you move from one place to another, you don’t go to the dentist unless you are in real, real pain.

In Istanbul, Mariam has opted not only for the urgent root canal treatment but also a longer and more complex treatment suggested by her consultant, who she says is a renowned doctor from Syria. This will include several extractions and implants of back and front teeth, and when I ask what she thinks of achieving a “Hollywood smile”, Mariam says:

Who doesn’t want a nice smile? I didn’t come here to be a model. I came because I was in pain, but I know this doctor is the best for implants, and my front teeth were rotten anyway.

Dentists in the UK warn about the risks of “overtreatment” abroad, but Mariam appears confident that this is her opportunity to solve all her oral health problems. Two of her sisters have already been through a similar treatment, so they all trust this doctor.

The UK’s ‘dental deserts’

To get a fuller understanding of the NHS dental crisis, I’ve also conducted 20 interviews in the UK with people who have travelled or were considering travelling abroad for dental treatment.

Joan, a 50-year-old woman from Exeter, tells me she considered going to Turkey and could have afforded it, but that her back and knee problems meant she could not brave the trip. She has lost all her lower front teeth due to gum disease and, when I meet her, has been waiting 13 months for an NHS dental appointment. Joan tells me she is living in “shame”, unable to smile.

In the UK, areas with extremely limited provision of NHS dental services – known as as “dental deserts” – include densely populated urban areas such as Portsmouth and Greater Manchester, as well as many rural and coastal areas.

In Felixstowe, the last dentist taking NHS patients went private in 2023, despite the efforts of the activist group Toothless in Suffolk to secure better access to NHS dentists in the area. It’s a similar story in Ripon, Yorkshire, and in Dumfries & Galloway, Scotland, where nearly 25,000 patients have been de-registered from NHS dentists since 2021.

Data shows that 2 million adults must travel at least 40 miles within the UK to access dental care. Branding travel for dental care as “tourism” carries the risk of disguising the elements of duress under which patients move to restore their oral health – nationally and internationally. It also hides the immobility of those who cannot undertake such journeys.

The 90-year-old woman in Dumfries & Galloway who now faces travelling for hours by bus to see an NHS dentist can hardly be considered “tourism” – nor the Ukrainian war refugees who travelled back from West Sussex and Norwich to Ukraine, rather than face the long wait to see an NHS dentist.

Many people I have spoken to cannot afford the cost of transport to attend dental appointments two hours away – or they have care responsibilities that make it impossible. Instead, they are forced to wait in pain, in the hope of one day securing an appointment closer to home.

‘Your crisis is our business’

The indignities of waiting in the UK are having a big impact on the lives of some local and foreign dentists in Turkey. Some neighbourhoods are rapidly changing as dental and other health clinics, usually in luxurious multi-storey glass buildings, mushroom. In the office of one large Istanbul medical complex with sections for hair transplants and dentistry (plus one linked to a hospital for more extensive cosmetic surgery), its Turkish owner and main investor tells me:

Your crisis is our business, but this is a bazaar. There are good clinics and bad clinics, and unfortunately sometimes foreign patients do not know which one to choose. But for us, the business is very good.

This clinic only caters to foreign patients. The owner, an architect by profession who also developed medical clinics in Brazil, describes how COVID had a major impact on his business:

When in Europe you had COVID lockdowns, Turkey allowed foreigners to come. Many people came for ‘medical tourism’ – we had many patients for cosmetic surgery and hair transplants. And that was when the dental business started, because our patients couldn’t see a dentist in Germany or England. Then more and more patients started to come for dental treatments, especially from the UK and Ireland. For them, it’s very, very cheap here.

The reasons include the value of the Turkish lira relative to the British pound, the low cost of labour, the increasing competition among Turkish clinics, and the sheer motivation of dentists here. While most dentists catering to foreign patients are from Turkey, others have arrived seeking refuge from war and violence in Syria, Iraq, Afghanistan, Iran and beyond. They work diligently to rebuild their lives, careers and lost wealth.

Regardless of their origin, all dentists in Turkey must be registered and certified. Hamed, a Syrian dentist and co-owner of a new clinic in Istanbul catering to European and North American patients, tells me:

I know that you say ‘Syrian’ and people think ‘migrant’, ‘refugee’, and maybe think ‘how can this dentist be good?’ – but Syria, before the war, had very good doctors and dentists. Many of us came to Turkey and now I have a Turkish passport. I had to pass the exams to practise dentistry here – I study hard. The exams are in Turkish and they are difficult, so you cannot say that Syrian doctors are stupid.

Hamed talks excitedly about the latest technology that is coming to his profession: “There are always new materials and techniques, and we cannot stop learning.” He is about to travel to Paris to an international conference:

I can say my techniques are very advanced … I bet I put more implants and do more bone grafting and surgeries every week than any dentist you know in England. A good dentist is about practice and hand skills and experience. I work hard, very hard, because more and more patients are arriving to my clinic, because in England they don’t find dentists.

While there is no official data about the number of people travelling from the UK to Turkey for dental treatment, investors and dentists I speak to consider that numbers are rocketing. From all over the world, Turkey received 1.2 million visitors for “medical tourism” in 2022, an increase of 308% on the previous year. Of these, about 250,000 patients went for dentistry. One of the most renowned dental clinics in Istanbul had only 15 British patients in 2019, but that number increased to 2,200 in 2023 and is expected to reach 5,500 in 2024.

Like all forms of medical care, dental treatments carry risks. Most clinics in Turkey offer a ten-year guarantee for treatments and a printed clinical history of procedures carried out, so patients can show this to their local dentists and continue their regular annual care in the UK. Dental treatments, checkups and maintaining a good oral health is a life-time process, not a one-off event.

Many UK patients, however, are caught between a rock and a hard place – criticised for going abroad, yet unable to get affordable dental care in the UK before and after their return. The British Dental Association has called for more action to inform these patients about the risks of getting treated overseas – and has warned UK dentists about the legal implications of treating these patients on their return. But this does not address the difficulties faced by British patients who are being forced to go abroad in search of affordable, often urgent dental care.

A global emergency

The World Health Organization states that the explosion of oral disease around the world is a result of the “negligent attitude” that governments, policymakers and insurance companies have towards including oral healthcare under the umbrella of universal healthcare. It as if the health of our teeth and mouth is optional; somehow less important than treatment to the rest of our body. Yet complications from untreated tooth decay can lead to hospitalisation.

The main causes of oral health diseases are untreated tooth decay, severe gum disease, toothlessness, and cancers of the lip and oral cavity. Cases grew during the pandemic, when little or no attention was paid to oral health. Meanwhile, the global cosmetic dentistry market is predicted to continue growing at an annual rate of 13% for the rest of this decade, confirming the strong relationship between socioeconomic status and access to oral healthcare.

In the UK since 2018, there have been more than 218,000 admissions to hospital for rotting teeth, of which more than 100,000 were children. Some 40% of children in the UK have not seen a dentist in the past 12 months. The role of dentists in prevention of tooth decay and its complications, and in the early detection of mouth cancer, is vital. While there is a 90% survival rate for mouth cancer if spotted early, the lack of access to dental appointments is causing cases to go undetected.

The reasons for the crisis in NHS dentistry are complex, but include: the real-term cuts in funding to NHS dentistry; the challenges of recruitment and retention of dentists in rural and coastal areas; pay inequalities facing dental nurses, most of them women, who are being badly hit by the cost of living crisis; and, in England, the 2006 Dental Contract that does not remunerate dentists in a way that encourages them to continue seeing NHS patients.

The UK is suffering a mass exodus of the public dentistry workforce, with workers leaving the profession entirely or shifting to the private sector, where payments and life-work balance are better, bureaucracy is reduced, and prospects for career development look much better. A survey of general dental practitioners found that around half have reduced their NHS work since the pandemic – with 43% saying they were likely to go fully private, and 42% considering a career change or taking early retirement.

Reversing the UK’s dental crisis requires more commitment to substantial reform and funding than the “recovery plan” announced by Victoria Atkins, the secretary of state for health and social care, on February 7.

The stories I have gathered show that people travelling abroad for dental treatment don’t see themselves as “tourists” or vanity-driven consumers of the “Hollywood smile”. Rather, they have been forced by the crisis in NHS dentistry to seek out a service 1,500 miles away in Turkey that should be a basic, affordable right for all, on their own doorstep.

*Names in this article have been changed to protect the anonymity of the interviewees.

For you: more from our Insights series:

GP crisis: how did things go so wrong, and what needs to change?

Insomnia: how chronic sleep problems can lead to a spiralling decline in mental health

To hear about new Insights articles, join the hundreds of thousands of people who value The Conversation’s evidence-based news. Subscribe to our newsletter.

Diana Ibanez Tirado receives funding from the School of Global Studies, University of Sussex.

pound pandemic treatment therapy spread recovery iran brazil european europe uk germany ukraine world health organizationInternational

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

The struggling chain has given up the fight and will close hundreds of stores around the world.

Share this:

It has been a brutal period for several popular retailers. The fallout from the covid pandemic and a challenging economic environment have pushed numerous chains into bankruptcy with Tuesday Morning, Christmas Tree Shops, and Bed Bath & Beyond all moving from Chapter 11 to Chapter 7 bankruptcy liquidation.

In all three of those cases, the companies faced clear financial pressures that led to inventory problems and vendors demanding faster, or even upfront payment. That creates a sort of inevitability.

Related: Beloved retailer finds life after bankruptcy, new famous owner

When a retailer faces financial pressure it sets off a cycle where vendors become wary of selling them items. That leads to barren shelves and no ability for the chain to sell its way out of its financial problems.

Once that happens bankruptcy generally becomes the only option. Sometimes that means a Chapter 11 filing which gives the company a chance to negotiate with its creditors. In some cases, deals can be worked out where vendors extend longer terms or even forgive some debts, and banks offer an extension of loan terms.

In other cases, new funding can be secured which assuages vendor concerns or the company might be taken over by its vendors. Sometimes, as was the case with David's Bridal, a new owner steps in, adds new money, and makes deals with creditors in order to give the company a new lease on life.

It's rare that a retailer moves directly into Chapter 7 bankruptcy and decides to liquidate without trying to find a new source of funding.

Image source: Getty Images

The Body Shop has bad news for customers

The Body Shop has been in a very public fight for survival. Fears began when the company closed half of its locations in the United Kingdom. That was followed by a bankruptcy-style filing in Canada and an abrupt closure of its U.S. stores on March 4.

"The Canadian subsidiary of the global beauty and cosmetics brand announced it has started restructuring proceedings by filing a Notice of Intention (NOI) to Make a Proposal pursuant to the Bankruptcy and Insolvency Act (Canada). In the same release, the company said that, as of March 1, 2024, The Body Shop US Limited has ceased operations," Chain Store Age reported.

A message on the company's U.S. website shared a simple message that does not appear to be the entire story.

"We're currently undergoing planned maintenance, but don't worry we're due to be back online soon."

That same message is still on the company's website, but a new filing makes it clear that the site is not down for maintenance, it's down for good.

The Body Shop files for Chapter 7 bankruptcy

While the future appeared bleak for The Body Shop, fans of the brand held out hope that a savior would step in. That's not going to be the case.

The Body Shop filed for Chapter 7 bankruptcy in the United States.

"The US arm of the ethical cosmetics group has ceased trading at its 50 outlets. On Saturday (March 9), it filed for Chapter 7 insolvency, under which assets are sold off to clear debts, putting about 400 jobs at risk including those in a distribution center that still holds millions of dollars worth of stock," The Guardian reported.

After its closure in the United States, the survival of the brand remains very much in doubt. About half of the chain's stores in the United Kingdom remain open along with its Australian stores.

The future of those stores remains very much in doubt and the chain has shared that it needs new funding in order for them to continue operating.

The Body Shop did not respond to a request for comment from TheStreet.

bankruptcy pandemic canadaGovernment

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

{kind=link}

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

Mortgage rates fall as labor market normalizes

February Employment Situation

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Low Iron Levels In Blood Could Trigger Long COVID: Study

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

Walmart joins Costco in sharing key pricing news

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex