Uncategorized

Sun Life Reports Third Quarter 2022 Results

Sun Life Reports Third Quarter 2022 Results

PR Newswire

TORONTO, Nov. 2, 2022

Sun Life Financial Inc. (“SLF Inc.”), its subsidiaries and, where applicable, its joint ventures and associates are collectively referred to as “the Company”, “Sun Life”…

Share this:

Sun Life Reports Third Quarter 2022 Results

PR Newswire

TORONTO, Nov. 2, 2022

Sun Life Financial Inc. ("SLF Inc."), its subsidiaries and, where applicable, its joint ventures and associates are collectively referred to as "the Company", "Sun Life", "we", "our", and "us". We manage our operations and report our financial results in five business segments: Canada, United States ("U.S."), Asset Management, Asia, and Corporate. The information in this document is based on the unaudited interim financial results of SLF Inc. for the period ended September 30, 2022 and should be read in conjunction with the interim management's discussion and analysis ("MD&A") and our unaudited interim consolidated financial statements and accompanying notes ("Interim Consolidated Financial Statements") for the period ended September 30, 2022, prepared in accordance with International Financial Reporting Standards ("IFRS"). We report certain financial information using non-IFRS financial measures. For more details, refer to the Non-IFRS Financial Measures section in this document. Additional information relating to SLF Inc. is available on www.sunlife.com under Investors – Financial results and reports, on the SEDAR website at www.sedar.com, and on the U.S. Securities and Exchange Commission's website at www.sec.gov. Reported net income (loss) refers to Common shareholders' net income (loss) determined in accordance with IFRS. Unless otherwise noted, all amounts are in Canadian dollars. |

TORONTO, Nov. 2, 2022 /PRNewswire/ - Sun Life Financial Inc. (TSX: SLF) (NYSE: SLF) announced its results for the third quarter ended September 30, 2022.

- Q3'22 reported net income of $466 million decreased 54% and underlying net income(1) of $949 million increased 5% from Q3'21.

- Q3'22 reported EPS(2) was $0.80 and underlying EPS(1)(2) was $1.62.

- Q3'22 reported ROE(1) was 7.6% and underlying ROE(1) was 15.5%.

- Increase common share dividend from $0.69 to $0.72 per share.

"Sun Life delivered strong third quarter results, continuing to reflect the strength of our diversified business mix, in a challenging economic environment," said Kevin Strain, President and CEO of Sun Life. "Sun Life U.S. benefited from the first full quarter of contribution from DentaQuest. Overall insurance sales across our businesses were strong, reflecting the increased importance Clients are placing on protection and health. In our Asset Management business, we announced our intention to acquire a majority stake in Advisors Asset Management, Inc., a leading independent U.S. high-net-worth retail distribution firm, and announced a strategic partnership with Phoenix Group for both MFS and SLC Management in conjunction with the intended sale of our UK business. These transactions provide attractive opportunities for continued growth in our Asset Management pillar."

Quarterly results | Year-to-date | ||||

Profitability | Q3'22 | Q3'21 | 2022 | 2021 | |

Reported net income - Common shareholders ($ millions) | 466 | 1,019 | 2,109 | 2,856 | |

Underlying net income ($ millions)(1) | 949 | 902 | 2,684 | 2,635 | |

Reported EPS ($)(2) | 0.80 | 1.74 | 3.59 | 4.85 | |

Underlying EPS ($)(1)(2) | 1.62 | 1.54 | 4.58 | 4.50 | |

Reported return on equity ("ROE")(1) | 7.6 % | 17.6 % | 11.7 % | 16.7 % | |

Underlying ROE(1) | 15.5 % | 15.6 % | 14.9 % | 15.4 % | |

Growth | Q3'22 | Q3'21 | 2022 | 2021 | |

Insurance sales ($ millions)(1) | 943 | 628 | 2,478 | 2,068 | |

Wealth sales and asset management gross flows ($ millions)(1) | 43,096 | 50,725 | 158,359 | 171,700 | |

Value of new business ("VNB") ($ millions)(1) | 256 | 290 | 785 | 852 | |

Assets under management ("AUM") ($ billions)(1)(3) | 1,275 | 1,386 | |||

Financial Strength | Q3'22 | Q3'21 | |||

LICAT ratios (at period end)(4) | |||||

Sun Life Financial Inc. | 129 % | 143 % | |||

Sun Life Assurance(5) | 123 % | 124 % | |||

Financial leverage ratio (at period end)(1) | 26.4 % | 22.2 % | |||

_________________ | |

(1) | Represents a non-IFRS financial measure. For more details, see the Non-IFRS Financial Measures section in this document and in our MD&A for the period ended September 30, 2022 ("Q3'22 MD&A"). |

(2) | All earnings per share ("EPS") measures refer to fully diluted EPS, unless otherwise stated. |

(3) | AUM is comprised of General Funds and Segregated Funds on our Statements of Financial Position, and other third-party assets managed by the Company ("other AUM"). For more details, see the Non-IFRS Financial Measures section in this document and in our Q3'22 MD&A. |

(4) | For further information on the Life Insurance Capital Adequacy Test ("LICAT"), see section E - Financial Strength in our Q3'22 MD&A. Our LICAT ratios are calculated in accordance with OSFI-mandated guideline, Life Insurance Capital Adequacy Test. |

(5) | Sun Life Assurance Company of Canada ("Sun Life Assurance") is SLF Inc.'s principal operating life insurance subsidiary. |

Financial and Operational Highlights - Quarterly Comparison (Q3 2022 vs. Q3 2021)

Our strategy is focused on key business segments, where we aim to be a leader in the markets in which we operate.

($ millions, unless otherwise noted) | ||||||||||||

Reported net income (loss) - | Underlying net income (loss)(1) | Insurance sales(1) | Wealth sales and asset | |||||||||

Q3'22 | Q3'21 | change | Q3'22 | Q3'21 | change | Q3'22 | Q3'21 | change | Q3'22 | Q3'21 | change | |

Canada | 210 | 393 | (47) % | 300 | 290 | 3 % | 233 | 182 | 28 % | 4,131 | 5,918 | (30) % |

U.S. | 94 | 46 | 104 % | 216 | 110 | 96 % | 366 | 199 | 84 % | — | — | — |

Asset Management | 215 | 301 | (29) % | 295 | 362 | (19) % | — | — | — | 36,434 | 40,682 | (10) % |

Asia | 125 | 288 | (57) % | 175 | 145 | 21 % | 344 | 247 | 39 % | 2,531 | 4,125 | (39) % |

Corporate | (178) | (9) | nm(2) | (37) | (5) | nm(2) | — | — | — | — | — | — |

Total | 466 | 1,019 | (54) % | 949 | 902 | 5 % | 943 | 628 | 50 % | 43,096 | 50,725 | (15) % |

(1) | Represents a non-IFRS financial measure. See the Non-IFRS Financial Measures section in this document and in the Q3'22 MD&A. |

(2) | Not meaningful. |

Reported net income of $466 million decreased $553 million or 54% from prior year, primarily reflecting unfavourable market-related impacts, a $170 million charge related to the sale of Sun Life UK(1), less favourable ACMA(2) impacts, and an increase in SLC Management's acquisition-related liabilities(3), partially offset by fair value changes on MFS'(4) share-based payment awards. Underlying net income of $949 million(5) increased $47 million or 5%, driven by business growth and experience in protection and health including a strong contribution from the DentaQuest acquisition. This was partially offset by lower fee-based income in wealth and asset management, mainly driven by declines in global equity markets.

Canada: A leader in insurance and asset management

Canada reported net income of $210 million decreased $183 million or 47% from prior year, mainly reflecting market-related impacts, due to interest rate movements and lower equity markets. Prior year reported net income also included increases in the value of real estate investments, partially offset by a par allocation adjustment(6). Underlying net income of $300 million increased $10 million or 3% from prior year, primarily driven by higher investment gains, partially offset by a higher effective tax rate. Growth in protection and health was mostly offset by lower wealth results mainly driven by declines in equity markets.

Canada insurance sales were $233 million, up 28% year-over-year, driven by large case group benefits sales in Sun Life Health and higher individual participating whole life insurance sales. Canada wealth sales were $4 billion, down 30%, reflecting lower defined contribution(7) and defined benefit solutions sales in Group Retirement Services ("GRS"), and lower individual wealth sales.

We continue to focus on helping our Clients achieve lifetime financial security and live healthier lives. In 2022, over 45,000 financial roadmaps were created using our Sun Life One Plan digital tool, contributing to our ambition for all Canadians to have a financial plan. This quarter, we also enhanced our tools with a digital navigation portal, making it easier for Clients to track progress and build flexible scenarios into financial plans. We also continue to focus on making it easier for Clients to do business with us. This quarter, we introduced a new Voluntary Benefit eApp which consolidates our voluntary benefit products into a single resource, reducing the application process time for Clients by up to 50%.

U.S.: A leader in health and benefits

U.S. reported net income of $94 million increased $48 million from prior year, driven by an increase in underlying net income, partially offset by market-related impacts and DentaQuest integration costs. Underlying net income of $216 million increased $106 million, driven by growth across all businesses, the contribution from the DentaQuest acquisition and favourable experience-related items. Experience in the quarter included favourable medical stop-loss margins and investment gains. Mortality experience in Group Benefits also improved significantly compared to prior year due to lower COVID-19-related claims.

Foreign exchange translation led to an increase of $4 million and $8 million in reported net income and underlying net income, respectively.

U.S. insurance sales were $366 million, up 84% year-over-year, driven by higher dental(8) and employee benefits sales.

________________ | |

(1) | On August 4, 2022, we entered into an agreement to sell SLF of Canada UK Limited ("Sun Life UK") to Phoenix Group Holdings plc ("Phoenix Group"). In Q3'22, we recognized an impairment charge of $170 million (£108 million) pertaining to the attributed goodwill that is not expected to be recovered through the sale ("sale of Sun Life UK"). For more details, see section E - Financial Strength in the Q3'22 MD&A. |

(2) | Assumption changes and management actions ("ACMA"). |

(3) | Reflects the changes in estimated future payments for acquisition-related contingent considerations and options to purchase remaining ownership interests of SLC Management affiliates. |

(4) | MFS Investment Management ("MFS"). |

(5) | Refer to section C - Profitability in the Q3'22 MD&A for more information about experience-related items and the Non-IFRS Financial Measures section in this document for a reconciliation between reported net income and underlying net income. |

(6) | An adjustment of investment income and expense allocations between participating policyholders and shareholders for prior years recorded in Q3'21 ("par allocation adjustment"). |

(7) | Defined contribution sales include retained business sales. |

(8) | Dental sales include sales from DentaQuest, acquired on June 1, 2022. |

As a leader in health and benefits, we are helping Clients get the right care at the right time. In Q3, we established a new partnership with AbleTo, a virtual behavioural health therapy and coaching program. Sun Life U.S. is the only disability carrier directly partnering with AbleTo, offering convenient mental health services supporting our disability and critical illness members with a cancer diagnosis.

In addition, DentaQuest announced a new program with Partners Health Plan, a non-profit managed care organization serving individuals with intellectual and other developmental disabilities. This partnership will increase access to oral health care and help improve outcomes for this underserved community, contributing to our goal of increasing health equity for all.

Asset Management: A global leader in both public and alternative asset classes through MFS and SLC Management

Asset Management reported net income of $215 million decreased $86 million or 29% from prior year, driven by an increase in SLC Management's acquisition-related liabilities(1) and a decline in underlying net income, partially offset by fair value changes on MFS' share-based payment awards. Underlying net income of $295 million decreased $67 million or 19%, due to lower results in MFS, largely reflecting declines in global equity markets, as well as in SLC Management, due to investment gains in the prior year and continued investments in the businesses.

Foreign exchange translation led to an increase of $10 million in both reported net income and underlying net income.

Asset Management ended Q3'22 with $912 billion in AUM, consisting of $703 billion (US$509 billion) in MFS and $208 billion in SLC Management. Total Asset Management net outflows of $7.7 billion in Q3'22 reflected MFS net outflows of approximately $13.4 billion (US$10.3 billion), partially offset by SLC Management net inflows of approximately $5.7 billion.

In the third quarter of 2022, 97%, 94% and 47% of MFS' U.S. retail mutual fund assets ranked in the top half of their Morningstar categories based on ten-, five- and three-year performance, respectively. The MFS pre-tax net operating profit margin(2) was 41% for Q3'22, compared to 42% in the prior year.

In August, we entered into an agreement with Phoenix Group Holdings plc ("Phoenix Group"), establishing a long-term strategic asset management partnership through MFS and SLC Management, in conjunction with the sale of our Sun Life UK(3) business. Phoenix Group is the UK's largest long-term savings and retirement business, with £270 billion(4) of assets under administration and approximately 13 million customers. Phoenix Group has set a goal to invest approximately US$25 billion in North American public and private fixed income and alternative investments over the next five years and Sun Life will be a material partner to Phoenix Group in achieving this goal.

In September, we announced our intention to acquire a 51%(5) interest in Advisors Asset Management Inc. ("AAM"), a leading independent retail distribution firm in the U.S., with the option to acquire the remaining interest starting in 2028. AAM will provide access to U.S. retail distribution for SLC Management. This will allow SLC Management to meet the growing demand for alternative assets among U.S. high-net-worth ("HNW") investors.

During the third quarter, InfraRed Capital Partners ("InfraRed") received a five-star rating in the latest Principles for Responsible Investment ("PRI") assessment(6) for the Direct – Infrastructure module. This marks the seventh consecutive assessment where InfraRed has achieved the highest possible PRI rating for this module, demonstrating the integration of ESG throughout its investment practices. InfraRed also received a five-star rating for Investment and Stewardship Policy module, which was also above the median score.

Sun Life is continuing progress on its climate commitments with a focus on setting interim targets towards net zero greenhouse gas ("GHG") emissions by 2050. MFS has set an interim target to commit 90% of in-scope assets(7) to be managed in-line with net zero carbon emissions by 2030. We expect our other asset management businesses that are members of the Net Zero Asset Managers ("NZAM") initiative to communicate their targets following finalization with NZAM. For Sun Life's General Account investments, we intend to publish interim targets as part of our 2022 sustainability reporting, to be published in March 2023. Sun Life has also set an interim target of a 50% absolute reduction in GHG emissions by 2030 relative to a 2019 baseline for its operations.

Asia: A regional leader focused on fast-growing markets

Asia reported net income of $125 million decreased $163 million or 57% from prior year, reflecting favourable ACMA impacts in the prior year. Underlying net income of $175 million increased $30 million or 21%, driven by improved mortality reflecting lower COVID-19-related claims, and higher investment gains and contributions from our joint ventures, partially offset by lower fee-based income mainly driven by equity market declines.

Foreign exchange translation led to a $4 million decline in both reported net income and underlying net income.

Asia insurance sales were $344 million, up 39% year-over-year, driven by sales growth across all markets. Asia wealth sales were $3 billion, down 39%, reflecting lower sales in India, the Philippines and Hong Kong.

_________________ | |

(1) | Reflects the changes in estimated future payments for acquisition-related contingent considerations and options to purchase remaining ownership interests of SLC Management affiliates. |

(2) | Represents a non-IFRS financial measure. For more details, see the Non-IFRS Financial Measures section in this document and in the Q3'22 MD&A. |

(3) | SLF of Canada UK Limited. |

(4) | As at June 30, 2022. |

(5) | On a fully diluted basis. |

(6) | InfraRed PRI Transparency and Assessment Reports are available at https://www.ircp.com/sustainability#documents. |

(7) | In-scope assets comprise approximately 92% of MFS's global AUM. |

We are committed to helping our Clients achieve lifetime financial security by offering products that fulfill their needs. In Hong Kong, we have seen strong Client reception for Stellar, the first ESG-focused savings plan(1) in the market that actively integrates environmental, social and governance ("ESG") concepts into investment strategies. Following this success, we enhanced our suite of Stellar offerings to include additional cost-effective, flexible options that allow for broader Client access to sustainable long-term savings products.

We also continue to enhance our product offerings for HNW Clients to diversify, protect, and grow their assets. This quarter, we launched Sun Global Aurora, a savings-oriented indexed universal life product. Sun Global Aurora is a cost-effective alternative to our core product, providing Clients the flexibility to customize premium payments to meet their wealth accumulation goals, while offering stable returns and exposure to equity markets.

Corporate

Corporate reported net loss was $178 million, compared to a net loss of $9 million in the prior year, reflecting a $170 million charge related to the sale of Sun Life UK, partially offset by favourable ACMA impacts. Underlying net loss was $37 million, compared to a net loss of $5 million in the prior year, reflecting a higher effective tax rate and lower available-for-sale ("AFS") gains.

IFRS 17 Insurance Contracts ("IFRS 17") and IFRS 9 Financial Instruments ("IFRS 9") to be Adopted in 2023

For periods beginning on or after January 1, 2023, we will be adopting IFRS 17, which replaces IFRS 4 Insurance Contracts. IFRS 17 establishes the principles for the recognition, measurement, presentation, and disclosure of insurance contracts. Effective January 1, 2023, we will also be adopting IFRS 9, which replaces IAS 39 Financial Instruments: Recognition and Measurement.

The adoption of IFRS 17 and IFRS 9 has no material implication on our business strategies. However, upon transition at January 1, 2022, the changes in measurement of insurance contract liabilities and timing of recognition of earnings would have resulted in the following impacts:

- A net transfer of approximately $4.5 billion from shareholders' equity, primarily driven by the establishment of the contractual service margin ("CSM") on the balance sheet, among other items.

- A mid-single digit decrease in our 2022 underlying net income as we restate the comparative year on an IFRS 17 basis.

The CSM balance will qualify as Tier 1 available capital. On July 21, 2022, OSFI finalized the LICAT guidelines to reflect the IFRS 17 adoption, effective January 1, 2023. We expect our LICAT ratio to improve on adoption and we also expect capital generation and capital volatility to be relatively unchanged under the new regime.

Our medium-term financial objectives following the adoption of IFRS 17 and 9 will be:

- Underlying EPS growth: 8-10%

- Underlying ROE: 18%+ (an increase from 16%+ prior to transition)

- Underlying Dividend payout ratio: 40-50%

We continue to assess the impact that the adoption of IFRS 17 and IFRS 9 will have on our Consolidated Financial Statements and estimates of the financial impacts are subject to change. For additional details, refer to Note 2 in the Interim Consolidated Financial Statements for the period ended September 30, 2022.

___________ | |

(1) | This is based on market conditions as of April 12, 2022 and comparison among other savings plans for new Composite and Long Term Businesses as defined by the Insurance Authority in the Register of Authorized Insurers. |

Earnings Conference Call

The Company's Q3'22 financial results will be reviewed at a conference call on Thursday, November 3, 2022, at 10:00 a.m. ET. Visit www.sunlife.com/QuarterlyReports 10 minutes prior to the start of the event to access the call through either the webcast or conference call options. Individuals participating in the call in a listen-only mode are encouraged to connect via our webcast. Following the call, the webcast and presentation will be archived and made available on the Company's website, www.sunlife.com, until the Q3 2023 period end.

Media Relations Contact: | Investor Relations Contact: |

Krista Wilson | Yaniv Bitton |

Director, Corporate Communications | Vice-President, Head of Investor Relations and Capital Markets |

Tel: 226-751-2391 | Tel: 416-979-6496 |

Non-IFRS Financial Measures | ||

We report certain financial information using non-IFRS financial measures, as we believe that these measures provide information that is useful to investors in understanding our performance and facilitate a comparison of our quarterly and full year results from period to period. These non-IFRS financial measures do not have any standardized meaning and may not be comparable with similar measures used by other companies. For certain non-IFRS financial measures, there are no directly comparable amounts under IFRS. These non-IFRS financial measures should not be viewed in isolation from or as alternatives to measures of financial performance determined in accordance with IFRS. Additional information concerning non-IFRS financial measures and, if applicable, reconciliations to the closest IFRS measures are available in Q3 2022 MD&A under the heading M - Non-IFRS Financial Measures, in our annual MD&A under the heading L - Non-IFRS Financial Measures and the Supplementary Financial Information packages that are available on www.sunlife.com under Investors – Financial results and reports. | ||

1. Underlying Net Income and Underlying EPS | ||

Underlying net income (loss) and financial measures based on underlying net income (loss), including underlying EPS or underlying loss per share, and underlying ROE, are non-IFRS financial measures. Underlying net income (loss) removes from reported net income (loss) the impacts of the following items in our results under IFRS and when removed assist in explaining our results from period to period: | ||

(a) | market-related impacts that differ from our best estimate assumptions, which include: (i) impacts of returns in equity markets, net of hedging, for which our best estimate assumptions are approximately 2% per quarter. This also includes the impact of the basis risk inherent in our hedging program, which is the difference between the return on underlying funds of products that provide benefit guarantees and the return on the derivative assets used to hedge those benefit guarantees; (ii) the impacts of changes in interest rates in the reporting period and on the value of derivative instruments used in our hedging programs including changes in credit and swap spreads, and any changes to the assumed fixed income reinvestment rates in determining the actuarial liabilities; and (iii) the impacts of changes in the fair value of investment properties in the reporting period; | |

(b) | assumption changes and management actions, which include: (i) the impacts of revisions to the methods and assumptions used in determining our liabilities for insurance contracts and investment contracts; and (ii) the impacts on insurance contracts and investment contracts of actions taken by management in the current reporting period, referred to as management actions which include, for example, changes in the prices of in-force products, new or revised reinsurance on in-force business, and material changes to investment policies for assets supporting our liabilities; and | |

(c) | other adjustments: | |

i) | fair value adjustments on MFS' share-based payment awards that are settled with MFS' own shares and accounted for as liabilities and measured at fair value each reporting period until they are vested, exercised and repurchased - this adjustment enhances the comparability of MFS' results with publicly traded asset managers in the United States; | |

ii) | acquisition, integration and restructuring costs - this adjustment enhances comparability of our results from period to period, by removing the impacts of costs, including the unwinding of the discount for certain liabilities related to acquisitions, that are not ongoing in nature and are incurred with the intent to generate benefits in future periods; | |

iii) | certain hedges in Canada that do not qualify for hedge accounting - this adjustment enhances the comparability of our results from period to period, as it reduces volatility to the extent it will be offset over the duration of the hedges; and | |

iv) | other items that are unusual or exceptional in nature. | |

All factors discussed in this document that impact our underlying net income are also applicable to reported net income. All EPS measures in this document refer to fully diluted EPS, unless otherwise stated. As noted below, underlying EPS excludes the dilutive impacts of convertible instruments. | ||

The following table sets out the post-tax amounts that were excluded from our underlying net income (loss) and underlying EPS and provides a reconciliation to our reported net income (loss) and EPS based on IFRS. | ||

Reconciliations of Select Net Income Measures | Quarterly results | Year-to-date | ||

($ millions, unless otherwise noted) | Q3'22 | Q3'21 | 2022 | 2021 |

Reported net income - Common shareholders | 466 | 1,019 | 2,109 | 2,856 |

Market-related impacts | ||||

Equity market impacts | ||||

Impacts from equity market changes | (53) | 19 | (246) | 181 |

Basis risk impacts | 5 | 5 | 37 | 14 |

Equity market impacts | (48) | 24 | (209) | 195 |

Interest rate impacts(1) | ||||

Impacts of interest rate changes | (123) | (2) | (273) | 109 |

Impacts of credit spread movements | 6 | 4 | 66 | (14) |

Impacts of swap spread movements | 2 | — | (6) | 12 |

Interest rate impacts | (115) | 2 | (213) | 107 |

Impacts of changes in the fair value of investment properties | 3 | 145 | 148 | 169 |

Less: Market-related impacts | (160) | 171 | (274) | 471 |

Less: Assumption changes and management actions | 7 | 95 | 8 | 93 |

Other adjustments | ||||

Fair value adjustments on MFS' share-based payment awards | 37 | (43) | 78 | (139) |

Acquisition, integration and restructuring(2)(3)(4)(5) | (142) | (21) | (237) | (108) |

Other(6)(7)(8)(9)(10) | (225) | (85) | (150) | (96) |

Less: Total of other adjustments | (330) | (149) | (309) | (343) |

Underlying net income | 949 | 902 | 2,684 | 2,635 |

Reported EPS (diluted) ($) | 0.80 | 1.74 | 3.59 | 4.85 |

Less: Market-related impacts ($) | (0.27) | 0.29 | (0.47) | 0.77 |

Assumption changes and management actions ($) | 0.01 | 0.16 | 0.01 | 0.16 |

Fair value adjustments on MFS' share-based payment awards ($) | 0.06 | (0.07) | 0.13 | (0.24) |

Acquisition, integration and restructuring ($) | (0.24) | (0.04) | (0.40) | (0.19) |

Other ($) | (0.37) | (0.14) | (0.25) | (0.16) |

Impact of convertible securities on diluted EPS ($) | (0.01) | — | (0.01) | 0.01 |

Underlying EPS (diluted) ($) | 1.62 | 1.54 | 4.58 | 4.50 |

(1) | Our exposure to interest rates varies by product type, line of business, and geography. Given the long-term nature of our business, we have a higher degree of sensitivity in respect of interest rates at long durations. |

(2) | Amounts relate to acquisition costs for our SLC Management affiliates, BentallGreenOak, InfraRed Capital Partners and Crescent Capital Group LP, which include the unwinding of the discount for Other financial liabilities of $15 million in Q3'22 and $47 million for the first nine months of 2022 (Q3'21 - $17 million; the first nine months of 2021 - $44 million). |

(3) | The restructuring charge of $57 million in Q1'21 related to our strategy for our workspace and redefining the role of the office. |

(4) | Reflects acquisition and integration costs associated with DentaQuest, acquired on June 1, 2022. |

(5) | Q3'22 reflects the changes in estimated future payments for acquisition-related contingent considerations and options to purchase remaining ownership interests of SLC Management affiliates of $80 million. |

(6) | Q3'22 reflects an impairment charge of $170 million (£108 million) pertaining to the attributed goodwill that is not expected to be recovered through the Sun Life UK sale. For more details, see section E - Financial Strength in the MD&A. |

(7) | Includes a charge of $55 million in Q3'22 reflecting the resolution of a matter related to reinsurance pricing for our U.S. In-force Management business. |

(8) | Q2'22 reflects a gain on the sale-leaseback of our Wellesley office in the U.S. |

(9) | Q3'21 reflects an adjustment for investment income and expense allocations between participating policyholders and shareholders for prior years. |

(10) | Q2'21 reflects the UK Finance Act that was signed into law on June 10, 2021, increasing the corporate tax rate from 19% to 25%, which will take effect for future tax periods beginning April 1, 2023. As a result, reported net income decreased by $11 million. |

The following table shows the pre-tax amount of underlying net income adjustments: | |

Quarterly results | Year-to-date | |||

($ millions, unless otherwise noted) | Q3'22 | Q3'21 | 2022 | 2021 |

Reported net income - Common shareholders (after-tax) | 466 | 1,019 | 2,109 | 2,856 |

Underlying net income adjustments (pre-tax): | ||||

Less: Market-related impacts | (212) | 231 | (128) | 696 |

Assumption changes and management actions | 15 | 93 | 16 | 89 |

Other adjustments(1) | (362) | (179) | (331) | (387) |

Total underlying net income adjustments (pre-tax) | (559) | 145 | (443) | 398 |

Less: Taxes related to underlying net income adjustments(1) | 76 | (28) | (132) | (177) |

Underlying net income (after-tax) | 949 | 902 | 2,684 | 2,635 |

(1) | Effective January 1, 2022, there was a change in presentation for the fair value adjustments on MFS' share-based payment awards. We have updated prior periods to reflect this change in presentation. The post-tax basis presentation was not affected. |

Taxes related to underlying net income adjustments may vary from the expected effective tax rate range reflecting the mix of business based on the Company's international operations. | |

2. Additional Non-IFRS Financial Measures | |

Management also uses the following non-IFRS financial measures: | |

Assets under management. AUM is a non-IFRS financial measure that indicates the size of our company's asset management, wealth, and insurance assets. There is no standardized financial measure under IFRS. In addition to the most directly comparable IFRS measures, which are the balance of General funds and Segregated funds on our Statements of Financial Position, AUM also includes Other AUM. | |

Other AUM is composed of retail, institutional and other-third party assets, as well as general fund and segregated fund assets managed by our joint ventures. In Canada, other AUM includes Client assets in retail mutual fund products of Sun Life Global Investments. In Asia, other AUM includes Client assets in Hong Kong managed fund products, International wealth products, Philippines mutual and managed fund products, Aditya Birla Sun Life AMC Limited equity and fixed income mutual fund products, Sun Life Everbright Asset Management products and our joint ventures' general fund and segregated fund assets based on our proportionate equity interest. In Asset Management, other AUM includes Client assets for retail and institutional Clients, as well as capital raising, such as uncalled commitments and fund leverage in SLC Management. There is no directly comparable IFRS financial measure. | |

Effective January 1, 2022, certain components of Other AUM were renamed to "Retail" and "Institutional and managed funds" to align with market naming conventions. Previously, these components were referred to as Mutual funds and Managed funds, respectively, in our interim and annual MD&A. While labeling changes have modified certain terminology, the composition of these components has not been affected. | |

Quarterly results | ||

($ millions) | Q3'22 | Q3'21 |

General fund assets | 203,567 | 197,948 |

Segregated funds | 118,564 | 133,305 |

Other AUM | 952,624 | 1,055,066 |

Total assets under management | 1,274,755 | 1,386,319 |

Assumption changes and management actions. In this document the impacts of ACMA on shareholders' net income (after-tax) is included in reported net income and is excluded from underlying net income, as described in section C - Profitability in the Q3'22 MD&A. |

Note 6.A of the Interim Consolidated Financial Statements for the period ended September 30, 2022 shows the pre-tax impacts of method and assumption changes on shareholders' and participating policyholders' insurance contract liabilities net of reinsurance assets, excluding changes in other policy liabilities and assets. The view in this document of ACMA is the impacts on shareholders' reported net income (after-tax). The Consolidated Financial Statements view is a component of the change in total company liabilities. |

The following table provides a reconciliation of the differences between the two measures. |

Quarterly results | Year-to-date | |||

($ millions) | Q3'22 | Q3'21 | 2022 | 2021 |

Impacts of method and assumption changes on insurance contract liabilities (pre-tax) | (17) | (240) | (12) | (274) |

Less: Participating policyholders(1) | — | 21 | 4 | (9) |

Less: Other items(2) | (20) | — | (20) | — |

Impacts of method and assumption changes excluding participating policyholders (pre-tax) | 3 | (261) | 4 | (265) |

Less: Tax | 5 | (91) | 5 | (93) |

Impacts of method and assumption changes excluding participating policyholders (after-tax) | (2) | (170) | (1) | (172) |

Add: Management actions (after-tax)(3) | 9 | 267 | 9 | 267 |

Other (after-tax)(4) | — | (2) | — | (2) |

Assumption changes and management actions (after-tax)(5)(6) | 7 | 95 | 8 | 93 |

(1) | Adjustment to remove the pre-tax impacts of method and assumption changes on amounts attributed to participating policyholders. |

(2) | Other includes a charge reflecting the resolution of a matter related to reinsurance pricing for our U.S. In-force Management business. |

(3) | Adjustment to include the impacts of management actions on insurance contract liabilities and investment contract liabilities which include, for example, changes in the prices of in-force products, new or revised reinsurance on in-force business, and material changes to investment policies for assets supporting our liabilities, on an after-tax basis. The pre-tax impact of management actions to Method and assumption changes on insurance contract liabilities was an increase of $12 million in Q3'22 and an increase of $12 million for the first nine months of 2022 (Q3'21 - an increase of $355 million; the first nine months of 2021 - an increase of $355 million). |

(4) | Adjustments to include the impacts of method and assumption changes on investment contracts and other policy liabilities, on an after-tax basis. The pre-tax impact to Method and assumption changes on insurance contract liabilities was $nil in Q3'22 and $nil for the first nine months of 2022 (Q3'21 - a decrease of $2 million; the first nine months of 2021 - a decrease of $2 million). |

(5) | Includes the tax impacts of ACMA on insurance contract liabilities and investment contract liabilities, reflecting the tax rates in the jurisdictions in which we do business. |

(6) | ACMA is included in reported net income and is excluded in calculating underlying net income, as described in section C - Profitability in the Q3'22 MD&A. |

Cash and other liquid assets. This measure is comprised of cash, cash equivalents, short-term investments, and publicly traded securities, net of loans related to acquisitions that are held at SLF Inc. (the ultimate parent company), and its wholly owned holding companies. This measure represents available funds for capital re-deployment to support business growth. | |

($ millions) | As at September 30, 2022 | As at December 31, 2021 |

Cash, cash equivalents & short-term securities | 892 | 2,383 |

Debt securities(1) | 1,426 | 1,421 |

Equity securities(2) | 103 | 861 |

Sub-total(3) | 2,421 | 4,665 |

Less: Loans related to acquisitions (held at SLF Inc. and its wholly owned holding companies)(4) | (957) | — |

Cash and other liquid assets (held at SLF Inc. and its wholly owned holding companies)(5) | 1,464 | 4,665 |

(1) | Includes publicly traded bonds. |

(2) | Includes ETF Investments. |

(3) | Q4'21 amounts included $2.0 billion of proceeds from the subordinated debt offerings completed in November 2021, of which $1.5 billion did not qualify as LICAT capital at issuance as it was subject to contractual terms requiring us to redeem the underlying securities in full if the closing of the DentaQuest acquisition did not occur. We completed the acquisition of DentaQuest on June 1, 2022. |

(4) | Loans related to acquisitions have been included as an adjustment to Cash and other liquid assets, as they reflect funding for the DentaQuest acquisition. |

(5) | Represents available funds for capital re-deployment. |

3. Reconciliations of Select Non-IFRS Financial Measures | |

Reported Net Income to Underlying Net Income Reconciliation - Pre-tax by Business Group | |

Q3'22 | ||||||

($ millions) | Canada | U.S. | Asset Management | Asia | Corporate | Total |

Reported net income (loss) - Common shareholders | 210 | 94 | 215 | 125 | (178) | 466 |

Less: Market-related impacts (pre-tax)(1) | (170) | (22) | — | 8 | (28) | (212) |

ACMA (pre-tax) | 62 | (33) | — | (58) | 44 | 15 |

Other adjustments (pre-tax)(1)(2) | (1) | (102) | (89) | — | (170) | (362) |

Tax expense (benefit) on above items(2) | 19 | 35 | 9 | — | 13 | 76 |

Underlying net income (loss) | 300 | 216 | 295 | 175 | (37) | 949 |

Q3'21 | ||||||

Reported net income (loss) - Common shareholders | 393 | 46 | 301 | 288 | (9) | 1,019 |

Less: Market-related impacts (pre-tax)(1) | 204 | 18 | — | 13 | (4) | 231 |

ACMA (pre-tax) | 56 | (98) | — | 132 | 3 | 93 |

Other adjustments (pre-tax)(1)(2) | (115) | (2) | (61) | (1) | — | (179) |

Tax expense (benefit) on above items(2) | (42) | 18 | — | (1) | (3) | (28) |

Underlying net income (loss) | 290 | 110 | 362 | 145 | (5) | 902 |

(1) | For a breakdown of this adjustment made to arrive at a non-IFRS financial measure, see the heading Underlying Net Income and Underlying EPS. |

(2) | Effective January 1, 2022, there was a change in presentation for the fair value adjustments on MFS' share-based payment awards. We have updated prior periods to reflect this change in presentation. The post-tax basis presentation was not affected. |

Forward-looking Statements

From time to time, the Company makes written or oral forward-looking statements within the meaning of certain securities laws, including the "safe harbour" provisions of the United States Private Securities Litigation Reform Act of 1995 and applicable Canadian securities legislation. Forward-looking statements contained in this document include statements (i) relating to our strategies; (ii) relating to our intention to divest Sun Life UK; (iii) relating to our intention to acquire a majority interest in AAM; (iv) relating to the expected impacts of the adoption of IFRS 17 and IFRS 9; (v) relating to our growth initiatives and other business objectives; (vi) relating to our targets and commitments (including with respect to our sustainability plan and net zero emissions); (vii) relating to the plans we have implemented in response to the COVID-19 pandemic and related economic conditions and their impact on the Company, (viii) that are predictive in nature or that depend upon or refer to future events or conditions, and (ix) that include words such as "achieve", "aim", "ambition", "anticipate", "aspiration", "assumption", "believe", "could", "estimate", "expect", "goal", "initiatives", "intend", "may", "objective", "outlook", "plan", "project", "seek", "should", "strategy", "strive", "target", "will", and similar expressions. Forward-looking statements include the information concerning our possible or assumed future results of operations. These statements represent our current expectations, estimates, and projections regarding future events and are not historical facts, and remain subject to change, particularly in light of the ongoing and developing COVID-19 pandemic and its impact on the global economy and its uncertain impact on our business.

Forward-looking statements are not a guarantee of future performance and involve risks and uncertainties that are difficult to predict. Future results and shareholder value may differ materially from those expressed in these forward-looking statements due to, among other factors, the impact of the COVID-19 pandemic and related economic conditions on our operations, liquidity, financial conditions or results and the matters set out in the Q3'22 MD&A under the headings C - Profitability - 5 - Income taxes, E - Financial Strength and H - Risk Management and in SLF Inc.'s 2021 AIF under the heading Risk Factors, and the factors detailed in SLF Inc.'s other filings with Canadian and U.S. securities regulators, which are available for review at www.sedar.com and www.sec.gov, respectively.

Important risk factors that could cause our assumptions and estimates, and expectations and projections to be inaccurate and our actual results or events to differ materially from those expressed in or implied by the forward-looking statements contained in this document, are set out below. The realization of our forward-looking statements, essentially depends on our business performance which, in turn, is subject to many risks, which have been further heightened with the current COVID-19 pandemic given the uncertainty of its duration and impact. Factors that could cause actual results to differ materially from expectations include, but are not limited to: market risks - related to the performance of equity markets; changes or volatility in interest rates or credit spreads or swap spreads; real estate investments; and fluctuations in foreign currency exchange rates; insurance risks - related to policyholder behaviour; mortality experience, morbidity experience and longevity; product design and pricing; the impact of higher-than-expected future expenses; and the availability, cost and effectiveness of reinsurance; credit risks - related to issuers of securities held in our investment portfolio, debtors, structured securities, reinsurers, counterparties, other financial institutions and other entities; business and strategic risks - related to global economic and political conditions; the design and implementation of business strategies; changes in distribution channels or Client behaviour including risks relating to market conduct by intermediaries and agents; the impact of competition; the performance of our investments and investment portfolios managed for Clients such as segregated and mutual funds; shifts in investing trends and Client preference towards products that differ from our investment products and strategies; changes in the legal or regulatory environment, including capital requirements and tax laws; the environment, environmental laws and regulations; operational risks - related to breaches or failure of information system security and privacy, including cyber-attacks; our ability to attract and retain employees; legal, regulatory compliance and market conduct, including the impact of regulatory inquiries and investigations; the execution and integration of mergers, acquisitions, strategic investments and divestitures; our information technology infrastructure; a failure of information systems and Internet-enabled technology; dependence on third-party relationships, including outsourcing arrangements; business continuity; model errors; information management; liquidity risks - the possibility that we will not be able to fund all cash outflow commitments as they fall due; and other risks - COVID-19 matters, including the severity, duration and spread of COVID-19; its impact on the global economy, and its impact on Sun Life's business, financial condition and or results; risks associated with IFRS 17 Insurance Contracts and IFRS 9 Financial Instruments; our international operations, including our joint ventures; market conditions that affect our capital position or ability to raise capital; downgrades in financial strength or credit ratings; and tax matters, including estimates and judgements used in calculating taxes.

The following risk factors are related to our intention to divest Sun Life UK and to acquire a majority interest in AAM that could have a material adverse effect on our forward-looking statements: (1) the ability of the parties to complete each transaction; (2) the failure of the parties to obtain necessary consents and approvals or to otherwise satisfy the conditions to the completion of each transaction in a timely manner, or at all; (3) our ability to realize the financial and strategic benefits of each transaction; and (4) the impact of the announcement of each transaction and the dedication of our resources to completing each transaction. Each of these risks could have an impact on our business relationships (including with future and prospective employees, Clients, distributors and partners) and could have a material adverse effect on our current and future operations, financial conditions and prospects.

The Company does not undertake any obligation to update or revise its forward-looking statements to reflect events or circumstances after the date of this document or to reflect the occurrence of unanticipated events, except as required by law.

About Sun Life

Sun Life is a leading international financial services organization providing asset management, wealth, insurance and health solutions to individual and institutional Clients. Sun Life has operations in a number of markets worldwide, including Canada, the United States, the United Kingdom, Ireland, Hong Kong, the Philippines, Japan, Indonesia, India, China, Australia, Singapore, Vietnam, Malaysia and Bermuda. As of September 30, 2022, Sun Life had total assets under management of $1.27 trillion. For more information, please visit www.sunlife.com.

Sun Life Financial Inc. trades on the Toronto (TSX), New York (NYSE) and Philippine (PSE) stock exchanges under the ticker symbol SLF.

View original content to download multimedia:https://www.prnewswire.com/news-releases/sun-life-reports-third-quarter-2022-results-301666844.html

SOURCE Sun Life Financial Inc.

Uncategorized

Did You Spot The Gorilla In The Fed’s Meeting Room?

Did You Spot The Gorilla In The Fed’s Meeting Room?

Authored by Simon White, Bloomberg macro strategist,

Monetary policy remains exceptionally…

Share this:

Authored by Simon White, Bloomberg macro strategist,

Monetary policy remains exceptionally loose given one of the fastest rate-hiking cycles seen. Pressure is likely to remain on rate expectations to move higher as the Federal Reserve reluctantly eases back on its December pivot, with the fed funds and SOFR futures curves continuing to steepen.

A famous experiment asks volunteers to watch a video of a basketball game and count the passes. Half way through, a gorilla strolls through the action. Almost no-one spots it, so focused they are on the game. As we count the dots and parse the language at this week’s Fed meeting, it’s easy miss the fact that policy overall remains very loose despite over 500 bps of rate hikes. The gorilla has gone by largely unnoticed.

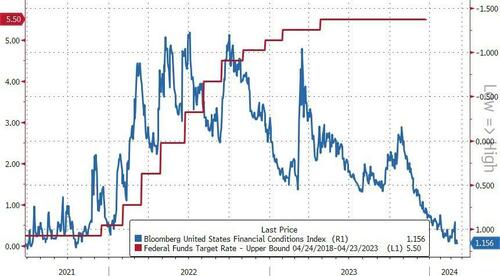

The Fed held rates steady at 5.5% as expected and continued to project three rate cuts this year. But standing back and looking at the totality of monetary policy in this cycle, we can see that - far from conditions tightening - we have instead seen one of the biggest loosening of them in decades.

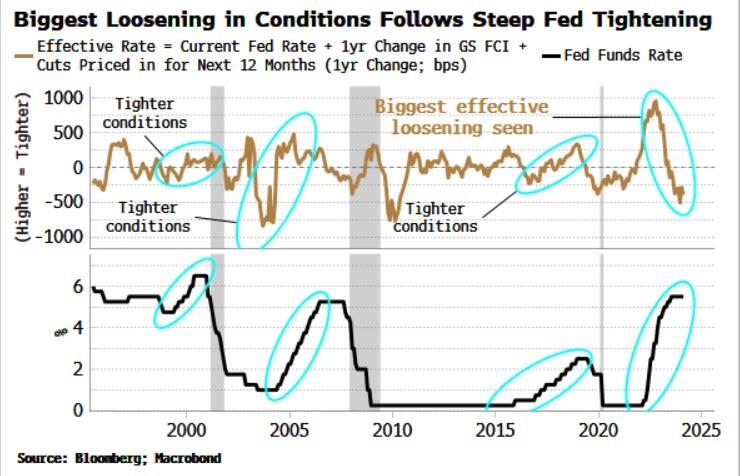

The chart below shows the Effective Fed Rate: the policy rate, plus its expected change over the next year, plus the one-year change in Goldman Sachs’ Financial Conditions Index, which is calibrated to convert the move in stocks, equity volatility, credit spreads and so on to an equivalent change in the Fed’s rate.

As we can see, in the three prior rate-hiking cycles the Effective Rate tightened; this time the rate has loosened, by more than it has done in at least 30 years.

It is against this backdrop the Fed’s pivot in December is even more inexplicable. By then it had become clear that a US recession was not imminent. Yet Jay Powell did not push back on the over six cuts that were priced in for 2024.

*POWELL: WE THINK FINANCIAL CONDITIONS ARE WEIGHING ON ECONOMY

— zerohedge (@zerohedge) March 20, 2024

dude, financial conditions are easier than when you started hiking

Since then inflation and growth data have come in better than expected. Still, though, the Fed may cut rates even if there is a smidge of an opening to do so. That would likely prove to be a mistake.

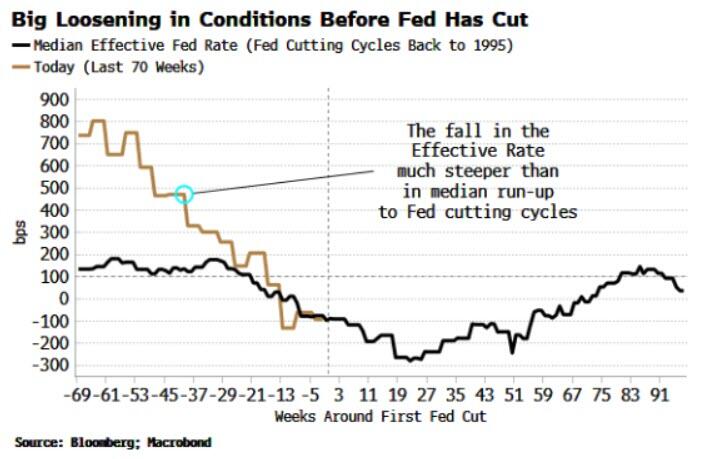

Typically the Effective Rate starts falling before the Fed makes its first cut and continues to fall after. This time around, the Effective Rate’s fall is already considerably steeper than normal – even before a cut is made. The Fed may end up spiking the punch bowl with more booze when the party is already quite tipsy.

The gorilla can be spotted in a number of different ways. Inflation has fallen, but it has done so largely despite the actions of the central bank, not because of them.

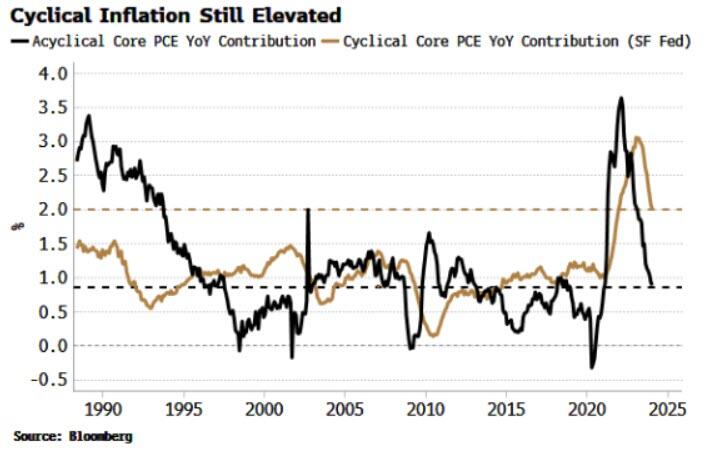

The San Francisco Fed splits core PCE inflation into a cyclical and an acyclical component. Cyclical inflation is made up of the PCE sub-components most sensitive to Fed interest rates, and acyclical is compiled from what’s left over, i.e. inflation that’s more influenced by non-Fed factors.

While acyclical inflation has fallen all the way back to its pre-pandemic average, cyclical PCE remains at its 40-year highs. The Wizard of the Fed has been pulling the rate-hiking levers, but they have done little to directly quell inflation.

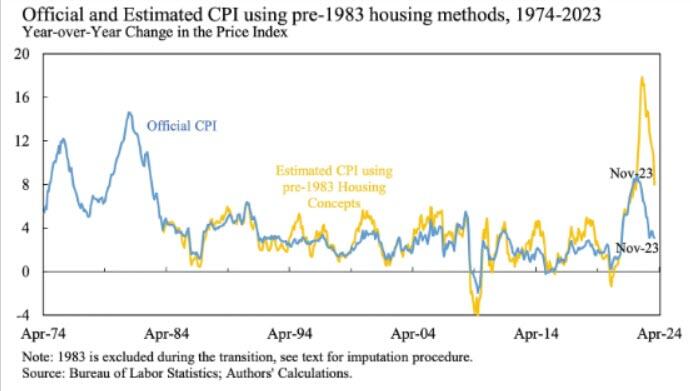

It’s even worse if we account for borrowing costs. Mortgage costs were taken out of CPI in 1983 and car repayments in 1998. In a recent NBER paper by Larry Summers et al, the authors reconstruct CPI to take account of housing borrowing costs.

Inflation on this measure not only peaked much higher than it did in the 1970s, it is still running at 8%. Again, the question lingering in the air is: … and the Fed is considering cutting rates?

Source: NBER Working Paper 32163

(The main point of the paper is that the reason consumer sentiment indices have been depressed despite falling inflation is that they do include the impact of higher borrowing costs.)

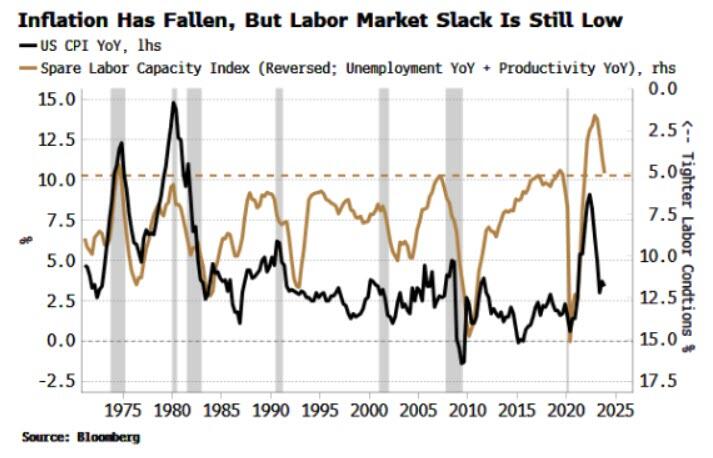

If monetary policy was operating in the way expected, we would expect to see more slack in the economy. Yet this has signally failed to happen. The index of spare labor capacity – composed of the unemployment rate and productivity - has fallen only marginally, and remains stuck at 50-year highs.

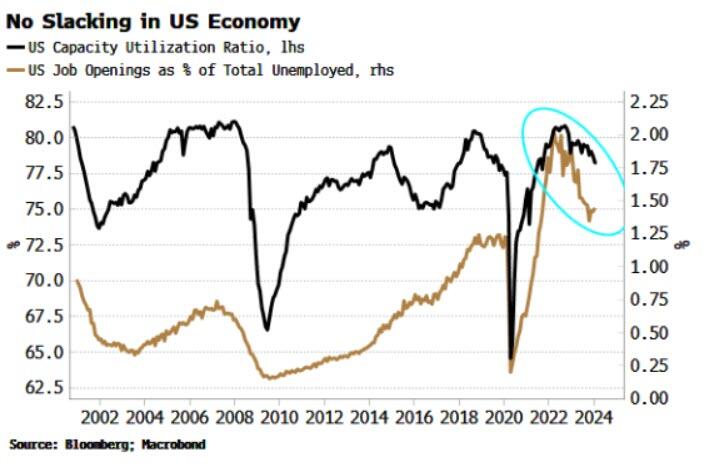

Other measures of slack, including capacity utilization and job openings as a percentage of the unemployed are still near highs or remain historically very elevated. Under this backdrop, a Fed cut looks distinctly unwise.

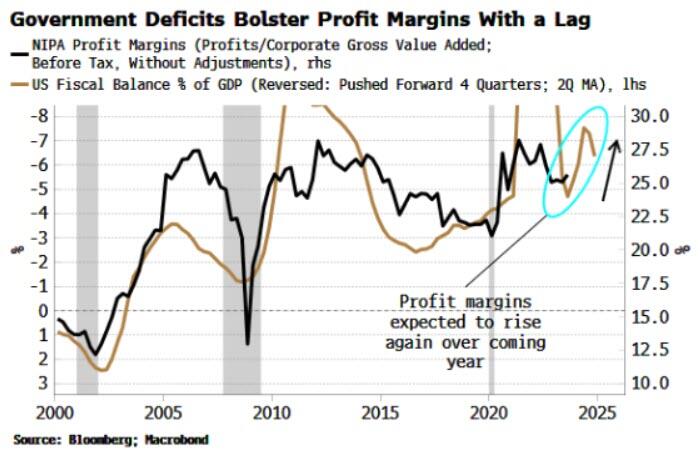

Why did we not see a bigger rise in unemployment or drop in job openings despite the steep rate-hiking cycle? In short, massive government deficits allowed job hoarding.

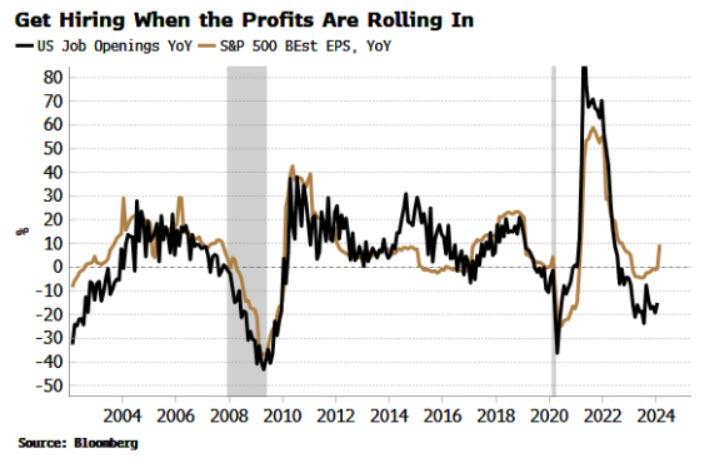

The Kalecki-Levy equation illustrates the link between corporate profits and private and foreign-sector savings. Simply put, the more the household or government sectors dissave, i.e. spend, the higher are profit margins.

In this cycle, it has been the government’s dissaving that has allowed the corporate sector in aggregate to grow profits and - capitalizing on monopolization and on the unique economic disruption seen in the wake of the pandemic - expand profit margins.

It’s for the same reason that EPS growth has bounced back. (Buybacks also play a part here, but they too tend to happen when companies’ profits are growing, which is much easier when the government is spending like a drunken sailor.) As the chart below shows, there is a strong relationship between EPS and job openings, with EPS growth recently turning back up.

With such little movement on slack, no wonder the fall in inflation was due to factors outside of the Fed’s direct influence, most notably China’s glacial recovery. But that leaves markets in an increasingly precarious spot.

Inflation likely lulled the Fed into a false in of security when it performed its policy pirouette in December. But as was clear then and is clear now, this CPI movie isn’t over yet. Furthermore, any recession the Fed may have been wanting to circumvent continues to look off the cards for the next 3-6 months.

Yet the bank may still cut rates, on limited pretext, so confident they sounded last year that they would. That will inflame stock and other asset-bubble risks even more, at a time when we already have bitcoin making new highs and a dog “wif” a hat buying ad space on the Las Vegas Sphere.

Gorillas playing basketball is a very odd thing; the Fed cutting rates before the last quarter of this year would be even odder. Before then, though, markets are likely to try to re-impose some sobriety by reducing or eliminating the number of rate cuts priced in.

Uncategorized

Futures, Global Stocks Soar After Dovish Powell Greenlights Meltup

Futures, Global Stocks Soar After Dovish Powell Greenlights Meltup

Futures and global stocks are soaring and building on Wednesday’s powerful…

Share this:

Futures and global stocks are soaring and building on Wednesday’s powerful gains after the Fed signaled expectations for three rate cuts this year and said inflation eased substantially while Powell greenlit the next big pre-election leg to the rally with dovish press conference comments that suggested the Fed has all but raised its inflation target to 3%. Both Tech and Small-caps are outperforming; while all of the Mag 7 are higher pre-mkt ex-AAPL which was hit on some negative regulatory headlines (AAPL shares have been a funding short for the group). As of 8:00am, S&P futures were 0.4% higher, trading just above 5,300 while Nasdaq futures up 0.8%, both in record territory. 10Y Treasury yields are lower, trading around 4.22% are the curve bull flattens while the USD trades higher after a shock rate cut by the SNB sent the swiss franc plunging. Today’s macro data focus includes flash PMIs, leading index, existing home sales, and jobless data. Powell flagged that a weakening labor market is cue for when to cut rates but did not indicate which data release is the most impactful but in the 5 years leading into COVID, weekly claims averaged 244k and today consensus is 213k.

In premarket trading, Micron shares surged 18%, lifting peers with it, after the maker of computer memory chips gave a 3Q forecast that was much stronger than expected. Chip equipment makers also gain after Micron said it plans to boost capital spending in fiscal 2025: Western Digital (WDC US) +6.7%, Seagate Technology (STX US) +1.2%; chip equipment makers Applied Materials (AMAT US) +3.4%, Lam Research (LRCX US) +3.1%. Here are some other notable premarket movers:

- Astera Labs shares rise 5.6%, set to extend Wednesday’s 72% gain. The semiconductor connectivity company’s initial public offering topped expectations to raise $713 million, adding momentum to AI-related stocks and a listings rebound.

- Broadcom shares gain 2.7% as analysts were positive about the chipmaker’s opportunities following its AI event. Cowen raised its rating to outperform from market perform.

- Guess shares advance 12% after the clothing company reported 4Q adjusted earnings per share and sales above consensus estimates.

- Li Auto ADRs fall 6.8% after the Chinese EV maker reduced its 1Q vehicle deliveries target, citing lower-than-expected order intake. CEO Li Xiang said the firm’s operating strategy for its newly launched Mega model was “mis-paced.”

Stock optimism was reignited after Federal Reserve policymakers kept their outlook for three cuts this year, despite a recent rebound in price pressures. While Chair Jerome Powell continued to highlight that officials would like to see more evidence prices are coming down, he also said it will be appropriate to start easing “at some point this year.” As part of the dovish hurricane response, treasuries advanced, lowering the 10-year yield by four basis points, while the dollar posted small moves. Brent crude traded around $86 a barrel and Bitcoin held at about $67,000. Gold rallied above $2,200 an ounce for the first time and a gauge of emerging-market stocks climbed the most since December.

While the Fed decision surprised some - especially the bears - there were more central bank shockers overnight, notably Taiwan which unexpected hiked 25bps to 2.00% and from the SNB which shockingly cut rates, sending the Swiss franc tumbling. The franc fell more than 1% against the dollar after the SNB lowered its key rate by 25 basis points in a move only a small minority of economists anticipated.

The decision to cut by Swiss policymakers was the first such reduction for one of the world’s 10 most-traded currencies since the pandemic abated.

“This signals to the world that we have turned a corner,” said Philipp Hildebrand, vice chairman at BlackRock and former Chairman of the SNB. “Central banks are easing and the question is where does all this settle in the long term.”

The Stoxx 600 traded up 0.4% after hitting a record earlier in the session. Mining and real estate stocks lead gains, while the health care sector lags. Equities in Europe paired some of their gains after euro-area manufacturing data missed estimates. S&P Global’s purchasing managers’ index showed sustained weakness in Germany and France — the bloc’s top two economies — even as overall private-sector activity for the euro-area rose to a nine-month high in March. Here are some of the most notable premarket movers:

- Chip equipment stocks lead a rally in European tech stocks after the US Fed maintained its outlook for interest-rate cuts, and US firm Micron signaled it will increase capex next year

- Glencore rises as much as 4% as it eyes a stake in Indonesian miner Harita Nickel, a sign of growing interest in the country’s fast-expanding nickel sector

- Argenx gains as much as 12% after a rival for the biotech firm said a phase 3 Luminesce study of Enspryng as an investigational treatment for generalized myasthenia gravis failed

- Remy Cointreau rises as much as 6.1% after Deutsche Bank lifts its recommendation on the stock to buy from hold, with inventory levels seen materially ahead of current market value

- 3i Group shares gain as much as 4.4%, reaching record highs, after its Action unit reported 21% like-for-like sales growth vs. a year earlier, which analysts note shows continued strength

- Energean rises as much as 6.1% as the company reiterated its guidance for this year. Analysts say markets are pleased that operations in Israel have so far not been disrupted

- Esso surged as much as 23%, its biggest intraday gain since April 2022, after the French unit of Exxon Mobil announced a €12-a-share special dividend as part of its full-year report

- Pernod Ricard rises as much as 2.9% as Deutsche Bank upgrades to hold from sell, saying the cognac maker is now “broadly fairly valued,” also seeing a fairly evenly balanced risk profile

- M&G gains as much as 4.2% as the pension fund and asset manager sees better-than-expected institutional flows and operating profit for the full year period

- Next gains as much as 5.9% after full-year results beat estimates and 2025 guidance was maintained. Analysts described the earnings as “pleasing”

- Douglas falls as much against its IPO price as the German perfume retailer began trading in Frankfurt, trading at €23.8 as of 11am, down from the IPO price of €26.

- Nemetschek falls as much as 5.4% after refining its 2024 guidance first proposed in March last year. Analysts deemed Ebitda margin and revenue growth targets cautious

Earlier in the session, the MSCI Asia Pacific Index advanced as much as 2.2%, the most since Nov. 15, with Taiwan Semiconductor, Toyota and Samsung among the biggest contributors to the move. The bullish session echoes US gains after Fed policymakers kept their outlook for three cuts in 2024 and moved toward slowing the pace of reducing their bond holdings, suggesting they aren’t alarmed by a recent rebound in price pressures. Sentiment on Chinese tech stocks got a lift after Tencent Holdings Ltd. announced plans to more than double its stock buyback program and boosted dividends. The region’s semiconductor shares gained after Micron Technology Inc. gave a surprisingly strong revenue forecast for the current quarter, buoyed by demand for memory chips used in artificial intelligence applications.

“With the FOMC event risk out and market pricing roughly in line with dot plots, we think focus of Asian equity investors should return to earlier themes of AI momentum,” Chetan Seth, a strategist at Nomura Holdings Inc., wrote in a note. “We still expect a US soft landing.”

In FX,the Swiss franc sits at the bottom of the G-10 FX pile, falling 0.7% against the dollar after the Swiss National Bank surprised with a 25bps interest rate cut. The Norges Bank stood pat, as expected, prompting an uptick in the krone. The pound is little changed as investors now turn their attention to the Bank of England decision at noon UK time.

In rates, treasuries extended Wednesday’s post-Fed rally, supported by gains in UK front-end as traders fully price in 75bps of easing by Bank of England easing this year for first time since March 12. Treasury yields richer by 3bp to 5bp across the curve with gains led by belly, steepening 5s30s spread by around 1.5bp and adding to Wednesday’s sharp steepening move as additional easing was priced back into the front-end; 10-year trades around 4.23% with bunds lagging by 1bp in the sector, gilts trading broadly in line. European bonds are firmly in the green, with rate markets drawing additional support from SNB’s surprise cut. US session includes several economic indicators and 10Y TIPS auction.

In commodities, oil prices decline, with WTI falling 0.3% to trade near $81. Spot gold rises 1%.

Bitcoin climbed back to best levels at USD 68k, before paring back to around the USD 66k level.

Looking at today's calendar, economic data calendar includes 4Q current account balance, March Philadelphia Fed business outlook and weekly jobless claims (8:30am), March preliminary S&P Global manufacturing and services PMIs (9:45am), February leading index and existing home sales (10am). Fed members scheduled to speak include Barr at 12pmTo contact the reporter on this story:

Market Snapshot

- S&P 500 futures up 0.5% to 5,311.25

- STOXX Europe 600 up 0.8% to 509.14

- MXAP up 2.0% to 178.40

- MXAPJ up 1.9% to 540.84

- Nikkei up 2.0% to 40,815.66

- Topix up 1.6% to 2,796.21

- Hang Seng Index up 1.9% to 16,863.10

- Shanghai Composite little changed at 3,077.11

- Sensex up 0.7% to 72,624.50

- Australia S&P/ASX 200 up 1.1% to 7,781.97

- Kospi up 2.4% to 2,754.86

- German 10Y yield little changed at 2.41%

- Euro down 0.2% to $1.0901

- Brent Futures up 0.5% to $86.36/bbl

- Gold spot up 0.7% to $2,202.16

- US Dollar Index up 0.19% to 103.58

Top Overnight News

- Taiwan’s central bank unexpectedly raises rates from 1.875% to 2% (the consensus was looking for rates to be unchanged). WSJ

- China’s PBOC signals an openness to additional bank reserve requirement ratio (RRR) cuts, but sounds reluctant about lowering interest rates until the Fed begins easing. BBG

- BOJ Governor Kazuo Ueda said the central bank scrapped its massive easing program this week partly to avoid the need for aggressive action later, a comment that may help market players judge his next moves. BBG

- SNB unexpectedly lowers its policy rate from 1.75% to 1.5% (the Street was looking for rates to stay unchanged) as the central bank highlights progress in the battle against inflation. RTRS

- Eurozone flash PMIs are mixed, with a soft manufacturing figure (45.7, down from 46.5 in Feb and below the Street’s 47 forecast) and a decent services number (51.1, up from 50.2 in Feb and above the Street’s 50.5 forecast). BBG

- AMZN is focusing its attention on combating Shein and Temu as the firm views both as larger competitive threats than Walmart and Target. WSJ

- Korean Air Lines passed Boeing over to order 33 Airbus SE A350 wide-body jets in a $14 billion deal. And Japan Airlines said it’ll buy 11 Airbus A321neos — alongside some Boeings — breaking the US planemaker’s hold as its sole single-aisle supplier. BBG

- The DOJ will sue Apple in federal court as soon as today for alleged antitrust violations, people familiar said, escalating the crackdown on Big Tech by regulators in the US and abroad. Apple is accused of blocking rivals from accessing hardware and software features of its iPhones. Shares slipped premarket. BBG

- MU +17% pre mkt after reporting strong EPS upside in FQ2/Feb at 42c (the Street was looking for a 24c loss), w/the beat driven by better sales ($5.82B vs. the Street $5.35B), higher gross margins (20% vs. the Street 13/5%), and superior operating margins (pos. 3.5% vs. the Street’s neg. 4.4% forecast). The FQ3 guide was very. Mgmt said supply/demand conditions are improving thanks to a “confluence of factors”, including strong AI server demand, a healthier demand backdrop in most other end markets (it sees PCs growing in the low-single digits this year, w/AI PCs becoming a larger factor in 2025, while smartphones grow in the low/mid-single digits), and supply reductions across the industry. RTRS

Central Banks

- SNB cut its Policy Rate by 25bps to 1.50% (exp. 1.75%); FX language reiterated "willing to be active in the foreign exchange market as necessary", Ready to intervene in FX; Loosening permitted by inflation progress.

- SNB Chairman Jordan says that rates were able to be lowered as the fight against inflation has been effective. Says we give no forward guidance on future interest rates and will see where we are in 3 months time. Says we remain willing to sue balance to be active on forex market and could be sales of purchases; situation in ME is tricky; neither sales of forex are in focus at the moment

- Norges Bank maintains its Key Policy Rate at 4.50% as expected; reiterates guidance that "policy rate will likely need to be maintained at the current level for some time ahead".

- Norges Bank Governor Bache says the rate path indicates a cut is most likely in September, second rate cut indicated by end of Q1'25

- Taiwan hikes its benchmark interest rate to 2.0% from 1.875%

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly underpinned after the fresh record levels on Wall St post-dovish FOMC where the Fed maintained the projection for 3 rate cuts in 2024 and Powell downplayed recent hot inflation data. ASX 200 strengthened with sentiment also helped by a stellar jobs report and a fall in unemployment, while gold miners outperformed after the precious metal rose above USD 2,200/oz to a new all-time high. Nikkei 225 rallied from the open to unprecedented levels north of 40,800 despite recent hawkish source reports. Hang Seng and Shanghai Comp. were mixed in which the Hong Kong benchmark rallied to just shy of the 17,000 level amid strength in the property sector and as the Fed projection for three rate cuts keeps similar action on the table for the HKMA. Conversely, the mainland lagged as the PBoC injected the least amount of funds in its open market operations since August last year despite the PBoC's Deputy Governor reaffirming that China's monetary policy has ample room and there is still room for cutting RRR

Top Asian News

- HKMA maintained its base rate unchanged at 5.75%, as expected. HKMA said financial and monetary markets in Hong Kong continue to operate in a smooth and orderly manner, while it added that the HKD exchange rate remains stable and Hong Kong dollar interbank rates might remain high for some time.

- PBoC Deputy Governor Changneng Xuan said they will promote effective investment and help resolve excess capacity, while he added that China's monetary policy has ample room and there is still room for cutting RRR. PBoC Deputy said he expects China's nominal economic growth to be around 8% in 2024 and will maintain appropriate growth in credit and total social financing, while they will guide banks to lower deposit rates and lower financing costs, support consumption and investment, as well as promote a rebound in prices.

- China's Vice Finance Minister said fiscal policy will provide the necessary support for achieving the 2024 growth target and China's government debt is at an appropriate level, while he said China has continued to reduce the overall level of tariffs, which has now been reduced to 7.3% and is relatively low in the world, according to Reuters and Global Times.

- China state planner vice chair said they will speed up approval for investment projects and that total bond funds for government investment will exceed CNY 6tln, while they will step up support for private investment and encourage private firms to participate in infrastructure investment projects, according to Reuters.

- BoJ Governor Ueda said the BoJ is expected to maintain an accommodative monetary policy for the time being and accommodative monetary policy is likely to underpin the economy, while he added that cost-push pressure on inflation is dissipating but service prices continue to rise moderately and the preliminary wage negotiation outcome tends to be revised down but even so, they thought the final outcome would be a fairly strong number. BoJ Governor Ueda said as they end massive stimulus, they will likely gradually shrink the balance sheet and at some point reduce JGB purchases but at present, they have no clear idea regarding the timing of reducing JGB buying and scaling back the size of the balance sheet. Furthermore, he said they are not immediately thinking of selling BoJ's ETF holdings and will take plenty of time examining how to reduce ETF holdings.

- BoJ is reportedly seen weighing the next rate hike in July or October as the Yen weakens, according to Nikkei. A source noted that additional hikes are of course on the table and that an early hike leaves room for the BoJ to consider rolling out another increase before the end of the year, while the timeline would keep the BoJ coming off like they are rushing to hike rates. Furthermore, it was stated that a growing number see a July rate boost as another possibility if a weak yen raises the price of imports and accelerates inflation, forcing the BoJ to step in. It was earlier reported that the Yen's decline appears to be raising little alarm at the BoJ for now which was to be expected given that Governor Ueda is maintaining an accommodative stance on policy, according to a source at the BoJ cited by Nikkei. However, it was noted that some at Japan's Finance Ministry are wary of rapid fluctuations in the currency market driven by speculative trades.

- Fitch expects BoJ to raise policy rate to 0.25% by 2025.

- CNOOC (600938 CH) FY (CNY) IFRS Net 123.84bln (exp. 130.33bln); In 2024, will insist on increasing oil and gas reserves and production; ongoing recovery trajectory in China will support demand for oil and gas

European equities, Stoxx600 (+0.4%) are entirely in the green, with sentiment lifted following a post-FOMC equity rally in the US & APAC. Following the release of poor French PMIs and bleak German commentary, equities have edged off best levels. European sectors are firmer; Tech takes the top spot, with optimism permeating within the sector after strong Micron results and Basic Resources benefits from broader strength in base metal prices. US equity futures (ES +0.4%, NQ +0.7%, RTY +0.6%) are stronger, in a continuation of the prior day's post-FOMC rally; Micron (+16% pre-market) is soaring after beating on EPS/Revenue and lifting guidance.

Top European News

- EU New car registrations (Feb): +10.1% (prev. 12.1%); battery electric market share 12% (prev. 10.9%). EU27 New Car Registrations by Manufacturer (Y/Y). Volkswagen (VOW3 GY) +8.7%; Stellantis (STLAM IM/STLAP FP) +11.2%; Renault (RNO FP) +5.9%; BMW (BMW GY) +7.0%; Mercedes Benz Group (MBG GY) -2.1%; Volvo Cars (VOLCAR SS) +33.9%. (acea)

- Portugal's President named centre-right democratic alliance leader Luis Montenegro as the new PM, according to Reuters.

FX

- USD is attempting to claw back post-FOMC losses with some help via EZ-PMI releases. DXY still has some way to go to close the gap to yesterday's best at 104.14. High print for today at 103.66 coincides with the 200DMA.

- EUR has been dragged lower by EZ PMIs which were indicative of the composite figure approaching neutral territory; EUR/USD on a 1.09 handle after slipping to a low of 1.0888.

- GBP is a touch softer vs. the USD but near post-FOMC highs which saw Cable peak at 1.2803. UK PMIs saw services and composite miss but the manufacturing print edge closer to neutral. Focus ahead is firmly on the BoE.

- JPY pausing for breath vs. the USD after vaulting to a high of 151.81 yesterday, which saw the pair stop shy of the 2023 high at 151.91 and 2022 peak at 151.94.

- AUD the best performer across the majors following encouraging jobs metrics. AUD/USD as high as 0.6634 but unable to breach last week's best at 0.6638. NZD marginally higher vs. USD despite the surprise contraction in Q4 GDP data.

- CHF is the clear laggard across the majors as the SNB surprises with a 25bps rate cut and reiterates a willingness to intervene in the FX market. EUR/CHF as been as high as 0.9782 to its highest level since July last year; 0.9842 was the high that year.

- An unchanged announcement from the Norges Bank but one which sparked NOK strength given the repo path has not formalised a Q4-2024 rate cut as some were hoping for. As such, EUR/NOK slipped from 11.5300 to 11.4857. However, a modest dovish move was seen on Governor Bache indicating the first cut is "likely" in September.

- PBoC set USD/CNY mid-point at 7.0942 vs exp. 7.1792 (prev. 7.0968).

Fixed Income

- Choppy price action for Bunds owing to varied PMIs from France and Germany. The former sparked a dovish reaction with Bunds lifting from 131.90 to 132.72, whilst the German metrics sent Bunds back down to 131.85, though downside was shortlived given the Manuf. miss and SNB rate cut.

- USTs are underpinned by the dovish fixed narrative which is dictating EGBs/Gilts into the BoE post-SNB/PMIs. Action which has taken USTs to a 110-24+ high, eclipsing the post-FOMC 110-22 peak.

- Gilt price action is in-fitting with EGBs and as such approached their own PMIs with gains of around 30 ticks on the session. A release which saw two-way action with Gilts initially slipping to 99.24 (strong Manuf.) before rebounding to 99.46 (Comp. & Serv. miss); BoE up next.

- Spain sells EUR vs exp. EUR 5.5-6.5bln 2.50% 2027, 5.75% 2032, 3.45% 2043 Bono

- France sells EUR 12.498bln vs exp. EUR 11-12.5bln 2.50% 2027, 2.75% 2029, and 1.50% 2031 OAT

Commodities

- Crude was initially firmer after the Fed-induced Dollar decline coupled with broader risk appetite, and geopolitics. However, the complex then trimmed gains after PMIs for France and Germany painted a bleak economic recovery picture; Brent is now lower on the session and just shy of USD 86/bbl.

- Precious metals extend on post-Powell gains despite an attempted recovery in the Dollar, with spot gold topping USD 2,200/oz to fresh ATHs in APAC trade while spot silver gained status above USD 25.50/oz.

- Base metals are higher across the board in the after-math of the FOMC which boosted broader market sentiment.

Geopolitics

- US military said coalition forces destroyed an unmanned aerial vehicle fired by Yemen's Houthis in the Red Sea and destroyed an unmanned surface vessel on March 20th, according to Reuters.

- Australia and Britain signed a defence pact which includes a status of forces agreement and makes it easier for the respective forces to operate together in each other’s countries, while the agreement also formalises the established practice of consulting on issues that affect our sovereignty and regional security.

- "Al-Arabiya sources: Pressure on Israel to postpone the Rafah operation for at least 45 days", according to Al Arabiya; "The mediators and America rejected a preliminary Israeli proposal on the military operation in Rafah"

US Event Calendar