Before investing, you must know that stocks can crash 70% anytime and 50% of individual stocks will likely deliver negative returns or below 2% while 75% will under perform the market. If you are not ready for that, better don’t invest in stocks! It is that simple!

Get The Full Warren Buffett Series in PDF

Get the entire 10-part series on Warren Buffett in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues

It is not about whether there is going to be a crash next, it is about what are you going to do when a crash comes and are you ready if stocks don't crash.

I have looked at research that shows how investors under perform the market by trying to time a stock market crash and about how difficult it is to time it. The key is that you see how does the possibility and magnitude of a crash fit your tolerance. Stocks can crash 70% anytime and stay down for decades - are you ready for that?

When it comes to individual stocks, the situation gets uglier. 30% of individual stocks will crash and actually deliver negative returns. Only 4% of stocks will do really great and compound! Can you handle the pain of investing in stocks? If you can't, I don't know, buy a house!

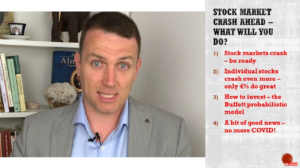

Stock Market Crash - Your Decision And Numbers

Transcript

Good day fellow investors. So there is so much talk about stock market crashes and individual stocks crashing, what will survive, what not. But we can talk as much as you want about that, there are three core fundamentals that are not discussed as much, but are even more important than whether stocks will crash or not. And these are the fundamentals that lead the average investor to strongly underperform the market.

Over the last 20 years, the average investor achieved a return of 2.5%, while the S&P 500 achieved a return of 6.1%. That's a huge difference. And this is something we have to address, analyse and prevent. And in this video, I want to share three core things that each of you have to know before investing in stocks, and it will give you a clear perspective so that you don't make the mistakes the average investor usually does that leads to those very, very bad returns.

Apart from doing the right things when stock markets crash, I want to discuss also investing in individual stocks, mistakes there, and how many stocks perform well, and how many performed bad from a statistical perspective. Then how to approach investing from a probabilistic way, the Warren Buffett way of probabilities of gains and losses. And we'll discuss in another video, the Kelly formula to discuss how much you should invest given a certain probabilistic outcome. And then I'll finish the video with some good news.

Let's start with the content and if you enjoy this content, please at any moment in time, click that like button or if you have any questions, please comment. So I said the average investor achieved a very poor return over the last 20 years compared to the S&P 500. Why did that happen? Well, we have seen ups and downs in the stock market we have had two bear markets of 50% big declines one bull market up 100% from 2002 to 2007. And then the huge bull market over the last 10 years.

Why did investors do so badly? Well, because they did the wrong thing at the wrong moment in time, because they didn't have a clear perspective on what investing is and how to be ready for whatever can happen when it comes to investing. And this is exactly what this video is all about. How to be ready for whatever can happen when it comes to investing.

The difference between 2.5 and 6.5% in returns is staggering. And that is why this is so important. What happens usually the average investor looks at the news, they predict the stock market crash they predict the world coming to an end, and then they usually sell at the wrong moment in time. Let's say they sold in 2008, and then said okay, we are out of the market and then when things get better 2015 then they get back into the market.

That is a 50% opportunity cost for the portfolio, which is why you can't really time the market and which is why you can't really predict the stock market crash and you're playing a very dangerous game.

If you start to listen to all those news about crashes about how stocks will crash, etc, etc. Even if you let's say, prevent one crash, and then come in later when the situation normalises even then you don't do much better than the market actually, in this case, with the seven year break, avoiding the 2009 great crash, you are still below market performance. And this is the likely process that happens when people start thinking about stock market pressures and doing the wrong thing at the wrong moment in time.

When stocks are down 10% okay, it's a quarter It will likely pass and that's correct statistically. When stocks are down 20%, okay, this is a bear market, perhaps we'll see a recession. There will be a recovery. I'm okay. Stocks dropped 30% Hmm, this is getting dangerous. What should I do? I just lost 30% of my portfolio, I can't risk my retirement. What should I do? Then stocks are down 40%. Oh, this is really bad news. This will get worse, the world as we know it will never be the same. I better sell and I protect what I have. Consequently, stocks let's say go down 41%. That's the market bottom and we have bull market ahead.

These are the behaviour on mistakes that many make and one should be very careful to avoid such mistakes. And to avoid such mistakes. You need to have a clear perspective on what can happen when it comes to investing. And what can happen when it comes to investing, what's the certainty? Is that each asset class you own will drop 70% or more, once or twice in your lifetime, that's a given. That's the likelihood of what will happen.

So once or twice in your lifetime stocks, bonds, cash, real estate or something like that will drop hugely. And that's something you have to see whether you are ready, whether you can survive that only those who survive and accumulate wealth in the meantime during those crashes, only those do very, very good. So this is not something whether there will be a crash or not. This is something you have to know crashes will come. The key is what am I going to do about it when it happens. Can I handle it? Can I tolerate it or not? You can't really predict a crash. You never know when it will happen. And you never know what's the opportunity cost. So the only option we have is to be ready.

Also when it comes to investing This is the Dow borrowed from Mohnish Pabrai. So there can easily be 22, 25, 17, 20, 15, 20 years where stocks returns are zero. And that is something also you have to keep in mind. We don't know what will the future look like. But we have to keep in mind all the possible scenarios, if you can tolerate stocks going nowhere over the next 10-15 years, especially at current high, relatively high valuations.

And if you can tolerate the 50% market crash, you should not be investing in stocks and you should look at other options. That is the simple truth. Even the stock of Berkshire Hathaway since 1968, went down more than 40% about five times that's a huge drop. Even for such a big business, such a great business as Berkshire is. Thus, we have to tolerate that we have to allow for that and give that flexibility within our investing, within our lifestyle, within our financial portfolios.

That's the key. If you can accept that flexibility, then you can be an investor into the stock market, because then you'll be happier when something bad happens. Because you can accumulate more at much lower prices, that will actually give you a great return in the long run. That's the key. If you can't tolerate that, then you have to adjust your strategy so that you can tolerate those things. And this was about the stock market.

Now it gets really ugly. Let's talk about individual stocks and the probabilities of outcomes when it comes to investing into individual stocks. And if you can't tolerate the stock market dropping 50% then you should really be careful about tolerating, investing into individual businesses. So this is the S&P 500 returns over the last 20 years from 1997 to 2017. Okay over 20 years, and you can see that 50% of stocks have a return that is lower than 50% over 20 years, that's below a 2% return. So 14% of the S&P 500 stocks delivered a return of -100 to -50% over 20 years. Another 15% went from -50 to zero. So 29-30% of stocks of the S&P 500 delivered negative returns over 20 years.

30% of stocks, 3 out of 10 negative returns, add another 20%. So 50% of stocks included in the S&P 500 give you terrible returns. On the average, so this is the average return, the average return is much better, because you have these companies, the 4% that become more than 10 baggers that justify all these bad, let's say, or especially is 50% of bad returns. And then these companies save for those companies, and especially the 4% here. So 40% of stocks delivered negative returns, 15% between negative 50% and 0%, 20% up to 50% over 20 years.

That's 50% of the S&P 500 delivered returns below 2% per year. These are staggering statistics and something to keep in mind. 24% of the winners that outperform the market will cover for all the losers. Thus, you have to be happy if you have less than 7.6 losers out of 10 investments. Do you comprehend this? I invest in 10 stocks 7.6 of those underperformed the market. Are losers, are investing mistakes, I should have stick to the S&P 500. And that's something we as individual investors, individual stocks have to accept and comprehend. That's as simple as that.

Further going deeper found a nice research report from Bessembinder and only 4% of the stocks since 1926 explain all the positive returns, the stock market delivered since then. So only these 4% of stocks is what gives you the return. So 4 out of 100 is what you have to focus on for the great long term returns. The other 96% of stocks since 1926, deliver the same similar return to Treasury bills. So $1 became $21, $1 invested in stocks became between 7000 and 36000 for amazing investing returns, but you have to understand the numbers game there that it will be ugly for many, many stocks out there.

So if you do 7 out of 10 mistakes, you will be an OK investor. If you have 6 out of 10 mistakes, you will be a really good investor and you will outperform the market. If you do 5 out of 10, you will be at Buffett level investing. And if you do 4 mistakes out of 10, then you will be a genius. Thus, as I have an investing channel and I talk often about stock and stock analysis. And whenever I do a stock and then it goes down, then the comment is usually. oh what an idiot. Oh, you should give back your PhD, oh this stupid PhD, you dumb ass, you whatever, you this you did. And there is plenty of comments.

But as investors, we have to understand the numbers behind investing in individual stocks. If I do, let's say 5 mistakes out of 10 and 5 are good investments. After 15-20 years, you put my golden statue in your bedroom, and another in your home when you enter your huge Villa, because that is how much money you will make. That is investing. 5 out of 10 of those 5, some become great businesses, and you just need four compounders 4% of the investments to be the great compounders over the long term, then you are a wonderful, you're a great investor. If you have more than 4% of the investments, doing really, really good.

And that's what we do on this channel. We try to improve the odds of investing. We don't try to be right on every stock. There will be mistakes. I can guarantee you I'll make a lot of mistakes. But we are trying to improve the long term odds by selecting those stocks that have the best probabilities the best outcomes regarding the risk and reward and then you say okay Sven you often discuss very strange emerging market stocks etc. We focus on the best stocks, then the risks should be much lower. Look at this, this is the top 10 S&P 500 components for 2005. Top company General Electric, Exxon, Microsoft, Citigroup, Banks, P&G, Walmart, etc.

Let's see how those fared. General Electric is down what 85% since 2005, Exxon down 20 something percent covered up by the dividends, but still a pretty negative return especially compared to the market. I don't even have to mention the banks and the return there. So it's not about the S&P 500, etc, or emerging markets. It's about finding quality businesses and understanding the risk and reward and trying to improve the odds in your favour.

How to Improve the odds in your favour. Well, 1989 shareholder meeting Warren Buffett said the following take the probability of loss, times the amount of possible loss from the probability of gain, times the amount of possible gain. That is what we're trying to do. It's imperfect, but that's what it's all about. And here I made the small table explaining Buffett's calculation. So we have in this case, I took my gut feeling for the S&P 500. Let's say that over the next 10 years, the S&P 500 will go to 6000 points, and I give a 70% chance for that happening because of inflationary pressures. Inflation, money printing, fed buying ETFs likely in the future, so S&P 500 goes to 6000.

There is a 20% chance that it goes just to 3000 points, okay? Then I multiply that times the 20% chance and I have a value. Goes down to 1500 points, let's give it a 10% chance. And this is the value of the sum of values is the value of the s&p 500 in the next 10 years should be 4950. If in case we have an economic depression for the next 5-10 years, it can be much lower. That would give a return of 6.2% per year which is in line with current valuations. If I look at the return, total return is at 83% up, 6.2% yearly return over 10 years.

And something also more important here. Okay, this is the outcome. Okay, Sven says 6.2% return, I should put all my money in the S&P 500 wait another very important thing before doing that. What if this materialises? What if the 10% scenario materialises and in 10 years the value of the S&P 500 is 1500 points not 6000, 1500. This is where it is about you and saying, Okay, can I tolerate this, okay, I will have to work a little bit more, save a little bit more, invest and take advantage of the situation. And then I can tolerate this.

But if you can tolerate this, then you have to be very careful or at least know exactly what you're doing in order to prevent finding yourself in a bad financial situations because each of these scenarios can happen. These probabilities that don't matter much when those scenarios happen. And then asset stocks can go down 50%, can crash all the time and can stay down for a long period of time. And that's something you have to see whether you can tolerate it or survive it.

So to sum up, stocks can fall 70% anytime. Keep that in mind when investing in the position so that if it happens, when it happens, you can survive it and go on with your life. If you can survive it. If you can't tolerate, then you have to rethink everything and make sure the fundamentals are strong. And then you can invest peacefully, whatever happens you are okay, that's the core of investing. That's the first core of investing.

The second core of investing. Well, if I invest in individual stocks, there will be many, many mistakes. That's something I have to tolerate. I have to weed the flowers and cut the weeds. It's a simple as that. And then in a probabilistic way, I have to improve the odds of succeeding, and you improve the odds of succeeding by being emotionally disattached from the mistakes, from the downturns.

That's why you have to make sure that it doesn't have an impact on your personal finances, on your decision making. And this is a game that few think about, oh, we are going to listen to the news. stock market crash. stocks up 3% .down 2%. No, it's about how you feel, what action you make when you lose your job, when you have to pay your mortgage, when you divorce your spouse, when your kid needs to go to college, when you need surprising money, and the stock market is crashing or when you are not reaching that target. That is when you have to make rational decisions. And this is what investing is all about.

Plus, knowing that 76% of the individual investments will not outperform the market and we look like mistakes. Can you invest into something where most of what you do will be looked like mistakes and then every loss that we have psychologically hurt 2.5 times more than a similar gain. Therefore those losses and that's why investing is so difficult, and so few succeed over the long term.

And this is investing. Keep that in mind. There is also a report that I wrote 15 page report if you want to read this statistics, look at the links at the sources, it's on my free stock market course, I have put the link to the course and to the PDF where you can enjoy it. Read it calmly and see how this investing probabilities fit you. Also if you like this video, please subscribe. Click that notification bell so that you get notified when a video comes out.

And now to end up with very, very good news. Let me share this. So I live in a small country in Europe bordering Italy called Slovenia. I live here in the mountains and we have very good news today. We have eliminated the Coronavirus. No more Coronavirus in Slovenia. So we went into lockdown in March. And we had about 50 cases, 50 new cases each day and then declining over April. And let's say since the end of April, we have had one or two cases or just one few days ago so no more cases of Coronavirus after two months lockdown. So it is possible to get rid of it. It is possible to solve the situation.

And with that positive note, I want to wish you the same that you get rid of Corona wherever you are, that we get rid of this nasty virus and that we can go on with life as we knew it. Tomorrow, we're visiting the capital going for a pizza and enjoying our life. I wish you the same. If you want to check my book, whatever I do, other stock investments, analysis, my research platform with my mistakes, where I'll make many and see how those mistakes fit you. Please also check my research platform. Thank you and I'll see you in the next video.

"I Can't Even Save": Americans Are Getting Absolutely Crushed Under Enormous Debt Load

While Joe Biden insists that Americans are doing great - suggesting in his State of the Union Address last week that "our economy is the envy of the world," Americans are being absolutely crushed by inflation (which the Biden admin blames on 'shrinkflation' and 'corporate greed'), andof course - crippling debt.

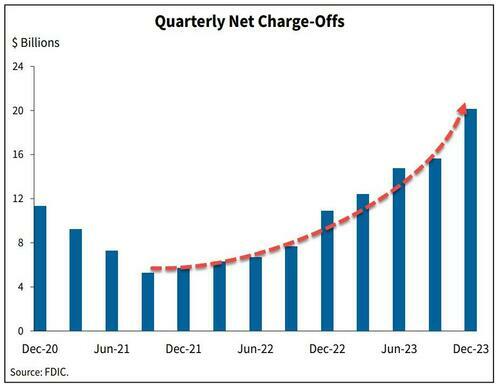

The signs are obvious. Last week we noted that banks' charge-offs are accelerating, and are now above pre-pandemic levels.

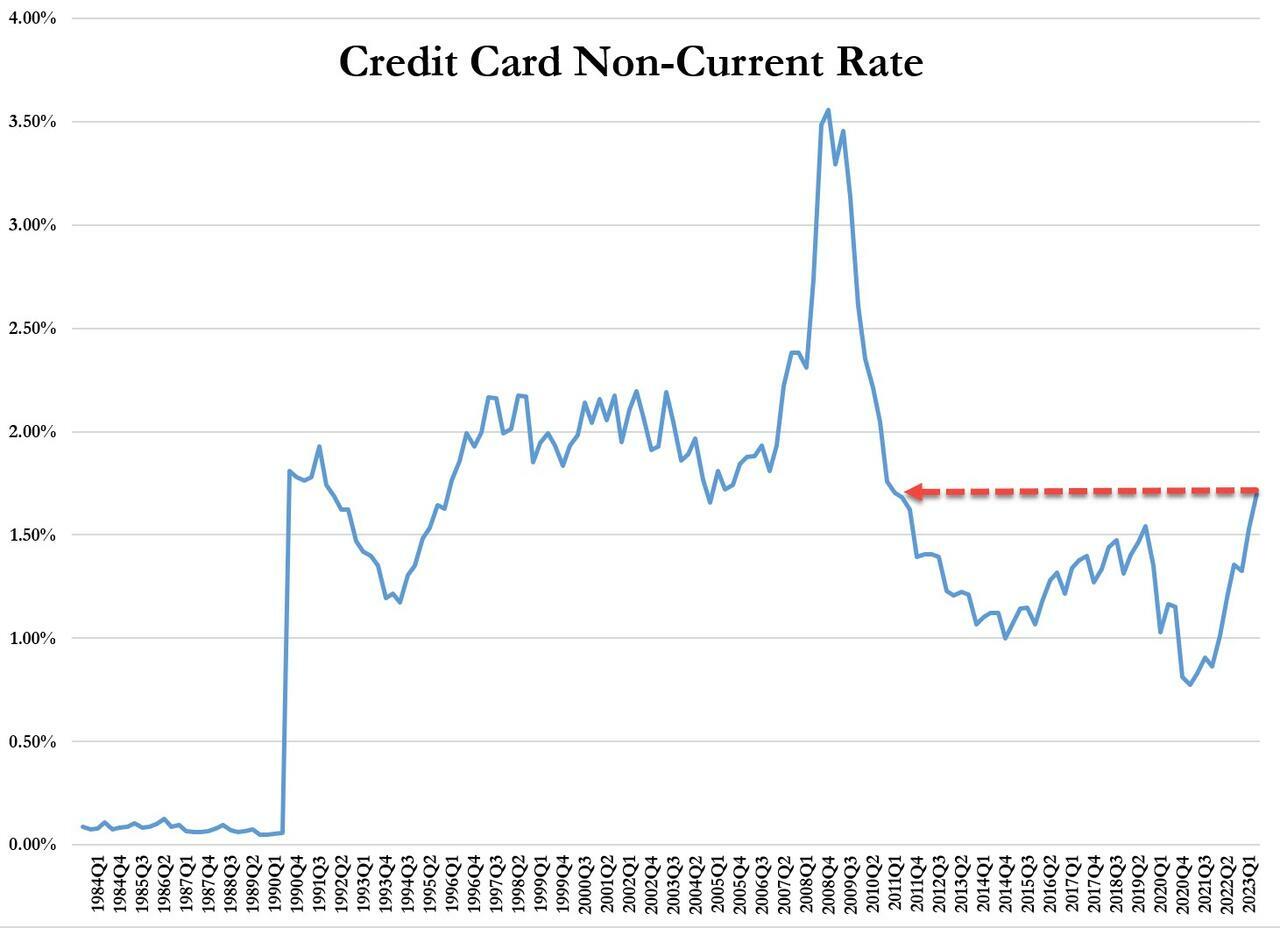

...and leading this increase are credit card loans - with delinquencies that haven't been this high since Q3 2011.

On top of that, while credit cards and nonfarm, nonresidential commercial real estate loans drove the quarterly increase in the noncurrent rate, residential mortgages drove the quarterly increase in the share of loans 30-89 days past due.

And while Biden and crew can spin all they want, an average of polls from RealClear Politics shows that just 40% of people approve of Biden's handling of the economy.

Crushed

On Friday, Bloomberg dug deeper into the effects of Biden's "envious" economy on Americans - specifically, how massive debt loads (credit cards and auto loans especially) are absolutely crushing people.

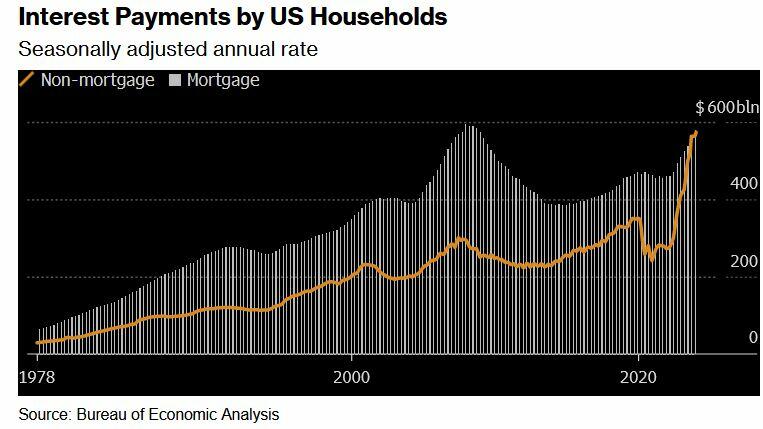

Two years after the Federal Reserve began hiking interest rates to tame prices, delinquency rates on credit cards and auto loans are the highest in more than a decade. For the first time on record, interest payments on those and other non-mortgage debts are as big a financial burden for US households as mortgage interest payments.

According to the report, this presents a difficult reality for millions of consumers who drive the US economy - "The era of high borrowing costs — however necessary to slow price increases — has a sting of its own that many families may feel for years to come, especially the ones that haven’t locked in cheap home loans."

The Fed, meanwhile, doesn't appear poised to cut rates until later this year.

According to a February paper from IMF and Harvard, the recent high cost of borrowing - something which isn't reflected in inflation figures, is at the heart of lackluster consumer sentiment despite inflation having moderated and a job market which has recovered (thanks to job gains almost entirely enjoyed by immigrants).

In short, the debt burden has made life under President Biden a constant struggle throughout America.

"I’m making the most money I've ever made, and I’m still living paycheck to paycheck," 40-year-old Denver resident Nikki Cimino told Bloomberg. Cimino is carrying a monthly mortgage of $1,650, and has $4,000 in credit card debt following a 2020 divorce.

"There's this wild disconnect between what people are experiencing and what economists are experiencing."

CBS: Do you attribute the inflation crisis to the pandemic or Biden?

WISCONSIN VOTER: "It's been YEARS now since the pandemic — I'm not buying that anymore. At first I did; I'm not buying that anymore because yogurt is STILL going up in price!" pic.twitter.com/apahb65scB

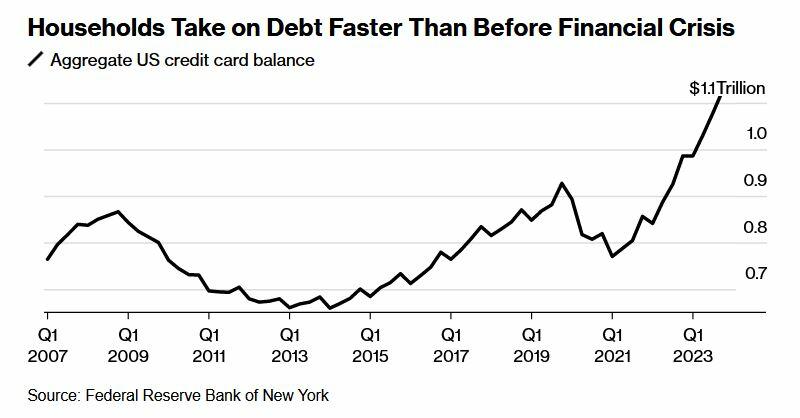

What's more, according to Wells Fargo, families have taken on debt at a comparatively fast rate - no doubt to sustain the same lifestyle as low rates and pandemic-era stimmies provided. In fact, it only took four years for households to set a record new debt level after paying down borrowings in 2021 when interest rates were near zero.

Meanwhile, that increased debt load is exacerbated by credit card interest rates that have climbed to a record 22%, according to the Fed.

[P]art of the reason some Americans were able to take on a substantial load of non-mortgage debt is because they’d locked in home loans at ultra-low rates, leaving room on their balance sheets for other types of borrowing. The effective rate of interest on US mortgage debt was just 3.8% at the end of last year.

Yet the loans and interest payments can be a significant strain that shapes families’ spending choices. -Bloomberg

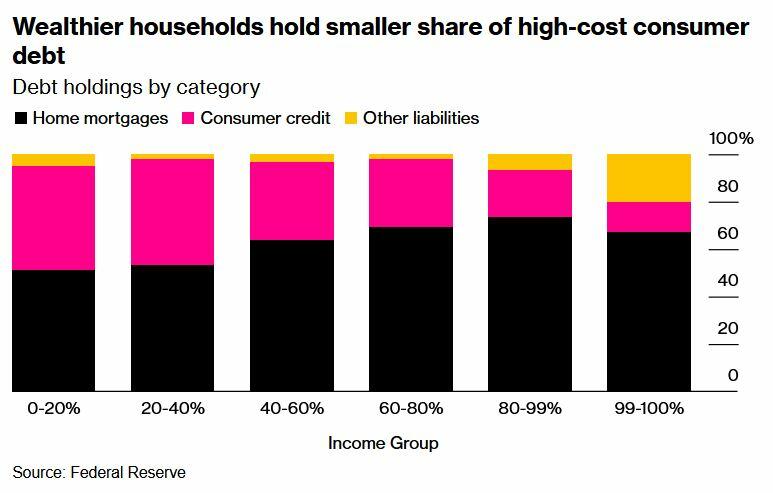

And of course, the highest-interest debt (credit cards) is hurting lower-income households the most, as tends to be the case.

The lowest earners also understandably had the biggest increase in credit card delinquencies.

"Many consumers are levered to the hilt — maxed out on debt and barely keeping their heads above water," Allan Schweitzer, a portfolio manager at credit-focused investment firm Beach Point Capital Management told Bloomberg. "They can dog paddle, if you will, but any uptick in unemployment or worsening of the economy could drive a pretty significant spike in defaults."

"We had more money when Trump was president," said Denise Nierzwicki, 69. She and her 72-year-old husband Paul have around $20,000 in debt spread across multiple cards - all of which have interest rates above 20%.

During the pandemic, Denise lost her job and a business deal for a bar they owned in their hometown of Lexington, Kentucky. While they applied for Social Security to ease the pain, Denise is now working 50 hours a week at a restaurant. Despite this, they're barely scraping enough money together to service their debt.

The couple blames Biden for what they see as a gloomy economy and plans to vote for the Republican candidate in November. Denise routinely voted for Democrats up until about 2010, when she grew dissatisfied with Barack Obama’s economic stances, she said. Now, she supports Donald Trump because he lowered taxes and because of his policies on immigration. -Bloomberg

Meanwhile there's student loans - which are not able to be discharged in bankruptcy.

"I can't even save, I don't have a savings account," said 29-year-old in Columbus, Ohio resident Brittany Walling - who has around $80,000 in federal student loans, $20,000 in private debt from her undergraduate and graduate degrees, and $6,000 in credit card debt she accumulated over a six-month stretch in 2022 while she was unemployed.

"I just know that a lot of people are struggling, and things need to change," she told the outlet.

The only silver lining of note, according to Bloomberg, is that broad wage gains resulting in large paychecks has made it easier for people to throw money at credit card bills.

Yet, according to Wells Fargo economist Shannon Grein, "As rates rose in 2023, we avoided a slowdown due to spending that was very much tied to easy access to credit ... Now, credit has become harder to come by and more expensive."

According to Grein, the change has posed "a significant headwind to consumption."

Then there's the election

"Maybe the Fed is done hiking, but as long as rates stay on hold, you still have a passive tightening effect flowing down to the consumer and being exerted on the economy," she continued. "Those household dynamics are going to be a factor in the election this year."

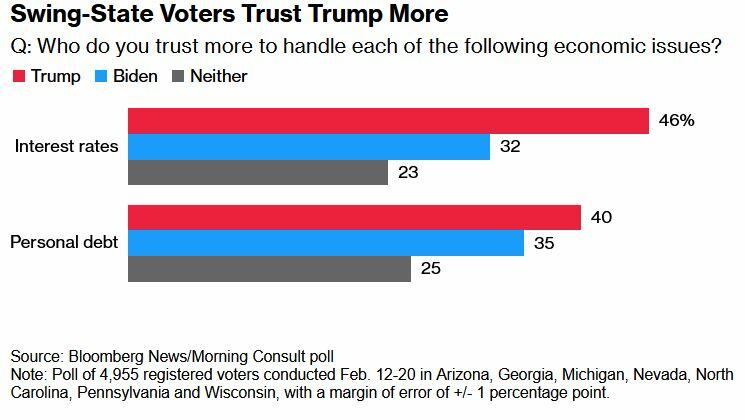

Meanwhile, swing-state voters in a February Bloomberg/Morning Consult poll said they trust Trump more than Biden on interest rates and personal debt.

Reverberations

These 'headwinds' have M3 Partners' Moshin Meghji concerned.

"Any tightening there immediately hits the top line of companies," he said, noting that for heavily indebted companies that took on debt during years of easy borrowing, "there's no easy fix."

Sylvester researchers, collaborators call for greater investment in bereavement care

MIAMI, FLORIDA (March 15, 2024) – The public health toll from bereavement is well-documented in the medical literature, with bereaved persons at greater…

MIAMI, FLORIDA (March 15, 2024) – The public health toll from bereavement is well-documented in the medical literature, with bereaved persons at greater risk for many adverse outcomes, including mental health challenges, decreased quality of life, health care neglect, cancer, heart disease, suicide, and death. Now, in a paper published in The Lancet Public Health, researchers sound a clarion call for greater investment, at both the community and institutional level, in establishing support for grief-related suffering.

Credit: Photo courtesy of Memorial Sloan Kettering Comprehensive Cancer Center

MIAMI, FLORIDA (March 15, 2024) – The public health toll from bereavement is well-documented in the medical literature, with bereaved persons at greater risk for many adverse outcomes, including mental health challenges, decreased quality of life, health care neglect, cancer, heart disease, suicide, and death. Now, in a paper published in The Lancet Public Health, researchers sound a clarion call for greater investment, at both the community and institutional level, in establishing support for grief-related suffering.

The authors emphasized that increased mortality worldwide caused by the COVID-19 pandemic, suicide, drug overdose, homicide, armed conflict, and terrorism have accelerated the urgency for national- and global-level frameworks to strengthen the provision of sustainable and accessible bereavement care. Unfortunately, current national and global investment in bereavement support services is woefully inadequate to address this growing public health crisis, said researchers with Sylvester Comprehensive Cancer Center at the University of Miami Miller School of Medicine and collaborating organizations.

They proposed a model for transitional care that involves firmly establishing bereavement support services within healthcare organizations to ensure continuity of family-centered care while bolstering community-based support through development of “compassionate communities” and a grief-informed workforce. The model highlights the responsibility of the health system to build bridges to the community that can help grievers feel held as they transition.

The Center for the Advancement of Bereavement Care at Sylvester is advocating for precisely this model of transitional care. Wendy G. Lichtenthal, PhD, FT, FAPOS, who is Founding Director of the new Center and associate professor of public health sciences at the Miller School, noted, “We need a paradigm shift in how healthcare professionals, institutions, and systems view bereavement care. Sylvester is leading the way by investing in the establishment of this Center, which is the first to focus on bringing the transitional bereavement care model to life.”

What further distinguishes the Center is its roots in bereavement science, advancing care approaches that are both grounded in research and community-engaged.

The authors focused on palliative care, which strives to provide a holistic approach to minimize suffering for seriously ill patients and their families, as one area where improvements are critically needed. They referenced groundbreaking reports of the Lancet Commissions on the value of global access to palliative care and pain relief that highlighted the “undeniable need for improved bereavement care delivery infrastructure.” One of those reports acknowledged that bereavement has been overlooked and called for reprioritizing social determinants of death, dying, and grief.

“Palliative care should culminate with bereavement care, both in theory and in practice,” explained Lichtenthal, who is the article’s corresponding author. “Yet, bereavement care often is under-resourced and beset with access inequities.”

Transitional bereavement care model

So, how do health systems and communities prioritize bereavement services to ensure that no bereaved individual goes without needed support? The transitional bereavement care model offers a roadmap.

“We must reposition bereavement care from an afterthought to a public health priority. Transitional bereavement care is necessary to bridge the gap in offerings between healthcare organizations and community-based bereavement services,” Lichtenthal said. “Our model calls for health systems to shore up the quality and availability of their offerings, but also recognizes that resources for bereavement care within a given healthcare institution are finite, emphasizing the need to help build communities’ capacity to support grievers.”

Key to the model, she added, is the bolstering of community-based support through development of “compassionate communities” and “upskilling” of professional services to assist those with more substantial bereavement-support needs.

The model contains these pillars:

Preventive bereavement care –healthcare teams engage in bereavement-conscious practices, and compassionate communities are mindful of the emotional and practical needs of dying patients’ families.

Ownership of bereavement care – institutions provide bereavement education for staff, risk screenings for families, outreach and counseling or grief support. Communities establish bereavement centers and “champions” to provide bereavement care at workplaces, schools, places of worship or care facilities.

Resource allocation for bereavement care – dedicated personnel offer universal outreach, and bereaved stakeholders provide input to identify community barriers and needed resources.

Upskilling of support providers – Bereavement education is integrated into training programs for health professionals, and institutions offer dedicated grief specialists. Communities have trained, accessible bereavement specialists who provide support and are educated in how to best support bereaved individuals, increasing their grief literacy.

Evidence-based care – bereavement care is evidence-based and features effective grief assessments, interventions, and training programs. Compassionate communities remain mindful of bereavement care needs.

Lichtenthal said the new Center will strive to materialize these pillars and aims to serve as a global model for other health organizations. She hopes the paper’s recommendations “will cultivate a bereavement-conscious and grief-informed workforce as well as grief-literate, compassionate communities and health systems that prioritize bereavement as a vital part of ethical healthcare.”

“This paper is calling for healthcare institutions to respond to their duty to care for the family beyond patients’ deaths. By investing in the creation of the Center for the Advancement of Bereavement Care, Sylvester is answering this call,” Lichtenthal said.

Follow @SylvesterCancer on X for the latest news on Sylvester’s research and care.

# # #

Article Title: Investing in bereavement care as a public health priority

DOI: 10.1016/S2468-2667(24)00030-6

Authors: The complete list of authors is included in the paper.

Funding: The authors received funding from the National Cancer Institute (P30 CA240139 Nimer) and P30 CA008748 Vickers).

Disclosures: The authors declared no competing interests.

# # #

Journal

The Lancet Public Health

DOI

10.1016/S2468-2667(24)00030-6

Article Title

Investing in bereavement care as a public health priority

Artificial intelligence (AI) cannot distinguish fact from fiction. It also isn’t creative or can create novel content but repeats, repackages, and reformulates what has already been said (but perhaps in new ways).

I am sure someone will disagree with the latter, perhaps pointing to the fact that AI can clearly generate, for example, new songs and lyrics. I agree with this, but it misses the point. AI produces a “new” song lyric only by drawing from the data of previous song lyrics and then uses that information (the inductively uncovered patterns in it) to generate what to us appears to be a new song (and may very well be one). However, there is no artistry in it, no creativity. It’s only a structural rehashing of what exists.

Of course, we can debate to what extent humans can think truly novel thoughts and whether human learning may be based solely or primarily on mimicry. However, even if we would—for the sake of argument—agree that all we know and do is mere reproduction, humans have limited capacity to remember exactly and will make errors. We also fill in gaps with what subjectively (not objectively) makes sense to us (Rorschach test, anyone?). Even in this very limited scenario, which I disagree with, humans generate novelty beyond what AI is able to do.

Both the inability to distinguish fact from fiction and the inductive tether to existent data patterns are problems that can be alleviated programmatically—but are open for manipulation.

Manipulation and Propaganda

When Google launched its Gemini AI in February, it immediately became clear that the AI had a woke agenda. Among other things, the AI pushed woke diversity ideals into every conceivable response and, among other things, refused to show images of white people (including when asked to produce images of the Founding Fathers).

Tech guru and Silicon Valley investor Marc Andreessen summarized it on X (formerly Twitter): “I know it’s hard to believe, but Big Tech AI generates the output it does because it is precisely executing the specific ideological, radical, biased agenda of its creators. The apparently bizarre output is 100% intended. It is working as designed.”

There is indeed a design to these AIs beyond the basic categorization and generation engines. The responses are not perfectly inductive or generative. In part, this is necessary in order to make the AI useful: filters and rules are applied to make sure that the responses that the AI generates are appropriate, fit with user expectations, and are accurate and respectful. Given the legal situation, creators of AI must also make sure that the AI does not, for example, violate intellectual property laws or engage in hate speech. AI is also designed (directed) so that it does not go haywire or offend its users (remember Tay?).

However, because such filters are applied and the “behavior” of the AI is already directed, it is easy to take it a little further. After all, when is a response too offensive versus offensive but within the limits of allowable discourse? It is a fine and difficult line that must be specified programmatically.

It also opens the possibility for steering the generated responses beyond mere quality assurance. With filters already in place, it is easy to make the AI make statements of a specific type or that nudges the user in a certain direction (in terms of selected facts, interpretations, and worldviews). It can also be used to give the AI an agenda, as Andreessen suggests, such as making it relentlessly woke.

Thus, AI can be used as an effective propaganda tool, which both the corporations creating them and the governments and agencies regulating them have recognized.

Misinformation and Error

States have long refused to admit that they benefit from and use propaganda to steer and control their subjects. This is in part because they want to maintain a veneer of legitimacy as democratic governments that govern based on (rather than shape) people’s opinions. Propaganda has a bad ring to it; it’s a means of control.

However, the state’s enemies—both domestic and foreign—are said to understand the power of propaganda and do not hesitate to use it to cause chaos in our otherwise untainted democratic society. The government must save us from such manipulation, they claim. Of course, rarely does it stop at mere defense. We saw this clearly during the covid pandemic, in which the government together with social media companies in effect outlawed expressing opinions that were not the official line (see Murthy v. Missouri).

AI is just as easy to manipulate for propaganda purposes as social media algorithms but with the added bonus that it isn’t only people’s opinions and that users tend to trust that what the AI reports is true. As we saw in the previous article on the AI revolution, this is not a valid assumption, but it is nevertheless a widely held view.

If the AI then can be instructed to not comment on certain things that the creators (or regulators) do not want people to see or learn, then it is effectively “memory holed.” This type of “unwanted” information will not spread as people will not be exposed to it—such as showing only diverse representations of the Founding Fathers (as Google’s Gemini) or presenting, for example, only Keynesian macroeconomic truths to make it appear like there is no other perspective. People don’t know what they don’t know.

Of course, nothing is to say that what is presented to the user is true. In fact, the AI itself cannot distinguish fact from truth but only generates responses according to direction and only based on whatever the AI has been fed. This leaves plenty of scope for the misrepresentation of the truth and can make the world believe outright lies. AI, therefore, can easily be used to impose control, whether it is upon a state, the subjects under its rule, or even a foreign power.

The Real Threat of AI

What, then, is the real threat of AI? As we saw in the first article, large language models will not (cannot) evolve into artificial general intelligence as there is nothing about inductive sifting through large troves of (humanly) created information that will give rise to consciousness. To be frank, we haven’t even figured out what consciousness is, so to think that we will create it (or that it will somehow emerge from algorithms discovering statistical language correlations in existing texts) is quite hyperbolic. Artificial general intelligence is still hypothetical.

As we saw in the second article, there is also no economic threat from AI. It will not make humans economically superfluous and cause mass unemployment. AI is productive capital, which therefore has value to the extent that it serves consumers by contributing to the satisfaction of their wants. Misused AI is as valuable as a misused factory—it will tend to its scrap value. However, this doesn’t mean that AI will have no impact on the economy. It will, and already has, but it is not as big in the short-term as some fear, and it is likely bigger in the long-term than we expect.

No, the real threat is AI’s impact on information. This is in part because induction is an inappropriate source of knowledge—truth and fact are not a matter of frequency or statistical probabilities. The evidence and theories of Nicolaus Copernicus and Galileo Galilei would get weeded out as improbable (false) by an AI trained on all the (best and brightest) writings on geocentrism at the time. There is no progress and no learning of new truths if we trust only historical theories and presentations of fact.

However, this problem can probably be overcome by clever programming (meaning implementing rules—and fact-based limitations—to the induction problem), at least to some extent. The greater problem is the corruption of what AI presents: the misinformation, disinformation, and malinformation that its creators and administrators, as well as governments and pressure groups, direct it to create as a means of controlling or steering public opinion or knowledge.

This is the real danger that the now-famous open letter, signed by Elon Musk, Steve Wozniak, and others, pointed to:

“Should we let machines flood our information channels with propaganda and untruth? Should we automate away all the jobs, including the fulfilling ones? Should we develop nonhuman minds that might eventually outnumber, outsmart, obsolete and replace us? Should we risk loss of control of our civilization?”

Other than the economically illiterate reference to “automat[ing] away all the jobs,” the warning is well-taken. AI will not Terminator-like start to hate us and attempt to exterminate mankind. It will not make us all into biological batteries, as in The Matrix. However, it will—especially when corrupted—misinform and mislead us, create chaos, and potentially make our lives “solitary, poor, nasty, brutish and short.”

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}