Uncategorized

The Beauty Parlor’s Full Of Sailors And The Circus Is In Town

The Beauty Parlor’s Full Of Sailors And The Circus Is In Town

Authored by James Howard Kunstler via Kunstler.com,

“They have tried to…

Share this:

Authored by James Howard Kunstler via Kunstler.com,

“They have tried to solve a wide range of insoluble problems, from the weather to poverty to viruses, and now they will attempt to solve us.”

- Eugyppius

This is that part of the movie where the hero — you — tumbles off the cliff on Kong Island in a lightning storm with a canyon full of tarantulas down below where you’ll soon be landing. I know, not a pretty picture.

The cliff is our country’s financial quandary; the lightning is us getting sucked directly into war; and the tarantula pit below is the emerging peril of Covid vaccine injury and death coming on hard, like your landing.

Gold and silver are vaulting up suddenly like nobody’s business (literally). This may be fun to see if you are sitting on a pile, even a small pile of the stuff. But to everybody else it’s a signal that something is messed up in the complex engine of the economy. You know, of course, that our money is debt. So, debt is the fuel that drives that engine. Debt is a promise to pay back money with interest to take advantage of the time-value of money. The time-value of money means it’s better to have the money now (to keep the engine running) than to wait until your work produces money (if it even can).

The trouble is, debt loses its credibility if there is no plausible way of paying it back, or even just to keep paying the interest. That’s exactly what is happening now. Everybody can see that the US government can’t pay the interest on its debt, which is Treasury bonds, notes, and bills (from long duration to short). That debt is running at well over $1-trillion a year. That’s a thousand billion, which is a thousand million, altogether a million million. See, it’s impossible to grok how more than a trillion dollars gets produced in an economy based on selling fried chicken nuggets and streamed movies to people with no jobs.

When the Treasury holds an auction on a new issue of bonds (needed to pay off the interest on old bonds) and nobody shows up to buy because they doubt its ability to pay interest on the new paper, our country’s debt becomes worthless. As a last resort, the Federal Reserve swoops in and buys that worthless paper by creating “money” on its computer. That “money” goes out into the economy. The Fed pretends to get paid interest. It’s all fakery, a swindle. It’s like putting water in the gas tank of your engine. You know that the engine is going to throw a rod. When it does, it’ll be such a shock that the vehicle it’s running in is liable to hit a bridge abutment or something else hard.

That’s what tumbling off the cliff is like.

The dopes running US foreign policy are so foolishly obsessed with taunting Russia (“poking the bear”), that they can’t give up their sponsorship of the war in Ukraine, which Ukraine is losing because they never had the mojo for the fight. That should have been obvious, but for some reason our “best-and-brightest” overlooked that. No amount of free weaponry and ammo can make up for the fact that Ukraine has run out of young men to pointlessly get shredded by Russian artillery. Russia is unwilling to get rolled by NATO and the US in a part of the world Russia has controlled for centuries. Yet, “Joe Biden” keeps hinting about sending America’s tranny army there, and even gearing up the military draft for the nose-ring and blue hair generation. Good luck with that.

Nor does “JB” exercise any control over what Israel does over in the Bible Lands. Bibi gonna do what Bibi gonna do. Israel can’t be persuaded that the current war is not a struggle for its existence. As Scott Adams points out, Israel has decided to pawn off its Holocaust cred in order to treat its enemies as harshly as possible, so as not to get wiped off the map. Israel has treated the Palestinians very harshly. (The October 7 Hamas raid was pretty darn harsh, too.) In any case, world opinion went all rancid on Israel. That hasn’t stopped them. Now Israel faces its ultimate foe, Persia, a.k.a. Iran, these days. Persia has a big army and a lot of weapons, and all sorts of wing-men in the neighborhood. . . as a practical matter, most of Islam right now. This week, Persia made noises about an imminent attack on Israel. Didn’t happen so far.

Let’s get real on Islam. Its core principle is to exterminate the humans on this planet who are not of Islam. Islam has been pissed-off at Western Civ since the Crusades, its animus renewed in 1683, when Islam’s advance into Europe was halted at the gates of Vienna, and then again in modern times when Islam got pushed around because Western Civ wanted its oil. Islam is overrunning Europe again and penetrating the USA through our southern border. Islam means business. It wants to wreck us, kill us, and take our stuff. And it dearly, sorely, wants to deep-six Israel, which Islam contemptuously refer to as “the Zionist entity,” as if it were some crypto-insectile space alien.

America (and Europe, too) wants to play this both ways: to grudgingly help Israel survive while at the same time pretending not to notice Islam’s true aims. Looks like Israel has decided to go for broke on this one whether we ride to rescue or not. Israel may have to go “Mad Dog” in its neighborhood. They may lose this thing anyway. The rest of the world will affect to hate them for it no matter how it ends. Meanwhile, all over Europe the Islamic birth-rate way outpaces the Euro peoples’ birth rate. And how many angry, determined “sleepers” has Islam snuck into the USA the past several years across “Joe Biden’s” open border. It’s a bit disturbing to contemplate. Also, never under-estimate the damage that can be wreaked with small arms against “a pitiful, helpless, giant,” as Dick Nixon once described our country in an earlier time of distress. There’s your lightning storm.

At the bottom of the cliff is the vaxxed-up population of the world waiting for their spike protein infested bodies and dysregulated immune systems to enter fatal break down. Many already have injured organs, hearts, brains, blood, ovaries, etc. Many others will get in trouble when a more efficient Covid-19 mutation goes lethal on them. The public health authorities are desperately trying to conceal the damage. Some organized groups of people are clamoring for the data on vaccine injury and death from places like the CDC, only to discover that the public health agencies not only won’t disclose it but probably avoided even collecting it over fear of what it would show. Horror creeps on little tarantula feet.

This is how the movie is going as of April. Spring is hardly fledged. Portent looms at every compass point. You’re in a tight spot. (We all are.) In modern times — and I mean going back to the first twinges of the Enlightenment — faith in the people running things has never been lower. It’s still an election year, har har! It makes you wonder if this movie is actually a comedy.

* * *

Support his blog by visiting Jim’s Patreon Page or Substack

Uncategorized

China Exports Collapse, Prompting Yuan Devaluation Fears

China Exports Collapse, Prompting Yuan Devaluation Fears

China’s export growth tumbled in March compared to last year, sparking questions…

Share this:

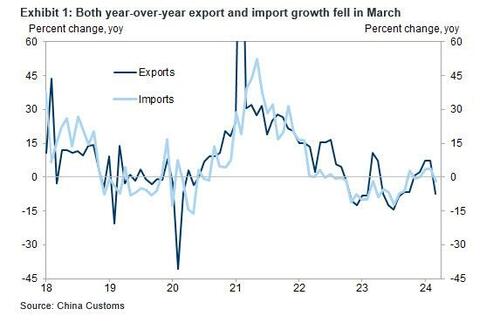

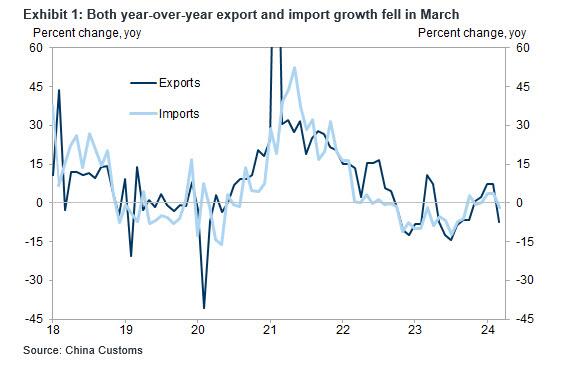

China’s export growth tumbled in March compared to last year, sparking questions about a possible yuan devaluation at a time when China's biggest mercantilist competitor in Asia - Japan - has intentionally cratered its currency.

Chinese Exports declined by 7.5% from a year earlier in March to $279.7 billion, far was than the median estimate of a 1.9% drop and was in sharp contrast to the 7.1% growth in combined figures for January and February. It was dragged down due to a higher base in the same period last year, when China reported robust growth of 14.8% at $315.6 billion. Imports also slumped, sliding -1.9% yoy in March, and far below the Bloomberg consensus of a +1.0% increase.

In sequential terms, exports increased by +1.2% in March (vs. +3.5% in January-February), while imports decreased by 1.4% in March (vs. +0.8% in January-February).

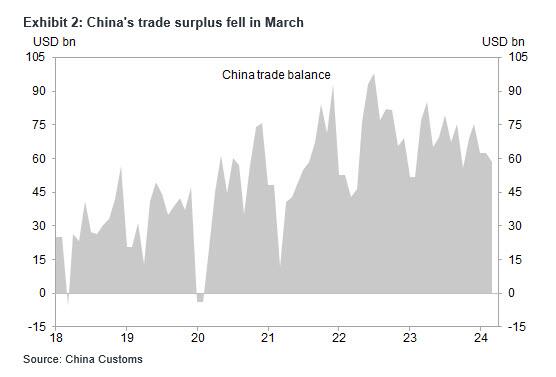

With exports collapsing, China's trade balance also slumped, dropping to just $58.6BN in March, far worse than the Bloomberg consensus of $69.1BN, and down from January-February average balance at US$62.6bn. Today's release of trade data only covers major trading partners and products. The detailed breakdown of trade by country and by product will be released on April 20.

Some more highlights:

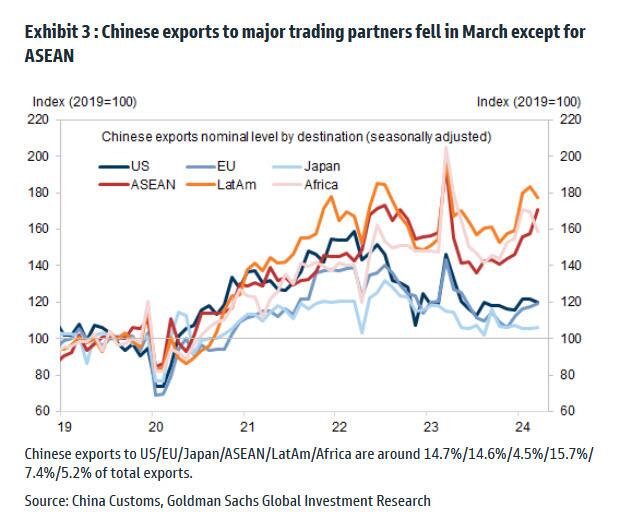

- By major destination, export value fell sequentially across major trading partners except for ASEAN. The high bases last March drove year-over-year export growth deeply negative. Among major DM countries, exports to the US dropped by 15.9% yoy in March (vs. +2.6% yoy in January-February), and exports to the European Union declined by 14.9% yoy in March (vs. -2.3% yoy in January-February). Among major EM economies, exports to ASEAN fell by 6.3% yoy in March (vs. +0.1% yoy in January-February).

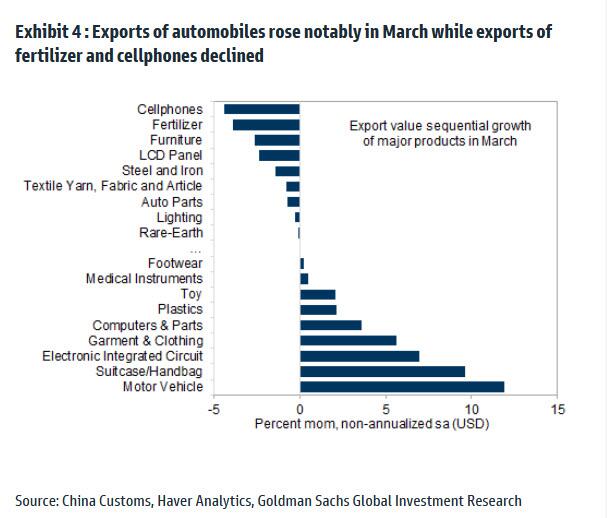

- By major category and in sequential terms, exports of automobiles rose notably in March while exports of fertilizer and cellphones declined. On a year-over-year basis, export growth of tech-related products remained strong. Export of chips increased by 11.5% yoy in March (vs. +21.4% yoy in January-February) with +7.0% sequential growth (mom non-annualized sa). Export growth of housing-related products moderated notably in March: for example, exports of furniture dropped by 12.3% yoy in March (vs. +28.7% yoy in January-February).

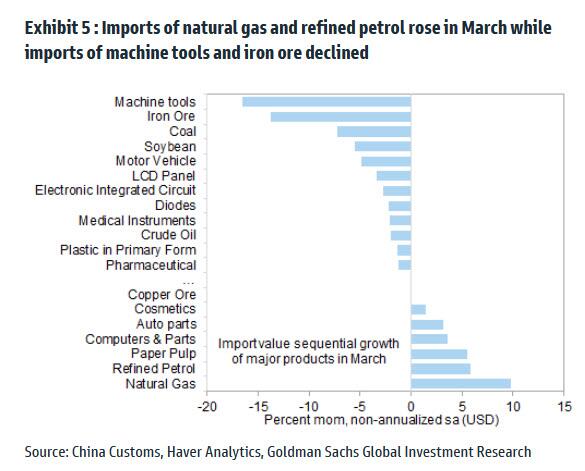

- Among major categories and in sequential terms, imports of natural gas and refined petrol rose in March while imports of machine tools and iron ore declined. For major commodities and on a year-over-year basis, import growth of metal ores remained solid in March while import growth of energy-related goods moderated. Specifically, import value of crude oil declined by 3.5% yoy in March (vs. +3.6% yoy in January-February) with import volume down 6.2% yoy (vs. +5.0% yoy in January-February). Import value of iron ore rose 7.5% yoy in March (vs. 33.0% yoy in January-February) with import volume up 0.5% yoy (vs. 7.9% yoy in January-February). On tech-related products, import growth of chips moderated significantly in March (+2.0% yoy in March vs. +14.4% yoy in January-February).

Last year, China experienced its first decline in export growth in seven years, with shipments dropping by 4.6% due to weak external demand. It created additional challenges amid Beijing’s efforts to revive the post-pandemic economy, as it was also grappling with an exodus of foreign investment, waning market confidence and potential trade barriers.

Meanwhile, as Bloomberg notes, the dismal trade numbers will only add to the worries over the world’s second-biggest economy, which bodes poorly for a yuan that’s been in retreat this year, which incidentally is just what Beijing wants since China desperately needs a weak currency to make its exports cheaper, which however is proving very difficult with the yen not only sliding to a record low against the yuan, but dropping below a key support level.

Dollar-yuan is being driven by the contrasting outlooks for central bank policy, along with the direction of USD/JPY.

Bloomberg's conclusion here is that until there is official support for the yen - which seems unlikely even as the Japanese currency crater to a new record low every single day - or a shift back to expectations for early Fed interest rate cuts, "there isn’t much Chinese authorities can do about an outperforming US dollar. Especially as the PBOC is seen easing monetary policy again this year." We disagree, especially because the PBOC is seen easing monetary policy: China can - and at this rate will have no choice but to - devalue the currency, and while so far it has been doing everything in its power to telegraph that it will defend the yuan and avoid a repeat of the record capital outflows from 2015, one day Beijing will shock everyone when it announced that the Yuan has lost 10% of its value overnight, and which point the surge in crypto and gold will truly shine.

The bottom line is that Beijing continues to be trapped: either keep the currency artificially "stable" and suffer continued trade loss to competitor Japan which is crushing its currency, or devalue the yuan and regain the mercantilist throne, however at the expense of massive capital outflows.

Uncategorized

McDonald’s is bringing back a discontinued favorite

Several of McDonald’s breakfast menu items were cut during the pandemic.

Share this:

While the chain relies on menu stability and experiments with things that deviate from that far less frequently than some of its competitors, McDonald’s (MCD) has launched several items that it later discontinued over the years.

As part of its efforts to expand its breakfast offering, the fast-food chain first introduced a breakfast bagel with egg and a protein such as sausage, steak or cheese in 1999. Bagels in some form would be reworked (at one point, the chain sold plain bagels with cream cheese like at a New York deli) and taken off the menu multiple times over the next two dec

Related: Coca-Cola has a new soda for Diet Coke fans

McDonald’s launched a new type of bagel with egg and meat in 2018 but, as the covid-19 pandemic gripped the world in 2020, discontinued it due to both low demand and to minimize staff needed in the stores.

TheStreet

This is where you’ll be able to find these McDonald’s bagels

Since then, McDonald’s has started slowly bringing back bagels at different locations across the country. In November 2022, the Steak, Egg & Cheese Bagel, the Bacon, Egg & Cheese Bagel and the Sausage, Egg & Cheese Bagel were returned to some Chicago and New York locations.

More Food + Dining:

- Taco Bell menu tries new take on an American classic

- McDonald's menu goes big, brings back fan favorites (with a catch)

- The 10 best food stocks to buy now

Eagle-eyed fans later started seeing the item in some Southern California, Louisiana, Kentucky and Tennessee restaurants.

The latest market to get the breakfast bagels includes South and Central Texas locations such as Austin, San Antonio, College Station, Bryan and Corpus Christie.

As first reported by industry website Chewboom, McDonald’s fans have been seeing them reappear at their local restaurants and posting the news online. The McDonald’s Breakfast Bagel has a cult following and, during the time it was discontinued, several petitions clamoring for its return started popping up.

The fans have spoken: ‘We want them back!’

“At the beginning of the pandemic McDonalds took away all the bagel breakfast sandwiches!” a 2021 petition launched by a fan named Brandon reads. “It’s been forever and we are sitting here waiting for it to come back but yet are always told they don’t think it is coming back!! Well, we want them back!!”

This particular petition received nearly 2,000 signatures and while McDonald’s rarely comments directly on such fan requests, it has been reading the general room and slowly re-introducing breakfast bagels to more and more places.

Not every bagel sandwich is available at all locations during the morning hours but it has now been brought back enough that it is not unlikely one will find it at one’s home restaurant — a quick search shows that the Bacon, Egg & Cheese Bagel Breakfast Sandwich is available in places like New York, Chicago and many parts of Florida. Once the chain brings it back, the bagels generally remain as a permanent part of its breakfast offering rather than a seasonal or temporary promotion.

“The loss of McDonald's bagels never made sense because aside from the steak version of the breakfast sandwich, the only added item was the bagel itself,” Daniel Kline wrote for TheStreet earlier this year. “It's simply not much extra work for the chain to stock another line of bread and toasting a bagel is no different than toasting an English muffin.”

stocks pandemic covid-19Uncategorized

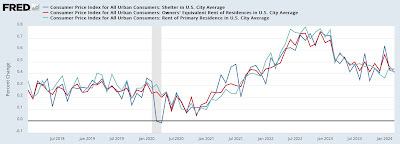

March consumer price inflation was still mainly about the dynamics of shelter and gas prices

– by New Deal democratThe one advantage of not reporting on the March CPI results for two days is I’ve had the opportunity to look at more data in…

Share this:

{kind=link}

{kind=link}

- by New Deal democrat

The one advantage of not reporting on the March CPI results for two days is I’ve had the opportunity to look at more data in depth and mull things over.

{kind=link}

Las Vegas Strip casino adds shows to star R&B singer’s residency

Superstar pop singer adds shows to Las Vegas Strip residency

Las Vegas Strip casino signs R&B superstar for extended residency

Gold’s recent performance draws parallels with major historical economic events

March consumer price inflation was still mainly about the dynamics of shelter and gas prices

Bankrupt essential retailer closing more stores across nation

DEI Cronyism And Woke Grifters

China Exports Collapse, Prompting Yuan Devaluation Fears

Las Vegas Strip casino extends superstar pop singer’s residency

Nearly 20% Of Recent San Francisco Home Sales Were Underwater

-

International3 weeks ago

International3 weeks agoParexel CEO to retire; CAR-T maker AffyImmune promotes business leader to chief executive

-

Spread & Containment1 month ago

Spread & Containment1 month agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Spread & Containment6 days ago

Spread & Containment6 days agoClimate-Con & The Media-Censorship Complex – Part 1

-

Spread & Containment4 days ago

Spread & Containment4 days agoFDA Finally Takes Down Ivermectin Posts After Settlement

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoVaccinated People Show Long COVID-Like Symptoms With Detectable Spike Proteins: Preprint Study

-

Uncategorized7 days ago

Uncategorized7 days agoCan language models read the genome? This one decoded mRNA to make better vaccines.

-

Uncategorized5 days ago

Uncategorized5 days agoWhat’s So Great About The Great Reset, Great Taking, Great Replacement, Great Deflation, & Next Great Depression?

-

International3 weeks ago

International3 weeks agoJapanese Preprint Calls For mRNA VaccinesTo Be Suspended Over Blood Bank Contamination Concerns