This article takes a tilt at increasing speculation about statist global resets, and why plans such as those promoted by the World Economic Forum will fail. Central bank digital currencies will simply run out of time.

Instead, the collapse of unbacked fiat currencies will end all supra-national government solutions to their policy failures. Already, there is mounting evidence of money beginning to flee bank accounts into stocks, commodities and even bitcoin. This is an early warning of a rapidly developing monetary collapse.

Moreover, nothing can now stop the collapse of fiat currencies, and with it schemes to control humanity for the convenience and ambitions of government planners. There can only be one statist solution and that is to mobilise gold reserves to back and save their currencies, which in order to succeed will have to be fully convertible into circulating gold coinage. It will also require the role of governments to be reset into a non-welfare, non-interventionist minimalist role, which can only be achieved after a complete collapse of the current fiat-financed system.

Anything less will fail.

The Deep State and The Blob fuel conspiracy theories

Increasingly, people are beginning to realise that their world is undergoing a period of rapid change, with the future of fiat money now uncertain. For most, it is too difficult to even contemplate. But growing uncertainties are driving wild speculation about what those in authority now have in store for the human race in the form of a global reset. It is a time for conspiracy theorists, aided and abetted by our politicians and central bankers who are being increasingly evasive, because events are spiralling out of their control.

Then there is America’s Deep State, or the British equivalent, the more recently christened Blob; an amorphous entity comprised of the permanent bureaucracy with its own agenda. These faceless planners have moved on from merely making ministers’ lives difficult if they deviate from the blob’s predetermined course — immortalised in “Yes Minister” and its sequel series “Yes Prime Minister”.

As we saw with Brexit, The Blob has been rigging political outcomes, even conniving in elections. Christopher Steele, an ex-MI6 officer produced a dodgy dossier on Trump to influence the American presidential election in 2016. But there is no such thing as an ex-MI6 Agent because of the Official Secrets Act, so we can only conclude that the intelligence arm of The Blob sanctioned it on a distanced basis. MI6 works with other intelligence agencies under the five-eyes agreement and is close to the CIA. Though they do not necessarily share intelligence, it is impossible to conceive of Steele’s role in influencing the outcome of a US presidential election without the CIA’s knowledge. Almost certainly, the fact that it was commissioned must have been with the CIA’s blessing.

At the time of writing, we do not know the outcome of the current presidential election, but enough doubt has been thrown on the validity of the voting process to implicate unknown parties in managing the outcome. It can never be proved, but for increasing numbers of sceptics it looks like a Deep State operation. It is therefore hardly surprising that conspiracies abound.

The World Economic Forum

The most prominent of these conspiracies has hit the headlines in recent weeks. Its ambition is to take the lead in resetting the world by dismantling the capitalist system in favour of a greater technocratic rule — a fourth industrial revolution no less, even planting microchips in humans to read their brains and control them. The leader is one Klaus Schwab, whose World Economic Forum runs the annual Davos bunfight.

As leader of the Davos forum, Schwab probably sees himself as the coordinator of world government. If so, at 82 years old he is probably getting impatient about the progress towards his personal vision of ultimate power. The covid chaos and the success of his climate change agenda must be encouraging him to think he is very close to a breakthrough. Alternatively, we might consider Schwab as a latter-day Charles Fourier (1772—1837), the utopian socialist philosopher, whose forgotten ideals were only marginally more narcissistic and bizarre than Schwab’s.

While the great and the not so good love the annual Davos party as a networking venue for the politics industry, when it comes to transferring real power to Schwab, it’s a no-no. The only time a politician transfers power is when he is deposed by his or her electorate, colleagues, or the military. And history is littered with utopians, like Schwab, grasping for power over their fellow men. In addition to Charles Fourier, we can include Georg Hegel (1770—1831) and Auguste Comte (1798—1857), as well, of course, as Karl Marx. As thinkers or philosophers, they were all influential in their day and some of their ideas persist in the naïve.

So, while increasing numbers of well-informed people are beginning to sense the end of the current world order, to assume that this will hasten the WEF’s grab for world domination by influencing events is a mistake. All our deep states, blobs and their branches, particularly central banks, will want to hold onto and enhance their executive power with the political class increasingly cast as cover. The planners at national level are not going to submit to Mr Schwab’s plans for world domination. Instead, international relations involve mutual cooperation to secure purely domestic objectives, something President Trump was in the process of destroying. From the Deep State’s point of view, perhaps that’s why he had to be deposed in favour of Biden, who is a long-serving compliant figure.

Central bank digital currencies (CBDCs)

There can be little doubt that central banks wish to increase their control over money and how it is used, cutting out the obstacle of commercial banks who produce most of the money in circulation through the expansion of bank credit. From a statist point of view, commercial banking is a dinosaur, an outdated remnant of free markets, perpetuating needless systemic risk and superseded by technology. Branch networks will disappear with cash, changing relationships between banks and the general public for ever.

By introducing direct central bank accounts for members of the public and every business, commercial banks become superfluous and can be allowed to die. And if one goes bust before commercial banking has ended, the facility to transfer all its loans and deposits onto a central bank’s books will then exist. The removal of systemic risk by the abolition of commercial banks is one of several likely long-term objectives of CBDCs. Commercial banks can be left with the role of investment banking activities in capital markets.

We can imagine the development of CBDCs going even further than just replacing cash. Stimulation by dropping money into personal accounts can be used to target increased spending by consumers, or even groups of consumers, sorted by wealth, location or other factors. Some consumers can be favoured relative to others, so in a swing state, for example, an incumbent administration might buy votes. While this would be strongly denied, as we have seen with unfettered fiat currency the state creeps incrementally towards unstated objectives, using every tool at its disposal. The election of Deep State-approved politicians then becomes possible.

Eventually, funding of all capital projects will come under the direct control of the central bank. And savings deposits, always seen to be a brake on consumption, can be banished. Capital can be made available for government schemes and favoured businesses on the say so of the central bank.

A future government statement might be issued on the following lines:

“Your Government is pleased to announce that the National Audit Office has approved a number of infrastructure projects targeted at improving communications between administrative centres. This investment over ten years will secure an estimated 500,000 jobs. The cost over the life of the project is XXX billion monetary units. The Central Bank has confirmed it will make funding for these projects available, both to your Government and approved private sector contractors.”

This would be a planners’ heaven. Furthermore, CBDC money can be withheld or frozen for anyone suspected of crimes and tax evasion, starving them into confessions of guilt. The justification is always that it is in the national interest to ensure that financial and tax crimes are eliminated — something commercial banks have singularly failed to do. Overseas payments can be routed through other CBDCs, giving the central banking network control over world trade. Just imagine foreign trade being conducted through a grander version of the Eurozone’s TARGET2 settlement system!

Worried yet? In the advanced economies Covid-19 has nearly eliminated cash, which doubtless is intended to be replaced entirely by CBDCs. The end of cash and bank deposits will allow the central bank to cap the amount of cash anyone can hold, and also ensure that everyone is paid a “living wage”. Already flagged, another intention is to eliminate the burden of interest rates and by controlling where money supply is expanded, manage the economy.

It is commonly assumed that those in charge of us know what they are doing — they don’t. They have become trapped at a socialist endpoint and are doubling down in their efforts towards greater socialism. But their dreams of future control are mere escapism. Individuals will lose yet more personal freedom, but ultimately the state cannot conquer human nature and the will of individuals to do what they want. The Soviets attempted it and failed, despite killing and starving many millions.

Central to the collapse of any state-directed reset will be the loss of faith in fiat currencies, and particularly that of the world’s reserve currency, the US dollar. This remains the case irrespective of whether circulating currency is in cash, bank deposits, or CBDCs. Indeed, the collapse could be hastened by CBDCs, because the intention is to increase the pace of injection of new money into the economy if it is required (it always is), and to impose deeper negative interest rates, which cannot be easily achieved under the current monetary system.

If these statist intentions are allowed to prevail, along with other agendas such as the elimination of cheap and effective fossil-based energy, the outlook for humanity is exceedingly grim. Like communism, the global reset into which the western world is drifting will destroy society. Those who believe in liberal values in the original sense of the term — not the modern socialist connotation — will find themselves welcoming the destruction of the current system before it is evolved any further.

The course of a currency collapse

The end of fiat currencies is likely to come sooner than later, from the consequences of today’s massive money-printing, particularly of dollars. Already, US government spending is financed substantially more by currency debasement than taxes, a condition that will almost certainly continue to deteriorate rapidly in the coming months. Furthermore, the global banking system, which is extremely thinly capitalised, faces a tsunami of bad debts which can only lead to a systemic failure — most likely in the Eurozone initially, but threatening all other jurisdictions through counterparty risks. It is coming to a head and is likely to happen soon, possibly triggered by the second covid wave.

Long before the two or three years required for any CBDC to be operational, the world’s reserve fiat currency, the US dollar, is already hyper-inflating. There are signs the markets are beginning to understand this. Bitcoin’s price has risen sharply, sending signals to everyone that the differential between its ultimately fixed quantity and the accelerating rates of fiat currency debasement is feeding dramatically into the price.

Despite the economic slump, equity markets are being driven to new highs as non-financial customers deem stocks to be preferable to bank deposits. It has not helped that the Fed reduced deposit rates to zero last March, well below everyone’s time preference. The Fed has also promised infinite QE in order to fund the fiscal deficit. Therefore, it is not surprising that individuals and corporations are shifting out of cash balances into financial and other assets, with the notable exception of fixed-interest bonds. Rising commodity and raw material prices are also telling us that dollars are been sold in those markets.

This is the point being missed in all commentaries: the mounting evidence that markets, being forward-looking, are beginning to abandon the dollar. And once it goes beyond a certain point, nothing will reverse a rapid loss of purchasing power to the point of worthlessness. To avoid this outcome central banks led by the Fed must immediately abandon inflationary financing of budget deficits.

That is not going to happen. In addition to the current hyperinflation must be added the inflationary cover for the costs and consequences of rescuing a failing global banking system. The costs are immediate, in that governments will take on their books everyone’s bad debts. The consequences are that through their central banks they will have no political alternative other than to counter the economic slump through yet more money printing.

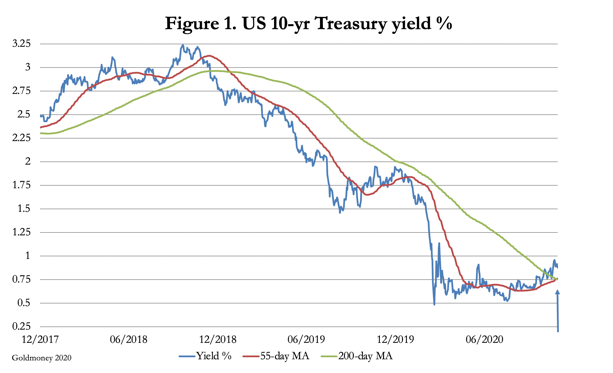

US Treasury bond yields are already beginning to rise, perhaps reflecting this developing outcome as Figure 1 shows.

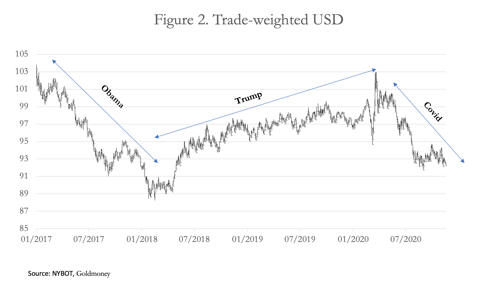

The up-arrow at the bottom-right of the chart shows that the downward momentum for the bond yield has reversed, forming a golden cross; that is to say the yield is above its two commonly followed moving averages which in turn are forming a cross with the 55-day moving average rising above the 200-day moving average, a strong indicator of a major turning point and of higher bond yields to come. The upward turn of bond yields is to be viewed in the context of the dollar’s trade weighted index, which is shown in Figure 2.

Currently standing at 92.40, if the dollar’s TWI breaks below 91.75 (the low on 1 September) it is likely to head significantly lower. With foreign holdings of dollars and dollar denominated financial securities totalling almost $27 trillion, the chances are that dumping of the dollar on the foreign exchanges will increase rapidly. That being the case, the Fed will not only be funding the unprecedentedly high (for peacetime) budget deficit but will have to absorb foreign sales of US Treasuries and dollars in order to keep the cost of government funding suppressed.

Evidence is mounting that it cannot be done. And with the end of the suppression of interest rates comes the collapse of accumulated malinvestments, of government finances, and of the currency itself.

First the ashes, then, hopefully the phoenix

Elected in 1929, Hoover was the first US President who thought he could improve on the capitalist system of markets reforming themselves, and the results were a disaster. He was thrown out of office and replaced with another interventionist, Roosevelt, and the supremacy of the US Government over markets reforming themselves became established. The situation today is the logical destination of the fallacy that governments can run the economy.

It will end with the collapse and replacement of today’s unbacked fiat currencies — the ashes and then the phoenix. There is every indication that the time when all is rendered into ashes is rapidly approaching. People with fiat, earning fiat, relying on fiat will be impoverished. A currency collapse with no foreign currency to escape into is a cataclysmic event, the like of which we haven’t seen before, not even in Roman times. If it doesn’t buy you food and warmth a million bucks is worthless.

Governments will also have no means of collecting taxes, other than in their worthless currencies. They will be unable to pay their administrators, who cannot even afford to attend their offices. Their pensions and everybody else’s will be worthless. There will be no incentive for anyone in government without money. And without money there is no political power.

There can only be one solution, and that is a reset with gold. The slide in currencies can be stopped by making them exchangeable into gold. The reason for a gold-backed reset is not so much to stop a fiat currency from further collapse but to use it to ensure the widest distribution of the national gold reserves through a reformed gold-backed currency. The US Treasury claims it still has over 8,000 tonnes of gold, which assuming the Deep State hasn’t raided it, can ensure that a new dollar, convertible by everyone into gold, can circulate as money.

The same is true for other currencies, to greater or lesser degrees depending on their national gold reserves. But to be credible, gold coins must also circulate freely alongside readily convertible paper and digital substitutes. The banking system must also be reformed to do away with bank credit expansion, which creates deposits unbacked by gold. By then most of them may be in public ownership or protection, so a reform to abolish bank credit expansion should not be too difficult.

The mobilisation of central bank gold is the best outcome by far. It returns the choice of money to the people who use it for the intermediation between their production and consumption. But very few in government, their Deep States or The Blobs, have the intellectual capacity to understand what needs to be done. Their advisors are inflationists to a man or woman. Furthermore, the US’s Deep State is obsessed with the threat from China and Russia, which between them control international bullion markets (London and Comex are just paper), and have substantial declared and undeclared reserves. Legitimising gold will transfer enormous monetary and geopolitical power from America to the Asian hegemons, which is likely to be strongly resisted.

Furthermore, it will require governments to backtrack on the socialising process, whereby by providing welfare and regulating everything their budgets got out of hand. They must aim to reduce the full burden of their activities on the economy to under 20%.

Following a currency collapse, any central bank that thinks it can use a CBDC to manage market outcomes will undermine its own credibility. Other than issuers of gold-backed notes, they will have no role. In order for the necessary reforms to stick, flights of fancy such as the statist ambitions of planners and of the Klaus Schwabs of this world must be abandoned, along with all the false sciences adopted by statists. But on the positive side, a collapse of fiat currencies is required to sweep away the current failing system, and sooner or later that is what we are going to get.

Bougie Broke The Financial Reality Behind The Facade

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive…

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive restaurants. Yet they complain about living paycheck to paycheck and lacking the means to support their lifestyle.

Bougie broke is like “keeping up with the Joneses,” spending beyond one’s means to impress others.

Bougie Broke gives us a glimpse into the financial condition of a growing number of consumers. Since personal consumption represents about two-thirds of economic activity, it’s worth diving into the Bougie Broke fad to appreciate if a large subset of the population can continue to consume at current rates.

The Wealth Divide Disclaimer

Forecasting personal consumption is always tricky, but it has become even more challenging in the post-pandemic era. To appreciate why we share a joke told by Mike Green.

Bill Gates and I walk into the bar…

Bartender: “Wow… a couple of billionaires on average!”

Bill Gates, Jeff Bezos, Elon Musk, Mark Zuckerberg, and other billionaires make us all much richer, on average. Unfortunately, we can’t use the average to pay our bills.

According to Wikipedia, Bill Gates is one of 756 billionaires living in the United States. Many of these billionaires became much wealthier due to the pandemic as their investment fortunes proliferated.

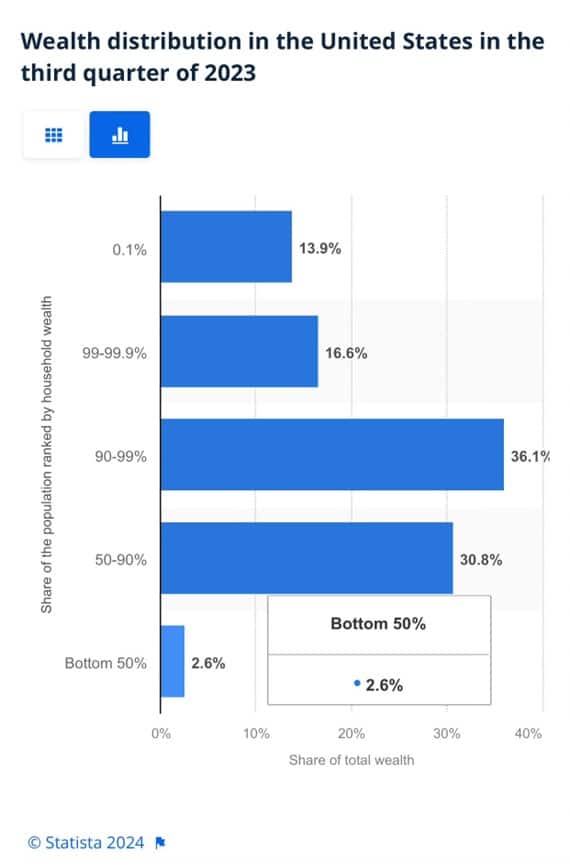

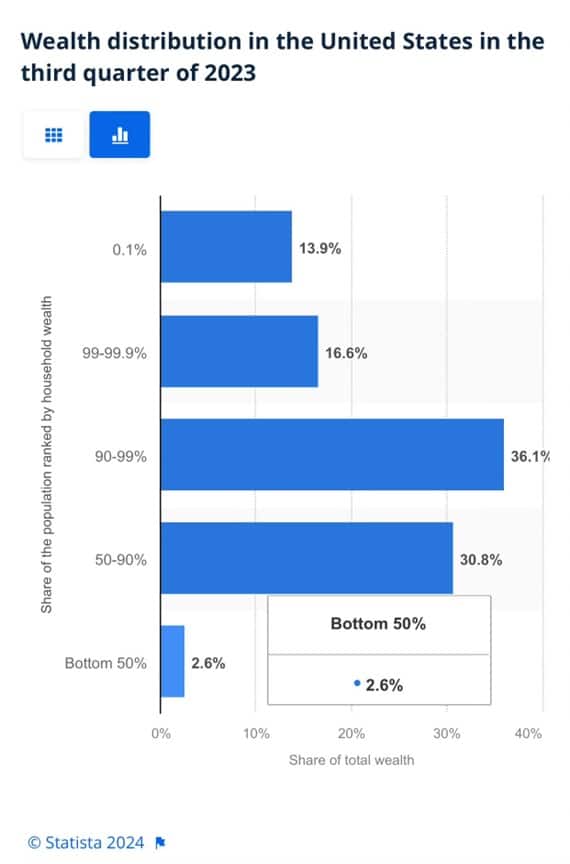

To appreciate the wealth divide, consider the graph below courtesy of Statista. 1% of the U.S. population holds 30% of the wealth. The wealthiest 10% of households have two-thirds of the wealth. The bottomhalf of the population accounts for less than 3% of the wealth.

The uber-wealthy grossly distorts consumption and savings data. And, with the sharp increase in their wealth over the past few years, the consumption and savings data are more distorted.

Furthermore, and critical to appreciate, the spending by the wealthy doesn’t fluctuate with the economy. Therefore, the spending of the lower wealth classes drives marginal changes in consumption. As such, the condition of the not-so-wealthy is most important for forecasting changes in consumption.

Revenge Spending

Deciphering personal data has also become more difficult because our spending habits have changed due to the pandemic.

A great example is revenge spending. Per the New York Times:

Ola Majekodunmi, the founder of All Things Money, a finance site for young adults, explained revenge spending as expenditures meant to make up for “lost time” after an event like the pandemic.

So, between the growing wealth divide and irregular spending habits, let’s quantify personal savings, debt usage, and real wages to appreciate better if Bougie Broke is a mass movement or a silly meme.

The Means To Consume

Savings, debt, and wages are the three primary sources that give consumers the ability to consume.

Savings

The graph below shows the rollercoaster on which personal savings have been since the pandemic. The savings rate is hovering at the lowest rate since those seen before the 2008 recession. The total amount of personal savings is back to 2017 levels. But, on an inflation-adjusted basis, it’s at 10-year lows. On average, most consumers are drawing down their savings or less. Given that wages are increasing and unemployment is historically low, they must be consuming more.

Now, strip out the savings of the uber-wealthy, and it’s probable that the amount of personal savings for much of the population is negligible. A survey by Payroll.org estimates that 78% of Americans live paycheck to paycheck.

More on Insufficient Savings

The Fed’s latest, albeit old, Report on the Economic Well-Being of U.S. Households from June 2023 claims that over a third of households do not have enough savings to cover an unexpected $400 expense. We venture to guess that number has grown since then. To wit, the number of households with essentially no savings rose 5% from their prior report a year earlier.

Relatively small, unexpected expenses, such as a car repair or a modest medical bill, can be a hardship for many families. When faced with a hypothetical expense of $400, 63 percent of all adults in 2022 said they would have covered it exclusively using cash, savings, or a credit card paid off at the next statement (referred to, altogether, as “cash or its equivalent”). The remainder said they would have paid by borrowing or selling something or said they would not have been able to cover the expense.

Debt

After periods where consumers drained their existing savings and/or devoted less of their paychecks to savings, they either slowed their consumption patterns or borrowed to keep them up. Currently, it seems like many are choosing the latter option. Consumer borrowing is accelerating at a quicker pace than it was before the pandemic.

The first graph below shows outstanding credit card debt fell during the pandemic as the economy cratered. However, after multiple stimulus checks and broad-based economic recovery, consumer confidence rose, and with it, credit card balances surged.

The current trend is steeper than the pre-pandemic trend. Some may be a catch-up, but the current rate is unsustainable. Consequently, borrowing will likely slow down to its pre-pandemic trend or even below it as consumers deal with higher credit card balances and 20+% interest rates on the debt.

The second graph shows that since 2022, credit card balances have grown faster than our incomes. Like the first graph, the credit usage versus income trend is unsustainable, especially with current interest rates.

With many consumers maxing out their credit cards, is it any wonder buy-now-pay-later loans (BNPL) are increasing rapidly?

Insider Intelligence believes that 79 million Americans, or a quarter of those over 18 years old, use BNPL. Lending Tree claims that “nearly 1 in 3 consumers (31%) say they’re at least considering using a buy now, pay later (BNPL) loan this month.”More telling, according to their survey, only 52% of those asked are confident they can pay off their BNPL loan without missing a payment!

Wage Growth

Wages have been growing above trend since the pandemic. Since 2022, the average annual growth in compensation has been 6.28%. Higher incomes support more consumption, but higher prices reduce the amount of goods or services one can buy. Over the same period, real compensation has grown by less than half a percent annually. The average real compensation growth was 2.30% during the three years before the pandemic.

In other words, compensation is just keeping up with inflation instead of outpacing it and providing consumers with the ability to consume, save, or pay down debt.

It’s All About Employment

The unemployment rate is 3.9%, up slightly from recent lows but still among the lowest rates in the last seventy-five years.

The uptick in credit card usage, decline in savings, and the savings rate argue that consumers are slowly running out of room to keep consuming at their current pace.

However, the most significant means by which we consume is income. If the unemployment rate stays low, consumption may moderate. But, if the recent uptick in unemployment continues, a recession is extremely likely, as we have seen every time it turned higher.

It’s not just those losing jobs that consume less. Of greater impact is a loss of confidence by those employed when they see friends or neighbors being laid off.

Accordingly, the labor market is probably the most important leading indicator of consumption and of the ability of the Bougie Broke to continue to be Bougie instead of flat-out broke!

Summary

There are always consumers living above their means. This is often harmless until their means decline or disappear. The Bougie Broke meme and the ability social media gives consumers to flaunt their “wealth” is a new medium for an age-old message.

Diving into the data, it argues that consumption will likely slow in the coming months. Such would allow some consumers to save and whittle down their debt. That situation would be healthy and unlikely to cause a recession.

The potential for the unemployment rate to continue higher is of much greater concern. The combination of a higher unemployment rate and strapped consumers could accentuate a recession.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}