International

Tesla earnings: 5 key issues for Elon Musk as investors’ confidence sinks

This could be the most important conference call in Tesla history.

Share this:

Tesla shares edged higher Tuesday, potentially snapping an eight-day losing streak, as investors brace for a crucial first-quarter earnings update from the electric-vehicle producer after the close of trading.

Shares in Tesla (TSLA) are still suffering their second-largest drawdown since the company went public in 2010 and have shed nearly $350 billion in market value this year.

The group is now under tremendous pressure to regain investors' confidence and define its near-term growth prospects as EV demand has been fading and its profit margins have been narrowing.

Analysts estimate Tesla will post a bottom line of around 53 cents a share, down from 85 cents a share over the year-earlier period.

Group revenue is pegged at $22.15 billion, down 5%, which would mark its first year-on-year decline since the 2020 pandemic.

Below is a quick compendium of what are likely to be the key takeaways from tonight's earnings report and the highly anticipated conference call with Chief Executive Elon Musk, slated for around 5:30 p.m. U.S. Eastern Time.

1. Profit margins: cars and related software

First and foremost, investors are going to scour Tesla's March-quarter earnings report for details of the amount of profit it managed to extract from each electric car, and each autonomous driving software package, it sells.

Tesla's profit margins, probably the most closely tracked metric by analysts on Wall Street, narrowed to 17.6% over the three months ended in December, down from a 23.8% margin over the year-earlier period.

Gross-profit margins, based on Refinitiv forecasts, are likely to narrow further, to around 17.2% over the three months ended in March, with estimates ranging between 14.7% and 20%.

"Tesla will likely miss amid softening sales and margins (big delivery miss), and the company risks no growth in volume in 2024 with further pressure on margins," said Nancy Tengler, CEO at Laffer Tengler Investments in Scottsdale, Ariz. "But Musk has shown his ability and willingness to make hard decisions and do what’s necessary to dig himself out of a hole. No matter the cost."

2. Delivery forecasts: pressure from China figures

Tesla handed over 387,000 new cars to customers in the first quarter, a 20% decline from the record 484,000 it notched over the final months of 2023 and the biggest miss to estimates since Wall Street began compiling data in the mid-2010s.

Weaker-than-expected sales figures from China, where last month's volumes fell to the lowest levels in more than a year, are also adding to pressure on the market's aggressive full-year delivery targets for Tesla.

Related: Tesla stock slumps after startling China decision

Tesla told investors in February that full-year delivery volumes would be "notably lower" than the 1.8 million tally from 2023, but it declined to provide a firm target.

Wall Street analysts have pared their own forecasts, but they'll be on high alert for any changes to either the group's 2024 estimate or a hard target from Musk following its challenging opening quarter.

3. Low-cost Model 2 plans: Whether and when

Investors and analysts have been waiting for a detailed update on Tesla's plans to produce a low-cost EV that can both challenge the group's China-based rivals and cement its position as the world's leading carmaker in the space.

However, earlier this month, Reuters reported that the Model 2 project had been canceled in favor of a focus on robotaxi production, which will leverage the group's push into artificial-intelligence-enhanced autonomous-driving software.

Related: Analysts take aim at Tesla stock after Elon Musk makes unpopular decision

Musk called the report "lies" but didn't address its specifics. That left analysts to wonder whether he was planning to pivot away from his "master plan" to provide a low-cost EV and instead focus on what he now calls a "blindingly obvious" strategy of extending the group's leadership in Full-Self-Driving.

Deutsche Bank analyst Emmanuel Rosner last week said that even a delayed Model 2 launch would "make the future of the company tied to Tesla cracking the code on full driverless autonomy, which represents a significant technological, regulatory and operational challenge." Rosner lowered his rating on Tesla to hold from buy and slashed his price target by $66 to $123 a share.

4. New autonomy focus: financial-metric overhaul

Any indication that Tesla is moving from an EV manufacturing focus to a strategy powered by self-driving technologies would trigger a massive overhaul in sales and profit metrics for the group, which has been one of the most compelling U.S. corporate growth stories of the past 10 years.

Musk has said that in order to effectively lead the group, he needs to gain 25% control of Tesla, a level that's tied to a $55.8 billion pay package to which the company agreed in 2018. But that package was rejected as an “an unfathomable sum” by Delaware Chancery Judge Kathaleen McCormick last year.

Tesla is appealing the ruling, and lobbying for shareholder support, but Musk has said he'll pursue his AI and robotics ambitions outside the Tesla structure if he isn't able to secure the 25% threshold.

Related: Analyst overhauls Tesla price target amid major strategy shift

That could leave investors to wonder whether he's fully committed to the EV maker as it's currently constructed, or whether he might take some of his higher-margin ideas — such as licensing Full Self-Driving software to other carmakers — into a different entity.

"The AI story, autonomous, FSD, Optimus, robots is another major value to the Tesla story, but it's all behind closed doors," said Wedbush analyst Dan Ives. Wall Street "needs to understand the road map, monetization, and overall strategy for the AI story at Tesla, which right now is getting no credit for its AI endeavors."

5. Stopping the stock slide

Ultimately, Musk's biggest challenge on the conference call today, and in the weeks that follow, will be convincing investors that the stock's year-to-date collapse, which has lopped nearly $350 billion from its market value, is coming to an end.

The stock is also suffering the second-longest drawdown of its share price since it went public in 2010. The slump has carved more than $760 billion from its market value since the November 2021 peak.

Shorting Tesla shares has been a hugely profitable trade this year, with data from S3 Partners suggesting investors who have bet against Tesla are sitting on profits of $8.3 billion, with around 4.2% of the stock's float outstanding still sold short.

More Tesla:

- Cathie Wood buys $22 million of battered tech stock

- Analyst revises Tesla stock price target after robotaxi news

- Top analyst reveals new Tesla price target ahead of Q1 earnings

Unveiling a massive round of corporate layoffs, probably around 10%, or 1,400, of the company's global staff, has failed to stop the stock's rot. And to some degree it has added to concern that Tesla is facing a pivotal moment in its hypergrowth history.

Musk himself told investors earlier this year that Tesla is "currently between two major growth waves," with "Full-Self-Driving, next-gen vehicle and energy storage" powering the group's next advance.

He'll need to define that vision sharply if he's going to bring investors back on board.

"This is a fork-in-the-road time to get Tesla through this turbulent period; otherwise dark days could be ahead," said Ives of Wedbush. "With the ongoing debacle around margins and demand, Musk will need to quickly take the reins back in to regain confidence in the eyes of the Street."

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic chinaInternational

World’s Biggest M&A Deal Is Terrible For Bonds

World’s Biggest M&A Deal Is Terrible For Bonds

Four years ago, we wrote an article, mocking the unspeakable reality that it appeared "The…

Share this:

Four years ago, we wrote an article, mocking the unspeakable reality that it appeared "The Fed and The Treasury had now merged"...

Last week, that reality dawned on one of Wall Street's best and brightest as BofA Chief Investment Strategist Michael Hartnett headlined his latest note with a 'zeitgeist' quote that sounded awfully familiar:

"Biggest piece of M&A in past 12 months was the merger of Treasury & Fed.”

And this morning, Bloomberg macro strategist Simon White takes up the story below, noting that monetary and fiscal policy in the US is becoming more intertwined as the Federal Reserve and the Treasury - implicitly or otherwise - increasingly coordinate their actions.

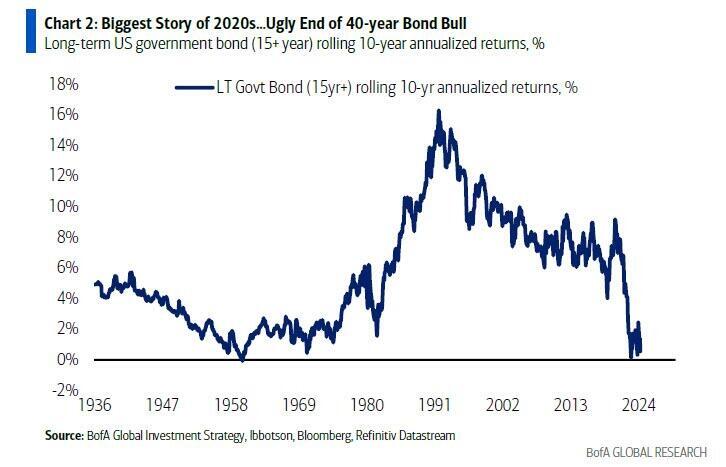

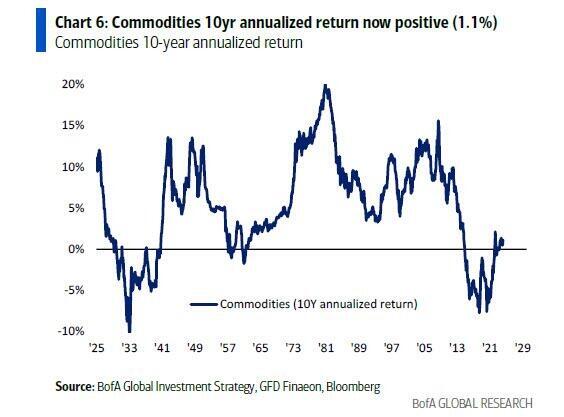

That’s a structural negative for US Treasuries, and signals an end to the long underperformance of commodities and other real assets.

Reflecting on the quote above Michael Hartnett of BofA - describing the greater coordination of fiscal and monetary policy in the US and the winnowing away of the Fed’s independence from the Treasury - White agrees that, viewed as an M&A deal, it’s certainly massive, given the Fed’s $7 trillion balance sheet and the government’s $34 trillion of debt.

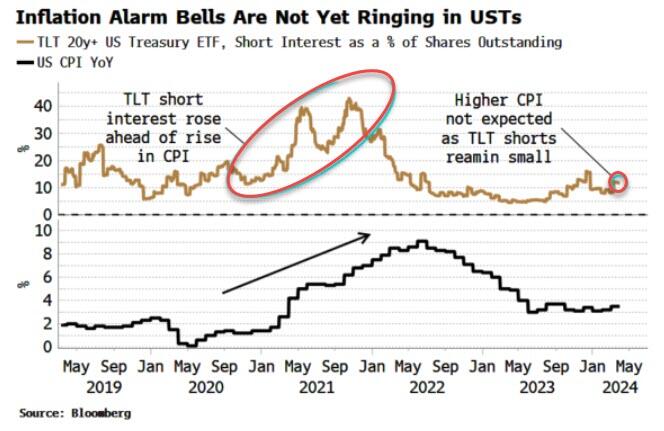

More importantly, it’s hazardous for Treasuries as it tilts the risks for persistently higher inflation firmly to the upside, even though the market continues to be under-appreciative of the ever-more malign landscape. Positioning in USTs has fallen this year, but it is still likely to be net long, while outright shorts remain near survey lows, corroborated by the muted short interest in Treasury ETFs such as the TLT.

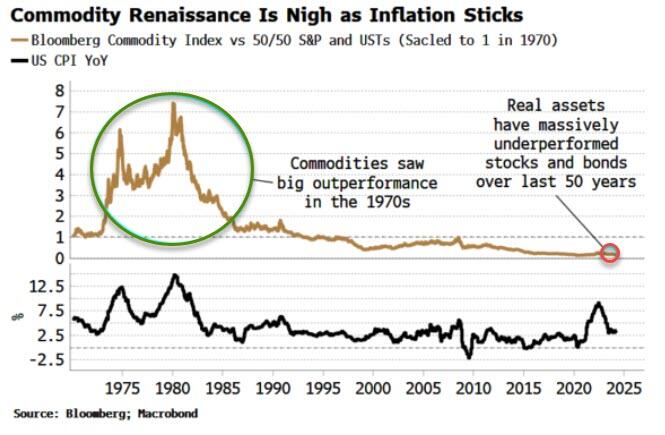

At the same time as entrenched inflation is bad for fixed income, it’s also very positive for real assets such as commodities. They have relentlessly underperformed financial assets - stocks and bonds - over the last four decades.

Governments are inherently inflationary. Wealth is very unevenly distributed, with many dollars held in only a few hands. But every person has exactly one vote. Thus there is an incentive for governments to take wealth from the rich — where it is mainly saved — and redistribute it to the less well-off, where it is more likely to be spent.

The sort of spending governments engage in in the run-up to elections is likely to be discretionary and debt-funded — which government wants to raise taxes ahead of a vote? Mandatory spending, such as entitlement programs and defense, is likely to see its biggest boost when the economy is in a slump. Increases in discretionary spending, on the other hand, more often than not happen when the economy is growing, and therefore are more likely to fan inflation.

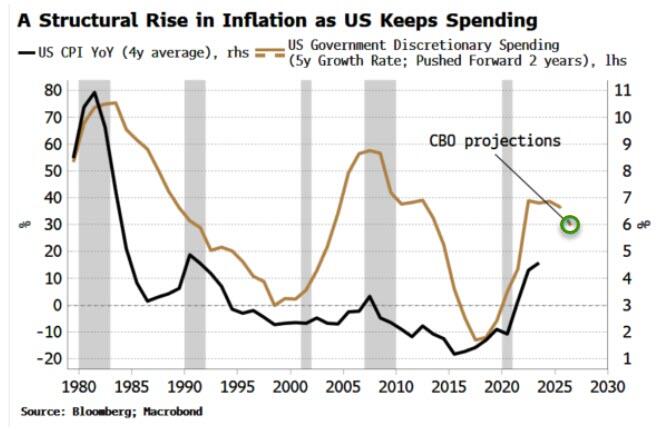

Discretionary spending in the US had already started to grow before the pandemic, and its five-year growth rate has leveled off at an elevated level and not yet fallen. As the chart below shows, longer-term rises in discretionary spending precede structural rises in inflation. Today’s spending is the largest ever seen in the US outside of war or recession.

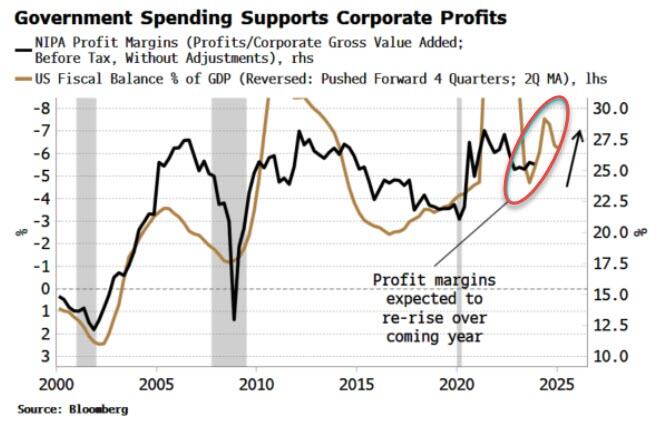

How is government spending stoking inflation in this cycle? Mainly through supporting corporate profits. Deeper fiscal deficits lead to higher profits and profit margins (see chart below), as net spending in one sector must lead to net saving in the others, with the corporate sector the main beneficiary as government deficits support spending in the household sector.

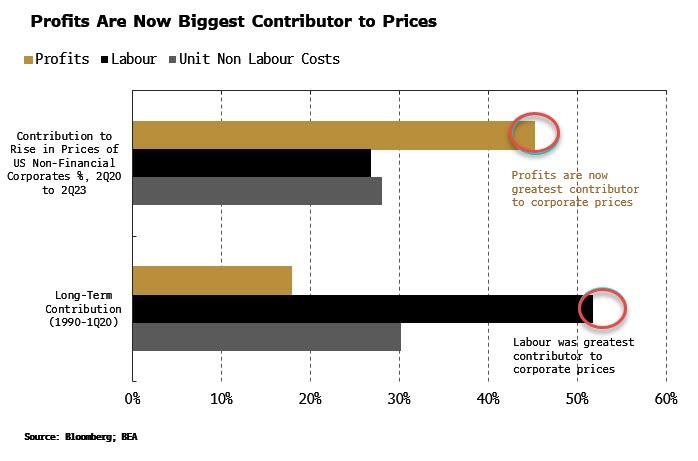

This is a marked change from the 1970s when wages directly drove prices higher. With much less trade-union membership and weakened union power, that’s less of a risk today.

But profits are lining up to be the main vector of persistent and elevated inflation in this cycle. The unique conditions of the pandemic allowed firms to raise profit margins almost as fast as they ever have done. A profit-price-wage spiral is a greater likelihood, and could already be underway.

The risk is that an increase in margins leads to higher prices and then to higher wages. Margins are increased again, but to a greater level than before, to maintain profits in real terms as prices have risen since the last increase.

Economy-wide margins are off their recent highs, but are still significantly elevated compared to their pre-pandemic levels. Labor costs in the decades running up until 2020 made up the bulk of corporate prices, accounting for over half of them on average. But that relationship has inverted since the pandemic, with profits now making up 45% of selling prices, versus under 30% for the cost of labor. Profits now drive prices.

Elevated government deficits can keep the carousel going by supporting spending. The CBO projects discretionary outlay’s five-year growth rate should fall back toward 10% in the next few years from over 35% now. But that’s smoking hopium. The expectations electorates have from their governments markedly rose in the pandemic, with the sovereign expected to underwrite an ever widening basket of risks. The “fiscal put” is becoming embedded and the longer spending keeps rising to pay for it, the harder it will be to reverse.

Government borrowing to fund discretionary spending is a highly inflationary mix on its own, but the addition of a compliant central bank fans the flames further. Notionally the Fed is still independent, but in actuality its maneuverability is increasingly circumscribed for three reasons:

-

the large amount of Treasuries outstanding and the rising interest payable on them;

-

the ungainly size of the Treasury’s account at the Fed;

-

and the increasing proportion of short-term bills, i.e. short-term liabilities that are very money-like.

History is replete with examples of large government deficits monetized by central banks preceding high or hyper-inflation, from China in the late 1940s, to Greece in the early 40s and to Zimbabwe early in this century. That’s not to say we should expect the US to see price growth hit such stupefying levels, but to underscore that spendthrift governments and subservient central banks is a terrible combination for price stability.

Treasuries are unlikely to thrive in this environment.

Nothing moves in a straight line, but the net path for yields is likely to be higher in the coming months and years. Embedded inflation is also likely to drive increasing demand for real assets such as property and commodities, ending their decades of underperformance.

Inflation is one of the most regressive of taxes, as well as being one of the hardest to lower. Almost everyone loses when it is elevated. Even though M&A deals are meant to be value creating, this one is likely to be precisely the opposite.

Spread & Containment

US PMIs Scream Stagflation As Manufacturing ‘Contracts’, Prices Rise, Heaviest Job Cuts Since GFC

US PMIs Scream Stagflation As Manufacturing ‘Contracts’, Prices Rise, Heaviest Job Cuts Since GFC

After a mixed bag from preliminary April…

Share this:

After a mixed bag from preliminary April European PMIs (Services strong-er, Manufacturing weaker-er, surging prices)...

“Accelerated increases in input costs, likely driven not only by higher oil prices but also, more concerningly, by higher wages, are a cause for scrutiny Concurrently service-sector companies have raised their prices at a faster rate than in March, fueling expectations that services inflation will persist. ”

and after March US PMIs exposed the end of the disinflation narrative...

"Most notable was an especially steep rise in prices charged for consumer goods, which rose at a pace not seen for 16 months, underscoring the likely bumpy path in bringing inflation down to the Fed's 2% target. ”

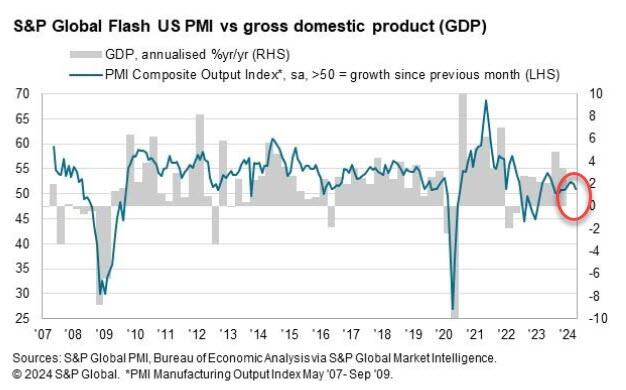

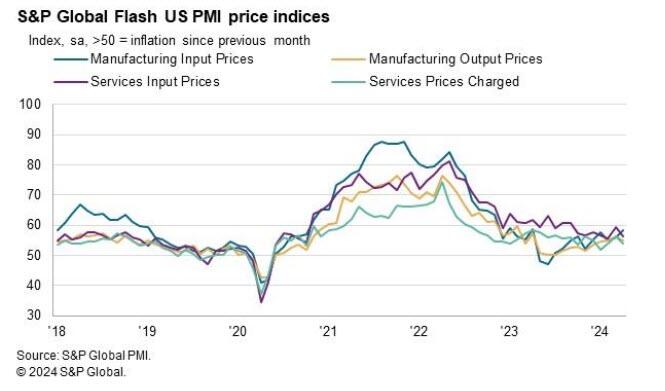

...S&P Global's preliminary US f°r April just dropped and they were ugly with both Manufacturing and Services disappointingly dropping further as the former dropped back into contraction:

-

• Flash US Services Business Activity Index at 50.9 (Exp: 52.0; March: 51.7) - 5-month low.

-

• Flash US Manufacturing PMI at 49.9 (Exp 52.0; March: 51.9) - 4-month low.

Source: Bloomberg

Commenting on the data, Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“The US economic upturn lost momentum at the start of the second quarter, with the flash PMI survey respondents reporting below-trend business activity growth in April. Further pace may be lost in the coming months, as April saw inflows of new business fall for the first time in six months and firms’ future output expectations slipped to a five-month low amid heightened concern about the outlook.

“The more challenging business environment prompted companies to cut payroll numbers at a rate not seen since the global financial crisis if the early pandemic lockdown months are excluded.

After March showed accelerating prices, flash April data confirmed the trend

“Notably, the drivers of inflation have changed.

"Manufacturing has now registered the steeper rate of price increases in three of the past four months, with factory cost pressures intensifying in April amid higher raw material and fuel prices, contrasting with the wagerelated services-led price pressures seen throughout much of 2023.”

So slower growth and much faster inflation - that does not sound like a recipe for rate-cuts... in fact quite the opposite.

International

Nike CEO blames oddly specific problem for brand issues

The footwear and apparel company has been losing ground to its competitors.

Share this:

{kind=link}

Blink and you might miss an important trend when it comes to the fashion industry.

Thanks to the rapid integration of social media by virtually all fashion brands – and the breakneck pace at which fans of fashion use social media – trends or movements can come and go in the blink of an eye.

Related: Some Walmarts make surprising self-checkout change

Whether its brands being showcased on Snapchat during New York Fashion Week, the metaverse hosting its very own fashion week, or influencers showing off their latest styles on TikTok, it can be tough to keep up.

This is especially the case with footwear. As athletes influencers build their own brands (and social media presence), it's important for them to stay on top of what's considered cool to wear, and what may be a little outdated. In fact, it's kind of a part of their jobs.

Currently, what's old is cool again. Vintage footwear styles like Adidas' Sambas and Campus sneakers are everywhere from the high streets of London to college campuses in the United States. So-called dad shoes – specifically New Balance's highly popular Unisex 530 sneakers – are almost always sold out in stores and online.

So establishing a foothold for Nike (NKE) , which has historically specialized in sleek silhouettes and bright colors, has been tough when neutral and chunky styles are now popular.

As a result, Nike has been struggling to gain back the enthusiasm its brand once enjoyed so steadily during the earlier 2000s.

Nike CEO identifies a problem

Some CEOs have called out Nike, claiming "they stopped a little bit bringing in new stuff,” per JD Sports CEO Régis Schultz earlier this month, adding "shoppers get bored very quickly."

Aware that growth and imagination seem to be an issue at his company, Nike CEO John Donahue isolated one particular issue that may be to blame, claiming the problem "is fairly straightforward."

Since the onset of the pandemic, Nike adopted a remote work policy that Donahue said hurt its competitive edge.

“But even more importantly, our employees were working from home for two and a half years,” Donahoe said in an interview with CNBC. “And in hindsight, it turns out, it’s really hard to do bold, disruptive innovation, to develop a boldly disruptive shoe, on Zoom.”

Eager to right the ship, however, Donahue says the company has been working on a “bold, disruptive” plan to churn out new products and hopefully reinvigorate excitement for the brand.

“So we realigned our company, and over the last year we have been ruthlessly focused on rebuilding our disruptive innovation pipeline along with our iterative innovation pipeline,” he said. “So the pipeline is as strong as ever.”

Nike plans a comeback

Nike stock is down 11% year-to-date, and in December the sneaker maker slashed its revenue outlook for the forthcoming fiscal year, citing weaker digital demand in the U.S. and stronger headwinds in its key Europe-Mideast-Asia region.

It also announced a $2 billion cost-cutting plan. In February, Nike laid off 2% of its employees. It has also been working to streamline and simplify some of its lines.

But the sneaker maker is planning a comeback in 2024.

It plans to make the upcoming 2024 Paris Summer Olympics an exhibition for some of its refreshed product lines, specifically in the track and field category.

“We’ve done more to advance running than any brand in the world over the last 50 years and we continue to lead with elite runners,” Donahoe added. “Innovation has always been what’s marked Nike in running, as in other categories, and so we’re not just going to copy what other people do.”

hong kong europe pandemic

Parrot fever cases amid a ‘mysterious’ pneumonia outbreak in Argentina – what you need to know about psittacosis

The Intel Agencies Of Government Are Fully Weaponized

Weekly Market Pulse: Situation Normal

US-Funded Experiments In China Could Secretly Manipulate Viruses: Email

World’s Biggest M&A Deal Is Terrible For Bonds

How Debt-to-GDP Ratios Have Changed Around The World Since 2000

How Debt-to-GDP Ratios Have Changed Around The World Since 2000

Delta Air Lines makes a baggage change that travelers will like

The language of insolvency: why getting it wrong can harm struggling firms

Nike CEO blames oddly specific problem for brand issues

-

International1 month ago

International1 month agoParexel CEO to retire; CAR-T maker AffyImmune promotes business leader to chief executive

-

Government2 weeks ago

Government2 weeks agoClimate-Con & The Media-Censorship Complex – Part 1

-

International4 days ago

International4 days agoJ&J’s AI head jumps to Recursion; Doug Williams resigns as Sana’s R&D chief

-

International1 week ago

International1 week agoWHO Official Admits Vaccine Passports May Have Been A Scam

-

Spread & Containment2 weeks ago

Spread & Containment2 weeks agoFDA Finally Takes Down Ivermectin Posts After Settlement

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoVaccinated People Show Long COVID-Like Symptoms With Detectable Spike Proteins: Preprint Study

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCan language models read the genome? This one decoded mRNA to make better vaccines.

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoWhat’s So Great About The Great Reset, Great Taking, Great Replacement, Great Deflation, & Next Great Depression?