Instead, it ended up being more or less the opposite, with crypto-led liquidations dragging futures and global markets lower, and extending Wednesday losses after central bankers issued warnings on inflation and fueled concern that aggressive policy will end with a hard-landing recession, which increasingly more now see as being 2022 business, an outcome that now appears assured especially after yesterday's disastrous guidance cut from RH, the second in three weeks!

Recession fears and inflation woes may be prolonged by today's PCE deflator report. The consumer price gauge favored by the Fed may have picked up to 6.4% last month from 6.3%. Personal income growth probably edged up but Bloomberg Economics highlights an anticipated decline in real personal spending as a major worry.

Meanwhile, China’s economy showed further signs of improvement in June with a strong pickup in services and construction, even if the latest Chinese PMI print came slightly below expectations. Also overnight, Russia said it withdrew troops from Ukraine’s Snake Island in the Black Sea after Ukraine said its forces drove Russian troops from the area.

In any case, with zero demand from pensions so far (even though the continued selling in stocks and buying in bonds will only make the imabalnce bigger), overnight Nasdaq 100 contracts dropped 1.8% while S&P 500 futures declined 1.3%, and cryptos crumbled, with bitcoin dragged back below $19000 and Ether on the verge of sliding below $1000. The tech-heavy gauge managed to end Wednesday’s trading slightly higher, while the S&P 500 fell for a third straight day. In Europe, the Stoxx Europe 600 Index slid 1.9%. Treasuries gained, the dollar was steady and gold declined and crude oil futures edged lower again.

Which brings us to the last trading day of a quarter for the history books: the S&P 500 is set for its biggest 1H decline since 1970 and the Nasdaq 100 since 2002, the height of the dot.com bust. The Stoxx 600 is set for the worst 1H since 2008, the height of the GFC.

Traders have ramped up bets that the global economy will buckle under central bank tightening campaigns -- and that policy makers will eventually backpedal. The bond market shifted to price in a half-point rate cut in the Federal Reserve’s benchmark rate at some point in 2023. On Wednesday, during the annual ECB annual forum, Fed Chair Jerome Powell and his counterparts in Europe and the UK warned inflation is going to be longer lasting. A view that central banks need to act fast on rates because they misjudged inflation has roiled markets this year, with global stocks about to close out their worst quarter since the three months ended March 2020.

“Markets are worried about growth as central bankers continue to emphasize that bringing down inflation is their overriding objective, and that it may take time to bring inflation down,” said Esty Dwek, chief investment officer at Flowbank SA. “We still haven’t seen total capitulation in markets, so further downside is possible.”

Meanwhile, the cost of insuring European junk bonds against default crossed 600 basis points for the first time in two years on Thursday.

And speaking of Europe, stocks are also down over 2% in early trading, with all sectors in the red. DAX and CAC underperform at the margin with autos, consumer discretionary and banking sectors the weakest within the Stoxx 600. Here are some of the biggest European movers today:

Uniper shares slump as much as 23% after the German utility withdrew its outlook and said it was discussing a possible bailout from the German government following Russia’s move to curb natural gas deliveries.

SAP sinks as much as 6.5% after Exane BNP Paribas downgraded stock to neutral from outperform, saying it sees risks on demand side in the near term as software spending decisions come under increased scrutiny.

Sanofi shares decline as much as 4.5% after the French drugmaker said the FDA placed late-stage clinical trials of tolebrutinib on partial hold in US because of concerns about liver injuries.

European semiconductor stocks fell, following peers in the US and Asia lower amid growing concerns that the industry might face a downturn soon as chip stockpiles build. ASML drops as much as 3.4%, Infineon -4.1%, STMicro -3.1%

Norsk Hydro shares slide as much as 6% amid metals decline and as DNB cuts the stock to sell from hold, citing concerns about rising aluminum supply.

Stainless steel stocks in Europe fall, with Morgan Stanley saying the settlement on the latest ferrochrome benchmark missed its expectations. Outokumpu shares down as much as 6.6%, Aperam -7.2%, Acerinox -4%

Saab shares jump as much as 8.4%, after getting an order worth SEK7.3b from the Swedish Defence Materiel Administration for GlobalEye Airborne Early Warning and Control aircraft.

Orsted shares rise as much as 2.5%, before paring some of the gains. HSBC raises to buy from hold, saying any further downside for the wind farm operator looks limited.

Bunzl shares rise as much as 2.6% after the specialist distribution company said it now expects very good revenue growth in 2022.

Grifols shares rise as much as 7.8% after slumping on Wednesday, as the company says that the board isn’t analyzing any capital increase “for the time being.”

Earlier in the session, Asian stocks fell for a second day as tech-heavy indexes in Taiwan and South Korea continued to get pummeled amid concerns over the potential for aggressive monetary tightening in the US to rein in inflation. The MSCI Asia Pacific Index declined as much as 1.2%, dragged down by technology shares including TSMC, Alibaba and Tencent. Taiwan slid more than 2%, while gauges in Japan, South Korea, Australia dropped more than 1%. Stocks in mainland China rose more than 1% after the economy showed further signs of improvement in June with a strong pickup in services and construction as Covid outbreaks and restrictions were gradually eased. Traders are also watching Chinese President Xi Jinping’s trip to Hong Kong, his first time outside of the mainland since 2020.

Asian stocks are struggling to recover from a May low as the threat of higher US rates outweighs China’s emergence from strict Covid lockdowns and its pledge of stimulus measures. While mainland Chinese stocks led gains globally this month, the rest of the markets in the region -- especially those heavy with technology stocks and exporters -- saw hefty outflows of foreign funds. “Investors continue to assess recession and also inflation risks,” Marcella Chow, JPMorgan Asset Management’s global market strategist, said in an interview with Bloomberg TV. “This tightening path has actually increased the chance of a slower economic growth going forward and probably has brought forward the recession risks.” Asian stocks are set to post a more than 12% loss this quarter, the worst since the one ended March 2020 during the pandemic-induced global market rout.

Japanese stocks declined after the release of China’s data on manufacturing and non-manufacturing PMIs that showed slower than expected improvements. The Topix Index fell 1.2% to 1,870.82 as of market close Tokyo time, while the Nikkei declined 1.5% to 26,393.04. Sony Group contributed the most to the Topix Index decline, falling 3.4%. Out of 2,170 shares in the index, 531 rose and 1,574 fell, while 65 were unchanged. “Although China is recovering from a lockdown, business sentiment in the manufacturing industry is deteriorating around the world,” said Tomo Kinoshita, global market strategist at Invesco Asset Management China’s Economy Shows Signs of Improvement as Covid Eases.

Indian stock indexes posted their biggest quarterly loss since March 2020 as the global equity market stays rattled by high inflation and a weakening outlook for economic growth. The S&P BSE Sensex ended little changed at 53,018.94 in Mumbai on Thursday, while the NSE Nifty 50 Index dropped 0.1%. The gauges shed more than 9% each in the June quarter, their biggest drop since the outbreak of pandemic shook the global markets in March 2020. The main indexes have fallen for all but one month this year as surging cost pressures forced India’s central bank to raise rates twice and tighten liquidity conditions. The selloff is also partly driven by record foreign outflows of more than $28b this year. Despite the turmoil in global markets, Indian stocks have underperformed most Asian peers, partly helped by inflows from local institutions, which made net purchases of more than $30b of local stocks. “Investors worry that the latest show of central bank determination to tame inflation will slow economies rapidly,” HDFC Securities analyst Deepak Jasani wrote in a note. Fourteen of the 19 sector sub-gauges compiled by BSE Ltd. fell Thursday, with metal stocks leading the plunge. The expiry of monthly derivative contracts also weighed on markets. For the June quarter, metal stocks were the worst performers, dropping 31% while information technology gauge fell 22%. Automakers led the three advancing sectors with 11.3% gain.

Australian stocks also tumbled, with the S&P/ASX 200 index falling 2% to close at 6,568.10, weighed down by losses in mining, utilities and energy stocks. In New Zealand, the S&P/NZX 50 index fell 0.8% to 10,868.70

In rates, treasuries advanced, led by the belly of the curve. German bonds surged, led by the short-end and outperforming Treasuries. US yields richer by as much as 5.4bp across front-end and belly of the curve which outperforms, steepening 2s10s, 5s30s by 2bp and 2.8bp; wider bull-steepening move in progress for German curve with yields richer by up to 13.5bp across front-end with 2s10s wider by 3.5bp on the day. US 10-year yields around 3.055%, richer by 3.5bp. Money markets aggressively trimmed ECB tightening bets on relief that French June inflation didn’t come in above the median estimate. Bonds also benefitted from haven buying as stocks slide. Month-end extension flows may continue to support long-end of the Treasuries curve. bunds outperform by 7bp in the sector. IG issuance slate empty so far; Celanese Corp. pushed back plans to issue in euros and dollars, most likely to next week, after deals struggled earlier this week. Focal points of US session include PCE deflator and MNI Chicago PMI.

In FX, the Bloomberg Dollar Spot Index was steady as the greenback traded mixed against its Group-of-10 peers. The yen advanced and Antipodean currencies were steady against the greenback. French inflation quickened to the fastest since the euro was introduced. Steeper increases in energy and food costs drove consumer-price growth to 6.5% in June from 5.8% in May . Sweden’s krona swung to a loss. It briefly advanced earlier after the Riksbank raised its policy rate by 50bps, as expected, signaled faster rate hikes and a quicker trimming of the balance sheet. The pound rose, snapping three days of losses against the dollar. UK household incomes are on their longest downward trend on record, as the nation’s cost of living crisis saps the spending power of British households. Separate figures showed that the current-account deficit widened sharply to £51.7 billion ($63 billion) in the first quarter. The yen rose and the Japan’s bonds inched up. The BOJ kept the amount and frequencies of planned bond purchases unchanged in the July-September period. The Australian dollar reversed a loss after data showed China’s official manufacturing purchasing managers index rose above 50 for the first time since February in a sign of improvement in the world’s second largest economy.

Bitcoin is on track for its worst quarter in more than a decade, as more hawkish central banks and a string of high-profile crypto blowups hammer sentiment. The 58% drawdown in the biggest cryptocurrency is the largest since the third quarter of 2011, when Bitcoin was still in its infancy, data compiled by Bloomberg show.

In commodities, WTI trades a narrow range, holding below $110. Brent trades either side of $116. Most base metals trade in the red; LME zinc falls 3.1%, underperforming peers. Spot gold falls roughly $3 to trade near $1,814/oz. Bitcoin slumps over 6% before finding support near $19,000.

Looking to the day ahead now, data releases include German retail sales for May and unemployment for June, French CPI for June, the Euro Area unemployment rate for May, Canadian GDP for April, whilst the US has personal income and personal spending for May, the weekly initial jobless claims, and the MNI Chicago PMI for June.

Market Snapshot

S&P 500 futures down 1.2% to 3,775.75

STOXX Europe 600 down 1.8% to 406.18

MXAP down 1.0% to 158.01

MXAPJ down 1.1% to 524.78

Nikkei down 1.5% to 26,393.04

Topix down 1.2% to 1,870.82

Hang Seng Index down 0.6% to 21,859.79

Shanghai Composite up 1.1% to 3,398.62

Sensex up 0.2% to 53,136.59

Australia S&P/ASX 200 down 2.0% to 6,568.06

Kospi down 1.9% to 2,332.64

Gold spot down 0.2% to $1,814.91

US Dollar Index little changed at 105.04

German 10Y yield little changed at 1.42%

Euro little changed at $1.0443

Brent Futures down 0.4% to $115.85/bbl

Top Overnight News from Bloomberg

The surge in the dollar has set Asian currencies on course for their worst quarter since the 1997 financial crisis and created a dilemma for central bankers

French Finance Minister Bruno Le Maire said the EU can deliver the global minimum corporate tax with or without the support of Hungary, circumventing Budapest’s veto earlier this month just as the bloc was on the brink of a agreement

German unemployment unexpectedly rose, snapping 15 straight months of decline as refugees from the war in Ukraine were included in those searching for work

The SNB bought foreign exchange worth 5.7 billion francs ($5.96 billion) in the first quarter of 2022 as the franc sharply appreciated against the euro and briefly touched parity in March

The ECB plans to ask the region’s lenders to factor in the economic hit of a potential cut off of Russian gas when considering payouts to shareholders

European stocks were poised for their biggest drop in any half-year period since 2008, as investors focused on the prospects for economic slowdown and stubbornly high inflation in the region

New Zealand will enter a recession next year that could be deeper than expected, Bank of New Zealand economists said after a survey showed business sentiment continues to slump

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were varied at month-end amid a slew of data releases including mixed Chinese PMIs. ASX 200 was dragged lower by weakness in energy, miners and the top-weighted financials sector. Nikkei 225 declined after disappointing Industrial Production data and with Tokyo raising its virus infection level. Hang Seng and Shanghai Comp. were somewhat mixed with Hong Kong indecisive and the mainland underpinned after the latest Chinese PMI data in which Manufacturing PMI printed below estimates but Non-Manufacturing PMI firmly surpassed forecasts and along with Composite PMI, all returned to expansion territory.

Top Asian News

NATO Secretary General Stoltenberg said China's growing assertiveness has consequences for the security of allies, while he added China is not our adversary, but we must be clear-eyed about the serious challenges it presents.

US blacklisted 5 Chinese firms for allegedly helping Russia in which Connec Electronic, King Pai Technology, Sinno Electronics, Winnine Electronic and World Jetta Logistics were added to the entity list which restricts access to US technology, according to WSJ.

Japan's government cut its assessment of industrial production and noted that production is weakening, while it stated that Japan's motor vehicle production declined 8% M/M and that industrial production likely saw the largest impact of Shanghai's COVID-19 lockdown in May, according to Reuters.

Tokyo metropolitan government will reportedly increase COVID infections level to the second-highest, according to FNN.

It’s been a downbeat session for global equities thus far as sentiment deteriorates further. European bourses are lower across the board, with losses extending during early European hours. European sectors are all in the red but portray a clear defensive bias. Stateside, US equity futures have succumbed to the glum mood, with the NQ narrowly underperforming.

Top European News

Riksbank hiked its Rate by 50bps to 0.75% as expected, and said the rate will be raised further and it will be close to 2% at the start of 2023. Bank said the balance sheet its to shrink faster than previously flagged, and suggested that policy rate will increase faster if needed. Click here for details.

Riksbank's Ingves said inflation over forecast probably not enough for Riksbank to hold extra policy meeting in summer. Ingves added that if the situation requires a 75bps hike, then Riksbank will carry out a 75bps hike.

Orsted Gains as HSBC Upgrades With Shares Seen ‘Good Value’

Aston Martin Extends Losses as Carmaker Reportedly Seeking Funds

Climate Litigants Look Beyond Big Oil for Their Day in Court

Ukraine Latest: Putin Warns NATO on Moving Military to Nordics

FX

DXY extends on gains above 105.00, but could see more upside on safe haven demand and residual rebalancing flows over fixes - EUR/USD inches towards 1.0400 to the downside.

Yen regroups as yields drop and risk sentiment deteriorates to compound corrective price action.

Franc unwinds some of its recent outperformance and Loonie lose traction from oil ahead of Canadian GDP.

Swedish Crown unable to take advantage of hawkish Riksbank hike in face of risk aversion - Eur/Sek stuck in a rut close to 10.7000.

Pound finds some underlying bids into 1.2100 and Kiwi at 0.6200, while Aussie holds above 0.6850 with encouragement from China’s services PMI that also propped the Yuan.

Fixed Income

Bonds on bull run into month, quarter and half year end - Bunds top 148.00 at best, Gilts approach 113.50 and 10 year T-note just a tick away from 118-00.

Debt in demand on safe haven grounds rather than duration as curves steepen on less hawkish/more dovish market pricing.

Italian supply comfortably covered to keep BTP futures propped ahead of US PCE data and yet another speech from ECB President Lagarde.

Commodities

WTI and Brent front-month futures are resilient to the broader risk downturn, and firmer Dollar as OPEC+ member members gear up for what is expected to be a smooth meeting.

Spot gold is uneventful but dipped under yesterday's low, with potential support at the 15th June low at USD 1,806.59/oz.

Base metals are softer across the board amid the broader risk profile. Dalian and Singapore iron ore futures were on track for quarterly losses.

Ship with 7,000 tonnes of grain leaves Ukraine port, according to pro-Russia officials cited by AFP.

US Event Calendar

08:30: June Initial Jobless Claims, est. 229,000, prior 229,000

08:30: June Continuing Claims, est. 1.32m, prior 1.32m

08:30: May Personal Income, est. 0.5%, prior 0.4%

08:30: May Personal Spending, est. 0.4%, prior 0.9%

08:30: May Real Personal Spending, est. -0.3%, prior 0.7%

08:30: May PCE Deflator MoM, est. 0.7%, prior 0.2%

08:30: May PCE Deflator YoY, est. 6.4%, prior 6.3%

08:30: May PCE Core Deflator YoY, est. 4.8%, prior 4.9%

08:30: May PCE Core Deflator MoM, est. 0.4%, prior 0.3%

09:45: June MNI Chicago PMI, est. 58.0, prior 60.3

DB's Jim Reid concludes the overnight wrap

We’ve just released the results of our monthly EMR survey that we conducted at the start of the week. It makes for some interesting reading, and we’re now at the point where 90% of respondents are expecting a US recession by end-2023, which is up from just 35% in our December survey. That echoes our own economists’ view that we’re going to get a recession in H2 2023, and just shows how sentiment has shifted since the start of the year as central banks have begun hiking rates. When it comes to people’s views on where markets are headed next, most are expecting many of the themes from H1 to continue, with a 72% majority thinking that the S&P 500 is more likely to fall to 3,300 rather than rally to 4,500 from current levels, whilst 60% think that Treasury yields will hit 5% first rather than 1%. Click here to see the full results.

When it comes to negative sentiment we’ll have to see what today brings us as we round out the first half of the year, but if everything remains unchanged today we’re currently set to end H1 with the S&P 500 off to its worst H1 since 1970 in total return terms. And there’s been little respite from bonds either, with US Treasuries now down by -9.79% since the start of the year, so it’s been bad news for traditional 60/40 type portfolios. Ultimately, a large reason for that has been investors’ fears that ongoing rate hikes to deal with inflation will end up leading to a recession, and yesterday saw a continuation of that theme, with Fed Chair Powell, ECB President Lagarde and BoE Governor Bailey all reiterating their intentions in a panel at the ECB’s Forum to return inflation back to target.

In terms of that panel, there weren’t any major headlines on policy we weren’t already aware of, although there was a collective acknowledgement of the risk that inflation could become entrenched over time and the need to deal with that. Fed Chair Powell described the US economy as in “strong shape”, but one that ultimately requires much tighter financial conditions to bring inflation back to target. Year-end fed funds expectations remained steady in response, down just -0.7bps to 3.45%. However, further out the curve the simmering slower growth narrative continued to grip markets and sent 10yr Treasury yields -8.2bps lower to 3.09%, and the 2s10s another -1.1bps flatter to 4.7bps. In line with a tighter Fed policy path and slower growth, 10yr breakevens drove the move in nominal yields, falling -8.2bps to 2.39%, their lowest levels since January, having entirely erased the gains seen after Russia’s invasion of Ukraine, when it peaked above 3% at one point in April. Along with 2s10s flattening, the Fed’s preferred measure of the near-term risk of recession, the forward spread (the 18m3m – 3m), similarly flattened by -5.7bps, hitting its lowest level in nearly four months at 154bps. And thismorning there’s only been a partial reversal of these trends, with 10yr Treasury yields (+1.3bps) edging back up to 3.10% as we go to press. Over in equities, the S&P 500 bounced around but finished off of its intraday lows with just a -0.07% decline, again with the macro view likely skewed by quarter-end rebalancing of portfolios. The NASDAQ was similarly little changed on the day, falling a mere -0.03%.

In terms of the ECB, President Lagarde said on that same panel that she didn’t think “we are going back to that environment of low inflation” that was present before the pandemic. But when it came to the actual data yesterday there was a pretty divergent picture. On the one hand, Spain’s CPI for June surprised significantly on the upside, with the annual inflation rising to +10.0% (vs. +8.7% expected) on the EU’s harmonised measure. But on the other, the report from Germany then surprised some way beneath expectations, coming in at +8.2% on the EU-harmonised measure (vs. +8.8% expected). So mixed messages ahead of the flash CPI print for the entire Euro Area tomorrow.

As in the US, there was a significant rally in European sovereign bonds, with yields on 10yr bunds (-10.7bps), OATs (-10.7bps) and BTPs (-16.0bps) all moving lower on the day. Equities also lost significant ground amidst the risk-off tone, and the STOXX 600 shed -0.67% as it caught up with the US losses from the previous session. That risk-off tone was witnessed in credit as well, where iTraxx Crossover widened +21.5bps to a post-pandemic high. At the same time, there were further concerns in Europe on the energy side, with natural gas futures up by +8.06% to a three-month high of €139 per megawatt-hour, which follows a reduction in capacity yesterday at Norway’s Martin Linge field because of a compressor failure.

Whilst monetary policy has been the main focus for markets lately, we did get some headlines on the fiscal side yesterday too, with a report from Bloomberg that Senate Democrats were working on an economic package that had smaller tax increases in order to reach a deal with moderate Democratic senator Joe Manchin. For reference, the Democrats only have a majority in the split 50-50 senate thanks to Vice President Harris’ tie-breaking vote, so they need every Democrat Senator on board in order to pass legislation. According to the report, the plan would be worth around $1 trillion, with half allocated to new spending, and the other half cutting the deficit by $500bn over the next decade.

Overnight in Asia we’ve seen a mixed market performance overnight. Most indices are trading lower, including the Nikkei (-1.45%) and the Kospi (-0.81%), but Chinese equities have put in a stronger performance after an improvement in China’s PMIs in June, and the CSI 300 (+1.62%) and the Shanghai Comp (+1.31%) have both risen. That came as manufacturing activity expanded for the first time in four months, with the PMI up to 50.2 in June (vs. 50.5 expected) from 49.6 in May. At the same time, the non-manufacturing climbed to 54.7 points in June, up from 47.8 in May, which also marked the first time it’d been above the 50 mark since February.

Nevertheless, that positivity among Chinese equities are proving the exception, with equity futures in the US and Europe pointing lower, with those on the S&P 500 (-0.28%) looking forward to a 4th consecutive daily decline as concerns about a recession persist.

When it came to other data yesterday, the third estimate of US GDP for Q1 saw growth revised down to an annualised contraction of -1.6% (vs. -1.5% second estimate). Separately, the Euro Area’s M3 money supply grew by +5.6% year-on-year in May (vs. +5.8% expected), which is the slowest pace since February 2020.

To the day ahead now, data releases include German retail sales for May and unemployment for June, French CPI for June, the Euro Area unemployment rate for May, Canadian GDP for April, whilst the US has personal income and personal spending for May, the weekly initial jobless claims, and the MNI Chicago PMI for June.

The SNF Institute for Global Infectious Disease Research announces new advisory board

From identifying the influenza virus that caused the pandemic of 1918 to developing vaccines against pneumococcal pneumonia and bacterial meningitis in…

From identifying the influenza virus that caused the pandemic of 1918 to developing vaccines against pneumococcal pneumonia and bacterial meningitis in the 1970s, combating infectious disease has a rich history at Rockefeller. That tradition continues as the Stavros Niarchos Foundation Institute for Global Infectious Disease Research at Rockefeller University (SNFiRU) caps a successful first year with the establishment of a new advisory board.

Credit: Lori Chertoff/The Rockefeller University

From identifying the influenza virus that caused the pandemic of 1918 to developing vaccines against pneumococcal pneumonia and bacterial meningitis in the 1970s, combating infectious disease has a rich history at Rockefeller. That tradition continues as the Stavros Niarchos Foundation Institute for Global Infectious Disease Research at Rockefeller University (SNFiRU) caps a successful first year with the establishment of a new advisory board.

This international advisory board was created in part to give guidance on how to best use SNFiRU’s resources, as well as bring forward innovative ideas concerning new avenues of research, public education, community engagement, and partnership projects.

SNFiRU was established to strengthen readiness for and response to future health crises, building on the scientific advances and international collaborations forged in the context of the COVID-19 pandemic. Launched with a $75 million grant from the Stavros Niarchos Foundation (SNF) as part of its Global Health Initiative (GHI), the institute provides a framework for international scientific collaboration to foster research innovations and turn them into practical health benefits.

SNFiRU’s mission is to better understand the agents that cause infectious disease and to lower barriers to treatment and prevention globally. To speed this work, the institute launched numerous initiatives in its inaugural year. For instance, SNFiRU awarded 31 research projects in 29 different Rockefeller laboratories for over $5 million to help get collaborative new research efforts off the ground. SNFiRU also supports the Rockefeller University Hospital, where clinical studies are conducted, and brought on board its first physician-scientist through Rockefeller’s Clinical Scholars program. “One of the surprises was the scope of interest from Rockefeller scientists in using their talents to tackle important infectious disease problems,” says Charles M. Rice, Maurice R. and Corinne P. Greenberg Professor in Virology at Rockefeller and director of SNFiRU. “The research topics range from the biology of infectious agents to the dynamics of the immune response to pathogens, and also include a number of infectious disease-adjacent studies.”

In the past 12 months, SNFiRU often brought together scientists studying different aspects of infectious disease as a way to spur new collaborations. In addition to hosting its first annual day-long symposium, SNFiRU initiated a Young Scientist Forum for students and post-doctoral fellows to meet regularly, facilitating cross-laboratory thinking. A bimonthly seminar series has also been established on campus.

Another aim of SNFiRU is to develop relationships with community-based organizations, as well as design and participate in community-engaged research, with a focus on low-income and minority communities. To that end, SNFiRU is helping develop a research project on Chagas disease, a tropical parasitic infection prevalent in Latin America that can cause congestive heart failure and gastrointestinal complications if left untreated. The project will bring together clinicians practicing at health centers in New York, Florida, Texas, and California and basic scientists from multiple institutions to help the communities that are most impacted.

“The SNFiRU international advisory board convenes globally recognized leaders with distinguished biomedical expertise, unrivalled experience in pandemic preparedness and response, and a shared commitment to translating scientific advancements into equitably distributed benefits in real-world settings,” says SNF Co-President Andreas Dracopoulos. “The advisory board will advance the institute’s indispensable mission, which SNF is proud to support as a key part of our Global Health Initiative, and we look forward to seeing breakthroughs in the lab drive better outcomes in lives around the globe.”

The new advisory board will hold its first meeting on April 11th, 2024, following the second annual SNF Institute for Global Infectious Disease Research Symposium at Rockefeller.

Its members are: Rafi Ahmed of Emory University School of Medicine, Cori Bargmann of The Rockefeller University, Yasmin Belkaid of the Pasteur Institute, Anthony S. Fauci, the former director of the National Institute of Allergy and Infectious Diseases, Peter Hotez of Baylor College of Medicine and Texas Children’s Hospital Center for Vaccine Development, Esper Kallas of of the Butantan Institute, Sharon Lewin of the University of Melbourne Doherty Institue, Carl Nathan of Weill Cornell Medicine, Rino Rappuoli of Fondazione Biotecnopolo di Siena and University of Siena, and Herbert “Skip” Virgin of Washington University School of Medicine and UT Southwestern Medical Center.

Today, in the Calculated Risk Real Estate Newsletter: Q4 Update: Delinquencies, Foreclosures and REO

A brief excerpt: I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened followi…

I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble). The two key reasons are mortgage lending has been solid, and most homeowners have substantial equity in their homes..

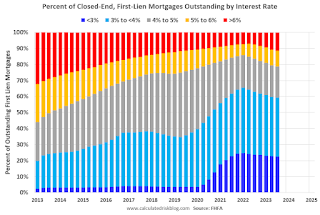

... And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023 (Q4 2023 data will be released in a two weeks).

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 22.6% of loans are under 3%, 59.4% are under 4%, and 78.7% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive restaurants. Yet they complain about living paycheck to paycheck and lacking the means to support their lifestyle.

Bougie broke is like “keeping up with the Joneses,” spending beyond one’s means to impress others.

Bougie Broke gives us a glimpse into the financial condition of a growing number of consumers. Since personal consumption represents about two-thirds of economic activity, it’s worth diving into the Bougie Broke fad to appreciate if a large subset of the population can continue to consume at current rates.

The Wealth Divide Disclaimer

Forecasting personal consumption is always tricky, but it has become even more challenging in the post-pandemic era. To appreciate why we share a joke told by Mike Green.

Bill Gates and I walk into the bar…

Bartender: “Wow… a couple of billionaires on average!”

Bill Gates, Jeff Bezos, Elon Musk, Mark Zuckerberg, and other billionaires make us all much richer, on average. Unfortunately, we can’t use the average to pay our bills.

According to Wikipedia, Bill Gates is one of 756 billionaires living in the United States. Many of these billionaires became much wealthier due to the pandemic as their investment fortunes proliferated.

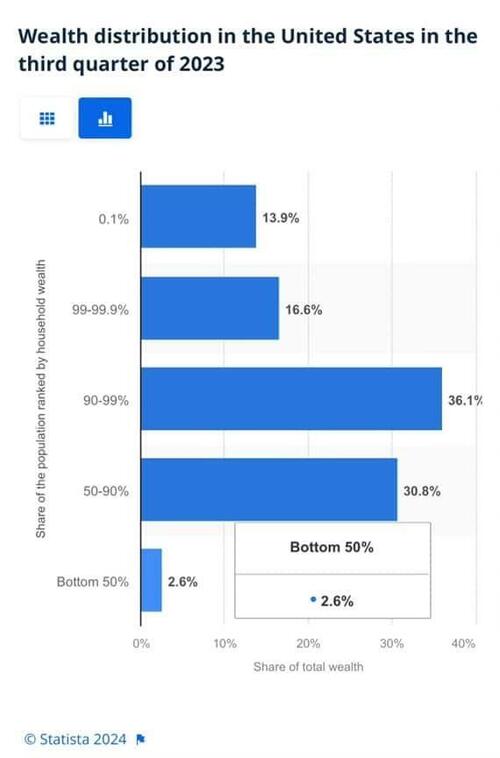

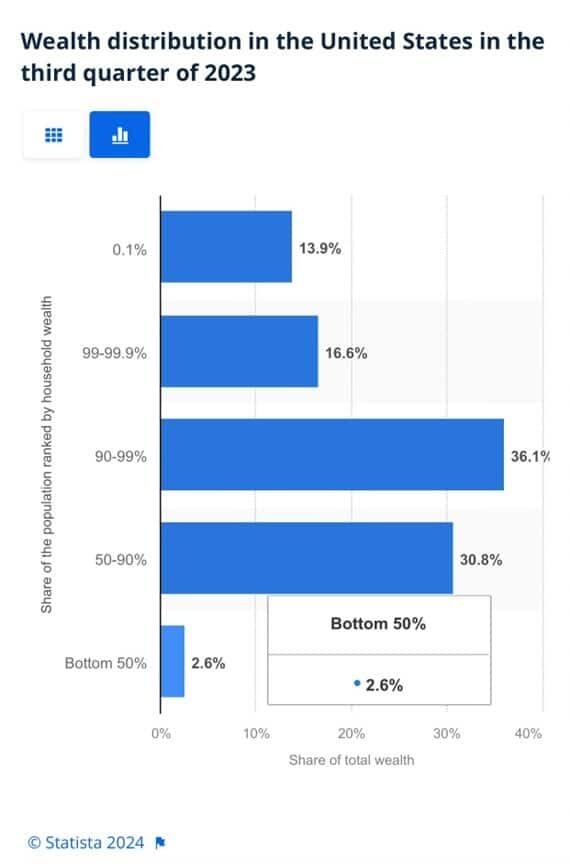

To appreciate the wealth divide, consider the graph below courtesy of Statista. 1% of the U.S. population holds 30% of the wealth. The wealthiest 10% of households have two-thirds of the wealth. The bottomhalf of the population accounts for less than 3% of the wealth.

The uber-wealthy grossly distorts consumption and savings data. And, with the sharp increase in their wealth over the past few years, the consumption and savings data are more distorted.

Furthermore, and critical to appreciate, the spending by the wealthy doesn’t fluctuate with the economy. Therefore, the spending of the lower wealth classes drives marginal changes in consumption. As such, the condition of the not-so-wealthy is most important for forecasting changes in consumption.

Revenge Spending

Deciphering personal data has also become more difficult because our spending habits have changed due to the pandemic.

A great example is revenge spending. Per the New York Times:

Ola Majekodunmi, the founder of All Things Money, a finance site for young adults, explained revenge spending as expenditures meant to make up for “lost time” after an event like the pandemic.

So, between the growing wealth divide and irregular spending habits, let’s quantify personal savings, debt usage, and real wages to appreciate better if Bougie Broke is a mass movement or a silly meme.

The Means To Consume

Savings, debt, and wages are the three primary sources that give consumers the ability to consume.

Savings

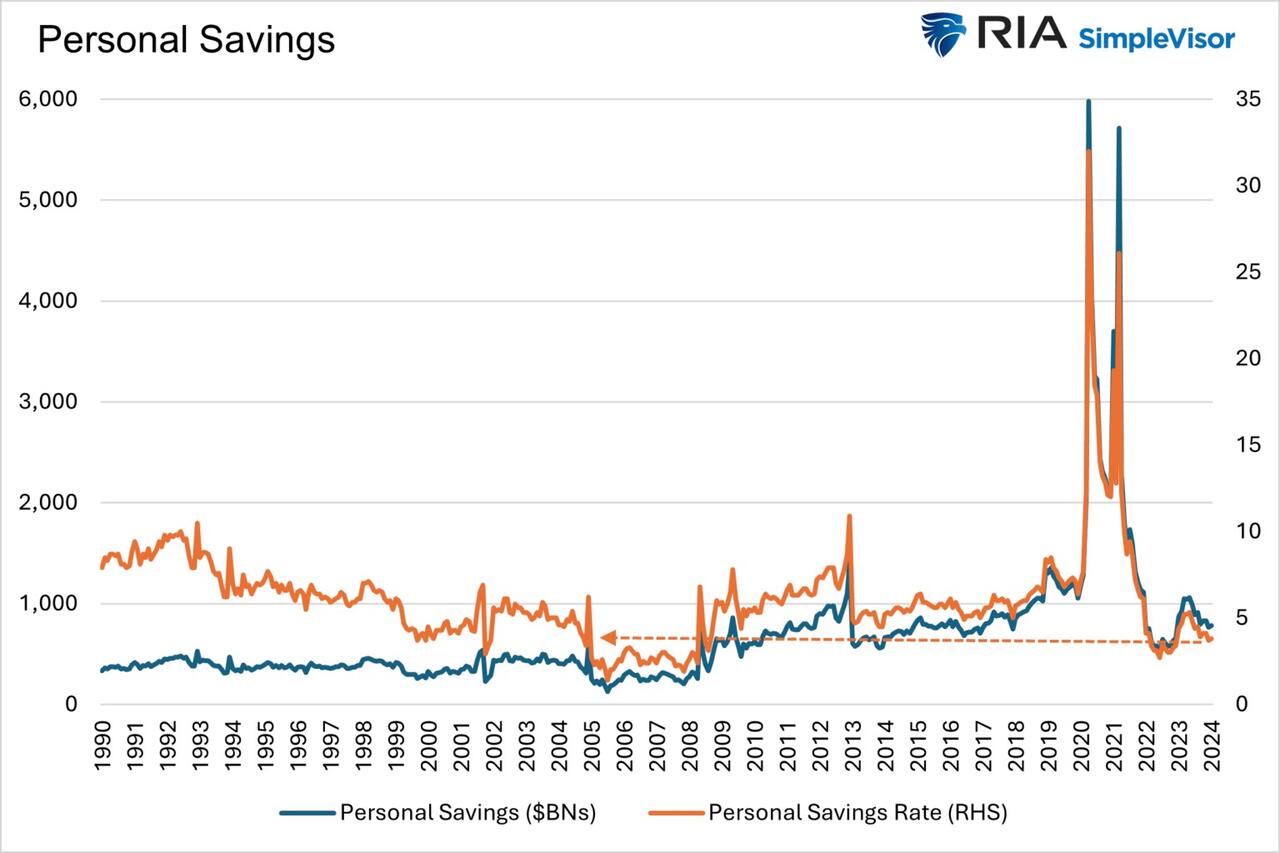

The graph below shows the rollercoaster on which personal savings have been since the pandemic. The savings rate is hovering at the lowest rate since those seen before the 2008 recession. The total amount of personal savings is back to 2017 levels. But, on an inflation-adjusted basis, it’s at 10-year lows. On average, most consumers are drawing down their savings or less. Given that wages are increasing and unemployment is historically low, they must be consuming more.

Now, strip out the savings of the uber-wealthy, and it’s probable that the amount of personal savings for much of the population is negligible. A survey by Payroll.org estimates that 78% of Americans live paycheck to paycheck.

More on Insufficient Savings

The Fed’s latest, albeit old, Report on the Economic Well-Being of U.S. Households from June 2023 claims that over a third of households do not have enough savings to cover an unexpected $400 expense. We venture to guess that number has grown since then. To wit, the number of households with essentially no savings rose 5% from their prior report a year earlier.

Relatively small, unexpected expenses, such as a car repair or a modest medical bill, can be a hardship for many families. When faced with a hypothetical expense of $400, 63 percent of all adults in 2022 said they would have covered it exclusively using cash, savings, or a credit card paid off at the next statement (referred to, altogether, as “cash or its equivalent”). The remainder said they would have paid by borrowing or selling something or said they would not have been able to cover the expense.

Debt

After periods where consumers drained their existing savings and/or devoted less of their paychecks to savings, they either slowed their consumption patterns or borrowed to keep them up. Currently, it seems like many are choosing the latter option. Consumer borrowing is accelerating at a quicker pace than it was before the pandemic.

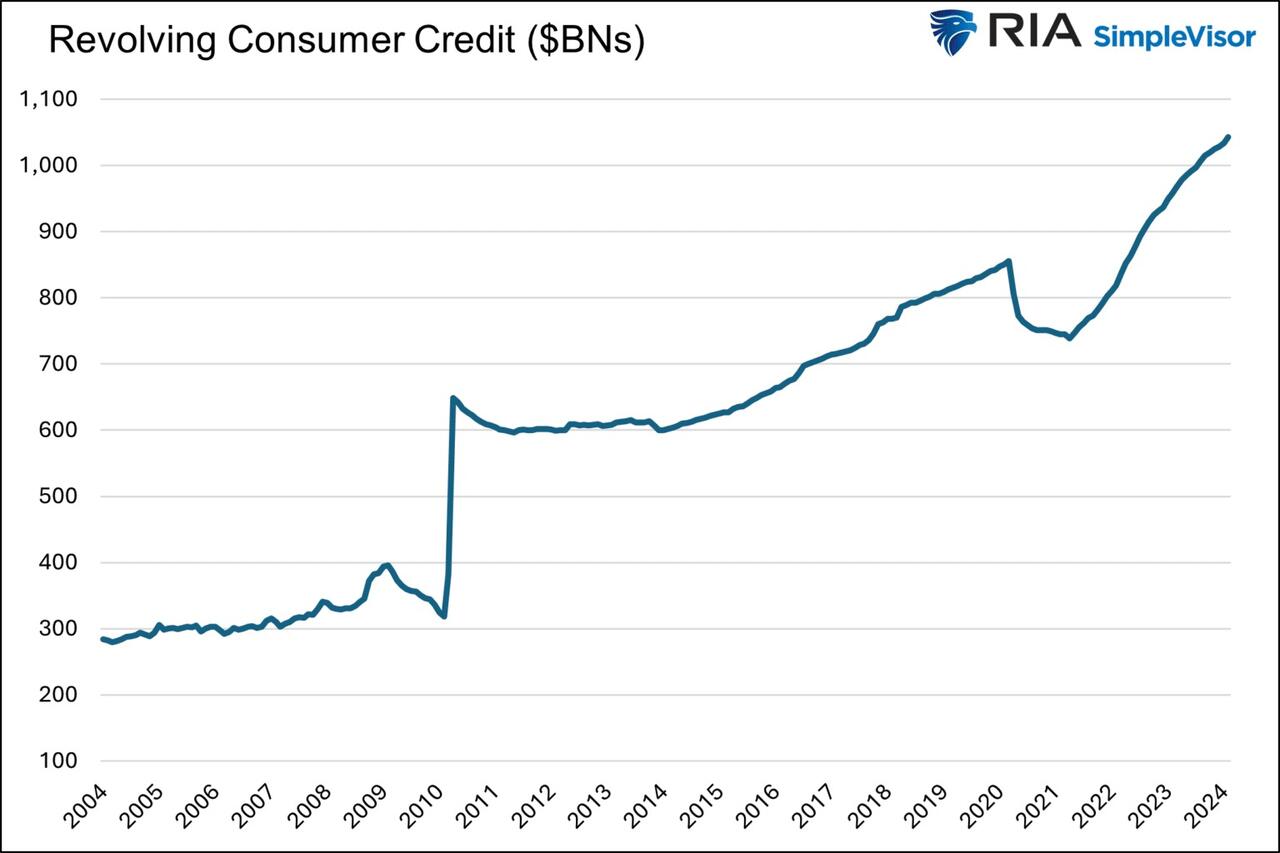

The first graph below shows outstanding credit card debt fell during the pandemic as the economy cratered. However, after multiple stimulus checks and broad-based economic recovery, consumer confidence rose, and with it, credit card balances surged.

The current trend is steeper than the pre-pandemic trend. Some may be a catch-up, but the current rate is unsustainable. Consequently, borrowing will likely slow down to its pre-pandemic trend or even below it as consumers deal with higher credit card balances and 20+% interest rates on the debt.

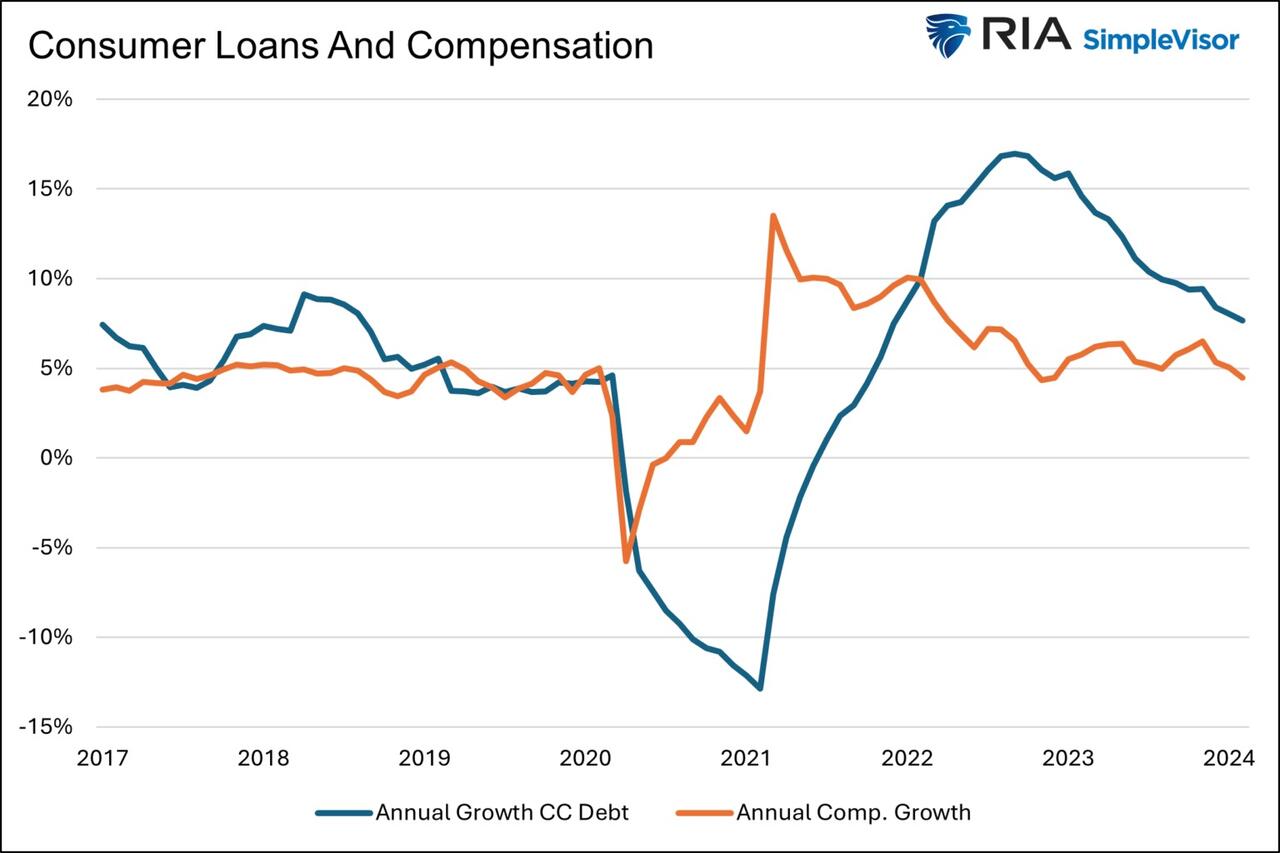

The second graph shows that since 2022, credit card balances have grown faster than our incomes. Like the first graph, the credit usage versus income trend is unsustainable, especially with current interest rates.

With many consumers maxing out their credit cards, is it any wonder buy-now-pay-later loans (BNPL) are increasing rapidly?

Insider Intelligence believes that 79 million Americans, or a quarter of those over 18 years old, use BNPL. Lending Tree claims that “nearly 1 in 3 consumers (31%) say they’re at least considering using a buy now, pay later (BNPL) loan this month.”More telling, according to their survey, only 52% of those asked are confident they can pay off their BNPL loan without missing a payment!

Wage Growth

Wages have been growing above trend since the pandemic. Since 2022, the average annual growth in compensation has been 6.28%. Higher incomes support more consumption, but higher prices reduce the amount of goods or services one can buy. Over the same period, real compensation has grown by less than half a percent annually. The average real compensation growth was 2.30% during the three years before the pandemic.

In other words, compensation is just keeping up with inflation instead of outpacing it and providing consumers with the ability to consume, save, or pay down debt.

It’s All About Employment

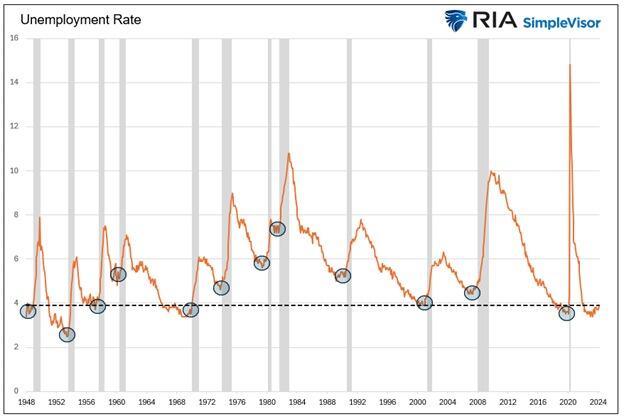

The unemployment rate is 3.9%, up slightly from recent lows but still among the lowest rates in the last seventy-five years.

The uptick in credit card usage, decline in savings, and the savings rate argue that consumers are slowly running out of room to keep consuming at their current pace.

However, the most significant means by which we consume is income. If the unemployment rate stays low, consumption may moderate. But, if the recent uptick in unemployment continues, a recession is extremely likely, as we have seen every time it turned higher.

It’s not just those losing jobs that consume less. Of greater impact is a loss of confidence by those employed when they see friends or neighbors being laid off.

Accordingly, the labor market is probably the most important leading indicator of consumption and of the ability of the Bougie Broke to continue to be Bougie instead of flat-out broke!

Summary

There are always consumers living above their means. This is often harmless until their means decline or disappear. The Bougie Broke meme and the ability social media gives consumers to flaunt their “wealth” is a new medium for an age-old message.

Diving into the data, it argues that consumption will likely slow in the coming months. Such would allow some consumers to save and whittle down their debt. That situation would be healthy and unlikely to cause a recession.

The potential for the unemployment rate to continue higher is of much greater concern. The combination of a higher unemployment rate and strapped consumers could accentuate a recession.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}

{kind=link}