Government

The Market Bubble is More Likely To Burst As The Coronavirus Crisis Deepens

Stocks Struggle As The Bull Market In Virus Cases Rises

Share this:

This article was originally published by ZeroHedge.

Stocks Struggle As The Bull Market In Virus Cases Rises Tyler Durden Sun, 07/19/2020 - 11:30Technically Trapped

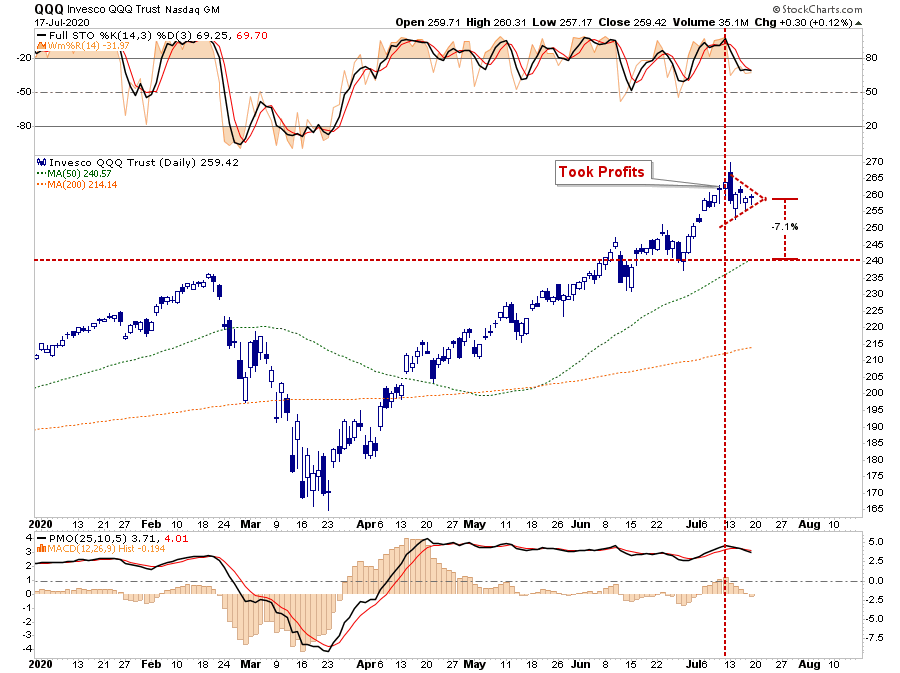

Last week, we discussed why we were taking profits in positions that had gotten egregiously overbought for the second time this year. To wit:“For the second time in a single year, we have begun the profit-taking process within our most profitable names. Apple, Microsoft, Netflix, Amazon, Costco, PG, and in Communications and Technology ETFs.”That turned out to be timely as technology shares struggled to maintain their altitude. The tight “wedge” pattern that has developed suggests a downside break could quickly lead to a test of the 50-dma. Such would equate to about a 7% decline.

“In the short-term, the bulls remain in charge currently, and as such, we must be mindful of those trends. Also, the month of July tends to be one of the better performing months of the year.”

The Bull Market In Virus Cases

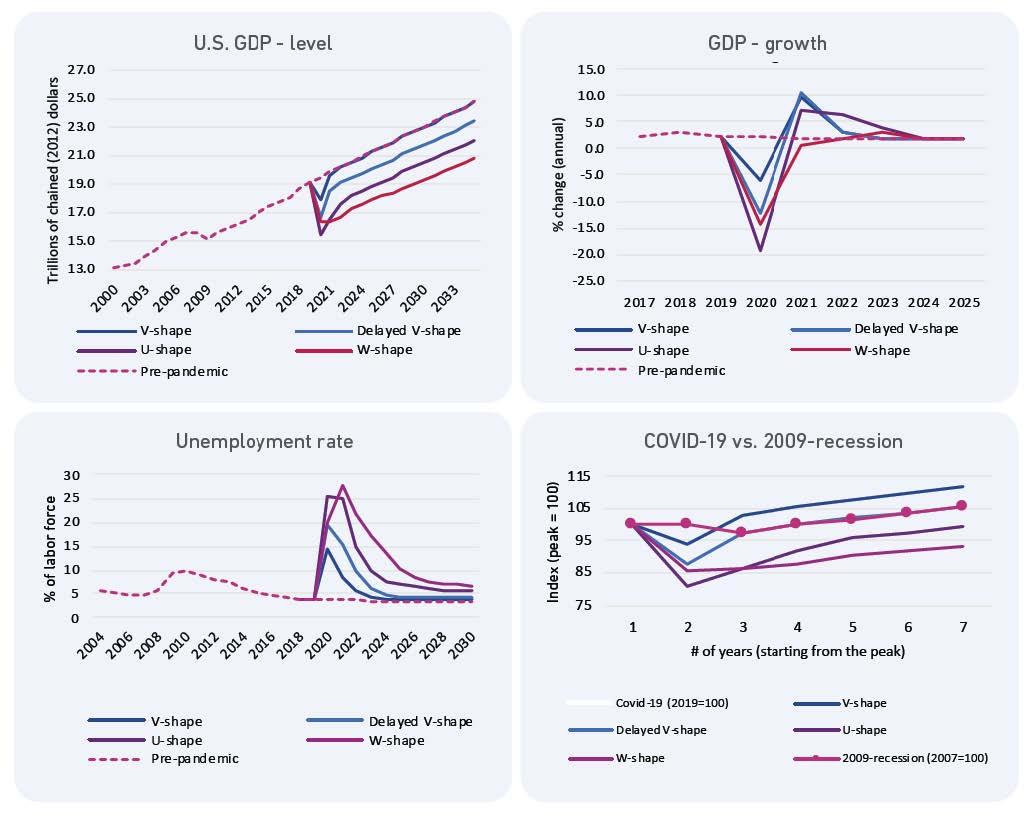

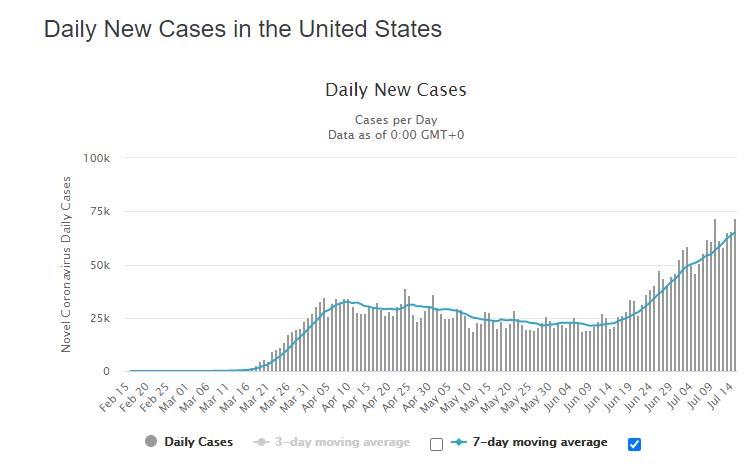

August and September’s seasonal tendencies will also be impacted by the ongoing “bull market” in “virus” cases. Our colleague Jeffrey Marcus noted a critical point for our RIAPro subscribers (30-day Risk-Free Trial)“The question for clients is this: ‘Is the pattern of the past 5-days a broadening of the rally since March 23rd lows, or are investors moving too far out on the risk curve?’ Experian’s 4 possible Covid-19 economic scenarios may provide an answer. The worst scenario was a W-shaped.”

“There were 72,045 new cases of Covid-19 in the U.S. The second worst daily number to date (chart below). Although the market seems to have ignored the worsening numbers so far, the V-shaped scenario seems a long-shot at this juncture. Can the U.S economy somehow rebound with ever-increasing cases of Covid-19? The market action over the past 5-days seems to depend on the belief of recovery, and the hope cheap valuations will buffer against tough financial conditions. Clients should own stocks of companies that can prosper during a pandemic ridden economy. Such is as opposed to just ‘hoping’ stocks with rocky roads ahead will continue to rally.”

Economic Expectations Slow

The most significant risk to the current bull market in stocks comes in two specific headwinds – Congress and the Fed. At the end of the month, the additional $600/week in jobless benefits will expire. Such is no small matter, as noted by CNBC:- 25.6 million individuals will lose the additional benefit on July 25th.

- $15.4 billion in additional weekly economic benefit nationwide up from states spending less than $1 billion pre-pandemic.

- Political football (R) – Republicans intend to end the enhancement to jobless benefits as they view it as a disincentive for people to return to work.

- Political football (D) – Democrats realize an election is soon. If the economy is doing well due to the benefits, the odds increase for a re-election of the incumbent.

- Debt Ceiling Debate – With the debt-ceiling, the debate on the next “continuing resolution” will become problematic. For conservative Republicans up for re-election, unbridled spending is going to become problematic.

Federal Contraction

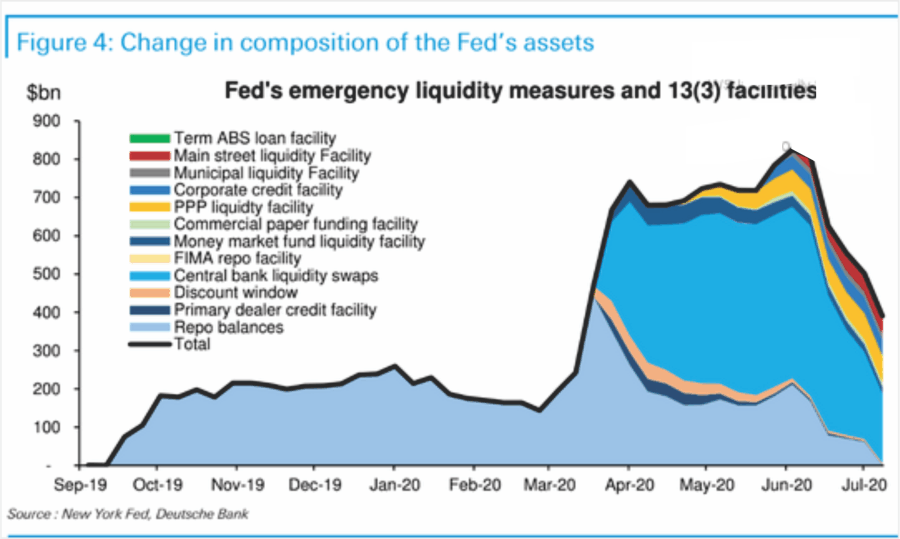

The other headwind for the market comes from the very thing that boosted asset prices to start with – the Fed’s balance sheet expansion. Over the last couple of months, the slowing rate of advance for the market has coincided with a reduction in the Fed’s “emergency measures.”

“Instead, as each year passed, more monetary policy was required just to sustain economic growth. Whenever the Fed tightened policy, economic growth weakened, and financial markets declined. The table shows it takes increasingly larger amounts of QE to create an equivalent increase in asset prices.”

“As with everything, there is a “diminishing rate of return” on QE over time. Since QE requires more debt to be issued, the consequence is slower economic growth over time.“

Who Ya Gonna Believe

My friend Doug Kass also made a salient comment regarding the economic risk in front of us.“Some fundamental investors (like myself) are looking closely at the flattening high-frequency economic data, and the rising chorus of company executives flagging economic and market uncertainties over the last few days. Specifically, the management of Citigroup, Wells Fargo, JPMorgan, and Goldman Sachs all echoed the same mantra. They are surprised by how optimistic the economic and business forecasts have grown, and the enthusiastic embrace of the capital markets. These wise managers of businesses have their feet on the ground and virtually dismiss a “V” type recovery that many have endorsed. To paraphrase, they all see many possible outcomes (many of which are adverse and not market-friendly). Look to the ground, not to the sky – believe them (bank CEOs) and not the markets’ seductive lying eyes.”As noted above, the data does confirm those views. More importantly, there is another issue that derives from a weaker economic outlook.

Stocks Are About To Get A Lot More Expensive

As Eric Parnell recently wrote:“The current forward price-to-earnings ratio on the S&P 500 based on 2020 earnings is 35.6 times earnings. The historical average forward price-to-earnings ratio on the S&P 500 dating back a century and a half is 15.6 times. Thus, today’s valuation is more than +125% greater than the historical average. The forward P/E ratio on the S&P 500 has been higher than 35.6 only two other times in history. Both are recent episodes. The first was from 2001-Q1 to 2002-Q2 during the bursting of the technology bubble. The second was from 2008-Q2 to 2009-Q1 during the Great Financial Crisis. During both of these past episodes, the P/E ratio moved in excess of 35 times forward earnings, because while the S&P 500 price was falling (the “P” in the P/E ratio), the earnings were falling much faster (the “E” in the P/E ratio). In contrast, the P/E ratio has moved in excess of 35 times forward earnings today because the S&P 500 price is rising even though earnings are falling considerably.”

More To Go

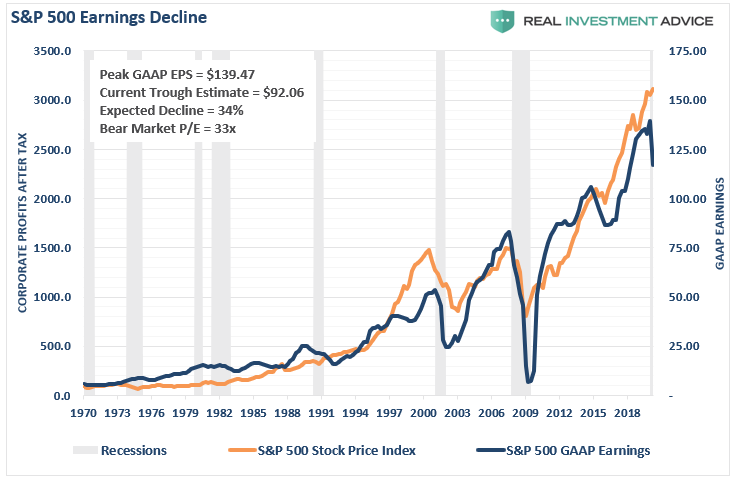

That is correct, and the issue currently is that expectations for earnings are still far too high through the end of 2020, and into 2021. As I discussed previously:“Currently, estimates have only been reduced by 34% of their previous peak. Such comes at a time where economic growth is weaker, job loss is higher, and consumption will drop lower than any previous point except during the ‘Great Depression.'”

“We are watching the chart closely as we expect that earnings will eventually drop closer to $60/share to align with historical norms. As such, stock prices will have to correct to align with those earnings.”(Note: Since that writing, trough estimates have declined to $91.79. The current bear market P/E is currently 35.13x.) However, even those estimates are likely optimistic, given the data that is coming in. We would not be surprised to see a negative sign in front Q2-GAAP earnings before it is over. At the moment, such “fundamental relics” like earnings may not seem to matter. Such has always seemed to be the case, just before they begin to matter, and matter a lot.

Updating Risk/Reward Ranges

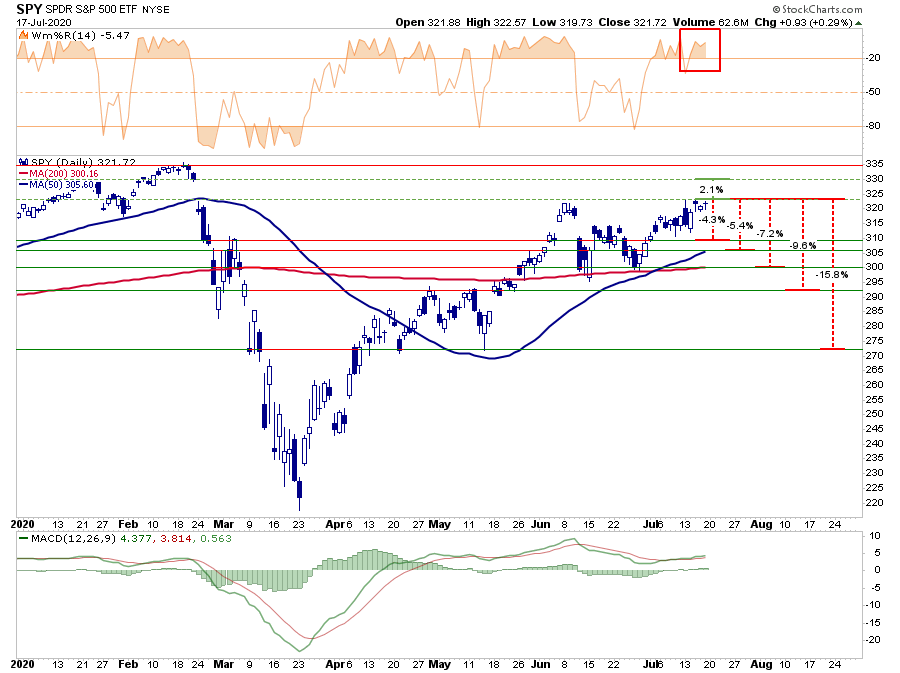

As noted last week:“The [advice to reduce risk] played out well this past week, given daily swings in the market. While the market was up for the week, it has not reclaimed the June highs. As such, the consolidation continues with risk/reward remaining primarily ‘neutral’ with a ‘negative’ bias.”That advice remains this week. After several failed tests of the June highs this week, we derisked our portfolios and added to our hedges. Even with those adjustments, our portfolios continued to perform as the rotation to “risk-off” sectors kept markets stable. The reason for the derisking is the negative tilt to the risk/reward ranges currently.

- -4.3% to initial March reflex rally top vs. +2.1% all-time highs.* (Negative)

- -5.4% to 50-dma support vs. +2.1% to all-time highs.* (Negative)

- -7.2% to 200-dma support vs. +2.1% to all-time highs.* (Negative)

- -9.6% to -15.8% to previous consolidation vs. +2.1% to all-time highs.* (Negative)

(* If the market breaks out to all-time this analysis is no longer valid and risk/reward ranges will recalibrate for the breakout.)

The Risk Of Confirmation Bias

I have written many times previously about the dangers of getting trapped into a “bullish” or “bearish” mindset. As an investor or portfolio manager, your job is to view the markets for opportunities to increase capital and protect it from loss. As Doug noted this week:“There are many who see the markets as “Them versus Us.” The bulls vs. the bears, the fundamentalists vs. the technicians, and so on. I view the investment marketplace as me vs. the markets, and not me vs. opposing views.“The most significant risk to any investor long-term is getting trapped in “confirmation bias.” Such is the psychological impediment of seeking out information that confirms your existing predisposition. However, such inherently leads to adverse outcomes as investors become blind to the risk that inherently upends their future outcome. In the end, it does not matter IF you are “bullish” or “bearish.” The reality is that the “broken clock” syndrome owns both “bulls” and “bears” during the full-market cycle. However, grossly important in achieving long-term investment success is not necessarily being “right” during the first half of the cycle, but by not being “wrong” during the second half.

Government

Looking Back At COVID’s Authoritarian Regimes

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked,…

Share this:

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked, in March 2020, when President Trump and most US governors imposed heavy restrictions on people’s freedom. The purpose, said Trump and his COVID-19 advisers, was to “flatten the curve”: shut down people’s mobility for two weeks so that hospitals could catch up with the expected demand from COVID patients. In her book Silent Invasion, Dr. Deborah Birx, the coordinator of the White House Coronavirus Task Force, admitted that she was scrambling during those two weeks to come up with a reason to extend the lockdowns for much longer. As she put it, “I didn’t have the numbers in front of me yet to make the case for extending it longer, but I had two weeks to get them.” In short, she chose the goal and then tried to find the data to justify the goal. This, by the way, was from someone who, along with her task force colleague Dr. Anthony Fauci, kept talking about the importance of the scientific method. By the end of April 2020, the term “flatten the curve” had all but disappeared from public discussion.

Now that we are four years past that awful time, it makes sense to look back and see whether those heavy restrictions on the lives of people of all ages made sense. I’ll save you the suspense. They didn’t. The damage to the economy was huge. Remember that “the economy” is not a term used to describe a big machine; it’s a shorthand for the trillions of interactions among hundreds of millions of people. The lockdowns and the subsequent federal spending ballooned the budget deficit and consequent federal debt. The effect on children’s learning, not just in school but outside of school, was huge. These effects will be with us for a long time. It’s not as if there wasn’t another way to go. The people who came up with the idea of lockdowns did so on the basis of abstract models that had not been tested. They ignored a model of human behavior, which I’ll call Hayekian, that is tested every day.

These are the opening two paragraphs of my latest Defining Ideas article, “Looking Back at COVID’s Authoritarian Regimes,” Defining Ideas, March 14, 2024.

Another excerpt:

That wasn’t the only uncertainty. My daughter Karen lived in San Francisco and made her living teaching Pilates. San Francisco mayor London Breed shut down all the gyms, and so there went my daughter’s business. (The good news was that she quickly got online and shifted many of her clients to virtual Pilates. But that’s another story.) We tried to see her every six weeks or so, whether that meant our driving up to San Fran or her driving down to Monterey. But were we allowed to drive to see her? In that first month and a half, we simply didn’t know.

Read the whole thing, which is longer than usual.

(0 COMMENTS) budget deficit coronavirus covid-19 white house fauci trump canadaInternational

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Authored by Zachary Stieber via The Epoch Times (emphasis…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

People who recovered from COVID-19 and received a COVID-19 shot were more likely to suffer adverse reactions, researchers in Europe are reporting.

Participants in the study were more likely to experience an adverse reaction after vaccination regardless of the type of shot, with one exception, the researchers found.

Across all vaccine brands, people with prior COVID-19 were 2.6 times as likely after dose one to suffer an adverse reaction, according to the new study. Such people are commonly known as having a type of protection known as natural immunity after recovery.

People with previous COVID-19 were also 1.25 times as likely after dose 2 to experience an adverse reaction.

The findings held true across all vaccine types following dose one.

Of the female participants who received the Pfizer-BioNTech vaccine, for instance, 82 percent who had COVID-19 previously experienced an adverse reaction after their first dose, compared to 59 percent of females who did not have prior COVID-19.

The only exception to the trend was among males who received a second AstraZeneca dose. The percentage of males who suffered an adverse reaction was higher, 33 percent to 24 percent, among those without a COVID-19 history.

“Participants who had a prior SARS-CoV-2 infection (confirmed with a positive test) experienced at least one adverse reaction more often after the 1st dose compared to participants who did not have prior COVID-19. This pattern was observed in both men and women and across vaccine brands,” Florence van Hunsel, an epidemiologist with the Netherlands Pharmacovigilance Centre Lareb, and her co-authors wrote.

There were only slightly higher odds of the naturally immune suffering an adverse reaction following receipt of a Pfizer or Moderna booster, the researchers also found.

The researchers performed what’s known as a cohort event monitoring study, following 29,387 participants as they received at least one dose of a COVID-19 vaccine. The participants live in a European country such as Belgium, France, or Slovakia.

Overall, three-quarters of the participants reported at least one adverse reaction, although some were minor such as injection site pain.

Adverse reactions described as serious were reported by 0.24 percent of people who received a first or second dose and 0.26 percent for people who received a booster. Different examples of serious reactions were not listed in the study.

Participants were only specifically asked to record a range of minor adverse reactions (ADRs). They could provide details of other reactions in free text form.

“The unsolicited events were manually assessed and coded, and the seriousness was classified based on international criteria,” researchers said.

The free text answers were not provided by researchers in the paper.

“The authors note, ‘In this manuscript, the focus was not on serious ADRs and adverse events of special interest.’” Yet, in their highlights section they state, “The percentage of serious ADRs in the study is low for 1st and 2nd vaccination and booster.”

Dr. Joel Wallskog, co-chair of the group React19, which advocates for people who were injured by vaccines, told The Epoch Times: “It is intellectually dishonest to set out to study minor adverse events after COVID-19 vaccination then make conclusions about the frequency of serious adverse events. They also fail to provide the free text data.” He added that the paper showed “yet another study that is in my opinion, deficient by design.”

Ms. Hunsel did not respond to a request for comment.

She and other researchers listed limitations in the paper, including how they did not provide data broken down by country.

The paper was published by the journal Vaccine on March 6.

The study was funded by the European Medicines Agency and the Dutch government.

No authors declared conflicts of interest.

Some previous papers have also found that people with prior COVID-19 infection had more adverse events following COVID-19 vaccination, including a 2021 paper from French researchers. A U.S. study identified prior COVID-19 as a predictor of the severity of side effects.

Some other studies have determined COVID-19 vaccines confer little or no benefit to people with a history of infection, including those who had received a primary series.

The U.S. Centers for Disease Control and Prevention still recommends people who recovered from COVID-19 receive a COVID-19 vaccine, although a number of other health authorities have stopped recommending the shot for people who have prior COVID-19.

Another New Study

In another new paper, South Korean researchers outlined how they found people were more likely to report certain adverse reactions after COVID-19 vaccination than after receipt of another vaccine.

The reporting of myocarditis, a form of heart inflammation, or pericarditis, a related condition, was nearly 20 times as high among children as the reporting odds following receipt of all other vaccines, the researchers found.

The reporting odds were also much higher for multisystem inflammatory syndrome or Kawasaki disease among adolescent COVID-19 recipients.

Researchers analyzed reports made to VigiBase, which is run by the World Health Organization.

“Based on our results, close monitoring for these rare but serious inflammatory reactions after COVID-19 vaccination among adolescents until definitive causal relationship can be established,” the researchers wrote.

The study was published by the Journal of Korean Medical Science in its March edition.

Limitations include VigiBase receiving reports of problems, with some reports going unconfirmed.

Funding came from the South Korean government. One author reported receiving grants from pharmaceutical companies, including Pfizer.

International

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

As the global pandemic unfolded, government-funded…

Share this:

{kind=link}

As the global pandemic unfolded, government-funded experimental vaccines were hastily developed for a virus which primarily killed the old and fat (and those with other obvious comorbidities), and an aggressive, global campaign to coerce billions into injecting them ensued.

{kind=link}

Then there were the lockdowns - with some countries (New Zealand, for example) building internment camps for those who tested positive for Covid-19, and others such as China welding entire apartment buildings shut to trap people inside.

It was an egregious and unnecessary response to a virus that, while highly virulent, was survivable by the vast majority of the general population.

Oh, and the vaccines, which governments are still pushing, didn't work as advertised to the point where health officials changed the definition of "vaccine" multiple times.

Tucker Carlson recently sat down with Dr. Pierre Kory, a critical care specialist and vocal critic of vaccines. The two had a wide-ranging discussion, which included vaccine safety and efficacy, excess mortality, demographic impacts of the virus, big pharma, and the professional price Kory has paid for speaking out.

Keep reading below, or if you have roughly 50 minutes, watch it in its entirety for free on X:

Ep. 81 They’re still claiming the Covid vax is safe and effective. Yet somehow Dr. Pierre Kory treats hundreds of patients who’ve been badly injured by it. Why is no one in the public health establishment paying attention? pic.twitter.com/IekW4Brhoy

— Tucker Carlson (@TuckerCarlson) March 13, 2024

"Do we have any real sense of what the cost, the physical cost to the country and world has been of those vaccines?" Carlson asked, kicking off the interview.

"I do think we have some understanding of the cost. I mean, I think, you know, you're aware of the work of of Ed Dowd, who's put together a team and looked, analytically at a lot of the epidemiologic data," Kory replied. "I mean, time with that vaccination rollout is when all of the numbers started going sideways, the excess mortality started to skyrocket."

When asked "what kind of death toll are we looking at?", Kory responded "...in 2023 alone, in the first nine months, we had what's called an excess mortality of 158,000 Americans," adding "But this is in 2023. I mean, we've had Omicron now for two years, which is a mild variant. Not that many go to the hospital."

'Safe and Effective'

Tucker also asked Kory why the people who claimed the vaccine were "safe and effective" aren't being held criminally liable for abetting the "killing of all these Americans," to which Kory replied: "It’s my kind of belief, looking back, that [safe and effective] was a predetermined conclusion. There was no data to support that, but it was agreed upon that it would be presented as safe and effective."

Tucker Carlson Asks the Forbidden Question

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

He wants to know why the people who made the claim “safe and effective” aren’t being held to criminal liability for abetting the “killing of all these Americans.”

DR. PIERRE KORY: “It’s my kind of belief, looking back, that [safe and… pic.twitter.com/Icnge18Rtz

Carlson and Kory then discussed the different segments of the population that experienced vaccine side effects, with Kory noting an "explosion in dying in the youngest and healthiest sectors of society," adding "And why did the employed fare far worse than those that weren't? And this particularly white collar, white collar, more than gray collar, more than blue collar."

Kory also said that Big Pharma is 'terrified' of Vitamin D because it "threatens the disease model." As journalist The Vigilant Fox notes on X, "Vitamin D showed about a 60% effectiveness against the incidence of COVID-19 in randomized control trials," and "showed about 40-50% effectiveness in reducing the incidence of COVID-19 in observational studies."

Dr. Pierre Kory: Big Pharma is ‘TERRIFIED’ of Vitamin D

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

Why?

Because “It threatens the DISEASE MODEL.”

A new meta-analysis out of Italy, published in the journal, Nutrients, has unearthed some shocking data about Vitamin D.

Looking at data from 16 different studies and 1.26… pic.twitter.com/q5CsMqgVju

Professional costs

Kory - while risking professional suicide by speaking out, has undoubtedly helped save countless lives by advocating for alternate treatments such as Ivermectin.

Kory shared his own experiences of job loss and censorship, highlighting the challenges of advocating for a more nuanced understanding of vaccine safety in an environment often resistant to dissenting voices.

"I wrote a book called The War on Ivermectin and the the genesis of that book," he said, adding "Not only is my expertise on Ivermectin and my vast clinical experience, but and I tell the story before, but I got an email, during this journey from a guy named William B Grant, who's a professor out in California, and he wrote to me this email just one day, my life was going totally sideways because our protocols focused on Ivermectin. I was using a lot in my practice, as were tens of thousands of doctors around the world, to really good benefits. And I was getting attacked, hit jobs in the media, and he wrote me this email on and he said, Dear Dr. Kory, what they're doing to Ivermectin, they've been doing to vitamin D for decades..."

"And it's got five tactics. And these are the five tactics that all industries employ when science emerges, that's inconvenient to their interests. And so I'm just going to give you an example. Ivermectin science was extremely inconvenient to the interests of the pharmaceutical industrial complex. I mean, it threatened the vaccine campaign. It threatened vaccine hesitancy, which was public enemy number one. We know that, that everything, all the propaganda censorship was literally going after something called vaccine hesitancy."

Money makes the world go 'round

Carlson then hit on perhaps the most devious aspect of the relationship between drug companies and the medical establishment, and how special interests completely taint science to the point where public distrust of institutions has spiked in recent years.

"I think all of it starts at the level the medical journals," said Kory. "Because once you have something established in the medical journals as a, let's say, a proven fact or a generally accepted consensus, consensus comes out of the journals."

"I have dozens of rejection letters from investigators around the world who did good trials on ivermectin, tried to publish it. No thank you, no thank you, no thank you. And then the ones that do get in all purportedly prove that ivermectin didn't work," Kory continued.

"So and then when you look at the ones that actually got in and this is where like probably my biggest estrangement and why I don't recognize science and don't trust it anymore, is the trials that flew to publication in the top journals in the world were so brazenly manipulated and corrupted in the design and conduct in, many of us wrote about it. But they flew to publication, and then every time they were published, you saw these huge PR campaigns in the media. New York Times, Boston Globe, L.A. times, ivermectin doesn't work. Latest high quality, rigorous study says. I'm sitting here in my office watching these lies just ripple throughout the media sphere based on fraudulent studies published in the top journals. And that's that's that has changed. Now that's why I say I'm estranged and I don't know what to trust anymore."

Vaccine Injuries

Carlson asked Kory about his clinical experience with vaccine injuries.

"So how this is how I divide, this is just kind of my perception of vaccine injury is that when I use the term vaccine injury, I'm usually referring to what I call a single organ problem, like pericarditis, myocarditis, stroke, something like that. An autoimmune disease," he replied.

"What I specialize in my practice, is I treat patients with what we call a long Covid long vaxx. It's the same disease, just different triggers, right? One is triggered by Covid, the other one is triggered by the spike protein from the vaccine. Much more common is long vax. The only real differences between the two conditions is that the vaccinated are, on average, sicker and more disabled than the long Covids, with some pretty prominent exceptions to that."

Watch the entire interview above, and you can support Tucker Carlson's endeavors by joining the Tucker Carlson Network here...

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

Looking Back At COVID’s Authoritarian Regimes

Health Officials: Man Dies From Bubonic Plague In New Mexico

Five Aerospace Investments to Buy as Wars Worsen Copy

Stock Market Today: Stocks turn lower as factory inflation spikes, retail sales miss target

The SNF Institute for Global Infectious Disease Research announces new advisory board

COVID-19 vaccines: CDC says people ages 65 and up should get a shot this spring – a geriatrician explains why it’s vitally important

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A