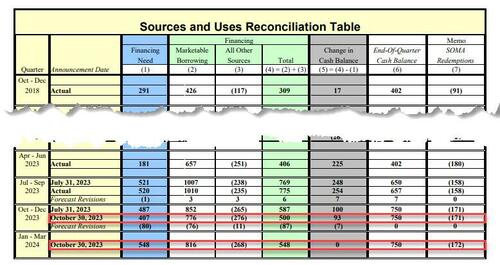

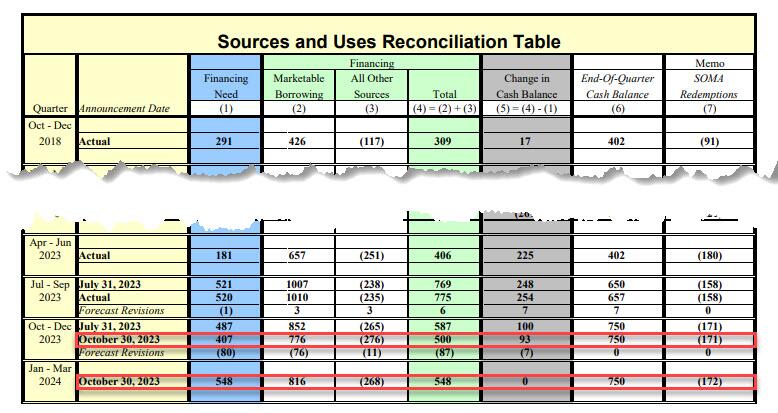

In the US, the Treasury borrowing target for Q4 set at $776bn, slightly lower than expected due to higher than anticipated revenues.

Even so, huge fiscal deficits are here to stay.

Tomorrow we find out how this will be financed, with Treasury Secretary Yellen likely to opt for short-term bill issuance. Druckenmiller just lambasted her for not locking in cheap long-term debt like “Every Tom, Dick, Harry, and Mary” in the US; and, elsewhere X quips, “Yellen's husband explaining why economists like his wife are imbeciles w/o using her name”, quoting Akerlof’s 2020 article arguing “observations that contradict the existing paradigm will be dismissed if they violate the prescribed methodology,” are why economists didn’t see the GFC, or the rise in inflation and rates, coming. Yes, more bill issuance might take upwards pressure off longer-dated bond yields. However, Yellen would be doing it to splurge on spending over the next 12 months to try to ensure she stays in the job for another 62. In which case, US GDP growth will keep looking like it did in Q3, as will inflation, and the Fed may have to act again, raising both T-bill rates and Treasury bond yields.

On a related front, the details of the UAW pay deal with major US automakers are, if you will excuse the pun, striking: a 25% pay rise over the next 4 years, 8 months; Restored cost-of-living allowance of $8,800 over the contract that lifts this to 30%; Immediate 11% pay-rise for top earners, while the lowest paid get an effective 88% hike; A $5,000 ratification bonus and a $1,500 voucher towards a new car; Profit sharing, which would have been equal to $1,200 in 2022; Current temporary workers become full-time, new temps after nine months; Ford to raise 401K contributions to 10% from 6.4%; Right to strike over plant closures; An extra day off and two weeks paid parental leave; and $8.1bn new CAPEX by the firms. I recall recent conversations where I was told *the* litmus tests of whether we would see higher yields for longer was if we saw real-terms pay rises in the West. It’s certainly now a happy Halloween for the UAW, and others will surely be looking to follow that lead. Moreover, if we keep seeing income gains like that, and a more ‘income rich, asset poor’ world, maybe the declines we are seeing in consumer borrowing aren’t the same signals they used to be(?)

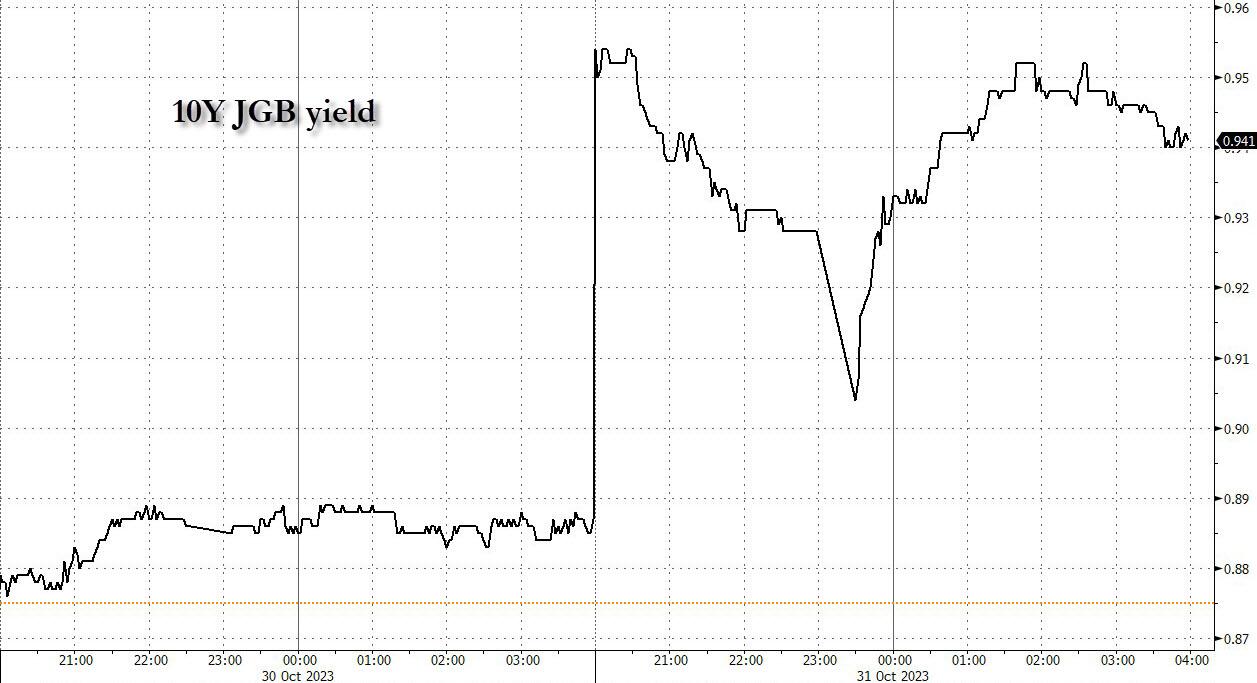

In Japan, today sees the BOJ meeting, with risks we could see an end to yield curve control. JPY already jumped on a report 10-year yields may be allowed to trade higher than their 1% ceiling – they were at 0.93% at time of writing. Yes, this is vastly lower than US yields at close to 5%, but not when FX hedged. In short, more bad news for bonds ahead, perhaps. Yet worse, if US yields rise further, the Dollar may benefit, leaving Japan with lower FX, higher imported inflation, higher bond yields, and higher debt servicing costs. And no way out.

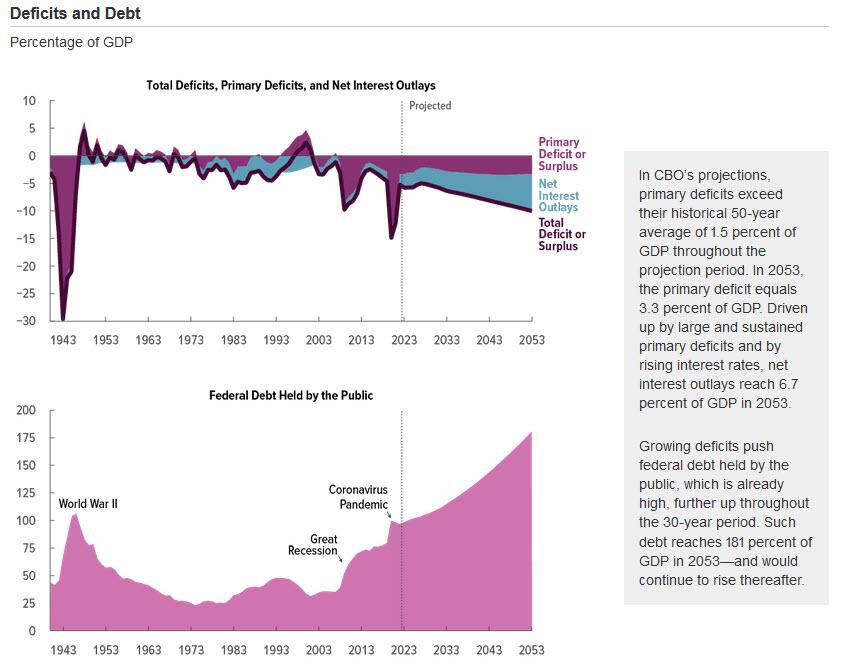

The IMF argues ‘The temptation to finance all spending through debt must be resisted’, as Director Gopinath claims state spending above current levels could hit $6trn (7% of GDP) in DM and $5.3trn (8% of GDP) in EM by 2030 as sustainability, defence, and industrial policies require vast budgets. In other words, a global fiscal crisis may loom, albeit with the US better placed than most. She argues for global cooperation on a minimum corporate tax rate (going nowhere), a carbon tax (rejected at the ballot box in some places, as carbon tariffs are rolled out in others), and strengthened fiscal frameworks (i.e., austerity). In short, a world arming itself to the teeth and trying to seize control of supply chains is supposed to cut spending and cooperate on taxes.

We have a horror-story geopolitical backdrop. So much so that, “We must get used to the idea that there may be a threat of war in Europe – the German Minister of Defence”, a headline no Western newspaper is prepared to run, it seems. (What did Akerlof say? “Observations that contradict the existing paradigm will be dismissed if they violate the prescribed methodology.”) None of the EUR100bn Germany promised on defense has been usefully spent 18 months later.

The first of three Middle-East dominoes we’ve flagged as triggers for a regional escalation already toppled: an Israeli ground war in Gaza. However, this is so far still small scale. The second domino is the entry of Hezbollah once Israel commits its forces in full – on which front, social media clips of their hide-away leader Nasrallah making an appearance like a new end-credit scene Marvel villain may be worth noting. The third domino is Iran which, as the World Bank concludes three weeks after us, risks oil back at $150 a barrel and European gas at 2022 levels. While oil will remain on the back foot unless we see the next phase of escalation, there has already been an impact on European gas, with December TTF futures up 7.1% as LNG flows to Egypt from Israel dry up, meaning they cannot flow on to Europe.

Oil itself may also react to news from Iran- and Russia-ally Venezuela, where promises to allow free(er) elections in exchange for a sanctions roll-back have immediately been broken: President Maduro called opposition primary votes a “fraud”, and the electoral court suspends “all effects” of them. The issue is now whether the US will snap sanctions back, so oil prices rise, or blink to show geopolitical weakness, in which case risks are oil prices rise for other, worse reasons.

Relatedly, China has stated it will deepen military cooperation with Russia, and is sending larger naval forces to the waters around Taiwan, after reiterating: “Once the Chinese government is forced to use force to resolve the Taiwan question, it will be a war for reunification, a just and legitimate war supported, and participated in by the Chinese people… A war to crush foreign interference.” China is also again confronting Filipino ships in their own territorial waters (which it claims) despite US warnings it will defend the Philippines. Not too far away, South Korea is preparing for a possible Hamas-style provocation from North Korea. And Russia is escalating a push to take territory around Avdiivka, while Ukraine claims it hit Crimea again.

It should be clear to all except those who Akerlof critiques that the West is facing coordinated pushbacks against their hegemony: even in their own streets and from their fat, plush universities. As Hal Brands notes, ‘Biden’s Foreign Policy Vision Is Officially Dead’. He calls for the US (and, by extension, Europe!) to accept geopolitical reality and shift to a pre-war footing – which will be incredibly expensive, require guns vs. butter choices, and/or be very inflationary, as well as disruptive to the global trading architecture.

This Daily has long argued that in the face of these threats, and the inflation threat, we would see a fiscal and monetary policy, and trade and industrial policy, fusion: we have simplified this to “rate hikes and acronyms”, i.e., QE or MMT. However, it is crucial to understand that is not a true solution if you are thinking about asset prices going up or down.

“Hamas has set a trap for us, and this trap is one of maximum horror, of maximum cruelty. And so there's a risk of an escalation in militarism… There's also a second major trap, which is that of Occidentalism… which today is being challenged by most of the international community… the idea that the West, which for five centuries managed the world's affairs, will be able to quietly continue to do so. And we can clearly see,… there is the idea that, faced with what is currently happening in the Middle East, we must continue the fight even more, towards what might resemble a religious or a civilizational war. That is to say, to isolate ourselves even more on the international stage.”

To follow, here are excerpts from a translated tweet from the President of Colombia, which until recently was a key LatAm US ally:

“The barbarity of consumption based on the death of others leads to an unprecedented rise of fascism, and thus to the death of democracy and freedom. It's barbarism, or the global 1933, as I call it. 1933 was the year Hitler came to power. What we see in Palestine will also be the sufferings in the world of all the peoples of the South.

The West defends its overconsumption and its standard of living based on destroying the atmosphere and the climate, and to defend it, knowing that it will cause the exodus from the south to the north, and not only of the Palestinian people; He prepares to respond with death. It does not want to reform its economic system until the market goes to decarbonize it. And he knows that the effort will be minuscule to save life on the planet...

The right wing of the West sees the solution to the climate crisis as a "final solution", the right wing dreams of Hitler again and conquers most of the rich and Aryan peoples of the West and our Latin American oligarchies, who see no other world in which to live than that of the "malls" of Florida or Madrid… We are going to barbarism if we don't change power. The life of humanity, and especially of the peoples of the South, depends on the way in which humanity chooses the path to overcome the climate crisis produced by the wealth of the North. Gaza is just the first experiment in considering us all disposable.”

In short, the ‘Global South’, with a few key exceptions, is seething with anger at what it sees as Western attempts to retain economic hegemony and living standards through a ‘painless’ climate transition that they cannot afford. From the Southern side, this is a zero-sum game. Indeed, in a world where we admit there are finite resources, it literally *is* zero-sum – with all the negative impacts that has on a diverse society and its social psychology.

As I have argued before, this doesn’t mean the South can create a new economic and financial system; they can’t. But they can destabilise the current one. Yes, de-dollarisation is not viable in terms of any replacement, some EM are now happy not to recycle their dollars back to the US, and to barter and clear bilaterally while pricing in dollars (for now). The more heated geopolitics gets, the more these choices will be made.

Against that backdrop, if the West cut rates and/or does MMT dressed up as QE, do you think EM will accept that fiat currency for their commodities and products at an exchange rate that will maintain Western standards of living? Only if forced to. And force is very much where we are at right now. And it is where the MMT will have to be channelled.

This Middle East war, on top of the Ukraine War, will partly determine which financial system holds ahead, and where: US dollars, or EM commodities, as the base of the Eurodollar-accounting collateral pyramid.

For now, the US dollar is winning thanks to higher rates. But realpolitik logic says the West needs to win in the field of arms too, tragic as that is for so many individuals. Economic and financial power flow from military power, and vice versa, even if most don’t choose to see it until the barrel of a gun is pointed at them.

Indeed, the outcome of this cluster of wars will arguably speak to the long-run status of liberal democracy, or what’s left of it, and Occidentalism. See this cluster of interviews for some extra public intellectual firepower behind that view, and the belief that the West will have to do much, much more as a result – even if markets don’t like it.

In short, those enjoying a comfortable, middle-class Western lifestyle and hoping for a quick end to this new war, and an easy energy transition at low cost, and a Happy Halloween, are likely to be disappointed on all fronts.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}